Government

Futures Slide, Nasdaq Plunges As Yields Surge And Oil Tops $80

Futures Slide, Nasdaq Plunges As Yields Surge And Oil Tops $80

For much of 2021, a vocal contingent of market bulls had claimed that there is no way the broader market could sell off as long as the gigacap tech "general" refused to drop….

Share this:

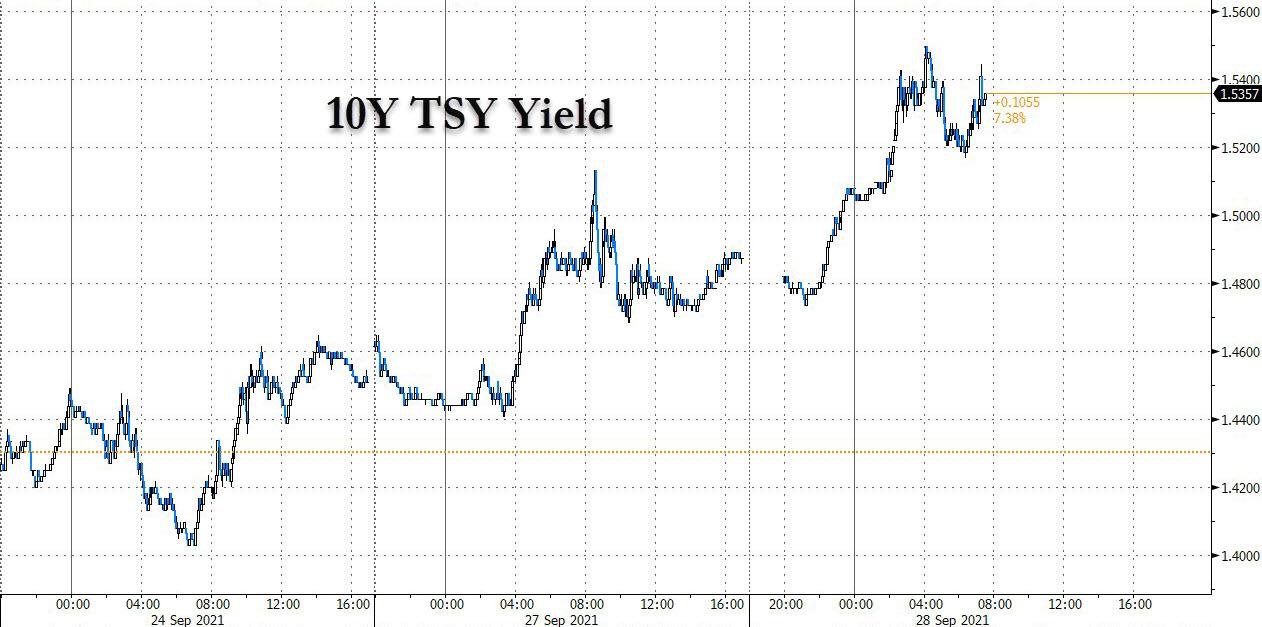

For much of 2021, a vocal contingent of market bulls had claimed that there is no way the broader market could sell off as long as the gigacap tech "general" refused to drop. Well, it looks like that day is finally upon us because this morning US equity futures are sliding again, continuing their Monday drop as yields from the US to Germany again, the 10Y TSY rising as high as 1.55%, driven to an extent by Fed tapering fears but mostly by the surge in oil which has pushed Brent above $80, the highest price since late 2018. The dollar gained amid the deteriorating global supply crunch from oil to semiconductors.

The surge in oil sparked a new round of stagflation fears, sending Nasdaq futures down 240 points or 1.3% as the yield on the benchmark 10-year U.S. Treasury climbed sharply. S&P 500 and Dow Jones futures also retreated, with spoos sliding below 4,400 as to a session low of 4,390.

Rising bond yields prompted a shift from growth to cyclical stocks in the United States, in a move that analysts expect could become more permanent after a prolonged period of supressed bond yields. The premarket selloff was led by semiconductor stocks which tracked similar falls for European peers, as a rising 10-year Treasury yield puts pressure on the tech sector. Applied Materials Inc. led a slump in chip stocks in New York premarket trading while Nvidia was down 2.6%, AMD -2.1%, Applied Materials -2.9%, Micron -1.6%. Meanwhile retail trader favorite meme stock Naked Brand Group, an underwear and swimwear retailer, rises again after having surged 40% in the past two trading sessions after Chairman Justin Davis-Rice said in a letter to shareholders that he believes the company has found a “disruptive” potential acquisition in the clean technology sector. Frequency Electronics also soared after being awarded a contract by the Office of Naval Research to develop an atomic clock. Chinese stocks listed in the U.S. were mixed and semiconductor stocks declined. Here are some of the other notable U.S. movers today:

- iPower (IPW US) shares rise as much as 61% in U.S. premarket trading after the online hydroponics equipment retailer posted 4Q and FY21 earnings

- Alibaba (BABA US) rises 2.5% in U.S. premarket trading after the company’s shares listed in Hong Kong rose, adding to the Hang Seng Tech Index’s gains

- Frequency Electronics (FEIM US) soars 20% in U.S. premarket trading after being awarded a contract by the Office of Naval Research to develop an atomic clock

- Concentrix (CNXC) jumped 5.9% in Monday after hours trading after setting its first dividend payment and buyback program since being spun off from from Synnex in December

- Brookdale Senior Living (BKD US) shares fell in extended trading on Monday after announcing a $200 million convertible bond offering

- Altimmune (ALT US) rose as much as 4.2% in Monday postmarket trading on plans to announce results for an early stage study of ALT-801 in overweight people on Tuesday

- Ziopharm Oncology (ZIOP US) fell in extended trading after company said it cut about 60 positions, or a more than 50% reduction in personnel, to extend its cash runway into 1H 2023

- Montrose Environmental Group (MEG US) was down 2.8% Monday postmarket after offering shares via JPMorgan, BofA Securities, William Blair

The main catalyst for the stock selloff was the continued drop in Treasurys which sent the 10-year Treasury rising as high as 1.55% while shorter-dated rates surged toward pre-pandemic levels.

This in turn was driven by the relentless meltup in commodities: overnight Brent roared above $80 a barrel - on its way to Goldman's revised $90 price target - on louder signs that demand is running ahead of supply and depleting inventories as the world finds itself in an unprecedented energy crisis. The international crude benchmark extended a recent run of gains to hit the highest since October 2018, while West Texas Intermediate also climbed.

Oil’s latest upswing has come with a flurry of bullish price predictions from banks and traders, forecasts for surging demand this winter, and speculation the industry isn’t investing enough to maintain supplies. The jump to $80 also is adding inflationary pressure to the global economy at a time when prices of energy commodities are soaring. European natural gas, carbon permits and power rose to fresh records Tuesday, with little sign of the rally slowing.

As Bloomberg notes, traders have begun reassessing valuations amid multiplying global risks, while Fed officials have communicated increasingly hawkish signals in recent days as supply-chain bottlenecks threaten to keep inflation elevated. China’s growth slowdown which saw Goldman lower its q/q Q3 GDP forecast to a flat 0.0%, and a debt crisis in the nation’s property market.have also fueled the risk-off shift.

"Central bankers have set out how they want to normalize monetary policy for some time,” Chris Iggo, chief investment officer for core investments at AXA Investment Managers, said in a note. “That process could start soon. The realization of this has the potential to provoke some volatility in rates and equities."

Elsewhere, European stocks also declined with the Stoxx Europe 600 dragged down most by technology shares. Europe’s Stoxx Tech Index drops as much as 2.8% to a five-week low after falling 1.5% on Monday having previously touched its highest level since 2000 earlier in the month. Single-stock downgrades also weighed. Stocks which performed particularly well this year are among the biggest fallers, with chip equipment makers BE Semi -4.6% and ASML -4.4%, and chipmaker Nordic Semi down 4.2%. Among other laggards, Logitech drops as much as 8.5% after being downgraded to underweight at Morgan Stanley.

Earlier in the session, Asian stocks fell for the first time in four days as declines in technology names overshadowed a rally in energy shares. The MSCI Asia Pacific Index dropped as much as 0.7%, with a jump in U.S. Treasury yields weighing on richly-valued tech stocks. That’s even as the region’s oil and gas shares climbed amid signs of a global energy crunch. Chipmakers Taiwan Semiconductor Manufacturing and Samsung Electronics were the biggest drags on the Asian benchmark.

“The climb in yields led to the selling of growth stocks that have been strong, with investors rotating into names that are sensitive to business cycles - not unlike what happened in U.S. equities,” said Shutaro Yasuda, an analyst at Tokai Tokyo Research Center. Asian equities have been recovering after being whipsawed by concerns over any fallout from China Evergrande Group’s debt troubles. As worries over the distressed property developer abate, the pace of rise in Treasury yields and global inflation data are being closely watched for clues on the U.S. Federal Reserve’s policy stance. Australia’s equity benchmark was among the biggest losers in Asia Tuesday, dragged down by losses in mining and healthcare stocks. Still, broad-based gains in oil explorers and refiners helped mitigate the Asian market’s retreat. In South Korea, importers and distributors of liquefied petroleum gas and liquefied natural gas rallied as the price of natural gas jumped.

The future of Evergrande is being forensically scrutinized by investors after the company last Friday did not meet a deadline to make an interest payment to offshore bond holders. Evergrande has 30 days to make the payment before it falls into default and Shenzen authorities are now investigating the company's wealth management unit. Without making reference to Evergrande, the People's Bank of China (PBOC) said Monday in a statement posted to its website that it would "safeguard the legitimate rights of housing consumers".

Widening power shortages in China, meanwhile, halted production at a number of factories including suppliers to Apple Inc and Tesla Inc and are expected to hit the country's manufacturing sector and associated supply chains. Analysts cautioned the ongoing blackouts could affect the country's listed industrial stocks.

"What we see in China with the developers and the blackouts is going to be a negative weight on the Asian markets," Tai Hui, JPMorgan Asset Management's Asian chief market strategist told Reuters. "Most people are trying to work out the potential contagion effect with Evergrande and how far and wide it could go. We keep monitoring the policy response and we have started to see some shift towards supporting homebuyers which is what we have been expecting."

In rates, as noted above, the selloff in Treasuries gathered pace in Asia, early Europe session leaving yields cheaper by 3.5bp to 5.5bp across the curve with 20s and 30s extending above 2% and 10-year through 1.50%. Treasury 10-year yields traded around 1.53%, cheaper by 4.5bp on the day after topping at 1.55%, highest since mid-June; in front- and belly, 2- and 5-year yields remain near cheapest levels in at least 18 months; in 10-year sector, gilts lag by 3bp vs. Treasuries while German yields are narrowly richer. Gilts underperformed further, where long-end yields are cheaper by up to 7.5bp on the day.

Treasury futures volumes over Asia, early European session were at more than twice usual levels, with most activity seen in 10-year note contract; eurodollar futures volumes were also well above recent average. With recent aggressive move higher in yields, threat of convexity hedging has exacerbated moves as rate hike premium continues to filter into the curve after last week’s FOMC. Auctions conclude Tuesday with 7-year note sale, while busy Fed speaker slate includes Fed Chair Powell.

In FX, the Bloomberg dollar index reached the highest level in more than a month as rising energy costs drove up Treasury yields for a fourth session. The dollar gained against all its peers; Japan’s currency slid for a fifth day against the greenback before a speech Tuesday from Fed Chair Jerome Powell who will say inflation is elevated and is likely to remain so in coming months, according to prepared remarks. Treasury two-year yields rose to the highest since March 2020. “Dollar-yen saw the clearest expression of Treasury yield increases and we attributed this divergence to the surge in energy prices,” says Christopher Wong, senior foreign-exchange strategist at Malayan Banking in Singapore. U.S. natural gas futures soared to their highest since February 2014 on concern over tight inventories. Brent oil topped $80 a barrel amid signs demand is outrunning supply. The euro slipped to hit its lowest level since Aug. 20, nearing the year-to-date low of $1.1664. The Treasury yield curve bear steepened; euro curves followed suit, with the yield on U.K. 10-year notes soaring past 1% for the first time since March 2020 on the prospects for Bank of England policy tightening.

In commodities, Crude futures extend Asia’s gains. WTI rises as much as 1.6% to highs of $76.67 before stalling. Brent holds above $80. Spot gold trades around last week’s lows near $1,740/oz. Base metals are mixed: LME aluminum outperforming, rising as much as 1.1%; nickel and copper are in the red.

Looking at the day ahead, one of the main highlights will be the appearance of Fed Chair Powell, and Treasury Secretary Yellen at the Senate Banking Committee. Otherwise, central bank speakers include ECB President Lagarde, Vice President de Guindos, and the ECB’s Schnabel, Panetta and Kazimir, along with the BoE’s Mann and the Fed’s Evans, Bowman and Bostic. US data highlights include the US Conference Board’s consumer confidence indicator for September and the FHFA house price index for July.

Market Snapshot

- S&P 500 futures down 0.7% to 4,403.50

- STOXX Europe 600 down 1.2% to 456.83

- MXAP down 0.4% to 200.06

- MXAPJ down 0.4% to 641.05

- Nikkei down 0.2% to 30,183.96

- Topix down 0.3% to 2,081.77

- Hang Seng Index up 1.2% to 24,500.39

- Shanghai Composite up 0.5% to 3,602.22

- Sensex down 1.4% to 59,209.94

- Australia S&P/ASX 200 down 1.5% to 7,275.55

- Kospi down 1.1% to 3,097.92

- Brent Futures up 0.8% to $80.15/bbl

- Gold spot down 0.4% to $1,742.61

- U.S. Dollar Index up 0.20% to 93.57

- German 10Y yield rose 2.7 bps to -0.196%

- Euro down 0.1% to $1.1681

Top Overnight News from Bloomberg

- Chinese authorities are striving to signal to traders that whatever happens to China Evergrande Group, its debt crisis won’t spiral out of control or derail the economy

- Brent oil roared above $80 a barrel, the latest milestone in a global energy crisis, on signs that demand is running ahead of supply and depleting inventories

- As the dust settles on Germany’s election, control over the finances of Europe’s largest economy could fall to a 42-year-old former tech entrepreneur who wants to lower taxes and tighten spending

- Wells Fargo agreed to pay $37 million in penalties and forfeiture to settle U.S. claims that it overcharged almost 800 commercial customers that used its foreign exchange services, the latest in a series of scandals at the bank

A more detailed look at global markets courtesy of Newsquawk

Asian equity markets traded mixed following on from a Wall Street lead where value outperformed growth and tech suffered as yields rose. ASX 200 (-1.5%) was the laggard with losses in healthcare, gold miners and tech frontrunning the declines which dragged the index beneath 7300. Nikkei 225 (-0.2%) was lacklustre and briefly approached 30k to the downside but then bounced off worse levels amid a softer currency, while the KOSPI (-1.1%) also declined following a suspected North Korean ballistic missile launch and with a recent South Korean court order to sell seized Mitsubishi Heavy assets as compensation for wartime forced labour, threatening a flare up of tensions between Japan and South Korea. Hang Seng (+1.2%) and Shanghai Comp. (+0.5%) were underpinned after the PBoC continued to inject liquidity ahead of the approaching National Day holidays and with Hong Kong led higher by strength in property names after the PBoC stated it will safeguard legitimate rights and interests of housing consumers which also provided Evergrande-related stocks further reprieve from their recent sell-off. Finally, 10yr JGBs retreated on spillover selling from T-notes after yields rose on the back of further Fed taper rhetoric and with prices not helped by the uninspiring 2yr and 5yr auctions stateside, while weaker results at the 40yr JGB auction also provided a headwind for prices.

Top Asian News

- Top-Performing Global Luxury Stock Seen Cooling After 680% Gain

- China Power Price Hike Sought Amid Supply Crunch: Energy Update

- Macau Evacuates Airport Quarantine Hotel After Outbreak

- Iron Ore Dips Again as China Power Crisis Adds to Steel Curbs

Bourses in Europe extended on the losses seen at the cash open and trade lower across the board (Euro Stoxx 50 -1.7%; Stoxx 600 -1.7%) as sentiment retreated from a mixed APAC handover as month-end looms alongside tier 1 data and a slew of central bank speakers. US equity futures have also succumbed to the mood in Europe alongside the surge in global yields – which takes its toll on the NQ (-1.5%) vs the ES (-0.8%), YM (-0.4%) and RTY (-0.3%). From a more technical standpoint, ESZ1 fell under its 50 DMA (4,431) and tested the 4,400 level to the downside, whilst NQZ1 briefly fell under 15k and the YMZ1 inches towards its 100 DMA (34,489). Back to Europe, the FTSE 100 (-0.4%) sees losses to a lesser extent vs its European peers as energy prices and yields keep the index oil giants and banks supported – with some of the top gainers including Shell (+2.8%), BP (+2.1%). Sectors in Europe are predominantly in the red, but Oil & Gas buck the trend. Sectors also portray more of a defensive bias, whilst the downside sees Tech, Real Estate, and Travel & Leisure at the foot of the bunch, with the former hit by the rise in yields, which sees the US 10yr further above 1.50%, the 20yr above 2.00% and the UK 10yr hitting 1.00% for the first time since March 2020. In terms of individual movers, Smiths Group (+3.8%) is at the top of the Stoxx 600 following encouraging earnings. ING (+0.3%) holds onto gains after sources noted SocGen's (-0.6%) interest in ING's retail banking arm. Finally, chip-maker ASM International (-3.5%) has succumbed to the broader tech weakness despite upping its guidance and announcing capacity expansion by early 2023.

Top European News

- U.K. 10-Year Yield Rises Past 1% for First Time Since March 2020

- Goldman’s Petershill Unit Valued at $5.5 Billion in U.K. IPO

- Go-Ahead Sinks as U.K. Takes Over Southeastern Rail Franchise

- Hedge Funds and Private Equity Are Targeting European Soccer

In FX, It took a while for the index to breach resistance ahead of 93.500, but when US Treasuries resumed their bear-steepening run and the intensity of the moves in futures and cash picked up pace the break beyond the half round number was relatively quick and decisive. Indeed, the DXY duly surpassed its post-FOMC peak (93.526) and a prior recent high from August 19 (93.587) on the way to reaching 93.619 amidst almost all round Dollar gains, as 5, 10, 20 and 30 year yields all rallied through or further above psychological levels (such as 1%, 1.5% and 2% in the case of the latter two maturities). However, petro and a few other commodity currencies are displaying varying degrees of resilience in the face of general Greenback strength that is compounded by buy signals for September 30 rebalancing on spot month, quarter and half fy end. Ahead, trade data, consumer confidence, more regional Fed surveys, speakers and the 7 year auction.

- NZD/CHF/JPY/AUD - The Kiwi was already losing altitude above 0.7000 vs its US counterpart and 1.0400 against the Aussie on Monday, so the deeper retreat is hardly surprising to circa 0.6975 and 1.0415 awaiting some independent impetus that may come via NZ building consents tomorrow. Meanwhile, the Franc has recoiled towards 0.9300 in advance of comments from SNB’s Maechler and the Yen continues to suffer on the aforementioned rampant yield and steeper curve trajectory on top of a more pronounced 1+ sd portfolio hedge selling requirement vs the Buck, with Usd/Jpy meandering midway between 110.94-111.42 parameters irrespective of renewed risk aversion due to same bond rout dynamic. Back down under, Aud/Usd has faded from around 0.7311 to the low 0.7260 area, though holding up a bit better in wake of not quite as weak as forecast final retail sales overnight.

- CAD/EUR/GBP - All softer against their US rival, but the Loonie putting up a decent fight with ongoing help from WTI crude that has now topped Usd 76.50/brl, and Usd/Cad also has decent option expiry interest to keep an eye on given 1.2 bn rolling off at 1.2615 and an even heftier 3 bn at 1.2675 compared to current extremes spanning 1.2693-1.2652. Elsewhere, the Euro has lost its battle to stay afloat of multiple sub-1.1700 lows even though EGBs are tumbling alongside USTs and the same goes for Sterling in relation to the 1.3700 handle irrespective of the 10 year Gilt touching 1% for the first time since March 2020.

- SCANDI/EM - Brent’s advances on Usd 80 brl have been offset to an extent by soft Norwegian retail sales data, as the Nok pares more of its post-Norges Bank gains, while the Sek looks somewhat caught between stalls following a recovery in Swedish consumption, but big swing in trade balance from surplus to larger deficit. However, the Try is taking no delight from the costlier price of oil or remarks from Turkey’s Deputy Finance Minister contending that interest rates can move lower by reducing the current account and budget deficits, or conceding that Dollarisation is a problem and steps need to be taken to enhance confidence in the Lira. Conversely, the Cnh and Cny are still holding a firm line following another net injection of 2 week funds from the PBoC and the Governor saying that China will lengthen the period for the implementation of normal monetary policy, adding that it has conditions to keep a normal and upward yield curve, as it sees no need to purchase assets at present.

In commodities, WTI and Brent futures have extended on the gains seen during APAC hours, which saw the Brent November contract topping USD 80/bbl, albeit the volume and open interest has migrated to the December contract – which topped out just before the USD 80/bbl mark. WTI November meanwhile advanced past the USD 76/bbl mark to a current peak at USD 76.67/bbl (vs low USD 75.21/bbl). Desks have been attributing the leg higher to tight supply – with the UK fuel situation further deteriorating amid a shortage of drivers coupled with panic buying. It's worth bearing in mind that the demand side of the equation has also seen supportive, with the US announcing the lifting of international travel curbs recently alongside the economic resilience to the Delta variant heading into the winter period. Traders would also be keeping an eye on the electricity situation in China, which in theory would provide tailwinds for diesel demand via generators, although this could be offset by a slowdown in economic activity due to power outages. There has also been growing noise for OPEC+ to hike output beyond the monthly plan of 400k BPD, with some African nations also struggling to ramp up production due to maintenance issues and lack of investments. Ministers recently noted that the plan would be maintained at next week's confab. As a reminder, the OPEC World Oil Outlook is set to be released at 13:30BST/08:30EDT, although the findings may be stale given the recent developments in crude dynamics. Major banks have also provided commentary on Brent following Goldman Sachs' bullish call recently, with Barclays upping its forecast for both benchmarks due to supply deficits, whilst Morgan Stanley maintained its forecast but suggested that the USD 85/bbl Brent scenario clearly exists. MS also noted that oil inventories continue to draw at high rates and suggest that the market is more undersupplied than generally perceived; the analysts see the market undersupplied into 2022 amid its expectation for further OPEC discipline. Nat gas also remains in focus, with prices +11% at one point, whilst Russia's Kremlin said Russia remains the safeguard of natural gas to Europe and Gazprom is ready to discuss new gas supply contracts with increased volumes to meet rising European demand. It's also worth being aware of the increasing likelihood of state intervention at these levels as nations attempt to save or at least cushion consumers and company margins. Elsewhere, precious metals are under pressure as the Buck remains buoyant, with spot gold still under USD 1,750/oz as it inches closer to the 11th August low of USD 1,722/oz. Spot silver remains within recent ranges above USD 22/oz. Overnight Chinese nickel and tin prices extended losses with traders citing subdued demand, whilst coking coal and coke futures leapt on tight supply.

US Event Calendar

- 8:30am: Aug. Advance Goods Trade Balance, est. -$87.3b, prior -$86.4b, revised -$86.8b

- 8:30am: Aug. Retail Inventories MoM, est. 0.5%, prior 0.4%; Wholesale Inventories MoM, est. 0.8%, prior 0.6%

- 9am: July S&P CS Composite-20 YoY, est. 20.00%, prior 19.08%

- 9am: July S&P/CS 20 City MoM SA, est. 1.70%, prior 1.77%

- 9am: July FHFA House Price Index MoM, est. 1.5%, prior 1.6%

- 10am: Sept. Conf. Board Consumer Confidence, est. 115.0, prior 113.8

- Expectations, prior 91.4

- Present Situation, prior 147.3

- 10am: Sept. Richmond Fed Index, est. 10, prior 9

Central Bank Speakers

- 9am: Fed’s Evans Makes Welcome Remarks at Payments Conference

- 10am: Powell and Yellen Appear Before Senate Banking Panel

- 1:40pm: Fed’s Bowman Speaks at Community Bank Event

- 3pm: Fed’s Bostic Discusses the Economic Outlook

- 7pm: Fed’s Bullard Discusses U.S. Economy and Monetary Policy

DB's Jim Reid concludes the overnight wrap

What a difference a week makes. You hardly hear the word Evergrande now. We asked in a flash poll last week whether we would still be talking about it in a month or whether it would be a distant memory by then. Maybe we should have narrowed the time frame to a week! We’ve quickly moved on to rate hikes and rising bond yields as the topic de jour. A further rise in the Bloomberg Commodity Spot Index (+1.87%) to a fresh high for the decade helped reinforce the move.

Indeed, sovereign bond yields moved higher once again yesterday amidst a sharp rise in inflation expectations, with those on 10yr Treasury yields rising +3.6bps to 1.487%, their highest level in over 3 months. Meanwhile the 2yr yield rose +0.8bps to 0.278%, its highest level since the pandemic began, which comes on the back of last week’s Fed meeting that prompted investors to price in an initial rate hike from the Fed by the end of 2022.

The moves in Treasury yields were almost entirely driven by higher inflation breakevens, with 10yr breakevens up +3.7bps. That echoed similar moves in Europe, where the German 10yr breakeven (+4.7bps) hit a post-2013 high of 1.653%, and their Italian counterparts (+3.9bps) hit a post-2011 high. The biggest move was in the UK however, where the 10yr breakeven (+13.2bps) reached its highest level since 2008, which comes amidst a continued fuel shortage in the country, alongside another rise in UK natural gas futures, which were up +8.20% yesterday to £190/therm, exceeding the previous closing peak set a week earlier. We were waiting for the wind to blow in this country to get alternatives back on stream and boy did it blow yesterday but with no impact yet on gas prices. Lower real rates dampened the rise in yields across the continent, though yields on 10yr bunds (+0.5bps), OATs (+0.9bps), BTPs (+1.3bps) and gilts (+2.7bps) had all moved higher by the close of trade.

Those spikes in commodity prices were evident more broadly yesterday, with energy prices in particular seeing a major increase. Brent crude oil prices were up +1.84% to $79.53/bbl, marking their highest closing level since late-2018, and this morning in trading they have now exceeded the $80/bbl mark with a further +0.94% increase. It was much the same story for WTI (+1.99%), which closed at $75.45/bbl, which was its own highest closing level since 2018 too. And those pressures in UK natural gas prices we mentioned above were seen across Europe more broadly, where futures were up +8.92%.

With yields moving higher and inflationary pressures growing stronger, tech stocks struggled significantly yesterday, with the NASDAQ down -0.52%. The megacap tech FANG+ index fell -0.15% on the day, but was initially down as much as -1.7% in early trading. The NASDAQ underperformed the S&P 500, which was only down -0.28%, but that masked significant sectoral divergences, with interest-sensitive growth stocks struggling, just as cyclicals more broadly posted fresh gains. More specifically, energy (+3.43%), bank (+2.29%) and autos (+2.19%) led the S&P, while biotech (-1.65%) and software (-1.39%) shares were among the largest laggards. European equities were also pretty subdued, with the STOXX 600 down -0.19%, though the DAX was up +0.27% following the results of the German election, which removed the tail risk outcome of a more left-wing coalition featuring the SPD, the Greens and Die Linke.

Staying on the political scene, we are now less than 72 hours away from a potential US government shutdown as it stands. As was expected, Republicans in the Senate blocked the House-passed measure to fund the government for another 2 months and raise the debt ceiling for 2 years. While Democrats have not put forward their alternative strategy if Republicans refuse to vote to lift the debt ceiling, their only option would be to attach it to the budget reconciliation plan that currently makes up much of the Biden economic agenda. In an effort to keep all party members on board, Speaker Pelosi moved the vote on the $550bn bipartisan infrastructure bill to Thursday in order to give all sides more time to finish the larger budget bill and pass both together. It is a going to be a very busy Thursday, since Congress will have to also pass the funding bill that day. Republicans and Democrats already agree on a funding bill to keep the government open that does not include the debt ceiling increase so it is just a matter of how exactly the debt ceiling provision goes through without a Republican Senate vote.

Overnight in Asia, equity indices are seeing a mixed performance. On the one hand, most of the region including the Nikkei (-0.24%) and KOSPI (-0.80%) are trading lower as investors begin to price in tighter monetary policy from the Fed. However, the Hang Seng (+1.50%), Shanghai Composite (+0.53%) and CSI (0.38%) have all advanced after the People’s Bank of China said that they would ensure a “healthy property market”. Looking forward, US equity futures are pointing to little change, with those on the S&P 500 down just -0.05%, and 10yr Treasury yields have risen +1.9bps this morning to trade above 1.50% again.

Back to the German election, where the aftermath yesterday saw various party leaders assess the results and stake their claims to participate in a new coalition. As a reminder, the SPD came in first place with 25.7%, but the CDU/CSU weren’t far behind on 24.1%, making it mathematically possible for either to form a government in a coalition with the Greens and the FDP. The SPD’s chancellor candidate, Finance Minister Olaf Scholz, appealed for the Greens and FDP to join him in forming a government, and told the media that he wanted to form a coalition before Christmas. Meanwhile Green co-leader Robert Habeck said that “Of course there is a certain priority for talks with the SPD and the FDP”, but said that this didn’t mean they wouldn’t speak with the CDU/CSU either.

As the SPD were calling for an alliance, the tone sounded more negative from the CDU’s leadership, even though Armin Laschet said that he had not given up on the idea of forming a government. Notably, Laschet said that no party was able to draw a clear mandate from the result, including the SPD, and this echoed remarks from the CSU leader Markus Söder, who said that the conservatives had no mandate to form a government, though they could “make an offer out of a sense of responsibility for the country.” Meanwhile, attention will turn to the FDP and the Greens to see which way they’re leaning when it comes to forming a government. FDP leader Lindner said that he would hold preliminary talks with the Greens, after which they would be open to invitations from either the SPD or the CDU/CSU for further discussions.

Back on the UK, there was an interesting speech from BoE Governor Bailey yesterday, where he echoed the line from the MPC minutes last week, saying that “all of us believe that there will need to be some modest tightening of policy to be consistent with meeting the inflation target sustainable over the medium-term”. However, he also said that their view was that “the price pressures will be transient”, and that “monetary policy will not increase the supply of semi-conductor chips … nor will it produce more HGV drivers.” He then further added that tighter policy “could make things worse in this situation by putting more downward pressure on a weakening recovery of the economy”. So a bit of a mixed message of backing rate hike expectations but warning about its impact on growth.

Over in the US we heard from a host of Fed speakers with Governor Brainard saying that while “employment is still a bit short of the mark” of “substantial further progress”, she expects that the labour market will recover enough to start tapering asset purchases soon. Separately on the inflation debate, Minneapolis Fed President Kashkari argued that this year’s pickup in US inflation has been a byproduct of the supply disruptions associated with Covid and that policy makers should not react to it just yet. He cited the need to get US employment back up as the Fed’s “highest priority”. New York Fed President Williams agreed with his colleague, saying that “this process of adjustment may take another year or so to complete as the pandemic-related swings in supply and demand gradually recede.” And Chicago Fed President Evans is even worried about downside inflation risks, as he is " more uneasy about us not generating enough inflation in 2023 and 2024 than the possibility that we will be living with too much.”

Lastly, news came out yesterday that Boston Fed President Rosengren will retire this week due to health concerns. He was due to step down in June regardless as there is a mandatory retirement age of 65. Dallas Fed President Kaplan also announced his retirement yesterday, which will take effect October 8th. Both officials have drawn scrutiny in recent days stemming from their recent disclosure of trading activity over the last year, though the activity did not violate the Fed’s ethics code even as Fed Chair Powell announced an official review of those rules. The Boston Fed President will be a voting member on the FOMC next year, and the Dallas Fed President in 2023.

Running through yesterday’s data, the preliminary reading for US durable goods orders in August showed growth of +1.8% (vs. +0.7% expected), and the previous month was also revised up to show growth of +0.5% (vs. -0.1% previously). Meanwhile core capital goods orders grew by +0.5% (vs. +0.4% expected), and the previous month’s growth was revised up two-tenths. Finally, the Dallas Fed’s manufacturing activity index for September came in at 4.6 (vs. 11.0 expected) – its lowest reading since July 2020.

To the day ahead now, and one of the main highlights will be the appearance of Fed Chair Powell, and Treasury Secretary Yellen at the Senate Banking Committee. Otherwise, central bank speakers include ECB President Lagarde, Vice President de Guindos, and the ECB’s Schnabel, Panetta and Kazimir, along with the BoE’s Mann and the Fed’s Evans, Bowman and Bostic. US data highlights include the US Conference Board’s consumer confidence indicator for September and the FHFA house price index for July.

Government

Looking Back At COVID’s Authoritarian Regimes

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

Share this:

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

These are the opening two paragraphs of my latest Defining Ideas article, “Looking Back at COVID’s Authoritarian Regimes,” Defining Ideas, March 14, 2024.

Another excerpt:

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

Read the whole thing, which is longer than usual.

(0 COMMENTS) budget deficit coronavirus covid-19 white house fauci trump canadaInternational

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Authored by Zachary Stieber via The Epoch Times (emphasis…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

People who recovered from COVID-19 and received a COVID-19 shot were more likely to suffer adverse reactions, researchers in Europe are reporting.

Participants in the study were more likely to experience an adverse reaction after vaccination regardless of the type of shot, with one exception, the researchers found.

Across all vaccine brands, people with prior COVID-19 were 2.6 times as likely after dose one to suffer an adverse reaction, according to the new study. Such people are commonly known as having a type of protection known as natural immunity after recovery.

People with previous COVID-19 were also 1.25 times as likely after dose 2 to experience an adverse reaction.

The findings held true across all vaccine types following dose one.

Of the female participants who received the Pfizer-BioNTech vaccine, for instance, 82 percent who had COVID-19 previously experienced an adverse reaction after their first dose, compared to 59 percent of females who did not have prior COVID-19.

The only exception to the trend was among males who received a second AstraZeneca dose. The percentage of males who suffered an adverse reaction was higher, 33 percent to 24 percent, among those without a COVID-19 history.

“Participants who had a prior SARS-CoV-2 infection (confirmed with a positive test) experienced at least one adverse reaction more often after the 1st dose compared to participants who did not have prior COVID-19. This pattern was observed in both men and women and across vaccine brands,” Florence van Hunsel, an epidemiologist with the Netherlands Pharmacovigilance Centre Lareb, and her co-authors wrote.

There were only slightly higher odds of the naturally immune suffering an adverse reaction following receipt of a Pfizer or Moderna booster, the researchers also found.

The researchers performed what’s known as a cohort event monitoring study, following 29,387 participants as they received at least one dose of a COVID-19 vaccine. The participants live in a European country such as Belgium, France, or Slovakia.

Overall, three-quarters of the participants reported at least one adverse reaction, although some were minor such as injection site pain.

Adverse reactions described as serious were reported by 0.24 percent of people who received a first or second dose and 0.26 percent for people who received a booster. Different examples of serious reactions were not listed in the study.

Participants were only specifically asked to record a range of minor adverse reactions (ADRs). They could provide details of other reactions in free text form.

“The unsolicited events were manually assessed and coded, and the seriousness was classified based on international criteria,” researchers said.

The free text answers were not provided by researchers in the paper.

“The authors note, ‘In this manuscript, the focus was not on serious ADRs and adverse events of special interest.’” Yet, in their highlights section they state, “The percentage of serious ADRs in the study is low for 1st and 2nd vaccination and booster.”

Dr. Joel Wallskog, co-chair of the group React19, which advocates for people who were injured by vaccines, told The Epoch Times: “It is intellectually dishonest to set out to study minor adverse events after COVID-19 vaccination then make conclusions about the frequency of serious adverse events. They also fail to provide the free text data.” He added that the paper showed “yet another study that is in my opinion, deficient by design.”

Ms. Hunsel did not respond to a request for comment.

She and other researchers listed limitations in the paper, including how they did not provide data broken down by country.

The paper was published by the journal Vaccine on March 6.

The study was funded by the European Medicines Agency and the Dutch government.

No authors declared conflicts of interest.

Some previous papers have also found that people with prior COVID-19 infection had more adverse events following COVID-19 vaccination, including a 2021 paper from French researchers. A U.S. study identified prior COVID-19 as a predictor of the severity of side effects.

Some other studies have determined COVID-19 vaccines confer little or no benefit to people with a history of infection, including those who had received a primary series.

The U.S. Centers for Disease Control and Prevention still recommends people who recovered from COVID-19 receive a COVID-19 vaccine, although a number of other health authorities have stopped recommending the shot for people who have prior COVID-19.

Another New Study

In another new paper, South Korean researchers outlined how they found people were more likely to report certain adverse reactions after COVID-19 vaccination than after receipt of another vaccine.

The reporting of myocarditis, a form of heart inflammation, or pericarditis, a related condition, was nearly 20 times as high among children as the reporting odds following receipt of all other vaccines, the researchers found.

The reporting odds were also much higher for multisystem inflammatory syndrome or Kawasaki disease among adolescent COVID-19 recipients.

Researchers analyzed reports made to VigiBase, which is run by the World Health Organization.

“Based on our results, close monitoring for these rare but serious inflammatory reactions after COVID-19 vaccination among adolescents until definitive causal relationship can be established,” the researchers wrote.

The study was published by the Journal of Korean Medical Science in its March edition.

Limitations include VigiBase receiving reports of problems, with some reports going unconfirmed.

Funding came from the South Korean government. One author reported receiving grants from pharmaceutical companies, including Pfizer.

International

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

{kind=link}

{kind=link}

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

{kind=link}

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

Net Zero, The Digital Panopticon, & The Future Of Food

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Looking Back At COVID’s Authoritarian Regimes

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Health Officials: Man Dies From Bubonic Plague In New Mexico

The SNF Institute for Global Infectious Disease Research announces new advisory board

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A