Uncategorized

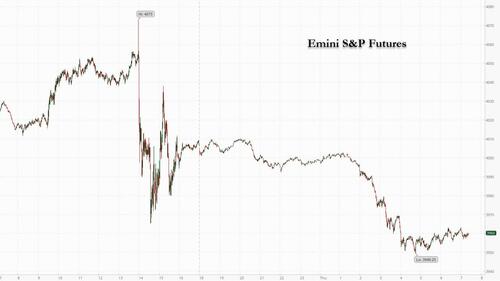

Futures Slide As Hawkish Fed Halts Global Risk Rally

Futures Slide As Hawkish Fed Halts Global Risk Rally

US futures extended declines on Thursday following hawkish signs from the Federal Reserve…

Share this:

US futures extended declines on Thursday following hawkish signs from the Federal Reserve that it would keep rates higher for longer even as it pushed the US economy into a stagflationary recession. Contracts on the technology heavy Nasdaq 100 were down 1.3% by 7:45 a.m. in New York, while S&P 500 futures fell 0.9% after dropping as much as 1.1% earlier. Both underlying indexes dropped yesterday after Fed Chair Jerome Powell delivered a 50-basis-point rate hike, as expected, and said the central bank had more work to do - and will push the terminal rate to 5.1% or higher - in taming inflation despite ebbing price pressures and mounting fears of job losses.

Demand for haven assets sent the dollar and Swiss franc higher amid a wave of rate hikes from Taiwan to Norway. Britain’s pound extended losses after an expected half-point rate hike by the Bank of England, while the euro fell before the European Central Bank’s decision.

A global rally sparked by softer-than-forecast US inflation came to a sudden end on Wednesday after policymakers signaled a peak rate that was far above market expectations and sought to dispel hopes for a rate cut next year. Chair Jerome Powell reaffirmed the central bank won’t back away from its fight against inflation despite mounting fears of job losses and a recession.

“The Fed was more hawkish than markets had expected,” Jack McIntyre, a money manager at Brandywine Global Investment Management, wrote in a note. “They seemingly still want financial markets to tighten further, which essentially means they want lower equity prices.”

Ronald Temple, chief market strategist at Lazard Asset Management, said that although the Fed has started to slow the pace of rate hikes, “that doesn’t mean smooth sailing ahead” for markets. “The effects of the tightening in 2022 will continue to be felt in 2023 through a weaker labor market, recession in Europe and potentially a recession in the US. The earnings hit from a recession is not priced into equity markets,” he said. And while prevailing post-FOMC sentiment among the skeleton crew of traders on Thursday was grim, Paul Kim, chief executive officer at Simplify ETFs, said a “vacuum of catalysts until the next Fed meeting in February” could also help markets continue their rebound over the next few weeks.

The Swiss franc held its gain after the nation’s central bank doubled the policy rate to 1% as forecast. China’s yuan fell as poor economic data and a surge in Covid cases weighed.

In premarket trading Tesla slumped again after CEO Elon Musk sold shares for the fourth time this year. Musk sold almost 22 million shares for $3.58 billion, according to filing late Wednesday. Bitcoin miner Core Scientific surged after one of its largest creditors B. Riley Financial issued an open letter Wednesday laying out a proposal for the company to avoid bankruptcy. Here are some other notable premarket movers:

- Novavax shares drop 10% after the biotechnology firm offered $125m of shares and $125m of convertible bonds, and said its agreement to supply Covid vaccines to the UK had been halved.

- Verizon stock rises 0.6% as Morgan Stanley upgrades it to overweight and downgrades AT&T (T US) to equal-weight, saying in a note that North American telecom services sector faces a balanced outlook heading into next year.

- Keep an eye on Nvidia as it was initiated with a reduce recommendation at HSBC, which says the near-term chip inventory correction and demand uncertainty will overshadow the company’s potential in autos and artificial intelligence segments.

- Watch Madison Square Garden Entertainment as Morgan Stanley upgrades the stock to equal-weight based on recent underperformance and proposed spin of traditional live entertainment business.

- Defense stocks may be in focus after Morgan Stanley upgraded L3Harris (LHX US) to overweight, downgraded Lockheed Martin to equal-weight and maintained overweight and top pick status on Northrop Grumman (NOC US).

Across the Atlantic, investors were gearing up for another day of central bank meetings with the European Central Bank set to announce its rate decisions later on Thursday. Europe’s equity benchmark, the Stoxx 600, fell the most since Oct. 7 on a closing basis; the Stoxx 50 slumped 1.3%. FTSE 100 outperforms peers, dropping 0.5% ahead of a decision by the ECB which hiked rates by 50bps, to the highest since 2008; the BOE is also on deck. Consumer products, tech and retailers are the worst performing sectors. Here are some of the most notable European movers:

- Juventus shares gain as much as 8.1% in Milan to lead gains on the FTSE Italia All-Share Index. Equita notes a report saying that Exor would be thinking of a delisting of the football club, adding that it doesn’t rule out this “could be a viable option.”

- Ackermans & van Haaren rises as much as 4.2% after Kepler Cheuvreux analyst Andre Mulder raised the recommendation to buy from hold.

- Zotefoams climbs as much as 7.7% after the UK foam-maker said pretax profit for 2022 is likely to come in ahead of market expectations.

- European luxury stocks underperform as new economic data from China disappointed and Bryan Garnier cut its price target for Kering on an expected double-digit drop in fourth-quarter sales for key brand Gucci. Kering falls as much as 5.6%, LVMH as much as 2.4%

- H&M drops as much as 4.7% after the apparel retailer reported quarterly sales which analysts said were in line with expectations, noting the lack of margin commentary. Focus has shifted to next month’s results, when there’ll be more clarity on margins.

- Currys falls as much as 10% to the lowest since Oct. 13 after the UK electronics retailer cut its profit guidance for the year. The stock may see further short-term pressure, according to Liberum, which lowered its price target.

- Ceconomy sinks as much as 11%, most since July, after the electronics retailer’s earnings. Analysts flag a vague outlook and potential margin pressure.

Earlier in the session, Asian stocks declined as the Federal Reserve signaled higher interest rates, while a disappointing set of economic data from China soured sentiment. The MSCI Asia Pacific Index dropped as much as 1.4%, led by consumer discretionary and technology shares. Most markets in the region were in the red, with Hong Kong and South Korea among the worst performers. A surprisingly hawkish tone by the Fed after an expected half-point hike fueled risk-off mood across Asia. Chair Jerome Powell said the Fed had a “ways to go” in its campaign to rein in inflation. Policymakers projected rates would end next year at 5.1%, higher than previously indicated.

Chinese benchmarks fell, with Hong Kong’s Hang Seng Index dropping more than 1%, as the nation’s economic activity worsened in November. There will likely be more disruption to growth as infections surge after the government abruptly dropped its Zero-Covid policy. “A broad-based miss in activity data could be attributed to the pre-Zero-Covid relaxation days, but challenges lie ahead as well with full reopening likely to be delayed by a large chunk of workers calling in sick as infections spread,” said Charu Chanana, market strategist at Saxo Capital Markets. The Asian stock benchmark may halt a six-week gaining streak if losses extend into Friday. The region’s shares had rallied since November following China’s Covid pivot and amid hopes of a more dovish Fed — with the latter getting a rude awakening from Wednesday’s meeting.

Japanese stocks followed US shares lower after the Federal Reserve signaled interest rates will climb higher than anticipated next year. The Topix Index fell 0.2% to 1,973.90 as of the market close in Tokyo, while the Nikkei declined 0.4% to 28,051.70. Keyence Corp. contributed the most to the Topix Index decline, decreasing 1.8%. Out of 2,163 stocks in the index, 1,082 rose and 935 fell, while 146 were unchanged. “Although it was hawkish, in a sense the content of the press conference gave the impression of a flexible stance,” said Hitoshi Asaoka, strategist at Asset Management One. “They would look to inflation data rather than just raising interest rates as they have done in the past.”

In FX, Bloomberg dollar spot index rose by as much as 0.7% as the greenback advanced versus all of its Group-of-10 peers. Risk- sensitive Antipodean and Scandinavian currencies were the worst performers.

- The euro fell for the first day in three but held above the $1.06 handle. Bunds twist-flattened while Italian bonds bear flattened as money markets added somewhat to ECB peak-rate wagers after the Fed’s policy tightening yesterday

- Norway’s krone held losses against the dollar and the euro after Norges Bank raised the deposit rate to 2.75%, in line with estimates, and kept its rate projection steady for next year

- The Swiss franc swung to a loss against the dollar after the SNB hiked its interest rate by 50bps, to 1%, matching the median estimate

- The pound slid amid broad-based dollar strength. The BOE hiked by the expected half-point; cable was generally flat after the decision.

- Australian dollar declined amid poor Chinese data that showed economic activity worsened in November before the government abruptly dropped its Covid Zero policy. Bonds fell after data showed the economy added 64,000 roles, trumping a forecast 19,000 gain

- New Zealand’s 10-year yield surged after GDP expanded more than twice as much as expected

- Japan’s bonds fell after a 20-year debt auction met tepid investor demand. The yen weakened amid broad strength in the dollar

In rates, all 2s10s yield curves flatten as Treasury yields rose, led by the belly, with the exception of the 30-year segment. Bund curve bull flattens with 2s10s narrowing 3.2bps. Peripheral spreads widen to Germany with 10y BTP/Bund adding 3.0bps to 195.2bps. Elsewhere, Bank of England hiked rates 50bp as expected, in a three-way vote. US yields edge lower after Bank of England decision across long- end, following wider gains across gilts where 10-year UK outperforms Treasuries by 6bp on the day; 10-year yields around 3.47%, slightly richer on day on outright basis. Long-end outperformance in US curve sees 2s10s, 5s30s spreads extend flatter by 1.7bp and 2.2bp on the day. Dollar issuance slate remains light, with up to $5b expected for this week; Fed decision day saw a blank slate Wednesday. Packed data slate for the US session includes retail sales and industrial production.

In commodities, oil fluctuated between gains and losses after rallying almost 9% over the previous three sessions as TC Energy restarted a section of the Keystone pipeline, allowing for some flows to resume on the major conduit. Crude futures were steady, having pared a bulk of the Asian losses with the move coming in spite of the downside seen across the equity complex and a firmer USD. WTI trades within Wednesday’s range near $77.21. TC Energy announced it communicated with regulators and customers about the restart of the Keystone pipeline system sections unaffected by the leak but noted that the affected segment remains isolated and will not be restarted until it is safe and they receive approval to do so, according to Reuters. Spot gold falls roughly $29 to trade near $1,778/oz

To the day ahead now, and the main highlight will be the monetary policy decisions from the ECB and the Bank of England. There are also a number of US data releases, including November’s retail sales and industrial production, December’s Empire state manufacturing survey and the Philadelphia Fed business outlook, as well as the weekly initial jobless claims. Finally, earnings releases today include Adobe.

Market Snapshot

- S&P 500 futures down 1.0% to 3,957.25

- STOXX Europe 600 down 1.2% to 437.27

- MXAP down 1.6% to 157.70

- MXAPJ down 1.6% to 511.73

- Nikkei down 0.4% to 28,051.70

- Topix down 0.2% to 1,973.90

- Hang Seng Index down 1.5% to 19,368.59

- Shanghai Composite down 0.2% to 3,168.65

- Sensex down 1.3% to 61,888.02

- Australia S&P/ASX 200 down 0.6% to 7,204.78

- Kospi down 1.6% to 2,360.97

- German 10Y yield little changed at 1.94%

- Euro down 0.6% to $1.0613

- Brent Futures down 0.8% to $82.02/bbl

- Brent Futures down 0.8% to $82.06/bbl

- Gold spot down 1.5% to $1,780.77

- U.S. Dollar Index up 0.53% to 104.32

Top Overnight News from Bloomberg

- The ECB is poised to slow the recent pace of interest-rate increases and outline plans to shrink its almost €5 trillion ($5.3 trillion) stash of bonds, broadening efforts to curb inflation that’s still five times the target

- UK bond traders seeking shelter from this year’s turmoil are piling into 10-year securities, a section of the market that’s been relatively insulated from central bank action

- Nurses have begun a round of historic strikes as Britain faces the prospect of heightened industrial action extending into next year

- Almost 1 million people in China may die from Covid-19 as the government rapidly abandons pandemic curbs, according to a new study by researchers in Hong Kong

- Expectations for long-term inflation rates in Sweden rose slightly in the latest Prospera survey, after a string of inflation outcomes that show price increases soaring far above the Riksbank’s 2% target

- Turkish President Recep Tayyip Erdogan said he wants a three-way meeting with Syria’s Bashar Al-Assad and Russia’s Vladimir Putin, signaling a thaw with Damascus that could help end the war in Syria

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were subdued in the aftermath of the FOMC. ASX 200 was dragged lower by weakness in nearly all sectors but with losses cushioned by strong jobs data. Nikkei 225 declined but just about remained above the 28K level following strong trade numbers in which the value of both exports and imports reached a record for the month of November. Hang Seng and Shanghai Comp were negative after disappointing Chinese Industrial Production and Retail Sales data, while property and tech stocks were driving the underperformance in Hong Kong after the HKMA raised rates in lockstep with the Fed, while attention was also on the PBoC which conducted a CNY 650bln 1-Year MLF operation vs. CNY 500bln maturing but maintained the rate at 2.75%.

Top Asian News

- PBoC conducted CNY 650bln of 1-year MLF vs. CNY 500bln maturing with the rate kept at 2.75%.

- HKMA raised its base rate by 50bps to 4.75%, as expected, following the Fed rate hike, while Macau's Monetary Authority raised its base rate for the discount window by 50bps to 4.75%.

- China's stats bureau said China's economy maintained its recovery trend in November despite multiple pressures but added that the foundation of the economic recovery is still not solid, according to Reuters.

- US Senate passes bill to ban federal employees from using TikTok on government devices.

European bourses and US futures under pressure, seemingly in a second wave of the post-FOMC price action after action stabilised a touch overnight. Currently, Euro Stoxx 50 -1.3% and ES -1.0%, with non-Central Bank updates relatively thin ahead of key US data and more Policy Announcements. Foxconn (2317 TT) has ended most closed-loop restrictions in 'iPhone city' ( Zhengzhou) , via Bloomberg.

Top European News

- UK PM Sunak eyes anti-strike laws which he vows would protect lives and livelihoods, according to Daily Mail.

- European Gas Prices Rise With Focus on Cold Snap and LNG Supply

- Norway Raises Key Rate and Signals It’s Nearing a Peak

- Kering Leads European Luxury Lower on Disappointing China Data

- Rebel European Soccer League Gets Setback in EU Court Opinion

- VW Sees Growing Challenges Next Year on Inflation, Downturn

- Hungary Says May Need to Amend Gazprom Contract on EU Price Cap

Central Banks

- Swiss SNB Policy Rate (Q4) 1.00% vs. Exp. 1.00% (Prev. 0.50%); cannot be ruled out that further hikes will be necessary. Willing to intervene in FX as necessary. Inflation forecasts cut, implying Switzerland is at the peak level. Click here for full details & analysis.

- SNB's Jordan (press conference) says we have sold foreign currency in recent months to ensure appropriate monetary conditions. Willing to buy/sell foreign currency as necessary.

- Norges Bank Policy Announcement (Dec): 2.75% vs. Exp. 2.75% (Prev. 2.50%); policy rate will most likely be raised further in Q1 2023. Inflation forecasts lifted, Repo Path forecasts tweaked but little changed, implying another 25bp move with some optionality for further tightening, if needed. Click here for full details & analysis.

FX

- USD has continued to climb throughout the morning, DXY above 104.40 at best.

- Action which has weighed on peers across the board, with EUR/USD and Cable testing 1.06 and 1.23 to the downside ahead of ECB & BoE.

- Antipodeans are at the bottom of the G10 pile irrespective of upbeat macro news.

- NOK undermined post-Norges Bank despite initial fleeting upside as the Bank guides towards further tightening, despite the domestic headwind.

- CHF similarly dented in a 'buy the rumour, sell the fact' style following the as-expected SNB and as the inflation forecasts show the economy at the peak, perhaps limited the need for further tightening.

- PBoC set USD/CNY mid-point at 6.9343 vs exp. 6.9325 (prev. 6.9535)

Fixed Income

- Gilts continue to outperform and lead the complex's revival, with Bunds and USTs lifting in turn though are comparably more contained and yet to make any real foray into positive territory.

- USTs appear to be guided by the risk tone and ongoing curve flattening post-Fed, with Central Bank activity since essentially in-line with expectations.

Commodities

- Crude benchmarks are flat, having pared a bulk of the APAC losses with the move coming in spite of the downside seen across the equity complex and a firmer USD.

- TC Energy announced it communicated with regulators and customers about the restart of the Keystone pipeline system sections unaffected by the leak but noted that the affected segment remains isolated and will not be restarted until it is safe and they receive approval to do so, according to Reuters.

- Canada said it decided to revoke the time-limited Nord Stream sanctions waiver that was granted to allow turbines to be repaired in Montreal for return to Germany with the decision made working closely with Ukrainian, German and other European allies, according to Reuters.

- Spot gold and silver are unable to benefit from any traditional haven allure as the USD continues to ramp up; pressure in the yellow metal has brought it below the 10- & 200-DMAs to a test of the 21-DMA, at USD 1788/oz. 1787/oz and 1771/oz respectively.

Geopolitics

- US is planning to send Ukraine advanced electronic equipment that converts unguided aerial munitions into "smart bombs", according to officials cited by Washington Post.

- US defence firms are in talks with Vietnam to sell helicopters and drones, while military deals with the US would signal a shift away from Vietnam's reliance on Russia, according to Reuters.

- Russia's Washington embassy has warned that a transfer of the Patriot System to Ukraine would result in "unpredictable consequences", via Walla News' Elster.

US Event Calendar

- 08:30: Nov. Retail Sales Advance MoM, est. -0.2%, prior 1.3%

- Nov. Retail Sales Ex Auto and Gas, est. 0%, prior 0.9%

- Nov. Retail Sales Ex Auto MoM, est. 0.1%, prior 1.3%

- Nov. Retail Sales Control Group, est. 0.1%, prior 0.7%

- 08:30: Dec. Initial Jobless Claims, est. 232,000, prior 230,000

- Dec. Continuing Claims, est. 1.67m, prior 1.67m

- 08:30: Dec. Empire Manufacturing, est. -1.0, prior 4.5

- 08:30: Dec. Philadelphia Fed Business Outl, est. -10.0, prior -19.4

- 09:15: Nov. Industrial Production MoM, est. 0%, prior -0.1%

- Nov. Capacity Utilization, est. 79.8%, prior 79.9%

- Nov. Manufacturing (SIC) Production, est. -0.2%, prior 0.1%

- 10:00: Oct. Business Inventories, est. 0.4%, prior 0.4%

- 16:00: Oct. Total Net TIC Flows, prior $30.9b

- Oct. Net Foreign Security Purchases, prior $118b

DB's Jim Reid concludes the overnight wrap

If you wanted to briefly sum up the FOMC meeting last night you would probably say that the Fed were hawkish but that the market doesn’t believe they will be. Going through the details (our full US econ review, here), they did hike +50bps as expected, downshifting from four successive +75bps hikes. This brings the upper bound of the fed funds target range to 4.5%, around 360bps above where the markets thought it would be at this point last December. Last night’s meeting also brought a fresh round of projections from the Committee, where the median participant projected policy rates to rise to 5.1% by the end of next year, with core PCE expected to be 3.5%, still plenty above target. The distribution of dots was hawkish as well, as only 2 out of 19 participants pencilled in a policy rate below 5% by the end of 2023, so a strong rebuke to any investors expecting Fed cuts next year.

Indeed, that proved to be a key tenet of the press conference as well. After two optimistic CPI reports, Chair Powell tried to talk financial conditions back from getting too optimistic and easy, saying that even with today’s hikes the Fed still had a “ways to go” to make sure the fight against inflation was well and truly won. Much like the November FOMC, the Chair noted that the step down to smaller hiking increments makes sense as the Committee approaches terminal, and that the pace of rate increases was not nearly as important as the ultimate level of terminal or time spent there, pointing to the dots showing policy above 5% in a year’s time. In that vein, he also opened up the door for a 25bp hike at the Fed’s next meeting in February which may have helped markets reverse some of the immediate sell-off. Powell did note that core goods and housing services inflation was rolling over, in line with the Fed’s expectations, but that core services would remain above target so long as the labour market remained historically tight, as wages are a larger cost input in those sectors.

Markets sold off a touch in the hour following the hawkish dots and communications from the Chair, but the strong messaging was already anticipated by many following the last two CPI prints, as the Fed tries to avoid yet another counterproductive pricing pivot. Therefore, the net price action following the meeting was relatively modest, albeit with a decent sized range in the aftermath. 2yr Treasury yields ended the day -0.9bps lower having been -4.9bps lower heading into the meeting but +10bps 35mins after the decision. Meanwhile 10yr yields were -2.4bps lower after being roughly flat heading into the meeting, and c.+5bps 10 mins after the decision. The terminal rate priced for May increased a modest +1.2bps to 4.87%, still well below the Fed’s own projection of terminal. So something will have to give in the first few weeks of 2023. This morning in Asia, yields on 10yr USTs (+1.82 bps) have moved upwards, trading at 3.50%.

The S&P 500 was +0.71% higher immediately before the meeting but ended -0.61% lower after bouncing around between gains and losses throughout the press conference. So it seems the equity market took the hawkish bias more to heart than fixed income markets.

Asian equity markets are trading in negative territory this morning following the overnight negative lead from Wall Street. The KOSPI (-1.21%) and Hang Seng (-1.14%) are the biggest underperformers while the Nikkei (-0.33%), the Shanghai Composite (-0.28%) and the CSI (-0.23%) are also sliding in early trading. In overnight trading, US stock futures are rangebound with contracts on the S&P 500 (-0.01%) just below flat and the NASDAQ 100 (-0.11%) trading slightly lower.

The big news overnight was data from China showing the toll that widespread Covid restrictions took on growth last month before the government announced that it would ease its policy. Industrial production slowed to +2.2% y/y (v/s +3.5% expected) in November from the +5.0% rise recorded in October. This marked the slowest growth since May when Shanghai was put under a two-month lockdown. At the same time, retail sales (-5.9% y/y) had their biggest contraction since May, underperforming expectations for a decline of -4.0% and greater than a -0.5% drop recorded in October.

Other economic data showed that Australia’s unemployment rate for November remained at 3.4%, in line with market expectations.

Elsewhere in Asia, the Japanese Yen was pretty flat against the USD yesterday even following a Bloomberg report that officials at the Bank of Japan were considering a policy review next year. Historically, reviews have led to policy changes, so it’ll be interesting to see if this ends up happening and whether that might mark a shift away from the ultra-loose monetary policy of recent years, which has increasingly made the BoJ an outlier internationally. Japan reported that exports rose +20.0% y/y in November (v/s +19.7% expected) compared to an increase of +25.3% in October and were outpaced by imports (up +30.3%). The trade deficit swelled more than expected to -2.03 trillion yen in November versus a revised shortfall of -2.17 trillion yen in October. This morning the Yen (+0.13%) is slightly higher, trading at $135.65.

Now that the Fed is out of the way, attention will turn to central banks in Europe today, with the ECB’s decision coming up at 13:15 London time. As with the Fed yesterday, it’s widely expected that the ECB will shift away from the 75bp hikes at the last couple of meetings in favour of a 50bp move today, which would take the deposit rate up to 2%. But even as they slow down their hikes, Mark Wall and our European economists write in their preview (link here) that they’ll maintain a hawkish communications strategy, since the ECB doesn’t want the market to interpret smaller hikes as meaning a lower terminal rate or earlier rate cuts. This hawkishness is likely to come through a number of channels, including upwardly revised staff inflation forecasts, which our economists expect will show stronger inflation in 2023 and 2024 relative to September.

If the ECB wasn’t enough, today will also bring the Bank of England’s decision just over an hour beforehand at 12:00 London time. In terms of what to expect, investors and economists are widely anticipating that the BoE will echo the pattern elsewhere and slow their hikes from 75bps last time to 50bps today. That would take the Bank Rate up to 3.5%, but unlike the ECB, our UK economist expects the MPC to strike another dovish tone this month, and sound more cautious around the risks of over-tightening. The decision today also follows the latest CPI data for November yesterday, which fell back by more than expected to +10.7% (vs. +10.9% expected). See our economist’s full preview here.

With all that to look forward to, European markets put in a pretty subdued performance yesterday, having closed ahead of the Fed decision. The main equity indices all lost modest ground, with the STOXX 600 (-0.02%), the DAX (-0.26%) and the FTSE 100 (-0.09%) posting declines. And for sovereign bonds it was a similar story, with yields on 10yr bunds (+1.7bps), OATs (+3.1bps) and BTPs (+6.7bps) all moving higher on the day. That said, some of the moves at the front-end were more positive, with the German 2yr yield actually falling -0.9bps on the day.

To the day ahead now, and the main highlight will be the monetary policy decisions from the ECB and the Bank of England. There are also a number of US data releases, including November’s retail sales and industrial production, December’s Empire state manufacturing survey and the Philadelphia Fed business outlook, as well as the weekly initial jobless claims. Finally, earnings releases today include Adobe.

Uncategorized

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-March 2024

A brief excerpt: This 2-part overview for mid-March provides a snapshot of the current housing market.

I always like to star…

Share this:

A brief excerpt:

This 2-part overview for mid-March provides a snapshot of the current housing market.There is much more in the article.

I always like to start with inventory, since inventory usually tells the tale!

...

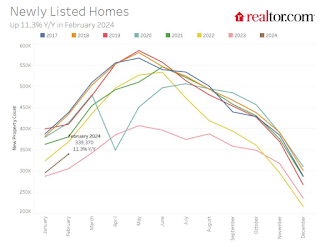

Here is a graph of new listing from Realtor.com’s February 2024 Monthly Housing Market Trends Report showing new listings were up 11.3% year-over-year in February. This is still well below pre-pandemic levels. From Realtor.com:

However, providing a boost to overall inventory, sellers turned out in higher numbers this February as newly listed homes were 11.3% above last year’s levels. This marked the fourth month of increasing listing activity after a 17-month streak of decline.Note the seasonality for new listings. December and January are seasonally the weakest months of the year for new listings, followed by February and November. New listings will be up year-over-year in 2024, but we will have to wait for the March and April data to see how close new listings are to normal levels.

There are always people that need to sell due to the so-called 3 D’s: Death, Divorce, and Disease. Also, in certain times, some homeowners will need to sell due to unemployment or excessive debt (neither is much of an issue right now).

And there are homeowners who want to sell for a number of reasons: upsizing (more babies), downsizing, moving for a new job, or moving to a nicer home or location (move-up buyers). It is some of the “want to sell” group that has been locked in with the golden handcuffs over the last couple of years, since it is financially difficult to move when your current mortgage rate is around 3%, and your new mortgage rate will be in the 6 1/2% to 7% range.

But time is a factor for this “want to sell” group, and eventually some of them will take the plunge. That is probably why we are seeing more new listings now.

Uncategorized

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45%…

Share this:

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45% of US respondents in 2023, according to the latest Harris Poll data. That’s exactly the same as the previous year.

Pharma’s highest point was in February 2021 — as Covid vaccines began to roll out — with a 62% positive US perception, and helping the industry land at an average 55% positive sentiment at the end of the year in Harris’ 2021 annual assessment of industries. The pharma industry’s reputation hit its most recent low at 32% in 2019, but it had hovered around 30% for more than a decade prior.

“Pharma has sustained a lot of the gains, now basically one and half times higher than pre-Covid,” said Harris Poll managing director Rob Jekielek. “There is a question mark around how sustained it will be, but right now it feels like a new normal.”

The Harris survey spans 11 global markets and covers 13 industries. Pharma perception is even better abroad, with an average 58% of respondents notching favorable sentiments in 2023, just a slight slip from 60% in each of the two previous years.

Pharma’s solid global reputation puts it in the middle of the pack among international industries, ranking higher than government at 37% positive, insurance at 48%, financial services at 51% and health insurance at 52%. Pharma ranks just behind automotive (62%), manufacturing (63%) and consumer products (63%), although it lags behind leading industries like tech at 75% positive in the first spot, followed by grocery at 67%.

The bright spotlight on the pharma industry during Covid vaccine and drug development boosted its reputation, but Jekielek said there’s maybe an argument to be made that pharma is continuing to develop innovative drugs outside that spotlight.

“When you look at pharma reputation during Covid, you have clear sense of a very dynamic industry working very quickly and getting therapies and products to market. If you’re looking at things happening now, you could argue that pharma still probably doesn’t get enough credit for its advances, for example, in oncology treatments,” he said.

vaccine pandemic covid-19Uncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

{kind=link}

{kind=link}

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

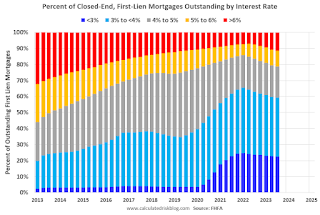

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

{kind=link}

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Digital Currency And Gold As Speculative Warnings

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Bougie Broke The Financial Reality Behind The Facade

Aging at AACR Annual Meeting 2024

The most potent labor market indicator of all is still strongly positive

‘Bougie Broke’ – The Financial Reality Behind The Facade

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges