Uncategorized

Futures Slide As Global Yields Soar, Pushing Bond Markets To Edge Of Breaking

Futures Slide As Global Yields Soar, Pushing Bond Markets To Edge Of Breaking

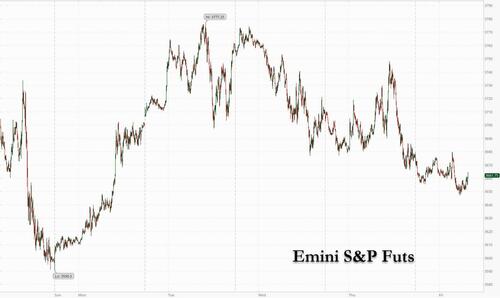

US equities extended their recent slump, set to trim their modest…

Share this:

US equities extended their recent slump, set to trim their modest weekly advance even further as soaring bonds yields and poor earnings renewed the gloom that’s sent stocks into a bear market this year. Contracts on the S&P 500 dipped 0.4% at 7:30 a.m. ET, putting the underlying index on track to sharply pare this week’s 2.3% gain...

... as the yield on the 10-year Treasury rose to 4.29%, the highest since 2007 and as Treasuries dropped for a 12th consecutive week, which would match longest stretch since 1984. Fed swaps price in a 5% peak policy rate in 2023 after Philly Fed President Patrick Harker said that the Fed is likely to raise interest rates to “well above” 4% this year and hold them at restrictive levels to combat inflation,

“The global inflation bogeyman continues to scare the bond markets,” said strategists at Societe Generale SA including Ninon Bachet. “Central banks have additional big moves to make in their tightening process, so we remain short duration.”

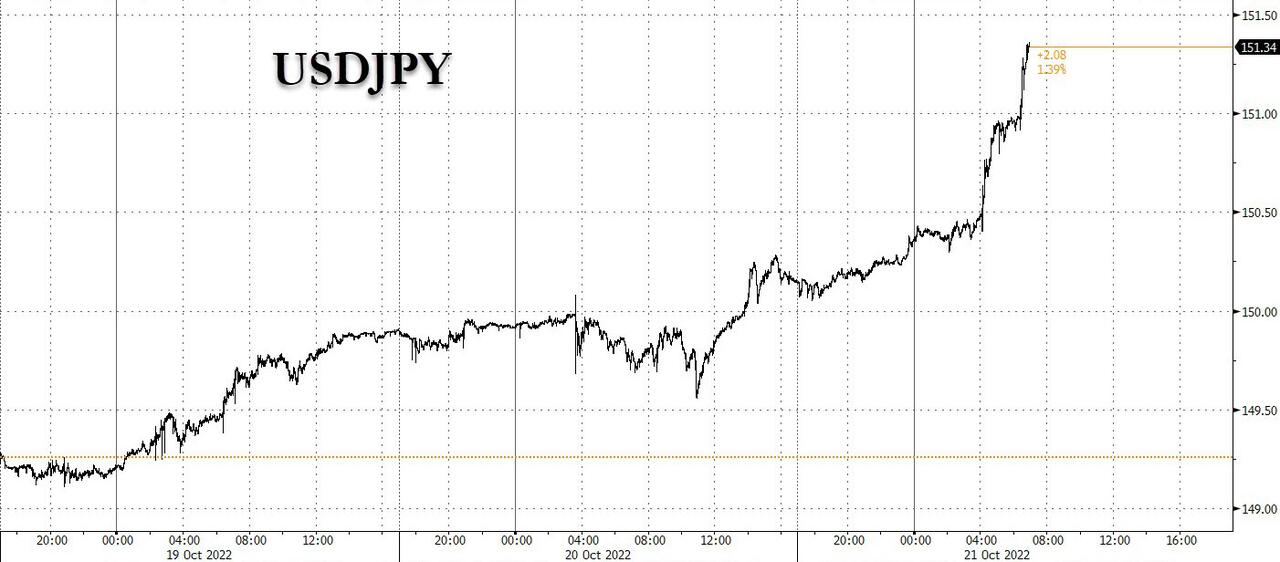

Nasdaq 100 futures fell 0.9% after the tech-heavy gauge advanced 3.3% from Monday through Thursday. Surging yields also pushed the dollar sharply higher, with USDJPY soaring above 151.50 and the yuan falling to the weakest level since 2008.

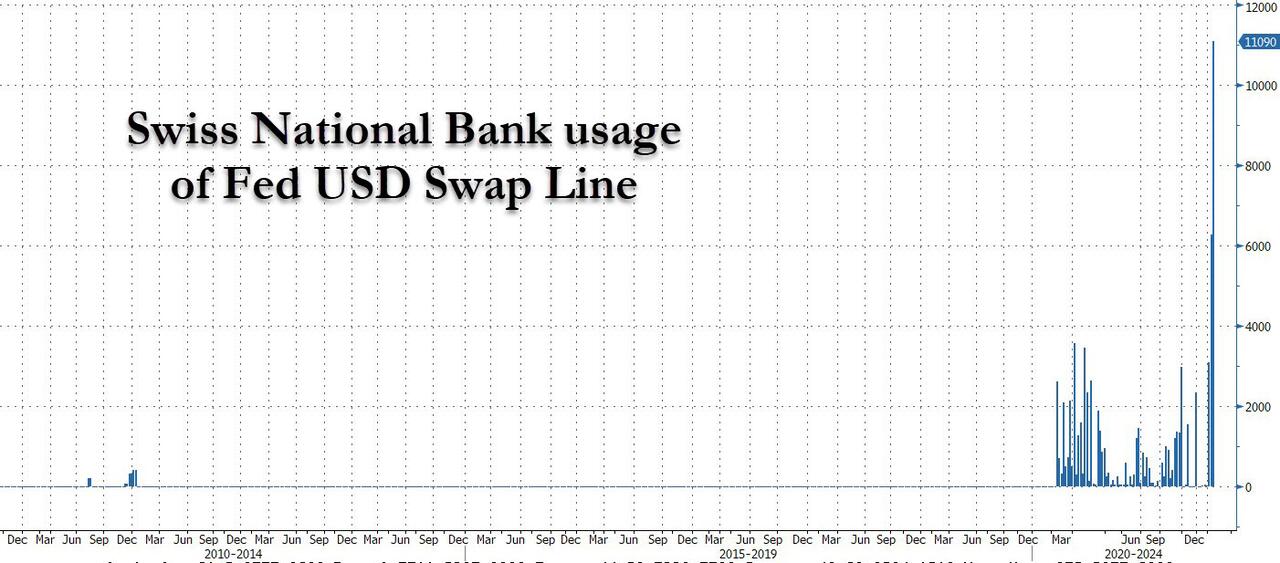

At this point, absent a Fed short-circuit of the soaring dollar (in the form of a major liquidity injection), a global currency crisis is all but assured; one look at the latest record weekly usage in the SNB swap line with the Fed confirms without a doubt that there is now a global currency shortage which is becoming more systemic by the week if not day.

In premarket trading, Twitter shares tumbled, falling as much as 16% and well below Elon Musk’s offer price, on concern the deal may be terminated by the government. Earnings from appliance maker Whirlpool and social-media platform Snap disappointed investors after the market closed Thursday. Snap plunged 27% in premarket trading Friday after its slowest quarterly sales growth ever. This sets the stage for what investors can expect when bigger players like Alphabet and Meta Platforms report next week. Earlier this week, firms among AT&T as well as IBM had beaten expectations earlier this week. Here are some of the biggest US movers today:

- Whirlpool shares drop 4% in US postmarket trading after the company cut its FY ongoing EPS guidance; shares of Swedish peer Electrolux also fall.

- CSX gained 3% in premarket trading. It’s unchanged FY guidance comes as a relief after peer Union Pacific cut its forecast for volume growth, Morgan Stanley analysts write after the freight transportation firm reported 3Q earnings that beat estimates.

- Opendoor Technologies slides 2.5% in premarket trading after Truist Securities cut the price target to $5 from $8 as the analyst trims their margin estimates for the real estate firm.

- Autoliv shares rise as much as 5.9% in premarket trading after the firm said it expects to see full-year organic revenue growth of about 15%, higher than the 14.5% that analysts had been expecting.

- Under Armour shares decline 3.2% in premarket trading after Telsey Advisory Group downgrades the sportswear brand to market perform from outperform, expecting high inventory rates from Nike and Adidas to weigh on FY23 and for the company to once again cut its 2022 outlook again when it reports on November 3.

- Immunic shares sink 71% in premarket trading after interim analysis of the biopharma company’s Phase 1b clinical trial of IMU-935 patients with moderate-to-severe psoriasis showed a placebo rate that Piper Sandler says was “surprisingly high.”

- SVB Financial dropped 17% in premarket trading after lowering its full-year forecast for net interest income growth.

- Tenet drops 18% in premarket trading after the health care company narrowed its operating revenue guidance to a level below Wall Street estimates.

As Bloomberg notes, the S&P 500 hasn’t been able to hold onto gains for more than a week since early August, a sign of persistent economic headwinds as the Federal Reserve continues raising interest rates. The earnings season will be key to dictating the direction of equities until the US central bank meets next month. Ironically, so far it is nowhere near as bad as some had suspected with 74% of companies have exceeded earnings expectations versus the long-term, prepandemic average of 72%, according to Bloomberg analysts Gina Martin Adams and Gillian Wolff.

“History tells us that markets don’t find a bottom until investors begin to anticipate rate cuts, leading indicators point to better growth, or valuations price a bear case scenario. That’s not the case today,” UBS Global Wealth Management strategists led by Mark Haefele wrote in a note. “Equity valuations, despite falling in absolute terms, don’t yet fully discount a bear case.”

Investor sentiment has turned deeply pessimistic but that’s not yet being reflected in equity flows and “final capitulation” remains elusive, according to strategists at Bank of America Corp. US funds had a second straight week of inflows at $12 billion in the week through Oct. 19, according to a note from the bank citing EPFR Global data.

European stocks fell amid the broader risk-off mood. Euro Stoxx 50 slumps 1.6% as retailers, consumer products and construction are the worst-performing sectors as all industry groups in Europe fall. Here are some of the biggest European movers today:

- L’Oreal’s 3Q sales showed “hairline fractures appearing,” according to Morgan Stanley, with volumes sequentially softening, pockets of weaker demand and changing consumer behavior. The stock fell as much as 5.5%, biggest intraday drop in more than two years.

- Adidas shares plunge as much as 10%, the most since March 7, after the German sportswear maker cut its outlook for the year flagging slowing demand, partly due to a weakening in footfall in China, and also because of inventory build-up, providing further warning about the consumer slowdown.

- Sika shares drop as much as 5.1% despite maintaining its FY guidance, as Jefferies says a third-quarter Ebit miss may trigger mild downgrades.

- Telia shares fall as muchy as 8.9% to their lowest level since 2003, as a steep increase in energy costs prompts a cut to its profit outlook, with operational free cash flow for 2022 set to be below the minimum dividend level.

- PostNL declines as much as 12%, the most since May 9, after the Dutch mail carrier withdrew its FY guidance, citing rising inflation and a drop in consumer confidence which has led to 3Q under performance, particularly in parcel delivery.

- Grifols shares dropped as much as 8.8% to their lowest level in 10 years following a media report that it could face legal claims in the US for as much as $270m. Banco Santander notes potential fine size could represent about 1% to 4% of plasma firm’s market cap.

- Deliveroo shares rise as much as 6.2%. The food delivery firm lifted its adjusted Ebitda margin guidance for the year, making progress on plans to improve profitability amid slowing growth.

- Borregaard shares climb as much as 3.7% after the specialized biochemicals supplier reports 3Q results that may push earnings per share estimates for 2023 and 2024 higher by 2%-3%, DNB analyst says in note.

Earlier in the session, Asian stocks fell, set to cap a second week of declines, as recession worries weighed on sentiment amid hawkish central-bank remarks and stringent China Covid restrictions. The MSCI Asia Pacific Index dropped as much as 1.2% Friday, with most of the markets in the region marking losses. The Hong Kong benchmark hit its lowest since April 2009, while gauges in Singapore and the Philippines declined more than 1%. China’s pandemic rules continued to weigh on regional investor sentiment amid additional lockdowns. Risk sentiment was also hurt by higher Treasury yields after a Federal Reserve official said he expects interest rates to be “well above” 4% this year.

“I think the risks for recession in the region are pretty high,” David Chao, Asia Pacific market strategist at Invesco, said in an interview with Bloomberg TV. Still, Chao believes Asia Pacific is “relatively more attractive” than Europe and the US as the region is somewhat insulated from high levels of inflation and central bank tightening. Traders will be on the watch for earnings reports in the coming days to understand the impact of high inflation and China’s virus restrictions on corporate health and growth. Down about 30% this year, the key Asian stock gauge is trading near its lowest level since April 2020.

Japanese stocks fell, as losses in chemical makers and railways offset gains in electronics makers. Japan’s core inflation reached 3% for the first time in over three decades excluding tax-hike impacts. The Topix fell 0.7% to close at 1,881.98, while the Nikkei declined 0.4% to 26,890.58. The yen slightly extended its loss after falling through 150 per dollar Thursday. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 1.5%. Out of 2,166 stocks in the index, 442 rose and 1,626 fell, while 98 were unchanged

Australian stocks also slid as banks, property shares weigh; the S&P/ASX 200 index fell 0.8% to close at 6,676.80, with banks and real estate stocks leading the declines. All sectors slumped except for energy as oil gained. The benchmark notched a second week of declines, down 1.2%. In New Zealand, the S&P/NZX 50 index fell 0.5% to 10,782.36.

India stocks posted their biggest weekly gain since July as investor sentiment was buoyant ahead of a key festival next week while corporate earnings season gathers steam. The S&P BSE Sensex rose 0.2% to 59,307.15 in Mumbai, while the NSE Nifty 50 Index was little changed. Both the gauges rose at least 2.3% this week. All but three of BSE Ltd.’s 19 sector sub-indexes declined, led by capital goods companies. For the week, banking stocks were the best performers, thanks to strong earnings performances by top lenders including HDFC Bank. After a stronger-than-expected quarterly performances by technology and banking companies, earnings were starting to reflect worries over elevated costs. Of 17 Nifty 50 Index firms, which have posted results so far, 11 have either met or surpassed the consensus view while five have missed.

In FX, the Bloomberg Dollar Spot Index roared higher after whipsawing in early European hours; the greenback rose against all its Group-of-10 peers. Long-dated Treasuries fell, driving the 10-year benchmark yield to a 15-year high, as traders bet the Federal Reserve will press ahead with rate hikes to defeat inflation.

- The euro reversed an early European session gain and bonds from the region fell across the board. Germany’s 10-year yield climbed above 2.5% for first time since 2011.

- The pound fell against all of its G-10 peers and tumbled as much as 1.2%, while gilts sold off as markets entered another bout of uncertainty amid a truncated leadership contest following the resignation of Liz Truss. The next leader could be decided as soon as Monday. The UK budget deficit in September exceeded estimates

- The yen fell beyond 151 per dollar as the disparity between US and Japanese yields continued to grow, putting the currency on track for a 10th straight weekly loss. The relative premium to own exposure in short-term dollar-yen options rose to levels not seen for more than six years due to the risk of intervention as realized volatility remains in defensive mode. The Bank of Japan will keep conducting monetary easing to support the economy and sustainably and stably achieve its price target accompanied by wage growth, Governor Haruhiko Kuroda said in a speech in Tokyo. Finance Minister Shunichi Suzuki told reporters that Japan is firmly confronting forex speculators in the market now.

- The onshore yuan fell to the weakest level since 2008 as the greenback surged on hawkish comments from a Federal Reserve official.

In rates, Treasuries dropped for 12th week, which would match longest stretch in 38 years. BOJ boosted bond purchases to hold 10-year yield at 0.25% ceiling, while Australian bonds drop. Longer-dated Treasuries extended Thursday’s declines, steepening 2s10s and 5s30s spreads by at least 4bp into early US session. Bigger bear-steepening move grips German curve as 10-year yields top 2.5% for first time since 2011. US yields were cheaper by nearly 7bp across long-end of the curve with 2s10s, 5s30s spreads steeper by about 4.5bp and 6.5bp on the day. German long-end yields are cheaper by 11.5bp on the day while Gilts 10-year yield rose 8bps, trading around 4% as traders add BOE and ECB rate-hike premium.

In commodities, WTI drifts 1.6% lower to trade near $83.19, but off lows amid the firmer Dollar and deterioration of broader risk sentiment. Saudi and China are said to be ready to cooperate oil market stability; Saudi remains the most trusted China oil supplier, according to a joint statement cited by Bloomberg. LME metals are lower across the board with 3M copper also weighed on by the risk mood – the red metal trades on either side of USD 7,500/t. Spot gold posts modest losses and remains under USD 1,650/oz after dipping below yesterday’s lows.

Bitcoin is under pressure and has lost the USD 19k handle and lies at the lower-end of a circa USD 700 range for the session.

Looking to the day ahead now, data releases include UK retail sales for September and the US Monthly budget statement. From central banks, we’ll hear from New York Fed President Williams. Finally, earnings releases include Verizon Communications and American Express.

Market Snapshot

- S&P 500 futures down 0.6% to 3,653.00

- STOXX Europe 600 down 1.4% to 393.11

- MXAP down 1.1% to 135.34

- MXAPJ down 0.9% to 438.50

- Nikkei down 0.4% to 26,890.58

- Topix down 0.7% to 1,881.98

- Hang Seng Index down 0.4% to 16,211.12

- Shanghai Composite up 0.1% to 3,038.93

- Sensex up 0.2% to 59,347.19

- Australia S&P/ASX 200 down 0.8% to 6,676.76

- Kospi down 0.2% to 2,213.12

- German 10Y yield up 3.7% at 2.49%

- Euro down 0.2% at $0.9758

- Brent Futures down 1% to $91.45/bbl

- Gold spot down 0.4% to $1,621.21

- U.S. Dollar Index up 0.42% to 113.357

Top Overnight News from Bloomberg

- Giorgia Meloni clinched a mandate from her coalition on the path to becoming Italy’s first female premier, after weeks of political stasis following her right-wing alliance’s election win

- The UK Treasury may be forced to delay its long-awaited Oct. 31 fiscal plan because of the resignation of Prime Minister Liz Truss, adding a layer of political risk to an event that had become crucial for markets and the Bank of England

- The Conservative Party is desperate to draw a line under Truss’s disastrous premiership, with a rapid leadership contest aimed at trying to give the winner a shot at overturning an unprecedented deficit in the polls

- Regardless of who wins the race to succeed Truss as UK Prime Minister, one thing is clear: the pound is set to keep falling. That’s the prognosis of market players who see sterling continuing its descent as economic headwinds and the Bank of England’s policy stance act as a drag

- Traders in UK government bonds helped topple Truss. Now they’re setting their sights on the next goal: ensuring her successor will stick to the fiscal discipline required to shore up the country’s fragile finances

- UK retail sales fell more than expected last month after the death of Queen Elizabeth II curtailed activity and cost-of- living pressures hit harder. The volume of goods sold in shops and online dropped 1.4% in September after a revised 1.7% decline the month before. Economists had expected an 0.5% drop

- ECB officials are considering whether to add a new overnight interest rate to co-exist with its three existing levers to manipulate the cost of money, Expansion reported, citing people familiar with the matter

- The EU agreed to press ahead with a set of emergency actions to address the bloc’s energy crisis, with Germany yielding to pressure from other member states to pave the way for a temporary price cap on natural gas. European natural gas prices fell after the accord

- US Treasuries have entered the longest sustained slump in 38 years, as policy makers signal their determination to keep raising rates until they are sure inflation is under control

- The Communist Party’s list of Central Committee members released Saturday will be scrutinized by economists for what it means for the People’s Bank of China. Governor Yi Gang, 64, and Guo Shuqing, 66, who is party chief and deputy governor at the central bank, are around the official retirement age, fueling speculation over whether they’ll remain in their posts

- China’s yuan is expected to weaken further after the Communist Party Congress ends this weekend, as the central bank loosens its grip on the currency, according to market watchers

A More detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded cautiously with the region lacking firm direction following the weak lead from Wall Street where stocks reversed initial gains amid mixed data releases and continued upside in yields. ASX 200 was dragged lower by underperformance in industrials and the top-weighted financials sector, while the Australian Treasurer also flagged a 25bps hit to Q4 GDP from recent floods. Nikkei 225 was slightly softer after mostly inline inflation data which showed Core CPI at its fastest pace of increase since 2014 and as participants remained on alert for intervention after the JPY weakened beyond the 150.00 level for the first time since 1990. Hang Seng and Shanghai Comp. were indecisive heading towards the conclusion of the Communist Party Congress and pending release of delayed key data. Furthermore, Chinese press reports noted analysts see room for an LPR cut by year-end, although there was also the threat of further tech restrictions with the US eyeing expanding its China tech ban to quantum computing and A.I. products.

Top Asian News

- US is reportedly eyeing expanding its China tech ban to quantum computing and AI products, according to Bloomberg.

- Australian PM Albanese said he is concerned about a delay to the implementation of the UK-Australia trade agreement amid UK political instability, according to Reuters.

- Australian Treasurer Chalmers said the latest floods are to cut 25bps from GDP growth in the December quarter, while floods will add 10bps to inflation in December and March quarters, according to Reuters.

- India Rate-Setter Wants RBI to Focus on Softening Core Inflation

- China Market Revival Hopes in Tatters as Congress Disappoints

- Hong Kong Cancels Screening of Batman Film Shot in the City

- Chinese City Plans Offshore Wind Farm That Could Power Norway

- Asian Development Bank Approves $1.5 Billion Loan for Pakistan

Cash bourses in Europe started the session with losses which then extended to the downside as market sentiment further deteriorated. Sectors in Europe are in a sea of red, but defensive sectors are faring better than cyclical peers, with Healthcare, Food & Beverages, Optimised Personal Goods, and Utilities towards the top of the bunch, whilst Retail, Consumer Products, Construction, Real Estate, and Basic Resources reside on the other end of the spectrum. US equity futures are also softer across the board with the NQ (-0.9%) lagging its peers (ES -0.6%, RTY -0.5%, YM -0.4%) as bond yields continue to climb. SNAP (SNAP) - Q3 2022 (USD): Adj. EPS 0.08 (exp. 0.00), Revenue 1.128 (exp. 1.14bln). Daily active users rose 19% Y/Y to 363mln (exp. 358.7mln), sees Q4 DAU of about 375mln. Quarterly sales growth was slowest on record. Authorized a stock repurchase program of up to USD 500mln of its Class A common stock. Not providing formal Q4 guidance and sees it as highly likely that Y/Y revenue growth will decelerate as we move through Q4, due in large part to the fact that Q4 has historically been relatively more dependent on brand-oriented advertising revenue, which declined slightly on a Y/Y basis in the most recent quarter. Estimate adj. EBITDA would be about USD 200mln under about flat Y/Y revenue growth assumption for D4. (businesswire) -25% in the pre-market. US government is reportedly mulling a security review regarding Elon Musk's deal to acquire Twitter (TWTR), according to Bloomberg. Additionally, Elon Musk is said to have told prospective investors that he planned to cut almost 75% of Twitter (TWTR) workers, according to documents cited by Washington Post. CATL slows battery investment plans in N. America, according to Reuters sources; due to concern that new US rules around sourcing battery material will increase costs.

Top European News

- German Parliament votes to approve the suspension of the debt brake, via Reuters.

- Italy's Meloni says she has been proposed by the rightist coalition as PM to President Mattarella, via Reuters.

- The ECB is planning to create a new interest rate, according to Expansion.

- Adidas’s Unsold Sneakers and Problems Are Piling Up for Next CEO

- Renault Slips as Inflation Worries Offset Revenue Gains

- French Central Banker Warns Against Algos in Currency Trading

- Credit Suisse Set to Settle Criminal Tax Case in France

FX

- DXY has continued to benefit from further yield upside with the 10-yr eclipsing 4.25% and the index to a 113.50+ best.

- As such, peers across the board are hampered with GBP lagging and approaching 1.11 amid the latest bout of political turmoil.

- EUR/USD seemingly found support as it neared the 0.97 mark and conscious of multiple chunky OpEx for the NY Cut.

- Traditional havens are also dented despite risk sentiment given differentials weighing; USD/JPY has risen to a test of 151.00, with participants attentive for any BoJ/MoF reaction.

- Antipodeans are unable to escape the USD's ascendance with CAD similarly dented, but off worst, amid the most recent paring of crude losses.

- China's major state-owned banks are seen selling USD in the onshore spot market to stabilise the Yuan, according to Reuters sources; meant to prevent the spot price from weakening past 7.25.

Fixed Income

- Debt has extended on initial downbeat performance amid Germany approving the debt brakes suspension to fund their EUR 200bln energy support scheme.

- As such, Bunds are subdued by over a full point; though, amid ongoing political turmoil, Gilts remain the laggard and briefly lost the 97.00 handle sending the corresponding yield back above 4.0%.

- Stateside, USTs are similarly pressured though a touch more contained ahead of Fed's Williams as we near the blackout period.

- Elsewhere, the periphery has been unreactive to the as-expected announcement that the Italian coalition has put Meloni forward to become PM.

Commodities

- WTI and Brent December contracts are lower intraday but off lows amid the firmer Dollar and deterioration of broader risk sentiment.

- Spot gold posts modest losses and remains under USD 1,650/oz after dipping below yesterday’s lows.

- LME metals are lower across the board with 3M copper also weighed on by the risk mood – the red metal trades on either side of USD 7,500/t.

- Saudi and China are said to be ready to cooperate oil market stability; Saudi remains the most trusted China oil supplier, according to a joint statement cited by Bloomberg.

- EU Council President Michel said the European Council reached an agreement on energy and agreed to work on measures to contain energy prices, according to Bloomberg.

- Belgium PM says it will take 2-3 weeks for energy ministers to come up with how to implement the gas price cap, via FT's Bounds; two energy ministers summit will probably be needed to agree energy package, via WSJ's Norman.

- Hungary's PM Orban said an agreement was reached that even if the EU imposes a gas price cap, long-term supply agreements will be exempt, according to a Facebook post.

- US Treasury Official estimates that Russia has sufficient tankers and services to trade about 80-90% of its oil, following the December 5th sanctions; circa. 1-2mln BPD of Russian crude and refined products could be shut in if they resist the price cap, via Reuters.

Geopolitcs

- US Secretary of State Blinken said they take the Russian threat to use nuclear weapons seriously but have not yet seen a reason to change our nuclear status, according to Al Jazeera.

- EU could reinforce sanctions on Iran if support for Russia isn't wound back; "Several leaders said they'd be open to additional sanctions this morning.", according to WSJ's Norman.

- US Secretary of State Blinken said they place great emphasis on making sure the differences between China and Taiwan are resolved peacefully and not through coercion or force, according to Al Jazeera.

US Event Calendar

- 3:15 p.m. ET: President Joe Biden delivers remarks on student debt relief in Dover, Delaware

Central Bank Speakers

- 09:10: Fed’s Williams Makes Opening Remarks at Careers Event

- 09:40: Fed’s Evans Speaks at Community Banking Symposium

DB's Jim Reid concludes the overnight wrap

Risk assets struggled and sovereign bond yields hit fresh multi-year highs yesterday as investors moved to price in the most aggressive path for central bank rate hikes so far. In fact, there was a notable milestone for Fed funds futures, since by the close they expected the Fed to take rates above 5% next year, which is the first time that futures for an upcoming meeting have closed that high in this cycle so far. Bear in mind that on the day of Chair Powell’s hawkish Jackson Hole speech in late-August they closed at 3.78% for the March meeting, so the stronger-than-expected inflation prints over the last couple of months have led to a big reappraisal in how hawkish the Fed and other central banks are expected to be.

Those increasingly hawkish expectations drove a fresh selloff in US Treasuries, with the 10yr yield up +9.5bps to close at 4.23%. That’s their highest level since 2008, and came as the 10yr real yield (+4.0bps) hit a post-2009 high of its own at 1.74%. And those rises have continued overnight, with 10yr yields up another +2.7bps to a new high of 4.26% as we go to print. Those moves have been partly supported by stronger-than-expected data, with the weekly initial jobless claims for the week ending October 15 unexpectedly falling to 214k (vs. 233k expected), which was seen as giving the Fed more space to keep hiking rates. But we also had a fresh round of speakers from the Fed, including Philadelphia Fed President Harker, who said that he expected rates to be “well above” 4% by the end of the year. In the meantime, Governor Cook reiterated the message from Chair Powell that the Fed would “keep at it until the job is done”, and that this would “likely will require ongoing rate hikes and then keeping policy restrictive for some time.” Remember that today is the last we’ll hear from any FOMC members, as the Fed will then be entering its blackout period ahead of the next meeting a week on Wednesday.

Central bank hawkishness had a knock-on effect on equities too, with the S&P 500 (-0.80%) losing ground for a second day running, reversing course from its early gains when it had been on track to hit a 2-week high. Those declines were led by the more cyclical sectors, but it was a broad-based move that saw over three-quarters of the index’s members lose ground on the day. Small-cap stocks underperformed in particular, with the Russell 2000 down -1.24%, whereas the Dow Jones only shed -0.30%. European equities had a comparatively better performance though, having closed before the US selloff, and the STOXX 600 advanced +0.26%.

Whilst markets are gearing up for the next round of central bank decisions, here in the UK we’re also set to have another Prime Minister by the end of next week after Liz Truss announced her resignation yesterday after just 44 days in office. That’ll mean she’s the shortest-serving PM in UK history, and caps off a brief but tumultuous period in office, with the turning point occurring on September 23 when the government’s mini-budget triggered market turmoil that eventually led the government to U-turn on most of what they announced that day. The mini-budget also led to a sharp decline in the Conservatives’ polling position against the backdrop of large rises in mortgage rates, with the opposition Labour Party seeing their largest poll leads since the late-1990s. As such, we saw growing numbers of Conservative MPs withdraw their support from Truss over recent days, ultimately leading to her resignation yesterday.

In terms of what happens next, there’s now going to be another Conservative leadership election to select the next Prime Minister, in a short contest that’ll conclude by Friday October 28 at the latest. Candidates will require nominations from 100 MPs by Monday afternoon to go onto the ballot, which means there can only be a maximum of three anyway. MPs will then vote on Monday to take that down to two candidates for grassroots Conservative members to vote on. But unlike before, MPs will also hold an indicative vote between the final two, and it’s certainly possible that the losing candidate comes under significant pressure to drop out, so we could potentially know the next PM by Monday.

When it comes to who’ll be the next PM, the bookmakers’ favourite is former Chancellor Rishi Sunak, who was the runner-up to Liz Truss over the summer. But speculation is also swirling around former PM Boris Johnson, who the Times newspaper reported is expected to stand in the contest, and who a number of Conservative MPs have already publicly endorsed.

In terms of the market reaction, there weren’t any discernible moves in response to Truss’ resignation. Sterling only saw a small movement of +0.14% against the US Dollar, and the moves in 10yr gilt yields (+2.9bps) echoed those in other European countries. However, one development that led investors to dial back the amount of rate hikes priced in for the coming months was a speech by BoE Deputy Governor Broadbent, who said that “Whether official interest rates have to rise by quite as much as currently priced in financial markets remains to be seen”.

As with gilts, sovereign bonds elsewhere in Europe lost ground, with yields on 10yr bunds (+2.8bps) rising to a post-2011 high of 2.39%. That followed growing expectations that the ECB were set to maintain their hawkish stance over the coming months, with the deposit rate priced in by overnight index swaps for the March meeting up a further +4.5bps to a new high of 2.76%, and this morning it’s up another +6.2bps to 2.82%. That rise in yields was driven by higher inflation breakevens yesterday rather than real rates, which wasn’t helped by the fact that natural gas futures rebounded by +13.01% to €127 per megawatt-hour, ending a run of 5 consecutive daily declines.

Overnight in Asia, the major equity indices have been struggling overnight as bond yields continue to rise. That’s seen the Nikkei (-0.33%), the Hang Seng (-0.17%) and the Kospi (-0.33%) all lose ground, although the CSI 300 (+0.15%) and the Shanghai Comp (+0.50%) have both made gains. US and European equity futures have similarly fallen back, with contracts tied to the S&P 500 (-0.23%) and the NASDAQ 100 (-0.57%) are both lower. Snap reported their weakest sales ever quarterly sales growth, up just 6% in Q3.

Elsewhere in Asia, the other big piece of news was that the Japanese Yen weakened through 150 per dollar for first time since 1990 just after we went to press yesterday. It’s now currently trading at 150.40, putting it well on track for a 10th consecutive weekly decline against the dollar. In response, finance minister Suzuki said that there had been “absolutely no change to our thinking that we’ll take an appropriate response against excessive moves”. The moves also came as Japanese inflation remained strong, with CPI staying at +3.0% (vs. +2.9% expected), and CPI excluding fresh food up to +3.0% as expected. Apart from the jump in 2014 following the sales tax hike, that’s the highest that core measure has been since 1991.

Looking at yesterday’s other data, US existing home sales fell to an annualised rate of 4.71m in September (vs. 4.70m expected), which is their lowest level in a decade if you exclude the pandemic months of April and May 2020. Meanwhile in Germany, producer price inflation remained at +45.8% year-on-year in September (vs. +45.4% expected).

To the day ahead now, and data releases include UK retail sales for September. From central banks, we’ll hear from New York Fed President Williams. Finally, earnings releases include Verizon Communications and American Express.

Uncategorized

Homes listed for sale in early June sell for $7,700 more

New Zillow research suggests the spring home shopping season may see a second wave this summer if mortgage rates fall

The post Homes listed for sale in…

Share this:

- A Zillow analysis of 2023 home sales finds homes listed in the first two weeks of June sold for 2.3% more.

- The best time to list a home for sale is a month later than it was in 2019, likely driven by mortgage rates.

- The best time to list can be as early as the second half of February in San Francisco, and as late as the first half of July in New York and Philadelphia.

Spring home sellers looking to maximize their sale price may want to wait it out and list their home for sale in the first half of June. A new Zillow® analysis of 2023 sales found that homes listed in the first two weeks of June sold for 2.3% more, a $7,700 boost on a typical U.S. home.

The best time to list consistently had been early May in the years leading up to the pandemic. The shift to June suggests mortgage rates are strongly influencing demand on top of the usual seasonality that brings buyers to the market in the spring. This home-shopping season is poised to follow a similar pattern as that in 2023, with the potential for a second wave if the Federal Reserve lowers interest rates midyear or later.

The 2.3% sale price premium registered last June followed the first spring in more than 15 years with mortgage rates over 6% on a 30-year fixed-rate loan. The high rates put home buyers on the back foot, and as rates continued upward through May, they were still reassessing and less likely to bid boldly. In June, however, rates pulled back a little from 6.79% to 6.67%, which likely presented an opportunity for determined buyers heading into summer. More buyers understood their market position and could afford to transact, boosting competition and sale prices.

The old logic was that sellers could earn a premium by listing in late spring, when search activity hit its peak. Now, with persistently low inventory, mortgage rate fluctuations make their own seasonality. First-time home buyers who are on the edge of qualifying for a home loan may dip in and out of the market, depending on what’s happening with rates. It is almost certain the Federal Reserve will push back any interest-rate cuts to mid-2024 at the earliest. If mortgage rates follow, that could bring another surge of buyers later this year.

Mortgage rates have been impacting affordability and sale prices since they began rising rapidly two years ago. In 2022, sellers nationwide saw the highest sale premium when they listed their home in late March, right before rates barreled past 5% and continued climbing.

Zillow’s research finds the best time to list can vary widely by metropolitan area. In 2023, it was as early as the second half of February in San Francisco, and as late as the first half of July in New York. Thirty of the top 35 largest metro areas saw for-sale listings command the highest sale prices between May and early July last year.

Zillow also found a wide range in the sale price premiums associated with homes listed during those peak periods. At the hottest time of the year in San Jose, homes sold for 5.5% more, a $88,000 boost on a typical home. Meanwhile, homes in San Antonio sold for 1.9% more during that same time period.

| Metropolitan Area | Best Time to List | Price Premium | Dollar Boost |

| United States | First half of June | 2.3% | $7,700 |

| New York, NY | First half of July | 2.4% | $15,500 |

| Los Angeles, CA | First half of May | 4.1% | $39,300 |

| Chicago, IL | First half of June | 2.8% | $8,800 |

| Dallas, TX | First half of June | 2.5% | $9,200 |

| Houston, TX | Second half of April | 2.0% | $6,200 |

| Washington, DC | Second half of June | 2.2% | $12,700 |

| Philadelphia, PA | First half of July | 2.4% | $8,200 |

| Miami, FL | First half of June | 2.3% | $12,900 |

| Atlanta, GA | Second half of June | 2.3% | $8,700 |

| Boston, MA | Second half of May | 3.5% | $23,600 |

| Phoenix, AZ | First half of June | 3.2% | $14,700 |

| San Francisco, CA | Second half of February | 4.2% | $50,300 |

| Riverside, CA | First half of May | 2.7% | $15,600 |

| Detroit, MI | First half of July | 3.3% | $7,900 |

| Seattle, WA | First half of June | 4.3% | $31,500 |

| Minneapolis, MN | Second half of May | 3.7% | $13,400 |

| San Diego, CA | Second half of April | 3.1% | $29,600 |

| Tampa, FL | Second half of June | 2.1% | $8,000 |

| Denver, CO | Second half of May | 2.9% | $16,900 |

| Baltimore, MD | First half of July | 2.2% | $8,200 |

| St. Louis, MO | First half of June | 2.9% | $7,000 |

| Orlando, FL | First half of June | 2.2% | $8,700 |

| Charlotte, NC | Second half of May | 3.0% | $11,000 |

| San Antonio, TX | First half of June | 1.9% | $5,400 |

| Portland, OR | Second half of April | 2.6% | $14,300 |

| Sacramento, CA | First half of June | 3.2% | $17,900 |

| Pittsburgh, PA | Second half of June | 2.3% | $4,700 |

| Cincinnati, OH | Second half of April | 2.7% | $7,500 |

| Austin, TX | Second half of May | 2.8% | $12,600 |

| Las Vegas, NV | First half of June | 3.4% | $14,600 |

| Kansas City, MO | Second half of May | 2.5% | $7,300 |

| Columbus, OH | Second half of June | 3.3% | $10,400 |

| Indianapolis, IN | First half of July | 3.0% | $8,100 |

| Cleveland, OH | First half of July | 3.4% | $7,400 |

| San Jose, CA | First half of June | 5.5% | $88,400 |

The post Homes listed for sale in early June sell for $7,700 more appeared first on Zillow Research.

federal reserve pandemic home sales mortgage rates interest ratesUncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemployment

{kind=link}

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex