Futures Slide On Renewed China Slowdown, Rate Hike Fears

Futures Slide On Renewed China Slowdown, Rate Hike Fears

US equity futures and world shares drifted lower following poor Chinese macro data which saw the country’s GDP slide to a weaker than expected 4.9%, and as surging energy prices and…

Share this:

US equity futures and world shares drifted lower following poor Chinese macro data which saw the country's GDP slide to a weaker than expected 4.9%, and as surging energy prices and inflation reinforced bets that central banks will be forced to react to rising inflation and hike rates faster than expected. Calls by China’s President Xi Jinping on Friday to make progress on a long-awaited property tax to help reduce wealth gaps also soured the mood. With WTI crude rising to a seven-year high, and Brent back over $85, investors remain concerned that living costs will be driven higher. The economic recovery also remains uneven with China’s gross domestic product slowing more than expected in the third quarter, increasing aversion to riskier assets. The dollar rose against all of its Group-of-10 peers as concerns about an acceleration in inflation damped risk appetite, while bircoin traded above $61K and just shy of an all time high ahead of the launch of the Proshares Bitcoin ETF on Tuesday.

An MSCI gauge of global stocks was down 0.1% by 0808 GMT as losses in Asia and a weak open in Europe erased part of the gains seen last week on a strong start to the earnings season. U.S. stock futures were also lower with S&P 500 e-minis last down 0.2%, while Dow and Nasdaq e-minis were both down 0.3%.

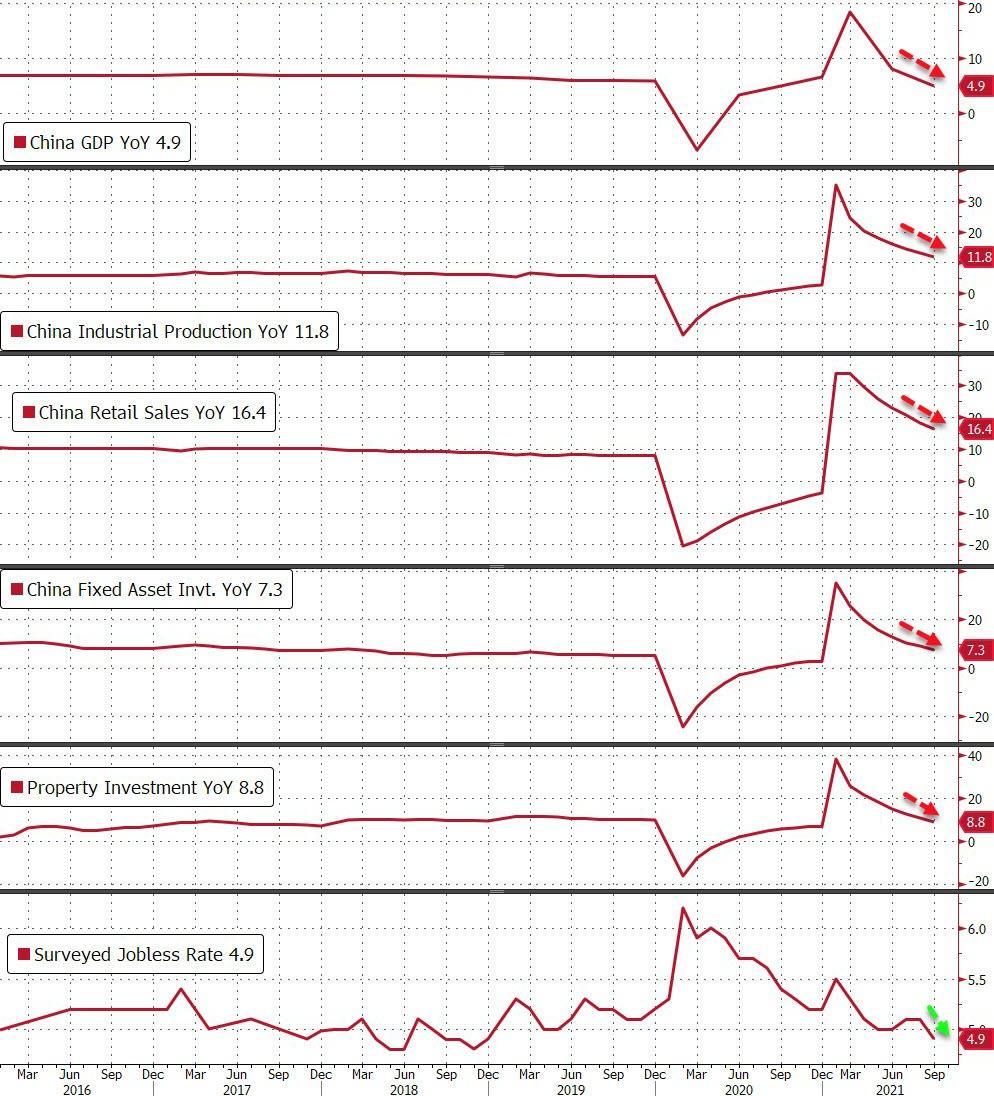

China’s gross domestic product grew 4.9% in the July-September quarter from a year earlier, its weakest pace since the third quarter of 2020. The world’s second-largest economy is grappling with power shortages, supply bottlenecks, sporadic COVID-19 outbreaks and debt problems in its property sector. Additionally, industrial output and fixed investment also missed expectations, while retail sales beat modestly (more here). Not even the latest attempt by China to ease Evergrande contagion fears was enough to offset worries about China's economy: on Sunday, PBOC Governor Yi Gang said authorities can contain risks posed to the Chinese economy and financial system from the struggles of China Evergrande Group. Because of course he will say that.

Oil prices extended a recent rally amid a global energy shortage with U.S. crude touching a seven-year high while Brent was set to surpass its 2018 highs just above $86, as Russia kept a tight grip on Europe’s energy market, opting against sending more natural gas to the continent even after President Vladimir Putin said he was prepared to boost supplies.

“The lingering energy crisis, while benefiting miners and other oil & gas related stocks, is otherwise weighing on the overall sentiment,” said ActivTrades’ Pierre Veyret. Investors will stay focused on macro news this week with major Chinese and U.S. releases as well as new monetary policy talks from Jerome Powell, he said.

Investors continue to grapple with worries that energy shortages and supply-chain disruptions will drive up living costs in most economies. At the same time, the recovery remains patchy and central bankers are inching closer to paring back stimulus. U.S. consumer sentiment fell unexpectedly in early October, but retail sales advanced.

“We are starting to see some cracks in the transitory narrative that we’ve been hearing for quite some time,” Meera Pandit, global market strategist at J.P. Morgan Asset Management, said on Bloomberg Radio. “Rates will continue to ground higher from where we are. But I don’t think from a Fed perspective, when you think about the short end of the curve, that they are going to move much earlier than 2023. They are going to be a little bit more patient than the market expects right now.”

And then there were rates: the global bond selloff gathered pace, with U.K. yields surging after Bank of England Governor Andrew Bailey warned on the need to respond to price pressures. Rate-hike bets have also picked up in the U.S., Australia and New Zealand, where inflation accelerated to the fastest pace in 10 years. Ten-year Treasury yields extended a climb , rising as high as 1.62%.

Mohammed El-Erian, the chief economic adviser at Allianz SE and a Bloomberg columnist, said investors should prepare for increased market volatility if the Federal Reserve pulls back on stimulus measures set in motion by the Covid-19 pandemic. On the other side of the argument, Goldman's flow trading desk said odds of a November meltup are rising as a result of a relentless appetite for stocks and an upcoming surge in stock buybacks.

In any case, Virgin Galactic Holdings Inc. shares fell 3% in U.S. premarket, extending losses from Friday that came after the firm pushed back the start of commercial flights further into next year after rescheduling a test flight. Here are some of the other notable U.S. pre-movers today:

- Baidu (BIDU US) shares erased earlier losses and climbed as much as 4.3% in Hong Kong, as China debates rules to make hundreds of millions of articles on Tencent’s WeChat messaging app available via search engines like Baidu’s.

- Crypto-related stocks in action as Bitcoin leaps as much as 5.3% and is just shy of a fresh six- month high. Riot Blockchain (RIOT US), Marathon Digital (MARA US) and Coinbase (COIN US) are all up

- Tesla (TSLA US) shares rise 0.2% in premarket trading Monday, poised for 50% rally from a March 8 low, ahead of its third-quarter results on Wednesday

- Dynavax (DVAX US) shares rise as much as 10% in U.S. pretrading hours after the biopharmaceutical company announced that Valneva reported the trial of inactivated, adjuvanted Covid-19 vaccine candidate VLA2001 met its co-primary endpoints

- Disney (DIS US) drops in premarket trading after Barclays downgrades to equal-weight as the company faces a “tough” task to get to its long-term streaming subscription guidance

- NetApp (NTAP US) slips 2.2% in premarket trading after Goldman Sachs analyst Rod Hall cut the recommendation on NetApp Inc. to sell from neutral

European stocks traded on the back foot from the open, with the benchmark Stoxx 600 Index down 0.4%, led by losses in retail stocks. The Euro Stoxx 50 dropped as much as 0.9%, FTSE 100 outperforms slightly. Mining stocks were among Europe's only gainers thanks to the ongoing metals rally: the Stoxx Europe 600 basic resources sub-index climbs for a third day for the first time since early September as the record rally of base metals is extended. The gauge rose 0.6%, outperforming main benchmark which trades 0.4% lower. Notable movers: Glencore +1.2%; BHP +1%; Norsk Hydro +2.5%; ArcelorMittal +0.9% Rio Tinto +0.3%. Offsetting these gains, European luxury stocks slipped after a Chinese Communist Party journal published a speech of President Xi Jinping that includes advancing legislation on property taxes. Here are some of the biggest European movers today:

- Playtech shares rise as much as 59% in London after the British gambling software developer agreed to be bought by Australia’s Aristocrat for $3.7 billion.

- Valneva SE shares rise as much as 42% as its experimental Covid-19 vaccine elicited better immunity than AstraZeneca Plc’s shot in a clinical trial that will pave the way for regulatory submissions.

- Shares of hydraulics manufacturer Concentric rise as much as 14%, the most since April 2020, after Danske Bank upgraded the stock to buy from hold, calling the company a strong performer in a difficult market.

- THG shares jump as much 12%, most since May 11, after founder and CEO Matthew Moulding confirmed his intention to cancel his special share rights. The removal of the special share points to the e-commerce company’s “willingness to engage on shareholder concerns,” according to Jefferies.

- Rational AG shares rise as much as 6.1%, the most since Aug. 5, after the German kitchen machinery maker is upgraded to buy from hold at Berenberg, which considers the shares “inexpensive” despite stretched multiples.

- Atrium European Real Estate share rises as much as 7.6% to the highest since March 2020 after controlling shareholder Gazit Globe raises the offer price to EU3.63 per Atrium share from EU3.35.

Earlier in the session, Asian equities fell, putting them on track to snap a three-day rally, as China’s economic growth slowed and prospects of higher bond yields weighed on some tech shares. The MSCI Asia Pacific Index fell as much as 0.4%, with tech and consumer staples shares setting the pace for declines. TSMC and Sony Group were among the biggest drags. Official data showed that China’s economy weakened in the third quarter amid tighter restrictions on the property market and China Evergrande Group’s debt crisis. For Asia stock traders, the concerns about China are adding to persistent inflation worries and energy shortages, which are sending bond yields higher. While inflation worries are “alive and well,” Asian markets will be predominantly focused on China data today, Jeffrey Halley, senior market analyst at Oanda Asia Pacific, wrote in a note. The weak data print “will lift expectations of an imminent PBOC RRR rate cut,” he added. China’s benchmark underperformed as the country explored property- and consumption tax-related changes and international funds sold shares of Kweichow Moutai Co., the country’s largest stock by market value. Tencent, Meituan and Alibaba pared losses prompted by the Chinese government saying it will introduce more regulations on the tech sector. China is considering asking media companies from Tencent Holdings Ltd. to ByteDance Ltd. to let rivals access and display their content in search results, according to people familiar with the matter. India’s Sensex index bucked the regional trend and is on track to rise for the seventh day, the longest such streak since January, helped by easy money.

Japanese equities declined, paring last week’s rally, weighed down by losses in electronics makers. The Topix dipped 0.2%, following a 3.2% gain last week. The Nikkei 225 fell 0.2%, with M3 Inc. and KDDI the biggest drags. Almost 30% of respondents to a Kyodo weekend poll said they plan to vote for the ruling Liberal Democratic Party in the proportional representation section of Japan’s Oct. 31 election.

U.K. rates steal the limelight amid a violent selloff that saw 2y gilt yields rise as much as 17bps to trade close to 0.75%. Weekend comments from BOE’s Bailey triggered a snap lower in short-sterling futures and bear-flattening across the gilt curve. MPC-dated OIS rates price in ~20bps of hiking by the November meeting. Bunds and Treasuries follow gitls lower, peripheral spreads widen to core with Italy underperforming.

Australian stocks closed higher as miners and banks advanced. The S&P/ASX 200 index rose 0.3% to close at 7,381.10, led by miners and banks. Nickel Mines surged after a subsidiary signed a limonite ore supply agreement with PT Huayue Nickel Cobalt. Domino’s was among the worst performers, closing at its lowest since Aug. 17. In New Zealand, the S&P/NZX 50 index fell 0.1% to 12,998.51.

In FX, the Bloomberg Dollar Spot Index advanced as the dollar traded higher versus all of its Group-of-10 peers Traders pulled forward rate- hike bets after BoE governor Bailey said the central bank “will have to act” on inflation. U.K. money markets now see 36 basis points of BoE rate increases in December and are pricing 15 basis points of tightening next month. Traders are also now betting the BoE’s key rate will rise to 1% by August, from 0.1% currently. The euro struggled to recover after falling below the $1.16 handle in the Asian session; money markets are betting the ECB will hike the deposit rate to -0.4% in September as expectations for global central-bank policy tightening gather pace. Resilience in the spot market and a divergence with rate differentials in the past sessions has resulted in a flatter volatility skew for the euro.

Commodity-linked currencies such as the Australian dollar and the Norwegian krone underperformed after Chinese data including third-quarter growth and September factory output trailed economists’ estimates. The kiwi rose to a one-month high versus the dollar, before giving up gains, and New Zealand’s bond yields rose across the curve after 3Q annual inflation rate surged, beating estimates. The yen steadied around a three-year low as U.S. yields extended their rise in Asian trading; the Japanese currency still held up best against the dollar among G-10 currencies, after performing worst last week.

In rates, treasuries were under pressure led by belly of the curve as rate-hike premium continues to increase in global interest rates. Yields, though off session highs, remain cheaper by nearly 5bp in 5-year sector; 2s5s30s fly topped at -12.5bp, cheapest since 2018; 10-year is up 2.8bp around 1.60% vs 3.4bp increase for U.K. 10-year. Belly-led losses flattened U.S. 5s30s by as much as 5.4bp to tightest since April 2020 at around 86.1bp; U.K. 5s30s curve is flatter by ~8bp after its 5-year yield rose as much as 14bp.

Gilts led the move, with U.K. 2-year yield climbing as much as 16.8bp to highest since May 2019 as money markets priced in more policy tightening after Governor Andrew Bailey said the Bank of England “will have to act” on inflation. With latest moves, U.S. swaps market prices in two Fed hikes by the end of 2022.

In commodities, WTI rose 1%, trading just off session highs near $83.20; Brent holds above $85. Spot gold drifts lower near $1,762/oz. Most base metals are in the green with LME lead and tin outperforming.

Looking at today's calendar, we have industrial production, US September industrial production, capacity utilisation, October NAHB housing market index. Fed speakers include Quarles, Kashkari.

Market Snapshot

- S&P 500 futures down 0.2% to 4,451.75

- STOXX Europe 600 down -1.6% to 467.76

- MXAP down 0.2% to 198.11

- MXAPJ little changed at 650.02

- Nikkei down 0.1% to 29,025.46

- Topix down 0.2% to 2,019.23

- Hang Seng Index up 0.3% to 25,409.75

- Shanghai Composite down 0.1% to 3,568.14

- Sensex up 1.0% to 61,918.22

- Australia S&P/ASX 200 up 0.3% to 7,381.07

- Kospi down 0.3% to 3,006.68

- Brent Futures up 0.9% to $85.65/bbl

- Gold spot down 0.3% to $1,762.70

- U.S. Dollar Index up 0.17% to 94.10

- German 10Y yield rose 3.5 bps to -0.132%

- Euro down 0.1% to $1.1586

- Brent Futures up 0.9% to $85.65/bbl

Top Overnight News from Bloomberg

- Germany’s prospective ruling coalition is targeting about 500 billion euros ($580 billion) in spending over the coming decade to address climate change and will seek loopholes in constitutional debt rules to raise the financing

- The ECB is exploring raising its limit on purchases of debt issued by international bodies such as the European Union from the current cap of 10%, the Financial Times reported, citing four ECB governing council members

- The ECB should keep some of the flexibility embedded in its pandemic bond-buying program for post-crisis stimulus measures, Governing Council member Ignazio Visco said

- People’s Bank of China Governor Yi Gang said authorities can contain risks posed to the Chinese economy and financial system from the struggles of China Evergrande Group

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded cautiously after disappointing Chinese GDP and Industrial Production data, while inflationary concerns lingered after the recent firmer than expected US Retail Sales data, a continued rally in oil prices and with New Zealand CPI at a decade high. Nonetheless, the ASX 200 (+0.1%) bucked the trend on reopening optimism with curbs in New South Wales to be further eased after having fully vaccinated 80% of the adult population and with the Victoria state capital of Melbourne set to lift its stay-at-home orders this week. Furthermore, the gains in the index were led by outperformance in the top-weighted financials sector, as well as strength in most mining names aside from gold miners after the precious metal’s retreat from the USD 1800/oz level. Nikkei 225 (-0.3%) was subdued after a pause in the recent advances for USD/JPY and with criticism of Japan after PM Kishida sent an offering to the controversial war shrine which sparked anger from both China and South Korea. Hang Seng (-0.5%) and Shanghai Comp. (-0.4%) were subdued after Chinese Q3 GDP data missed expectations with Y/Y growth at 4.9% vs exp. 5.2% and Industrial Production for September fell short of estimates at 3.1% vs exp. 4.5%, while the beat on Retail Sales at 4.4% vs exp. 3.3% provided little consolation. There was plenty of focus on China’s property sector with PBoC Governor Yi noting authorities can contain risks posed to the Chinese economy and financial system from the struggles of Evergrande, and with its unit is said to make onshore debt payments due tomorrow. However, attention remains on October 23rd which is the end of the grace period for its first payment miss that would officially place the Co. in default and it was also reported on Friday that China Properties Group defaulted on notes worth USD 226mln. Finally, 10yr JGBs were lower amid spillover selling from T-notes which were pressured after the recent stronger than expected Retail Sales data and higher oil prices boosted the inflation outlook, with demand for JGBs is also hampered amid the absence of BoJ purchases in the market today.

Top Asian News

- Tesla Shares Roaring Back, Set for 50% Gain From March Lows

- Kishida’s Offering to Japan War Shrine Angers Neighbors

- Baidu Jumps as China Said to Weigh More Access to WeChat Content

- AirAsia X Proposes Paying Creditors 0.5% of $8 Billion Owed

European equities (Eurostoxx 50 -0.7%; Stoxx 600 -0.4%) have kicked the week off on the backfoot as market participants digest disappointing Chinese GDP metrics, a continued rally in energy prices and subsequent inflationary concerns which has seen markets price in more aggressive tightening paths for major global central banks. Overnight, Chinese Q3 GDP data missed expectations with Y/Y growth at 4.9% vs exp. 5.2% and Industrial Production for September fell short of estimates at 3.1% vs exp. 4.5%, while the beat on Retail Sales at 4.4% vs exp. 3.3% provided little consolation. Stateside, index futures have conformed to the downbeat tone with the ES softer to the tune of -0.3%, whilst the RTY narrowly lags with losses of 0.4%. In a note this morning, JP Morgan has flagged that investor sentiment remains that “the upcoming reporting season will be challenging, given the combination of the activity slowdown, significant supply distortions impacting volumes, and the energy price acceleration that is seen to be hurting profit margins and consumer disposable incomes”. That said, the Bank is of the view that investors are likely braced for such disappointments. In Europe, sectors are mostly lower with Retail names lagging post-Chinese GDP as Kering (accounts for 28.7% of the Stoxx 600 Retail sector) sits at the foot of the CAC with losses of 3.2%; other laggards include LVMH (-2.7%) and Hermes (-2.3%). To the upside, Banking names are firmer and benefitting from the more favourable yield environment, whilst Basic Resources and Oil & Gas names are being supported by price action in their respective underlying commodities. In terms of individual movers, THG (+7.6%) sits at the top of the Stoxx 600 after confirming that it intends to move its listing to the 'premium segment' of the LSE in 2022; as part of this, CEO & Executive Chairman Moulding will surrender his 'founders share' next year. Finally, Umicore (-4.5%) sits at the foot of the Stoxx 600 after cutting its FY21 adj. EBIT outlook.

Top European News

- Traders Ramp Up U.K. Rate-Hike Bets on Bailey Inflation Warning

- Nordea Equity Research Hires Pareto Analyst for Tech Team

- ECB’s Visco Says Flexible Policy Should Remain Part of Toolkit

- Scholz Coalition Eyes $580 Billion in Spending on German Reboot

In FX, the broader Dollar and index has waned off its 94.174 pre-European cash open high but remains underpinned above 94.000 by risk aversion and firmer yields, with the US 10yr cash now hovering around 1.60%. Stateside, US President Biden confirmed that the reconciliation package will likely be less than USD 3.5trln, although this was widely expected in recent weeks. Aside from that, the Greenback awaits further catalysts but until then will likely derive its impetus from the yield and risk environment. From a tech standpoint, a breach of 94.000 to the downside could see a test of the 21 DMA (93.865) – which has proven to provide some support over the last two trading sessions, with Friday and Thursday’s lows at 93.847 and 93.759 respectively. The upside meanwhile sees the YTD high at 94.563, printed on the 12th of Oct.

- CNH - The offshore is relatively flat on the day in a contained 6.4265-4387 range following a set of overall downbeat Chinese activity metrics. GDP growth momentum waned more than expected whilst industrial production was lower than expected, largely impacted by the electricity crisis and local COVID outbreaks during Q3. Retail sales meanwhile rebounded more than expected – albeit due to reopening effects, with inflation a concern heading forward. The Chinese National Bureau of Stats later hit the wires suggesting that major economic data are seen in reasonable ranges from Q1-Q3. The PBoC governor meanwhile downplayed the current risks of spillover from default fears.

- AUD, NZD, CAD - The overall cautiousness across the market has pressured high-betas. The AUD fails to glean support from the firmer base metal prices and the surge in coal prices overnight, with overall downbeat Chinese data proving to be headwinds for the antipodean. The NZD is more cushioned as inflation topped forecasts and reinforced the RBNZ’s hawkishness, whilst AUD/NZD remains capped at around 1.0500. AUD/USD fell back under its 100 DMA (0.7409) from a 0.7437 peak, whilst NZD/USD hovers around 0.7050 (vs high 0.7100), with the 100 DMA at 0.7021. The Loonie narrowly lags as a pullback in oil adds further headwinds. USD/CAD aims for a firmer footing above 1.2400 from a 1.2348 base.

- EUR, GBP- The single currency and Sterling are relatively flat on the day and within tight ranges of 1.1572-1.1605 and 1.3720-65 respectively. The latter was unreactive to weekend commentary from the BoE governor, sounding cautious over rising inflation but ultimately labelling it temporary, although suggesting that monetary policy may have to step in if risks materialise. From a Brexit standpoint, nothing major to report in the runup to negotiations on the Northern Ireland protocol. Across the Channel, FT sources suggested that four ECB GC members would support upping the PSPP share of APP from the current 10% - with the plan to be discussed across two meetings next month and requiring a majority from the 25 members. All-in-all, the EUR was unswayed ahead of a plethora of ECB speakers during the week and as the clock ticks down to flash PMIs on Friday.

- JPY, CHF - The traditional safe-havens have fallen victim to the firmer Buck, with USD/JPY extending on gains north of 114.00 as it inches closer towards 114.50 – which also matches some highs dating back to 2017. The Swiss Franc is among the laggards after USD/CHF rebounded from its 50 DMA (0.9214) as it heads back towards 0.9300, with the weekly Sight deposits also seeing W/W increases.

In commodities, WTI and Brent front-month futures have drifted from best levels as the cautious risk tone weighs on prices, but nonetheless, the complex remains overall firmer with the former within a USD 82.55-83.06 range and the latter in a 84.93-85.31 intraday parameter. Fresh catalysts remain quiet for the complex, while there were some comments over the weekend from Iraq's Oil Ministry which noted that prices above USD 80/bbl are a positive indicator. Elsewhere on the supply-side, Iran is to resume nuclear negotiations on October 21, an Iranian lawmaker said Sunday, although it is unclear how far talks will go as the US and Iran affirm their stances. It is also worth noting that a fire was reported at Kuwait's Mina al-Ahmadi (346k BPD) refinery, but refining and export operations are unaffected. UK nat gas futures meanwhile are relatively flat in a tight range, although prices remain elevated on either side of GBP 2.5/Thm. Elsewhere, spot gold and silver trade sideways amid a lack of catalysts, although the firmer found some support at 1,760/oz - matching its 21 DMA. Over to base metals, LME copper remains supported around USD 10,250/t. Overnight, Shanghai zinc and Zhengzhou coal hit a record high and limit up respectively, with some citing supply constraints.

US Event Calendar

- 9:15am: Sept. Industrial Production MoM, est. 0.2%, prior 0.4%;

- Capacity Utilization, est. 76.5%, prior 76.4%

- Manufacturing (SIC) Production, est. 0.1%, prior 0.2%

- 10am: Oct. NAHB Housing Market Index, est. 75, prior 76

- 2:15pm: Fed’s Kashkari Discusses Improving Financial Inclusion

- 4pm: Aug. Total Net TIC Flows, prior $126b

DB's Jim Reid concludes the overnight wrap

Straight to China this morning where the monthly data dump has just landed. GDP expanded in Q3 by +4.9% on a year-on-year basis, which is a touch below the +5.0% consensus expectation and a shift down from the +7.9% expansion back in Q2. That’s come as their economy has faced multiple headwinds, ranging from the property market crisis with the issues surrounding Evergrande group and other developers, an energy crisis that’s forced factories to curb output, alongside a number of Covid-19 outbreaks that have led to tight restrictions as they seek to eliminate the virus from circulating domestically. Industrial production for September also came in beneath expectations with a +3.1% year-on-year expansion (vs. +3.8% expected), though retail sales outperformed in the same month with +4.4% year-on-year growth (vs. +3.5% expected), and the jobless rate also fell back to 4.9% (vs. 5.1% expected).

That data release alongside continued concerns over inflation has sent Asian markets lower this morning, with the Shanghai Composite (-0.35%), Hang Seng (-0.36%), CSI (-1.40%) KOSPI (-0.01%), and the Nikkei (-0.16%) all trading lower. Speaking of inflation, there’ve also been fresh upward moves in commodity prices overnight, with WTI up a further +1.58% this morning to follow up a run of 8 successive weekly moves higher, which takes it to another post-2014 high, whilst Brent crude is also up +1.14%. Furthermore, data overnight has shown that New Zealand’s CPI surged to a 10-year high of +4.9% in Q3, which was some way above the +4.2% expected. Looking forward, equity futures in the US are pointing lower, with those on the S&P 500 down -0.11%.

Another interesting weekend story comes again from the Bank of England, which seems to be using the weekends of late to prime the markets for imminent rate hikes. Governor Bailey yesterday said inflation “will last longer and it will of course get into the annual numbers for longer as a consequence… That raises for central banks the fear and concern of embedded expectations. That’s why we, at the Bank of England have signalled, and this is another signal, that we will have to act. But of course that action comes in our monetary policy meetings.” It’s difficult to get much more explicit than this and it’ll be interesting to see if we get even more priced into the very immediate front end this morning. For now, sterling has seen little change, weakening -0.13% against the US dollar, but markets were already pricing in an initial +15bps move up to 0.25% by the end of the year before the speech.

Now the big China data is out of the way we’ll have to wait until Friday for the main releases of the week, namely the global flash PMIs. Outside of that, there’s plenty of Fedspeak as they approach the blackout period at the weekend ahead of their November 3rd meeting where they’re expected to announce the much discussed taper.

On top of this, earnings season will ramp up further, with 78 companies in the S&P 500 reporting. Early season positive earnings across the board have definitely helped sentiment over the last few days. 18 out of 19 that reported last week beat expectations across varying sectors. As examples, freight firm JB Hunt climbed around 9% after beating, Alcoa over 15% and Goldman Sachs nearly 4%. So much for inflation squeezing margins. My view remains that we’re still seeing “growthflation” and not “stagflation”, particularly in the US even if there are obvious risks to growth. For now, there is still a buffer before we should get really worried. On the back of the decent earnings, the S&P 500 had its best week since July last week and is now only less than -1.5% off its record high from early September.

Given that earnings season has made a difference the 78 companies in the S&P 500 and 58 from the Stoxx 600 will be important for sentiment this week. In terms of the highlights, tomorrow we’ll get reports from Johnson & Johnson, Procter & Gamble, Netflix, Philip Morris International and BNY Mellon. Then on Wednesday, releases include Tesla, ASML, Verizon Communications, Abbott Laboratories, NextEra Energy and IBM. On Thursday, there’s Intel, Danaher, AT&T, Union Pacific and Barclays. Lastly on Friday, well hear from Honeywell and American Express.

It’ll also be worth watching out for the latest inflation data, with CPI releases for September from the UK, Canada (both Wednesday) and Japan (Friday). The UK is by far and away the most interesting given the recent pressures and likely imminent rate hike. This month is likely to be a bit of calm before the future storm though as expectations are broadly similar to last month. Given the recent rise in energy prices, this won’t last though.

In terms of the main US data, today’s industrial production (consensus +0.2% vs. +0.4% previously) will be a window into supply-chain disruptions, particularly in the auto sector. Outside of that, you’ll see in the day-by-day week ahead guide at the end that there’s a bit of US housing data to be unveiled (NAHB today, housing starts and permits tomorrow). Housing was actually the most interesting part of the US CPI last week as rental inflation came in very strong, with primary rents and owners’ equivalent rent growing at the fastest pace since 2001 and 2006, respectively. The strength was regionalised (mainly in the South) but this push from recent housing market buoyancy into CPI, via rents, has been a big theme of ours in recent months. The models that my colleague Francis Yared has suggest that we could be at comfortably above 4% inflation on this measure by next year given the lags in the model. Rents and owners’ equivalent rent makes up around a third of US CPI. So will a third of US inflation be above 4% consistently next year before we even get to all the other things?

Moving to Germany, formal coalition negotiations are set to commence soon between the SPD, the Greens and the FDP. They reached an agreement on Friday with some preliminary policies that will form the basis for talks, including the maintenance of the constitutional debt brake, a pledge not to raise taxes or impose new ones, along with an increase in the minimum wage to €12 per hour. There are also a number of environmental measures, including a faster shift away from coal that will be complete by 2030. The Green Party voted in favour of entering the formal negotiations over the weekend, with the SPD agreeing on Friday, and the FDP is expected to approve the talks today.

Reviewing last week now and strong earnings, along with the rather precipitous decline in long-end real yields drove the S&P 500 +1.82% higher over the week (+0.75% Friday), while the STOXX 600 gained +2.65% (+0.74% Friday). No major sector ended the week lower in Europe, while only communications (-0.52%) were down in the U.S. Interest rate sensitive sectors were among the outperformers in each jurisdiction.

The 2s10s yield curve twist flattened -11.7bps over the week, as investors brought forward the timing of an increase to the Fed’s policy rate, driving the 2-year +7.8bps higher (+3.5 bps Friday), whilst the 10-year declined -4.2 bps (+6.0bps Friday). This is consistent with our US econ team bringing forward their call for the Fed lift-off to late 2022. Markets are actually pricing in a 50/50 likelihood of a hike by June. Particularly notable was the decline in long-end real yields, with 10yr real yields finishing the week -9.5bps lower, and at one point closed beneath the -1.00% mark for the first time in a month. Hence breakevens were up +5.4bps to 2.565%, leaving them right around their year-to-date highs last reached in May.

The curve flattening trend was a global one last week, with 2-year gilts yields up +3.7bps whilst the 10-year fell -5.2bps. The bund curve flattened mildly as well, with 2-year bunds increasing +2.6 bps and the 10-year -1.6 bps. 10-year breakevens increased +7.9 bps in the UK, and +7.3 bps in Germany, which marks the highest reading since 2008 in the UK and the highest in Germany since 2013.

The increases in inflation compensation were matched by commodities. WTI and Brent futures increased +3.69% and +3.00%, respectively last week, whilst metals also posted strong gains, with copper up +10.62% and aluminium +6.93% higher on the week.

On the data front, September retail sales were much stronger than expectations, with the prior month’s components being revised higher across the board as well. The University of Michigan consumer survey saw sentiment and 5yr inflation expectations dip, while year ahead inflation expectations inched up to 4.8%. Friday’s strong data brought a brief reprieve from the curve flattening exhibited the rest of the week.

International

Shakira’s net worth

After 12 albums, a tax evasion case, and now a towering bronze idol sculpted in her image, how much is Shakira worth more than 4 decades into her care…

Share this:

Shakira’s considerable net worth is no surprise, given her massive popularity in Latin America, the U.S., and elsewhere.

In fact, the belly-dancing contralto queen is the second-wealthiest Latin-America-born pop singer of all time after Gloria Estefan. (Interestingly, Estefan actually helped a young Shakira translate her breakout album “Laundry Service” into English, hugely propelling her stateside success.)

Since releasing her first record at age 13, Shakira has spent decades recording albums in both Spanish and English and performing all over the world. Over the course of her 40+ year career, she helped thrust Latin pop music into the American mainstream, paving the way for the subsequent success of massively popular modern acts like Karol G and Bad Bunny.

In December 2023, a 21-foot-tall beachside bronze statue of the “Hips Don’t Lie” singer was unveiled in her Colombian hometown of Barranquilla, making her a permanent fixture in the city’s skyline and cementing her legacy as one of Latin America’s most influential entertainers.

After 12 albums, a plethora of film and television appearances, a highly publicized tax evasion case, and now a towering bronze idol sculpted in her image, how much is Shakira worth? What does her income look like? And how does she spend her money?

How much is Shakira worth?

In late 2023, Spanish sports and lifestyle publication Marca reported Shakira’s net worth at $400 million, citing Forbes as the figure’s source (although Forbes’ profile page for Shakira does not list a net worth — and didn’t when that article was published).

Most other sources list the singer’s wealth at an estimated $300 million, and almost all of these point to Celebrity Net Worth — a popular but dubious celebrity wealth estimation site — as the source for the figure.

A $300 million net worth would make Shakira the third-richest Latina pop star after Gloria Estefan ($500 million) and Jennifer Lopez ($400 million), and the second-richest Latin-America-born pop singer after Estefan (JLo is Puerto Rican but was born in New York).

Shakira’s income: How much does she make annually?

Entertainers like Shakira don’t have predictable paychecks like ordinary salaried professionals. Instead, annual take-home earnings vary quite a bit depending on each year’s album sales, royalties, film and television appearances, streaming revenue, and other sources of income. As one might expect, Shakira’s earnings have fluctuated quite a bit over the years.

From June 2018 to June 2019, for instance, Shakira was the 10th highest-earning female musician, grossing $35 million, according to Forbes. This wasn’t her first time gracing the top 10, though — back in 2012, she also landed the #10 spot, bringing in $20 million, according to Billboard.

In 2023, Billboard listed Shakira as the 16th-highest-grossing Latin artist of all time.

How much does Shakira make from her concerts and tours?

A large part of Shakira’s wealth comes from her world tours, during which she sometimes sells out massive stadiums and arenas full of passionate fans eager to see her dance and sing live.

According to a 2020 report by Pollstar, she sold over 2.7 million tickets across 190 shows that grossed over $189 million between 2000 and 2020. This landed her the 19th spot on a list of female musicians ranked by touring revenue during that period. In 2023, Billboard reported a more modest touring revenue figure of $108.1 million across 120 shows.

In 2003, Shakira reportedly generated over $4 million from a single show on Valentine’s Day at Foro Sol in Mexico City. 15 years later, in 2018, Shakira grossed around $76.5 million from her El Dorado World Tour, according to Touring Data.

Related: RuPaul's net worth: Everything to know about the cultural icon and force behind 'Drag Race'

How much has Shakira made from her album sales?

According to a 2023 profile in Variety, Shakira has sold over 100 million records throughout her career. “Laundry Service,” the pop icon’s fifth studio album, was her most successful, selling over 13 million copies worldwide, according to TheRichest.

Exactly how much money Shakira has taken home from her album sales is unclear, but in 2008, it was widely reported that she signed a 10-year contract with LiveNation to the tune of between $70 and $100 million to release her subsequent albums and manage her tours.

How much did Shakira make from her Super Bowl and World Cup performances?

Shakira co-wrote one of her biggest hits, “Waka Waka (This Time for Africa),” after FIFA selected her to create the official anthem for the 2010 World Cup in South Africa. She performed the song, along with several of her existing fan-favorite tracks, during the event’s opening ceremonies. TheThings reported in 2023 that the song generated $1.4 million in revenue, citing Popnable for the figure.

A decade later, 2020’s Superbowl halftime show featured Shakira and Jennifer Lopez as co-headliners with guest performances by Bad Bunny and J Balvin. The 14-minute performance was widely praised as a high-energy celebration of Latin music and dance, but as is typical for Super Bowl shows, neither Shakira nor JLo was compensated beyond expenses and production costs.

The exposure value that comes with performing in the Super Bowl Halftime Show, though, is significant. It is typically the most-watched television event in the U.S. each year, and in 2020, a 30-second Super Bowl ad spot cost between $5 and $6 million.

How much did Shakira make as a coach on “The Voice?”

Shakira served as a team coach on the popular singing competition program “The Voice” during the show’s fourth and sixth seasons. On the show, celebrity musicians coach up-and-coming amateurs in a team-based competition that eventually results in a single winner. In 2012, The Hollywood Reporter wrote that Shakira’s salary as a coach on “The Voice” was $12 million.

Related: John Cena's net worth: The wrestler-turned-actor's investments, businesses, and more

How does Shakira spend her money?

Shakira doesn’t just make a lot of money — she spends it, too. Like many wealthy entertainers, she’s purchased her share of luxuries, but Barranquilla’s barefoot belly dancer is also a prolific philanthropist, having donated tens of millions to charitable causes throughout her career.

Private island

Back in 2006, she teamed up with Roger Waters of Pink Floyd fame and Spanish singer Alejandro Sanz to purchase Bonds Cay, a 550-acre island in the Bahamas, which was listed for $16 million at the time.

Along with her two partners in the purchase, Shakira planned to develop the island to feature housing, hotels, and an artists’ retreat designed to host a revolving cast of artists-in-residence. This plan didn’t come to fruition, though, and as of this article’s last update, the island was once again for sale on Vladi Private Islands.

Real estate and vehicles

Like most wealthy celebs, Shakira’s portfolio of high-end playthings also features an array of luxury properties and vehicles, including a home in Barcelona, a villa in Cyprus, a Miami mansion, and a rotating cast of Mercedes-Benz vehicles.

Philanthropy and charity

Shakira doesn’t just spend her massive wealth on herself; the “Queen of Latin Music” is also a dedicated philanthropist and regularly donates portions of her earnings to the Fundación Pies Descalzos, or “Barefoot Foundation,” a charity she founded in 1997 to “improve the education and social development of children in Colombia, which has suffered decades of conflict.” The foundation focuses on providing meals for children and building and improving educational infrastructure in Shakira’s hometown of Barranquilla as well as four other Colombian communities.

In addition to her efforts with the Fundación Pies Descalzos, Shakira has made a number of other notable donations over the years. In 2007, she diverted a whopping $40 million of her wealth to help rebuild community infrastructure in Peru and Nicaragua in the wake of a devastating 8.0 magnitude earthquake. Later, during the COVID-19 pandemic in 2020, Shakira donated a large supply of N95 masks for healthcare workers and ventilators for hospital patients to her hometown of Barranquilla.

Back in 2010, the UN honored Shakira with a medal to recognize her dedication to social justice, at which time the Director General of the International Labour Organization described her as a “true ambassador for children and young people.”

Shakira’s tax fraud scandal: How much did she pay?

In 2018, prosecutors in Spain initiated a tax evasion case against Shakira, alleging she lived primarily in Spain from 2012 to 2014 and therefore failed to pay around $14.4 million in taxes to the Spanish government. Spanish law requires anyone who is “domiciled” (i.e., living primarily) in Spain for more than half of the year to pay income taxes.

During the period in question, Shakira listed the Bahamas as her primary residence but did spend some time in Spain, as she was dating Gerard Piqué, a professional footballer and Spanish citizen. The couple’s first son, Milan, was also born in Barcelona during this period.

Shakira maintained that she spent far fewer than 183 days per year in Spain during each of the years in question. In an interview with Elle Magazine, the pop star opined that “Spanish tax authorities saw that I was dating a Spanish citizen and started to salivate. It's clear they wanted to go after that money no matter what."

Prosecutors in the case sought a fine of almost $26 million and a possible eight-year prison stint, but in November of 2023, Shakira took a deal to close the case, accepting a fine of around $8 million and a three-year suspended sentence to avoid going to trial. In reference to her decision to take the deal, Shakira stated, "While I was determined to defend my innocence in a trial that my lawyers were confident would have ruled in my favour [had the trial proceeded], I have made the decision to finally resolve this matter with the best interest of my kids at heart who do not want to see their mom sacrifice her personal well-being in this fight."

How much did the Shakira statue in Barranquilla cost?

In late 2023, a 21-foot-tall bronze likeness of Shakira was unveiled on a waterfront promenade in Barranquilla. The city’s then-mayor, Jaime Pumarejo, commissioned Colombian sculptor Yino Márquez to create the statue of the city’s treasured pop icon, along with a sculpture of the city’s coat of arms.

According to the New York Times, the two sculptures cost the city the equivalent of around $180,000. A plaque at the statue’s base reads, “A heart that composes, hips that don’t lie, an unmatched talent, a voice that moves the masses and bare feet that march for the good of children and humanity.”

Related: Taylor Swift net worth: The most successful entertainer joins the billionaire's club

bonds pandemic covid-19 real estate africa mexico spainInternational

Delta Air Lines adds a new route travelers have been asking for

The new Delta seasonal flight to the popular destination will run daily on a Boeing 767-300.

Share this:

Those who have tried to book a flight from North America to Europe in the summer of 2023 know just how high travel demand to the continent has spiked.

At 2.93 billion, visitors to the countries making up the European Union had finally reached pre-pandemic levels last year while North Americans in particular were booking trips to both large metropolises such as Paris and Milan as well as smaller cities growing increasingly popular among tourists.

Related: A popular European city is introducing the highest 'tourist tax' yet

As a result, U.S.-based airlines have been re-evaluating their networks to add more direct routes to smaller European destinations that most travelers would have previously needed to reach by train or transfer flight with a local airline.

Shutterstock

Delta Air Lines: ‘Glad to offer customers increased choice…’

By the end of March, Delta Air Lines (DAL) will be restarting its route between New York’s JFK and Marco Polo International Airport in Venice as well as launching two new flights to Venice from Atlanta. One will start running this month while the other will be added during peak demand in the summer.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

“As one of the most beautiful cities in the world, Venice is hugely popular with U.S. travelers, and our flights bring valuable tourism and trade opportunities to the city and the region as well as unrivalled opportunities for Venetians looking to explore destinations across the Americas,” Delta’s SVP for Europe Matteo Curcio said in a statement. “We’re glad to offer customers increased choice this summer with flights from New York and additional service from Atlanta.”

The JFK-Venice flight will run on a Boeing 767-300 (BA) and have 216 seats including higher classes such as Delta One, Delta Premium Select and Delta Comfort Plus.

Delta offers these features on the new flight

Both the New York and Atlanta flights are seasonal routes that will be pulled out of service in October. Both will run daily while the first route will depart New York at 8:55 p.m. and arrive in Venice at 10:15 a.m. local time on the way there, while leaving Venice at 12:15 p.m. to arrive at JFK at 5:05 p.m. on the way back.

According to Delta, this will bring its service to 17 flights from different U.S. cities to Venice during the peak summer period. As with most Delta flights at this point, passengers in all fare classes will have access to free Wi-Fi during the flight.

Those flying in Delta’s highest class or with access through airline status or a credit card will also be able to use the new Delta lounge that is part of the airline’s $12 billion terminal renovation and is slated to open to travelers in the coming months. The space will take up more than 40,000 square feet and have an outdoor terrace.

“Delta One customers can stretch out in a lie-flat seat and enjoy premium amenities like plush bedding made from recycled plastic bottles, more beverage options, and a seasonal chef-curated four-course meal,” Delta said of the new route. “[…] All customers can enjoy a wide selection of in-flight entertainment options and stay connected with Wi-Fi and enjoy free mobile messaging.”

stocks pandemic european europeUncategorized

The Question You Should Ask Whenever You’re Wrong

“Never bet on the end of the world. It only comes once, which is pretty long odds.” — Arthur Cashin, New York Stock Exchange Floor Manager (“Maxims…

Share this:

{kind=link}

“Never bet on the end of the world. It only comes once, which is pretty long odds.” — Arthur Cashin, New York Stock Exchange Floor Manager (“Maxims of Wall Street,” p. 110)

Since Joe Biden gave his State of the Union (or shall we say “Disunion”) speech last week, I’ve encountered a plethora of negative comments about the future of America.

Is the American Dream Over?

“If Biden is re-elected, it will be the end of the American Dream as we know it,” said one pundit on Fox News.

The critics are out in force. Supply-side economist Steve Moore writes, “Biden is intentionally trying to dismantle the American economy with his imbecile energy, climate change, crime, border, inflation, debt and high tax policies.”

Glenn Beck, the host of Blaze TV, recently warned that America may face multiple terrorist attacks in one day, similar to 9/11, given the open borders policy of the Biden Administration.

Recently, I attended a private meeting of political leaders and pundits who thought that President Biden’s address was the most polemical, shrill and divisive talk they had ever heard.

I’ve been watching State of the Union addresses all my adult life, by both Republicans and Democrats, and in many ways they are always polemical and divisive. What was amazing to me is how “sleepy” Joe Biden performed. He must have been well rested and jacked up with some pretty incredible drugs to do as well as he did.

President Biden did say some things that were crazy, such as when he asserted that voting for former president Donald Trump is a “vote against democracy.”

Hey, wasn’t it the Democrats who want to remove Trump from the November ballot in Colorado and other states? Talk about anti-democratic! I was glad to see the Supreme Court ruled 9-0 against the Colorado decision. Let the people decide. Isn’t that what democracy is all about?

Why Then Is the Stock Market at an All-Time High?

Kevin Roberts, the new president of the Heritage Foundation, recently declared, “The American Dream is being threatened as never before!”

If that is true, why is the stock market at or near an all-time high? What are the prophets of doom and gloom missing?

That’s the question I always ask when I’m wrong about something:

“What am I missing?”

Wall Street is a good bellwether of what is going on the country. So far, the benefits outweigh the costs. The economy is recovering from the Covid pandemic, inflation is coming down, corporate profits are strong, new technologies are being introduced and there’s a strong movement to reverse the “cancel” and “woke” culture in the United States.

We have gridlock on Capitol Hill that is keeping a lot of bad legislation from becoming law. The Supreme Court has reversed many bad decisions by the lower courts.

We Remain Fully Invested

So, all is not lost after all. In my newsletter, Forecasts & Strategies, we remain fully invested, despite occasional corrections in the market.

We are also well diversified in some “contrarian” investments such as Bitcoin and gold, both of which continue to outperform and offset any selloffs in the stock market.

By remaining positive and fully invested, we have made good money in 2024.

The American Obituary Has Been Written Many Times

The American economy has been left for dead many times, only to be resuscitated with renewed vigor. We have survived civil and world wars, the Great Depression, the inflationary 1970s, terrorist attacks and more.

As J.P. Morgan once said, “The man who is a bear on the United States will eventually go broke” (“Maxims,” p. 111).

I encourage you to read my favorite J.P. Morgan story found on pp. 218-219 in “The Maxims of Wall Street.” See www.skousenbooks.com.

American exceptionalism is alive and well. We are still the Promised Land with millions wanting to live and work here.

Solving Our Unfunded Liability Problem: Look to Canada!

One serious problem in America is the irresponsible, out-of-control deficit spending and national debt, created by both Republican and Democratic leaders over the years. The trouble is getting worse, with rising interest rates to pay the debt and the growing unfunded liabilities from Social Security and Medicare.

Robert Poole of the Reason Foundation warns:

“The Congressional Budget Office (CBO)’s latest 10-year projection is frightening. CBO projects annual federal budget deficits to increase steadily, exceeding $2.5 trillion by 2034, assuming current policies continue… The federal government is projected to borrow an additional $20 trillion over the next decade, the CBO estimates.

“One driving factor is the impact of higher interest rates on the current $34 trillion (and growing) national debt… By 2034, annual interest expense is projected to be $1.6 trillion — more than one-fourth of all federal tax revenue.

“The Penn Wharton Budget Model suggests that the United States has about 20 years to fix this debt/deficit problem — ‘after which no amount of future tax increases or spending cuts could avoid the government defaulting on its debt.’

“On August 2, 2023, Fitch Ratings downgraded the federal government’s long-term debt rating from AAA to AA+. And on November 10, 2023, Moody’s Investors Service reduced its outlook on the U.S. credit rating from ‘stable’ to ‘negative.’ Standard & Poor’s did its downgrade in 2011. These are warning shots across the ship of state’s bow.”

Sounds ominous. What to do?

Canada faced a similar problem back in the mid-1990s. Deficits were getting out of hand, and the Canadian dollar was sinking. The Conservative Party and the Liberty Party of Canada worked together and resolved to cut government spending, lay off federal workers and then went on a supply-side tax-cutting program that resulted in economic growth and deficit reduction.

What about the unfunded liability problem, which causes national bankruptcy? Again, Canada offers an incredible example of solving the issue.

Last week, Andy Puzder and Terrence Keeley wrote an op-ed in The Wall Street Journal on the success of the Canadian social security system, which has earned a 9.3% annualized return over the past 10 years (versus almost zero return in our Social Security Trust Fund). They wrote:

“The Canada Pension Plan’s superiority stems from its asset allocation. The fund invests about 57% of its assets in equities and 12% in bonds; the rest is divided among real estate, infrastructure and credit. Over the past 10 years, the Canada Pension Plan has realized a 9.3% annualized net return. Similarly to how Social Security works, Canadian citizens pay into the program and are guaranteed lifetime benefits.”

At some point, the United States will need to imitate the Canadian model. Here is a chart on the difference between the two:

In sum, there are solutions to all of our problems — if we know where to look and remain optimistic.

Sound Advice from the ‘Investment Bible’

In my home, I have a whole section of my library devoted to dozens of books written by doomsayers and Cassandras, such as “The Coming Deflation”…. “How to Prosper During the Coming Bad Years”… “Bankruptcy 1995”… “The End of Inflation” and so on.

I’ve also collected a bunch of quotes on doomsayers and Cassandras in “The Maxims of Wall Street.”

Jim Woods, my colleague at Eagle Publishing, is a big fan.

Jim states, “I’ve always felt that a collection of wisdom from the best brains in that industry has been most special to me. And on this front, there is no better ‘how to’ anthology than the one by my friend, fellow Fast Money Alert co-editor and brilliant economist, Dr. Mark Skousen. The ‘Maxims of Wall Street’ is a collection of some of the greatest wisdom ever to flow from the biggest and brightest names on Wall Street. Great investors such as Jesse Livermore, Baron Rothschild, J.P. Morgan, Benjamin Graham, Warren Buffett, Peter Lynch and John Templeton are just a sneak peek at some of the names you’ll discover in this fantastic collection. Then, there is profundity from the likes of Ben Franklin, John D. Rockefeller, Joe Kennedy, Bernard Baruch, John Maynard Keynes, Steve Forbes and numerous other luminaries too copious to mention.”

If you don’t have an autographed copy of my collection of quotes, stories and wisdom of the world’s top traders and investors, please order a copy now.

It is in its 10th edition, having sold nearly 50,000 copies. It has been endorsed by Warren Buffett, Kevin O’Leary, Jack Bogle, Kim Githler, Bert Dohmen, Richard Band and Gene Epstein in Barron’s.

I offer it cheaply to my Skousen CAFÉ readers: Only $21 for the first copy, and all additional copies are $11 each (they make a great gift to clients, friends, relatives and your favorite broker or money manager). I sign and number each one, then mail it at no extra charge if you live in the United States. If you order an entire box (32 copies), the price is only $327. As Hetty Green, the first female millionaire, once said, “When I see a good thing going cheap, I buy a lot of it!”

To order, go to www.skousenbooks.com.

You Nailed it!

Friedrich Hayek Won the Nobel Prize 50 Years Ago

“Mises and Hayek articulated and vastly enriched the principles of Adam Smith at a crucial time in this century.” — Vernon Smith (2002 Nobel prize in economics)

March 23 is the anniversary of the passing of a giant in economics — the Austrian economist Friedrich Hayek (1899-1992).

He is most famous for his bestselling book “The Road to Serfdom,” written near the end of World War II, an admittedly a pessimistic book, warning the West that its move toward socialism, fascism and communism was indeed a “road to serfdom.”

Then, when he won the Nobel prize in economics in 1974, he warned again of the dangers of “accelerating inflation,” which he said, were “brought about by policies which the majority of economists recommended and even urged governments to pursue. We have indeed at the moment little cause for pride: as a profession we have made a mess of things.”

Fortunately, we have moved away from the road to serfdom, especially after the collapse of the Berlin Wall and the Soviet socialist central planning model.

But the road to freedom has been a checkered one, and we must always be alert to losing our liberties in the name of inequality, fairness and social justice.

Last month, Tom Woods interviewed me in honor of the 50th anniversary of Hayek’s winning the Nobel prize. Watch the interview here.

Mark Skousen, Friedrich Hayek and Gary North in Austria, 1985

I had the pleasure of interviewing Hayek for three hours in the Austrian alps in 1985. He was especially happy to hear I resurrected his macroeconomic model in developing gross output (GO). See www.grossoutput.com, a measure of Hayek’s triangles.

This week, Larry Reed, former president of the Foundation for Economic Education, wrote this wonderful tribute to Hayek.

Highly recommended.

Good investing, AEIOU,

Mark Skousen

The post The Question You Should Ask Whenever You’re Wrong appeared first on Stock Investor.

bonds pandemic equities bitcoin real estate canadian dollar gold

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

The Question You Should Ask Whenever You’re Wrong

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Health Officials: Man Dies From Bubonic Plague In New Mexico

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International6 days ago

International6 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges