Futures Reverse Overnight Plunge As European Banks Stabilize From Historic Rout

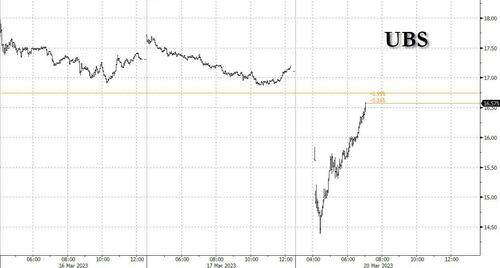

US equity futures, global markets and European bank stocks have stabilized, rebounding off worst levels which saw Europe's brand new banking megagiant UBS plunge as much as 16% before recouping most of the losses...

... as investors digested UBS’s agreement to buy Credit Suisse as well as central bank moves to boost dollar liquidity in an effort to restore confidence in the global financial system. Futures contracts on the S&P 500 were little changed at 7:30 a.m. ET after tumbling 1% earlier. The Stoxx Europe 600 index was modestly higher, with banks and financial services still the sharpest fallers. UBS shares sank as much as 16%, while Credit Suisse sank 60%. European bank stocks pared losses with the Stoxx Europe 600 Banks Index down less than 1%, after after dropping as much as 6%. A gauge of Asian shares fell by more than 1%.

In premarket trading, First Republic Bank was poised to extend last week’s record loss as the US lender’s shares plunged 19% after S&P cut its credit rating again. Wells Fargo and Citigroup trimmed US premarket declines. Gold-mining stocks rallied in premarket trading on Monday, after a $3.2 billion deal between UBS and troubled lender Credit Suisse failed to calm nerves in the banking industry, knocking risk appetite. Newmont, the biggest US-listed gold miner, gains as much as 2.6%; Harmony Gold Mining +5.6%, Gold Fields +2.2%, New Gold +3.4%, Wheaton Precious Metals +1.5%, First Majestic Silver +2%, Pan American Silver +0.7%. The price of gold rose above $2,000 an ounce for the first time in a year amid safe-haven appeal. Here are some other notable premarket movers:

Cryptocurrency-exposed stocks rise after Bitcoin extended its gains for a fifth consecutive session, with the digital asset reaching levels not seen in about nine months. Marathon Digital (MARA US) +5.6%, Riot Platforms (RIOT US) +8% and Coinbase (COIN US) +4.2%

Energy stocks decline as investors’ concern about the banking system spur broad risk aversion and drag crude prices lower. Exxon Mobil (XOM US) slid 1.3%, Chevron (CVX US) -1.1%, Occidental Petroleum (OXY US) -1.1%.

For those who were lucky enough to be away from their computers this weekend, this is what you missed:

Credit Suisse shareholders will receive 1 share in UBS (UBSN SW) for 22.48 shares in Credit Suisse which reflects a merger consideration of CHF 3bln and that FINMA determined that Credit Suisse’s additional tier 1 capital in the aggregate nominal amount of around CHF 16bln will be written off. Credit Suisse also told staff in a memo that the details of the transaction are being worked through and no disruption to client services is expected, while it told staff there will be no changes to payroll arrangements and bonuses will still be paid on March 24th.

UBS said the company will suspend share buybacks and that they did not initiate the discussions but believe the transaction is financially attractive to UBS shareholders and are planning to de-risk and downsize Credit Suisse’s investment banking operations. UBS also noted its strategy is unchanged in US and APAC and said that Credit Suisse is quite complementary to the wealth business in Southeast Asia. Furthermore, Colm Kelleher will be Chairman and Ralph Hamers will be Group CEO of the combined entity, while the transaction is not subject to shareholder approval and there is a material adverse change clause on the Credit Suisse deal.

SNB said it is providing substantial liquidity assistance to support the UBS takeover of Credit Suisse and the takeover was made possible with the support of the Swiss federal government, FINMA and SNB, while it added that both banks have unrestricted access to the SNB’s existing facilities. There were also comments from the Swiss Finance Minister that this is a commercial solution and not a bailout, while she noted the cost of bankruptcy to the Swiss economy would have been huge.

ECB said it welcomes the swift actions and decisions taken by Swiss authorities and noted that the Euro area banking sector is resilient with strong capital and liquidity positions. ECB’s Lagarde also stated that the ECB’s policy toolkit is fully equipped to provide liquidity support to the euro area financial system if needed.

BoE said it welcomes the comprehensive actions by the Swiss authorities to merge UBS and Credit Suisse, while it has been engaging with international counterparts throughout preparations for the announcement. Furthermore, it stated that the UK banking system remains safe and sound and is well-capitalised and funded.

Fed Chairman Powell and US Treasury Secretary Yellen said they welcome the announcements by Swiss authorities to support financial stability and noted the capital and liquidity positions of the US banking system are strong and US financial system resilience is strong. Furthermore, they have been in close contact with international counterparts to support their implementation.

At least two major banks in Europe are examining scenarios of contagion potentially spreading across Europe’s banking sector and looking to the Fed and ECB to step in with stronger signals of support, according to Reuters citing executives with knowledge of the deliberations.

Banking stocks and bonds plummeted after UBS Group sealed a state-backed takeover of troubled peer Credit Suisse, a deal that was shoved down Credit Suisse investors' throats - literally - in an attempt to restore confidence in a battered sector.

The Federal Reserve and five other central banks announced coordinated action on Sunday to boost liquidity in US dollar swap arrangements. The Fed’s next policy decision is due later this week, with market attention on whether it may slow or pause interest-rate hikes.

UBS emerged as Switzerland’s one and only global bank, a risky bet that makes the Swiss economy more dependent on a single lender. Credit Suisse told staff its wealth assets are operationally separate from UBS for now, but once they merged clients might want to consider moving some assets to another bank if concentration was a concern.

The rudest shock in the rushed deal was reserved for the holders of Credit Suisse's riskiest tranche of bonds. UBS is salvaging the most value from the wreckage, says Breakingviews columnist Liam Proud.

Hedge fund managers and other large investors believe it is far too soon to call an all-clear on turmoil in the global financial sector.

Amid the endless turmoil, the KBW Bank Index plunged 28% over the past two weeks, with financials rattled by concerns over Credit Suisse as well the recent failures of Silicon Valley Bank and two other US lenders. Gains in tech stocks have helped support the overall market, however, as investors look for a safe haven.

"The turmoil still has at least a couple of days to play out, and only the Fed can come in and calm that,” Chris Beauchamp, chief market analyst at IG Group Holdings Plc, said on Bloomberg Television. He expects the US central bank to hike rates by 25 basis points as a pause would be interpreted by markets as a sign that the stress in banks is bigger than initially thought.

“Assuming these banking stresses do not evolve into something more serious, the European Central Bank and the Fed may perceive that they are at or near their objectives with current policy,” said Brad Tank, chief investment officer for fixed income at Neuberger Berman. “The Fed, in particular, is further along in its tightening cycle and should have more flexibility to pause — and markets are indeed pricing for 2023 fed funds rate cuts once again.”

Meanwhile, one day after he revealed his shock that stocks remain resilient and just under 4,000 despite calling for a crah for the past 3 months, Morgan Stanley’s Michael Wilson said the stress in the banking system marks what’s likely to be the beginning of a painful and “vicious” end to the bear market in US stocks, adding that the risk of a credit crunch has increased materially. The S&P 500 will remain unattractive until equity risk premium climbs to as high as 400 basis points from the current 230 level, according to the bearish strategist who two weeks ago flip-flopped briefly to bullish before getting rugpulled by the banking crisis.

European stocks are higher after reversing the negative knee-jerk reaction to the terms of the UBS takeover of Credit Suisse. The Stoxx 600 is up 0.6% as gains in utilities, miners and consumer products outweigh declines in bank stocks. European oil stocks declined as investors’ concern about the potential for a global banking crisis spur broad risk aversion and drag crude prices lower. The Stoxx Europe 600 Energy index slid 1%; among oil majors, Shell declined 1.5%, TotalEnergies -1.3%, and BP -0.6%. Smaller producers also dropped with Harbour Energy falling 5.7% and Tullow Oil -7.7%. Here are the biggest European movers:

UBS shares drop as much as 16%, the most in eight years, after a government-brokered deal for it to buy rival Credit Suisse prompted a slew of downgrades

Deutsche Bank declines 11%, ING -9.6%, Commerzbank -9.6%, Standard Chartered -8.7%, BNP Paribas -9% following UBS’s agreement to buy Credit Suisse

El.En shares slide as much as 9.6% after Berenberg downgrades the laser- equipment maker to hold from buy, saying the company has a “tough year ahead”

JM AB falls as much as 7.7% after DNB Markets gave the Swedish construction and building management company its sole sell rating in reinstated coverage

Centamin shares rise as much as 6.6%, Endeavour Mining up as much as 7.2% and Fresnillo rises as much as 4.1% as gold gains owing to haven demand amid banking concerns

Earlier in the session, Asian stocks declined as the UBS takeunder failed to quell investor concerns about the health of the global financial system. The MSCI Asia Pacific Index fell as much as 1.4%, reversing most of its gain from Friday, with tech and financial names among the biggest drags. Hong Kong gauges led losses in the region as financial stocks including HSBC and AIA Group fell due to worries over risky bond exposures. While the takeover of Credit Suisse is seen to reduce the immediate systemic risk for the banking sector, investors are worried over further repercussions from its bonds. Traders are also focused on the Federal Reserve’s rate decision later this week.

“Even with the rescue plans over the weekend, it is hard to predict what will happen in the near future,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Ltd. “The measures to restore confidence in banks and to tame inflation go in opposite directions, and the dilemma is reducing risk appetite in the stock market.” China’s onshore equity benchmark erased earlier gains even after its central bank unexpectedly cut the reserve requirement ratio late Friday. The PBOC’s announcement timing “seems to fall in line with recent global banking jitters, which suggests that the PBOC is on high alert to provide any cushion against any knock-on impact from recent turmoil,” said Jun Rong Yeap, market strategist at IG Asia

In FX, the Bloomberg Dollar Spot Index steadied, erasing a decline of as much as 0.2% earlier while the Japanese yen is the best performer among the G-10’s. The New Zealand dollar is the weakest. Australia and New Zealand’s currencies flipped to losses amid souring risk sentiment.

“Traders are looking for haven assets again with bank stocks falling, and worries about CoCo bonds gaining momentum,” Mingze Wu, a foreign exchange trader at StoneX Group, said of contingent convertible bonds. “The insistence of the Swiss National Bank to make the UBS-Credit Suisse deal happen suggests the rot was deeper and greater than they might have thought, and the dollar is an obvious beneficiary of this rush to safety”

In rates, the nervous start to the trading week prompted a flight to safety, with German and UK government bonds rallying. 2-year TSY yield fell as much as 21bps to 3.63%, while its 10- year peer slid to as low as 3.29%, the lowest since September; traders bet on 15bps of Fed hikes this week but eased tightening beyond by as much as 12bps, pricing 105bps of cuts from the peak in May through to year-end. Bund futures are off their best levels but still in the green with 10-year yields down 4bps while two-year yields fall 8bps.

In commodities, oil prices fell again with West Texas Intermediate briefly plunging below $65 a barrel, as escalating investor concerns about a global banking crisis eroded appetite for risk assets including commodities. Gold steadied, after rising above $2,000 an ounce for the first time in a year.

Bitcoin remains bid and has extended comfortably above the USD 28k handle for the first time since June, though is yet to convincingly breach USD 28.5k to the upside.

There is nothing scheduled on the macro calendar today but there will be plenty of bank related newsflow.

Market Snapshot

S&P 500 futures down 0.1% to 3,943.50

MXAP down 1.1% to 155.86

MXAPJ down 1.4% to 498.89

Nikkei down 1.4% to 26,945.67

Topix down 1.5% to 1,929.30

Hang Seng Index down 2.7% to 19,000.71

Shanghai Composite down 0.5% to 3,234.91

Sensex down 1.3% to 57,214.31

Australia S&P/ASX 200 down 1.4% to 6,898.51

Kospi down 0.7% to 2,379.20

STOXX Europe 600 up 0.6% to 438

German 10Y yield little changed at 1.95%

Euro down 0.3% to $1.0641

Brent Futures down 3.8% to $70.18/bbl

Gold spot up 0.8% to $2,005.59

U.S. Dollar Index up 0.17% to 103.88

Top Overnight News from Bloomberg

The Federal Reserve and five other central banks announced coordinated action Sunday to boost liquidity in US dollar swap arrangements, the latest effort by policymakers to ease growing strains in the global financial system.

UBS Group AG shares slumped Monday as investors digested the news of its historic acquisition of rival Credit Suisse Group AG and began to assess the job of integrating the troubled Swiss lender.

The riskiest bonds of European lenders are plunging after holders of Credit Suisse Group AG’s contingent convertible securities suffered a historic loss as part of its takeover by UBS Group AG.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were on the back foot amid ongoing banking sector jitters despite the announcement that UBS will take over Credit Suisse in an emergency rescue valued at CHF 3bln which would wipe out CHF 16bln of additional tier 1 bonds. ASX 200 extended its retreat from a recent break beneath 7,000 with declines led by weakness in the energy, real estate, consumer and financial sectors, although gold miners were boosted after last week’s climb in the precious metal. Nikkei 225 was pressured amid the banking sector woes and after the BoJ’s Summary of Opinions provided little in the way of new information whereby it reiterated that the BoJ must patiently maintain monetary easing. Hang Seng and Shanghai Comp. were varied with Hong Kong underperforming on broad weakness across sectors, while the mainland was kept afloat for most of the session after Friday’s surprise RRR cut by the PBoC in an effort to boost liquidity and support the economy, but opted to maintain its benchmark lending rates.

Top Asian News

PBoC 1-Year Loan Prime Rate (Mar) 3.65% vs. Exp. 3.65% (Prev. 3.65%); 5-Year Loan Prime Rate (Mar) 4.30% vs. Exp. 4.30% (Prev. 4.30%)

PBoC warned the collapse of Silicon Valley Bank shows rapid monetary policy shifts in developed economies are having a hazardous impact on financial stability, according to Bloomberg citing comments from Deputy Governor Xuan.

PBoC adviser Cai said China needs household stimulus to boost the recovery and noted that residents' incomes have not grown well in the past few years, so the recovery in consumption is not enough to support economic growth, according to Caijing.

Russian President Putin said he expects total trade volume with China to exceed USD 200bln this year and it is important to increase the share of trade with China conducted in national currencies, according to Reuters.

WHO advisers urged China to release all information related to the origin of the COVID-19 pandemic after new findings were briefly shared on an international database to track pathogens, while they recommended researchers in China investigate upstream sources of animals and animal products present in the Huanan Market before January 1st 2020, according to Reuters.

BoJ Summary of Opinions from the March meeting stated that the BoJ must patiently maintain monetary easing until the price target is achieved and the BoJ must scrutinise without any preset idea the state of market function but must maintain easy policy at present. Furthermore, it stated the BoJ must focus on the risk of losing the chance to meet the price target with a premature policy shift, rather than the risk of being too late in shifting policy and must be mindful of the risk inflation may overshoot expectations.

European bourses are mixed/flat, as marked banking-led pressure has eased throughout the morning following the initial reaction to the UBS-Credit Suisse merger. On this, Credit Suisse and UBS opened lower by over 60% and 8% respectively, but have since eased off lows with the broader SX7P index now ~2% lower vs downside of over 5% at worst. On the merger, attention is on Credit Suisse's AT1 bonds being written off; a detail which pressured such bonds in APAC trade, with HSBC for instance a notable initial laggard on this. Since, we have seen European regulators reiterate that CET instruments are the first to absorb losses, with AT1 only required after their full use. Stateside, futures are in similar proximity to the unchanged mark given the above as participants await updates around First Republic and look ahead to the FOMC.

Top European News

BoE's plans to revamp bank capital rules risk a 25% reduction in lending to small businesses which threatens jobs and economic growth, according to a study by consultants Oxera cited by FT.

PoliticsHomes' Payne reminds that DUP MPs meet today to discuss their stance on Wednesday's Windsor Framework vote, expected to announce their stance on Tuesday.

Moody’s affirmed Greece at Ba3; Outlook revised to Positive from Stable and affirmed Luxembourg at AAA; Outlook Stable, while S&P affirmed Belgium at AA; Outlook Stable.

FX

The DXY has struggled to benefit from the subdued start to the session, with the index near the mid-point of 103.68-103.96 parameters for much of the morning.

Given the tone, the JPY is the standout outperformer with USD/JPY down to 130.55 vs 132.64 peak; though, given the relative pickup in equity performance USD/JPY is now holding above 131.00.

Despite the subdued risk tone, CHF is the underperformer as the market's focus remains on Credit Suisse/UBS; USD/CHF above 0.93 and EUR/CHF above 0.99.

Given their high-beta status, the Antipodeans are also faring poorly with RBA minutes and Kiwi trade data scheduled ahead.

Elsewhere, peers are comparably more contained with EUR/USD holding above 1.0650 and Cable near 1.22.

PBoC set USD/CNY mid-point at 6.8694 vs exp. 6.8701 (prev. 6.9052)

Fixed Income

EGBs and USTs are benefitting from marked haven demand, with Bunds over 140.00 and USTs nearing 117.00 at best, though the benchmarks have eased from highs as equity sentiment improves.

Specifically, Bunds soared to a 140.30 peak vs 137.10 low, but have since pulled back to just below 140.00 as the associated 10yr yield slipped to a 1.92% intraday low.

Stateside, USTs are similar in both direction and magnitude with yields lower across the curve and action more pronounced in the short-end currently; as it stands, market pricing via Reuters is leaning towards the Fed leaving rates unchanged on Wednesday, with around a 40% chance of a 25bp hike implied.

Commodities

WTI and Brent are lower intraday given the broader risk tone and while they are off lows, are yet to stage a 'recovery' akin to that seen in equities; currently, the benchmarks are lower by circa. USD 2/bbl just above USD 64.12/bbl and USD 70.12/bbl respective lows.

Spot gold surpassed USD 2000/oz, but failed to hang onto the level as the DXY makes its way back into positive territory and broader sentiment improves slightly while base metals are moving with equity sentiment and as such are turning incrementally firmer on the session.

Iraq’s Oil Minister said his country is committed to OPEC’s agreed production rates and obliged some oil companies' operations in the south to cut production to come in line with OPEC’s agreed rates, while it was also reported that Iraq and OPEC stressed the importance to coordinate to stabilise prices, according to Reuters.

Iran set April Iranian light crude oil price to Asia at Oman/Dubai plus USD 2.50/bbl, according to Reuters.

India plans to extend export restrictions on diesel and gasoline beyond March 31st, according to Reuters sources.

TotalEnergies (TTE FP) said 34% of operational staff at its refineries and depots conducted a strike on Sunday morning in protest against the government’s move to raise the retirement age by two years, according to Reuters.

Kuwait Oil Company declares a state of emergency re. an oil spill located in west Kuwait; production unaffected.

Geopolitics

Russian President Putin visited Crimea on the 9th anniversary of its annexation from Ukraine and also visited Mariupol in the occupied Donetsk region of Ukraine, while he also met with the top command of Russia’s military operation in Ukraine at the Rostov-on-Don command post in southern Russia, according to Reuters.

Russian President Putin said the visit by Chinese President Xi confirms the special character of the Russian-Chinese partnership and Russia is pinning big hopes on the visit, while he added Russia is expecting a powerful impulse to relations and that relations are at their highest ever point. Putin also said there are no limits or forbidden subjects in relations with China and he is grateful for China’s balanced line on events in Ukraine, as well as welcomes China’s willingness to play a constructive role in solving the Ukrainian crisis. Furthermore, Putin said that they are worried about dangerous actions that could undermine global nuclear security and Russia is open to a diplomatic settlement of the Ukraine crisis but rejects ultimatums, according to Reuters.

Chinese President Xi said China has always taken an objective and impartial position on the situation in Ukraine and has made efforts to promote reconciliation and peace negotiations, according to Rossiiskaya Gazeta.

ICC judge issued an arrest warrant for Russian President Putin over alleged war crimes related to ‘unlawful deportation’ of Ukrainian children, according to The Guardian. It was also reported that German Chancellor Scholz said ICC is an important institution that has been given a mandate through international treaties and noted that nobody is above the law which is becoming clear now, according to Reuters.

Ukrainian President Zelensky’s Chief of Staff and several top security officials including the Defence Minister held a call with US counterparts to discuss military aid for Ukraine, according to Reuters.

Ukrainian Infrastructure Minister said the Black Sea grain deal has been extended for 120 days which is longer than the 60-day touted by Russia, while a UN spokesman confirmed the extension of the export deal but didn’t specify the length of the renewal, according to Reuters.

EU foreign policy chief Borrell said an agreement was reached on ways to implement an EU-backed deal on normalising ties between Serbia and Kosovo, while he added that the sides agreed to implement their respective obligations in good faith.

Saudi Arabia’s King Salman invited Iranian President Raisi to visit Riyadh, while it was also reported that Iran’s Foreign Minister agreed to hold a meeting at the foreign minister level with Saudi Arabia and said that Iran has declared a readiness to reopen embassies. In other news, Iraq and Iran signed a deal to tighten their border security.

South Korea said that North Korea fired a short-range ballistic missile off the east coast into the sea on Sunday which flew 800km before hitting a target and is a clear violation of the UN Security Council resolution. In relevant news, G7 foreign ministers said they regret inaction by the UN Security Council regarding North Korea’s missile tests and that the March 16th ICBM launch undermines international peace, according to Reuters.

North Korea confirmed it conducted exercises aimed at improving tactical nuclear capability on March 18th-19th and said the US and South Korea are expanding joint military drills aimed at North Korea involving US nuclear assets and its exercises are meant to send strong warnings against US and South Korea. Furthermore, North Korean leader Kim said the country should be ready to conduct nuclear attacks at any time in a deterrence of war, according to KCNA.

US Event Calendar

Nothing major scheduled

DB's Jim Reid concludes the overnight wrap

This weekend felt like being transported back into 2007-2008 in many respects with a race-against-time deal between UBS and Credit Suisse being put together in full view of the market. The most remarkable thing about yesterday was the huge swings in Credit Suisse AT1s on a Sunday. Clips of the $17.3bn of outstanding CS AT1 bonds seemed to trade at both ends of a mid-20s to around 70c range as the outline of the UBS deal filtered through. It was eventually a shock that the AT1s were zeroed in the deal even as UBS eventually bought CS for $3.3bn, a firmly positive number. This was however less than half what they were worth at the close on Friday and down 99% from their peak pre-GFC.

The decisions to wipe out AT1 bondholders is going to be the biggest issue medium and longer-term for the European banking sector, especially when the company was bought with a positive value yesterday. It's hard to argue with the morals of it but it will likely increase the cost of capital for banks which could lead to an additional tightening of lending conditions. So that c.$17bn of debt destruction could eventually be worth multiples of that to the wider European economy and in other regions too. Selected Asian AT1 securities are trading around 5-10% down as we type and HSBC equity is around -6% in Hong Kong so this serves as a benchmark for the European banking open.

The good news at the macro level is that the CS situation has been dealt with and there are no obvious European next shoes to drop at this stage. CS had been decoupled from the rest of the continents' banking sector for months now and therefore was by far and away the weakest link when the US regional banking woes began less than 2 weeks ago. So the market has now got to balance the reduction of systemic risk with the likely higher cost of some forms of bank capital. There will also be nervousness as to how easy it was to change laws and market conventions in order to get this deal done. Some risk premium will surely be factored in to the cost of capital for the sector now.

Meanwhile, in a coordinated global response, the Fed in a statement along with five other central banks - including the BOE, the BOJ, the ECB and the SNB - last night announced that they would enhance dollar swap lines i.e., to increase the frequency of swap line agreements from weekly to daily, beginning March 20 and will continue “at least” through the end of next month. In doing so, the central banks indicated that the move would serve as an “important backstop” amid financial market unease, thereby helping to keep credit flowing to households and businesses.

Overall, Asian equity markets have started the week on a weaker footing with the Hang Seng (-2.56%) leading losses across the region, with the Nikkei (-1.01%) and the KOSPI (-0.46%) also dipping in early trade. Elsewhere, stocks in mainland China are bucking the regional negative trend with the CSI (+0.12%) and the Shanghai Composite (+0.12%) both trading slightly higher. Note their was a 25bps RRR cut on Friday.

Outside of Asia, US stock futures tied to the S&P 500 (+0.12%) and NASDAQ 100 (+0.23%) are relatively flat which helps after the weekend news but then again as you'll see from the weekly review at the end the S&P 500 was higher last week in the face of incredible turmoil elsewhere. Meanwhile, yields on 10yr US Treasuries are stable while 2yr yields (+2.92bps) briefly touched 4% before sliding back to 3.87% as we go to press.

Moving forward, it's hard not to have sympathy for the Fed this week. Any criticism of their policy should probably be more directed to the actions of 2020-2021 for keeping policy excessively too loose as government spending, money supply and inflation was surging. Today they are in a catch-22 position where the excesses of those days (and earlier) are now unravelling while inflation is still way above target. Their rate decision on Wednesday will be the undoubted non-banking related highlight of the week but we will also have the BoE meeting (Thursday), UK CPI (Wednesday), Japan CPI (Thursday), flash global PMIs (Friday) which might capture a small amount of the turmoil period, and importantly Chinese President Xi Jinping will be in Moscow from today to Wednesday.

After the FOMC, it will be the BoE's turn on Thursday to decide on rates. Our UK economists preview the meeting here and expect a final +25bps hike as well as likely dovish forward guidance amid concerns over overtightening risks. The decision will follow a host of UK inflation data released on Wednesday. Also on Thursday markets may follow the SNB meeting more closely than usual following this week's turmoil around Credit Suisse.

Aside from several monetary policy decisions, there will also be a plenty of central bank speakers, especially from the ECB, including President Lagarde (twice), following last week's +50bps hike.

In the US, aside from the PMIs investors will also get durable goods orders (DB forecast -0.5% vs -4.5% in January) on Friday and a host of regional Fed indicators throughout the week to gauge economic sentiment. Housing market data including existing home sales (tomorrow) and new home sales (Thursday) are also due.

Over in Europe, other key data will include the PPI (today) and the ZEW survey (tomorrow) for Germany, Eurozone consumer confidence on Thursday and UK consumer confidence and retail sales on Friday.

Moving on to Japan, the key release will be the CPI report on Thursday. Our Chief Japan Economist (full preview of the week ahead here) expects government subsidies for electricity and gas to weigh on core CPI inflation (3.2% vs +4.2% in January) but core-core CPI ex. energy to pick up 3.4% (3.2%) but reach its peak for the cycle.

Looking back on a tumultuous last week now. On Friday, with market volatility already elevated from the growing concerns around the global financial system the preliminary University of Michigan sentiment survey dropped -4.6pts to 63.4. That was just the second monthly drop since last June, and the lowest reading since December. The declines pre-dated the SVB collapse. If one wanted to find a positive in the report inflation expectations were lower with 5-10yr expectations down to 2.8% (2.9% expected), while the 1yr inflation expectation was 3.8% (4.1% expected). That’s the lowest 1yr expectations have been since April 2021.

That was just the last link in a chain of market moving events last week that repriced Fed futures across the curve. Expectations for a 25bps hike at the March meeting is now at just 60% with a 15.0bp hike priced in. That is down -18.3bps on the week and -4.2bps on Friday, as well as -27.8bps since Powell’s testimony before the Senate Banking Committee the week before last. At the same time, the expected terminal rate ended the week at 4.794% by the May meeting after starting the week at 5.285% at the June meeting and being as high as 5.691% at the September meeting on the prior Wednesday before the SVB news broke. Futures are also now pricing in nearly -96bps of rate cuts by year-end after starting the week with -40bps of cuts priced.

10yr Treasury yields fell back another -14.8bps on Friday and -27.0bps over the course of the week to their lowest level since early-February at 3.429%. The 2yr yield saw a much bigger move, coming down -74.9bps last week (-32.0bps on Friday) to their lowest level since September 2022. On this side of the pond, 10yr bund yields fell back -40.0bps (-18.2bps on Friday) last week to 2.108%, its lowest point since the first week of February. The 2yr bund yield fell by -71bps last week (-22.0bps Friday) in its most significant weekly down move since September 1992.

While sovereign bonds outperformed last week, US equities whipsawed with a large amount of dispersion. Even though the S&P 500 closed the five days higher, US banks continued to selloff with the KBW bank index down -14.55% last week (-5.25% Friday), with major banks like JPM (-5.87%), BofA (-8.09%), Citi (-8.46%), and GS (-7.26%) outperforming while the regional bank ETF KRE was down -14.30% last week. With CS seeing pressure from a lack of depositor and investor confidence, the SNB offered the Swiss bank a 50bn franc credit line. However this was not enough to stop the stock from ending the week -25.48% lower (-8.01% Friday), while European Banks at large were down -13.40% (-2.72% Friday) leaving the index up just +1.2% YTD. The STOXX 600 was down -3.85% week-on-week (-1.21% on Friday), whilst the CAC and DAX fell -4.09% (-1.43% on Friday) and -4.28% (-1.33% on Friday) respectively.

With risk markets selling off, credit spreads widened significantly on the week once again. The Euro Crossover HY CDS index was +66.7bps wider (+18.8bps wider Friday) and EUR IG CDS +18.1bps wider on the week (+3.8bps Friday). EUR HY CDS is now +18.9bps wider YTD, with EUR IG +9.9bps wider since the start of the year. US credit also significantly widened again as the US HY CDS index was +31.6bps wider (+26.8bps Friday) with IG +4.8bps wider following a +5.1bps move on Friday. The weekly widening has left USD HY CDS +45.7bps wider YTD, while US IG CDS was +5.8bps wider YTD.

Finally in commodities, industrial inputs sold off as recession fears rose. Brent crude fell back -11.85% (-2.32% on Friday) and WTI was down -12.96% (-2.36% on Friday), meanwhile European natural gas futures reversed the prior week’s significant rally with energy prices falling -18.92% week-on-week (-3.35%). Copper was down -3.26% (+0.72% Friday) while the overall Bloomberg Commodity index was down -1.87% (-0.16% Friday). With the risk-off tone throughout markets, Gold was a notable outperformer with the precious metal up +6.48% on the week (+3.63% Friday) in its best weekly performance since Covid to close at its highest level in a year at $1989/oz.

Meet the Bitcoinetas, a fleet of transformative vehicles on a mission to spread the bitcoin message everywhere they go. From Argentina to South Africa,…

You may have seen that picture of Michael Saylor in a bitcoin-branded van, with a cheerful guy right next to the car door. This one:

Ariel Aguilar and La Bitcoineta European Edition at BTC Prague.

That car is the Bitcoineta European Edition, and the cheerful guy is Ariel Aguilar. Ariel is part of the European Bitcoineta team, and has previously driven another similar car in Argentina. In fact, there are currently five cars around the world that carry the name Bitcoineta (in some cases preceded with the Spanish definite article “La”).

Argentina: the original La Bitcoineta

The story of Bitcoinetas begins with the birth of 'La Bitcoineta' in Argentina, back in 2017. Inspired by the vibrancy of the South American Bitcoin community, the original Bitcoineta was conceived after an annual Latin American Conference (Labitconf), where the visionaries behind it recognized a unique opportunity to promote Bitcoin education in remote areas. Armed with a bright orange Bitcoin-themed exterior and a mission to bridge the gap in financial literacy, La Bitcoineta embarked on a journey to bring awareness of Bitcoin's potential benefits to villages and towns that often remained untouched by mainstream financial education initiatives. Operated by a team of dedicated volunteers, it was more than just a car; it was a symbol of hope and empowerment for those living on the fringes of financial inclusion.

The concept drawing for La Bitcoineta from December 2017.

Ariel was part of that initial Argentinian Bitcoineta team, and spent weeks on the road when the car became a reality. The original dream to bring bitcoin education even to remote areas within Argentina and other South American countries came true, and the La Bitcoineta team took part in dozens of local bitcoin meetups in the subsequent years.

The original La Bitcoineta from Argentina.

One major hiccup came in late 2018, when the car was crashed into while parked in Puerto Madryn. The car was pretty much destroyed, but since the team was possessed by a honey badger spirit, nothing could stop them from keeping true to their mission. It is a testament to the determination and resilience of the Argentinian team that the car was quickly restored and returned on its orange-pilling quest soon after.

Argentinian Bitcoineta after a major accident (no-one got hurt); the car was restored shortly after.

Over the more than 5 years that the Argentinian Bitcoineta has been running, it has traveled more than 80,000 kilometers - and as we’ll see further, it inspired multiple similar initiatives around the world.

In early 2021, the president of El Salvador passed the Bitcoin Law, making bitcoin legal tender in the country. The Labitconf team decided to celebrate this major step forward in bitcoin adoption by hosting the annual conference in San Salvador, the capital city of El Salvador. And correspondingly, the Argentinian Bitcoineta team made plans for a bold 7000-kilometer road trip to visit the Bitcoin country with the iconic Bitcoin car.

However, it proved to be impossible to cross so many borders separating Argentina and Salvador, since many governments were still imposing travel restrictions due to a Covid pandemic. So two weeks before the November event, the Labitconf team decided to fund a second Bitcoineta directly in El Salvador, as part of the Bitcoin Beach circular economy. Thus the second Bitcoineta was born.

Salvadoran’s Bitcoineta operates in the El Zonte region, where the Bitcoin Beach circular economy is located.

The eye-catching Volkswagen minibus has been donated to the Bitcoin Beach team, which uses the car for the needs of its circular economy based in El Zonte.

Late 2021 saw one other major development in terms of grassroots bitcoin adoption. On the other side of the planet, in South Africa, Hermann Vivier initiated the Bitcoin Ekasi project. “Ekasi” is a colloquial term for a township, and a township in the South African context is an underdeveloped urban area with a predominantly black population, a remnant of the segregationist apartheid regime. Bitcoin Ekasi emerged as an attempt to introduce bitcoin into the economy of the JCC Camp township located in Mossel Bay, and has gained a lot of success on that front.

Bitcoin Ekasi was in large part inspired by the success of the Bitcoin Beach circular economy back in El Salvador, and the respect was mutual. The Bitcoin Beach team thus decided to pass on the favor they received from the Argentinian Bitcoineta team, and provided funds to Bitcoin Ekasi for them to build a Bitcoineta of their own.

Bitcoin Ekasi’s Bitcoineta as seen at the Adopting Bitcoin Cape Town conference.Bitcoin Ekasi’s Bitcoineta as seen at the Adopting Bitcoin Cape Town conference. Hermann Vivier is seen in the background. South African Bitcoineta serves the needs of Bitcoin Ekasi, a local bitcoin circular economy in the JCC Camp township.

Bitcoin Ekasi emerged as a sister organization of Surfer Kids, a non-profit organization with a mission to empower marginalized youths through surfing. The Ekasi Bitcoineta thus partially serves as a means to get the kids to visit various surfer competitions in South Africa. A major highlight in this regard was when the kids got to meet Jordy Smith, one of the most successful South African surfers worldwide.

Coincidentally, South African surfers present an intriguing demographic for understanding Bitcoin due to their unique circumstances and needs. To make it as a professional surfer, the athletes need to attend competitions abroad; but since South Africa has tight currency controls in place, it is often a headache to send money abroad for travel and competition expenses. The borderless nature of Bitcoin offers a solution to these constraints, providing surfers with an alternative means of moving funds across borders without any obstacles.

Photo taken at the South African Junior Surfing Championships 2023. Back row, left to right:

Mbasa, Chuma, Jordy Smith, Sandiso. Front, left to right: Owethu, Sibulele.

To find out more about Bitcoineta South Africa and the non-profit endeavors it serves, watch Lekker Feeling, a documentary by Aubrey Strobel:

The European Bitcoineta started its journey in early 2023, with Ariel Aguilar being one of the main catalysts behind the idea. Unlike its predecessors in El Salvador and South Africa, the European Bitcoineta was not funded by a previous team but instead secured support from individual donors, reflecting a grassroots approach to spreading financial literacy.

European Bitcoineta sports a hard-to-overlook bitcoin logo along with the message “Bitcoin is Work. Bitcoin is Time. Bitcoin is Hope.”

The European Bitcoineta is a Mercedes box van adorned with a prominent Bitcoin logo and inspiring messages, and serves as a mobile hub for education and discussion at numerous European Bitcoin conferences and local meetups. Inside its spacious interior, both notable bitcoiners and bitcoin plebs share their insights on the walls, fostering a sense of camaraderie and collaboration.

Inside the European Bitcoineta, one can find the wall of fame, where visitors can read messages from prominent bitcoiners such as Michael Saylor, Uncle Rockstar, Javier Bastardo, Hodlonaut, and many others.On the “pleb wall”, any bitcoiner can share their message (as long as space permits).

Introduced in December 2023 at the Africa Bitcoin Conference in Ghana, the fifth Bitcoineta was donated to the Ghanaian Bitcoin Cowries educational initiative as part of the Trezor Academy program.

Bitcoineta West Africa was launched in December 2023 at the Africa Bitcoin Conference. Among its elements, it bears the motto of the Trezor Academy initiative: Bitcoin. Education. Freedom.

Bitcoineta West Africa was funded by the proceeds from the bitcoin-only limited edition Trezor device, which was sold out within one day of its launch at the Bitcoin Amsterdam conference.

With plans for an extensive tour spanning Ghana, Togo, Benin, Nigeria, and potentially other countries within the ECOWAS political and economic union, Bitcoineta West Africa embodies the spirit of collaboration and solidarity in driving Bitcoin adoption and financial inclusion throughout the Global South.

Bitcoineta West Africa surrounded by a group of enthusiastic bitcoiners at the Black Star Square, Accra, Ghana.

All the Bitcoineta cars around the world share one overarching mission: to empower their local communities through bitcoin education, and thus improve the lives of common people that might have a strong need for bitcoin without being currently aware of such need. As they continue to traverse borders and break down barriers, Bitcoinetas serve as a reminder of the power of grassroots initiatives and the importance of financial education in shaping a more inclusive future. The tradition of Bitcoinetas will continue to flourish, and in the years to come we will hopefully encounter a brazenly decorated bitcoin car everywhere we go.

If the inspiring stories of Bitcoinetas have ignited a passion within you to make a difference in your community, we encourage you to take action! Reach out to one of the existing Bitcoineta teams for guidance, support, and inspiration on how to start your own initiative. Whether you're interested in spreading Bitcoin education, promoting financial literacy, or fostering empowerment in underserved areas, the Bitcoineta community is here to help you every step of the way. Together, we will orange pill the world!

This is a guest post by Josef Tetek. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite. Such isn’t surprising given the evolution…

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite. Such isn’t surprising given the evolution of the market into a “casino” following the pandemic, where retail traders have increased their speculative appetites.

“Such is unsurprising, given that retail investors often fall victim to the psychological behavior of the “fear of missing out.” The chart below shows the “dumb money index” versus the S&P 500. Once again, retail investors are very long equities relative to the institutional players ascribed to being the “smart money.””

“The difference between “smart” and “dumb money” investors shows that, more often than not, the “dumb money” invests near market tops and sells near market bottoms.”

That enthusiasm has increased sharply since last November as stocks surged in hopes that the Federal Reserve would cut interest rates. As noted by Sentiment Trader:

“Over the past 18 weeks, the straight-up rally has moved us to an interesting juncture in the Sentiment Cycle. For the past few weeks, the S&P 500 has demonstrated a high positive correlation to the ‘Enthusiasm’ part of the cycle and a highly negative correlation to the ‘Panic’ phase.”

That frenzy to chase the markets, driven by the psychological bias of the “fear of missing out,” has permeated the entirety of the market. As noted in “This Is Nuts:”

“Since then, the entire market has surged higher following last week’s earnings report from Nvidia (NVDA). The reason I say “this is nuts” is the assumption that all companies were going to grow earnings and revenue at Nvidia’s rate. There is little doubt about Nvidia’s earnings and revenue growth rates. However, to maintain that growth pace indefinitely, particularly at 32x price-to-sales, means others like AMD and Intel must lose market share.”

Of course, it is not just a speculative frenzy in the markets for stocks, specifically anything related to “artificial intelligence,” but that exuberance has spilled over into gold and cryptocurrencies.

Birds Of A Feather

There are a couple of ways to measure exuberance in the assets. While sentiment measures examine the broad market, technical indicators can reflect exuberance on individual asset levels. However, before we get to our charts, we need a brief explanation of statistics, specifically, standard deviation.

“Like a rubber band that has been stretched too far – it must be relaxed in order to be stretched again. This is exactly the same for stock prices that are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average.”

The idea of “stretching the rubber band” can be measured in several ways, but I will limit our discussion this week to Standard Deviation and measuring deviation with “Bollinger Bands.”

“Standard Deviation” is defined as:

“A measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is calculated as the square root of the variance.”

In plain English,this meansthat the further away from the average that an event occurs, the more unlikely it becomes. As shown below, out of 1000 occurrences, only three will fall outside the area of 3 standard deviations. 95.4% of the time, events will occur within two standard deviations.

A second measure of “exuberance” is “relative strength.”

“In technical analysis, the relative strength index (RSI) is a momentum indicator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. The RSI is displayed as an oscillator (a line graph that moves between two extremes) and can read from 0 to 100.

Traditional interpretation and usage of the RSI are that values of 70 or above indicate that a security is becoming overbought or overvalued and may be primed for a trend reversal or corrective pullback in price. An RSI reading of 30 or below indicates an oversold or undervalued condition.” – Investopedia

With those two measures, let’s look at Nvidia (NVDA), the poster child of speculative momentum trading in the markets. Nvidia trades more than 3 standard deviations above its moving average, and its RSI is 81. The last time this occurred was in July of 2023 when Nvidia consolidated and corrected prices through November.

Interestingly, gold also trades well into 3 standard deviation territory with an RSI reading of 75. Given that gold is supposed to be a “safe haven” or “risk off” asset, it is instead getting swept up in the current market exuberance.

The same is seen with digital currencies. Given the recent approval of spot, Bitcoin exchange-traded funds (ETFs), the panic bid to buy Bitcoin has pushed the price well into 3 standard deviation territory with an RSI of 73.

In other words, the stock market frenzy to “buy anything that is going up” has spread from just a handful of stocks related to artificial intelligence to gold and digital currencies.

It’s All Relative

We can see the correlation between stock market exuberance and gold and digital currency, which has risen since 2015 but accelerated following the post-pandemic, stimulus-fueled market frenzy. Since the market, gold and cryptocurrencies, or Bitcoin for our purposes, have disparate prices, we have rebased the performance to 100 in 2015.

Gold was supposed to be an inflation hedge. Yet, in 2022, gold prices fell as the market declined and inflation surged to 9%. However, as inflation has fallen and the stock market surged, so has gold. Notably, since 2015, gold and the market have moved in a more correlated pattern, which has reduced the hedging effect of gold in portfolios. In other words, during the subsequent market decline, gold will likely track stocks lower, failing to provide its “wealth preservation” status for investors.

The same goes for cryptocurrencies. Bitcoin is substantially more volatile than gold and tends to ebb and flow with the overall market. As sentiment surges in the S&P 500, Bitcoin and other cryptocurrencies follow suit as speculative appetites increase. Unfortunately, for individuals once again piling into Bitcoin to chase rising prices, if, or when, the market corrects, the decline in cryptocurrencies will likely substantially outpace the decline in market-based equities. This is particularly the case as Wall Street can now short the spot-Bitcoin ETFs, creating additional selling pressure on Bitcoin.

Just for added measure, here is Bitcoin versus gold.

Not A Recommendation

There are many narratives surrounding the markets, digital currency, and gold. However, in today’s market, more than in previous years, all assets are getting swept up into the investor-feeding frenzy.

Sure, this time could be different. I am only making an observation and not an investment recommendation.

However, from a portfolio management perspective, it will likely pay to remain attentive to the correlated risk between asset classes. If some event causes a reversal in bullish exuberance, cash and bonds may be the only place to hide.

BUFFALO, NY- March 11, 2024 – Impact Journals publishes scholarly journals in the biomedical sciences with a focus on all areas of cancer and aging research. Aging is one of the most prominent journals published by Impact Journals.

Credit: Impact Journals

BUFFALO, NY- March 11, 2024 – Impact Journals publishes scholarly journals in the biomedical sciences with a focus on all areas of cancer and aging research. Aging is one of the most prominent journals published by Impact Journals.

Impact Journals will be participating as an exhibitor at the American Association for Cancer Research (AACR) Annual Meeting 2024 from April 5-10 at the San Diego Convention Center in San Diego, California. This year, the AACR meeting theme is “Inspiring Science • Fueling Progress • Revolutionizing Care.”

Visit booth #4159 at the AACR Annual Meeting 2024 to connect with members of the Agingteam.

About Aging-US:

Agingpublishes research papers in all fields of aging research including but not limited, aging from yeast to mammals, cellular senescence, age-related diseases such as cancer and Alzheimer’s diseases and their prevention and treatment, anti-aging strategies and drug development and especially the role of signal transduction pathways such as mTOR in aging and potential approaches to modulate these signaling pathways to extend lifespan. The journal aims to promote treatment of age-related diseases by slowing down aging, validation of anti-aging drugs by treating age-related diseases, prevention of cancer by inhibiting aging. Cancer and COVID-19 are age-related diseases.

Agingis indexed and archived byPubMed/Medline (abbreviated as “Aging (Albany NY)”), PubMed Central, Web of Science: Science Citation Index Expanded (abbreviated as “Aging‐US” and listed in the Cell Biology and Geriatrics & Gerontology categories), Scopus (abbreviated as “Aging” and listed in the Cell Biology and Aging categories), Biological Abstracts, BIOSIS Previews, EMBASE, META (Chan Zuckerberg Initiative) (2018-2022), and Dimensions (Digital Science).

Please visit our website at www.Aging-US.com and connect with us:

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}