Uncategorized

Futures Rise On China Reopening, End Of Tech Crackdown As Asia Enters Bull Market

Futures Rise On China Reopening, End Of Tech Crackdown As Asia Enters Bull Market

Futures extended their Friday post payrolls gain on the…

Share this:

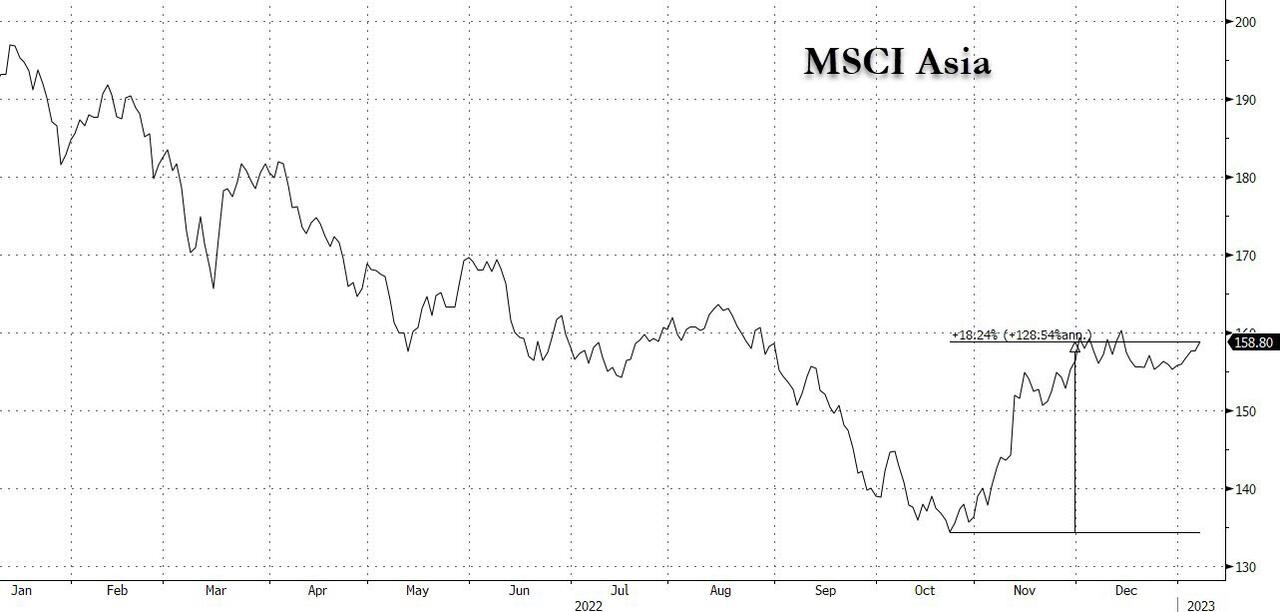

Futures extended their Friday post payrolls gain on the back of Chine reopening optimism coupled with speculation that China's tech crackdown is finally ending - just as we speculated this weekend when reporting on Jack Ma's ceding control of Ant Financial. S&P futures rose 0.4% as of 7:30 am ET while Nasdaq contracts 100 added 0.5%. And while European stocks were mostly in the green, the bulk of overnight action was in Asia where the Hang Seng Tech Index jumped 3.2% Monday, led by Alibaba Group after a top central bank official said the clampdown on the Internet sector was drawing to a close. The broader market also advanced, with a gauge of Chinese equities listed in Hong Kong rising 2%, helping push the MSCI Asia Index up 20% from its October low, setting it up for a bull market. The dollar weakened to a seven month low and oil rallied.

Among premarket movers, Bed Bath & Beyond shares surged as much as 75%, set to rally after losing nearly half of their value in the previous week on bankruptcy worries amid mounting losses, and ahead of the company’s earnings due Tuesday. Coinbase and Riot Platforms led cryptocurrency-exposed stocks higher in premarket trading as Bitcoin rallied to extend gains for a sixth consecutive session — its longest streak in nearly a year. Lululemon dropped after the athletic apparel maker forecast a weaker gross margin. Here are other notable premarket movers:

- Oracle is upgraded to overweight from neutral at Piper Sandler as its cloud transformation takes hold. The brokerage also noted that fiscal 2024 might be a watershed year for the software company, where growth in operating profits and earnings per share could accelerate to more than 10%. Oracle shares are up 1.3%.

- Piper Sandler upgrades Uber to overweight and cuts DoorDash to underweight, recommending a pair-trade between the two as it favors ride-hailing over delivery in 2023. Elsewhere, Jefferies starts DoorDash with an underperform rating, with a buy on Uber. Uber shares rose 2.3%. Dash shares down 4.2%.

- Ally Financial upgraded to neutral from underweight at Piper Sandler, with headwinds seen as now priced into the stock. Shares rise 1.9%.

- Credit Suisse says fertilizer prices are on a downward trajectory in a note double-downgrading Mosaic (MOS) to underperform. Shares fall 1.1%.

- Elf Beauty is downgraded to hold from buy at Jefferies, with broker saying risk-reward is balanced for the cosmetics company against an uncertain macroeconomic backdrop. Shares fall 1.1%.

- Ipsen shares drop after it agreed to acquire Albireo for $42/share in cash plus a contingent value right (CVR) of $10/share related to the U.S. FDA approval of Bylvay in biliary atresia. Albireo shares soar 93%.

- Jefferies sees another year of uncertainty ahead for US bank stocks, in a note upgrading its ratings on Truist (TFC) and First Republic (FRC) and downgrading both Signature Bank (SBNY) and Regions Financial (RF). TFC falls 0.09%. FRC rises 1.2%. SBNY shares fall 0.4%. RF falls 1%.

- KeyBanc trims its natural gas price estimates for 2023 following a relatively mild winter to date and cuts its ratings on Comstock Resources (CRK) and Pioneer Natural Resources (PXD). CRK shares rise 0.8%. PXD rises 1%.

- There is a strong industry backdrop for Harmonic (HLIT), with greater competition in the broadband service market pushing cable multiple-system operators (MSOs) to invest aggressively, Jefferies writes in note that upgrades the stock to buy. Shares rise 1.8%.

- Lanvin Group is rated neutral at Citi, which initiated coverage on the stock noting that the luxury fashion group has solid brands but clear evidence of a turnaround is required to merit a buy call. Shares rise 3.5%.

Markets closed last week solidly in the green, encouraged by Friday's jobs report which showed wage growth slowing, lifting the S&P 500 2.3% to notch its first winning week in over a month. They face another test on Thursday with CPI data that will likely help determine the size of the Federal Reserve’s next interest-rate increase. After the easing in wage inflation, swaps contracts showed investors expect the policy rate to peak at under 5% this cycle, down from 5.06% just before Friday’s jobs report. While traders remain divided about the size of February’s hike, with 32 basis points of tightening priced in, it appears that a quarter-point move is seen as more likely than a half-point increase.

While pressure on the Fed to hike by 50 basis points on Feb. 1 has eased, “policy makers appear to be increasingly frustrated by market-pricing at odds with Fed signaling in terms of both the terminal funds rate and timing of initial rate cut,” BNP Paribas economists led by Carl Riccadonna wrote in a note to clients. “This could tilt their bias toward a more forceful response at the next meeting.”

And while market pessimism is still dominant, analysts at Wells Fargo said Friday’s gains may be more durable than some expect, being “driven by a pro-cyclical post-jobs report reaction — not by risk/short-covering.” This market action “probably creates some positive investor sentiment since long-only’s are making money and short-sellers are faring better than one might expect.”

On the other hand, Morgan Stanley strategists said US equities face much sharper declines than many pessimists expect with the specter of recession likely to compound their biggest annual slump since the global financial crisis. The bank's equity strategist, Michael Wilson, long one of the most vocal bears on US stocks, said while investors are generally pessimistic about the outlook for economic growth, corporate profit estimates are still too high and the equity risk premium is at its lowest since the run-up to 2008. That suggests the S&P 500 could fall much lower than the 3,500 to 3,600 points the market is currently estimating in the event of a mild recession, he said. At the same time, US stocks have been lagging the rebound in European, Asian and emerging-market peers as American equities trade at a hefty valuation premium.

European markets also started the week amid a generally buoyant mood, as continental bourses opened higher, after posting the best week since March on optimism about China’s reopening, an easing energy crisis and signs of cooling inflation. Europe’s Stoxx 600 Index climbed 0.5%, touching the highest since mid-December with construction, technology and energy leading gains amid optimism over China’s demand for raw materials. On the data front, euro zone unemployment was unchanged in November at 6.5% as expected. Here are some of Europe's biggest movers:

- UCB gains as much as 4.9%, the most in almost 11 months, after the Belgian biopharma company said its 2022 results should come in toward the high end of guidance

- Geberit shares climb as much as 3.5% after Goldman Sachs raised its recommendation on the Swiss manufacturer to neutral from sell, citing reduced risk related to energy prices

- BioArctic rises as much as 29% after Eisai and Biogen’s Alzheimer’s drug Leqembi (lecanemab-irmb) received accelerated approval from the FDA. The treatment originates from BioArctic

- TGS gains as much as 15%, the most intraday since 2020, after a 4Q update that DNB said showed a strong beat on late sales and supportive management comments on order inflow

- SAES Getters shares surge as much as 36%, the most on record, after SAES Group entered an agreement with Resonetics to sell its Nitinol production business for about $900m in cash

- AstraZeneca falls after agreeing to buy US biotech CinCor Pharma for as much as $1.8 billion. Analysts say the acquisition is a good fit for the firm’s existing cardiovascular franchise

- Fresnillo falls as much as 2.5% as RBC Capital Markets downgrades stock to sector perform, as it sees operational momentum widely priced in and expects limited growth in the pipeline

- Frontier Developments shares fall as much as 42%, its biggest intraday decline on record, after the video-game firm said it no longer expects to meet FY23 consensus expectations

- Ambea drops as much as 6.9%, the most since Dec. 23, after the Swedish elder care company saw its target price cut at DNB to SEK52 from SEK73 on continued headwinds due to inflation

- Devolver Digital shares fall as much as 9.5%, dropping to a record low, after downgrading profit expectations for FY22 in a trading update. Goodbody called the update “disappointing.”

Earlier in the session, Asia’s benchmark stock index was on track to enter a bull market, as China’s reopening and a weakening dollar lure investors back to the region. The MSCI Asia Pacific Index climbed as much as 1.9% on Monday, taking its advance from an Oct. 24 low to more than 20%. The Asian benchmark is up 3.7% so far in 2023, beating the S&P 500 Index by about two percentage points. That’s after they both slumped about 19% last year, their worst performance since 2008.

Gauges in Hong Kong, Taiwan and South Korea led gains in the session, while Japan was closed for a holiday. Strategists have predicted a better year for Asian equities after a dismal 2022, especially as stocks in China, which carry the second-highest weighting in the regional gauge after Japan, turned a corner in November following the nation’s shift away from stringent virus curbs. The bull market milestone comes after the MSCI Asia gauge tumbled nearly 40% from a peak in early 2021. The MSCI Emerging Markets Index is on track to enter a bull market after surging more than 20% from its October low, boosted by Chinese stocks after the nation pivoted on its Covid strategy and offered more policy support for the economy.

“The rally has been fast and furious, so it is only natural to expect some profit-taking,” said Charu Chanana, senior strategist at Saxo Capital Markets Pte. “There are also some risks to keep a tap on, such as BOJ’s hawkish shift and company earnings. But that being said, there is still room for Asian markets to outperform global peers in 2023.”

Australian stocks climbed for a fourth day as miners advanced. The S&P/ASX 200 index rose 0.6% to close at 7,151.30, capping four consecutive days of advances. The winning streak is the benchmark’s longest since Nov. 25. The gauge followed Wall Street shares higher after US economic data boosted optimism for slower Fed rate hikes. Miners and energy shares contributed the most to the Australian index’s move. In New Zealand, the S&P/NZX 50 index rose 0.2% to 11,646.45.

In FX, the Bloomberg Dollar Spot Index fell to its lowest level since June as the dollar weakened against all of its Group-of-10 peers apart from the yen. It pared the drop in European hours. NOK, NZD are best performers among G10’s.

- The euro pared gains after rising to $1.07. Bunds and Italian bonds underperformed Treasuries, with the largest losses seen in the belly of curves, while money markets added to peak ECB rate wagers. Focus is also on the EU’s first bond sales of the year

- The pound advanced, while gilts bear flattened. Bank of England Chief Economist Huw Pill comments are due later

- Norway’s krone and the Australian dollar led G-10 gains, with the latter climbing to $0.6947, its highest level in more than four months, supported by China’s reopening. AUD curve bull steepens with 3-year yield ~13bps lower

- Turkey’s lira weakened as investors weighed President Recep Tayyip Erdogan’s signal that general elections will be held in early May, a month earlier than scheduled

In rates, Treasuries were pressured lower with losses led by long-end, continuing Friday’s post-payrolls steepening move amid wave of block trades. US yields are higher by as much as 4bp at long-end, steepening 5s30s, 2s10s spreads by around 2bp; 10-year around 3.595%, cheaper by 3.5bp on day but outperforming bunds in the sector by ~2.5bp. Treasuries took their cue from wider bear-steepening move across core European rates following first EU bond sales of the year. Another heavy IG credit issuance slate is expected this week, which also includes December CPI data Thursday and Fed Chair Powell appearance Tuesday.

In commodities, crude futures advanced, pushing Brent up almost 3.5% to trade near $81.11. Spot gold rises roughly $8 to trade near $1,873/oz while base metals are in the green.

In crypto, Bitcoin is firmer and has managed to surpass and gain a more convincing foothold above USD 17k, after fleeting breaches of the figure in recent sessions, with the 16th Dec USD 17524 peak into play

The only event on today's quiet calendar is the consumer credit print at 3pm ET. There are two Fed speakers on deck as well, Bostic and Daly, speaking shortly after noon.

Market Snapshot

- S&P 500 futures up 0.4% to 3,932.00

- STOXX Europe 600 up 0.5% to 446.56

- MXAP up 1.7% to 161.51

- MXAPJ up 2.4% to 535.12

- Nikkei up 0.6% to 25,973.85

- Topix up 0.4% to 1,875.76

- Hang Seng Index up 1.9% to 21,388.34

- Shanghai Composite up 0.6% to 3,176.08

- Sensex up 1.4% to 60,752.44

- Australia S&P/ASX 200 up 0.6% to 7,151.33

- Kospi up 2.6% to 2,350.19

- German 10Y yield little changed at 2.27%

- Euro up 0.3% to $1.0677

- Brent Futures up 3.0% to $80.90/bbl

- Brent Futures up 3.0% to $80.89/bbl

- Gold spot up 0.4% to $1,873.06

- U.S. Dollar Index down 0.27% to 103.60

Top Overnight News from Bloomberg

- Central banks aren’t giving up their inflation fight yet with the peak in interest rates still to come in most economies, but pauses will come at some point in 2023 — and perhaps even pivots

- The ECB predicts wage growth — a key indicator of where inflation is headed — will be “very strong” in the coming quarters, strengthening the case for more interest-rate hikes, the institution said Monday in an article to be published in its Economic Bulletin

- UK Prime Minister Rishi Sunak is set for talks with the union leaders directing the wave of strikes that have hobbled the UK since the start of the year, as the threat of more widespread action hangs over the country

- Russian President Vladimir Putin’s plans to squeeze Europe by weaponizing energy look to be fizzling at least for now. Mild weather, a wider array of suppliers and efforts to reduce demand are helping, with gas reserves still nearly full and prices tumbling to pre- war levels

- The SNB expects an annual loss of about 132 billion francs ($143 billion), more than five times the previous record, it said Monday in preliminary results. The largest part of this, 131 billion francs, stems from collapsed valuations of its large pile of holdings in foreign currencies, accrued as a result of decade-long purchases to weaken the franc

- A ship has been refloated after running aground in the Suez Canal and briefly disrupting traffic in the waterway that’s vital for global trade

- Brazil’s capital was recovering early Monday from an insurrection by thousands of supporters of ex-President Jair Bolsonaro who stormed the country’s top government institutions, leaving a trail of destruction and testing the leadership of Luiz Inacio Lula da Silva just a week after he took office

- Chinese officials are considering a record quota for special local government bonds this year and widening the budget deficit target as they ramp up support for the world’s second- largest economy, according to people familiar with the matter

- Japanese Prime Minister Fumio Kishida said careful explanation and communication with markets would be part of consideration on monetary policy, when asked about possible future changes in the Bank of Japan’s ultra-loose policy

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks gained with the MSCI Asia Pacific index on course to enter a bull market as the region took impetus from last Friday’s rally on Wall St. ASX 200 was led higher by strength in the commodity-related sectors and with sentiment also helped by China’s border reopening which JPMorgan predicts could boost Australia’s economy by nearly one percentage point over the next two years, although gains are capped following disappointing building approvals data. KOSPI outperformed with the index and shares in LG Electronics unfazed by the Co.’s softer preliminary Q4 earnings. Hang Seng and Shanghai Comp were supported after China’s border reopening over the weekend added to the hopes of an economic recovery and with Alibaba shares spearheading the advances in Hong Kong after Jack Ma ceded control of affiliate Ant Group.

Top Asian News

- Chinese President Xi Jinping stressed the importance of remaining committed to advancing reform, exploring new ground and carrying forward the fighting spirit, in a bid to modernize the work of judicial, procuratorial, and public security organs, according to China Economic Net.

- PBoC official Guo Shuqing said China’s growth will return to a normal path as China provides further support to households and companies to help recover following the end of the zero-Covid policy, according to People’s Daily.

- Tens of thousands of travellers began to fly in and out of mainland China on Sunday following the removal of nearly all of China’s border restrictions, according to WSJ.

- China’s health security administration said talks to include Pfizer’s (PFE) Paxlovid in the drug list for basic state health insurance failed due to the Co.’s high quotation for the antiviral medicine, according to Reuters.

- Six Chinese cities set GDP targets for this year ranging from 5.5%-7.0%, according to Securities Daily.

- Japanese PM Kishida said they must choose a successor to BoJ Governor Kuroda best suited for the post at the time when Kuroda’s term ends in April and must discuss with the next BoJ Governor the relationship between the government's and BoJ's policies. Kishida added that the government and BoJ must work closely together and each should play their own roles in achieving sustained price stability, while he noted that the government is ready to respond flexibly using reserves when asked if further steps could be taken to soften the blow on households from rising prices, according to Reuters.

- China reportedly considering a record special debt quota and a wider budget deficit, via Bloomberg; considering a deficit ratio of circa. 3% for the year. New special bond quota of up to CNY 3.8tln.

European bourses are firmer across the board, Euro Stoxx 50 +0.3%, as the constructive APAC tone continues amid a limited European docket. Sectors are primarily in the green, with defensive names lagging somewhat in-fitting with the risk tone.

US futures are in the green, ES +0.4%, in-fitting with the above sentiment ahead of Fed speak and a NY Fed Consumer Expectations survey. Apple's (AAPL) iPhone exports from India have doubled to a record USD 2.5bln, via Bloomberg.

Top European News

- BoE’s Mann said energy price caps could be lifting inflation in other sectors by boosting consumer spending and noted it is unclear what would happen to inflation when caps are removed, according to Bloomberg.

- UK PM Sunak said inflation is not guaranteed to decline this year and that the government will need to be disciplined to ensure inflation is brought down, according to Reuters. In other news, PM Sunak said he was willing to discuss pay increases for nurses in an effort to end strikes as ministers prepare to meet union leaders on Monday, according to FT.

- Czech Central Bank Governor Michl said they expect a significant drop in inflation from spring and are ready to raise rates further if the baseline scenario of a decline in inflation does not materialise, while he added that policy will be strict until inflation begins declining, according to Reuters.

FX

- DXY continues to slip below the 104.00 mark between 103.860-420 parameters towards key technical support and its December low (103.380).

- Action which is benefitting peers across the board ex-JPY, which is suffering amid the easing in USTs/EGBs and a Japanese holiday, with USD/JPY above 132.50.

- Antipodeans are the current outperformers with AUD surpassing 0.69 and Kiwi eclipsing 0.64 vs USD, before waning slightly.

- EUR/USD hit, but failed to breach, 1.07 while Cable is off best but still above 1.21 in a 1.2089-1.2174 range.

- PBoC set USD/CNY mid-point at 6.8265 vs exp. 6.8276 (prev. 6.8912)

Fixed Income

- EGBs under pressure and continuing to retreat from Friday's best, with Bunds down by nearly 100 ticks and Gilts similarly dented though managing to retain 102.00 at present

- USTs are similarly softer, though have largely been consolidating towards the APAC trough given the absence of Japanese participants ahead of Fed speak and NY survey, with yields modestly firmer across the curve.

Commodities

- Crude benchmarks are bid this morning, with WTI Feb and Brent Mar posting upside in excess of 3.0% or USD 2.0/bbl respectively.

- Action has been driven by China’s ongoing reopening and fresh geopolitical headlines, alongside other crude-specific developments (see below).

- Qatar set February marine crude OSP at Oman/Dubai plus USD 0.75/bbl and land crude OSP at Oman/Dubai plus USD 2.10/bbl. In relevant news, Qatar Energy is to sign Ras Laffan Petrochemicals Complex agreements with the project to cost USD 6bln and it created a JV with Chevron Phillips Chemicals of which it owns 70% and Chevron (CVX) owns 30%, according to Reuters.

- Iraq’s Oil Minister said the Karbala oil refinery will begin commercial production in mid-March, according to Reuters.

- US DoE rejected the initial batch of bids from oil companies to resupply a small amount of oil to the SPR in February, according to Reuters.

- Colonial Pipeline said repairs at the Witt Booster Station were completed and Line 3 returned to normal operations as of 17:51 EST on Sunday, according to Reuters.

- China has issued a second batch of 2023 crude oil import quotas to independent refiners totalling 111.82mln/T, via Reuters citing sources.

- Iraq February Basrah medium crude OSP to Asia -USD 1.40/bbl vs Oman/Dubai average, via Somo; to Europe at -USD 8.95/bbl vs Dated Brent.

- Spot gold is fairly contained around the mid-point of USD 1864-1880/oz parameters, with the yellow metal deriving some upside from the DXY struggling to attain a positive foothold; next resistance mark is USD 1885/oz from the 9th of May.

Geopolitics

- Ukrainian President Zelensky said Ukrainian forces were repelling Russian attacks on Bakhmut in eastern Donbas and were holding position in nearby Soledar under very difficult conditions, according to Reuters.

- Russia’s Defence Ministry said it struck a building in eastern Ukraine which killed more than 600 Ukrainian troops in retaliation for Ukraine’s deadly strike against a Russian barracks, although Ukrainian officials denied there were any casualties and said the strike by Russia only damaged civilian infrastructure, according to Reuters and ITV.

- Russia and Belarus will conduct joint air force drills on January 16th-February 1st, according to the Belarusian Defence Ministry cited by Reuters.

- Russian Kremlin has rejected suggestions from Ukraine that Russian official Kozak is sounding out officials in Europe about a potential peace deal.

- Swedish PM Kristersson said they have fulfilled commitments made to Turkey at the Madrid summit but noted that Turkey is demanding concessions that Stockholm cannot give to approve its application to join NATO, according to FT.

- China's military said it carried out combat drills around Taiwan on Sunday, while Taiwan's Defence Ministry stated 28 Chinese aircraft crossed the Taiwan Strait median line and entered the air defence zone in the past 24 hours. Furthermore, Taiwan's presidential office said it condemns China's recent military drills around Taiwan and that Taiwan's position is very clear whereby it will not escalate conflict nor provoke disputes but added that it will firmly defend its sovereignty and national security, according to Reuters.

Crypto

- Bitcoin is firmer and has managed to surpass and gain a more convincing foothold above USD 17k, after fleeting breaches of the figure in recent sessions, with the 16th Dec USD 17524 peak into play. Bafin warns of Godfather malware attack on banking/crypto apps.

US Event Calendar

- 15:00: Nov. Consumer Credit, est. $25b, prior $27.1b

Central bank Speakers

- 12:30: Fed’s Bostic Takes Part in Moderated Discussion

- 12:30: Fed’s Daly Interviewed in WSJ Live event

DB's Jim Reid concludes the overnight wrap

I hope your Sunday was more peaceful than mine. I played my first round of golf since back surgery (don't tell my consultant) and got stuck at the golf course afterwards as there was a big police search with helicopters over the area I walk home across. My wife and kids were out in the garden at the time and had to rush in as the copter nearly landed in the adjoining field. So at least they knew I wasn't making up being delayed. Had it not been pouring with rain I would have had time for another 9 by the time I could make it home via a huge detour. To be fair for me there are worst places to be stuck but it was a touch concerning.

That capped the end of a week where if you thought 2023 might start calmer than 2022 then you may have wanted to think again as there was plenty to debate and plenty of big swings in markets and data. In fact, after weak European headline inflation last week and a bad miss for the US Services ISM on Friday it was the best week for 10yr German bunds (-35.8bps) since data on Bloomberg starts around reunification in 1990. This week the main highlights are a speech from Powell in Sweden tomorrow morning, US and China CPI on Thursday, and Q4 US earnings season starting in earnest with 3 big financials on Friday.

Before we go through things in more detail it's worth recapping Friday's US data which resulted in a major shift lower in yields. Payrolls were firm as expected with the headline at +223k and unemployment unexpectedly falling a tenth to 3.5%, the lowest since Neil Armstrong first walked on the moon. As our US economists discuss here though, there were signs of slowing growth in the report with, for example, hours worked (34.3hrs vs. 34.4hrs) and average hourly earnings (+0.3% vs. +0.4%) declining. These factors led US yields lower after the report but the Services ISM dropping from 56.5 to 49.6 was a bit of shocker, especially when the consensus was at 55. There’s a chance the exceptionally cold weather could have artificially depressed the survey but the associated commentary wasn’t great and new orders fells 10.8 points to 45.2 which outside the pandemic is the lowest since the GFC and levels only previously associated with recessions. 2 and 10yr yields fell -21bps and -16bps on the day but around 15-16bps of both moves came after the ISM which shows its impact. Ironically the S&P 500 climbed +2.28% on the day but c.1.75% of this was after this shocker of a print showing that the influence of rates on equities outweighed the economic concerns. Such an equity move couldn't possibly last if this ISM print heralded in a stream of recessionary data. It can only last if the data suggests an environment weak enough to merit the Fed pausing soon with the economy managing a soft landing. Remarkably European PMIs now stand near a record high relative to the US which is part of the reason for preferring European credit given it still trades wide to the US.

A fuller review of the week for assets (a significant one to start the year) can be found at the end as usual. Let's move on to this week now and start with the US CPI print for December on Thursday which will be the pivotal data point in January. In terms of the MoM rate, the headline CPI is expected at -0.15% at DB (consensus 0.0% vs. +0.10% previously) with core CPI expected at +0.22% at DB (+0.3% consensus vs. +0.20% previously). In terms of YoY, headline is expected to drop from 7.1% to 6.3% at DB (6.5% consensus) with core falling from 6% to 5.6% (5.7% consensus).

Another inflation-related data point will come from the University of Michigan survey on Friday, where the gauge of consumer inflation expectations will be in focus. Other US data releases will include consumer credit (DB forecast +$30.5B vs +$27.1 in October) today and the NFIB small business optimism index on Tuesday.

Central bank speakers will also be in the spotlight with appearances from Fed Chair Powell and BoE Governor Bailey at the Riksbank's International Symposium on Central Bank Independence tomorrow. We will also hear from a number of other Fed and ECB speakers throughout the week (see day by day calendar for the list).

In Europe, key data releases will include industrial production and trade data in Germany, France and the Eurozone. Over in the UK, all eyes will be on the monthly GDP report for November on Friday. Elsewhere, retail sales (Wednesday) figures will be published in Italy along with the unemployment rate (today) for November. Over in China, the CPI and the PPI on Thursday will be the standout.

Turning to earnings now and some of the largest American banks including JPMorgan, Citi and BofA will kick off the earnings season on Friday. We will also hear from BlackRock and UnitedHealth that day. The day before all eyes will be on results from TSMC as concerns over supply-demand dynamics and US-China tensions continue to weigh on the sector, with the Philadelphia semiconductor index down -35% in 2022.

Asian equity markets are continuing their buoyant start to the year overnight and carried on where Wall Street left off it on Friday night. As I type, the KOSPI (+2.33%) is the strongest performer across the region with the Hang Seng (+1.60%), the CSI (+0.67%) and the Shanghai Composite (+0.54%) also edging higher amid receding risk-off sentiment after Hong Kong and China resumed quarantine-free travel over the weekend thereby marking the end of the Covid Zero policy. Elsewhere, markets in Japan are closed for a holiday. Futures on the S&P 500 (+0.36%), the NASDAQ 100 (+0.54%) and the DAX (+0.75%) are trading higher as well. Crude oil prices are also higher with Brent futures (+1.18%) at $79.50/bbl and WTI (+1.25%) at $74.69/bbl as we go to print.

Early morning data showed that Australia’s building approvals (-9.0% m/m) dropped further in November compared to a downwardly revised -5.6% decline in October.

In the US, the House Republican leadership standoff came to an end over the weekend after Republican Kevin McCarthy was elected as speaker after 14 failed attempts following days of gruelling negotiations.

Recapping last week now, and markets put in a strong start to 2023 as signs of economic weakness and declining inflationary pressures raised hopes that central banks wouldn’t be as aggressive as feared on hiking rates. In particular, the aforementioned ISM services index on Friday created a major bond and equity rally to end the week. However ominously it means December was the first month since May 2020 that both the ISM US services and manufacturing components were in contractionary territory.

On the back of ISM and payrolls, investors immediately moved to price in a less aggressive pace of rate hikes from the Federal Reserve. For instance, futures pricing for the end-2023 rate came down by -10.3bps over the week (-19.0bps on Friday) to 4.48%. That was a big catalyst for risk assets, with the S&P 500 surging +2.28% on Friday, which brought the index back into positive territory for the week at +1.45%. It also led to a massive decline in Treasury yields, with the 10yr down -31.7bps over the week (-16.0bps Friday) to 3.558%.

Over in Europe there was a similarly optimistic picture, aided by the news on Friday from the flash Euro Area CPI release. That showed headline inflation falling to +9.2% in December (vs. +9.5% expected), although core inflation did hit a record high of +5.2%. This backdrop meant equities and bonds surged across the continent, with the STOXX 600 up +4.60% (+1.16% Friday) to mark its strongest weekly performance since March. At the same time, 10yr bund yields fell -35.8bps (-10.5bps Friday), marking their largest weekly decline in records going back to German reunification in 1990.

Let's see what week 2 of 2023 brings

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

Stock indexes are breaking records and crossing milestones – making many investors feel wealthier

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire