Futures Slide After Fed "Not-Dovish-Enough", Tech Tumbles On Reflation Rotation FearsTyler DurdenThu, 09/17/2020 - 08:08

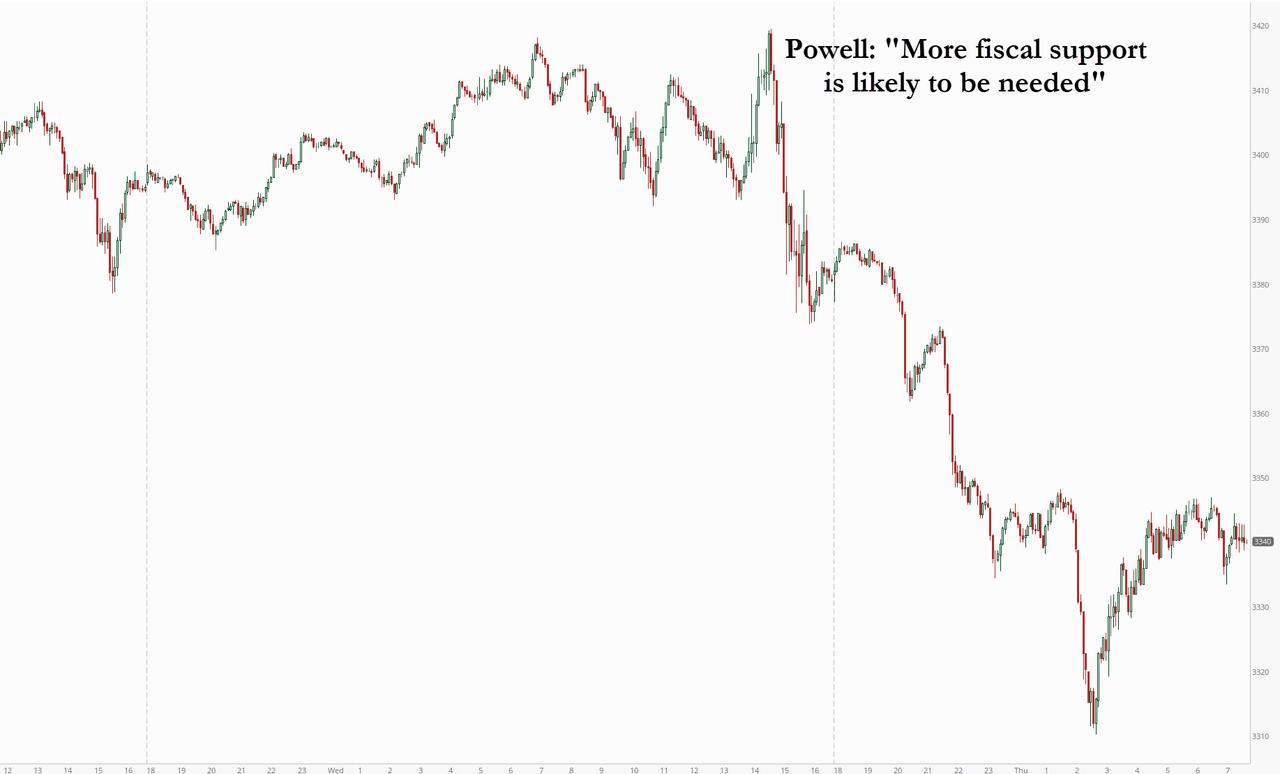

It all started just before 3pm on Wednesday, when during his press conference, Fed chair Jerome Powell said that "more fiscal support is likely to be needed", sparking concerns that the Fed's monetary toolkit is running dry and that the next move will be a massive $1.5+ trillion fiscal injection from Congress (not surprisingly, Trump also flipped yesterday and advised Senate republicans to agree with Democrat demands for "much higher numbers." It also launched a cascade of complaints that the Fed was "not dovish enough" (just as we warned would happen), and as JPM said "there may be increasing calls for the Fed to do more" as the stocks are now habituated to a Fed that constantly caters to their every whim.

What happened next was that stocks, which had just hit session highs just before Powell's statement, tumbled led by tech names on fears a "growth to value" reflation rotation was imminent should Congress kickstart inflation. Emini futures continued to selloff all night, and dropped as much as 100 points sliding as low as 3,310 before rebounding modestly once Europe reopened.

"The market was probably hoping for something more tangible on QE," said Chris Chapman, a portfolio manager at Manulife Investment. "But overall this should be supportive for risk assets longer term."

Jitters persisted on Thursday when investors braced for data expected to show persistently high levels of weekly jobless claims: the Labor Department’s weekly Initial Claims report, due at 8:30 a.m. ET, was expected to show about 850,000 Americans filing for unemployment benefits in the week ended Sept. 12, a touch lower than 884,000 in the previous week, but still suggesting the labor market’s recovery from the COVID-19 pandemic was stalling. On Wednesday, in justifying the need for trillions in fiscal stimulus, Powell also indicated a long road to "maximum employment" and said the central bank was limited in its capacity to address some of the gaps around wage growth and workforce participation.

As futures dropped, so did Treasury yields, which hammered the big U.S. banks including Goldman Sachs Group, Bank of America Corp, Citigroup and Wells Fargo all of which fell about 1% in thin premarket trading. Carnival dropped 3.8% after its British cruiseline P&O Cruises extended a cancellation in sailings until early 2021. Other cruise operators such as Royal Caribbean Cruises and Norwegian Cruise Line Holdings shed about 2%. On Wednesday, the Nasdaq 100 Index fell 1.7%; Facebook’s 3.3% drop was among the worst amid reports about a potential FTC antitrust lawsuit and more user boycotts; Apple closed down 3%.

It wasn't just US futures: global equities were in retreat after the Fed's last policy decision before the US presidential election on Nov. 3 (the next Fed meeting is on Nov 5). In Europe, the Stoxx 600 Technology index declined as much as 2%, among the worst-performing subgroups on the wider benchmark, after U.S. tech giants dropped late Wednesday amid regulatory scrutiny and after the abovementioned Fed disappointment. ASML, SAP and Infineon are the biggest contributors to the sector drop, all down more than 2%. Elsewhere, European automakers slumped after data showed European car sales plunged by nearly a fifth in August. U.K. retailers today warned of grim signs for the economy.

Earlier in the session, Asian stocks also fell, led by materials and IT. All markets in the region were down, with Hong Kong's Hang Seng Index dropping 1.6% and Australia's S&P/ASX 200 falling 1.2%. The Topix declined 0.4%, with Diamond Electric Holdings and Shin Nippon Bio falling the most. The Shanghai Composite Index retreated 0.4%, with KraussMaffei and Beijing Dahao Technology posting the biggest slides.

And so, in a world that is now centrally-planned by a handful of clueless technocrats, all eyes remain on central bankers and their role in propping up economies, pardon markets. Cable tumbled after the Bank of England surprised traders when it said they were exploring negative rates to counter ongoing risks to the labor market after voting unanimously to maintain their key interest rate at 0.1%. Earlier the Bank of Japan kept its asset-purchases and bond-yield targets in place.

In FX, the Bloomberg Dollar Spot Index steadied after giving back Asia session gains. The Aussie edged lower after earlier rallying following a strong jobs report. Scandinavian currencies slipped amid a declines in European equities and a dip in oil prices. The yen led G-10 gains against the dollar, with the USDJPY sluiding below 105 overnight.

Elsewhere, weakness spread to commodities as WTI crude oil slipped to around $40 a barrel. Gold declined.

Looking at today's session, South Africa is expected to cut rates while initial jobless claims in the US are forecast to decelerate. Other data include housing starts and the Philadelphia Fed business outlook. The U.S. sells 4-week and 8-week bills and a 10-year TIPS auction re-opens.

Market Snapshot

S&P 500 futures down 1.1% to 3,351.25

STOXX Europe 600 down 0.8% to 370.30

MXAP down 0.8% to 173.19

MXAPJ down 1% to 568.14

Nikkei down 0.7% to 23,319.37

Topix down 0.4% to 1,638.40

Hang Seng Index down 1.6% to 24,340.85

Shanghai Composite down 0.4% to 3,270.44

Sensex down 0.6% to 39,054.39

Australia S&P/ASX 200 down 1.2% to 5,883.22

Kospi down 1.2% to 2,406.17

Brent Futures down 0.6% to $41.98/bbl

Gold spot down 0.8% to $1,944.21

U.S. Dollar Index down 0.02% to 93.19

German 10Y yield rose 1.4 bps to -0.47%

Euro down 0.09% to $1.1805

Brent Futures down 0.6% to $41.98/bbl

Italian 10Y yield fell 3.0 bps to 0.763%

Spanish 10Y yield rose 3.0 bps to 0.291%

Top Overnight News from Bloomberg

The ECB offered lenders another round of capital relief to help them maintain the flow of credit to the virus-struck economy

Bank of England policy makers have the opportunity on Thursday to signal to investors and economists whether they’re right to predict more monetary stimulus this year

After meeting Conservative MPs who were threatening to rebel against him, Boris Johnson agreed to give the House of Commons a veto over whether the government can exercise its proposed powers to override parts of the Brexit divorce treaty

European car sales plunged by nearly a fifth in August, dashing hopes that the industry was starting to recover from the pandemic

The ECB has to continue providing “ample” stimulus to support the pandemic- scarred euro-area economy, Governing Council member Olli Rehn said

Asian equity markets traded subdued as the soured mood rolled over into the region following the uninspiring finish on Wall St where the major indices whipsawed post-FOMC. At the meeting, the Fed kept rates at 0.00%-0.25% as expected, left its asset purchase schedule and median FFR dot plot forecasts unchanged, while it guided that it expects to maintain an accommodative stance of monetary policy until its goals of maximum employment and inflation at the rate of 2% over the longer run are achieved, which initially boosted risk appetite on the prospects that rates are to remain low for the years ahead. However, stocks then faltered during Fed Chair Powell’s press conference, where despite there being no specific trigger headline, he did suggest the pace of the recovery would slow and that the lack of fiscal aid will eventually hurt the economy, while the dot plots had earlier showed that some policymakers viewed a lift off in 2022 and 2023. As such, ASX 200 (-1.2%) and Nikkei 225 (-0.7%) were weaker as tech stocks succumbed to the underperformance of the sector stateside and with Tokyo trade lacklustre due to adverse currency effects, as well as tentativeness amid the BoJ policy announcement which failed to spark off any major fireworks as the central bank kept policy settings unchanged and although it upped its assessment of the economy, exports and output, this was widely anticipated. Hang Seng (-1.6%) and Shanghai Comp. (-0.4%) were also negative after the PBoC drained liquidity from the interbank market and as participants await TikTok’s fate with President Trump to review the deal on Thursday morning but noted that he doesn't like that the US part of TikTok would not be sold to Oracle, while reports had also suggested that the proposal did not address US government security concerns. Finally, 10yr JGBs were flat with price action stuck once again at the 152.00 focal point and with a non-committal tone seen after the BoJ policy announcement proved to be a damp squib.

Top Asian News

ByteDance Rival Kuaishou Said to Mull $5 Billion Hong Kong IPO

Adelson Casino Hires Lawyer to Probe $1 Billion in Transfers

Australian Employment Rose 111,000 in Aug.; Est. 35,000 Decline

Virus Cases at Dorms Add to Singapore Construction Woes

Stocks in Europe remain in negative territory but have nursed some losses since the cash open (Euro Stoxx 50 -0.8%), in a continuation of the post-Fed global stocks slide. European bourses see broad-based losses with Italy’s FTSE MIB (-1.2%) modestly underperforming given its exposure to banks – with the sector weighed among the laggards, whilst Telecom Italia (-2.5%) resides at the foot of the Italian index after the EU regulator said it is likely to oppose Italy's plan to create a single national broadband network. Back to sectors, material names are also pressured amid the USD-induced slide in base metal prices, subsequently cushioning losses for the industrial sector. In terms of individual movers, LSE (-1%) shares trade lower as Deutsche Boerse (-0.6%) and Six gear up to submit their bids for LSE’s Borsa Italiana, with reports stating that the exchanges reportedly launched a charm offensive to win the backing of Italian officials. Richemont (-1.6%) and Swatch (-0.9%) are pressured amid another MM contraction in Swiss watch exports; separately, European auto names see broad losses after dismal EU new car registration figures. On the flip side, Next (+6.1%) is among the top gainers in the region post-earnings after raising guidance, after which the CEO suggested profit would be resilient in the event of another national lockdown.

Top European News

Europe Autos Index Declines After August Car-Market Setback

German Coal-Plant Profit Jumps as Hot Weather Boosts Demand

Unibail Raising $4 Billion as Covid Batters Mall Owners

Rehn Sees Consequences For ECB Policy From Fed’s Goal Change

In FX, the Yen is back in the ascendency after conceding ground to the Dollar in wake of Fed and BoJ policy meetings, with Usd/Jpy briefly back above 105.00 before reversing to fresh September lows around 104.70. In truth, there was little new or unexpected from either Central Bank, but the former did upgrade its 2020 outlook and another tech-related retreat in US stocks exacerbated the broad Buck bounce that boosted the index beyond 93.500 at one stage. However, the DXY is already fading fast within a 93.614-93.140 range and the Yen has reclaimed safe-haven status following the Nikkei’s overnight decline and a degree of re-flattening along the Treasury curve. At this stage, hefty option expiry interest at the 105.00 strike (1.9 bn) may be losing influence, but could yet come back into play pending US housing data, IJC and the Philly Fed survey.

CAD/NZD/GBP - All unwinding more of their pre-FOMC gains relative to the Greenback, as the Loonie extended its post-Canadian CPI downturn towards 1.3250, the Kiwi briefly relinquished 0.6700+ status in wake of Q2 NZ GDP confirming a technical recession, albeit not quite as contractionary as expected and Sterling failed to sustain momentum through 1.3000 in the run up to the BoE at midday (full preview of the event available via the Research Suite).

CHF/AUD/EUR - Not much to be gleaned from Swiss trade that revealed a moderately wider surplus, but the Franc is trying to pare losses below 0.9100 against US Dollar and the Aussie is revisiting 0.7300 after holding just above 0.7250 and 1 bn expiries between 0.7240-35, with some underlying support via a significantly better than forecast jobs report. Elsewhere, the Euro has retested 1.1800+ from sub-1.1750 lows, but looking hampered by decent expiry interest at the round number and from 1.1845 to 1.1855 in 1 bn and 1.5 bn respectively, with little independent impetus from final Eurozone inflation data or ECB commentary.

SCANDI/EM - Bearish risk sentiment and a pull-back in oil prices are weighing on the Sek and Nok, but the Try and Rub are also feeling increased investor angst over diplomatic issues as the Lira slides to new all time lows beneath 7.5000 and the Rouble is back under 75.0000. Similarly, the Zar is on the backfoot pre-SARB and Brl look set for corrective losses even though the BcB held the Selic rate at 2% as widely anticipated.

In commodities, WTI and Brent front month futures are attempting to nurse overnight losses which were induced by the sentiment deterioration post-Fed, alongside a firmer Dollar heading into today’s JMMC meeting due to commence at 1300BST/0800ET. In terms of the findings from yesterday’s JTC meeting, the OPEC+ panel sees initial signs of a decline in oil inventories and noted that the increase in COVID-19 cases may weigh on economic recovery and oil demand – comments that are in-line with the OPEC MOMR which stated that risks remain elevated and skewed to the downside, particularly in relation to the development of COVID-19 infection cases and potential vaccines. JMMC focus will fall on any commentary surrounding the recent oil price decline and demand outlook alongside compliance. Separately, in the Gulf of Mexico, Sally has weakened to a tropical storm but is still producing torrential rains, according to the NHC WTI Oct meanders around USD 40/bbl (vs. low 39.42/bbl) while its Brent counterpart hovers around USD 42.00/bbl (vs. low 41.50/bbl). Elsewhere, precious metals remain subdued by the USD in the aftermath of the FOMC, with spot gold flatlined throughout the European morning sub-USD 1950/oz (vs. overnight high 1960/oz), whilst spot silver surrendered its USD 27/oz status. In terms of base metals, LME copper also succumbs to the Dollar strength and broader losses in the stock markets, whilst Dalian iron ore futures dipped to the lowest level in over six weeks amid the USD’s movements and the growing prospect for further supply improvements, whilst steel demand in China was not as strong as some had expected.

US Event Calendar

8:30am: Initial Jobless Claims, est. 850,000, prior 884,000; Continuing Claims, est. 13m, prior 13.4m

8:30am: Housing Starts, est. 1.48m, prior 1.5m; Housing Starts MoM, est. -0.91%, prior 22.6%

8:30am: Building Permits, est. 1.51m, prior 1.5m; Building Permits MoM, est. 1.96%, prior 18.8%

8:30am: Philadelphia Fed Business Outlook, est. 15, prior 17.2

DB's Jim Reid concludes the overnight wrap

Did the Fed glow last night? Well the initial market reaction was positive as the Fed verbally formalised their extended accommodation. However markets turned during Powell’s press conference. More on that later. As was universally expected, the committee signalled rates would remain near zero through 2023 while keeping QE, through Treasury and MBS purchases, at its current rate. In a slightly dovish development there were only two dissents and only one Fed official supporting rates rising before 2023. As was signalled at Jackson Hole the committee “expects to maintain an accommodative stance of monetary policy” until it achieves inflation averaging 2% over time and longer-term inflation expectations remain anchored at 2%. Therefore, it is noteworthy that in the Summary of Economic Projections inflation is only anticipated to reach 2.0% in 2023, indicating that even with average inflation targeting the committee is not expecting inflation to overshoot until sometime after that date. For more, please see our US economics team’s full review here.

In terms of the overall economy, Chair Powell acknowledged that “the recovery has progressed more quickly than generally expected,” but did caution that the recent pace may slow as “the path ahead remains highly uncertain.” Within their SEP forecasts, they are essentially projecting the economy to reach Q4 2019 pre-covid levels by the end of 2021. The Chair once again stated that further fiscal stimulus would be needed to further support the recovery.

Prior to the FOMC, we got another flurry of fiscal news out of the White House, with the President’s Chief-of-Staff Meadows saying the administration was open to the $1.5 trillion bi-partisan compromise proposed by moderates in the House. This deal is far higher than what Senate Republican leaders have said they would support, with second-ranking GOP senator Thune saying that stimulus of that size would cause “a lot of heartburn” in his caucus. Speaker Pelosi and Senate Minority Leader Schumer were said to be “encouraged” by Trump’s endorsement of higher spending, though the negotiating window gets tighter the closer this drifts into the heart of election season for the President and lawmakers alike.

Prior to the policy decision and Chair Powell’s news conference, risk assets were trading slightly higher with the S&P 500 up +0.5%, climbing to +0.8% in the first few moments of the press conference before dropping around 1% as the chair spoke. Following the whipsaw, the index finished the session -0.46%. Tech in particular drove much of the selling, with the NASDAQ falling -1.25% on the day. While the broad index lagged there was a clear move into cyclical sectors as Financials (+1.01%), Energy (+4.04%) and Industrials (+0.99%) stocks finished higher – though energy was helped by rising crude prices as well. The dollar was flat when the committee decision was announced and rose moderately through the rest of the session to finish up +0.18%, but still below last Friday’s closing levels. On the other hand US 10yr Treasury yields rose +3.5bps after the decision to finish +1.8bps higher on the day at 0.697%.

Overnight in Asia, the Bank of Japan decided to maintain its current policy stance as expected, with the statement saying that “Japan’s economy has started to pick up with economic activity resuming gradually”. We should hear more this morning from Governor Kuroda, who’ll be holding a media briefing at 7:30 UK time. Meanwhile Asian equity markets followed the US lower, with the Nikkei (-0.71%), the Hang Seng (-1.59%), the Shanghai Comp (-0.99%) and the KOSPI (-1.30%) all losing ground. S&P 500 futures are also pointing to a weak session, and are currently -1.07% lower.

Attention will remain on central banks following the Fed and the BoJ, with the Bank of England announcing their latest decision at noon UK time. In terms of what to expect, our UK economist expects both rates and QE will remain on hold at this meeting, but there’s a big chance that today’s decision won’t be unanimous. Our base case is that there’ll be a further £60bn top-up to the QE program in December, though risks are rising that this might be announced slightly earlier at the November meeting. The meeting comes against the backdrop of rising Brexit uncertainty, which will only serve to heighten uncertainty and weaken confidence. Brexit wasn’t mentioned once in the minutes of the August meeting, but it’ll be interesting to see if this changes. Yesterday also saw a notable fall in CPI inflation to +0.2% in August (from +1.0% in July), which was its lowest level since December 2015, though it was a bit higher than the consensus expectation for a 0.0% reading. That fall was supported by the government’s Eat Out to Help Out Scheme, which offered a discount when eating out, along with a fall in air fares.

On the coronavirus, it was a mixed bag of news yesterday. On the positive side, it was reported that the illness which caused the pause in the Oxford vaccine trial was unlikely to be linked to the shot, according to documents that were sent to participants. Nevertheless, we got conflicting timetables as to when a vaccine might be available in the US. The director of the CDC, Robert Redfield, suggesting that “we’re probably looking at late second quarter, third quarter 2021” in terms of availability to the public, though the deputy chief of staff for policy at the Department of Health and Human Services said every American should be able to get one by the end of March. Dr Fauci then later said it was possible but tough to vaccinate everyone by April, and it was more likely there’d be broad access by the middle or end of 2021. This was all before President Trump then said a vaccine could be distributed as early as October, well ahead any of the previous timelines. Vice President Pence then said the administration’s goal is to have 100 million vaccine doses available by year-end.

Meanwhile the number of cases in Western Europe continued to rise, with the UK reporting a further 3,991 cases yesterday, which was the highest number of confirmed cases since May 8. And over in France, weekly cases have now exceeded 60,000 for the first time, compared to the April peak of just over 40,000 cases per week, albeit on lower testing levels. Optically new cases are likely to rival the first wave in many places over the next few weeks but it’s not really a fair comparison. It won’t stop it being made though. Weekly cases in the US have ticked higher over the past few days as well, with over 277,000 newly confirmed cases since last Wednesday compared to 242,000 weekly cases for the period prior. One place to keep an eye on is Wisconsin, a swing state that was very close in 2016 and in which both Mr Trump and Mr Biden are spending quite a lot of resources. The state has seen new cases double in the last week and are currently seeing their highest absolute levels since the start of the pandemic.

Ahead of the Fed’s decision, European markets saw a variable performance yesterday. While the STOXX 600 climbed +0.58% to reach a 3-week high, that was in spite of declines in the UK, where the FTSE 100 (-0.44%) moved lower after paring back its gains from the start of the session. Oil continued its recovery however, with Brent crude up +4.17% to $42.22/bbl, while WTI also rose +4.91%. Finally in the fixed income space, sovereign bonds also performed positively, with yields on 10yr bunds (-0.5bps), OATs (-1.2bps) and BTPs (-2.9bps) all fell.

Looking at yesterday’s other data, the main highlight came from the US retail sales figures. They underperformed expectations, with a +0.6% rise in August (vs. +1.0% expected), as the previous month was revised down three-tenths to +0.9%. Otherwise, the NAHB housing market index rose to a record 83 (vs. 78 expected). Finally, the OECD upgraded their global growth projection for this year, now seeing a smaller contraction in the global economy of -4.5%.

To the day ahead now, and the highlights will include the aforementioned Bank of England decision, as well as monetary policy decisions from the South African Reserve Bank and Bank Indonesia. In terms of central bank speakers, we’ll also hear from the ECB’s de Guindos, Rehn and Muller. On the data front, today’s releases from the US include August’s housing starts and building permits, the weekly initial jobless claims, along with the Philadelphia Fed’s business outlook for September. Meanwhile in Europe, there’s the EU27 new car registrations for August and the Euro Area’s final CPI reading for August.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}