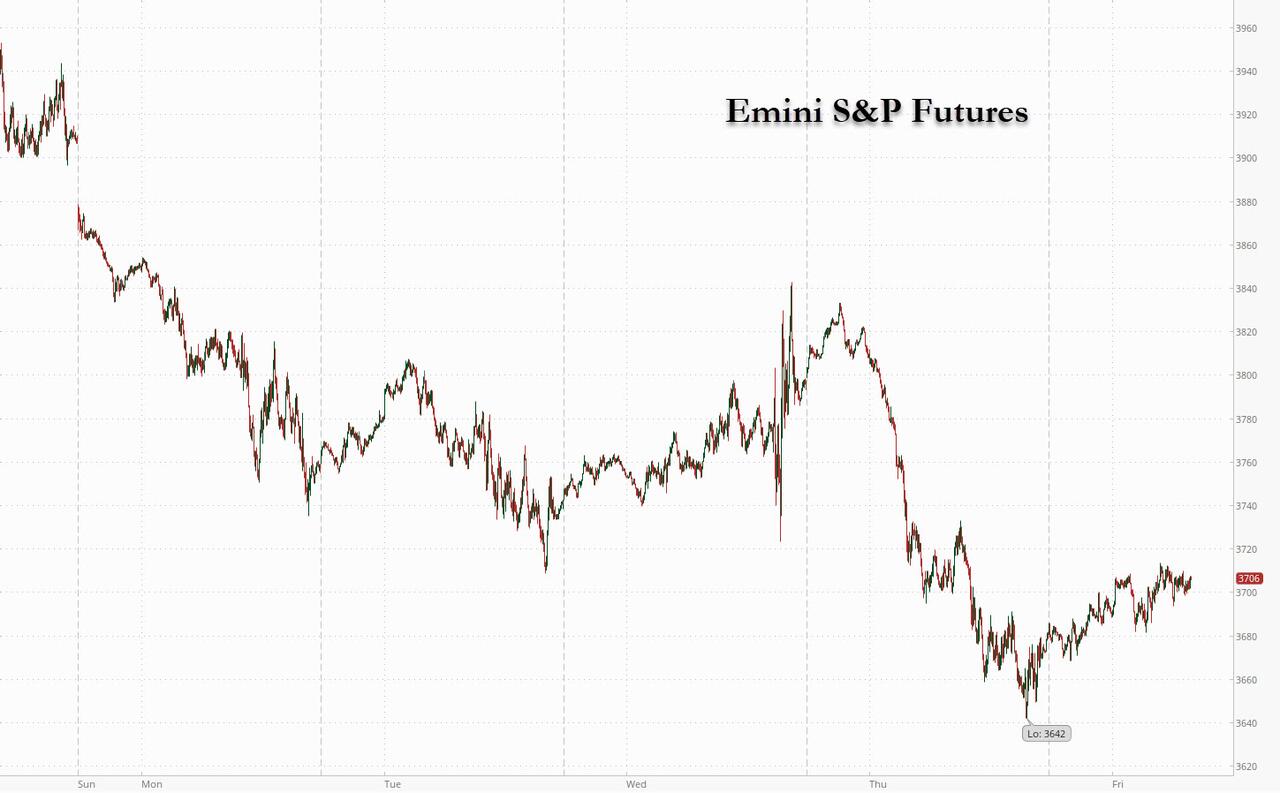

Futures Rebound, Yen Crashes To End Turbulent Week On $3.4 Trillion Quad-Witch Day

Ending a rollercoaster - but mostly lower - week for risk assets around the globe which saw the Fed hike the most since 1994, a shock Swiss National Bank hike and the latest boost in UK borrowing costs, as well as a bevy of central banks surprising hawkishly, stocks in Europe finally rebounded after hitting an 18 month low earlier this week, while US equity futures were bid Friday after a rout triggered by fears of recession pushed the S&P into a bear market on Monday. S&P futures rose 1% and Nasdaq futures rebounded 1.2% signaling steadier sentiment compared with Thursday’s plunge in US shares to the lowest since late 2020, after the BOJ refused to change its Yield Curve Control conditions, sending the Yen plunging, and helping the dollar snap two days of losses as Treasury yields were flat with the 10Y around 3.21%. The Stoxx Europe 600 index jumped about 1.2% after hitting its lowest level in more than a year.

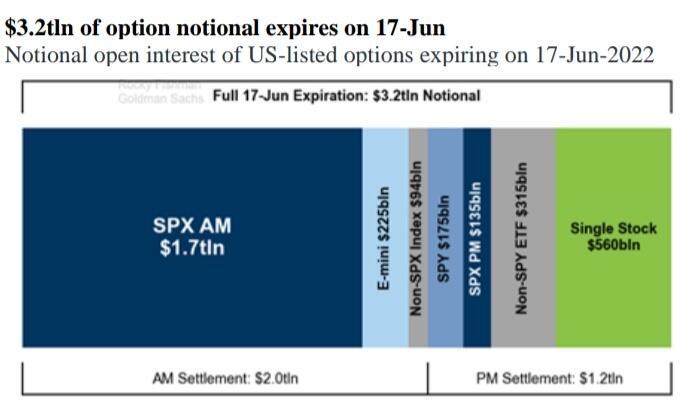

Friday also brings an absolutely massive triple-witching, and although Bloomberg believes that the roughly $3.2 trillion in options expiry may lead to short covering, which could bring temporary relief for the stock market...

... we disagree, as the bulk of open interest is around 4,100 or several hundred points above spot, meaning moves today will have little impact on "derivative tails wagging the dog."

In any case, absent a massive 5% rally today which sends stocks into the green, the S&P is looking at being down 10 of the past 11 weeks, a feat that has been repeated just once in history: 1970. Let's go Brandon!

In premarket trading, Revlon surged after a report that Reliance Industries Ltd. is considering buying the company. Major technology and internet stocks were higher, rebounding from Thursday’s rout. Apple Inc., Microsoft Corp. and Meta Platforms Inc. were among those advancing. US-listed Chinese stocks also soared in the premarket, a day after the Nasdaq Golden Dragon China Index’s 4.4% slide, with e-commerce giant JD.com (JD US) leading the pack ahead of the closely watched 618 online shopping event. Additionally, Chinese tech giants such as Alibaba surges on a Reuters report that China’s central bank has accepted Ant Group’s application to set up a financial holding company. Alibaba shares surge 11% following the report. Among other large- cap Chinese internet stocks, JD.com +9.3%, Pinduoduo +7.5%, Baidu +5.6%. Here are some of the biggest U.S. movers today:

Adobe (ADBE US) shares fall 4% in premarket trading on Friday after the software company cut its revenue forecast for the full year as it expects currency fluctuations, seasonal shifts in demand and the decision to end sales in Russia and Belarus to weigh on its business.

Roku (ROKU US) shares climb 3.9% in premarket trading after the company and Walmart said they entered a pact to enable streamers to purchase featured products fulfilled by Walmart directly on Roku.

US Steel (X US) shares rise 5.2% in US premarket trading after the metal giant’s 2Q22 guidance came in well above consensus estimates, according to Morgan Stanley analysts led by Carlos De Alba.

Rhythm (RYTM US) shares are 13% lower in US premarket trading after the company’s Imcivree injection failed to win approval for one of the two supplemental indications it sought and the company announced a financing agreement with HealthCare Royalty Partners.

Revlon (REV US) shares surge 65% in premarket trading after Reliance Industries is considering buying Revlon in the US, ET Now reports, citing people familiar with the matter.

Markets are rounding off a turbulent week buffeted by interest-rate increases which are rapidly draining liquidity, sparking losses in a range of assets. Global stocks face one of their worst weeks since pandemic-induced turmoil of 2020. The question is how far assets have to sink before the tightening cycle is fully priced in. Bucking the global hawkish trend, Japan, retianed super-easy monetary policy and yield curve control, defying pressure to track the global trend toward tighter settings. As a result, the Japanese yen is on course for its biggest fall against the dollar since March 2020 while Japan’s 10-year bond yield retreated below the Bank of Japan’s cap of 0.25%, after earlier hitting 0.265%, the highest since 2016. The Swiss franc surged to its highest level against the yen since 1980.

“Investors have to ask themselves how long the rate-hiking cycle will go and how deep the economic slowdown will be,” said Michael Strobaek, global chief investment officer at Credit Suisse Group AG, which is overweight equities and recently closed its underweight position in bonds. “Peak hawkishness, i.e. the peak in expectations repricing, might be close. Once we are there, it is not only possible but likely that we will see a rebound in both equities and bonds. However, this rebound will be very difficult to time.”

Despite the ongoing slow-motion crash, US stocks attracted another $14.8 billion in the week to June 15, their sixth consecutive week of additions, according to EPFR Global data. In total, $16.6 billion flowed into equities globally in the period, while bonds had the largest redemptions since April 2020 and just over $50 billion exited cash, the data showed.

European equities climbed after a choppy start. Euro Stoxx 600 rallied 1.4%. FTSE MIB outperforms peers, adding 1.7%. European real estate companies are among the best performers, rebounding after several days of losses following concerns higher interest rates will weigh on the sector’s financing abilities. Sweden’s Samhallsbyggnadsbolaget i Norden (SBB) rises as much as 10%, Aroundtown +6.5%, Wallenstam +5.9%, Vonovia +4.9%. Here are some of the biggest European movers:

Nokian Renkaat shares gain as much as 11% after the Finnish tire manufacturer raised its net sales guidance for 2022 while also keeping its profit guidance intact.

Italy’s FTSE MIB index rises as much as 2%, leading gains among major European stock markets; Italy-Germany 10-year bond yield spread falls to one- month low. Best performers on the index include Campari +5.4%, Pirelli +5.3%, DiaSorin +5.1%, Recordati +4%

Ferrari gains as much as 2.4% in the wake of upgrades from Intesa Sanpaolo and Banca Akros after the luxury carmaker unveiled its electrification strategy on Thursday.

Glencore climbs as much as 3.9% in London after the commodities group said its first-half trading profit will be bigger than it typically reports for an entire year.

Playtech rises as much as 6.4% after the gambling operator announced the deadline for TTB to make a firm offer has been extended to next month.

Lisi advances as much as 9.6% after Kepler Cheuvreux upgraded the Boeing supplier to buy, saying its post-Covid recovery isn’t yet priced in.

Volvo Cars falls as much as 5.4% to the lowest since April after DNB cut its recommendation on the shares to sell due to falling demand, also noting risks related to the Polestar SPAC listing.

Rexel drops as much as 3.9% as Kepler Cheuvreux analyst William Mackie cuts his recommendation to hold from buy, citing the “rapidly rising probability of a recession.”

Italian bonds led a rally in European debt after European Central Bank President Christine Lagarde pledged that borrowing costs of more indebted nations in the euro-area won’t be allowed to spiral out of control. Italy’s 10-year yield fell 20 basis points and German equivalents dropped six basis points.

Asian stocks tumbled to a two-year low as traders fear the global rush to hike interest rates may result in a steep economic downturn. The MSCI Asia Pacific Index slumped as much as 1.5% Friday. The measure has fallen every session this week, and is on track to post its largest weekly drop since since the early days of the pandemic in March 2020. Asia stocks have fallen along with global peers as concerns over the potential for more jumbo rate hikes by the Federal Reserve, which raised its benchmark by 75 basis points on Wednesday, triggered a broad market rout. As the global campaign to rein in decades-high inflation continues, investors worry policy tightening may become overdone and throw major economies into recessions. Japanese shares led Friday’s slump in Asia, with the decision by the Bank of Japan to keep its ultra-loose monetary settings unchanged providing limited fillip as volatility in the yen grows. Stocks in China and Hong Kong bucked the regional selloff, as Beijing’s pro-growth policy lends support to views that Chinese equities can keep outperforming. Read: Yen Tumbles as BOJ Stands Pat, Makes Rare Reference to FX Market “In the immediate short term (next 2-3 months), we continue to expect Asian stocks to remain volatile,” Chetan Seth, Asia Pacific equity strategist at Nomura Holdings in Singapore, wrote in a note.“However, we do expect some stabilization into late 3Q as equity valuations reset and positive catalysts emerge.” The catalysts Nomura is looking for are the Fed turning less hawkish as US inflation shows signs of softening and China loosening its Covid-Zero stance. Equity benchmarks in Australia and Vietnam were the other big losers in Asia on Friday, with each dropping more than 1.5%.

Japanese stocks trimmed losses as the yen weakened after the Bank of Japan’s decision to maintain its easy-money policy. The Topix fell 1.7% to 1,835.90 as of market close, while the Nikkei declined 1.8% to 25,963.00. Both gauges had been down more than 2.6% earlier in the day. The yen was down 1.3% to around 134 per dollar. Toyota Motor Corp. contributed the most to the Topix Index decline, decreasing 3.6%. Out of 2,170 shares in the index, 423 rose and 1,689 fell, while 58 were unchanged. The Topix fell 5.5% this week, its worst since April 2020. BOJ Holds Firm to Deepen Outlier Status, Keep Pressure on Yen “If the yen further weakens, this will help the Nikkei 225 to remain firm to some extent,” said Makoto Furukawa, chief portfolio strategist at Mitsubishi UFJ Morgan Stanley. “The Japanese stock market is not so different from the global trend, and monetary policy that comes out from the US and Europe is much more important for Japanese equities.”

Key stock gauges in India completed their worst weekly declines in more than two years as spiraling inflation and rate hikes by central banks dampened the outlook for business recovery. The S&P BSE Sensex slipped 0.3% to 51,360.42 in Mumbai, bringing its weekly decline to 5.4%, the most since May 2020. The NSE Nifty 50 Index dropped 0.4% on Friday, taking its tumble to 5.6%. Tata Consultancy Services lost 1.7% and was the biggest drag on the Sensex, which had 22 of the 30 member stocks trade lower. Fifteen of 19 sectoral indexes compiled by BSE Ltd. declined, led by a gauge of oil and gas companies. Among central bank monetary-policy measures this week, the US Federal Reserve made its biggest increase in policy rates since 1994. India’s markets “are largely taking cues from the global markets, in absence of any major domestic event,” Ajit Mishra, vice-president research at Religare Broking Ltd. wrote in a note. Foreign institutional investors have withdrawn $25.7 billion from Indian stocks this year through June 15, and the sell-off is headed for its ninth consecutive month. “We reiterate our negative view on markets and suggest continuing with the ‘sell on rise’ approach,” according to the note.

In FX, Bloomberg dollar spot index rose by around 0.4% as the greenback advanced against all of its Group-of-10 peers apart from the Swiss franc. Treasury yields rose by up to 9 bps, led by the front end. The yen was the worst G-10 performer and slumped as much as 1.8% to 134.63 per dollar after the Bank of Japan kept policy on hold, defying speculation it would follow its global peers and move toward tightening. The BOJ made a rare reference to the currency market, saying it needed to watch its impact on the economy and markets. The euro fell below $1.05 before paring, after touching an almost one-week high yesterday. European bond yields fell and investors rushed back to Italian debt for a third day after ECB President Christine Lagarde pledged that borrowing costs of more indebted nations in the euro-area won’t be allowed to spiral out of control. Sterling eased against a broadly stronger dollar, giving up some of its sharp gains made the previous day, when the Bank of England’s pledge to take a more aggressive stance against inflation boosted the UK currency. Market awaits speeches by BOE policymakers Silvana Tenreyro and Huw Pill later in the day for possible clues into the outlook for inflation and monetary policy.

In rates, Treasuries are cheaper across the curve with losses led by front-end following flurry of block trade in 2-year note futures over the European session. US yields cheaper by up to 5bp across front-end of the curve, flattening 2s10s spread by 2.5bp on the day; 10-year yields around 3.22%, cheaper by 2.5bp and underperforming bunds by 7bp Italian bonds outperform after ECB President Christine Lagarde’s pledge to support borrowing costs of indebted nations in the euro-area. Bloomberg notes five block trades in 2-year note futures for combined 25k were posted between 3:25am ET and 4:36am ET appeared skewed toward sellers, helping front-end of the cash curve underperform. IG dollar issuance slate empty so far; at least six IG issuers are said to have stood down over the past couple of days, as investors wait for market calm before re-launching deals.

The German cash curve bull steepens, trading richer by ~12bps in 5s. Gilts bull flatten, with 10y yields down 8bps around this week’s lows near 2.4%. US 2s10s narrow 3bps. Peripheral spreads tighten to Germany with 10y BTP/Bund narrowing ~14bps to a one-month low near 188bps.

In commodities, crude futures advance. WTI drifts 1% higher to trade near $118.75. Base metals are mixed; LME tin falls 0.9% while LME nickel gains 1.1%. Spot gold falls roughly $7 to trade near $1,850/oz

Bitcoin is currently modestly firmer, but the overall sessions range is in proximity to USD 20k with the current trough at USD 20.19k.

Looking at the day ahead now, and data releases include US industrial production and capacity utilisation for May, along with the final Euro Area CPI reading for May. Central bankers include Fed Chair Powell, the ECB’s Simkus and the BoE’s Tenreyro and Pill. Of note, Jerome Powell gives welcome remarks before the Inaugural Conference on the International Roles of the U.S. Dollar at 845am ET. He is not expected to discuss monetary policy.

Market Snapshot

S&P 500 futures up 1.0% to 3,703.75

MXAP down 1.2% to 157.22

MXAPJ down 0.4% to 521.87

Nikkei down 1.8% to 25,963.00

Topix down 1.7% to 1,835.90

Hang Seng Index up 1.1% to 21,075.00

Shanghai Composite up 1.0% to 3,316.79

Sensex little changed at 51,457.72

Australia S&P/ASX 200 down 1.8% to 6,474.80

Kospi down 0.4% to 2,440.93

STOXX Europe 600 up 1.2% to 407.54

German 10Y yield little changed at 1.66%

Euro down 0.4% to $1.0502

Brent Futures up 0.5% to $120.35/bbl

Brent Futures up 0.5% to $120.39/bbl

Gold spot down 0.4% to $1,849.84

U.S. Dollar Index up 0.75% to 104.41

Top Overnight News from Bloomberg

A small tweak to the BOJ’s bond purchase plan this week blew up an arbitrage strategy popular with overseas investors known as the basis trade. It exacerbated a supply shortage of government bonds that has ramped up pressure on domestic financial institutions, leading them to turn to the BOJ for help to relieve the strain

President Joe Biden said a US recession isn’t inevitable and acknowledged that aides warned him about the inflationary risk of his flagship relief bill, while insisting that he won’t soften his stance on Russia even if it costs him re-election

The WTO clinched a historic package of accords including on vaccine production and fishery subsidies, ending the trade body’s seven-year negotiating drought

China’s local governments are caught in an unexpectedly severe budget squeeze, creating a dilemma for officials over whether to boost debt or tolerate weaker economic growth

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks mostly suffered firm losses amid the global risk-aversion after the recent flurry of central bank rate increases and with weak data in the US stoking recession fears. ASX 200 was led lower by underperformance in tech and the commodity-related sectors, although gold miners have weathered the storm after the recent upside in the precious metal. Nikkei 225 was pressured and failed to benefit from the BoJ decision to keep policy settings unchanged. Hang Seng and Shanghai Comp. pared opening losses amid virus-related optimism after Beijing reported zero cases outside of quarantine and with US-China defence meetings showing signs of cooling tensions.

Top Asian News

China in Talks With Qatar for Gas Field Stakes, Reuters Says

Kuroda Deepens BOJ’s Outlier Status, Keeping Pressure on Yen

ByteDance Disbands Shanghai Games Studio in Expansion Setback

BOJ Offers to Buy Cheapest-to-Deliver JGBs for Extended Time

Gold Heads for Weekly Drop as Traders Weigh Rate Hikes, Growth

European bourses are now firmer across the board, Euro Stoxx 50 +1.2%, as performance picks up following a mixed open amid comparably quiet newsflow. Stateside, US futures are performing similarly, ES +1.0%, though the complex is cognisant of commentary from Chair Powell later. Note, today is Quad Witching; recently, GS’ Rubner highlighted “literally massive” USD 3.2tln notional open interest of US listed options which expire on June 17th, writing that the passing of this may allow the market to move more freely.

Top European News

UK is to set out new data rules which diverge from the EU on Friday as it seeks to ease pressure on businesses, while it believes the new rules will maintain free flow of data from Europe and does not expect the EU to object to its data reforms, according to Reuters.

German Finance Minister Lindner told ECB President Lagarde that the ECB's talk regarding fragmentation threatens to dent confidence, according to FT.

Hungarian Chief of Staff Gulyas says the idea of a global minimum tax is not accepted by the Hungarian government.

Central Banks

BoJ kept policy settings unchanged as expected with rates at -0.10% and QQE with yield curve control maintained to target 10yr JGB yields at around 0% with the decision on YCC made via an 8-1 vote as Kataoka dissented. BoJ repeated its April guidance that it will offer to buy 10yr JGBs at 0.25% every business day unless it is highly likely that no bids will be submitted and it also reiterated guidance on policy bias that it will take additional easing steps without hesitation as needed with an eye on the pandemic's impact on the economy. Furthermore, the BoJ said the economy is picking up as a trend though some weakness has been seen and they must carefully watch the impact of FX moves on Japan's economy and prices.

BoJ's Kuroda says upward pressure is being seen in bond yields, and it is important for FX to move stable reflecting fundamentals, no change to the concept that YCC strongly supports the economic recovery; does not see a limit in YCC. Recent rapid JPY weakness is a weakness for the economy.. Does not see a need for further policy easing now. Not thinking about raising the cap on the BoJ's long-term yield target above 0.25%, as it could result in higher yields and weaken the effect of monetary easing.

BoJ purchases JPY 70.1bln in ETFs.

BoJ offers to purchase the cheapest-to-deliver issuance for an extended time as of June 20th.

ECB's Knot says that several 50bps rate increases are possible in the event that inflation worsens, via BNR; does not see hikes reaching 200bp before early-2023.

BoE's Pill says markets will have to make their own judgement on whether the BoE is considering a 50bp hike, via Bloomberg TV; stresses the conditionality around the inclusion of "forcefully" in the statement, in the context of "if necessary". Trying to signal that we may need to act further, looking at the persistence of inflationary pressure. Price pressures becoming embedded would be a trigger for more aggressive BoE action.

FX

Yen recoils after racking up big risk averse gains as BoJ sticks rigidly to ultra accommodative stance with additional measures to maintain YCC, USD/JPY hovers just under 135.00 vs 131.49 low on Thursday.

Buck benefits after extending post-FOMC retreat in wake of weak US data and pronounced bounce in Treasuries, DXY extends recovery to 104.540 from 103.410 low.

Franc maintains SNB hike momentum to rally further across the board, USD/CHF around 0.9650 compared to par-plus peaks earlier in the week.

Euro underpinned by decent option expiry interest and hawkish ECB commentary, but Aussie undermined as Government gives authorities power to stop coal exports; EUR/USD on the 1.0500 handle and above 1+ bln rolling off between 1.0500-1.0495, AUD/USD capped just under 0.7000.

Kiwi gleans some traction from a rise in NZ manufacturing PMI and RBNZ rate hike calls; NZD/USD straddles 0.6350, AUD/NZD cross sub-1.1050.

Lira lags following latest CBRT survey showing higher inflation forecasts and USD/TRY rate, latter at 18.8874 by year end vs 17.5682 previously and circa 17.3200 at present.

Fixed Income

Debt extends intraday ranges as volatility remains high on Friday.

Bunds veer from 142.56 to 144.99, Gilts between 111.83 and 112.91 and the 10 year T-note within a 116-19/115.28+ range.

Hawkish comments from ECB's Knot largely discounted as EZ periphery bonds outperform on anti-fragmentation dynamic, but BoE's Pill rattles Sonia strip.

Commodities

WTI and Brent are currently set to end the week with gains in excess of USD 1.00/bbl overall, though the benchmarks reside towards the mid-point of the over USD 11.00/bbl range for the week.

Newsflow has been comparably limited but primarily focused on familiar themes.

US Energy Secretary called an emergency meeting with oil refiners next week to discuss steps companies can take to increase refining capacity and output, according to Reuters citing a DoE spokesperson.

White House is reportedly considering fuel export limits as pump prices surge and options such as waiving anti-smog rules are also being discussed, according to Bloomberg.

Qatar Energy set August Al-Shaheen crude term price at a premium of USD 9.24/bbl above Dubai quotes which is the highest in 3 months, according to traders cited by Reuters.

Brazil's Petrobras is to announce a fuel price increase today, according to Reuters citing local press.

China's national oil majors are reportedly in advanced discussions with Qatar around investment in North Field East LNG and for long-term contractual purchases of LNG, according to Reuters sources.

Australia has invoked measures to give authorities the power to prevent coal exports if needed in an attempt to avert the risk of blackouts, according to the FT.

Spot gold is rangebound in European hours having successfully surpassed the cluster of DMAs between USD 1843-1848/oz during Thursday’s blockbuster session.

US Event Calendar

09:15: May Capacity Utilization, est. 79.2%, prior 79.0%

09:15: May Manufacturing (SIC) Production, est. 0.3%, prior 0.8%

09:15: May Industrial Production MoM, est. 0.4%, prior 1.1%

10:00: May Leading Index, est. -0.4%, prior -0.3%

DB's Jim Reid concludes the overnight wrap

The Bank of Japan (BOJ) continues to buck the global trend of monetary tightening, as this morning the central bank decided to maintain its purchases of government bonds and equities. The decision was widely anticipated but the BOJ indicated that it must “pay due attention” to foreign exchange markets, following the yen’s rapid weakening to its lowest level in 24 years earlier this week. The Yen has weakened around -1.3% to 134/USD as we type. Meanwhile, Japan’s benchmark 10yr bond yields hit a six-year high of 0.268% at one point, moving beyond the BOJ’s 0.25% cap ahead of the policy decision. However, yields retreated to the 0.25% after its daily unlimited fixed-rate purchasing operations.

This just continues what has been a very expensive week for the BoJ in terms of JGB QE after having had to buy $9.6tn yen worth. As one of our Asian FX strategists Tim Baker highlighted this morning, that's US$72bn. Tim highlighted that this is almost what the Fed and ECB were doing in an entire month last year, for economies 5-3x larger than Japan's. Japan's QE this week has been running more than 20x the pace of the Fed's QE in 2021, adjusted for the size of the economy. Can they continue to hold this line? You wouldn't think they could but it depends on global yields and central banks, the Yen and Japanese inflation. See my CoTD (link here) on this earlier this week. Watch out for the BoJ press conference after this goes to print this morning for any hints as to how determined they are to continue their policy settings.

The BoJ caps an array of central bank meetings over recent days, and markets have experienced another rout over the last 24 hours as multiple headlines added to investors fears about an imminent recession. It marked a big shift from just a day earlier, when the initial focus after Chair Powell’s press conference had been on his comment (when referring to +75bps) that he didn’t “expect moves of this size to be common”. But futures swiftly turned negative as growing doubts were cast on how firm that commitment really was, not least since we’ve all seen just how swiftly the Fed have shifted posture over the last week in response to worse-than-expected data. On top of that, the latest decisions by the SNB and the BoE (more on which below) only added to the hawkish drumbeat that much higher rates are in the offing, whilst weak US housing data served to aggravate those fears about an imminent growth slowdown.

With all said and done, you were hard-pressed to find a major asset that didn’t lose ground yesterday. The major equity indices slumped heavily on both sides of the Atlantic, with the S&P 500 (-3.24%) losing more than -3% for the second time this week, as it also hit its lowest level since late 2020. Indeed, just 14 companies in the entire index moved higher on the day. Elsewhere, the NASDAQ saw an even larger decline, falling -4.08% to have now lost more than a third of its value since its all-time closing peak back in November. It’s lost -9.96% since Friday’s CPI and -6.12% this week. And it was a similar story in Europe too, as the STOXX 600 (-2.47%) fell to a one-year low of its own.

Whilst equities were selling off, sovereign bonds continued to trade with elevated volatility, a function of continued central bank surprises, murky forward guidance, and heightened uncertainty around the near-to-medium-term outlook as economic data gets worse. In short it was a wild, wild ride yesterday. The sell-off initially accelerated after the SNB became the latest central bank to surprise. They hiked rates for the first time in 15 years, executing a 50bps move, combined with a change in FX policy, that our strategist Robin Winkler argues marks a once-in-a-decade policy regime shift (link here). In turn, that led to a massive reaction in the Swiss Franc, which strengthened by +2.91% against the US Dollar on the day in its biggest daily appreciation since 2015.

Then we had the Bank of England, where they hiked rates by +25bps as widely expected, with 3 of the 9 committee members continuing to vote for a larger 50bp increment. Notably, their statement sent a stronger signal on inflation, saying that the Committee would be “particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response.” In turn, that saw investors reappraise the path of future rate hikes in a more hawkish direction, and are now expecting more than +150bps worth of hikes over the next 3 meetings, so equivalent to at least a 50bp move at each one. Our UK economist writes in his reaction note (link here) that he expects the BoE to hike by 50bps in August and September now, which for reference would be the largest single hikes since they gained operational independence in 1997.

Against that backdrop, sovereign bond yields whipped around yet again. European yields were much higher on tighter policy and then Treasury yields moved higher in sympathy during European trading but gradually fell after another batch of underwhelming housing data lent new fears that growth was on unstable footing. Yields on 10yr Treasuries fell -8.9bps to 3.20%, but at their intraday peak they’d been up +20.7bps, so some sizeable moves in both directions. The move in nominal yields traced real yields, which were as high as +21.7bps intraday at the 10yr point, before finishing the day just +1.1bps higher. 10yr breakevens fell -10.4bps on the prospect of slower growth, which drove nominal yields lower on the day. In Asia, this morning, 10yr yields are witnessing a reversal with yields up +4.33bps to 3.24% while 2yr yields (+6bps) also moved higher to 3.15% as I type. Our US rates strategists have updated their views in the face of some large forces in both directions with the 10yr now expected to hit 3.85%. They also updated their year-end 2yr call to 3.85%, so a flat curve. See the full update here.

Meanwhile in Europe, 10yr bunds gained +7.2bps (+28.3bps at the peak) in a very choppy session. However, there was a considerable tightening in peripheral spreads for a second day running, with the gap between Italian and German 10yr yields down -13.7bps to 202bps, which followed comments from Italian central bank governor Visco that the spread should be under 150bps based on economic fundamentals. The heightened uncertainty and wild swings in yields also translated to heightened currency volatility, where the Euro traded in its widest intraday range since March 2020, which was as low as -0.60% and as strong as +1.50% against the dollar before ultimately appreciating +1.01%.

As mentioned, sentiment was further dampened by weak US housing data yesterday, with both housing starts and building permits in May falling by even more than expected. Housing starts were down to an annualised rate of 1.549m (vs. 1.693m expected), their lowest level in over a year, whilst building permits were down to an annualised rate of 1.695m (vs. 1.778m expected). We also got a sign of how tighter monetary policy was affecting the market, with Freddie Mac’s data showing that a 30-year fixed mortgage rate for the week ending yesterday rose to 5.78% (vs. 5.23% in the previous week). That’s the highest level since November 2008, as well as the largest weekly increase in the rate since 1987. And it just shows how the much more rapid pace of Fed hikes now expected by investors over the last week is already filtering its way through to the real economy.

Those moves lower in the US and European equities have been echoed in Asian markets this morning. The Nikkei (-1.59%) is the largest underperformer with the Kospi (-1.08%) also trading sharply lower. Elsewhere, the Hang Seng (+0.78%) is recovering from earlier losses while mainland Chinese stocks also turning around with the Shanghai Composite (+0.15%) and CSI (+0.26%) both trading up.

Outside of Asia, stock futures in the DMs are bouncing with contracts on the S&P 500 (+0.52%), NASDAQ 100 (+0.67%) and DAX (+0.31%) all heading higher.

Looking forward, Russian President Putin will be giving a speech today at the St Petersburg Economic Forum, which his press secretary Peskov has tried to build anticipation for, and could offer a flavour of how combative the Kremlin plans to be in its international approach. That came as German Chancellor Scholz, French President Macron and Italian PM Draghi endorsed Ukraine’s EU candidacy in a visit to the country yesterday. Otherwise, European natural gas futures pared back their significant increases in the morning to close -1.94% lower, marking a change in direction after their massive increases over the previous 2 sessions.

To the day ahead now, and data releases include US industrial production and capacity utilisation for May, along with the final Euro Area CPI reading for May. Central bankers include Fed Chair Powell, the ECB’s Simkus and the BoE’s Tenreyro and Pill.

Simple blood test could predict risk of long-term COVID-19 lung problems

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to…

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to suffer “long-haul” lung problems. That finding could help doctors better personalize treatments for individual patients.

Credit: UVA Health

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to suffer “long-haul” lung problems. That finding could help doctors better personalize treatments for individual patients.

UVA’s new research also alleviates concerns that severe COVID-19 could trigger relentless, ongoing lung scarring akin to the chronic lung disease known as idiopathic pulmonary fibrosis, the researchers report. That type of continuing lung damage would mean that patients’ ability to breathe would continue to worsen over time.

“We are excited to find that people with long-haul COVID have an immune system that is totally different from people who have lung scarring that doesn’t stop,” said researcher Catherine A. Bonham, MD, a pulmonary and critical care expert who serves as scientific director of UVA Health’s Interstitial Lung Disease Program. “This offers hope that even patients with the worst COVID do not have progressive scarring of the lung that leads to death.”

Long-Haul COVID-19

Up to 30% of patients hospitalized with severe COVID-19 continue to suffer persistent symptoms months after recovering from the virus. Many of these patients develop lung scarring – some early on in their hospitalization, and others within six months of their initial illness, prior research has found. Bonham and her collaborators wanted to better understand why this scarring occurs, to determine if it is similar to progressive pulmonary fibrosis and to see if there is a way to identify patients at risk.

To do this, the researchers followed 16 UVA Health patients who had survived severe COVID-19. Fourteen had been hospitalized and placed on a ventilator. All continued to have trouble breathing and suffered fatigue and abnormal lung function at their first outpatient checkup.

After six months, the researchers found that the patients could be divided into two groups: One group’s lung health improved, prompting the researchers to label them “early resolvers,” while the other group, dubbed “late resolvers,” continued to suffer lung problems and pulmonary fibrosis.

Looking at blood samples taken before the patients’ recovery began to diverge, the UVA team found that the late resolvers had significantly fewer immune cells known as monocytes circulating in their blood. These white blood cells play a critical role in our ability to fend off disease, and the cells were abnormally depleted in patients who continued to suffer lung problems compared both to those who recovered and healthy control subjects.

Further, the decrease in monocytes correlated with the severity of the patients’ ongoing symptoms. That suggests that doctors may be able to use a simple blood test to identify patients likely to become long-haulers — and to improve their care.

“About half of the patients we examined still had lingering, bothersome symptoms and abnormal tests after six months,” Bonham said. “We were able to detect differences in their blood from the first visit, with fewer blood monocytes mapping to lower lung function.”

The researchers also wanted to determine if severe COVID-19 could cause progressive lung scarring as in idiopathic pulmonary fibrosis. They found that the two conditions had very different effects on immune cells, suggesting that even when the symptoms were similar, the underlying causes were very different. This held true even in patients with the most persistent long-haul COVID-19 symptoms. “Idiopathic pulmonary fibrosis is progressive and kills patients within three to five years,” Bonham said. “It was a relief to see that all our COVID patients, even those with long-haul symptoms, were not similar.”

Because of the small numbers of participants in UVA’s study, and because they were mostly male (for easier comparison with IPF, a disease that strikes mostly men), the researchers say larger, multi-center studies are needed to bear out the findings. But they are hopeful that their new discovery will provide doctors a useful tool to identify COVID-19 patients at risk for long-haul lung problems and help guide them to recovery.

“We are only beginning to understand the biology of how the immune system impacts pulmonary fibrosis,” Bonham said. “My team and I were humbled and grateful to work with the outstanding patients who made this study possible.”

Findings Published

The researchers have published their findings in the scientific journal Frontiers in Immunology. The research team consisted of Grace C. Bingham, Lyndsey M. Muehling, Chaofan Li, Yong Huang, Shwu-Fan Ma, Daniel Abebayehu, Imre Noth, Jie Sun, Judith A. Woodfolk, Thomas H. Barker and Bonham. Noth disclosed that he has received personal fees from Boehringer Ingelheim, Genentech and Confo unrelated to the research project. In addition, he has a patent pending related to idiopathic pulmonary fibrosis. Bonham and all other members of the research team had no financial conflicts to disclose.

The UVA research was supported by the National Institutes of Health, grants R21 AI160334 and U01 AI125056; NIH’s National Heart, Lung and Blood Institute, grants 5K23HL143135-04 and UG3HL145266; UVA’s Engineering in Medicine Seed Fund; the UVA Global Infectious Diseases Institute’s COVID-19 Rapid Response; a UVA Robert R. Wagner Fellowship; and a Sture G. Olsson Fellowship in Engineering.

To keep up with the latest medical research news from UVA, subscribe to the Making of Medicine blog at http://makingofmedicine.virginia.edu.

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

These are the themes that emerged when I invited nine Black women to chronicle their professional experiences and relationships with colleagues as they earned their Ph.D.s at a public university in the Midwest. I featured their writings in the dissertation I wrote to get my Ph.D. in curriculum and instruction.

“It’s not just the beating me down that is hard,” one participant told me about constantly having her intelligence questioned. “It is the fact that it feels like I’m villainized and made out to be the problem for trying to advocate for myself.”

The women told me they did not feel like they belonged. They spoke of routinely being isolated by peers and potential mentors.

One participant told me she felt that peer community, faculty mentorship and cultural affinity spaces were lacking.

Participants also discussed the ways they felt they were duped into taking on more than their fair share of work.

“I realized I had been tricked into handling a two- to four-person job entirely by myself,” one participant said of her paid graduate position. “This happened just about a month before the pandemic occurred so it very quickly got swept under the rug.”

Why it matters

The hostility that Black women face in higher education can be hazardous to their health. The women in my study told me they were struggling with depression, had thought about suicide and felt physically ill when they had to go to campus.

Other studies have found similar outcomes. For instance, a 2020 study of 220 U.S. Black college women ages 18-48 found that even though being seen as a strong Black woman came with its benefits – such as being thought of as resilient, hardworking, independent and nurturing – it also came at a cost to their mental and physical health.

Several anthologies examine the negative experiences that Black women experience in academia. They include education scholars Venus Evans-Winters and Bettina Love’s edited volume, “Black Feminism in Education,” which examines how Black women navigate what it means to be a scholar in a “white supremacist patriarchal society.” Gender and sexuality studies scholar Stephanie Evans analyzes the barriers that Black women faced in accessing higher education from 1850 to 1954. In “Black Women, Ivory Tower,” African American studies professor Jasmine Harris recounts her own traumatic experiences in the world of higher education.

What’s next

In addition to publishing the findings of my research study, I plan to continue exploring the depths of Black women’s experiences in academia, expanding my research to include undergraduate students, as well as faculty and staff.

I believe this research will strengthen this field of study and enable people who work in higher education to develop and implement more comprehensive solutions.

The Research Brief is a short take on interesting academic work.

Ebony Aya received funding from the Black Collective Foundation in 2022 to support the work of the Aya Collective.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}