Government

Futures Rebound From Monday’s Plunge On Strong Earnings, Mega Merger

Futures Rebound From Monday’s Plunge On Strong Earnings, Mega Merger

Share this:

U.S. index futures and European stocks rebounded on Tuesday following the S&P 500’s worst day in a month as investors parsed through strong corporate earnings which offset Monday's SAP shocker, while bracing for volatility ahead of Election Day, assessing rising coronavirus cases across the globe and conceding that a fiscal stimulus deal just won't happen now that the Senate has closed for recess after rushing through the appointment of Amy Coney Barrett to the SCOTUS late on Monday night, which was also Hillary Clinton's birthday. AMD's $35 billion acqusition of Xilinx also helped boost trader optimism.

The S&P 500 and Nasdaq hit three week lows on Monday as record number of new coronavirus infections in the United States and some European countries and a lack of agreement in Washington over the next U.S. fiscal stimulus raised worries about the economic recovery. The chances are "very, very slim," Appropriations Chairman Richard Shelby said talking about a stimulus, pointing out the patently obvious. Differences between the two sides “have narrowed,” but “the more it narrows, the more conditions come up on the other side,” White House economic adviser Larry Kudlow told reporters. Of course, Nancy Pelosi remains optimistic, her spokesman said, but she's used similar language throughout three months of talks as she does not want to take the blame for the continued gridlock.

Also on Monday, the VIX spiked to its highest closing level in nearly two months on "concerns" about President Donald Trump's unexpected victory or the uncertain election outcome we first reported on Sunday night. As we also reported, while Joe Biden leads the official polls, the race is much tighter in battleground states which determine the election outcome.

In premarket trading, Drugmaker Eli Lilly fell 4% after it reported a fall in quarterly profit. Industrial companies 3M Co and Caterpillar Inc were also slightly lower after results. Investors are looking forward to results from Apple, Amazon.com, Alphabet and Facebook Inc in an earnings-heavy week as the technology giants have managed to stand out during the coronavirus pandemic. Chipmaker Xilinx soared after AMD announced a $35BN takeover offer, while Merck climbed after the drugmaker boosted its guidance.

At 8am S&P 500 E-minis rose 0.47% to 3,409.5 points.

The Stoxx Europe 600 Index erased most of its decline after earlier heading toward its lowest close since June on coronavirus lockdown fears. France’s benchmark CAC 40 Index underperformed other major European stock indexes on Tuesday, amid concerns that tougher restrictions may be introduced in the country as soon as tomorrow to curb a spike in coronavirus cases. Declines in miners and energy firms offset positive earnings from banking powerhouses HSBC Holdings and Banco Santander, which both signaled a brighter outlook for dividends. Following two tumultuous quarter, HSBC said it would consider paying a 2020 dividend after the bank unveiled a better-than-expected third quarter profit on lower provisions for bad loans. The bank on Tuesday reported a 36 per cent year-on-year drop in pre-tax profits to $3.1bn for the third-quarter, which was above analysts’ forecasts. Noel Quinn, HSBC’s chief executive, labelled the results “promising." Energy giant BP Plc warned of many challenges ahead as the pace of recovery in oil demand remained uncertain. Meanwhile, Europe took a step closer to the strict rules imposed during the initial wave of the pandemic, with leaders struggling to regain control of the spread while confronting growing opposition to restrictions.

Earlier in the session, Asian stocks fell, led by the energy and finance sectors, after falling in the last session. Most markets in the region were down, with Australia's S&P/ASX 200 dropping 1.7% and South Korea's Kospi falling 0.6%, while India's S&P BSE Sensex Index increased 0.5%. The Topix was little changed, with Nintendo climbing and Nidec slipping.

As Bloomberg notes, with time effectively over to finish an aid package before Americans vote, investors are looking for market catalysts later on Tuesday from data and earnings. Durable-goods orders and consumer confidence reports are due, as well as results from Microsoft Corp. and AMD after market.

In rates, Treasuries were steady overnight, holding Monday session gains despite gains in S&P 500 e-minis amid poor volumes, trading around 60% of recent average during Asia, early Europe. Preliminary open interest data shows some unwind of long-end short positions into Monday’s rally. Yields were mixed, although within a basis point of Monday’s close across the curve; 10-year steady at around 0.80%, trading inline with bunds and outperforming gilts by ~1bp. Treasury auctions kick-off with $54b 2-year note sale today, followed by 5- and 7- year sales Wednesday and Thursday, respectively.

On Monday, BlackRock strategists downgraded U.S. Treasuries and upgraded their inflation-linked peers ahead of the U.S. election on a growing likelihood of significant fiscal expansion. They said Covid infections in Europe threaten to derail a fragile recovery as they recommended investors hold a neutral position on bunds to hedge a downturn.

“As Covid infections have picked up, the focus on further policy response has shifted to more monetary easing including additional asset purchases,” said strategists Mike Pyle, Scott Thiel and Beata Harasim.

In Fx, a gauge of the dollar’s strength edged lower after Monday's bounce, while the euro and the pound were little changed; cable slipped earlier with strategists predicting limited gains in the currency on a Brexit trade-deal breakthrough. The Norwegian krone and the Japanese yen led G-10 currency gains, while the Swiss franc and the Swedish krona weakened the most. China’s currency weakened after Reuters reported the country’s central bank asked lenders to suspend a key factor used to calculate the yuan’s daily reference rate.

Elsewhere, crude oil nudged higher while gold remains largely unchanged.

In terms of data today we will get the preliminary September durable goods orders and nondefence capital goods orders ex-air. There will also be August’s FHFA house price index, the Richmond Fed manufacturing index and the October Conference Board consumer confidence reading. The Fed’s Kaplan is the only major speaker on the docket. Lastly the second major week of earnings ramps up as Microsoft, Novartis, Pfizer, Merck & Co., Eli Lilly & Co, Caterpillar, HSBC and BP all report.

Market Snapshot

- S&P 500 futures up 0.2% to 3,3400.50

- STOXX Europe 600 down 0.4% to 354.57

- MXAP down 0.2% to 175.21

- MXAPJ down 0.3% to 581.84

- Nikkei down 0.04% to 23,485.80

- Topix down 0.09% to 1,617.53

- Hang Seng Index down 0.5% to 24,787.19

- Shanghai Composite up 0.1% to 3,254.32

- Sensex up 0.6% to 40,372.74

- Australia S&P/ASX 200 down 1.7% to 6,051.02

- Kospi down 0.6% to 2,330.84

- Brent futures up 0.7% to $40.75/bbl

- Gold spot down 0.1% to $1,900.30

- U.S. Dollar Index little changed at 93.07

- German 10Y yield unchanged at -0.581%

- Euro down 0.04% to $1.1805

- Italian 10Y yield fell 1.9 bps to 0.536%

- Spanish 10Y yield fell 0.2 bps to 0.184%

Top Overnight News from Bloomberg

- The world’s biggest money manager is shorting the dollar on expectations that unprecedented fiscal and monetary stimulus will prolong its losses -- regardless of who wins the U.S. election

- Turkey’s banking regulator took another step to slow lending after a massive credit boom contributed to a currency rout

- U.S. President Donald Trump’s push for a second poll-defying victory is relying on a hallmark of his first -- raucous campaign rallies that Trump sees as a crucial sign of voter enthusiasm but that pollsters say may only be cementing his defeat

- More than 50 of Boris Johnson’s own Conservative members of Parliament have demanded a clear route out of lockdown for parts of northern Britain that helped give his party a majority in last year’s election. In a letter to the prime minister, the MPs warned that his pandemic strategy of targeting local areas with restrictions is disproportionately damaging the economies of northern regions of the country

Asian equity markets resumed the weak performance seen across global peers amid the ongoing risk-averse themes including the worsening COVID-19 pandemic, tougher lockdown restrictions in Europe and the continued US stimulus stalemate which culminated in Wall St’s worst day in more than a month. ASX 200 (-1.7%) and Nikkei 225 (-0.1%) were lower with the Australian benchmark the underperformer amid losses across all sectors and the declines led by energy as the COVID-19 situation did no favours for the demand outlook, while sentiment in Tokyo was also lacklustre but with downside limited by a relatively stable currency and the KOSPI (-0.9%) briefly nursed opening losses after better than expected GDP data and stronger revenue from Kia Motors which drove shares in the automaker higher by nearly double-digits. Hang Seng (-0.9%) and Shanghai Comp. (Unch.) were both lacklustre after data showed Industrial Profit growth in September moderated to 10.1% from 19.1% and due to lingering US-China tensions after the US government approved potential USD 2.4bln in arms sale to Taiwan despite an earlier announcement by China's Foreign Ministry to impose sanctions on US entities that partake in arms sales to Taiwan, although there were some bright spots with HSBC shares rallying around 5% on return from the lunch break following better than expected Q3 results and with Tencent also buoyed after US Appeals Court rejected an attempt by the Justice Department to impose an immediate ban on WeChat. Finally, 10yr JGBs traded higher as prices conformed to the mild upside seen in T-notes and with demand also spurred by the risk aversion, although gains were capped by the 2 year auction results which were marginally weaker than prior.

Top Asian News

- HSBC Flags Conservative Return to Dividends on Profit Beat

- Hong Kong Police Arrest Activist Seeking U.S. Asylum, SCMP Says

- Dubai in Talks on London Air-Travel Agreement to Boost Demand

Ahead of the cash open, index futures indicated a positive open in Europe with the DAX Dec’20 contract at one stage showing gains of 0.7% in what was initially a paring of yesterday’s heavy losses. However, as cash products opened, indices faced a bout of selling pressure with the DAX Dec’20 contract now lower by 0.5%; Eurostoxx 50 cash is down -0.6% - notably, both are off session lows. In terms of fundamental drivers, downbeat sentiment from yesterday has been carried over into today’s session as the spread of COVID across the region saps investor risk appetite. One of the more concerning updates this morning has comes from Germany with the economy minister warning that the number of new infections in the nation are rising exponentially and will likely have 20k daily new infections by the end of the week (on October 24th it posted 14.7k new infections). From a sectoral standpoint, banking names have bucked the downbeat trend this morning with HSBC (+6.6%) one of the Stoxx 600’s best performers following Q3 earnings. HSBC exceeded expectations for revenues, net income and adj. pretax profits, whilst noting that it will reduce 2022 costs by more than the initially targeted USD 31bln. Santander (+3.6%) are also firmer on the session and providing support to peripheral banks after the Co. reported a marked improvement in Q3 earnings, compared to Q2 and noted a 14% decline in quarterly provisions. Other large cap earnings include BP (+1.6%), who trade firmer on the session after reporting an unexpected Q3 profit of USD 86mln with results underpinned by a lack of significant write-offs and a recovery in the broader oil & gas environment. Despite opening higher, Novartis (-1.3%) have drifted lower throughout the session in the wake of Q3 earnings, which saw revenues miss analyst estimates

Top European News

- Merkel Wants to Shutter Restaurants in Battle Against Virus

- Italy Readies New Virus Relief Package Amid Mounting Protests

- Lockdowns Loom for European Governments Running Out of Options

- Novartis Lifts 2020 Forecast as Drugmaker Counters Covid Impact

In FX, although the Dollar is somewhat mixed vs major counterparts, the DXY looks firmly anchored around 93.000 and eclipsed Monday’s high amidst underlying safe-haven demand when EU stocks lost their initial/early recovery momentum due to ongoing COVID contagion, exacerbated by Germany’s Economy Minister warning of the pandemic’s exponential resurgence that may see the daily rate of new cases reach 20k by the end of this week. The index has stalled at 99.137 for now with some technical resistance in the form of a double top around 93.100 perhaps weighing, but the latest pull-back was relatively shallow, at 92.875 vs 92.784 yesterday and last week’s 92.469 base.

- CAD/NZD – Both bucking the overall trend, as the Loonie rebounds from sub-1.3200 alongside a partial/mild bounce in crude prices and the clock ticks down to Wednesday’s BoC policy meeting. Meanwhile, crosswinds continue to keep the Kiwi afloat close to 0.6700 and 1.0650 vs its US and Aussie rivals in wake of broadly in line NZ trade data.

- JPY/AUD/EUR/CHF/GBP – All rangebound against the Greenback and within familiar confines, with the Yen meandering between 104.90-67 and well inside decent option expiries at 104.25 (1 bn) and the 105.00 strike (1.8 bn). Back down under, the Aussie remains comfortably above 0.7100 ahead of Q3 CPI overnight and in wake of supportive comments from RBA Assistant Governor Debelle seeing signs of growth in Q3. Conversely, the Euro, Franc and Sterling seem more precarious near round numbers (1.1800, 0.9100 and 1.3000 respectively) as the coronavirus spreads and the former eyes 1.2 bn expiry interest in close proximity (1.2 bn from 1.1800 to 1.1805), while the Pound awaits Brexit developments.

- SCANDI/EM – Not much sign of a positive reaction to Sweden turning a trade deficit around in September to show a wider surplus, as Eur/Sek pivots 10.3300, but the modestly firmer tone in oil is capping Eur/Nok around 10.9000 and well off recent 11.0000+ peaks. Elsewhere, the Yuan has found some support beneath 6.7100 vs the Dollar after a firmer than forecast PBoC midpoint fix and hardly responding to the request made for banks to neutralise the counter-cyclical factor in the formula, but the Lira’s travails rumble on as fresh all time lows are hit below 8.1600.

In commodities, WTI and Brent front month futures are holding in positive territory of around USD 0.30/bbl as the session stands in-spite of the deterioration in risk-sentiment post the European cash equity open. The current relative resilience is largely a factor of Hurricane Zeta which as of yesterday had shuttered around 16% of Gulf of Mexico oil production and 6% of gas output. The BSEE will provide another update later in the session at 18:00GMT/14:00ET which could well see further impact as the NHC believes the storm will re-strengthen as it progress to the Northern side of the Gulf prior to making landfall. Additionally, it’s worth highlighting that yesterday’s BSEE survey only focused on 7 companies in the Gulf compared to the survey’s sample contained in excess of 20 companies during Hurricane Delta earlier in the month. Elsewhere, post-earnings this morning BP noted that the Hurricane has shut down 20/30k BPD of its oil & gas production thus far. Storm updates aside, the sessions scheduled focus point explicitly for crude is the private inventory release which is expected to show a build of around 1.1mln barrels for the prior week as the effect of Delta diminishes but Zeta is yet to be included in the survey period. Moving to metals, spot gold has come under pressure this morning as while the metal isn’t currently suffering from USD strength as the DXY has dropped into negative territory it has failed to benefit from traditional safe-haven demand with silver & JPY seemingly receiving some of this allure.

US Event Calendar

- 8:30am: Durable Goods Orders, est. 0.5%, prior 0.5%; Durables Ex Transportation, est. 0.35%, prior 0.6%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.5%, prior 1.9%; Cap Goods Ship Nondef Ex Air, est. 0.4%, prior 1.5%

- 9am: FHFA House Price Index MoM, est. 0.7%, prior 1.0%

- 9am: S&P CoreLogic CS 20- City MoM SA, est. 0.5%, prior 0.55%; S&P CoreLogic CS 20-City YoY NSA, est. 4.2%, prior 3.95%

- 10am: Conf. Board Consumer Confidence, est. 102, prior 101.8; Present Situation, prior 98.5; Expectations, prior 104

- 10am: Richmond Fed Manufact. Index, est. 17.5, prior 21

DB's Jim Reid concludes the overnight wrap

Nice to be back luxuriating in the home office again after a few days of high intensity childminding over part of half-term. The drive through safari park was the highlight with lions, tigers and cheetahs brushing up to the car and monkeys climbing on top of it. The last time I went on safari was during a school cricket tour to Kenya in 1991. We were told before the trip not to take expensive cameras as the risk was they would get stolen. I didn’t have an alternative option anyway as I only had a basic one I’d bought for 10 pounds with my paper round money. However some of the other kids ignored this and brought cameras with big telescopic lenses. As such with my photos you were unable to tell whether the orangish blobs were rocks or lions whereas with my friends you could tell whether the lions had recently flossed or not. 29 years later my trusty iPhone got me some very decent pictures even if it did cost more than 10 pounds.

Looking at the finance pages on my iPhone this morning, it’s quite clear that global equities have taken a large step back at the start of this week after a weekend that saw covid-19 cases hit new highs in the US and fresh restrictions seemingly building daily in Europe. The S&P 500 finished down -1.86% last night, its worst daily performance since 23 September as the US saw its highest weekly cases of the pandemic so far. Sentiment was not helped by the ever dropping probability of a fiscal stimulus agreement prior to the election. Nearly 92% of stocks in the S&P were lower by the end of the session, led by declines in the energy sector (-3.47%) as oil prices fell sharply. WTI and Brent crude fell -3.24% and -3.14% respectively, as the global demand outlook worsened. Tech hardware (-0.58%) and Biotech (-0.85%) were among the more resilient industries, however the NASDAQ was still down -1.64%. The VIX rose +4.9pts to 32.5pts in its biggest move since 3 September.

Overnight Asian markets have tracked Wall Street’s move though the declines are more modest. The Nikkei (-0.24%), Hang Seng (-0.97%), Shanghai Comp (-0.37%), Kospi (-0.50%) and Asx (-1.70%) are all down. Meanwhile, in a sign of abating risk off sentiment, the US dollar index is down -0.11% this morning and futures on the S&P 500 are up +0.18%. HSBC is trading up +1.86% after reporting better than expected earnings as the bank paired back its expected credit losses. They also said that they are considering paying a conservative dividend for 2020 contingent on economic conditions in early 2021, subject to regulatory consultation. In terms of overnight data, South Korea’s Q3 GDP print came in better than expectations at 1.9% qoq (vs. 1.3% qoq expected).

Earlier European equities, and the DAX (-3.71%) in particular, pulled back strongly on news that SAP was lowering its revenue forecast for the full year of 2020 and that the pandemic could weigh on demand into the first half of next year. The largest tech company in Europe was down -22.20% and is now -18.55% YTD. Contrast this to Apple - the largest US tech company - which is +56.7% YTD with the NYFANG index +76.9% against Europe’s tech index at -8.0% YTD.

With risk sentiment souring, core sovereign bond yields fell on both sides of the Atlantic. After rising sharply last week, US 10yr Treasuries yields fell -5.0bps to 0.793%, while 10yr bund yields fell a surprising modest -0.6bps to -0.58% given the risk-off. In other havens, the dollar rose (+0.30%) for just the second session in the last seven, while gold (+0.00%) was unchanged.

Every sector in the Stoxx 600 (-1.81%) declined led by Technology (-7.37%) and Travel & Leisure (-3.29%). The latter was heavily influenced by the new restrictions across the continent, which outweighed the positive vaccine news from Astrazenca and Johnson and Johnson that we highlighted yesterday morning. After the positive vaccine news yesterday, our CoTD highlighted the work of our colleague Robin Winkler, looking at different R0 and efficacy scenarios to see what is required for herd immunity. We likely remain multiple quarters away from a mass rollout however the upcoming efficacy data should in theory have a major impact on life and markets going forward. As a benchmark the FDA has set its threshold as 50% - similar to the flu vaccine. See the CoTD here to see how much of the population would have to be vaccinated if the efficacy was only 50%, as well as the link to Robin’s note.

We are now just one week away from Election Day in the US. However, over 58.6 million ballots have already been cast across the country. This is more early votes (both in-person and mail-in) than in all of 2016, and there is still a week to go. Early indications point to a possible record turnout, if this pace continues, especially given the number of “new and infrequent” voters. The AP reported as many as 26.3% of Georgia’s early voters and just over 30% of Texas’s early voters are either a new or infrequent voter, which points to just how much important some feel this election is.

National polls have tightened slightly in the last 2 weeks. Former Vice President Biden led by as much +10.7% in fivethirtyeight.com’s polling average back on October 17 but that has come in to +9.4% as of today. This is still a substantial lead and Biden still holds the polling advantage in key battleground states such as Michigan (+8.3%), Wisconsin (+7.1%) and Pennsylvania (+5.1%). The fivethirtyeight.com model gives Biden an 87% chance of winning the Electoral College and therefore the election.

Lastly on US politics, late last night the Senate confirmed Amy Coney Barrett to the Supreme Court of the US, thereby giving the court a 6-3 conservative majority. The vote was 52-48 and mostly along party lines, with one Republican, Senator Susan Collins, joining Democrats in opposition.

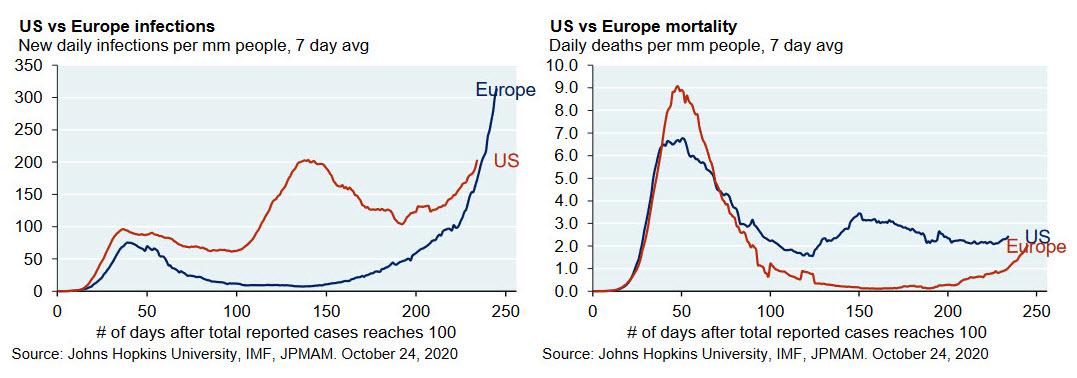

Coronavirus cases remain in focus as more regions of Europe contemplate or enact further restrictions to quell the current wave. France reported over 250,000 new cases over the last week and nearly 70% of ICU beds in the Paris region are occupied, according to local authorities. President Macron is expected to convene a defense cabinet meeting later today to address the issue, which may lead to further restrictions. This comes as the head of the scientific council that advises the French government on the pandemic said the situation is moving towards that of early March, and that the second wave will probably be worse than the first one. The Netherlands passed 300,000 confirmed cases yesterday, after over 10.3k new cases yesterday. Dutch Prime Minister Rutte has said he wants to wait for the new data over the coming days before making a final call on further restrictions for the country.

Elsewhere, German Chancellor Angela Merkel convened her task force yesterday and it was reported she plans to present a “lockdown light” plan which would see bars, restaurants and public events shut in order to minimise a second wave. Furthermore, shops would remain open and schools would not have to close under the new plan. Meanwhile, Italy’s new rules went into effect yesterday after Prime Minister Conte approved the government’s plan to limit hours for bars and restaurants as well as shutting down gyms and entertainment venues. Italians have also been asked not to travel under the new restrictions, which are currently in place until November 24. Meanwhile on top of the national curfew that was set in Spain, the country’s parliament approved an extension of the state of emergency until May 9, in order for the Prime Minister to avoid continually seeking approval to implement further restrictions.

In the US, the rolling 7-day Covid-19 case count hit a new high with over 480,000 cases. This surpasses the high of 472,083 we saw back in late July. While testing capacity is higher, the number of newly confirmed weekly cases as a percent of weekly US tests is over 6% for the first time since August and has been rising sharply over the last 2-3 weeks. On therapeutics, Eli Lilly has confirmed overnight that its US clinical trial of experimental antibody therapy will end as data suggested that the treatment is unlikely to help hospitalised patients recover from advanced forms of the virus. The stock is down -1% in after-hours trading. In other worrying news, according to a large Imperial College London covid study, the proportion of people in England with antibodies dropped by more than a quarter in the space of three months. This will raise concerns about how long people can go without risking being reinfected.

European risk sentiment was not helped by the German October Ifo business climate indicator, which fell to 92.7 (93.0 expected). This is -0.5pts down from last month and was the first monthly decline since April. In the US, the September reading of the Chicago Fed national activity index missed expectations by quite a bit, down to 0.27 (0.73 expected) from an upwardly revised 1.11 last month. A reading above ‘0’ translates to above-trend growth, indicating that while growth is positive it has slowed significantly. Similarly, new home sales dropped to 959k from 994k the month prior, and well below the 1,025k homes expected. Lastly, the October Dallas Fed manufacturing index beat expectations at 19.8 (vs 13.5 expected) in its highest reading since October 2018.

In terms of data today we will get Euro Area M3 money supply for September as well as slew of US data. In hard data there is the preliminary September durable goods orders and nondefence capital goods orders ex-air. There will also be August’s FHFA house price index, the Richmond Fed manufacturing index and the October Conference Board consumer confidence reading. The Fed’s Kaplan is the only major speaker on the docket. Lastly the second major week of earnings ramps up as Microsoft, Novartis, Pfizer, Merck & Co., Eli Lilly & Co, Caterpillar, HSBC and BP all report.

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Government

Walmart joins Costco in sharing key pricing news

The massive retailers have both shared information that some retailers keep very close to the vest.

Share this:

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trumpGovernment

Walmart has really good news for shoppers (and Joe Biden)

The giant retailer joins Costco in making a statement that has political overtones, even if that’s not the intent.

Share this:

{kind=link}

As we head toward a presidential election, the presumed candidates for both parties will look for issues that rally undecided voters.

The economy will be a key issue, with Democrats pointing to job creation and lowering prices while Republicans will cite the layoffs at Big Tech companies, high housing prices, and of course, sticky inflation.

The covid pandemic created a perfect storm for inflation and higher prices. It became harder to get many items because people getting sick slowed down, or even stopped, production at some factories.

Related: Popular mall retailer shuts down abruptly after bankruptcy filing

It was also a period where demand increased while shipping, trucking and delivery systems were all strained or thrown out of whack. The combination led to product shortages and higher prices.

You might have gone to the grocery store and not been able to buy your favorite paper towel brand or find toilet paper at all. That happened partly because of the supply chain and partly due to increased demand, but at the end of the day, it led to higher prices, which some consumers blamed on President Joe Biden's administration.

Biden, of course, was blamed for the price increases, but as inflation has dropped and grocery prices have fallen, few companies have been up front about it. That's probably not a political choice in most cases. Instead, some companies have chosen to lower prices more slowly than they raised them.

However, two major retailers, Walmart (WMT) and Costco, have been very honest about inflation. Walmart Chief Executive Doug McMillon's most recent comments validate what Biden's administration has been saying about the state of the economy. And they contrast with the economic picture being painted by Republicans who support their presumptive nominee, Donald Trump.

Image source: Joe Raedle/Getty Images

Walmart sees lower prices

McMillon does not talk about lower prices to make a political statement. He's communicating with customers and potential customers through the analysts who cover the company's quarterly-earnings calls.

During Walmart's fiscal-fourth-quarter-earnings call, McMillon was clear that prices are going down.

"I'm excited about the omnichannel net promoter score trends the team is driving. Across countries, we continue to see a customer that's resilient but looking for value. As always, we're working hard to deliver that for them, including through our rollbacks on food pricing in Walmart U.S. Those were up significantly in Q4 versus last year, following a big increase in Q3," he said.

He was specific about where the chain has seen prices go down.

"Our general merchandise prices are lower than a year ago and even two years ago in some categories, which means our customers are finding value in areas like apparel and hard lines," he said. "In food, prices are lower than a year ago in places like eggs, apples, and deli snacks, but higher in other places like asparagus and blackberries."

McMillon said that in other areas prices were still up but have been falling.

"Dry grocery and consumables categories like paper goods and cleaning supplies are up mid-single digits versus last year and high teens versus two years ago. Private-brand penetration is up in many of the countries where we operate, including the United States," he said.

Costco sees almost no inflation impact

McMillon avoided the word inflation in his comments. Costco (COST) Chief Financial Officer Richard Galanti, who steps down on March 15, has been very transparent on the topic.

The CFO commented on inflation during his company's fiscal-first-quarter-earnings call.

"Most recently, in the last fourth-quarter discussion, we had estimated that year-over-year inflation was in the 1% to 2% range. Our estimate for the quarter just ended, that inflation was in the 0% to 1% range," he said.

Galanti made clear that inflation (and even deflation) varied by category.

"A bigger deflation in some big and bulky items like furniture sets due to lower freight costs year over year, as well as on things like domestics, bulky lower-priced items, again, where the freight cost is significant. Some deflationary items were as much as 20% to 30% and, again, mostly freight-related," he added.

bankruptcy pandemic trump

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Catastrophic Risk: Investing and Business Implications

When Military Rule Supplants Democracy

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Deterra Royalties half-yearly result: stable performance and growth Initiatives

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges