Government

Futures Rebound To Record High As Crudes Spikes Ahead Of Jobs Report

Futures Rebound To Record High As Crudes Spikes Ahead Of Jobs Report

Tyler Durden

Fri, 12/04/2020 – 08:05

Another day, another record high in the S&P, with S&P futures rising as high as 3,680 and up 0.3% last, as investors..

Share this:

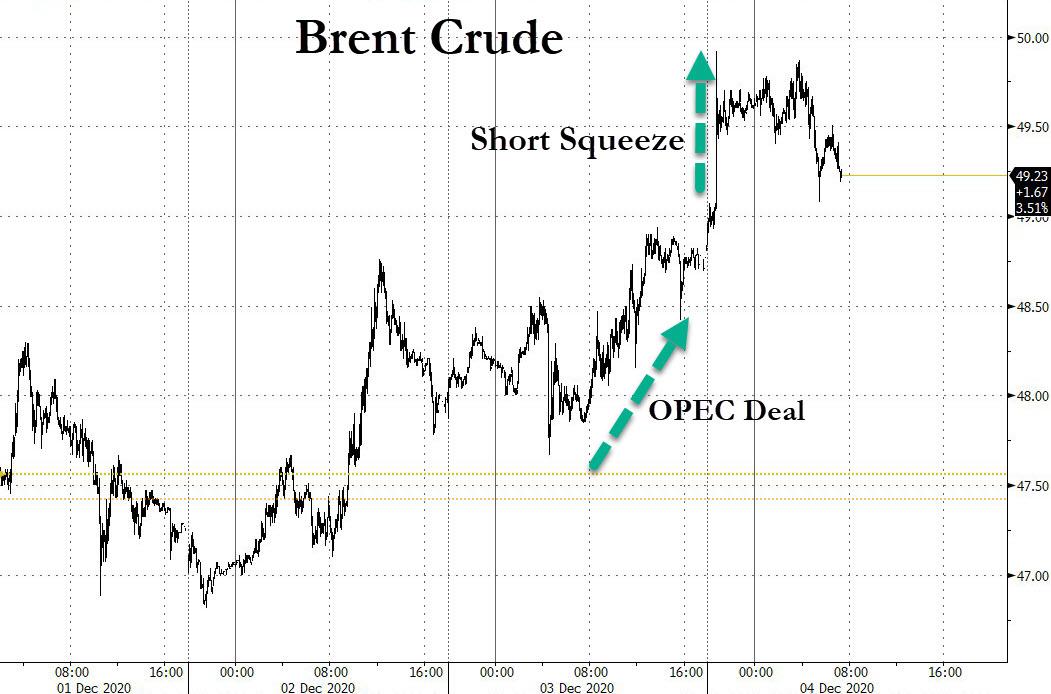

Another day, another record high in the S&P, with S&P futures rising as high as 3,680 and up 0.3% last, as investors await the November payrolls data which is expected to show a +470K print, a sharp slowdown from October's +638K due to the spike in covid cases and the return of lockdowns (full preview here). The dollar continued to slide, hitting a fresh 2.5 year low, headed for its biggest weekly decline in five, while Treasury yields nudged higher; but the highlight of the session was the sudden short squeeze in oil just before 9pmET which sent Brent to nearly $50, a nine-month high after Thursday's OPEC+ deal.

Despite a late Thursday wobble which sent stocks tumbling after Pfizer warned it was behind schedule on its 2020 vaccine deliveries, futures stabilized and were supported by renewed optimism that a fiscal stimulus bill was imminent as a bipartisan, $908 billion coronavirus aid plan gained momentum in the U.S. Congress after conservative lawmakers expressed their support.

"Positive vaccine and fiscal progress" will outweigh near-term uncertainties for rallying stock markets, according to Mark Haefele, chief investment officer at UBS Global Wealth Management.

Monetary stimulus is coming too: the Fed also expected to tweak guidance on its asset-purchase scheme later this month and expand the maturity of its purchases, while the ECB will likely increase its bond buying by at least €500BN next week.

"We expect major central banks to remain very accommodative over the coming quarters as output remains below its pre-crisis level - and well below its pre-crisis trend - and inflation remains subdued,” said Elia Lattuga, co-head of strategy research at Unicredit. In short: buy everything.

The MSCI index of world shares ticked up 0.17% to within a fraction of the previous day’s record high. It is set for a fifth straight week of gains, which have seen it surge 15%.

In Europe, the Stoxx 600 rose 0.3%, with energy companies leading the index higher; U.K. equities outperformed as negotiators edged closer to a Brexit trade agreement. German industrial orders rose 2.9%, more than the 1.5% expected, in October raising hopes the manufacturing sector in Europe’s biggest economy started the fourth quarter on a solid footing during a second wave of the COVID-19 pandemic.

Earlier in the session, Asian shares hit a record high overnight. MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.82%, surpassing its Nov. 25 high, led by gains in the tech sector. Japan’s Nikkei dipped 0.22% on profit-taking. China's Shanghai Composite closed fractionally in the green, with Chinese consumer stocks including liquor producers rallying on Friday as investors rotate from energy stocks and financials in search of companies that are seen to have better growth potential. A sector gauge for consumer staples gained as much as 2.6%, best on CSI 300 Index and poised to close at a fresh record high. Energy and financials are the worst performers among all 10 industry groups on CSI 300 on Friday; they were among most favored stocks in past month.

In rates, treasury yields were higher across the curve after climbing during European morning amid measured gains for risk assets. Yields are higher by 2bp-3bp from 10- to 30-year sectors, steepening 2s10s by more than 2bp, 5s30s by more than 1bp; 10- year around 0.93% is ~9bp higher on the week, most of which occurred on Dec. 1 as fiscal stimulus talks gained momentum; it peaked at 0.964% on Dec. 2. That said, price action was minimal on low volume during Asia session following Thursday’s late-day gains on report Pfizer cut vaccine rollout target. German government bond yields ticked down to -0.557%.

The big overnight move was in the commodity complex, where oil prices got an additional lift after OPEC and Russia agreed to reduce their deep oil output cuts from January by 500,000 barrels per day despite failing failed to find a compromise on a broader and longer-term policy. OPEC+ agreed to cut production by 7.2 million barrels per day, or 7% of global demand from January, compared with current cuts of 7.7 million barrels per day. Late in the Thursday session an unexpected spike higher in Brent sent the benchmark just cents away from $50.

In Fx, the broadly upbeat mood saw the U.S. dollar continue to lose ground to its major peers. “One of the elements of the better news we are getting, for instance the vaccine, is to increase the attraction of risky assets and that reduces the appetite for the U.S. dollar,” said Eric Brard, head of fixed income at asset manager Amundi. The euro was among the top performers, along with Scandinavian currencies; the common currency advanced a fourth day versus the dollar to a fresh 2020 high of $1.2177. The pound rose 0.2% to $1.3475, a shade below recent one-year highs, with traders hoping for a trade deal between the European Union and Britain.

Michel Barnier, the EU’s chief negotiator, said it was an important day in the talks as he left his hotel in London, while his planned update for national envoys to the bloc was cancelled due to “intensive negotiations”, an EU spokesman said. According to Reuters, a negotiated deal was “imminent” and expected before the end of the weekend, barring a last-minute breakdown in talks, an official with the bloc told Reuters. But a British minister said the talks were in a difficult phase.

The yen weakened after reaching a two-week low Thursday while the Australian and New Zealand dollars retreat from multi-year highs on unwinding of long positions ahead of U.S. employment data. Meanwhile, emerging markets continued their gains. The Mexican peso, Brazilian real, Turkish lira, South African rand, Russian rouble and Polish zloty have all jumped 7% to 11% over the past month, adding to 5%-12% leaps in China, Taiwan and Korea’s currencies since June.

Looking to the day ahead, the main highlight will be the aforementioned US jobs report for November. Other data highlights however will include German factory orders for October, along with the November construction PMIs from Germany and the UK. In the US, there’s also data on October’s trade balance and factory orders. On the central bank front, we’ll hear from the Fed’s Bowman and Kashkari, along with the BoE’s Saunders and Tenreyro.

Market Snapshot

- S&P 500 futures up 0.3% to 3,675.25

- MXAP up 0.5% to 194.11

- MXAPJ up 0.8% to 641.77

- STOXX Europe 600 up 0.2% to 392.46

- German 10Y yield fell 0.4 bps to -0.56%

- Euro up 0.2% to $1.2166

- Italian 10Y yield fell 3.0 bps to 0.491%

- Spanish 10Y yield fell 0.7 bps to 0.064%

- Nikkei down 0.2% to 26,751.24

- Topix up 0.04% to 1,775.94

- Hang Seng Index up 0.4% to 26,835.92

- Shanghai Composite up 0.07% to 3,444.58

- Sensex up 0.9% to 45,047.89

- Australia S&P/ASX 200 up 0.3% to 6,634.10

- Kospi up 1.3% to 2,731.45

- Brent futures up 1.4% to $49.39/bbl

- Gold spot little changed at $1,841.90

- U.S. Dollar Index down 0.2% to 90.57

Top Overnight News from Bloomberg

- Hungary’s prime minister said he won’t end his block on the European Union’s $2.2 trillion budget and coronavirus-rescue package unless Brussels relents in tying spending to upholding democratic values, denting hopes for a deal at a summit next week

- Germany agreed to extend a backstop for commercial credit insurers by six months to keep trade flowing and prevent bankruptcies as the economy is hit by a second wave of the coronavirus pandemic

- Bank of England policy maker Michael Saunders said there’s some room to cut interest rates further and bond buying by itself may not be the best option

- The U.K. Treasury is getting almost 10 billion pounds ($13 billion) a year in interest on its own debt under the Bank of England’s bond-buying plan

- Chart patterns, including the so-called inverted hammer and the Elliot Wave, show the euro is likely to breach the all-important $1.25 level. The currency is also being buoyed by a vote of confidence in the European Union’s timely response to the pandemic, as well as a revival in reflation trades that have kept the dollar under pressure

Global market snapshot courtesy of Newsquawk

Asia-Pac bourses traded mixed following a similar performance stateside where stock markets stalled after notching fresh record levels, amid tentativeness heading into today’s NFP data and with a bout of pressure before the Wall St closing bell after Pfizer cut its vaccine rollout targets for this year by half due to supply chain issues, although it still expects over 1bln doses rolled out in 2021. ASX 200 (+0.3%) was positive as financials lead the mild gains across cyclicals but with upside capped after weaker than expected retail sales data and as the mining sectors reversed yesterday’s outperformance. Nikkei 225 (-0.2%) was pressured as exporters suffered from recent currency inflows and with participants awaiting PM Suga’s press conference in which he is expected to discuss measures against the coronavirus, while KOSPI (+1.3%) resumed its outperformance with the index and its largest-weighted constituent Samsung Electronics extend on record levels as the tech giant continued to benefit from the firm outlook for the chip industry. Hang Seng (+0.4%) and Shanghai Comp. (+0.1%) were lacklustre after another consecutive liquidity drain by the PBoC and after the US added four Chinese companies to the Department of Defense blacklist for alleged ties with the Chinese military which include SMIC, CNOOC, China Construction Technology Co. and China International Engineering Consulting. Conversely, the latest reports surrounding Huawei were of a more constructive nature with the US reportedly in talks with Huawei's CFO on resolving criminal charges which would allow her to return home from Canada for admitting wrongdoing and after Japanese chipmaker Kioxia received permission from the US to export some products to Huawei, while Chinese stocks then pared losses in late trade. India's NIFTY (+0.8%) also gained overnight after the RBI rate decision in which the central bank kept rates unchanged as unanimously expected but also maintained its accommodative stance and announced quasi-measures to support stressed sectors. Finally, 10yr JGBs eked minimal gains with initial support after recent upside in T-notes, weakness in Japanese stocks and the BoJ's presence in the market for JPY 540bln of 5yr-25yr JGBs, but with advances limited by a gravitational pull towards the key 152.00 level.

Top Asian News

- Malaysia’s Top Pension Fund Sees Minimal Hit From Extra Outflows

- Strongest Taiwan Dollar Since ‘97 Shows Central Bank Easing Grip

- Qatar Says Doesn’t Plan Normalization With Israel For Now

- Next Digital Soars in Hong Kong After Jimmy Lai’s Arrest

In Europe, major bourses trade with modest gains across the board (Euro Stoxx 50 +0.2%) following a lukewarm cash open, and with positive Brexit newsflow briefly feeding impetus to risk appetite as an EU official stated that a Brexit trade deal is "imminent" and expected by the end of the weekend barring a last-minute breakdown in discussions. That being said, markets now await the UK's take on the state of talks to see if this optimism is reciprocated or downplayed, whilst reports overnight suggested negotiations took a step back, and France reaffirmed that it will veto an unsatisfactory proposal. Nonetheless the region was provided with a lift on the headlines, although EZ indices have since pared back the move, whilst the FTSE 100 outpaces peers with added tailwinds from the post-OPEC crude rally (see Commodities section), which sees Oil & Gas clearly outperforming. Delving deeper into sectors, the overall picture is mostly positive as with some cyclical sectors towards to the top of the board, albeit sectors do not provide a clear risk profile as Retail, Financials and Chemicals reside at the bottom of the pile. The Travel & Leisure sector meanwhile remains a gainer, underpinned by vaccine euphoria whilst a positive Fraport (+3.6%) broker move lends a hand. Elsewhere, Cineworld (-10%) plumbed the depths at the open as Warner Bros plans to debut movies online and in cinemas simultaneously next year, thus providing less incentive for consumers to step into cinemas. Finally, AstraZeneca (+1.2%) is firmer with some pointing to the Pfzier vaccine rollout target cut as a positive for the UK pharma giant's candidate.

Top European News

- ECB Seen Extending and Boosting Stimulus to Battle Longer Crisis

- Asda Mulls Sales of Gas Stations to EG Group Amid Mega Buyout

- EU’s Barnier Not Returning to Brussels, Sky’s Rigby Says

- Defiant Orban Says Hungary Won’t Blink in EU Budget Standoff

In FX, it would be far too premature to draw any conclusions or contend that the tide has turned for the Greenback, but it has pared declines and the DXY is holding above a fractionally higher 90.538 low compared to yesterday’s 90.504 base amidst tentative recovery gains. However, the Buck’s mini revival owes much to weakness or a loss of momentum elsewhere and it remains on the back foot against certain major and EM currencies, such as the Pound, Euro and Yuan. Ahead, NFP may provide the Dollar with more lasting or sustained respite, but only if the BLS report is bad and sparks a pronounced risk-off market reaction, perversely – for a full preview of the jobs release see the Newsquawk Research Suite. Back to the index, and a subsequent fade from 90.729 leaves the DXY meandering around 90.600.

- GBP/EUR/CNH - As noted above, all bucking the broad trend as Cable rebounds firmly from a stop-fuelled drop towards 1.3300 and Eur/Gbp recoils from a fix-related pop above 0.9065 on the back of reports via an EU official intimating that a trade deal with the UK is ‘imminent’, barring a last minute breakdown in discussions. Cable retested offers into 1.3500 in response, albeit somewhat belatedly awaiting any rebuttal from the UK side, while the cross is back under 0.9050 and perhaps wary about the prospect of France pouring cold water on the seemingly very positive update. However, the Euro is eyeing Thursday’s apex vs the Dollar circa 1.2175 and the offshore Renminbi has tested 6.5150 compared to the PBoC’s 6.5507 midpoint fix for the Cny to set fresh multi-year peaks.

- NZD/AUD - The Kiwi has lost its admittedly loose grip on the 0.7100 handle against its US counterpart and a bit more traction vs the Aussie as Aud/Nzd consolidates above 1.0500 and Aud/Usd retains 0.7400+ status even though retail sales rose slightly less than forecast in October.

- CAD/CHF/JPY - Relatively strong and perhaps psychologically significant retracements in crude prices (WTI and Brent beyond Usd 46/brl and Usd 49/brl respectively) could be keeping the Loonie propped on the 1.2850 axis before the Canadian-US jobs data showdown, while the Franc is still hovering close to 0.8900 and Yen sticking in close proximity to 104.00, albeit off best levels.

In commodities, WTI and Brent futures are firmer after OPEC+ ministers agreed to increase production by 500k BPD beginning in January. The ministers will meet each month to assess market conditions and decide on further production adjustments for the following month with further adjustments not to exceed 500k bpd, while they agreed to extend compensation cuts to the end of March. Although the decision at face value seems to be sub-par vs. expectations heading into the meeting, the consensus reached among producers for policy flexibility in the upcoming months has provided the crude markets with impetus, with oil ministers stating that upcoming meetings will not necessarily only take decisions on production increases, but could also decide on output decreases, if the market requires it. WTI Jan and Brent Feb have waned off best levels in recent trade, with no crude-specific headlines or developments to prompt the modest pullback, but more-so a pullback in risk. Nonetheless, the former holds onto its USD 46/bbl handle (vs. low USD 46.61/bbl) and the latter north of USD 49/bbl (vs. low 48.84/bbl). Elsewhere, precious metals are uneventful with spot gold and silver contained under 1850/oz and above USD 24/oz respectively. In terms of base metals, Dalian iron ore prices hit a record high to notch its fifth week of gains, bolstered by China's demand, Vale's guidance cut and the softer Dollar, whilst LME copper meanwhile hit eight-year highs.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 475,000, prior 638,000

- 8:30am: Unemployment Rate, est. 6.75%, prior 6.9%

- 8:30am: Average Hourly Earnings MoM, est. 0.1%, prior 0.1%; YoY, est. 4.2%, prior 4.5%

- 8:30am: Trade Balance, est. $64.8b deficit, prior $63.9b deficit

- 10am: Factory Orders, est. 0.8%, prior 1.1%; Factory Orders Ex Trans, prior 0.5%

- 10am: Durable Goods Orders, est. 1.3%, prior 1.3%; Durables Ex Transportation, est. 1.3%, prior 1.3%

- 10am: Cap Goods Orders Nondef Ex Air, est. 0.7%, prior 0.7%; 10am: Cap Goods Ship Nondef Ex Air, prior 2.3%

DB's Jim Reid concludes the overnight wrap

Happy Friday to all and hope you had a good week. Last night saw Jim attend a client virtual wine-tasting event in New York, which was streamed direct to his Surrey house via Zoom. Don’t ask me how it worked since I haven’t done one either, but because of this he asked me yesterday afternoon if I could step in to send out this morning’s email. As it happened, yesterday was also my birthday, and for the first time in my career I didn’t take it off work, so this request came as something of an unexpected present. Given the alarm clock I had to set this morning however, I may have learnt my lesson for next year.

While I was celebrating my birthday, markets were also celebrating as US equities looked set to rise to fresh all-time highs on hopes of a stimulus package in the coming days. However, late in the session a Dow Jones report came out saying that Pfizer expected to ship only half the amount of Covid-19 vaccines it had originally planned for this year because of supply-chain issues, which shone a light on some of the potential obstacles to vaccine distribution there’s likely to be in as production is scaled up massively.

As a result, the S&P 500 ended up falling slightly by the close (-0.06%), even as the NASDAQ (+0.23%) inched to a new record, with the stimulus talks giving added life to the cyclical trade as Consumer Durables (+2.03%) and Energy (+1.07%) were among the best performing sectors in the S&P. In terms of the latest details there, momentum continues to gather on the bipartisan stimulus deal that the Democratic leadership supported yesterday. Republican Senator Romney, part of the group that proposed the new bill, noted that they’re “getting more and more support from Republicans and Democrats”, even though Majority Leader McConnell has yet to voice his support for the bill. McConnell would need to agree to bring any vote to the floor of the Senate, but said he was “heartened” that Democratic Leadership was stepping away from the $2.4 trillion from late October.

The prospects of further stimulus gave support to inflation expectations, with US 10yr breakevens reaching a fresh 18-month high yesterday of 1.87% yesterday. Sovereign bond yields fell back on both sides of the Atlantic however, with yields on 10yr Treasuries (-3.0bps), bunds (-3.7bps) and gilts (-3.2bps) all moving lower. The other big move yesterday was the continued fall in the dollar, which reached a fresh 2-year low yesterday as both the euro (+0.24%) and the pound sterling (+0.64%) rose to their own 2-year highs against the greenback.

Speaking of deals, this morning both Brent Crude ($49.65/bbl) and WTI Oil ($46.39/bbl) reached their highest levels since the pandemic began after the OPEC+ group reached an agreement to roll back production cuts in 2021 more gradually than before. They’ll raise production by 500,000 barrels a day in January, which is a quarter of what would have occurred under the prior plan, and ministers are expected to consult monthly on next steps.

Overnight in Asia, equity markets have moved slightly lower for the most part, with the Nikkei (-0.30%), the Hang Seng (-0.09%) and the Shanghai Comp (-0.37%) all losing ground. The exception was the KOSPI, which saw a +1.26% advance, which came alongside a strong outperformance for the South Korean Won as well, which is up +1.25% against the US Dollar this morning. US futures are also pointing to a positive performance, with the S&P 500’s up +0.20%.

With equity futures indicating today could see fresh highs in the US, you might recall that Jim’s chart of the day on Wednesday looked at the fact that the S&P 500 CAPE ratio has just gone above 1929 levels. He’s already had a lot of emails on this, so yesterday he did another on the same theme (link here), graphing CAPE levels against real total returns over the decade ahead. Previous market valuation peaks saw future 10yr real returns broadly flat or negative, with 2007 being the main exception given the strong rally in the post-GFC years. So if history is to be relied upon the current point doesn’t bode well for returns over the next decade.

On the coronavirus, Italy reported a record number of deaths themselves (993), compared to just under 970 on a day back in March. Daily infection numbers are also continuing to rise globally, albeit with wider testing, as worldwide cases rose by over 700,000 yesterday for the first time. In terms of lockdowns and restrictions, Sweden announced that upper secondary schools would be closed for a month as the country moves to tighten restrictions. And after Germany and Spain extended measures on Wednesday, Greece extended their lockdown another week yesterday. From the US, we had confirmation from Dr Fauci that he will continue on at the National Institutes of Health under President-elect Biden’s administration.

Looking ahead now, the Brexit negotiations are likely to remain in focus today with both sides locked in last-minute talks ahead of the year-end deadline to the transition period. As of yet, there’s no sign of a deal being reached, and Sky’s Sam Coates reported a UK government source saying that the talks took a “turn for the worse” yesterday afternoon, while the FT reported that British officials had accused the French of making last minute demands. So it’s quite possible that the talks will continue through today into the weekend as the two sides seek agreement on the long-standing issues of fishing, the level playing field, and governance arrangements.

Should the talks end up going into next week, there’ll likely be a further round of obstacles to contend with, since Commons Leader Jacob Rees-Mogg announced yesterday that the UK government intended to reject the House of Lord’s amendments to the controversial Internal Market Bill on Monday, which took out the parts of the bill that breached the Brexit Withdrawal Agreement and created a major controversy when they were announced. If the Commons re-inserts those clauses next week, that is likely to be seen by the EU as a hostile act that breaches an agreement the two sides have already reached, particularly given it’s been reported by the BBC that the UK Finance Bill expected next week might similarly contain clauses breaching the Withdrawal Agreement. Irish foreign minister Coveney has tweeted that “a 2nd piece of legislation deliberately breaching WA & Int law, will be taken as a signal that U.K doesn’t want a deal.” So definitely worth keeping an eye on the progress of both those bills.

Attention later today will also be on November’s US jobs report, which is expected to show the slowest pace of monthly job growth since the pandemic, with DB’s US economists forecasting payrolls growth of +500k (vs. +475k consensus). Although they think this should be enough to see the unemployment rate fall to 6.8%, they say it’s also worth keeping an eye out for the broader U-6 measure of labour underutilisation, which is likely to better reflect the labour market’s underlying health. One piece of good news however yesterday were the weekly initial jobless claims for the week through November 28. They came in at a better-than-expected 712k (vs. 775k expected), marking an end to 2 consecutive weekly increases in the numbers.

The main data releases yesterday were the services and composite PMIs from around the world. In the Euro Area, the composite PMI was revised up from the flash reading to 45.3 (vs. flash 45.1), while the UK also saw a decent upward revision to 49 (vs. flash 47.4), even if that still left it in contractionary territory. Over in the US, the ISM services index came in at 55.9 (vs. 55.8 expected), though this was the second consecutive monthly decline in the reading.

To the day ahead now, and the main highlight will be the aforementioned US jobs report for November. Other data highlights however will include German factory orders for October, along with the November construction PMIs from Germany and the UK. In the US, there’s also data on October’s trade balance and factory orders. On the central bank front, we’ll hear from the Fed’s Bowman and Kashkari, along with the BoE’s Saunders and Tenreyro.

International

United Airlines adds new flights to faraway destinations

The airline said that it has been working hard to "find hidden gem destinations."

Share this:

Since countries started opening up after the pandemic in 2021 and 2022, airlines have been seeing demand soar not just for major global cities and popular routes but also for farther-away destinations.

Numerous reports, including a recent TripAdvisor survey of trending destinations, showed that there has been a rise in U.S. traveler interest in Asian countries such as Japan, South Korea and Vietnam as well as growing tourism traction in off-the-beaten-path European countries such as Slovenia, Estonia and Montenegro.

Related: 'No more flying for you': Travel agency sounds alarm over risk of 'carbon passports'

As a result, airlines have been looking at their networks to include more faraway destinations as well as smaller cities that are growing increasingly popular with tourists and may not be served by their competitors.

Shutterstock

United brings back more routes, says it is committed to 'finding hidden gems'

This week, United Airlines (UAL) announced that it will be launching a new route from Newark Liberty International Airport (EWR) to Morocco's Marrakesh. While it is only the country's fourth-largest city, Marrakesh is a particularly popular place for tourists to seek out the sights and experiences that many associate with the country — colorful souks, gardens with ornate architecture and mosques from the Moorish period.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

"We have consistently been ahead of the curve in finding hidden gem destinations for our customers to explore and remain committed to providing the most unique slate of travel options for their adventures abroad," United's SVP of Global Network Planning Patrick Quayle, said in a press statement.

The new route will launch on Oct. 24 and take place three times a week on a Boeing 767-300ER (BA) plane that is equipped with 46 Polaris business class and 22 Premium Plus seats. The plane choice was a way to reach a luxury customer customer looking to start their holiday in Marrakesh in the plane.

Along with the new Morocco route, United is also launching a flight between Houston (IAH) and Colombia's Medellín on Oct. 27 as well as a route between Tokyo and Cebu in the Philippines on July 31 — the latter is known as a "fifth freedom" flight in which the airline flies to the larger hub from the mainland U.S. and then goes on to smaller Asian city popular with tourists after some travelers get off (and others get on) in Tokyo.

United's network expansion includes new 'fifth freedom' flight

In the fall of 2023, United became the first U.S. airline to fly to the Philippines with a new Manila-San Francisco flight. It has expanded its service to Asia from different U.S. cities earlier last year. Cebu has been on its radar amid growing tourist interest in the region known for marine parks, rainforests and Spanish-style architecture.

With the summer coming up, United also announced that it plans to run its current flights to Hong Kong, Seoul, and Portugal's Porto more frequently at different points of the week and reach four weekly flights between Los Angeles and Shanghai by August 29.

"This is your normal, exciting network planning team back in action," Quayle told travel website The Points Guy of the airline's plans for the new routes.

stocks pandemic south korea japan hong kong europeanInternational

Walmart launches clever answer to Target’s new membership program

The retail superstore is adding a new feature to its Walmart+ plan — and customers will be happy.

Share this:

It's just been a few days since Target (TGT) launched its new Target Circle 360 paid membership plan.

The plan offers free and fast shipping on many products to customers, initially for $49 a year and then $99 after the initial promotional signup period. It promises to be a success, since many Target customers are loyal to the brand and will go out of their way to shop at one instead of at its two larger peers, Walmart and Amazon.

Related: Walmart makes a major price cut that will delight customers

And stop us if this sounds familiar: Target will rely on its more than 2,000 stores to act as fulfillment hubs.

This model is a proven winner; Walmart also uses its more than 4,600 stores as fulfillment and shipping locations to get orders to customers as soon as possible.

Sometimes, this means shipping goods from the nearest warehouse. But if a desired product is in-store and closer to a customer, it reduces miles on the road and delivery time. It's a kind of logistical magic that makes any efficiency lover's (or retail nerd's) heart go pitter patter.

Walmart rolls out answer to Target's new membership tier

Walmart has certainly had more time than Target to develop and work out the kinks in Walmart+. It first launched the paid membership in 2020 during the height of the pandemic, when many shoppers sheltered at home but still required many staples they might ordinarily pick up at a Walmart, like cleaning supplies, personal-care products, pantry goods and, of course, toilet paper.

It also undercut Amazon (AMZN) Prime, which costs customers $139 a year for free and fast shipping (plus several other benefits including access to its streaming service, Amazon Prime Video).

Walmart+ costs $98 a year, which also gets you free and speedy delivery, plus access to a Paramount+ streaming subscription, fuel savings, and more.

If that's not enough to tempt you, however, Walmart+ just added a new benefit to its membership program, ostensibly to compete directly with something Target now has: ultrafast delivery.

Target Circle 360 particularly attracts customers with free same-day delivery for select orders over $35 and as little as one-hour delivery on select items. Target executes this through its Shipt subsidiary.

We've seen this lightning-fast delivery speed only in snippets from Amazon, the king of delivery efficiency. Who better to take on Target, though, than Walmart, which is using a similar store-as-fulfillment-center model?

"Walmart is stepping up to save our customers even more time with our latest delivery offering: Express On-Demand Early Morning Delivery," Walmart said in a statement, just a day after Target Circle 360 launched. "Starting at 6 a.m., earlier than ever before, customers can enjoy the convenience of On-Demand delivery."

Walmart (WMT) clearly sees consumers' desire for near-instant delivery, which obviously saves time and trips to the store. Rather than waiting a day for your order to show up, it might be on your doorstep when you wake up.

Consumers also tend to spend more money when they shop online, and they remain stickier as paying annual members. So, to a growing number of retail giants, almost instant gratification like this seems like something worth striving for.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic mexicoInternational

President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

President Biden Delivers The "Darkest, Most Un-American Speech Given By A President"

Having successfully raged, ranted, lied, and yelled through…

Share this:

Having successfully raged, ranted, lied, and yelled through the State of The Union, President Biden can go back to his crypt now.

Whatever 'they' gave Biden, every American man, woman, and the other should be allowed to take it - though it seems the cocktail brings out 'dark Brandon'?

{kind=link}

Tl;dw: Biden's Speech tonight ...

-

Fund Ukraine.

-

Trump is threat to democracy and America itself.

-

Abortion is good.

-

American Economy is stronger than ever.

-

Inflation wasn't Biden's fault.

-

Illegals are Americans too.

-

Republicans are responsible for the border crisis.

-

Trump is bad.

-

Biden stands with trans-children.

-

J6 was the worst insurrection since the Civil War.

(h/t @TCDMS99)

Tucker Carlson's response sums it all up perfectly:

"that was possibly the darkest, most un-American speech given by an American president. It wasn't a speech, it was a rant..."

Carlson continued: "The true measure of a nation's greatness lies within its capacity to control borders, yet Bid refuses to do it."

"In a fair election, Joe Biden cannot win"

And concluded:

“There was not a meaningful word for the entire duration about the things that actually matter to people who live here.”

Victor Davis Hanson added some excellent color, but this was probably the best line on Biden:

"he doesn't care... he lives in an alternative reality."

— Tucker Carlson (@TuckerCarlson) March 8, 2024

* * *

Watch SOTU Live here...

* * *

Mises' Connor O'Keeffe, warns: "Be on the Lookout for These Lies in Biden's State of the Union Address."

On Thursday evening, President Joe Biden is set to give his third State of the Union address. The political press has been buzzing with speculation over what the president will say. That speculation, however, is focused more on how Biden will perform, and which issues he will prioritize. Much of the speech is expected to be familiar.

The story Biden will tell about what he has done as president and where the country finds itself as a result will be the same dishonest story he's been telling since at least the summer.

He'll cite government statistics to say the economy is growing, unemployment is low, and inflation is down.

Something that has been frustrating Biden, his team, and his allies in the media is that the American people do not feel as economically well off as the official data says they are. Despite what the White House and establishment-friendly journalists say, the problem lies with the data, not the American people's ability to perceive their own well-being.

As I wrote back in January, the reason for the discrepancy is the lack of distinction made between private economic activity and government spending in the most frequently cited economic indicators. There is an important difference between the two:

-

Government, unlike any other entity in the economy, can simply take money and resources from others to spend on things and hire people. Whether or not the spending brings people value is irrelevant

-

It's the private sector that's responsible for producing goods and services that actually meet people's needs and wants. So, the private components of the economy have the most significant effect on people's economic well-being.

Recently, government spending and hiring has accounted for a larger than normal share of both economic activity and employment. This means the government is propping up these traditional measures, making the economy appear better than it actually is. Also, many of the jobs Biden and his allies take credit for creating will quickly go away once it becomes clear that consumers don't actually want whatever the government encouraged these companies to produce.

On top of all that, the administration is dealing with the consequences of their chosen inflation rhetoric.

Since its peak in the summer of 2022, the president's team has talked about inflation "coming back down," which can easily give the impression that it's prices that will eventually come back down.

But that's not what that phrase means. It would be more honest to say that price increases are slowing down.

Americans are finally waking up to the fact that the cost of living will not return to prepandemic levels, and they're not happy about it.

The president has made some clumsy attempts at damage control, such as a Super Bowl Sunday video attacking food companies for "shrinkflation"—selling smaller portions at the same price instead of simply raising prices.

In his speech Thursday, Biden is expected to play up his desire to crack down on the "corporate greed" he's blaming for high prices.

In the name of "bringing down costs for Americans," the administration wants to implement targeted price ceilings - something anyone who has taken even a single economics class could tell you does more harm than good. Biden would never place the blame for the dramatic price increases we've experienced during his term where it actually belongs—on all the government spending that he and President Donald Trump oversaw during the pandemic, funded by the creation of $6 trillion out of thin air - because that kind of spending is precisely what he hopes to kick back up in a second term.

If reelected, the president wants to "revive" parts of his so-called Build Back Better agenda, which he tried and failed to pass in his first year. That would bring a significant expansion of domestic spending. And Biden remains committed to the idea that Americans must be forced to continue funding the war in Ukraine. That's another topic Biden is expected to highlight in the State of the Union, likely accompanied by the lie that Ukraine spending is good for the American economy. It isn't.

It's not possible to predict all the ways President Biden will exaggerate, mislead, and outright lie in his speech on Thursday. But we can be sure of two things. The "state of the Union" is not as strong as Biden will say it is. And his policy ambitions risk making it much worse.

* * *

The American people will be tuning in on their smartphones, laptops, and televisions on Thursday evening to see if 'sloppy joe' 81-year-old President Joe Biden can coherently put together more than two sentences (even with a teleprompter) as he gives his third State of the Union in front of a divided Congress.

President Biden will speak on various topics to convince voters why he shouldn't be sent to a retirement home.

The state of our union under President Biden: three years of decline. pic.twitter.com/Da1KOIb3eR

— Speaker Mike Johnson (@SpeakerJohnson) March 7, 2024

According to CNN sources, here are some of the topics Biden will discuss tonight:

Economic issues: Biden and his team have been drafting a speech heavy on economic populism, aides said, with calls for higher taxes on corporations and the wealthy – an attempt to draw a sharp contrast with Republicans and their likely presidential nominee, Donald Trump.

Health care expenses: Biden will also push for lowering health care costs and discuss his efforts to go after drug manufacturers to lower the cost of prescription medications — all issues his advisers believe can help buoy what have been sagging economic approval ratings.

Israel's war with Hamas: Also looming large over Biden's primetime address is the ongoing Israel-Hamas war, which has consumed much of the president's time and attention over the past few months. The president's top national security advisers have been working around the clock to try to finalize a ceasefire-hostages release deal by Ramadan, the Muslim holy month that begins next week.

An argument for reelection: Aides view Thursday's speech as a critical opportunity for the president to tout his accomplishments in office and lay out his plans for another four years in the nation's top job. Even though viewership has declined over the years, the yearly speech reliably draws tens of millions of households.

Sources provided more color on Biden's SOTU address:

The speech is expected to be heavy on economic populism. The president will talk about raising taxes on corporations and the wealthy. He'll highlight efforts to cut costs for the American people, including pushing Congress to help make prescription drugs more affordable.

Biden will talk about the need to preserve democracy and freedom, a cornerstone of his re-election bid. That includes protecting and bolstering reproductive rights, an issue Democrats believe will energize voters in November. Biden is also expected to promote his unity agenda, a key feature of each of his addresses to Congress while in office.

Biden is also expected to give remarks on border security while the invasion of illegals has become one of the most heated topics among American voters. A majority of voters are frustrated with radical progressives in the White House facilitating the illegal migrant invasion.

It is probable that the president will attribute the failure of the Senate border bill to the Republicans, a claim many voters view as unfounded. This is because the White House has the option to issue an executive order to restore border security, yet opts not to do so

Maybe this is why?

Most Americans are still unaware that the census counts ALL people, including illegal immigrants, for deciding how many House seats each state gets!

— Elon Musk (@elonmusk) March 7, 2024

This results in Dem states getting roughly 20 more House seats, which is another strong incentive for them not to deport illegals.

While Biden addresses the nation, the Biden administration will be armed with a social media team to pump propaganda to at least 100 million Americans.

"The White House hosted about 70 creators, digital publishers, and influencers across three separate events" on Wednesday and Thursday, a White House official told CNN.

Not a very capable social media team...

The State of Confusion https://t.co/C31mHc5ABJ

— zerohedge (@zerohedge) March 7, 2024

The administration's move to ramp up social media operations comes as users on X are mostly free from government censorship with Elon Musk at the helm. This infuriates Democrats, who can no longer censor their political enemies on X.

Meanwhile, Democratic lawmakers tell Axios that the president's SOTU performance will be critical as he tries to dispel voter concerns about his elderly age. The address reached as many as 27 million people in 2023.

"We are all nervous," said one House Democrat, citing concerns about the president's "ability to speak without blowing things."

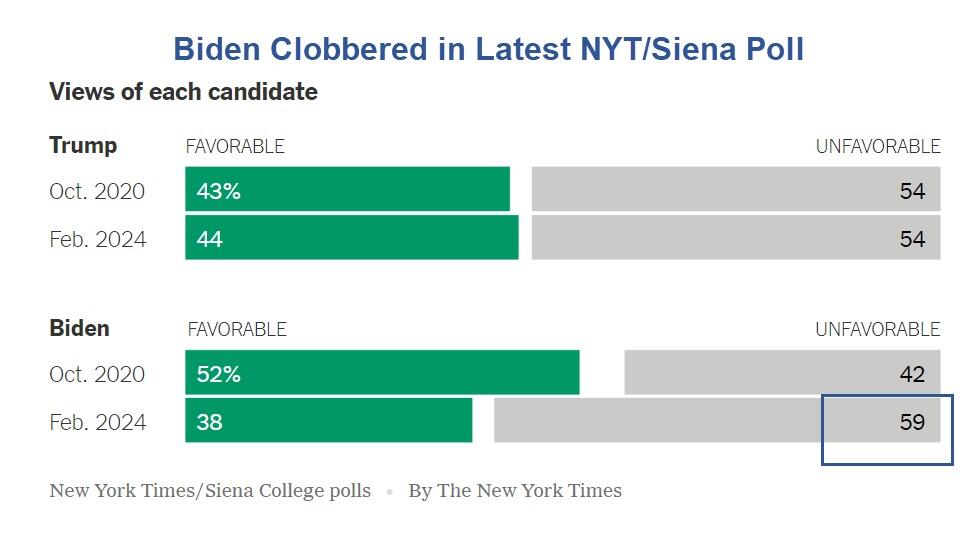

The SOTU address comes as Biden's polling data is in the dumps.

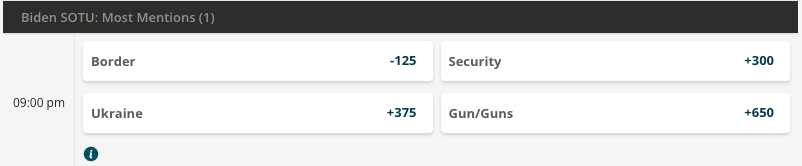

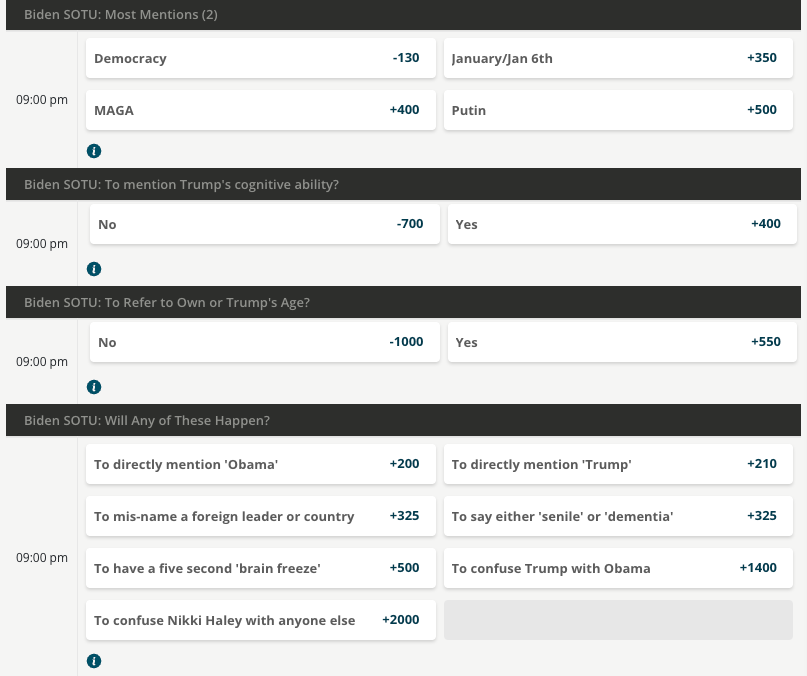

BetOnline has created several money-making opportunities for gamblers tonight, such as betting on what word Biden mentions the most.

As well as...

We will update you when Tucker Carlson's live feed of SOTU is published.

Fuck it. We’ll do it live! Thursday night, March 7, our live response to Joe Biden’s State of the Union speech. pic.twitter.com/V0UwOrgKvz

— Tucker Carlson (@TuckerCarlson) March 6, 2024

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Walmart launches clever answer to Target’s new membership program

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Catastrophic Risk: Investing and Business Implications

Biden to call for first-time homebuyer tax credit, construction of 2 million homes

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

GBPINR: Analysis and Projections for 2024

CADCHF: Central Bank Policies and Projections for 2024

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges