Futures Rise Ahead Of Jobs Data That Could “Wreak Havoc In Markets”

Futures Rise Ahead Of Jobs Data That Could "Wreak Havoc In Markets"

US index futures climbed on Friday, paring this week’s losses fractionally as investors braced for jobs data that should provide clues about the pace of Fed tightening…

Share this:

US index futures climbed on Friday, paring this week’s losses fractionally as investors braced for jobs data that should provide clues about the pace of Fed tightening and which is expected to come in strong (whisper number at 502k, above 447k estimate, up from 210K last month; Wednesday’s ADP print was 807k, well above 410k estimate, our full preview is here) but not too strong - remember we now live in a "good news is bad news" world - or else the market will freak out that the Fed will hike even faster than is currently expected. Nasdaq futures also showed signs of recovery after a three-day selloff even as cryptocurrencies crashed again during the Asian session. As of 730am, emini S&P futures were up 4 points or 0.1%, Nasdaq futures were 0.24% higher, or 37 points and Dow futures were unchanged.Treasuries were steady, with the two-year yield heading for the biggest weekly spike since October 2019. Crude oil headed for the longest streak of weekly gains since October on tightening supplies.

U.S. hiring likely more than doubled in December from the previous month to 447,000 new jobs, according to consensus projections for nonfarm payrolls. “A low figure, around 100,000-200,000, wouldn’t change the direction the Fed is preparing to take,” Ipek Ozkardeskaya, a senior analyst at Swissquote, wrote in a note. “However, a strong NFP print, and a beat on unemployment rate, have the power of boosting the Fed hawks, on the idea that the jobs market no longer needs the Fed’s support.” That “could wreak havoc in risk markets.”

A surprisingly hawkish stance from the Fed revealed in the latest Minutes roiled financial markets at the start of a new year, with investors reassessing how to price assets in an environment of rising interest rates. The removal of crisis-era accommodation marks a shift not seen in at least three years, a time that also saw a spike in volatility.

“We knew coming into 2022 that the Fed was going to be a creator of volatility within the market and we’re seeing that right out of the gate at the start of the year,” said Lindsey Bell, chief markets and money strategist at Ally. “The good news is that today things seem to be stabilizing a little bit after yesterday’s knee-jerk reaction.”

Comments by regional Fed presidents provided some additional insight Thursday as traders attempted to predict a possible schedule for tightening. St. Louis Fed President James Bullard, a more hawkish policy maker, said in a speech the central bank could raise its target interest rate as soon as March. Meanwhile, San Francisco Fed President Mary Daly said at a virtual event that trimming the Fed balance sheet would come after normalizing the Fed funds rate.

Back to markets, Among meme stocks, GameStop jumped 18% in premarket trading after a report that the gaming retailer plans to launch a marketplace for non-fungible tokens this year. AMC Entertainment gained 6.5%. Discovery Inc. rose in New York premarket trading after BofA Global Research recommended the stock. Cryptocurrency-exposed stocks slip as Bitcoin extended its decline, falling below $42,000, before recovering slightly; the largest token declined as much as 4.9% to $41,008, marking a tumble of about 40% from its record near $69,000 reached Nov. 10. Marathon Digital dropped 1.6% in U.S. premarket, Riot Blockchain -1.3%, MicroStrategy -0.4% In Europe, Safello -4%, Arcane Crypto -5.7%, Northern Data -3.1%. Other notable premarket movers:

- GameStop (GME US) shares surge 19% in U.S. premarket trading after the gaming retailer was said to be planning to launch an NFT marketplace.

- Kohl’s (KSS US) falls 3.8% in premarket trading after UBS downgrades it to sell and slashes price target to a Wall Street-low on the “challenging” outlook for the stock in 2022 on inflationary pressures.

- Cryptocurrency-exposed stocks slip as Bitcoin extends its decline, falling below $42,000, before recovering slightly. Marathon Digital (MARA US) drops 1.6% in U.S. premarket, Riot Blockchain -1.3% (RIOT US), MicroStrategy -0.4% (MSTR US).

- Thursday’s court ruling was a “clear win” for Sonos (SONO US), and provides further proof that the firm has industry-leading intellectual property that it can successfully defend, Morgan Stanley (overweight) says. Shares rose 5.7% post-market.

- Marin Software (MRIN US) soars 36% in U.S. premarket trading after the marketing software firm announced an integration with Amazon Ads’ demand-side platform. Marin’s market capitalization was about $53m at Thursday’s close.

- Duck Creek Technologies’ (DCT US) net new annual recurring revenue is “back to beating,” Barclays (overweight) says. The shares rose 7.7% in postmarket trading after co. boosted its full-year revenue forecast.

- Quidel (QDEL US) rose 3% postmarket after the maker of Covid tests reported 4Q preliminary revenue that sailed past expectations.

- Armada Hoffler Properties (AHH US) fell 4.7% in premarket after launching a share sale to help pay the cash cost of its previously announced deal for the Exelon Building in Baltimore.

- Absci Corp. jumped 48% after announcing a research agreement with Merck & Co.

European equities had a choppy morning, settling flat to small lower as losses for travel and real-estate stocks outweighed gains in the mining industry, pulling the Stoxx Europe 600 Index down 0.3%. The gauge has had a bumpy first week of the year, pulling back from three consecutive record highs. In Milan, STMicroelectronics rose as much as 6.5%, the most since October, after the chipmaker reported higher-than-expected revenue. DAX lagged peers, dropping as much as 0.75%. Most indexes trade around lows for the week. Travel and real estate are the weakest sectors; miners, tech and oil & gas stocks lead to the upside. Here are some of the biggest European movers today:

- STMicroelectronics shares rise as much as 6.5% in Milan, the most since Oct. 28, after the chipmaker reported 4Q21 revenue that exceeded projections.

- Banca Carige soars as much as 13% amid reports that Cerberus submitted a non-binding offer for the troubled lender.

- Lanxess jumps as much as 3.3% to the highest since Nov. 3 after the stock is upgraded to overweight from equal-weight at Barclays, which sees “an attractive set-up” for share outperformance this year.

- Aston Martin gains as much as 3.8% after an update from the luxury car-maker that Jefferies (hold) called a “reassuring profit warning.”

- Inpost falls as much as 8.6%, reversing early gains, after the firm posted a 4Q and FY operational update. Growth in 4Q parcel volumes was 1% below Jefferies’ estimates, writes analyst David Kerstens (buy).

- Evolution drops as much as 6.2% after Berenberg says the market is “overly optimistic” about the Swedish online gambling giant’s top-line growth prospects, initiating with a hold rating on the stock.

- M&C Saatchi falls as much as 12%, the most intraday since July 2020, erasing some of the gains since the Jan. 5 announcement that AdvancedAdvT acquired a stake. The drop came after AdvancedAdvT said it’s interested in exploring a share- exchange merger.

- C&C falls as much as 5.8% after the Irish cider maker said performance was behind expectations in December due to the latest U.K. and Ireland measures to control the spread of Covid-19.

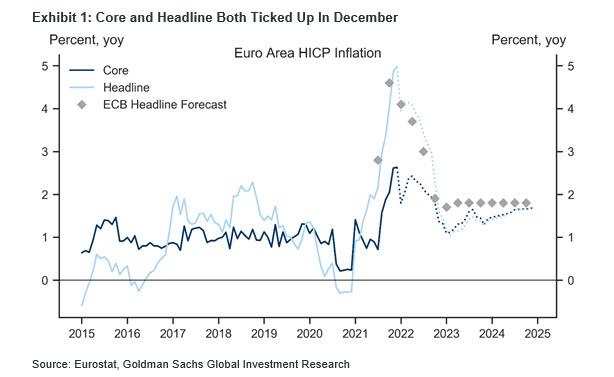

Consumer prices in the euro area jumped a record 5% from a year earlier in December, adding pressure on the ECB to join a growing legion of central banks from the Fed to the Bank of England in tightening monetary conditions.

Earlier in the session, Asian stocks rose, rebounding after a two-day drop, as financials gained amid the outlook for higher U.S. interest rates while traders remained wary of risks from the end of easy-money policies and coronavirus flare-ups. The MSCI Asia Pacific Index pared gains after rising by as much as 0.7%. South Korean chipmakers and Chinese internet giants were among stocks supporting the advance, helping offset drops in Taiwanese and Japanese tech stocks. The regional stock benchmark was poised for a weekly loss of 0.8%, sparked by a more hawkish than expected tone in the Federal Reserve’s December meeting minutes. The prospects of faster-than-expected monetary tightening spooked global investors, triggering a selloff of growth stocks.

“Value stocks continue to be strong, with higher yields pushing up banking stocks,” said Shogo Maekawa, a strategist at JP Morgan Asset Management in Tokyo. But, “for value and cyclicals to continue to be strong, the reasoning over monetary tightening needs to be backed by robust economic fundamentals and corporate earnings.”

Key gauges in Hong Kong, South Korea and Australia rose more than 1%. Japan’s Topix swung from a gain of as much as 1% to a loss of 0.8% at one point as investors reacted to news of spiking Covid-19 cases in some areas and possible restrictions to counter them. For Japan, the “risk of going into a state of emergency again seems to be weighing on the minds of investors,” said Serdar Armutcu, head of electronic trading at Mita Securities Co. in Tokyo.

Japanese stocks finished a volatile day slightly down amid concerns on interest rates and virus measures. Electronics makers and service providers were the biggest drags on the Topix, which closed 0.1% lower after swinging from a gain of 1% to a loss of 0.8%. Banks outperformed amid a rally in global lenders on an outlook for higher U.S. rates. The Nikkei 225 was little changed, with SoftBank Group gaining while Omron and Daikin dropped. “I guess it’s the continuation of yesterday’s market weakness, concerns over the FOMC,” said Serdar Armutcu, head of electronic trading at Mita Securities Co. in Tokyo. Plus, the “risk of going into a state of emergency again seems to be weighing on the minds of investors.” Okinawa was set to record over 1,400 new Covid cases, FNN reported. Kyodo reported earlier that Japan will delay resumption of its “Go To” travel subsidy program until after February and that Tokyo may tighten guidelines on group dining.

Indian stocks rose on optimism that state governments will opt for specific restrictions, instead of broad-based lockdowns, to curb a surge in coronavirus cases. The S&P BSE Sensex climbed 0.2% to 59,744.65, in Mumbai, taking its advance this week to 2.6%, the biggest five-day advance since early September. The NSE Nifty 50 Index gained 0.4%. Reliance Industries Ltd. climbed 0.8% and was the biggest boost for both gauges. Thirteen of 19 sector indexes compiled by BSE Ltd. advanced, led by a gauge of basic materials companies. Of 30 shares in the Sensex index, 16 rose and 14 fell. Mumbai, India’s financial capital, has no plans to shut down even as daily Covid-19 cases increase, the city’s municipal commissioner said. Separately, India will release its official estimate of the economy’s expansion for the fiscal year ending in March later today

In Australia, the S&P/ASX 200 index rose 1.3% to close at 7,453.30, regaining ground after Thursday’s 2.7% slump. All sectors advanced, led by energy shares and banks. Overall, the benchmark added 0.1% in the shortened first trading week of the year. Medibank was the top performer on Friday, gaining the most since March 2020. Magellan was among the worst performers after reporting net outflows of about A$1.55 billion for the December quarter. In New Zealand, the S&P/NZX 50 index fell 0.1% to 12,970.65

In FX, Bloomberg dollar spot drifts 0.2% lower. The euro was marginally higher against the greenback. Scandies top the G-10, AUD lags although ranges are relatively narrow.

In rates, price action was subdued with cash USTs and eurodollars quiet ahead of today’s payrolls report, with yields marginally cheaper across the curve but within Thursday session range. Treasury yields were cheaper by up to 1bp across long-end of the curve with spreads marginally steeper; 10-year yields around 1.725%, remain near top of weekly range. Long-end bunds and gilts richen ~1.5bps, peripheral spreads widen to core.

In commodities, oil was on course for a third weekly increase amid supply constraints; crude futures tagged on another percentage point of gains. WTI regains a $80-handle, Brent stalls near $83 in early London trade. Gains in commodities and emerging-market stocks further underscored the Friday rebound in risk sentiment. Spot gold drifts either side of $1,790/oz. Base metals are set to end the week strongly with LME nickel leading. Cryptos crashed during the Asian session, as usual.

Looking at the day ahead now, and the main highlight will be the aforementioned US jobs report for December. Otherwise, data releases from the Euro Area include the flash CPI reading for December, the final consumer confidence reading for December, and retail sales for November. Elsewhere, there’s also industrial production in November for France and Germany. Central bank speakers include the Fed’s Daly and Bostic, and the BoE’s Mann.

Top Overnight News from Bloomberg

- Federal Reserve policy makers could start to raise their target interest rate as soon as March and shrink the central bank’s balance sheet as a next step in response to surging inflation, Federal Reserve Bank of St. Louis President James Bullard said

- China’s delta variant-fueled Covid-19 outbreak isn’t showing signs of easing, with cases now cropping up elsewhere and technology hub Shenzhen on high alert, despite a dropoff in the latest epicenter Xi’an

- Local governments in China have started mapping out their economic blueprints for 2022, setting moderate to ambitious growth targets that give a signal of national goals

- President Kassym-Jomart Tokayev declared that order had largely been restored in Kazakhstan, after efforts to suppress mass protests that erupted over fuel price increases

- Oil was poised for a third weekly gain as the market tightened due to supply constraints across OPEC+ members following civil unrest.

- Peru hiked for a sixth straight month as inflationary pressure mounts amid the economy’s strong rebound from the pandemic. Argentina also raised its benchmark interest rate for the first time in over a year as it faces calls from the International Monetary Fund to tighten its monetary policy

- Japanese Finance Minister Shunichi Suzuki says he’s closely watching moves in foreign exchange markets and the impact of currencies on the economy

Market Snapshot

- S&P 500 futures up 0.18% to 4,696.00

- STOXX Europe 600 down 0.3% to 486.86

- MXAP up 0.5% to 191.98

- MXAPJ up 0.8% to 625.21

- Nikkei little changed at 28,478.56

- Topix little changed at 1,995.68

- Hang Seng Index up 1.8% to 23,493.38

- Shanghai Composite down 0.2% to 3,579.54

- Sensex up 0.1% to 59,687.14

- Australia S&P/ASX 200 up 1.3% to 7,453.35

- Kospi up 1.2% to 2,954.89

- Brent Futures up 0.9% to $82.71/bbl

- Gold spot little changed at $1,790.39

- U.S. Dollar Index down 0.21% to 96.12

- German 10Y yield little changed at -0.05%

- Euro up 0.2% to $1.1316

A more detailed look at global markets, courtesy of Newsquawk

Asia-Pac equities traded mostly higher but off best levels following a choppy Wall Street session – which saw the Russell 2000 close in the green whilst mild losses were seen across the Dow Jones, Nasdaq and S&P 500. US equity futures resumed trade with modest gains but the upside momentum faded, with the ES Mar'22 on either side of 4,700 in the run-up to the US jobs data. European equity futures traded flat with an upside bias for most of the overnight session. In APAC, the ASX 200 (+1.3%) was supported by its Financials, Energy, and Consumer Discretionary sectors. The Nikkei 225 (unch) was choppy but ultimately negative, with the index subdued by reports the Japanese government is seeking approval to declare COVID "quasi-emergencies" in three prefectures. The KOSPI (+1.2%) saw its Tech sector among the top performers after Samsung Electronic rose over 1.5% following its prelim earnings. The Hang Seng (+1.8%) and Shanghai Comp (-0.2%) held onto the mild gains seen at the cash open, although the property sector felt no reprieve as Shimao – thought to be one of the safer property firms – reportedly defaulted on a trust loan, thus triggering freefalls across its stock and bonds. In fixed income, US 10yr cash yield trimmed some of the prior session's gains.

Top Asian News

- Hong Kong to Send All Partygoers to Government Quarantine

- Hong Kong’s Growth Forecasts at Risk as Omicron Spreads in City

- Property Stocks Rally, Shimao Pares Losses: Evergrande Update

- China Says It Supports Kazakhstan’s Efforts to End ‘Chaos’

European equities trade mixed/flat (Stoxx 600 -0.1%) with the Stoxx 600 on course to end the week in minor positive territory as markets await the December US NFP report. The handover from Asia was a mixed bag with upside seen for the ASX 200 (+1.3%) and Hang Seng (+1.8%) whilst the Nikkei (unch) was unable to gain much traction to the upside amid reports the Japanese government is seeking approval to declare COVID "quasi-emergencies" in three prefectures. Stateside, after yesterday’s session which saw the Russell 2000 close in the green and modest losses for the Nasdaq and S&P 500, futures are indicative of a relatively flat open with the ES +0.2%. In a recent note, Morgan Stanley suggested that this year’s equity set-up is “is best in Europe and Japan, where estimates look low while valuations are undemanding.” Sectors in Europe are mixed with Basic Resources the clear outperformer amid price action in underlying commodity prices whilst Rio Tinto (+2.0%) has also garnered support from a broker upgrade at Berenberg. Banking names are taking a breather today after gains of 4.4% for the Stoxx 600 Banking Index this week amid the more favourable yield environment seen since the beginning of the year. To the downside, Travel & Leisure names lag peers with no obvious catalyst behind the move whilst Real Estate and Food & Beverage names are also seen lower. In terms of individual movers, STMicroelectronics (+5.5%) is the best performer in the Stoxx 600 after Q4 prelim. revenue exceeded expectations, citing better than anticipated operations in an ongoing dynamic market; gains in the Co. have provided support for the likes of Infineon (+2.8%) and ASML (+2.1%). Shell (+0.2%) has seen marginal, but waning, support after announcing that the remaining USD 5.5bln of proceeds from the Permian divestment are to be distributed in the form of share buybacks at pace. To the downside, Airbus (-1.2%) is a laggard in the CAC after reports that Qatar Airways is seeking compensation regarding surface flaws on the A350.

Top European News

- Sanofi Forms Potential $5.2 Billion AI Deal With Exscientia

- Aston Martin Assures Valkyrie Is On Track After Ramp-Up Issues

- Polish Inflation Hits 21-Year-High With More Rate Hikes Expected

- ABG Hires Partners for Equity Sales From Nordea and Arctic

In FX, not much deviation and perhaps inclination for the Dollar to venture too far before the latest BLS report that may be key in terms of determining whether the Fed pulls the rate hike trigger in March and sets the ball rolling for QT at the next or a nearby FOMC meeting. The index remains finely poised between 96.086-299 parameters amidst fractionally softer US Treasury yields and another downturn in broad risk sentiment, albeit relatively mild compared to previous episodes of aversion this week. Moreover, several Greenback/G10 pairings could be preoccupied with option expiries in the run up to the jobs data (and after pending the outcome) given hefty interest rolling off at today’s NY cut.

- EUR/GBP - The Euro and Pound are marginally outperforming, with the former reclaiming 1.1300+ status vs the Buck and latter retesting resistance around 1.3550 that includes the 100 DMA. However, Eur/Usd has faded multiple times above the round number and needs to breach 1.1350 convincingly to turn the corner, so 1.5 bn option expiry interest from 1.1290 to 1.1300 may still prove to be an impediment. Conversely, Eur/Gbp continues to hold above the 0.8333 mark that equates to the psychological 1.2000 level in the inverse cross to offer the Euro support and cap Sterling regardless of another encouraging UK PMI (construction this time) or flash Eurozone inflation flash ‘surprising’ to the upside (in line with Germany’s preliminary CPI outcome yesterday).

- NZD/CAD - Aud/Nzd dynamics rather than NZ specifics might be propping up the Kiwi as well, while the Loonie is deriving traction from ongoing strength in crude oil (WTI pivoting Usd 80/brl and Brent basically bid within a Usd 82-83 range) before Canada’s LFS. Nzd/Usd is hovering around 0.6750, as the aforementioned Antipodean cross probes 1.0600 and Usd/Cad is inching towards 1.2700.

- CHF/AUD/JPY - The Franc is treading water sub-0.9200 against its US counterpart with little reaction to an unexpected dip in Swiss sa unemployment or an acceleration in retail sales, while the Aussie and Yen both look trapped by option expiries very close or not far outside intraday extremes. Note, Aud/Usd has been up to 0.7178 and down to 0.7143 and Usd/Jpy topped and tailed at 116.05 and 115.75, so well within striking distance of 2.6 bn at 0.7160, 2.2 bn at 0.7200, 1.1 bn between 115.45-50 and 2.7 bn at 116.00.

In commodities, crude benchmarks are firmer in European trade with action directionally following, but eclipsing in magnitude, broader equity/risk performance. Currently, posting gains of around USD 1.0/bbl featuring WTI back above USD 80.00/bbl and Brent probing USD 83.00/bbl. Specific newsflow has been limited. Focus remains on geopolitics with increasingly punchy rhetoric emanating from Kazakhstan leaders regarding fuel-protests, though updates to output there remain limited after the sparse developments yesterday, highlighted by the Tengiz facility making a temporary adjustment. Elsewhere, adding to the positive tones from earlier in the week, the French Foreign Minister says there has been progress in Iranian nuclear discussions, but caveated that time is running out. Moving to metals, spot gold and silver are essentially unchanged at present despite some modest gyrations around the APAC/Europe crossover with newsflow sparse and broader sentiment cagey pre-NFP. Note, the weekly BofA Flow Show highlights the first inflow in a five-week period for precious metals, amounting to USD 0.3bln. Elsewhere, particularly for the copper watchers, a magnitude 5.2 earthquake occurred in Ricardo Palma, Peru – does not appear to be in direct proximity to a copper mine though, no commentary/guidance on any potential impacts yet.

US Event Calendar

- 8:30am: Dec. Change in Nonfarm Payrolls, est. 447,000, prior 210,000

- Dec. Change in Private Payrolls, est. 405,000, prior 235,000

- Dec. Change in Manufact. Payrolls, est. 35,000, prior 31,000

- Dec. Unemployment Rate, est. 4.1%, prior 4.2%

- Dec. Underemployment Rate, prior 7.8%

- Dec. Labor Force Participation Rate, est. 61.9%, prior 61.8%

- Dec. Average Hourly Earnings YoY, est. 4.2%, prior 4.8%

- Dec. Average Hourly Earnings MoM, est. 0.4%, prior 0.3%

- Dec. Average Weekly Hours All Emplo, est. 34.8, prior 34.8

- 3pm: Nov. Consumer Credit, est. $20b, prior $16.9b

DB's Jim Reid concludes the overnight wrap

My wife dropped a bombshell last night over dinner. She says she is going to start life drawing classes as of next week. I felt slightly better once I had it confirmed that she would be going as an artist rather than the subject. My offer to allow her to draw me at home was swiftly rebuked. She used to do a lot of this when she was at art college but ultimately now the children are at school she wants to get back into art in some form or another. Her long-term goal is to write and illustrate children’s books. So in couple of years time it will be buy one EMR and get a children’s book for free. Or indeed the other way round.

Talking of new jobs, today is another important payrolls report as the Fed is rapidly catching up to the tightness in the labour market that has been clear in most of the data for many months now outside of the actual headline payroll data. We’ll review what our economists are expecting below but for now the consequences of Wednesday’s FOMC minutes continue to reverberate in markets, as Fed officials across the dove-hawk spectrum emphasised support for starting QT shortly after rate hikes. See my CoTD from yesterday here for what happened to assets the last time we saw QT.

Sovereign bond yields saw another leg higher yesterday even as there were some initial signs that equities might be beginning to stabilise. The moves came as investors dialled up their hawkish bets on the Fed’s policy trajectory for this year, with Fed funds futures now pricing in an 84% chance of an initial rate hike as soon as the March meeting, which is the highest probability to date and up from just 33% only a month earlier.

These growing expectations of future rate hikes meant that yields on 10yr Treasuries rose +1.6bps to 1.72%. That’s just below the 2021 highs of 1.74% reached on March quarter-end last year. If I ran a poll asking when yields will move above that level back in March last year, I’m not sure many people would’ve said January 2022. However it was only just before Xmas that we closed at 1.34%. Indeed this marks the 5th consecutive move higher in yields, which is their longest run of increases since October. If we get a 6th today, it would then become the longest sustained run since February. The moves were driven by higher real rates once again, with the 10yr real yield up +5.5bps to -0.80%, its highest level since June. The latest rise also means that real yields have surged by an astonishing +30.2bps since their close on New Year’s Eve, and so are entirely responsible for the increase in nominal yields, with inflation breakevens having continued to fall back as investors grow in confidence that the Fed’s hikes will be able to keep a handle on inflation.

It wasn’t just the US that was affected though, with sovereign bond yields moving higher throughout the world. Yields on 10-year bunds continued to edge closer to the zero mark (not seen since May 2019), after rising another +2.3bps yesterday to -0.07%, and those on gilts (+6.9bps), OATs (+3.1bps) and BTPs (+3.7bps) followed likewise. That said, it was evident how markets are increasingly pricing in a policy divergence between the Fed and the BoE relative to the ECB, with the gap between yields on 2yr Treasuries and 2yr bunds hitting a post-pandemic high, whilst the gap between yields on 2yr gilts and 2yr bunds hit its widest since August 2019.

For US equities, there were some initial signs that the selloff was beginning to stabilise yesterday, with the S&P 500 down just -0.1% and the NASDAQ (-0.13%) mire becalmed, though remaining in negative territory on a YTD basis, albeit after four business days of 2022. Traditional cyclicals led the way, with energy (+2.29%) benefitting from climbing commodity prices and financial shares (+1.55%) enjoying this yield run. Big tech shares were notably mixed today after a rocky start to the year, evidenced by the aforementioned flat Nasdaq, with 4 of 6 FANG (+0.58%) stocks advancing, and 6 declining on the day.

Europe was weaker, having closed the previous day before the release of the minutes, and that saw the STOXX 600 (-1.25%) lose ground for the first time so far this year. The main exception to the broader trend lower in European equities were banks, with the STOXX Banks Index (+0.95%) continuing its run of having advanced in every session so far this year, in turn taking the index to a 3-year high.

Overnight in Asia, most major indices are trading in positive territory, rebounding from its previous session losses. The Shanghai Composite (+0.35%) and CSI (+0.36%) are both edging up. Elsewhere, the Kospi (+1.02%) is outperforming after the index heavyweight Samsung Electronics Q4 operating profit jumped to its highest in four years, while the Hang Seng (+1.15%) is also seeing a decent move higher. However, the Nikkei slipped (-0.33%), giving up its early gains following a -3% drop yesterday.

Staying on Japan, data released earlier this morning showed that household spending eased more than anticipated by -1.3% y/y in November and -1.2% m/m. Separately, real wages fell -1.6% y/y for the third straight month in November reinvigorating concerns about the nation’s economic recovery. Meanwhile, core consumer prices for Tokyo advanced +0.5% y/y, notching its fastest pace in nearly two years in December.

Moving ahead, Futures market in the US are pointing towards a stronger start with the S&P (+0.22%), Nasdaq (+0.21%) and Dow Jones (+0.16%) contracts all in positive territory. US Treasury yields have edged slightly lower with 10yrs back below 1.72%.

Looking forward now, the main highlight today will be the US jobs report for December, which will be an important one as markets look to assess the potential implications for monetary policy. In terms of our what to expect, DB’s US economists are looking for nonfarm payrolls to grow by +600k in December, its fastest pace since July, with the unemployment rate ticking down a tenth to a post-pandemic low of 4.1%. And although their view is that Omicron-related disruptions present some downside risk, that’s more likely to be seen in the January report. You can see their full preview here

Ahead of that, there was somewhat underwhelming data out of the US yesterday, with the ISM services index falling by more than expected to 62.0 in December (vs. 67.0 expected), which was beneath every economist’s estimate on Bloomberg and down from 69.1 the previous month. In fact, that fall of -7.1pts in the space of a month marks the biggest monthly decline since April 2020 at the height of the initial phase of the pandemic, although to be fair it still remains firmly in expansionary territory and is down from a record high the previous month. In addition the prices paid measure rose to 82.5, so not echoing the decline in the prices paid reading that we saw in the ISM manufacturing a couple of days earlier. Meanwhile the weekly initial jobless claims ticked up to 207k in the week through January 1 (vs. 195k expected), and November’s factory orders grew by +1.6% (vs. +1.5% expected).

Alongside the persistent rise in Treasury yields, another familiar pattern of 2022 so far has been the gains in oil prices, which are continuing to cement their place as one of the top 2022 performers, having risen by at least +1% every day so far this year. In fact there was a particular milestone yesterday as WTI (+2.47%) and Brent Crude (+1.88%) both closed above their pre-Omicron level for the first time yesterday, which just shows you how markets have brushed off the risks of the new variant having a significant impact on growth.

Speaking of Omicron, there were some further positive signs yesterday as the total number of Covid-19 hospitalisations in London actually fell for the first time in over 3 weeks. Of course this is only one day, but as one of the first places among the developed economies to be seriously affected by the new variant, London is an important leading indicator for how other places may fare. One caveat to note however is that the UK has one of the most advanced booster programmes in the world, with a majority of the country’s population having now had a booster dose.

The other main data release yesterday came from Germany, where inflation fell to +5.7% in December on the EU-harmonised measure (vs. +5.6% expected). Separately, factory orders in the country rose by a stronger-than-expected +3.7% in November (vs. +2.3% expected).

To the day ahead now, and the main highlight will be the aforementioned US jobs report for December. Otherwise, data releases from the Euro Area include the flash CPI reading for December, the final consumer confidence reading for December, and retail sales for November. Elsewhere, there’s also industrial production in November for France and Germany. Central bank speakers include the Fed’s Daly and Bostic, and the BoE’s Mann.

International

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Ramiro Ribeiro

After six years as head of clinical development at Apellis Pharmaceuticals, Ramiro Ribeiro is joining EyePoint Pharmaceuticals as CMO.

“The…

Share this:

After six years as head of clinical development at Apellis Pharmaceuticals, Ramiro Ribeiro is joining EyePoint Pharmaceuticals as CMO.

“The retinal community is relatively small, so everybody knows each other,” Ribeiro told Endpoints News in an interview. “As soon as I started to talk about EyePoint, I got really good feedback from KOLs and physicians on its scientific standards and quality of work.”

Ribeiro kicked off his career as a clinician in Brazil, earning a doctorate in stem cell therapy for retinal diseases. He previously held roles at Alcon and Ophthotech Corporation, now known as Astellas’ M&A prize Iveric Bio.

At Apellis, Ribeiro oversaw the Phase III development, filing and approval of Syfovre, the first drug for geographic atrophy secondary to age-related macular degeneration (AMD). The complement C3 inhibitor went on to make $275 million in 2023 despite reports of a rare side effect that only emerged after commercialization.

Now, Ribeiro is hoping to replicate that success with EyePoint’s lead candidate, EYP-1901 for wet AMD, which is set to enter the Phase III LUGANO trial in the second half of the year after passing a Phase II test in December.

Ribeiro told Endpoints he was optimistic about the company’s intraocular sustained-delivery tech, which he said could help address treatment burden and compliance issues seen with injectables. He also has plans to expand the EyePoint team.

“My goal is not just execution of the Phase III study — of course that’s a priority — but also looking at the pipeline and which different assets we can bring in to leverage the strength of the team that we have,” Ribeiro said.

— Ayisha Sharma

Remco Steenbergen

Remco Steenbergen→ Sandoz CFO Colin Bond will retire on June 30 and board member Remco Steenbergen will replace him. Steenbergen, who will step down from the board when he takes over on July 1, had a 20-year career with Philips and has held the group CFO post at Deutsche Lufthansa since January 2021. Bond joined Sandoz nearly two years ago and is the former finance chief at Evotec and Vifor Pharma. Investors didn’t react warmly to Wednesday’s news as shares fell by almost 4%.

The Swiss generics and biosimilars company, which finally split from Novartis in October 2023, has also nominated FogPharma CEO Mathai Mammen to the board of directors. The ex-R&D chief at J&J will be joined by two other new faces, Swisscom chairman Michael Rechsteiner and former Unilever CFO Graeme Pitkethly.

On Monday, Sandoz said it completed its $70 million purchase of Coherus BioSciences’ Lucentis biosimilar Cimerli sooner than expected. The FDA then approved its first two biosimilars of Amgen’s denosumab the next day, in a move that could whittle away at the pharma giant’s market share for Prolia and Xgeva.

Sean Marett

Sean Marett→ BioNTech’s chief business and commercial officer Sean Marett will retire on July 1 and will have an advisory role “until the end of the year,” the German drugmaker said in a release. Legal chief James Ryan will assume CBO responsibilities and BioNTech plans to name a new chief commercial officer by the end of the month. Marett was hired as BioNTech’s COO in 2012 after gigs at GSK, Evotec and Next Pharma, and led its commercial efforts as the Pfizer-partnered Comirnaty received the first FDA approval for a Covid-19 vaccine. BioNTech has also built a cancer portfolio that TD Cowen’s Yaron Werber described as “one of the most extensive” in biotech, from antibody-drug conjugates to CAR-T therapies.

Chris Austin

Chris Austin→ GSK has plucked Chris Austin from Flagship and he’ll start his new gig as the pharma giant’s SVP, research technologies on April 1. After a long career at NIH in which he was director of the National Center for Advancing Translational Sciences (NCATS), Austin became CEO of Flagship’s Vesalius Therapeutics, which debuted with a $75 million Series A two years ago this week but made job cuts that affected 43% of its employees six months into the life of the company. In response to Austin’s departure, John Mendlein — who chairs the board at Sail Biomedicines and has board seats at a few other Flagship biotechs — will become chairman and interim CEO at Vesalius “later this month.”

→ BioMarin has lined up Cristin Hubbard to replace Jeff Ajer as chief commercial officer on May 20. Hubbard worked for new BioMarin chief Alexander Hardy as Genentech’s SVP, global product strategy, immunology, infectious diseases and ophthalmology, and they had been colleagues for years before Hardy was named Genentech CEO in 2019. She shifted to Roche Diagnostics as global head of partnering in 2021 and had been head of global product strategy for Roche’s pharmaceutical division since last May. Sales of the hemophilia A gene therapy Roctavian have fallen well short of expectations, but Hardy insisted in a recent investor call that BioMarin is “still very much at the early stage” in the launch.

Pilar de la Rocha

Pilar de la Rocha→ BeiGene has promoted Pilar de la Rocha to head of Europe, global clinical operations. After 13 years in a variety of roles at Novartis, de la Rocha was named global head of global clinical operations excellence at the Brukinsa maker in the summer of 2022. A short time ago, BeiGene ended its natural killer cell therapy alliance with Shoreline Biosciences, saying that it was “a result of BeiGene’s internal prioritization decisions and does not reflect any deficit in Shoreline’s platform technology.”

Andy Crockett

Andy Crockett→ Andy Crockett has resigned as CEO of KalVista Pharmaceuticals. Crockett had been running the company since its launch in 2011 and will hand the keys to president Ben Palleiko, who joined KalVista in 2016 as CFO. Serious safety issues ended a Phase II study of its hereditary angioedema drug KVD824, but KalVista is mounting a comeback with positive Phase III results for sebetralstat in the same indication and could compete with Takeda’s injectable Firazyr. “If approved, sebetralstat may offer a compelling treatment option for patients and their caregivers given the long-standing preference for an effective and safe oral therapy that provides rapid symptom relief for HAE attacks,” Crockett said last month.

Steven Lo

Steven Lo→ Vaxart has tapped Steven Lo as its permanent president and CEO, while interim chief Michael Finney will stay on as chairman. Endpoints News last caught up with Lo when he became CEO at Valitor, the UC Berkeley spinout that raised a $28 million Series B round in October 2022. The ex-Zosano Pharma CEO had a handful of roles in his 13 years at Genentech before his appointments as chief commercial officer of Corcept Therapeutics and Puma Biotechnology. Andrei Floroiu resigned as Vaxart’s CEO in mid-January.

Kartik Krishnan

Kartik Krishnan→ Kartik Krishnan has taken over for Martin Driscoll as CEO of OncoNano Medicine, and Melissa Paoloni has moved up to COO at the cancer biotech located in the Dallas-Fort Worth suburb of Southlake. The execs were colleagues at Arcus Biosciences, Gilead’s TIGIT partner: Krishnan spent two and a half years in the CMO post, while Paoloni was VP of corporate development and external alliances. In 2022, Krishnan took the CMO job at OncoNano and was just promoted to president and head of R&D last November. Paoloni came on board as OncoNano’s SVP, corporate development and strategy not long after Krishnan’s first promotion.

→ Genesis Research Group, a consultancy specializing in market access, has brought in David Miller as chairman and CEO, replacing co-founder Frank Corvino — who is transitioning to the role of vice chairman and senior advisor. Miller joins the New Jersey-based team with a number of roles under his belt from Biogen (SVP of global market access), Elan (VP of pharmacoeconomics) and GSK (VP of global health outcomes).

Adrian Schreyer

Adrian Schreyer→ Adrian Schreyer helped build Exscientia’s AI drug discovery platform from the ground up, but he has packed his bags for Nimbus Therapeutics’ AI partner Anagenex. The new chief technology officer joined Exscientia in 2013 as head of molecular informatics and was elevated to technology chief five years later. He then held the role of VP, AI technology until January, a month before Exscientia fired CEO Andrew Hopkins.

→ Paul O’Neill has been promoted from SVP to EVP, quality & operations, specialty brands at Mallinckrodt. Before his arrival at the Irish pharma in March 2023, O’Neill was executive director of biologics operations in the second half of his 12-year career with Merck driving supply strategy for Keytruda. Mallinckrodt’s specialty brands portfolio includes its controversial Acthar Gel (a treatment for flares in a number of chronic and autoimmune indications) and the hepatorenal syndrome med Terlivaz.

David Ford

David Ford→ Staying in Ireland, Prothena has enlisted David Ford as its first chief people officer. Ford worked in human resources at Sanofi from 2002-17 and then led the HR team at Intercept, which was sold to Italian pharma Alfasigma in late September. We recently told you that Daniel Welch, the former InterMune CEO who was a board member at Intercept for six years, will succeed Lars Ekman as Prothena’s chairman.

Ben Stephens

Ben Stephens→ Co-founded by Sanofi R&D chief Houman Ashrafian and backed by GSK, Eli Lilly partner Sitryx stapled an additional $39 million to its Series A last fall. It has now welcomed a pair of execs: Ben Stephens (COO) had been finance director for ViaNautis Bio and Rinri Therapeutics, and Gordon Dingwall (head of clinical operations) is a Roche and AstraZeneca vet who led development operations at Mission Therapeutics. Dingwall has also served as a clinical operations leader for Shionogi and Freeline Therapeutics.

Steve Alley

Steve Alley→ MBrace Therapeutics, an antibody-drug conjugate specialist that nabbed $85 million in Series B financing last November, has named Steve Alley as CSO. Alley spent two decades at Seagen before the $43 billion buyout by Pfizer and was the ADC maker’s executive director, translational sciences.

→ California cancer drug developer Apollomics, which has been mired in Nasdaq compliance problems nearly a year after it joined the public markets through a SPAC merger, has recruited Matthew Plunkett as CFO. Plunkett has held the same title at Nkarta as well as Imago BioSciences — leading the companies to $290 million and $155 million IPOs, respectively — and at Aeovian Pharmaceuticals since March 2022.

Heinrich Haas

Heinrich Haas→ Co-founded by Oxford professor Adrian Hill — the co-inventor of AstraZeneca’s Covid-19 vaccine — lipid nanoparticle biotech NeoVac has brought in Heinrich Haas as chief technology officer. During his nine years at BioNTech, Haas was VP of RNA formulation and drug delivery.

Kimberly Lee

Kimberly Lee→ New Jersey-based neuro biotech 4M Therapeutics is making its Peer Review debut by introducing Kimberly Lee as CBO. Lee was hired at Taysha Gene Therapies during its meteoric rise in 2020 and got promoted to chief corporate affairs officer in 2022. Earlier, she led corporate strategy and investor relations efforts for Lexicon Pharmaceuticals.

→ Another Peer Review newcomer, Osmol Therapeutics, has tapped former Exelixis clinical development chief Ron Weitzman as interim CMO. Weitzman only lasted seven months as medical chief of Tango Therapeutics after Marc Rudoltz had a similarly short stay in that position. Osmol is going after chemotherapy-induced peripheral neuropathy and chemotherapy-induced cognitive impairment with its lead asset OSM-0205.

→ Last August, cardiometabolic disease player NeuroBo Pharmaceuticals locked in Hyung Heon Kim as president and CEO. Now, the company is giving Marshall Woodworth the title of CFO and principal financial and accounting officer, after he served in the interim since last October. Before NeuroBo, Woodworth had a string of CFO roles at Nevakar, Braeburn Pharmaceuticals, Aerocrine and Fureix Pharmaceuticals.

Claire Poll

Claire Poll→ Claire Poll has retired after more than 17 years as Verona Pharma’s general counsel, and the company has appointed Andrew Fisher as her successor. In his own 17-year tenure at United Therapeutics that ended in 2018, Fisher was chief strategy officer and deputy general counsel. The FDA will decide on Verona’s non-cystic fibrosis bronchiectasis candidate ensifentrine by June 26.

Nancy Lurker

Nancy Lurker→ Alkermes won its proxy battle with Sarissa Capital Management and is tinkering with its board nearly nine months later. The newest director, Bristol Myers Squibb alum Nancy Lurker, ran EyePoint Pharmaceuticals from 2016-23 and still has a board seat there. For a brief period, Lurker was chief marketing officer for Novartis’ US subsidiary.

→ Chaired by former Celgene business development chief George Golumbeski, Shattuck Labs has expanded its board to nine members by bringing in ex-Seagen CEO Clay Siegall and Tempus CSO Kate Sasser. Siegall holds the top spots at Immunome and chairs the board at Tourmaline Bio, while Sasser came to Tempus from Genmab in 2022.

Scott Myers

Scott Myers→ Ex-AMAG Pharmaceuticals and Rainier Therapeutics chief Scott Myers has been named chairman of the board at Convergent Therapeutics, a radiopharma player that secured a $90 million Series A last May. Former Magenta exec Steve Mahoney replaced Myers as CEO of Viridian Therapeutics a few months ago.

→ Montreal-based Find Therapeutics has elected Tony Johnson to the board of directors. Johnson is in his first year as CEO of Domain Therapeutics. He is also the former chief executive at Goldfinch Bio, the kidney disease biotech that closed its doors last year.

Habib Dable

Habib Dable→ Former Acceleron chief Habib Dable has replaced Kala Bio CEO Mark Iwicki as chairman of the board at Aerovate Therapeutics, which is signing up patients for Phase IIb and Phase III studies of its lead drug AV-101 for pulmonary arterial hypertension. Dable joined Aerovate’s board in July and works part-time as a venture partner for RA Capital Management.

Julie Cherrington

Julie Cherrington→ In the burgeoning world of ADCs, Elevation Oncology is developing one of its own that targets Claudin 18.2. Its board is now up to eight members with the additions of Julie Cherrington and Mirati CMO Alan Sandler. Cherrington, a venture partner at Brandon Capital Partners, also chairs the boards at Actym Therapeutics and Tolremo Therapeutics. Sandler took the CMO job at Mirati in November 2022 and will stay in that position after Bristol Myers acquired the Krazati maker.

Patty Allen

Patty Allen→ Lonnie Moulder’s Zenas BioPharma has welcomed Patty Allen to the board of directors. Allen was a key figure in Vividion’s $2 billion sale to Bayer as the San Diego biotech’s CFO, and she’s a board member at Deciphera Pharmaceuticals, SwanBio Therapeutics and Anokion.

→ In January 2023, Y-mAbs Therapeutics cut 35% of its staff to focus on commercialization of Danyelza. This week, the company has reserved a seat on its board of directors for Nektar Therapeutics CMO Mary Tagliaferri. Tagliaferri also sits on the boards of Enzo Biochem and is a former board member of RayzeBio.

→ The ex-Biogen neurodegeneration leader at the center of Aduhelm’s controversial approval is now on the scientific advisory board at Asceneuron, a Swiss-based company focused on Alzheimer’s and Parkinson’s. Samantha Budd-Haeberlein tops the list of new SAB members, which also includes Henrik Zetterberg, Rik Ossenkoppele and Christopher van Dyck.

nasdaq covid-19 vaccine treatment fda therapy rna brazil europeUncategorized

Is the biotech market rally real? Data suggest comeback in private, public markets

After some halting starts, false dawns and fragile rallies, the biotech market may finally be back.

No, really.

In the last several months, several important…

Share this:

After some halting starts, false dawns and fragile rallies, the biotech market may finally be back.

No, really.

In the last several months, several important signals have added up to what feels like a rally, with more depth and certainty than some of the short-lived upticks during the doldrums of 2022 and 2023, when only the industry’s most optimistic souls were willing to call it a comeback.

But now, public biotechs are releasing positive data and raising money in follow-on offerings with ease. Biopharmas have already raised $13.7 billion in secondary raises in 2024, according to Stifel’s Tim Opler. Biotech’s benchmark index, the $XBI, is up 56% from last year’s lows and has broken the $100 mark, thanks to gains that go deep into the 120-company index. And in the private markets, crossover rounds are trickling back, and IPOs are showing signs of life.

Investors and executives told Endpoints News that this moment feels different, encouraged by a return to the basics, a focus on data, and signs of a healthier — if smaller — biotech ecosystem.

“We should be beyond any of the lows,” said Chris Garabedian, a venture portfolio manager at Perceptive Advisors and founder of the firm’s early-stage investing unit Xontogeny. “We are going to see continued forward momentum.”

Investor sentiment is “very different from what it was in ‘22 to ‘23, where it was all doom and gloom,” MoonLake Immunotherapeutics CEO Jorge Santos da Silva said. A year ago, “The question was like, ‘What are the 22 ways in which you can die?’ That has really changed.”

The XBI cracking $100 is encouraging, but a deeper look at the index shows more signs of strength. The exchange-traded fund, which lets investors buy shares of its basket of 120 biotech companies, has seen $457 million in net inflows over the past month, according to YCharts data. And about 80% of biotechs on the index — which includes giants like Vertex $VRTX and small companies like Avidity Biosciences $RNA — have seen their stock in the green over the past three months.

Some of that gain is clearly driven by a surge in M&A, including the buyouts of Seagen, Horizon, Cerevel, and Karuna, all of which have returned billions of dollars back to investors who need to put it back to work in the private or public markets. And industry insiders have said there’s also a breadth in the disease areas drawing interest, including obesity, cancer, cardiology, neurology, and inflammation.

Even ARCH Venture Partners managing director Bob Nelsen voiced some broader — albeit measured — optimism for the market.

“For our internal base case, we’re still assuming that things are going to suck like they have in the last couple of years,” Nelsen told Endpoints. “But we all believe that it has turned.”

Nelsen still implores his portfolio companies and limited partners to “assume it’s going to be worse than you think.” But his optimism is driven by two major trends: the easing of macro factors like interest rates and the persistence of M&A. He’s closely watching whether generalist investors — whose huge dollars can swing a sector up or down, as they did dramatically during the pandemic — will come back to biotech.

“The conventional wisdom in Q4 is, they were never coming back in the market,” he said. “Turns out, in Q4 they were buying.”

From atonement to ‘FOMO’

Jorge Santos da Silva

Jorge Santos da SilvaDa Silva said the industry had been “paying for our sins” committed in the boom years of 2019 to 2021, when hundreds of biotechs went public — many far from going into the clinic. Along with layoffs and company closures, it resulted in an infestation of the corporate walking dead in companies trading at values below the amount of cash on their books.

But the number of those companies with negative equity value has dropped in the past few months, suggesting that a much-needed cleanup from the go-go years is well in progress.

“I call it a detox,” da Silva said. “Whatever we did was clearly excessive and everyone knew it at the time. But when you’re at a party, it’s like, ‘Oh my God, this is crazy, but let’s keep going.’ The detox phase is definitely coming to an end.”

Otello Stampacchia

Otello StampacchiaOtello Stampacchia, the managing director of the Boston-based VC firm Omega Funds, said the mood is even “getting a little bit bubblicious” for biotechs with clinical-stage drug candidates in large markets with meaningful milestones in the next 12 to 18 months.

“There’s really a rush to get into those, particularly now that the indices have started flipping their dynamic,” said Stampacchia, who founded Omega two decades ago. “Up until early last fall, nobody wanted to catch the falling knife. It’s now the exact opposite dynamic, and there’s a bit of crowding in some of these names.”

“There’s real FOMO to invest in the right therapeutic products and the right therapeutic companies,” he added.

That’s carried through the private and public markets, Stampacchia said, noting that Omega participated in Alumis’ recent $259 million Series C raise — biotech’s biggest round this year. He said he was “incredibly surprised by the amount of demand there was for the deal.” All told, Omega has seen roughly half a dozen of its portfolio companies raise close to half a billion dollars over the last few months, with increased valuations.

“In each case, it really wasn’t difficult to syndicate,” he said. “There’s real demand.”

rna pandemic interest ratesInternational

Deflationary pressures in China – be careful what you wish for

Until recently, China’s decelerating inflation was welcomed by the West, as it led to lower imported prices and helped reduce inflationary pressures….

Share this:

{kind=link}

Until recently, China’s decelerating inflation was welcomed by the West, as it led to lower imported prices and helped reduce inflationary pressures. However, China’s consumer prices fell for the third consecutive month in December 2023, delaying the expected rebound in economic activity following the lifting of COVID-19 controls. For calendar year 2023, CPI growth was negligible, whilst the producer price index declined by 3.0 per cent.

China’s inflation dynamics

Chinese consumers are hindered by the weaker residential property market and high youth unemployment. Several property developers have defaulted, collectively wiping out nearly all the U.S.$155 billion worth of U.S. dollar denominated-bonds.

Meanwhile, the Shanghai Composite Index is at half of its record high, recorded in late 2007. The share prices of major developers, including Evergrande Group, Country Garden Holdings, Sunac China and Shimao Group, have declined by an average of 98 per cent over recent years. Some economists are pointing to the Japanese experience of a debt-deflation cycle in the 1990s, with economic stagnation and elevated debt levels.

Australia has certainly enjoyed the “pull-up effect” from China, particularly with the iron-ore price jumping from around U.S.$20/tonne in 2000 to an average closer to U.S.$120/tonne over the 17 years from 2007. With strong volume increases, the value of Australia’s iron ore exports has jumped 20-fold to around A$12 billion per month, accounting for approximately 35 per cent of Australia’s exports.

For context, China takes 85 per cent of Australia’s iron ore exports, whilst Australia accounts for 65 per cent of China’s iron ore imports. China’s steel industry depends on its own domestic iron ore mines for 20 per cent of its requirement, however, these are high-cost operations and need high iron ore prices to keep them in business. To reduce its dependence on Australia’s iron ore, China has increased its use of scrap metal and invested large sums of money in Africa, including the Simandou mine in Guinea, which is forecast to export 60 million tonnes of iron ore from 2028.

The Chinese housing market has historically been the source of 40 per cent of China’s steel usage. However, the recent high iron ore prices are attributable to the growth in China’s industrial and infrastructure activity, which has offset the weakness in residential construction.

Whilst this has continued to deliver supernormal profits for Australia’s major iron ore producers (and has greatly assisted the federal budget), watch out for any sustainable downturn in the iron ore price, particularly if the deflationary pressures in China continue into the medium term.

unemployment covid-19 bonds shanghai composite housing market africa china

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Liquidity Problems Are Closer Than You Think

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Is the biotech market rally real? Data suggest comeback in private, public markets

The Digest #187

Interest rates, the best it gets. It’s time to deploy cash

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Deterra Royalties half-yearly result: stable performance and growth Initiatives

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges