With futures flat for much of the overnight session, markets needed that extra oomph to start the week and push them above a key psychological level, and they got that after news that Pfizer and German biotech BioNTech SE were granted fast track designation by the FDA for two of the companies’ four vaccine candidates against the coronavirus. The news, which is purely procedural and was expected all along, was misinterpreted by the market as if the two companies have a promising virus vaccine, and sent Pfizer shares 2%, while BioNTech jumped 5%. More importantly, the news was enough to push Eminis up more than 21 point and above 3,200 which will surely help the market's mood ahead of tomorrow's official start of Q2 earnings which are expected to be the worst since the financial crisis.

In corporate news, Pepsi kicked off the second-quarter earnings season on a bright note, gaining over 2% as it benefited from a surge in at-home consumption of salty snacks such as Fritos and Cheetos during lockdowns, while a multi-billion dollar semiconductor deal also lifting the mood. Analog Devices rose 0.9% in premarket trading after it confirmed a Sunday report from the WSJ, offering to buy peer Maxim Integrated Products Inc for $20.91 billion in an all-stock deal. Maxim shares jumped 17%.

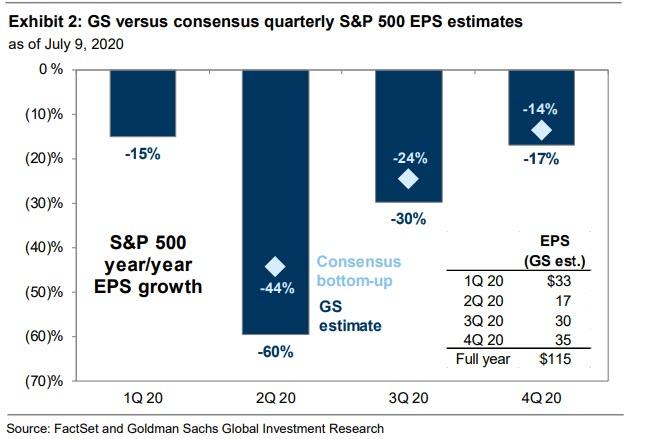

The renewed covid optimism and strong results offered some cheer as investors are bracing for what could be the sharpest drop in quarterly earnings for S&P 500 firms since the financial crisis, with Goldman expected a 60% drop in Q2 EPS.

Results from big banks will be in focus this week. The April-June reports will reveal the extent of the damage wreaked by the coronavirus-induced lockdowns on corporate profits. With a record jump in cases in the United States and some other hotspots around the world, analysts have predicted a return to S&P 500 earning s growth only by 2022. Recent economic data, however, has pointed to a revival in business activity, helping the Nasdaq clinch its sixth record close in seven weeks on Friday as broader markets rose on positive data from Gilead’s potential COVID-19 treatment.

Earlier in the session, Asian stocks gained, led by materials and industrials, after falling in the last session. Markets in the region were mixed, with Japan's Topix Index rising, and Singapore's Straits Times Index and Thailand's SET falling. Amusingly, Beijing appears to be losing control of its stock market bubble, as the Shanghai Composite brushes off another mainland media call for ‘rational’ behavior to gain 1.8%, Shenzhen 2.7% higher.

Trading volume for MSCI Asia Pacific Index members was 42% above the monthly average. The Topix gained 2.5%, with AIT and Nomura System Corp rising the most. The Shanghai Composite Index rose 1.8%, with Xinhu Zhongbao and Flying Technology posting the biggest advances

European markets initially failed to echo Asia’s optimism, with the majority of indexes trading well off opening levels. FTSE MIB underperformed, trading flat after opening ~1.5% higher. Banks, autos and travel names gave back ~1% of gains, having outperformed in early trading. However, as US traders walked in, European share rose alongside US bond yields.

And so, with global stocks trading near their highest since February, focus now turns to whether the profit outlook will back up bullishness fueled by central bank and fiscal policy support. Traders have largely shrugged off new coronavirus outbreaks in some parts of the world, with Florida on Sunday posting the biggest one-day rise in cases since the pandemic began in the U.S., reporting 15,300 new infections. As Bloomberg notes, "there’s reason for optimism even though earnings are estimated to have contracted by more than 40% in the worst quarter since the financial crisis, as analysts upgrade their forecasts for the rest of the year."

“We think earnings are likely to recover in the second half of the year and excess liquidity will continue to support risk assets,” said Julie Fox at UBS Private Wealth Management. “We see further potential in global equities and think there’s some upside in segments of the market that have underperformed during the crisis.”

In rates, Treasuries were unchanged after trading in a narrow range, the 10Y moving from 0.625% to 0.655% during the European session and within 2bps of Friday’s closing levels, having pared declines as U.S. equity index futures tracked European stocks higher, TSYs outperformed other developed market bonds which were pressured by supply; there’s no Treasury coupon supply this week. Yields so far remain inside Friday’s ranges, which featured multi-month lows for all tenors and a record low for the 5-year. The 10-year yield was little changed at 0.646%, traded at 0.5678% Friday, lowest yield since April 22. German and U.K. 10-year yields were 2bp-3bp cheaper vs U.S., while Japan’s and Australia’s bond markets were pressured by supply. Peripheral spreads traded off session wides as BTPs and PGBs put in a firm bounce off the lows.

In FX, the dollar traded mixed versus its Group-of-10 peers and hovered around 1.13 per euro; most currencies were confined to narrow moves as they consolidated recent trading ranges. The Bloomberg dollar index faded Asia’s losses to trade flat. Cable traded near 1.2600, having printed highs of 1.2666. The Australian dollar was on the top of the table while the New Zealand dollar slipped; asset managers last week increased Aussie long positions to the most since September 2017 and decreased kiwi longs for the first time in a month, Commitments of Traders (COT) reports showed. Norway’s krone fell versus all Group-of-10 peers as oil edged lower ahead of an OPEC+ meeting this week at which the group may announce plans to start tapering historic production cuts even as the coronavirus surges unabated in many parts of the world.

In commodities, crude futures drifted lower, front-month WTI dips below $40 ahead of an OPEC+ meeting at which the group may announce plans to start tapering historic production cuts.

Market Snapshot

S&P 500 futures up 0.2% to 3,183.50

STOXX Europe 600 up 0.3% to 367.88

MXAP up 1.1% to 166.56

MXAPJ up 0.7% to 551.10

Nikkei up 2.2% to 22,784.74

Topix up 2.5% to 1,573.02

Hang Seng Index up 0.2% to 25,772.12

Shanghai Composite up 1.8% to 3,443.29

Sensex down 0.04% to 36,578.49

Australia S&P/ASX 200 up 1% to 5,977.52

Kospi up 1.7% to 2,186.06

German 10Y yield rose 0.4 bps to -0.461%

Euro up 0.06% to $1.1307

Italian 10Y yield rose 0.2 bps to 1.099%

Spanish 10Y yield rose 1.1 bps to 0.424%

Brent futures down 1.4% to $42.65/bbl

Gold spot up 0.5% to $1,808.06

U.S. Dollar Index little changed at 96.61

Top Overnight News from Bloomberg

When the ECB meets this week to review its radical suite of measures to revive the economy, there’s one tool it insists it’ll stay away from: yield curve control

Faced with the prospect of restricted access to U.S. dollars, China’s answer is to get more people to use its own currency instead

The dollar rallied during the March market turmoil due to its haven status, yet ongoing repricing in options may be challenging the idea that a second wave of the pandemic or another black swan event could see similar results

China announced sanctions against U.S. officials including Senators Marco Rubio and Ted Cruz, in a largely symbolic retaliation over legislation intended to punish Beijing for its treatment of ethnic minorities in the Xinjiang region

Boris Johnson’s government will launch a campaign Monday to urge businesses to prepare for the end of the Brexit transition period on Dec. 31, as a survey showed only a quarter of directors said their companies were fully ready

France will unveil “massive” support for youth employment this week and a new broad stimulus plan including tax cuts for companies at the end of August, Finance Minister Bruno Le Maire said

Asian equity markets began the week mostly positive as the region benefitted from the recent tailwinds from Wall St. where encouraging Remdesivir data and outperformance in financials last Friday ahead of upcoming earnings, helped markets shrug off the rising COVID infection numbers to lift all major US indices and helped the Nasdaq to a fresh all-time high. ASX 200 (+1.0%) was led higher by outperformance in utilities and the top-weighted financials sector, as the latter took its cue from its counterpart stateside and as big 4 bank Westpac was buoyed by reports it is mulling divesting over AUD 4bln in non-core wealth assets, while Nikkei 225 (+2.2%) outperformed on a break above the 22,500 level with participants unfazed by the increasing risks associated with the outbreak flare-up in Tokyo. Hang Seng (+0.2%) and Shanghai Comp. (+1.8%) were also positive after the PBoC provided its first liquidity injection following a 2-week hiatus and amid recent better than expected lending data from China. This helped domestic markets shake off the initial tentativeness after local press continued to urge rationality regarding stocks and amid the continued US-China tensions with US President Trump suggesting a Phase 2 trade deal was unlikely at this point and the US State Department warned US citizens in China of increased arbitrary detention, while China had also threatened to impose reciprocal measures if the US insists on moving forward with sanctions. Finally, 10yr JGBs were weaker amid gains in stocks and spillover selling following Friday’s pullback in USTs, while the lack of BoJ presence in the market ahead of its 2-day policy meeting tomorrow, also contributed to the tame demand for bonds.

Top Asian News

Tokyo Virus Numbers Fuel Concern of Spread Beyond Nightclubs

After 133% Rally, SoftBank Investors Bet There’s More Ahead

Netanyahu Ally Calls for Immediate Lockdown to Halt Virus Spread

European equities have kicked the week off on the front-foot (Eurostoxx 50 +0.8%) in an extension of the gains seen last week as markets thus far continue to shrug off the rising global COVID-19 case count whereby the WHO reported a record daily increase of over 230k cases in a 24 hour period over the weekend. From a European perspective, it is worth noting that the WHO stated that the largest increases in cases were seen in the US, Brazil, India and South Africa and therefore a bulk of the focus currently resides outside the continent. Furthermore, some desks have attributed the positive sentiment thus far to mounting hopes ahead of the upcoming EU summit as the bloc continues to negotiate its recovery fund. That said, work is still be done on appeasing the so-called “frugal four” and as such, some have cautioned that a deal might not come until later in the month. Gains in Europe are currently favouring cyclical names with autos, basic resources and travel & leisure names outperforming peers. However, as European indices pullback from earlier session highs, the composition of sector-wide performance could stage a rotation if sentiment deteriorates further. In terms of stock specifics, Akzo Nobel (+4.1%) trade higher after posting a Q2 update, whilst the same can also be said for the likes of DNB (+10.8%) and G4S (+8.7%). To the downside, the main outlier is Atlantia (-15.5%) after Italian PM Conte warned that proposals from the Co. are unsatisfactory thus far and the government will not sacrifice public interest over the Co. Additionally, Ubisoft (-9.0%) also trade lower on the session after undertaking multiple personal changes in response to allegations/accusations of misconduct.

Top European News

EU Carbon Permits Climb to 14-Year High as Bloc Goes Green

G4S Jumps Most Since May; Panmure Notes Security Unit Resilience

Ubisoft Drops After Harassment Reports, Analysts Cut Stock

Sweden’s Alfa Laval Agrees to Buy Neles in $2 Billion Deal

In FX, although the US Dollar has pared some losses and the DXY is holding above 96.500 within 96.387-685 parameters, the Aussie is still outpacing G10 counterparts in wake of a 2nd consecutive Usd/CNY midpoint fixing below the psychological 7.0000 level and a broad upturn in risk sentiment. Aud/Usd is hovering within a 0.6984-41 range ahead of NAB business conditions and confidence overnight, while the Aud/Nzd cross has rebounded through 1.0600 as the Kiwi lags vs its US peer around 0.6560 in advance of NZ CPI data on Wednesday. Note also, a dovish note from ANZ may be weighing on the Nzd as the bank believes that the RBNZ should carefully consider policies to weaken the exchange rate and is keeping all options on the agenda (ie NIRP).

CAD/EUR - The Loonie is also benefiting from the positive risk tone with Usd/Cad meandering from 1.3602 to 1.3556 even though crude prices are softer, while the Euro is just keeping afloat of 1.1300 after topping out ahead of 1.1340 and decent option expiry interest extending to 1.1350 (1 bn).

GBP/CHF/JPY - Sterling ran in to supply at 1.2660+ levels again and faded a fraction shy of Friday’s circa 1.2667 high to form a 2nd consecutive marginally lower peak having hit 1.2670 on July 9, and Cable is now striving to retain the 1.2600 handle as Eur/Gbp bounces from just under 0.8950 towards 0.8975 in the run up to the next round of Brexit talks. Also ahead and a potential Pound mover, 2 separate speeches by BoE Governor Bailey. Elsewhere, the Franc is pivoting 0.9400 against the Greenback and 1.0640 vs the Euro following another sizeable increase in Swiss domestic bank sight deposits on the eve of a speech by SNB chair Jordan. Similarly, the Yen is straddling 107.00 and 121.00 vs the single currency after a loss of safe haven premium, and now eyeing Japanese ip tomorrow for some independent impetus.

SCANDI/EM - Some loss of bullish momentum for the Norwegian Krona as risk appetite wanes and oil drifts, while the Swedish Crown is also apprehensive awaiting CPI on Tuesday. However, the Turkish Lira has pared some declines in wake of better than expected, albeit still bleak ip and a narrower than forecast current account deficit.

In commodities, WTI and Brent have had a downbeat start to the week with both benchmarks posting losses in excess of 1% and WTI Aug’20 future having dropped back below the USD 40/bbl handle. The most recent declines have arisen as sentiment more broadly takes a slight leg lower; albeit, with European and US equity futures still very much in positive territory. Over the weekend there were a number of updates on the crude front firstly, and one of the likely drivers of the morning’s downside, Saudi Arabia and other producers are seen as likely to increase output in August. In light of the easing of COVID-19 lockdown restrictions but the ongoing spread of cases is weighing on these plans. Additionally, desks note that OPEC+ are to begin easing production cuts from August, a measure which would be in-fitting with the current deal. Further clarity on the plans for OPEC+ ahead will arise from Wednesday’s JMMC meeting; although, it is worth bearing in mind the JMMC do not have the power to set policy themselves, they can only make recommendations to the broader OPEC+ members. Elsewhere, a resumption of woes for Libya’s NOC as the force majeure on all oil exports has been reimplemented, after cargoes docked and loaded late last week at Es Sider, due to LNA saying the blockade is to continue. Turning to metals, spot gold is firmer by some USD 10/oz thus far for the session and resides towards the top end of a relatively confined range which has notable seen the lower end drop beneath USD 1800/oz. Price action for the metal has largely been dictated by the mild pullback in general sentiment and broader USD moves.

US Event Calendar

11:30am: Fed’s Williams Discusses Libor

1pm: Fed’s Kaplan Speaks in Webinar Hosted by National Press Club

2pm: Monthly Budget Statement, est. $863.0b deficit, prior $398.8b deficit

DB's Jim Reid concludes the overnight wrap

I hope you all had a good weekend. At the start of lockdown we decided to buy a swing, slide and climbing frame set for the garden. We thought the kids could make use of it after we’d had a go ourselves. Three and a half months later, and one week after playgrounds reopened here in the U.K., it arrived at the weekend. I’ve never seen the kids so excited. It made me feel less guilty about playing golf where I am pleased to announce that my comeback from the most dreadful run known to man (or woman) continued. In a field of 144 I was just inside the top 10 shooting my handicap and banishing the previous weekend’s third last (ahead of only two octogenarians) to the dustbin. Readers on Friday will now know I shout “back” and “hit” during my swing to maintain rhythm. Apart from confusing my playing partners it seems to be working for now.

In a week ahead as packed as my golf club is at the moment, the main highlight is the EU summit on Friday where leaders will gather to discuss the recovery fund. In addition to this, we’ll also see the ECB, the Bank of Japan and others make their latest monetary policy decisions. Meanwhile, earnings season kicks off, including a number of US financials reporting. Economic data includes China’s Q2 GDP reading along with a number of June releases out from the US.

More on this below but first the weekend news and Asian market developments. Risk has started the week on the front foot with the Nikkei (+1.89%), Hang Seng (+0.92%), Shanghai Comp (+1.27%) and Kospi (+1.52%) all up. Futures on the S&P 500 are up +0.46% and yields on 10y USTs are down -1.4bps. Spot gold and silver prices are up +0.25% and +0.86% respectively.

Coronavirus cases continued to accelerate over the weekend with the US registering average case growth of +1.95% on Saturday and Sunday combined. This is higher than the last 5 weekends average of +1.38%. In terms of states, Texas registered new case growth of +3.66% vs. the last 5 weekend average of 2.71% and in Florida this stood at +5.13% (vs. 4.45%) and California (+2.11%) in line with previous 5 weekends average. The growth rate of new deaths actually declined slightly for the US overall (+0.35% this weekend vs. +0.39% in the previous 5 weekends) but at state level, Texas (+2.16% vs. 0.80%), Florida (+1.69% vs. +0.80%) and Arizona (+3.66% vs. 1.39%) all saw higher death rates even if the pace of fatalities vs cases is still significantly behind that of the first wave.

Meanwhile, New York City, once the epicenter of the US coronavirus outbreak, reported its first day with zero confirmed or probable virus deaths on Sunday since the pandemic began. Elsewhere, Japan’s economy minister, Yasutoshi Nishimura, said that the country needs to remain on high alert for further coronavirus outbreaks as the number of cases with unclear contagion routes increases and added that testing should be strategically and greatly increased. Japan reported 681 new cases on Sunday with Tokyo reporting more than 200 cases for four straight days.

In terms of other weekend news, here in the UK, the Telegraph reported that Chancellor Sunak is planning sweeping Brexit tax cuts to protect the economy. The report added that the Chancellor is also considering an overhaul of planning laws in up to 10 new ‘freeports’ within a year of the UK becoming fully independent from the EU in December. Meanwhile, the FT has reported overnight that the UK is proposing to withhold power to control state aid from its devolved nations when the Brexit transition ends. This could lead to friction with Scotland and Wales. The report added that the proposal, which would give Westminster statutory powers to control policies for the entire UK, is expected to appear in a bill this autumn laying the legal foundations of a new internal market.

In other news, the New York Times reported that OPEC, Russia and other producers are expected to modestly ease the record production cuts in August as coronavirus lockdowns end and demand begins to rise again. A committee of key officials from OPEC and Russia will meet on Wednesday by video conference to discuss their approach to the market. Oil prices are trading c. -1% this morning.

More on this week now. The EU leaders summit in Brussels on Friday and into Saturday will discuss the recovery fund in response to the pandemic, as well as the EU’s new long-term budget. The baseline expectations from our economists (link here ) is that there will be a deal on the recovery fund at this meeting, but it remains a close call. If an agreement weren’t to be reached there, then they still expect one within weeks. It’s worth remembering that there are number of complex issues to be worked out, including the ratio of grants to loans, with the so-called “frugal four” of the Netherlands, Austria, Sweden and Denmark looking for there to be loans rather than grants. Their support for the fund will be necessary as it requires the unanimous approval of the member states.

The ECB a day earlier should be a non event (see DB’s preview here) with maybe some focus on any comments from President Lagarde on the German Constitutional Court, now that the German Bundestag has passed a motion on proportionality. The BoJ meeting on Wednesday should also be a relatively tame affair (see DB’s preview here ). Also in the world of central banks the Canadian, Korean and Indonesian policy makers meet and the Fed release their Beige Book on Wednesday.

Moving on to data releases, the main highlight is likely to be China’s Q2 GDP release on Thursday. Our economists are expecting a notable rebound in GDP growth to +3% year-on-year in Q2, following the -6.8% contraction in Q1. At the same time, there’ll also be the release of retail sales and industrial production for June, with our economists expecting an expansion in retail sales of +0.7% yoy in June (vs. -2.8% in May), and IP growth of +4.5% (vs. +4.4% in May).

Turning elsewhere, the US also has a number of data releases out next week, including an increasing amount of hard data for June. The highlights include the June CPI reading on Tuesday, before the industrial production number on Wednesday, retail sales on Thursday, and housing starts and building permits data on Friday, which should give us a clearer indication of how the economy has performed into the end of the quarter. Meanwhile the U.K. sees a number of data releases, including GDP for May, CPI for June, and unemployment in the three months to May. Another thing to look out for in the UK will be the release of the Office for Budget Responsibility’s Fiscal sustainability Report tomorrow, which will present alternative scenarios for the economy and public finances.

Earnings season kicks slowly into gear as 32 S&P 500 companies report along with a further 57 from the STOXX 600. The highlights include PepsiCo today, JPMorgan, Citigroup and Wells Fargo tomorrow, UnitedHealth Group, ASML, Goldman Sachs, US Bancorp, BNY Mellon on Wednesday, Johnson & Johnson, Netflix, Bank of America, Abbott Laboratories and Morgan Stanley on Thursday and on Friday, there’s Danaher, Honeywell International and BlackRock.

Back to last week, where markets were generally constructive even as the outlook for the virus has continued to worsen in recent weeks, especially in the US and Emerging Markets. The S&P 500 gained +1.76% (+1.05% Friday) on the week, and now sits just under 1.5% away from being flat on the year just as earning season is about to begin. The tech-focused Nasdaq greatly outperformed last week, rallying +4.01% (+0.66% Friday) led primarily by the index’s most heavily weighted stocks. European equities generally underperformed the S&P with the Stoxx 600 gaining a lesser +0.38% (+0.88% Friday) over the five days. Overall European bourses were mixed with the DAX (+0.84%), and FTSE MIB (+0.21%) up on the week, while indices such as the IBEX (-1.11%) and CAC (-0.73%) pulled back. Asian indices were even more disparate as Chinese stocks saw a large rise with the CSI 300 gaining +7.55% but with the Nikkei (-0.07%) and Kospi (-0.10%) largely unchanged over the week.

Core sovereign bonds rose as US 10yr Treasury yields fell -2.5bps (+3.1bps Friday) to finish at 0.645%, while 10yr Bund yields fell -3.3bps (-0.2bps Friday) to -0.47%. In other fixed income, HY cash spreads tightened on both sides of the Atlantic as US HY spreads tightened -4bps (-1bps Friday) and Europe HY tightened -1bps (+2bps Friday).

The dollar fell -0.54% on the week to its lowest weekly close since the first week of March. Against this backdrop and with global yields continuing to fall, gold gained +1.28% (-0.27% Friday). It was the 5th straight weekly gain for the yellow metal and took it to its highest weekly close since 2011. In other metals, copper rose +5.62% on the week to levels last seen in April of last year, while silver gained +3.88% to its highest value since September 2019.

Ahead of this Friday’s summit of EU leaders on the bloc’s long-term budget and the recovery fund, European Council President Michel issued new proposals on Friday that sought to achieve agreement between the member states. These maintained the existing plan to distribute €500bn in grants and €250bn in loans to member states. However, budget rebates would continue for fiscally conservative states such as the Netherlands, and repayments would be brought forward. He also proposed a Brexit reserve of €5bn that would support against “unforeseen consequences” in the member states and sectors most affected.

On the data front, we got French and Italian industrial production for May, both came ahead of forecasts. Italian industrial output rose +42.1% (vs. +24.0% expected) after falling by -20.5% in April. France saw a similar rebound, jumping up +19.6% (vs. +15.4% expected) after falling a nearly identical -20.6% the month prior. We also saw the June PPI reading from the US, where prices fell unexpectedly. PPI fell -0.2% (vs. +0.4% expected) after the month prior saw them rise +0.4%. It was the fourth monthly decline out of the last five.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}