Uncategorized

Futures Slide As Small Bank Selling Returns

Futures Slide As Small Bank Selling Returns

US index futures retreated as the short squeeze that lifted distressed regional banks fizzled…

Share this:

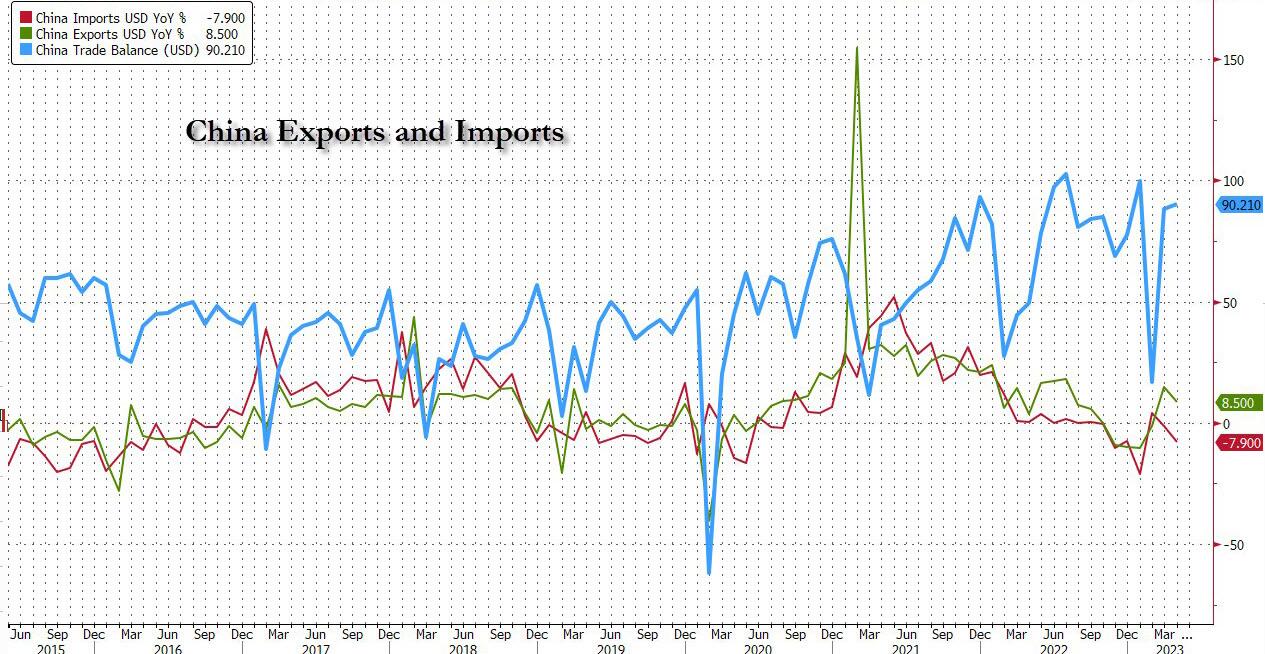

US index futures retreated as the short squeeze that lifted distressed regional banks fizzled and went into reverse, dragging names such as PacWest as much as 20% lower in premarket trading, while the latest Chinese macro data spooked investors after imports dropped much more than expected; lastly investors braced for key US CPI data due tomorrow. Both S&P 500 and Nasdaq 100 contracts slipped 0.4% on Tuesday as of 8:00 a.m. ET. Meanwhile, the dollar is edging higher, set for a second day of muted gains. Oil prices have lost the momentum of the past two sessions, falling back in today’s trading. Gold is set for its third day of gains. Iron ore dropped in the wake of data that showed China’s imports of the steel-making ingredient fell to a 10-month low in April. Copper also slides.

In premarket trading, PacWest shares tumbled as much as 16% in premarket trading Tuesday, set to decline after two days of gains, while other US regional banks were also lower. Lucid Group fell 9.1% in premarket trading after the EV maker’s revenue and expected production disappointed investors. PayPal dropped 4.3% after the payment company warned that its adjusted operating margin won’t grow as quickly as it had anticipated earlier. By contrast, Palantir jumped 19% in premarket after the software firm published a surprise profit and a strong forecast, as well as reporting solid demand for its upcoming artificial intelligence tool. Some other notable premarket movers:

- Skyworks shares fall 9.5% in US premarket trading after the update from the wireless semiconductor company showed continued headwinds for the Android ecosystem, weighing on its margin guidance and overshadowing an otherwise in-line quarterly print.

- Coherus Bio slid 15% in low-volume premarket trading after the biopharma firm’s quarterly results showed a revenue miss driven by weakness at its Udenyca product, with analysts split on the quality of the outlook for the biopharma. Shares were down 8.4% in extended trading Monday.

- Premier’s announcement of a strategic review is not a major surprise, analysts say, given a stagnant share-price and trading performance in recent times. Private equity buyers are seen as the most likely suitors, according to Credit Suisse, while SVB Securities sees significant value in a breakup of the business. Premier shares climbed 7.2% in after-hours trading on the news.

- Shockwave Medical shares topped expectations and showed growth remains strong for the medical-devices company, though its shares will be put under pressure from a report that talks on a potential takeover offer for the firm by Boston Scientific have broken down. The shares declined 4.6% in after- hours trading.

- International Flavors & Fragrances’ first-quarter results are mixed, with sales slightly above expectations but guidance below for the group. Shares fell 1.5% in after-hours trading.

- McKesson’s quarterly earnings were solid but the pharmaceuticals distributor’s guidance is the highlight of its update, coming in well ahead of expectations. Analysts flagged continued growth in key areas for the group and that its guidance indicates it is executing successfully on its strategy. Shares in the group rose around 4% in after-hours trading.

Sentiment was also hit by a report showing a drop in Chinese imports last month, raising concerns about the country’s ability to boost the global economy. Investors also weighed signs that the world’s central banks may need to do more to fight sticky inflation.

Focus is now shifting to the US consumer-prices data due on Wednesday to gauge the interest-rate path, according to Michael Hewson, chief analyst at CMC Markets in London. “The US labor market remains tight and there is still inflationary pressure within the underlying economy,” he said. “For all the expectation that last week’s Federal Reserve rate hike might be the last, the strength of the US economy might mean that there may be one left to come.”

Separately, investors are also tracking efforts in Washington to end a standoff over the US debt ceiling, with President Joe Biden due to sit down with House Speaker Kevin McCarthy Tuesday for their first meeting in three months as the two face pressure to forge a deal. As we discussed previously, this game of chicken is unlikely to be resolved without a market panic first.

“Whilst we expect a last-minute resolution to the US debt-ceiling melodrama, anxiety is now starting to creep into markets,” said John Leiper, chief investment officer at Titan Asset Management.

In Europe, the Stoxx 600 is down 0.6% with the consumer product and energy sectors also underperforming. Real estate stocks are leading the broader market lower in Europe as Swedish landlord SBB slumps after halting its dividend. Here are the biggest European movers:

- SBB slumps as much as 13% to the lowest since April 2018, dragging the European real estate sector lower, after the Swedish landlord halted dividend payments and canceled a SEK2.6 billion rights issue

- Fresenius SE shares gain as much as 7.4% on better-than-expected first quarter that Barclays says was boosted by its medicines and nutritions unit Kabi, as well as its separately listed dialysis unit

- Grifols shares rise as much as 8.5%, the most since Feb. 16., with Jefferies saying the quarterly update from the Spanish blood-plasma firm beat on the top line and issued better margin guidance

- Media stocks top all other Stoxx 600 sectors on Tuesday and buck weakness in the broader market, after Pearson said it’s working to embed generative AI technology across its product lineup

- JD Sports shares rise as much as 3.2% after saying it’s in exclusive talks to buy French chain Courir for an enterprise value of €520m. Analysts say the deal fits with the company’s strategy

- Banco BPM shares rise as much as 6%, with analysts saying the Italian lender’s quarterly results were strong, with the highlights being higher guidance and potentially greater shareholder returns

- Amadeus shares rise as much as 1.7% with the travel IT services provider reported better-than-expected results across three main divisions as air traffic recovered across the globe

- Marshalls slumps as much as 16% after the building materials group says trading this year has been weaker than expected. Analysts point to the weaker environment for housebuilding in 2023

- Daimler Truck falls as much as 4.6% after 1Q results analysts say are consistent and in line with the pre-release last month, with the German truckmaker also confirming 2023 guidance

- Evonik shares decline as much as 2.8% after it posted mixed results in 1Q. Analyst say the firm’s outlook will be a main focus after it said it now sees adjusted FY Ebitda “more likely” at the lower end

- Victrex shares fall as much as 11%, hitting the lowest since April, as analysts said deteriorating volumes for the thermoplastics maker will put pressure on consensus estimates

JPMorgan strategists, who have been permabearish all year after cheering the 2022 collapse all year, are now calling for an end of European stock outperformance. Europe benefited from China’s reopening and a less-severe energy crisis than initially anticipated, but JPMorgan said these tailwinds are showing signs of fading, with economic surprises in the region now turning negative. After euro-zone stocks rose in the past seven months, investors “should be locking in these gains,” strategists led by Mislav Matejka wrote in a note on Tuesday.

Earlier in the session, Asian stocks edged lower as sentiment soured on China’s weak import data, while a recent rally in the nation’s state-owned enterprises fizzled. The MSCI Asia Pacific Index gave up earlier gains to fall as much as 0.2%, led lower by communication shares. Benchmarks in Hong Kong fell the most in two months, while Japanese shares outperformed the region as investors cheered latest corporate earnings. The Topix is approaching its highest level since August 1990. Chinese stocks slid in afternoon trading as a rally in state-owned firms reversed, dragging on the broader market. Meanwhile, fresh data showed imports slumped in April while export growth slowed, adding to pressures on an economic recovery that’s already been called into question.

“The imports miss could signal that Chinese household consumption still has a way to go,” said David Chao,global market strategist for Asia Pacific at Invesco Asset Management, adding that Chinese households are “not ready to pry open their purse strings to buy discretionary goods and products.” The reopening rally in China has stalled in recent months due to a lack of fresh catalysts. Still, market conditions are favorable for the country’s equities, said William Fong, head of Hong Kong China equities at Baring Asset Management Asia. “Recovering consumption and supportive government policies are driving improvement in Chinese corporate fundamentals.” Investors will be watching the US inflation data due Wednesday for more clues on the Federal Reserve’s next moves. A decline in the inflation reading and the recent banking turmoil have fueled expectations that the Fed will soon halt its monetary tightening or even begin cutting interest rates.

Japanese stocks rose as investors applauded results from major local firms and awaited key US inflation data. The Topix rose 1.3% to close at 2,097.55, while the Nikkei advanced 1% to 29,242.82. Steelmakers and trading houses were the biggest advancing industry groups after reports from companies including JFE and Sumitomo Corp. Toyota Motor contributed the most to the Topix gain, increasing 3.3%. Out of 2,160 stocks in the index, 1,720 rose and 360 fell, while 80 were unchanged. “US earnings and employment data were strong, and if monetary tightening continues, the dollar will strengthen and the yen will weaken, which is positive for Japanese equities.” said Tetsuo Seshimo, a portfolio manager at Saison Asset Management. “The market had low expectations for Japanese earnings, so the solid results should also be viewed positively.”

Stocks in India failed to hold initial gains and closed nearly flat, with banks among worst performers on profit-taking by investors. The S&P BSE Sensex was little changed at 61,761.33 in Mumbai, while the NSE Nifty 50 Index was flat at 18,265.95. The gauges surged more than 1% each on Monday, their biggest rally since March and are trading close to their highest levels since mid-December. India VIX, a gauge of volatility, has risen for three straight sessions through Tuesday amid selling in some sectors including banks after some lenders reported higher provisions for the March quarter. Out of 28 companies in the Nifty 50 guage that have so far reported quarterly earnings, 15 have either met or beaten consensus earnings estimates, while 10 have trailed. Construction major L&T and generic drug maker Dr Reddy’s will be reporting earnings on Wednesday.

In FX, the Bloomberg Dollar Spot Index inches up 0.1%; weakness in most global share markets spur light demand for the haven currency. The Norwegian krone is the weakest of the G-10 currencies while the Japanese yen is the strongest. Traders are also weighing “the outlook for interest rates alongside debt ceiling talks,” Jeff Ng, a senior currency analyst at MUFG Bank in Singapore, wrote in a note. “We anticipate more FX moves against the US dollar to materialize” as the US releases CPI numbers Wednesday, which may indicate that inflation stayed sticky. Investors are also bracing for US CPI figures due on Wednesday, as an expected steadying or slowdown in prices could bolster the view that Fed rate rises have ended after last week’s hike; further evidence of this could weigh on the dollar, strategists say. “While the short-term outlook for the dollar remains neutral in our view, thanks to positioning skewed to the short-side and unstable risk sentiment, markets remain ready to price in more Fed rate cuts, so downside risks are non- negligible,” ING strategists write in a note

In rates, Treasuries are slightly richer across the curve, erasing some of Monday’s losses, as stock futures retreat from Monday’s highs. Treasury yields richer by 2bp to 3bp across the curve with spreads slightly steeper, although broadly within a basis point of Monday’s closing levels; 10-year yields around 3.485%, richer by 2bp on the day with bunds lagging by 1.5bp in the sector; the two-year Treasury yield slips 2bps to 3.98%, pulling back form 4.01% hit on Monday, its highest in a week. Sentiment weakened slightly during Asia session when Chinese import data showed a steep drop. Focal points of US session include 3-year note auction, with critical April CPI data ahead Wednesday. Treasury auctions cycle begins with $40b 3-year note sale at 1pm, followed by 10- and 30-year sales Wednesday and Thursday. WI 3-year yield at ~3.655% is 15.5bp richer than April’s result, which stopped on the screws. In Europe, Bunds are little changed while Gilts have dropped, pushing UK 10-year yields up 4bps to 3.83% ahead of the Bank of England rate decision on Thursday.

In commodities, crude futures decline with WTI falling 0.8% to trade near $72.60. Spot gold adds 0.3% to around $2,027.

Bitcoin is essentially unchanged within sub-USD 300 parameters and holding just above the USD 27.5k mark.

Looking at the day ahead, in the US we will get NFIB small business optimism, which will dovetail nicely with the SLOOS data that was released yesterday. Additionally, there is France’s March trade balance. From Central Banks, market participants will hear from the Fed’s Williams and Jefferson, as well as the ECB's Lane, Vasle and Rehn. Lastly, while we are in the back-nine of earnings season there will be interest in reports from Saudi Aramco, Airbnb, Nintendo, Mitsubishi, Apollo, Electronic Arts, Daimler, and Wynn Resorts today.

Market Snapshot

- S&P 500 futures down 0.4% to 4,137.50

- STOXX Europe 600 down 0.5% to 464.49

- MXAP down 0.2% to 162.34

- MXAPJ down 0.9% to 517.13

- Nikkei up 1.0% to 29,242.82

- Topix up 1.3% to 2,097.55

- Hang Seng Index down 2.1% to 19,867.58

- Shanghai Composite down 1.1% to 3,357.67

- Sensex down 0.1% to 61,688.29

- Australia S&P/ASX 200 down 0.2% to 7,264.08

- Kospi down 0.1% to 2,510.06

- German 10Y yield little changed at 2.31%

- Euro down 0.2% to $1.0977

- Brent Futures down 1.2% to $76.07/bbl

- Gold spot up 0.1% to $2,023.51

- U.S. Dollar Index up 0.16% to 101.54

Top overnight news

- China exports rise 8.5% Y/Y in April, above the Street’s +8% forecast, while imports sink 7.9% (significantly worse than the -0.2% consensus forecast). BBG

- UBS appointed Ulrich Koerner to its top management body, giving the CEO of Credit Suisse a key role in overseeing the combination of the two firms. The announcement was part of a broader management shuffle that also saw Todd Tuckner, a veteran UBS banker, take over as CFO from Sarah Youngwood, who only joined the bank last year. BBG

- Sweden's Riksbank announced a half percentage-point hike to 3.50% on April 26 and said it would probably tighten policy again, by a quarter point this time, in either June or September before the hiking cycle comes to an end. RTRS

- Investors shouldn’t count on the ECB’s unprecedented bout of interest-rate increases ending in July, as the majority of economists currently predicts, according to Governing Council member Martins Kazaks. “I don’t think it is that clear yet,” the hawkish Latvian official told Bloomberg on Monday by phone. “We still have quite some ground to cover and further rate increases will be necessary to tame inflation.” BBG

- Americans have low confidence in Biden, Powell and Yellen on the economy according to a new Gallup poll (Biden’s economic polling numbers are nearly as low as they were for George W Bush during the heart of the ’08 financial crisis). CNN

- Treasury Secretary Janet Yellen is reaching out to U.S. business and financial leaders to explain the "catastrophic" impact a U.S. default on its debt would have on the U.S. and global economies. RTRS

- US lenders warned that commercial property is ‘next shoe to drop’. Executives and investors fret about impact of rising rates and empty buildings on $5.6tn market. FT

- Fed steps up scrutiny of CRE risks at banks (“the Federal Reserve has increased monitoring of the performance of CRE loans and expanded examination procedures for banks with significant CRE concentration risk”). Fed

- AMZN is offering certain Prime customers cash payments if they pick up their packages at various locations (including Whole Foods) instead of having them delivered to their home. RTRS

- Stocks and bonds moved in lockstep for much of 2022, but that relationship has flipped this year. The two asset classes now display the largest negative correlation since August 2020...(WSJ)

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed following the indecisive performance from Wall St where the focus was on the Fed’s SLOOS which showed banks tightened credit terms and demand for loans declined, while the attention in the region shifted to earnings and data releases including mixed Chinese trade figures. ASX 200 was lower with early pressure seen across nearly all sectors and with the top-weighted financial industry choppy after earnings from Australia’s largest lender CBA which reported a slight increase in Q3 cash profit although NII was lower compared to the quarterly average in H1 and the Co. also noted that many customers are feeling the strain of higher interest rates and rising living costs. Nikkei 225 outperformed and reclaimed the 29,000 status, with the index unfazed by weak household spending data as participants digested earnings. Hang Seng and Shanghai Comp. were varied after the latest Chinese trade figures which showed stronger-than-expected export growth but imports disappointed with a surprise contraction.

Top Asian News

- EU Ambassador to China thinks the comment by EU's Borrell suggesting that EU navies patrol the Taiwan Strait has been grossly exaggerated, while he also commented regarding China's anti-espionage law and consultancy crackdown in which he stated that this is not good news and expressed doubts regarding the compatibility of this policy with the opening up of China's economy.

- Chinese embassy said China strongly condemns and firmly opposes Canada's decision to expel the Chinese diplomat and has lodged a protest with the Canadian government. China also claimed that Canada 'sabotaged' relations and vowed 'resolute countermeasures'. Subsequently, China said it will expel a Canadian diplomat as a countermeasure.

- BoJ Governor Ueda said their scheduled review won't have any pre-set idea in mind on specific monetary policy moves and said they will take necessary policy action at each meeting with an eye on financial and price developments even while conducting the review. Ueda also commented that if the price target is met in a sustainable manner, the BoJ will end YCC and then shrink its balance sheet, while he added they are seeing some bright signs including on inflation expectations which have heightened and remain at elevated levels.

- Australian Budget: Government forecasts 2022/23 budget surplus of AUD 4.2bln (exp. AUD 4bln), 2023/24 budget deficit at AUD 13.9bln (0.5% of GDP), 2024/25 budget AUD 35.1bln (1.3% of GDP). Click here for more detail.

European bourses are softer across the board, Euro Stoxx 50 -0.7%, as the region struggles to find a foothold in relatively quiet trade after a mixed APAC handover. Sectors are similarly softer with Real Estate lagging after soft Halifax data and SBB headwinds; individual movers dictated by earnings updates for Fresenius, Daimler Trucks & more. ES -0.4% dips with the region again lacking firm direction ahead of Fed speak and Biden's debt ceiling meeting; NQ and RTY roughly in-fitting.

Top European News

- ECB's Kazaks says rate hiking may not be finished in July, via Bloomberg; bets on Spring 2024 ECB cuts are significantly premature. Doing too little remains the greater danger. Not impossible for the ECB to hike/pause in the scenario the Fed is cutting.

- ECB's Kazimir says based on current data, will need to keep raising rates for longer than anticipated; September projections are the earliest time to gauge the effectiveness of measures and see if inflation is heading to target.

- Norges Bank Governor Bache says does not need additional policy tools, FX interventions to influence NOK are costly and not very efficient.

- German Chancellor Schloz says the EU must reduce risks in China relations without cutting ties saying this is not decoupling, but smart de-risking is the way forward with China.

- UK Barclaycard April consumer spending rose 4.3% Y/Y but was impacted by inflation squeeze on disposable incomes and higher food prices, according to Reuters.

FX

- Buck finds its feet vs most majors bar the Yen as Treasury yields ease off Monday's peaks and BoJ Governor Ueda notes higher Japanese inflation expectations.

- DXY forms a firmer base around 101.500 and USD/JPY pivots 135.00 where 1bln option expiries roll off at the NY cut.

- Aussie retreats as Chinese imports unexpectedly tumble and AUD/USD eyes support into 0.6750 from Monday's high just over 0.6800.

- Euro loses 1.1000+ status vs Dollar and Fib support against Pound as Cable retains underlying bid mostly above 1.2600.

- PBoC set USD/CNY mid-point at 6.9255 vs exp. 6.9251 (prev. 6.9158)

- Turkey raises the wages of some civil servants by 45%, according to Turkish President Erdogan.

Fixed Income

- Choppy trade in bonds, but Bunds piggy-back bounce in Bobls after super-strong 5 year German auction, both holding near intraday highs within 118.34-06 and 135.90-33 ranges.

- Gilts lag in catch-up trade after long UK weekend between 100.85-43 parameters.

- US Treasuries regroup after Monday's slump amidst a decline in NFIB business optimism and awaiting Fed commentary ahead of latest debt ceiling talks, T-note near 115-15+ peak vs 115-06+ trough.

Commodities

- WTI and Brent are back on a modest downward trajectory after recent positive sessions and yesterday's Alberta-driven upside; currently, the benchmarks are circa. USD 0.80/bbl lower.

- Newsflow has been focused on UAE remarks and Aramco's update after Chinese trade data was mixed with an unexpected contraction in imports potentially a signal towards weaker demand and a headwind for the complex.

- Saudi Aramco Q1 - Saw lower crude oil prices. Major investments advance strategic downstream expansion in key global markets. Global downstream strategy is gaining momentum. 99.7% supply reliability. Believe oil and gas will remain critical components of the energy mix for the foreseeable future. Moving forward with the capacity expansion and long-term outlook remains unchanged.. "Based on the government budget figures the Saudi Government 2023 budgeted revenues are likely based on Brent of ~USD 81/bbl", according to Al Rajhi Bank cited by Energy Intel's Bakr.

- Spot gold remains underpinned around the USD 2025/oz mark and surrounded by resistance/support marks in relatively close proximity. Base metals are broadly softer, given the mentioned Chinese trade data.

Geopolitics

- Head of Russian Wagner Group Prigozhin said that they have not received the promised ammunition after earlier stating that shipments were preliminarily sent, according to Reuters.

- US is to provide USD 1.2bln more in long-term military aid to Ukraine to further bolster its air defences, according to US officials cited by AP.

- UK Foreign Secretary Cleverly is visiting the US and will hold talks with US Secretary of State Blinken on Tuesday to discuss support for Ukraine, according to Sky News.

- US State Department said the US Ambassador to China told Chinese Foreign Minister Qin that there has been no change to US one-China policy, while US Secretary of State Blinken would like to visit China and intends to go when conditions allow.

US Event Calendar

- 06:00: April SMALL BUSINESS OPTIMISM, 89.0, est. 89.7, prior 90.1

- 08:30: Fed’s Jefferson Speaks to Atlanta Black Chamber

- 12:05: Fed’s Williams Speaks to Economic Club of New York

DB's Jim Reid concludes the overnight wrap

We're back from the King's Coronation holiday today. I've had more quiche since I last sent the EMR than I've had in the previous decade. The weather over the three day weekend was in order; awful, quite nice, awful. Thankfully the big street party was on the sunny day. I'm looking forward to leaving the rain (and the leftover quiche) behind for a couple of days as I escape to Spain. DB is hosting a morning macro outlook event in our Madrid offices tomorrow, with a selection of research speakers, so please reach out to your DB sales coverage if you'd like to attend.

So London returns back to work today between the hotly anticipated US senior loan officers' opinion survey (SLOOS) last night and US CPI tomorrow.

On the former, the headline numbers were weak but maybe not as bad as feared, but there were plenty of weakness in the report regardless. The headliner saw the net percentage of banks tightening lending standards on commercial and industrial (C&I) loans to medium/large businesses rise to 46% from 44.8% in Q4, and for small banks 46.7% from 44.8%. The medium/large businesses number is still below the peaks observed during the pandemic, GFC, early-2000s and early 1990s but is in recessionary territory. Meanwhile, the percentage of banks reporting stronger demand for C&I loans dropped to 55.6% in Q1 - the lowest level since 2009. Even as demand is lower, the willingness of banks to lend continues to fall. This dynamic was more apparent at smaller lenders, as one would expect.

There was a relatively muted market response to the SLOOS data, as the results were broadly in-line with expectations, or as a minimum didn't bring any additional fear to the market. US 10yr Treasury yields were already around +6bps higher before the report and finished the day just off their highs to close +7.0bps higher at 3.507%. This morning in Asia, 10yr yields (-1.15bps) are slightly down as we go to press. 2yr yields similarly closed just off their highs, up +8.7bps on the day at 4.001% (-2bps in Asia). The rate selloff came despite minimal movements in Fed pricing. The chance of a rate cut in July fell from 40% to just under 37%, while fed futures are still implying two full 25bp rate cuts by year-end and a better-than-not chance of a third 25bp cut.

The SLOOS survey was followed by the Fed’s Financial Stability Report, which comes following the collapse of 3 of the 4 largest bank failures in US history in the last 2 months. The Fed remains concerned that worries about “the economic outlook, credit quality, and funding liquidity could lead banks and other financial institutions to further contract the supply of credit to the economy.” This would directly raise the cost of funding and potentially result in a meaningful slowdown in the broader economy. In terms of specific risks, the Fed pointed to high property valuations despite weakening fundamentals, high levels of business debt, and funding risks due to banks holding high amounts of AFS and HTM securities. They note that financial leverage is not in poor shape, saying “high levels of capital and moderate interest rate risk exposures mean that a large majority of banks are resilient to potential strains from higher interest rates.”

Treasury Secretary Yellen last night appeared on CNBC calling for congress to raise the Debt Ceiling, announcing that the Treasury could “run out of cash” as soon as June 1. This comes ahead of today’s meeting between the White House and Congressional leadership where they are expected to discuss a path forward. On the banking sector, Secretary Yellen noted that the system remains well capitalized but that the regulators are “ready to use tools if bank pressures arise”. She also did not rule out the possibility of a recession, but argued it is not the most likely path.

The US banking sector saw a slight pullback yesterday after Friday’s strong rally in US regional banks following reports that the FDIC is set to exempt smaller US banks from contributing to the deposit insurance fund. The KBW bank index was down -0.26%, but embattled regionals such as Western Alliance (+0.59%), PacWest (+3.65%), and Zion (+2.10%) were able to finish higher on the day. PacWest was up nearly +30% at the open though, highlighting the whipsawing price action. More broadly, the S&P 500 was just better than flat (+0.05%) as cyclicals such as media (+1.45%) and autos (+0.95%) outperformed at the expense of bond-proxies and defensives like REITs (-0.65%), software (-0.48%), utilities (-0.32%), and food & beverage (-0.38%).

While the UK was out, the STOXX 600 (+0.35%) rose to a 2-week high on the back of cyclicals such as travel & leisure (+0.75%), banks (+0.75%) and retail (+0.56%), while defensives fell back slightly. 10yr yields also rose moderately, with those on bunds (+2.8bps), OATs (+3.0bps) and BTPs (+4.9bps) all closing higher.

The drop in commodity prices over the spring has been a positive for consumer inflation, however that trend has reversed over the past few sessions with commodity prices jumping again yesterday after closing last week rather strong. Indeed, Brent crude rose +2.27% to close at $77.01/bbl, after reaching a 16-month low last Wednesday. It was a similar story for European natural gas prices (+0.82%), which is now just over 3% higher than its recent 20-month lows of €35.65/MWh.

US inflation data is in focus this week with CPI tomorrow, followed by PPI (Thursday) and the University of Michigan survey (Friday). In terms of CPI, our US economists expect headline and core to come in at +0.3% m/m (vs +0.1% and +0.4% in March, respectively). For PPI, they are expecting a +0.3% core rise as well and a -0.5% headline contraction, due to falling energy prices. Lastly on the Michigan survey they are forecasting a 62.0 reading vs 63.5 for the sentiment gauge. The inflation expectations component both 1yr and 5-10 years especially will be in the spotlight.

Outside of the US inflation data, there will be a good deal of interest surrounding the Bank of England policy decision on Thursday. Our UK economist (see preview here) expects the central bank to deliver a +25bps hike, leaving the Bank Rate at 4.5%, and while they do not anticipate any major changes to forward guidance they acknowledge there is a risk that the MPC leans dovish. Further out, they expect a final +25bps hike in June, while underscoring upside risks to their terminal view. After the meeting, UK GDP Q1 will be out on Friday showing how the economy has fared through the winter.

Asian equity markets are mixed this morning with the Hang Seng (-0.52%) and the KOSPI (-0.51%) lower, whilst the Nikkei (+0.77%), the CSI (+0.42%) and the Shanghai Composite (+0.36%) are bucking the trend. In overnight trading, US stock futures are printing mild losses with those on the S&P 500 (-0.05%) and NASDAQ 100 (-0.10%) slightly lower.

Early morning data showed that China’s exports (USD) recorded a second straight month of growth, advancing +8.5% y/y in April (v/s +8.0% expected), compared with an increase of +14.8% while imports (-7.9% y/y) contracted sharply in April, higher than the market expected decline of -0.2% and compared to prior month’s drop of -1.4% indicating that domestic demand remains tepid. Elsewhere, household spending in Japan unexpectedly fell -1.9% y/y in March, notching its biggest decline since March 2022 asagainst a Bloomberg consensus forecast for a +0.4% rise and following a +1.6% gain in February. Separately data showed that real wages declined for the 12th consecutive month, dropping -2.9% y/y in March (v/s -2.4% expected) as persistent inflation works through the system.

Now looking at the day ahead, in the US we will get NFIB small business optimism, which will dovetail nicely with the SLOOS data that was released yesterday. Additionally, there is France’s March trade balance. From Central Banks, market participants will hear from the Fed’s Williams and Jefferson, as well as the ECB's Lane, Vasle and Rehn. Lastly, while we are in the back-nine of earnings season there will be interest in reports from Saudi Aramco, Airbnb, Nintendo, Mitsubishi, Apollo, Electronic Arts, Daimler, and Wynn Resorts today.

Uncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Uncategorized

Economic Earthquake Ahead? The Cracks Are Spreading Fast

Economic Earthquake Ahead? The Cracks Are Spreading Fast

Authored by Brandon Smith via Alt-Market.us,

One of my favorite false narratives…

Share this:

{kind=link}

{kind=link}

Authored by Brandon Smith via Alt-Market.us,

One of my favorite false narratives floating around corporate media platforms has been the argument that the American people “just don’t seem to understand how good the economy really is right now.” If only they would look at the stats, they would realize that we are in the middle of a financial renaissance, right? It must be that people have been brainwashed by negative press from conservative sources…

{kind=link}

I have to laugh at this notion because it’s a very common one throughout history – it’s an assertion made by almost every single political regime right before a major collapse. These people always say the same things, and when you study economics as long as I have you can’t help but throw up your hands and marvel at their dedication to the propaganda.

One example that comes to mind immediately is the delusional optimism of the “roaring” 1920s and the lead up to the Great Depression. At the time around 60% of the U.S. population was living in poverty conditions (according to the metrics of the decade) earning less than $2000 a year. However, in the years after WWI ravaged Europe, America’s economic power was considered unrivaled.

The 1920s was an era of mass production and rampant consumerism but it was all fueled by easy access to debt, a condition which had not really existed before in America. It was this illusion of prosperity created by the unchecked application of credit that eventually led to the massive stock market bubble and the crash of 1929. This implosion, along with the Federal Reserve’s policy of raising interest rates into economic weakness, created a black hole in the U.S. financial system for over a decade.

There are two primary tools that various failing regimes will often use to distort the true conditions of the economy: Debt and inflation. In the case of America today, we are experiencing BOTH problems simultaneously and this has made certain economic indicators appear healthy when they are, in fact, highly unstable. The average American knows this is the case because they see the effects everyday. They see the damage to their wallets, to their buying power, in the jobs market and in their quality of life. This is why public faith in the economy has been stuck in the dregs since 2021.

The establishment can flash out-of-context stats in people’s faces, but they can’t force the populace to see a recovery that simply does not exist. Let’s go through a short list of the most faulty indicators and the real reasons why the fiscal picture is not a rosy as the media would like us to believe…

The “miracle” labor market recovery

In the case of the U.S. labor market, we have a clear example of distortion through inflation. The $8 trillion+ dropped on the economy in the first 18 months of the pandemic response sent the system over the edge into stagflation land. Helicopter money has a habit of doing two things very well: Blowing up a bubble in stock markets and blowing up a bubble in retail. Hence, the massive rush by Americans to go out and buy, followed by the sudden labor shortage and the race to hire (mostly for low wage part-time jobs).

The problem with this “miracle” is that inflation leads to price explosions, which we have already experienced. The average American is spending around 30% more for goods, services and housing compared to what they were spending in 2020. This is what happens when you have too much money chasing too few goods and limited production.

The jobs market looks great on paper, but the majority of jobs generated in the past few years are jobs that returned after the covid lockdowns ended. The rest are jobs created through monetary stimulus and the artificial retail rush. Part time low wage service sector jobs are not going to keep the country rolling for very long in a stagflation environment. The question is, what happens now that the stimulus punch bowl has been removed?

Just as we witnessed in the 1920s, Americans have turned to debt to make up for higher prices and stagnant wages by maxing out their credit cards. With the central bank keeping interest rates high, the credit safety net will soon falter. This condition also goes for businesses; the same businesses that will jump headlong into mass layoffs when they realize the party is over. It happened during the Great Depression and it will happen again today.

Cracks in the foundation

We saw cracks in the narrative of the financial structure in 2023 with the banking crisis, and without the Federal Reserve backstop policy many more small and medium banks would have dropped dead. The weakness of U.S. banks is offset by the relative strength of the U.S. dollar, which lures in foreign investors hoping to protect their wealth using dollar denominated assets.

But something is amiss. Gold and bitcoin have rocketed higher along with economically sensitive assets and the dollar. This is the opposite of what’s supposed to happen. Gold and BTC are supposed to be hedges against a weak dollar and a weak economy, right? If global faith in the dollar and in the U.S. economy is so high, why are investors diving into protective assets like gold?

Again, as noted above, inflation distorts everything.

Tens of trillions of extra dollars printed by the Fed are floating around and it’s no surprise that much of that cash is flooding into the economy which simply pushes higher right along with prices on the shelf. But, gold and bitcoin are telling us a more honest story about what’s really happening.

Right now, the U.S. government is adding around $600 billion per month to the national debt as the Fed holds rates higher to fight inflation. This debt is going to crush America’s financial standing for global investors who will eventually ask HOW the U.S. is going to handle that growing millstone? As I predicted years ago, the Fed has created a perfect Catch-22 scenario in which the U.S. must either return to rampant inflation, or, face a debt crisis. In either case, U.S. dollar-denominated assets will lose their appeal and their prices will plummet.

“Healthy” GDP is a complete farce

GDP is the most common out-of-context stat used by governments to convince the citizenry that all is well. It is yet another stat that is entirely manipulated by inflation. It is also manipulated by the way in which modern governments define “economic activity.”

GDP is primarily driven by spending. Meaning, the higher inflation goes, the higher prices go, and the higher GDP climbs (to a point). Eventually prices go too high, credit cards tap out and spending ceases. But, for a short time inflation makes GDP (as well as retail sales) look good.

Another factor that creates a bubble is the fact that government spending is actually included in the calculation of GDP. That’s right, every dollar of your tax money that the government wastes helps the establishment by propping up GDP numbers. This is why government spending increases will never stop – It’s too valuable for them to spend as a way to make the economy appear healthier than it is.

The REAL economy is eclipsing the fake economy

The bottom line is that Americans used to be able to ignore the warning signs because their bank accounts were not being directly affected. This is over. Now, every person in the country is dealing with a massive decline in buying power and higher prices across the board on everything – from food and fuel to housing and financial assets alike. Even the wealthy are seeing a compression to their profit and many are struggling to keep their businesses in the black.

The unfortunate truth is that the elections of 2024 will probably be the turning point at which the whole edifice comes tumbling down. Even if the public votes for change, the system is already broken and cannot be repaired without a complete overhaul.

We have consistently avoided taking our medicine and our disease has gotten worse and worse.

People have lost faith in the economy because they have not faced this kind of uncertainty since the 1930s. Even the stagflation crisis of the 1970s will likely pale in comparison to what is about to happen. On the bright side, at least a large number of Americans are aware of the threat, as opposed to the 1920s when the vast majority of people were utterly conned by the government, the banks and the media into thinking all was well. Knowing is the first step to preparing.

The second step is securing your own financial future – that’s where physical precious metals can play a role. Diversifying your savings with inflation-resistant, uninflatable assets whose intrinsic value doesn’t rely on a counterparty’s promise to pay adds resilience to your savings. That’s the main reason physical gold and silver have been the safe haven store-of-value assets of choice for centuries (among both the elite and the everyday citizen).

* * *

As the world moves away from dollars and toward Central Bank Digital Currencies (CBDCs), is your 401(k) or IRA really safe? A smart and conservative move is to diversify into a physical gold IRA. That way your savings will be in something solid and enduring. Get your FREE info kit on Gold IRAs from Birch Gold Group. No strings attached, just peace of mind. Click here to secure your future today.

Wendy’s has a new deal for daylight savings time haters

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Wealth Inequality by Age in the Post‑Pandemic Era

These Are The 5 Charts The FDIC Does Not Want You Paying Attention To

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

Mortgage rates fall as labor market normalizes

People Who Received Ivermectin Were Better Off, Study Finds

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International23 hours ago

International23 hours agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges