Uncategorized

Futures Rise On First Trading Day Of 2023 But Far From Record High Hit Year Ago Today

Futures Rise On First Trading Day Of 2023 But Far From Record High Hit Year Ago Today

US stock futures rose on the first trading day of 2023,…

Share this:

US stock futures rose on the first trading day of 2023, with some of the most beaten down and shorted stocks and sectors outperforming, as optimism crept - however briefly - into the market on the one-year anniversary of the S&P 500’s last record high. Contracts on the S&P 500 climbed as much as 1.1% before fading much of their earlier gains. One year ago, the S&P closed at 4,796.56: since Jan. 3, 2022, the US stock benchmark endured its biggest annual decline since the global financial crisis, ending the year down 19%. Nasdaq 100 futures rose 0.6% Tuesday. The dollar jumped as the euro tumbled, while Treasuries were headed for their strongest start to a year in more than two decades as investors scooped up government debt on wagers the Federal Reserve will further slow its pace of rate hikes.

Stocks that were among last year’s worst performers rise in the first US premarket trading session of the new year, with riskier names like meme stocks, cryptocurrency-related shares and electric- vehicle makers gaining amid a return in risk appetite and renewed optimism over China’s reopening. However, not all beaten down names jumped: Tesla fell 3.8% after the electric-car maker delivered fewer vehicles than expected. Analysts noted that the company is facing significant demand issues as it ramps up production capacity and offers hefty incentives in of its two biggest markets. Here are some other notable premarket movers:

- Chinese stocks rose in US premarket trading amid signs that Covid infections in China may have peaked, boosting optimism over the nation’s reopening.

- Gilead Sciences is downgraded to sector perform from outperform at RBC Capital Markets as the broker says it will take time to gain more definitive visibility on the next sets of potential drivers.

- Mondelez International was downgraded to sector perform from outperform at RBC Capital Markets, with the brokerage saying that it is now difficult to justify further upside to EPS estimates as the macro environment weakens.

Stocks are set to gain at the open despite concern that the Fed's interest rate increases will cause the economy to slow significantly in 2023, if not contract. The Big Short Michael Burry said on Twitter late Sunday that the US this year is likely to be “in recession by any definition”, in other words, Powell will be able to declare mission accomplished. Optimists are counting on inflation to slowly cool even as the labor market remains strong. Some pressure eased in the final months of 2022 as Fed officials pointed to a less-aggressive tightening path, while China’s exit from its Zero Covid policy also helped sentiment.

“The Fed has pushed up rates well into restrictive levels and has signaled a willingness to go further,” said Rajeev De Mello, a global macro portfolio manager at GAMA Asset Management, who’s cautious on US stocks. “I would become more comfortable with US equities when we are closer to a pause. Even after the 2022 decline, some US equities still trade at high valuations.”

“Hopes that supply chain issues in China will continue to ease, which could help bring down inflation, may be feeding into sentiment,” said Susannah Streeter, senior investment and markets analyst at Hargreaves Lansdown. Traders are “seizing onto glimmers of hope that once the winter waves die down, China’s recovery could be back on track.”

In Europe the Stoxx 50 rallied as much as 1.4% before fading some gains after a surprise drop in German unemployment signaled resilience in the region’s biggest economy; FTSE 100 outperforms, higher by 1.5% on the day. Travel and leisure and tech stocks led gains while defensive sectors including utilities and telecoms underperformed. Here are some of the biggest European movers:

- UK stocks outperformed as the London Stock Exchange reopened following Monday’s New Year holiday. Domestic-focused shares, which slumped last year, rose, with homebuilders Barratt Developments and Persimmon up at least 4% and banks Lloyds and NatWest up at least 2%.

- Travel stocks rose, with TUI up as much as 6.6% and carrier IAG up as much as 5.6%. Strong pricing power driven by the reopening of Asian and trans-Atlantic routes is one of the multiple catalysts that should benefit European long- haul carriers in 2023, according to Citigroup.

- AstraZeneca and Novo Nordisk both rose more than 2% after JPMorgan said the firms were its most favored in the European pharma-biotech sector alongside Merck KGaA.

- Brenntag shares rose as much as 6% after the German chemicals distributor said it was no longer proceeding with discussions to potentially acquire US rival Univar Solutions.

- Zalando shares rose as much as 4.3%, touching the highest since June, after Hauck & Aufhaeuser predicted the company would remain a winning platform in European online fashion.

- Aker Carbon Capture gained as much as 13% after it signed a Letter of Intent for the delivery of two Just Catch units for an undisclosed European customer.

- Fresenius Medical Care fell as much as 5.2% after JPMorgan flagged “significant” risks to estimates for the dialysis provider in the near term in a review of the European medtech sector. The shares were also downgraded at Jefferies, while parent Fresenius SE was upgraded.

- Gaztransport & Technigaz fell as much as 7.7% after the French maker of cargo containment systems for liquefied natural gas said it’s ceasing activities in Russia.

Earlier in the session, Asian stocks erased an initial decline, spurred by a rebound in Chinese equities as traders assessed peaks in China’s Covid-19 infections and the outlook for the economy. The MSCI Asia Pacific ex-Japan Index was 0.2% higher, reversing a drop of as much as 1.5% and poised for a third straight daily gain. Chinese stocks listed in Hong Kong had their best start to a year since 2018 as subway use recovered in nearly a dozen major cities. A decline earlier in the day in Chinese stocks was triggered by weak manufacturing for December as well as tourism data for the New Year holiday.

“While it is inevitable to see further surges and more widespread infections at the initial stage of opening, the outlook for the Chinese economy has brightened for 2023,” Saxo Capital Markets strategists wrote in a note. China’s renewed support for private enterprise and the property sector, and an improved credit impulse mean “Hong Kong and mainland Chinese equities have a more positive tendency,” they added. Korea’s Kospi gauge fell to a two-month low as local funds sold tech stocks such as Samsung amid worries about the earnings outlook. Japan and New Zealand were closed for a holiday. After a dismal 19% slide in 2022, strategists are expecting the MSCI Asia Pacific Index to outperform US peers this year with a stronger rebound in the second half. China’s full reopening, a pivot in Fed policy and an end to the chip downcycle are among the positive catalysts seen to outweigh a slowdown in global growth.

Indian stocks rose for a second straight session, helped by gains in lenders after most banks reported strong growth in credit offtake for the previous month. Gains in local shares tracked most Asian peers, with Chinese equities rallying as traders assess the outlook for economic recovery on signs of Covid peaking in some cities. The S&P BSE Sensex rose 0.2% to 61,294.20 in Mumbai, while the NSE Nifty 50 Index was higher by a similar measure. Fifteen out of BSE Ltd.’s 20 sector sub-indexes advanced, led by consumer durables makers. Axis Bank and HDFC Bank were the key gainers among Sensex’s 30 companies, 17 of which ended higher, while the rest declined. Tata Consultancy Services led the gains in software companies. Reliance Industries fell after the Indian government revised windfall tax on domestic crude and diesel exports higher.

In Australia, the S&P/ASX 200 index fell 1.3% to close at 6,946.20, its lowest since Nov. 7. All sectors dropped on the benchmark’s first trading day of the year, with banks and miners contributing the most to its decline. In New Zealand, the market was closed for a holiday.

In FX, the Bloomberg dollar spot index rallied by as much as 0.9% as the greenback strengthened against all Group-of-10 peers save the Japanese yen. The JPY is the only G-10 currency that’s up against the dollar. NZD and AUD underperform. The yen briefly reversed gains against the dollar in early European trading before resuming its advance; the Japanese currency advanced to a six-month high in the Asian session after an initial bout of stop-loss selling through a key technical level was followed by momentum buying against the dollar and euro. Front-end volatility in the majors is better bid as the new year kicks off, with the yen being at the forefront of traders’ attention. The euro fell by as much as 1.3% to a three-week low of 1.0534 following some weaker than expected German inflation prints. The Australian and New Zealand dollars flipped to gains amid signs that Covid cases in major Chinese cities may have peaked. Positive comments toward Americans from China’s Foreign Minister Qin Gang also lifted risk sentiment

In rates, Treasuries traded sharply higher, outperforming core European rates with yields as much as 11bp richer on the day across intermediates vs Friday’s closing levels. US 10-year yields around 3.765%, richer by 11bp on the day and outperforming bunds and gilts by 6bp and 3bp; belly-led gains richen 2s5s30s Treasuries fly by 4.2bp vs Friday’s close while 2s10s curve flattens ~4bp. Gilts and Treasuries yields across the curve decline, led by the 10-year yields, each down about 13bps. Comparative bunds underperform, declining some 8bps. There is no fresh catalyst for the first trading day of the year, as investors look to fade current rate-hike premium priced into front-end. In Europe, Treasury and bund curves bull-flattened while money markets eased Fed and ECB tightening wagers after German regional inflation figures signaled slowing inflation. Fed-dated swaps price Fed peak rate at around 4.95% by June meeting, down from 4.98% at Friday’s close.

In commodities, oil declined under pressure from a stronger dollar, reversing earlier gains. European gas prices slid as a warmer-than-expected start to winter across large parts of the world rapidly have eased fears of a natural gas crisis. Most base metals trade in the green. Spot gold rises roughly $12 to trade near $1,836/oz.

In crypto, bitcoin traded flat, just below $17K. Sam Bankman-Fried is expected on Tuesday to enter a plea of not guilty to criminal charges that he cheated investors and looted billions of dollars at his now-bankrupt FTX cryptocurrency exchange, according to a source cited by Reuters.

Today's calendar is relatively quiet with just S&P Global Manufacturing PMI and US Construction spending on deck.

Market Snapshot

- S&P 500 futures up 1.1% to 3,902.00

- MXAP up 0.6% to 156.64

- MXAPJ up 0.3% to 507.14

- Nikkei little changed at 26,094.50

- Topix down 0.2% to 1,891.71

- Hang Seng Index up 1.8% to 20,145.29

- Shanghai Composite up 0.9% to 3,116.51

- Sensex little changed at 61,227.58

- Australia S&P/ASX 200 down 1.3% to 6,946.19

- Kospi down 0.3% to 2,218.68

- STOXX Europe 600 up 1.8% to 436.53

- German 10Y yield little changed at 2.38%

- Euro down 1.1% to $1.0549

- Brent Futures up 0.5% to $86.30/bbl

- Gold spot up 0.9% to $1,840.74

- U.S. Dollar Index up 1.03% to 104.59

Top Overnight News from Bloomberg

- German unemployment unexpectedly fell in December. Joblessness dropped by 13,000 in December, the Federal Labor Agency said in a statement on Tuesday. All 15 economists surveyed by Bloomberg anticipated an increase. The unemployment rate was 5.5%, also better than expected

- British rail workers will walk off the job much of this week, paralyzing transport and adding to the troubles piling up for Prime Minister Rishi Sunak’s government

- A warmer-than-expected start to winter across large parts of the world is rapidly easing fears of a natural gas crisis that had been predicted to trigger outages and add to pressure on power bills

- Nearly a dozen major Chinese cities are reporting a recovery in subway use, a sign that an ‘exit wave’ of Covid infections may have peaked in some urban areas

- Official Chinese data over the weekend showed the decline in manufacturing worsened last month, while activity in the services sector plunged the most since February 2020. Separately, a private survey of businesses by China Beige Book International on Monday suggests the economy contracted in the fourth quarter from a year earlier

- Turkey’s consumer prices rose an annual 64.3% in December, down from 84.4% the previous month, according to data released by state statistics agency TurkStat on Tuesday. The median forecast of economists surveyed by Bloomberg was 66.7%

A more detailed look at global markets courtesy of Newsquawk

Stocks in Asia were a mixed bag (Japan and New Zealand are away from market). ASX (-1.3%) is the laggard whilst Chinese bourses are on a firmer footing (Shanghai Comp +0.8%, Hang Seng +2.1%). Weekend developments focused around China's NBS PMIs, with the official NBS manufacturing PMI dropping to 47.0 (exp. 48.0) in December from 48.0 in November, the largest monthly decline since the start of the pandemic in February 2020, and remaining below the neutral 50-mark for the third consecutive month. Reuters notes that the data gives the first glimpse of the manufacturing sector after China removed its COVID restrictions in early December. Meanwhile, the Caixin version of the manufacturing PMI declined to 49.0 in December (exp. 48.8, prev. 49.4). EU Health Commissioner Kyriakides has reportedly contacted China offering variant-adapted EU vaccine donations alongside public health expertise, via FT citing sources which add China has not responded yet. IMF chief Georgieva said one-third of the global economy will be hit by recession this year, and 2023 will likely be tougher for the world economy than the previous 12 months.

Top Asian News

- Evergrande Vows Debt Payment After Restructuring Delay

- Samsung Veteran Sounds Alarm on Korea Losing Global Chip War

- Copper Advances as Chinese Stimulus Eyed After Poor Factory Data

- Garuda Shares Fall as Trading Resumes After Debt Restructuring

- Marcos Seeks to Move China Ties to ‘Higher Gear’ in Trip

- More Flight Delays as Philippine Airport Reels From Glitch

European bourses are firmer across the board, Euro Stoxx 50 +1.4%, as the region's strong start to 2023 continues. Post-APAC individual developments have been somewhat limited and primarily focused on Chinese PMIs and USD action. Stateside, futures are firmer across the board with the ES back above 3900 ahead of the week's risk events from Wednesday onwards. TikTok owner ByteDance has cut hundreds of jobs at multiple departments in China, according to SCMP sources; the job reductions came after the CEO told employees in December that the company needs to ‘get fit and beef up the muscle’ to streamline operations.

Top European News

- European Stocks Extend Recovery on China as Traders Await Data

- UK Stocks Outperform, Catching Up With Europe After Holiday

- Genus, Scor, Aroundtown, Royal Unibrew Short Sellers Active

- Bulgaria Starts New Bid to Form Coalition as Snap Elections Loom

FX

- Dollar erases and reverses losses on positional, fundamental and technical grounds

- DXY picks off late December peaks within 103.460-104.820 range, Yen retreats after testing multi-month peaks vs Buck in holiday-thinned trade overnight, USD/JPY back on 130.00 handle from circa 129.51 low

- Kiwi and Aussie unable to evade Greenback revival with NZD/USD eyeing 0.6200 and AUD/USD probing 0.6700 vs 0.6360+ and 0.6830+ highs

- Euro deflated by sub-consensus German state CPIs ahead of prelim. national data

- EUR/USD towards bottom of 1.06830-1.0526 band and Pound unable to benefit from upward revision to final UK manufacturing PMI, Cable closer to 1.1900 than 1.2100

Fixed Income

- Bunds boosted by softer than forecast German regional inflation reports as stops are triggered between 133.79-135.55 parameters

- Gilts catch up and carry on after the extended UK New Year break as 10 year bond hits 101.66 from 99.97 low and 99.90 prior close

- T-note climbs without cash-backing to 113-02 from 112-12+ ahead of final US manufacturing PMI and construction spending data

Commodities

- Crude benchmarks have come under modest pressure as the European morning progresses, with the benchmarks currently lower by circa. USD -0.70/bbl having more than retracted a concerted bid that occurred around the European cash equity open.

- Spot gold and silver are firmer despite the mentioned USD strength with Chinese data points perhaps proving favourable for the traditional haven. Albeit, the yellow metal has retreated from a USD 1850/oz peak.

- Base metals are supported despite the China metrics as the overall tone remains constructive amid a relatively thin docket to start a particularly busy week.

- Indian gov't is reportedly considering selling 2.1mln/T of wheat, with a decision due in the next 10-days, via Reuters citing sources.

- Chinese Foreign Ministry says some nations restrictions on Chinese travellers lack scientific basis and are unreasonable; will take corresponding measures accordingly.

US Event Calendar

- 09:45: Dec. S&P Global US Manufacturing PM, est. 46.2, prior 46.2

- 10:00: Nov. Construction Spending MoM, est. -0.4%, prior -0.3%

Uncategorized

The most potent labor market indicator of all is still strongly positive

– by New Deal democratOn Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently…

Share this:

- by New Deal democrat

On Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently than not indicated a recession was near or underway. But I concluded by noting that this survey has historically been noisy, and I thought it would be resolved away this time. Specifically, there was strong contrary data from the Establishment survey, backed up by yesterday’s inflation report, to the contrary. Today I’ll examine that, looking at two other series.

Uncategorized

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

US futures are trading modestly in positive territory and just shy of…

Share this:

US futures are trading modestly in positive territory and just shy of all time highs, after swinging between gains and losses as Europe trades higher and Asia closed weaker after US markets shrugged of a higher core CPI print and focused on the more constructive disinflation components (Super core 47bps vs 85bps). As of 7:50am, S&P futures traded +0.1% while Nasdaq futures were modestly red; earlier, Germany's DAX hit 18K for first time, while EuroStoxx50 hit 5K for first time in 24 years.

Overnight newsflow was relatively quiet outside of early results from Japan’s wage negotiations which showed majority of companies agreeing to unions demands: previously, BOJ's Ueda said wage negotiations were critical in deciding when to phase out its big stimulus program while Japan PM Kishida noted in Parliament that Japan has not emerged out of deflation, pushing back some expectations of BOJ exiting negative rates next week. UK Jan Industrial Production printed softer, Jan GPD/Manf Production in-line, and EZ Industrial Production printed weaker as well. Donald Trump clinched the Republican presidential nomination, setting up a combative election race with President Joe Biden. Elsewhere, US TSY 10Y yields are trading 1bp higher at 4.17% while bond yields across Europe ticked lower; the Bloomberg dollar index is fractionally lower, WTI crude is +$1.05 at $78.65, and bitcoin just hit a new all time high above $73,000.

In premarket trading, Nvidia shares rose again after the chipmaker rallied 7.2% and added $153 billion in market value on Tuesday. Tesla slipped after Wells Fargo downgraded the stock to underweight from equal-weight. Dollar Tree slumped after reporting fourth-quarter sales and profit that missed Wall Street’s expectations. The retailer also announced plans to close about 600 Family Dollar stores in the first half of the fiscal year.

- Beauty Health soars 21% after the skin-care company reported fourth-quarter sales that topped consensus estimates. The company named Marla Beck as CEO after a stint as interim CEO that began in November.

- Clover Health rises 9% after the Medicare Advantage insurer reported revenue for the fourth quarter that beat the average analyst estimate.

- Dollar Tree slumps 6% after issuing an annual sales outlook that fell short of the average analyst estimate at the midpoint of the forecast range.

- Eli Lilly rises about 1% after teaming up with Amazon.com Inc. to expand its nascent business of selling weight-loss drugs directly to patients.

- Petco (WOOF) rises 3% after the company reported comparable sales for the fourth quarter that topped the consensus estimate. Petco also said Ron Coughlin has stepped down as CEO/Chairman.

- Tesla (TSLA) falls 2% after Wells Fargo cuts the recommendation on the EV maker’s stock to underweight, saying there are fresh risks to EV volumes as price cuts are not having as much impact as before.

- ZIM Integrated Shipping (ZIM) falls 4% after the marine shipping company reported its fourth-quarter results and gave an outlook.

Traders held onto Fed rate cut bets for this year even after US inflation came in higher than expected on Tuesday. Futures are pricing in nearly 70% odds that the central bank will start easing in June and enact at least three quarter-point cuts over the course of 2024. Policymakers next gather March 19-20, where investors will key into the Federal Open Market Committee’s quarterly forecasts for rates, including whether fresh employment and inflation figures have prompted any changes.

“It’s going to be hard for the Fed not to be hawkish in the next meeting as the fight against inflation clearly isn’t won yet,” said Justin Onuekwusi, chief investment officer at wealth manager St. James’s Place. “That print does make you sit up and be alert of the risk inflation remain stubbornly high and that has massive feed-across right across portfolios. Markets may be underestimating impact of sticky inflation as they are still aggressively pricing a June rate cut.”

European stocks rise with the Stoxx 600 hovering near a record high and the Stoxx 50 breaching 5,000 for the first time in 24 years. Retail shares are leading gains after positive updates from Zalando and Inditex. Utilities and banks also outperform. Here are some of the biggest movers on Wednesday:

- Zalando shares jump as much as 18%, the most in five years, after results that analysts describe as positive, with a beat on adjusted ebit for 2023 and updated targets for growth through 2028. RBC analysts say they are confident in the German company’s ability to capture growth as consumer demand recovers.

- Inditex shares climbed as much as 5.2% to a fresh record high after the Zara parent reported what analysts called strong results thanks to continued robust demand for its clothing collections. The Spanish retailer plans to increase its annual dividend by 28% to €1.54 per share. H&M and the broader retail index also gain.

- BNP Paribas rises as much as 3.4% after the lender forecast higher-than-expected profit and stepped up cost savings measures.

- Balfour Beatty shares gain as much as 10%, its biggest intraday gain since August 2022, after the construction and infrastructure group reported full-year adjusted earnings per share that came ahead of consensus expectations. Additionally, the company announced a share buyback of £100 million for 2024. Liberum noted the strength in the company’s Gammon Construction joint venture, with Jardine Matheson.

- E.On shares jump as much as 7%, most in more than a year, after it reported a positive update according to Jefferies, with outlook ahead of consensus. Company also announced CFO Marc Spieker will assume role of COO and Nadia Jakobi is set to become CFO.

- Keywords Studios shares gain as much as 13%, the most since May 2020, after the company maintained FY goals issued in January, offering reassurance in a video game industry marked by layoffs at bellwethers including Sony and Electronic Arts. Keywords provides external technical support to video-game makers.

- Vallourec shares gain 9.8% after ArcelorMittal said it’s buying a stake in the tubular steel company from Apollo Global Management for about €955 million. Analysts highlight the deal triggers M&A speculation around Vallourec, and Oddo BHF expects ArcelorMittal to launch a takeover bid once the six-month lock-up period expires.

- Adidas shares fall as much as 4.1% as a lack of a full-year guidance upgrade from the sportswear maker disappointed some analysts, even as results were in line with January’s pre-released figures. The focus turns to the German firm’s growth outlook for the first quarter, and whether it will indeed see a pick-up in trading in the second half of the year.

- Solvay drops as much as 5.2% after guidance for lower Ebitda in 2024. Analysts note that the chemicals company’s commitment to a stable or growing divided may offset negatives from falling Ebitda. Investors will focus on the soda ash price assumptions, Morgan Stanley said.

- Geberit falls as much as 4.8% after the Swiss maker of building materials missed earnings estimates. The stock had rallied ahead of the earnings, gaining almost 8% from the start of February through Tuesday.

- Stadler Rail shares fall 3.3% after the Swiss train manufacturer’s sales and operating margins came in lower than estimates. The company’s 2024 outlook also weighs on sentiment, according to Vontobel.

The European Central Bank is also poised to start rate cuts soon, with Governing Council member Martins Kazaks saying on Wednesday reductions could come “within the next few meetings.” Bank of France Governor Francois Villeroy de Galhau said borrowing costs may be cut in the spring, with June more likely than April for a first move.

In FX, the Bloomberg Spot Index slips to reverse modest earlier gains while the yen was the weakest of the G-10 currencies, falling 0.2% versus the greenback to 148.05; the krone led G-10 gains. “BOJ Governor Kazuo Ueda clearly indicated yesterday that wages were the last piece of information needed before the central bank could decide whether to end its negative interest rate policy next week, said David Forrester, a senior FX strategist at Credit Agricole CIB in Singapore. “So the partial tally of the spring wage negotiations this Friday will be a decisive factor for the BOJ and the JPY in the coming week.” The pound was flat.

In rates, treasuries edged lower, with US 10-year yields rising 1bps to 4.16%. Gilts fall after data showed the UK economy rebounded in January. UK 10-year yields rise 2bps to 3.96%. Gilts lag across core European rates as market digests an offering of 30-year inflation-linked debt and a wave of domestic data. US session includes 30-year bond reopening, following soft reception for Tuesday’s 10-year sale. Treasury auction cycle concludes with $22b 30-year bond reopening after $39b 10-year reopening tailed by 0.9bp, while Monday’s 3-year new issue stopped through by 1.3bp. WI 30-year yield at ~4.320% is roughly 4bp richer than February refunding, which stopped through by 2bp in a strong auction

In commodities, oil advanced after four days of losses as an industry report pointed to shrinking US crude stockpiles, offsetting wavering OPEC cuts. WTI rose 1.5% to trade near $78.70. Spot gold adds 0.2%. and trades near all time highs.

Bitcoin rises 3% to a record high above $73,000 with Ethereum (+2.7%) also catching wind.

To the day ahead now, and data releases include UK GDP and Euro Area industrial production for January. Central bank speakers include the ECB’s Cipollone and Stournaras. And in the US, there’s a 30yr Treasury auction taking place.

Market Snapshot

- S&P 500 futures little changed at 5,176.25

- STOXX Europe 600 little changed at 506.38

- MXAP down 0.3% to 176.21

- MXAPJ down 0.3% to 540.31

- Nikkei down 0.3% to 38,695.97

- Topix down 0.3% to 2,648.51

- Hang Seng Index little changed at 17,082.11

- Shanghai Composite down 0.4% to 3,043.84

- Sensex down 1.0% to 72,924.23

- Australia S&P/ASX 200 up 0.2% to 7,729.44

- Kospi up 0.4% to 2,693.57

- German 10Y yield little changed at 2.30%

- Euro little changed at $1.0929

- Brent Futures little changed at $81.99/bbl

- Gold spot up 0.0% to $2,158.75

- US Dollar Index little changed at 102.93

Top Overnight News

- US President Biden secured enough votes to clinch the Democratic presidential nomination and Donald Trump secured enough delegates to win the Republican nomination, according to Reuters.

- Eli Lilly (LLY) is partnering with Amazon Pharmacy (AMZN) to deliver prescriptions sold through direct-to-consumer website.

- Some of Japan’s biggest companies, including Toyota, Nissan, and Nippon Steel, hand out large wage hikes to their workers (the biggest increases in decades), paving the way for a BOJ rate hike next week. FT

- China is scrapping a string of infrastructure projects in indebted regions as it struggles to reconcile a need to save money with this year’s target for economic growth. FT

- Chinese state media has touted President Xi Jinping as a market-friendly reformer on par with the paramount leader Deng Xiaoping, in an apparent attempt to dispel skepticism over the country’s growth outlook. BBG

- The European Central Bank will lower borrowing costs in the spring, with June more likely than April for a first move, Bank of France Governor Francois Villeroy de Galhau said. BBG

- Putin says Russia is willing to resolve the Ukraine war “by peaceful means”, but insists Moscow would require security guarantees to do so. BBG

- Donald Trump and Joe Biden have both secured enough delegates to clinch their respective party nominations, cementing a November rematch. The 2024 election is expected to be one of the most expensive on record. BBG

- US crude stockpiles fell by 5.5 million barrels last week, the API is said to have reported, registering the first decline in seven weeks if confirmed by the EIA. Gasoline and distillate supplies also dropped. BBG

- Global dividends hit a record $1.66 trillion last year, according to Janus Henderson. Payouts were up 5%, with almost half the growth coming from the banking sector. It’s the third annual record for dividends and the fund manager expects another all-time high this year. BBG

- Hedge funds are unwinding short Treasury futures bets at a rapid clip, a sign that basis-trade positions are diminishing. This is probably due to asset managers pivoting into investment-grade credit. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as early momentum from the tech-led gains on Wall St was offset by Chinese developer default concerns and as participants digested Japanese wage hike announcements. ASX 200 was led higher by consumer stocks after China's MOFCOM released an interim proposal to remove tariffs on Australian wine although the advances in the index were limited by losses in the mining sector as iron ore prices continued to tumble. Nikkei 225 swung between gains and losses with initial strength reversed amid firm wage hike announcements. Hang Seng and Shanghai Comp. were varied and price action was contained within relatively narrow ranges with the Hong Kong benchmark kept afloat by strength in auto names and tech, while the mainland was pressured amid developer default fears and with the US House set to vote later on the TikTok crackdown bill.

Top Asian News

- Country Garden Holdings (2007 HK) onshore bondholders said they have not received a coupon payment due on Tuesday, while the developer said funds for a CNY 96mln coupon payment due on Tuesday were not fully in place and it plans to do its best to raise money for payment within a 30-day grace period, according to Reuters.

- TikTok US executives told headquarters recently that a ban wasn't an imminent risk, according to WSJ citing sources. However, it was separately reported that the US House plans to vote on the TikTok crackdown bill today at around 10:00EDT (14:00GMT).

European bourses, Stoxx600 (+0.2%), are modestly firmer, though with overall trade rangebound in what has been an uneventful session. The IBEX 35 (+1.3%) outperforms, led higher by post-earning strength in Inditex (+4.2%). European sectors are mixed; Retail outperforms, propped up by gains in Zalando (+13.5%) and Inditex. Autos is found at the foot of the pile, hampered by a poor Volkswagen (-0.8%) update. US equity futures (ES U/C, NQ -0.2%, RTY +0.1%) are trading around the unchanged mark, with slight underperformance in the NQ, paring back some of the strength seen in the prior session.

Top European News

- ECB's Villeroy noted broad agreement in the ECB to start cutting rates in spring as the battle against inflation is being won, while he noted the risk of waiting too long before loosening monetary policy and unduly hurting the economy is now “at least equal” to acting too soon and letting inflation rebound, according to an interview with Le Figaro; In another batch of comments: Says the ECB is winning the battle against inflation; will remain vigilant on inflation but victory is within sight; Spring rate cut remains probably; more likely to cut rates in June than April.

- ECB's Kazaks says ECB rate cut decision will come in the next few meetings; uncertainty remains high, and tensions in the labour market is still high.

- Citi expects BoE to start cutting rates in June (vs prev forecast of August).

Japan

- Japan Chief Cabinet Secretary Hayashi said it is important for wage hikes to spread to mid-sized and small companies, while he added they are seeing strong momentum for wage hikes. It was also reported that Toyota, Nissan, Panasonic, Hitachi & Nippon Steel were among the companies that have responded to unions' wage hike demands in full.

- Japanese PM Kishida says will call for pay hikes exceeding last year at small and mid-sized firms during the meeting with labour union and management; Japan not yet emerging out of deflation.

- BoJ Governor Ueda says BoJ will consider tweaking negative rates, YCC, and other monetary easing tools if the sustained achievement of price target comes into sight. We must scrutinize whether positive wage-inflation cycle merges in deciding whether conditions for phasing out stimulus are falling into place. This year's wage talks is critical in deciding timing on exit from stimulus. Unions have demanded higher pay, seeing many corporate management making offers that will stream in today and beyond. Will scrutinize the wage talk outcomes, as well as other data and information from hearings when making policy decisions.

- Japanese PM Adviser Yata says wage hikes this year likely to exceed last year's; Must continue pay rises next year and thereafter to defeat deflation; must broaden pay hikes to workers nationwide and in every prefecture. When asked if solid wage offers could trigger end to NIRP in march, Yata says government will not meddle with the BoJ's independent policy-making.

- BoJ is reportedly to mull ending all ETF purchases if price goal is in sight; likely to keep buying bonds to keep market stable and to intervene in the event of sharp yield upside, according to Bloomberg sources.

- Japan's Business Lobby Keidanren Head Tokura says wage increases indicated in the preliminary survey of big firms' wage talks are likely to exceed last years levels.

- Early signs of a strong outcome in this year's annual wage talks have heightened changes the BoJ will end its negative interest rate policy next week, according to Reuters sources; "There seems to be enough factors that justify a March policy shift".

FX

- Marginal upside for the USD which has seen DXY kiss the 103 mark in quiet trade. If the level is cleared, yesterday's 103.17 will come into view.

- Uneventful price action for EUR with ECB comments unable to shift the dial. As such, the pair is sticking to a 1.09 handle and within yesterday's 1.0902-43 range.

- GBP is steady vs. the USD and stuck on a 1.27 handle as in-line GDP metrics failed to inspire price action. For now, yesterday's 1.2746-1.2823 range holds.

- JPY is marginally softer vs. the USD but with losses tempered by reports that the BoJ could end ETF purchases. Today's 147.24-89 range sits within yesterday's 146.62-148.18 parameters. More broadly, focus is on in

- AUD is holding up vs. the USD despite falling iron ore prices, with AUD/USD maintaining 0.66 status and within yesterday's 0.6596-0.6627 range. Likewise, NZD/USD is unable to break out of yesterday's 0.6133-6184 range. RBNZ's Conway later today could help to decide direction.

- PBoC set USD/CNY mid-point at 7.0930 vs exp. 7.1775 (prev. 7.0963).

Fixed Income

- Gilts are the relative laggards, at lows of 99.68, with the paper unreactive to the UK's GDP data (which was broadly in-line). The downside can be attributed to Gilts paring some of Tuesday's outperformance following the labour data and a strong DMO sale.

- USTs are essentially unchanged in a quieter session for the US (on paper) after Tuesday's marked CPI moves and a soft 10yr auction, despite the marked concession built in by the post-CPI reaction. Currently holds near session lows at 111-04.

- Bunds are slightly firmer after Tuesday's marked US CPI-induced pressure. Specifics are relatively light thus far, but focus will be on the ECB Operational Framework Review (tentatively due today). Currently, Bunds hold around 133.24, with the peak for today at 133.27.

- Italy sells EUR 7.25bln vs exp. EUR 6-7.25bln 2.95% 2027, 3.50% 2031, 3.25% 2038 BTP Auction and EUR 1.25bln vs exp. EUR 1-1.25bln 4.0% 2031 BTP Green.

- Germany sells EUR 3.738bln vs exp. EUR 4.5bln 2.20% 2034 Bund: b/c 2.29x (prev. 2.10x), average yield 2.31% (prev. 2.38%) & retention 16.9% (prev. 17.5%)

Commodities

- Crude is firmer, taking impetus from Tuesday's bullish private inventory data, with specifics light in the session thus far; Brent holds near session highs at +1.1%.

- Flat trade in gold and a mild upward bias in silver with the Dollar steady, calendar light, and with the ongoing geopolitical landscape potentially providing a modest underlying bid; XAU trades in a tight USD 2,155.86-2,161.66/oz range.

- Base metals are mixed with copper prices outperforming following reports that top Chinese copper smelters have reportedly reached an agreement to take action to curb falling fees.

- Azerbaijan oil production stood at 476k BPD in Feb (prev. 474k BPD in Jan), according to the Energy Ministry.

- Top Chinese copper smelters have reportedly reached an agreement to take action to curb falling fees, according to Reuters sources; smelters to cut output at loss-making plants.

- BP (BP/ LN) and ADNOC suspend USD 2bln talks to take Israel-based Newmed private, via Bloomberg.

Geopolitics: Middle East

- CIA Director Burns said there is "still a possibility" of a Gaza ceasefire deal but added that many complicated issues are still to be worked through.

- US may urge partners and allies to fund a privately run operation to send aid by sea to Gaza that could begin before a much larger US military effort, according to sources cited by Reuters.

- US Central Command announced that Houthis fired a close-range ballistic missile from Yemen toward USS Laboon in the Red Sea on March 12th but it did not impact the vessel, while CENTCOM forces and a coalition vessel successfully engaged and destroyed two unmanned aerial systems launched from Yemen.

Geopolitics: Other

- Ukrainian Army Chief Syrskyi and Ukraine's Defence Minister Umerov held a phone call with US Defense Secretary Austin on weapons delivery to Ukraine, according to Reuters.

- A fire at oil refinery in Ryazan region extinguished, according to the governor cited by Reuters.

US event calendar

- 07:00: March MBA Mortgage Applications 7.1%, prior 9.7%

Government Agenda

- 4 p.m: US President Joe Biden delivers remarks in Milwaukee, Wisconsin on how his investments are rebuilding communities and creating jobs

- 11.15 a.m: US Secretary of State Antony Blinken meets with EU foreign affairs chief Josep Borrell

DB's Jim Reid concludes the overnight wrap

Next stop on the global tour is Singapore as I'm about to board the plane from Melbourne here this evening. My vaguely fascinating fact about Singapore is that my grandfather was a civil engineer there in the 1920s and 1930s and helped build much of its rapid development at the time. He was Scottish and met my Dutch grandmother there and got married without speaking each other's language and being able to understand each other. My wife says she's done the same thing! His brother owned a very successful industrial company on the island and lost all his wealth and his company after the 1929 stock market crash. My entire family were eventually left penniless after the 1930s crash and then WWII. 90 years later and my kids have had the same impact on me!

I'm looking forward to landing in the pretty standard 35 degree heat that Singapore always seems to have on landing. Talking of the heat, even with another hot US inflation print, risk assets put in another strong performance yesterday, with both the S&P 500 (+1.12%) and Europe’s STOXX 600 (+1.00%) driven by strong tech gains (sound familiar?). The highs in the main indices came despite the latest US CPI report for February, which saw inflation come in strongly for a second month running, and led to growing fears that the last phase of getting inflation back to target would be the hardest. But despite the persistence of inflation, investors were remarkably unphased for the most part, and they continue to see a June rate cut as the most likely outcome.

In terms of the details of the report, headline CPI came in at a 6-month high of +0.44%, which meant the year-on-year measure actually ticked up a bit to +3.2% (vs. +3.1% expected). Alongside that, core CPI was at +0.36%, which also meant annual core CPI was also above expectations at +3.8% (vs. +3.7% expected). Some of the blame was placed on shelter inflation, which was up by a monthly +0.43%. But even if you looked at core CPI excluding shelter, it was still up by +0.30%, so it’s difficult to say that shelter was the whole story behind the ongoing persistence. See our US economists’ reaction to the print here.

For the Fed, there must be some concern even if markets show little of this. For instance, if you look at core CPI on a 3-month annualised basis, it rose to +4.2%, so it’s getting harder to explain this away as just one month of bad data. Bear in mind that this is pretty high by historic standards as well, and apart from the post-Covid inflation, 3m core CPI hasn’t been that high since 1991. Alongside that, there was evidence that the inflation was coming from the stickier categories in the consumer basket. In fact the Atlanta Fed’s sticky CPI series is now up by +5.1% on a 3m annualised basis, the fastest it’s been since April 2023. So the concern for markets will be that inflation is showing some signs of rebounding, or at the very least stabilising at above-target levels.

When it comes to the Fed, the report led investors to dial back the rate cuts priced this year by -6.1bps, and futures now see 85bps of cuts by the December meeting. There was also a bit more doubt creeping into the chance of a cut by June, with 78% now priced in, down from 86% the previous day. But even with this slightly hawkish repricing, June is still considered the most likely timing for the first cut, which helped to support risk assets even though the print was above expectations. For the Fed, the most important question now will be how this affects the PCE measure of inflation, which is what they officially target. We won’t find that out until March 29th (Good Friday), but we should get a bit more info from the PPI report tomorrow, which has several components that feed into PCE.

The report led to a selloff for US Treasuries, with the 2yr yield (+5.0bps) up to 4.59%, whilst the 10yr yield (+5.4bps) rose to 4.15%. The 10yr yield had peaked at 4.17% intra-day shortly after the latest 10yr Treasury auction which saw slightly soft demand, with bonds issued +0.9bps above the pre-sale yield.

The fixed income selloff was echoed in Europe too, even if the overall performance was better there, with yields on 10yr bunds (+2.7bps) and OATs (+1.6bps) rising by a smaller amount. At the same time, markets remain confident of an ECB cut by June (priced at 91% vs 95% the day before). This is consistent with the latest ECB commentary, with Austria’s Holzmann (strong hawk) saying that a June cut was more likely than April, while France’s Villeroy suggested that “there’s a very broad agreement” to cut rates by the June meeting.

Yesterday’s main outperformer in the rates space were 10yr gilts (-2.5bps), which came after the UK labour market data was a bit weaker than expected over the three months to January. Notably, wage growth slowed to an 18-month low of +5.6% (vs. +5.7 expected), and the unemployment rate ticked up to 3.9% (vs. 3.8% expected).

Although sovereign bonds struggled yesterday for the most part, there was a much better performance for equities. In the US, the S&P 500 (+1.12%) closed at a new record, with tech stocks and the Magnificent 7 (+2.88%) leading the advance. Nvidia was +7.16% higher. Likewise in Europe, the STOXX 600 (+1.00%) hit an all-time high, and there were new records for the DAX (+1.23%) and the CAC 40 (+0.84%) as well. That said, gains more moderate outside of tech, with the equal-weighted S&P 500 up by +0.26%, while the small-cap Russell 2000 (-0.02%) narrowly lost ground for a 3rd consecutive day.

This backdrop was mostly positive for other risk assets. US HY credit spread fell -6bps, closing just 3bps above their 2-year low reached in late February. Meanwhile, Bitcoin posted a new intra-day high just shy of $73,000, surpassing the market cap of silver. Marion Laboure and Cassidy Ainsworth-Grace's new report this morning discusses the upcoming halving event's impact on Bitcoin prices, along with the Dencun upgrade scheduled for Ethereum today (link here).

Asian equity markets are mixed this morning with the Hang Seng (+0.26%) and the KOSPI (+0.11%) edging higher while the Nikkei (-0.36%) continues to drift back from last week's all time highs. Elsewhere, stocks in mainland China are also seeing losses with the CSI (-0.59%) and the Shanghai Composite (-0.26%) dragged lower by property developers as Country Garden Holdings Co. missed a 96-million-yuan ($13 million) coupon payment on a yuan bond for the first time. Outside of Asia, US stock futures are struggling to gain momentum with those on the S&P 500 (-0.03%) and NASDAQ 100 (-0.06%) flat. In early morning data, the unemployment rate in South Korea unexpectedly dropped to +2.6% in February from January's 3.0% level (v/s +3.0% consensus expectation).

Although the CPI release was the main data focus yesterday, there was also the NFIB’s small business optimism index from the US. That f ell to a 9-month low in February of 89.4 (vs. 90.5 expected). And there were also further signs of softening in the labour market, as the share planning to increase employment was down to a net +12, the lowest since May 2020 at the height of the Covid-19 pandemic. Likewise, the share of firms with positions they weren’t able to fill hit a three-year low of 37%.

To the day ahead now, and data releases include UK GDP and Euro Area industrial production for January. Central bank speakers include the ECB’s Cipollone and Stournaras. And in the US, there’s a 30yr Treasury auction taking place.

Uncategorized

Bougie Broke The Financial Reality Behind The Facade

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive…

Share this:

{kind=link}

{kind=link}

{kind=link}

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

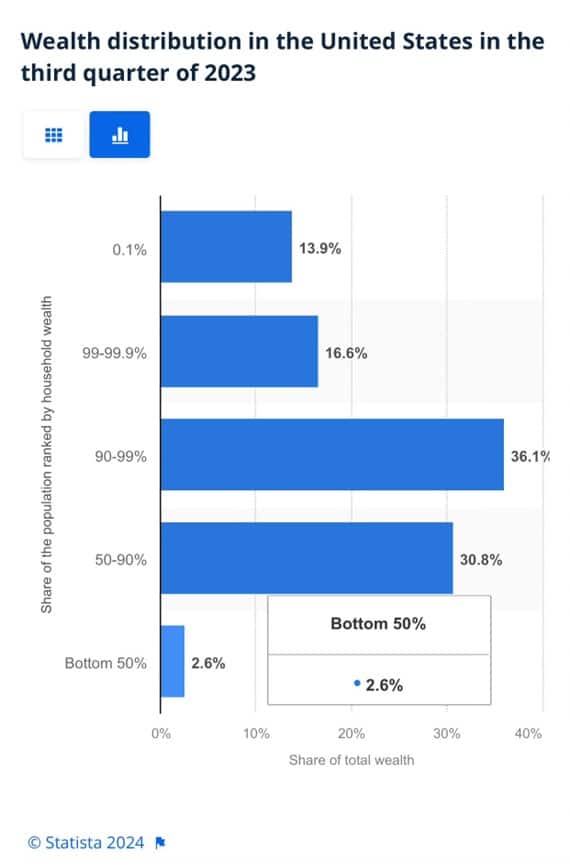

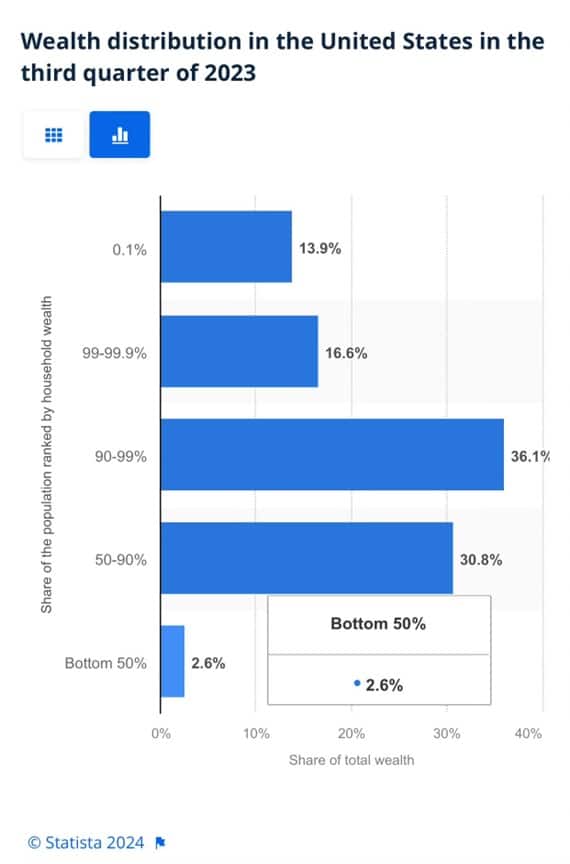

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

{kind=link}

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

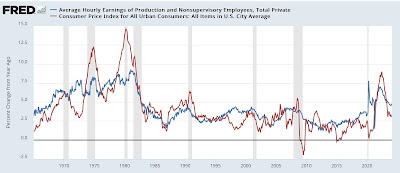

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

The post Bougie Broke The Financial Reality Behind The Facade appeared first on RIA.

recession unemployment pandemic economic recovery stimulus fed recession recovery interest rates unemployment stimulus

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

Aging at AACR Annual Meeting 2024

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges