Futures Hit Fresh Record High Ahead Of PPI, Claims Data

Futures Hit Fresh Record High Ahead Of PPI, Claims Data

Another day, another all time high in US equity futures with spoos trading at the nice, round 4,444 on Thursday morning, while Dow futures also hit a record high on Thursday ahead of…

Futures Hit Fresh Record High Ahead Of PPI, Claims Data

Another day, another all time high in US equity futures with spoos trading at the nice, round 4,444 on Thursday morning, while Dow futures also hit a record high on Thursday ahead of earnings reports from companies including Walt Disney and data expected to show a jobs market recovery was on track.

Yet while nothing can stop the relentless juggernaut in US stocks, global equity markets fluctuated on Thursday, with European shares taking a pause after an eight-day rally of record highs on a mixed batch of earnings as Asian shares failed to follow a strong close on Wall Street with fears about the spread of the Delta variant of the coronavirus weighing on sentiment even as tame U.S. inflation eased fears the Federal Reserve would rush to reduce its economic support. As of 715am S&P futures were up 4 points to 4,444, Dow futures traded up 43 points or 0.12% and Nasdaq futures were 4.75 higher or 0.03% to 15,024. Treasury 10Y yields rose as high as 1.36%, reversing the drop after yesterday's stellar 10Y auction as a 30Y auction looms; the dollar nudged higher while copper prices jumped after workers at a mine in Chile threatened to strike. Bitcoin dropped to $45,000.

In premarket trading, EBay slipped 1.7% after forecasting third-quarter revenue below analysts’ estimates, signaling that reopening economies and vaccine rollouts could be putting an end to the pandemic-led shopping boom. Shares of steelmaker Nucor Corp and equipment maker Caterpillar Inc inched higher in premarket trading, building on gains made on expectations of future infrastructure projects. Baidu shares fell 2.1% even after it beat expectations for quarterly revenue, buoyed by a rebound in advertising sales and higher demand for its artificial intelligence and cloud products. Here are some of the other notable movers today:

Clover Health Investments (CLOV) shares surge 12% in premarket trading, after its sales guidance for the year surpasses the highest analyst estimate.

Opendoor Technologies (OPEN) shares rise 18% with KeyBanc saying its 2Q results serve as a positive inflection point for the company.

Sonos (SONO) shares gain 12% in premarket following a third-quarter earnings beat and guidance raise that was driven by speaker sales, according to Raymond James.

Xeris Pharmaceuticals (XERS) shares rise 21% after the firm announced it has received U.S. FDA clearance for phase 1 clinical trials for its hypothyroidism treatment.

On Wednesday, the S&P 500 and the Dow Jones Industrial Average logged a new record closing high helped by a rally in economy-linked value stocks following the passage of a large infrastructure bill, while the BLS reported the largest drop in month-to-month inflation in 15 months, easing concerns about the potential for runaway inflation. U.S. policymakers are publicly discussing how and when they should begin to trim the massive asset purchases launched by the Fed last year to stabilize financial markets and support the economy through the coronavirus pandemic. The easing of fears about inflation reduces the pressure to taper those asset purchases soon rather than later in the year, after strong employment figures last week had given ammunition to those with a more hawkish tilt. As a result, U.S. Treasury yields fell on Wednesday across most maturities, though trading was choppy.

Meanwhile, the Labor Department’s Initial jobless claims report due at 0830 a.m. ET is likely to show the number of Americans filing new claims for unemployment benefits fell further in the week ended Aug. 7. Focus will also be on U.S. producer prices data after soft inflation figures for July on Wednesday assuaged fears of sooner-than-expected policy tightening by the Federal Reserve.

“The data yesterday was encouraging but any signs here that it was a blip could unwind all of yesterday’s good feeling and replace it with anxiety once more,” said Craig Erlam, senior market analyst at OANDA Europe.

Palantir, DoorDash, Disney and Airbnb are among companies reporting earnings; DoorDash was up 2.3% on a report that the company held talks to buy grocery delivery firm Instacart for a likely price of between $40 billion and $50 billion.

Expected data include unemployment claims and indexes of producer prices: "If today’s U.S. PPI numbers for July follow a similar pattern to yesterday’s CPI, then that could reinforce further the transitory narrative that the U.S. Federal Reserve has been pushing,” said Michael Hewson, chief market analyst at CMC Markets in London. “It’s also likely to be good news for stocks."

European equities ground higher after a slow start. The Euro Stoxx 50 rose 0.25%, trading just shy of best levels for the week. The Stoxx 600 Index rose 0.15% as gains in insurance and telecom firms offset declines in miners. France’s CAC Index climbed within about 1% of an all-time high, which would mark the first record in two decades. Insurance, telecoms and auto names outperform; miners are the standout laggard so far. FTSE 100 underperforms, trading slightly in the red.

Corporate earnings results were the biggest driver behind individual stock moves. Insurer Aegon NV surged 7%, the top gain in the Stoxx 600 Index, after posting strong second-quarter results. Delivery Hero SE and German office supply maker Bechtle AG sank after disappointing analysts.

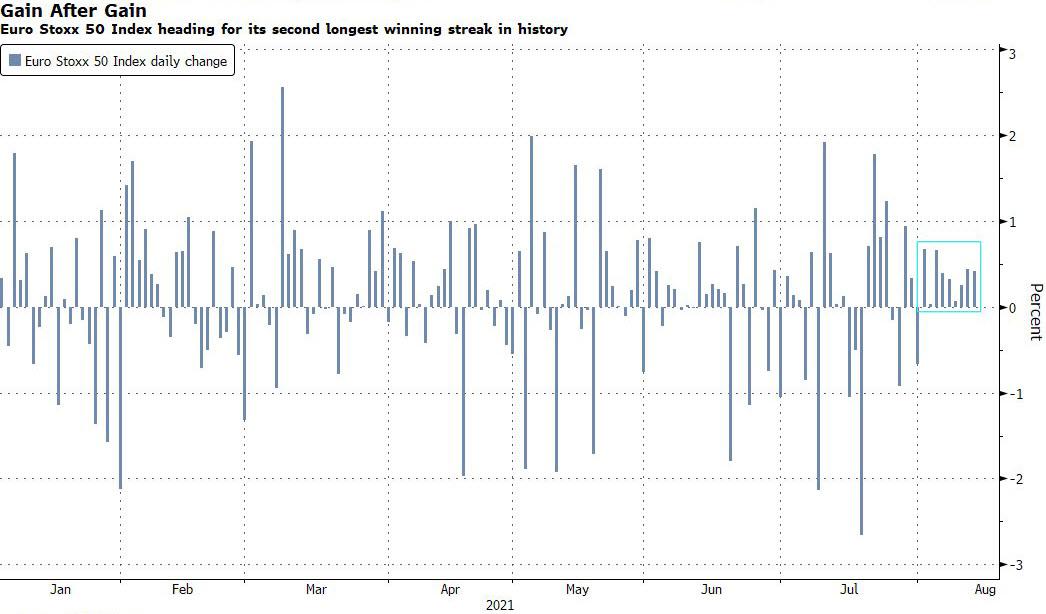

Still, while today's market action was been subdued, European equities have steadily made their way higher as investors put their faith in the economic reopening story. The blue-chip Euro Stoxx 50 Index is up for nine straight days and on track for the second-longest winning streak in its history.

Earlier in the session, Asian stocks fell for the first time in four days, hurt by losses in heavyweight chipmaking companies. The MSCI Asia Pacific Index fell as much as 0.5% dragged by a decline in Chinese bluchips. The Hong Kong benchmark fell 0.2% while Australian shares were largely flat and Japan's Nikkei rose 0.35%. The weaker performance by Asian benchmarks contrasts with the situation elsewhere in the world. On Wednesday the MSCI all-country index hit a record high. In comparison the Asian benchmark is down over 10% from its February peak.

"The money is just in the U.S. and European markets right now, and that's our preferred market too," said Daniel Lam, senior cross-asset strategist, Standard Chartered Wealth Management. Lam pointed to a strong U.S. earning season and Europe's high vaccination rates meaning the pace of reopening has been less harmed by the spread of the Delta variant of the new coronavirus, and "recent China regulation blues" in sectors such as education and technology.

"I think that the rotation from emerging markets to Western markets could continue in the near-term," said David Chao, Global Market Strategist, Asia Pacific (ex-Japan) at Invesco. "The APAC region’s zero-tolerance policy coupled with a relatively low vaccination rate has led to vicious lockdown-release cycle which could continue for a while."

Technology was Asia's worst-performing sector, with Samsung Electronics and SK Hynix among the biggest drags, as Morgan Stanley lowered its view on memory-chip makers. Gains in industrial and materials shares cushioned the benchmark index’s downside. “For the past few months, there’s been worry that memory prices will hit a peak and pull back,” said Nomura analyst C.W. Chung, noting that “chip prices can’t rise forever” given their supply and demand cycle. Rising virus cases across the region and China’s moves to regulate businesses continue to be a risk for equity investors in Asia. China released a five-year blueprint calling for greater regulation of vast parts of the economy, providing a sweeping framework for the broader crackdown on key industries that has left markets reeling. The benchmark CSI 300 Index fell 0.8% in a second day of losses.

China's State Council and the CCP's Central Committee released paperwork calling for significant increases in regulation in numerous sectors of the economy over the coming years. The news further demonstrates the ability of the CCP to strategically shape its economy in its own interests, but it also points to a limited role for the private sector over the medium-term.

Philippines’ equity benchmark was the worst performer in Asia on Thursday as the nation’s daily Covid-19 cases climbed to the highest in almost four months. Meanwhile, South Korea warned of more social distancing rules to contain the virus and in Japan, Tokyo reported 4,989 new virus cases, up from 4,200 Wednesday.

Japanese equities closed lower, erasing earlier gains, as profit-takers emerged following four days of gains. Tech stocks were the biggest drags on the Topix, which closed less than 0.1% lower after wiping out a gain of as much as 0.8%. Most sectors rose, including chemicals, machinery and banks. Chip equipment makers Tokyo Electron and Advantest were the biggest contributors to a 0.2% loss in the Nikkei 225. Japanese stocks opened higher after the S&P 500 climbed to a fresh record following a report showing that U.S. inflation moderated. The Nasdaq 100 declined as investors rotated to cyclical shares from growth. Meanwhile, the Japanese government is considering expanding the areas of the state of emergency and may extend the current order through September, the Sankei newspaper reported. “Investors may be taking profits ahead of the Obon holidays, adjusting positions,” said Shoichi Arisawa, an an analyst at Iwai Cosmo Securities Co. “While the debate over whether to extend and expand the state of emergency damps the market mood, some of the sectors are looking ahead to the post-pandemic world. The state of emergency might not be directly impacting Japanese markets at the moment.” The MSCI Asia Pacific Index was down 0.3% after China released a five-year blueprint calling for greater regulation of vast parts of the economy.

In India, gains in information technology stocks propelled shares to record closing highs on Thursday, ahead of data expected to show a slowdown in monthly inflation. The blue-chip NSE Nifty 50 index closed 0.50% higher at 16,364 and the benchmark S&P BSE Sensex ended up 0.6% at 54,843.98. Leading the gains among sectoral indexes, the Nifty IT services index rose 1.82%. “High liquidity has helped markets touch fresh highs. The comeback of small and mid-cap stocks after the clarification (from BSE) also helped,” said Vinod Nair, head of research at Geojit Financial Services. The Nifty mid-cap index and small-cap index gained 1% and 2.1%, respectively, after falling more than 2% each earlier this week. The weakness had come after a circular here on Monday from BSE Ltd over price curbs to curb volatility. But the exchange clarified here on Wednesday the rules would only be applicable on stocks that are priced above 10 rupees and have a market capitalization of less than 10 billion Indian rupees ($134.71 million). Among individual stocks, Indian budget carrier SpiceJet Ltd rose 5.1% after a report that the country was set to allow Boeing’s 737 Max jets to resume flights in the country within days. Helped by strong quarterly earnings, Drugmaker Indoco Remedies rose over 17%, luggage maker VIP Industries Ltd surged 20% and Punjab Chemicals and Crop Protection Ltd advanced 18%.

In rates, Treasuries rebounded from Wednesday's post CPI and 10Y Auction lows, with the yield on U.S. 10- year Treasuries rising 2bps to 1.35% after slipping by the same amount Wednesday following muted price action in Asia and early European sessions. Gilts lagged following a raft of U.K. data including GDP and industrial production figures. The market will focus on 30-year bond auction Thursday, following yesterday’s strong 10-year reception. Refunding U.S. auctions conclude with $27BN 30-year bond sale at 1pm ET, follows Wednesday’s stellar 10-year auction which traded over 3bp through the WI level.

In Fx, the dollar hovered below a four-month peak against major peers on Thursday, after retreating overnight as yields dropped. The Bloomberg Dollar Spot Index was flat following its 0.2% fall Wednesday after a release showed prices paid by U.S. consumers climbed in July at a more moderate pace. The Australian dollar declined against all its Group-of-10 peers as the nation’s capital is set to enter a lockdown to curb the coronavirus spread. Most other Group-of-10 currencies traded in narrow ranges, with the Nordic currencies leading.

"I expect the dollar to be range-bound on the recent strong unemployment and tempered CPI data," said Invesco's Chao.

In commodities, crude oil fluctuated after the International Energy Agency cut forecasts for global demand “sharply” and predicted a new surplus in 2022. Most Asian markets fell after China released a five-year plan calling for greater business regulation as Beijing steps up scrutiny of insurance technology platforms. WTI dipped 0.03% to $69.23 a barrel. Brent crude was flat at $71.43 per barrel. Gold also held on to overnight gains on Thursday, with the spot price down 0.1% having risen 1.3% in the previous session. Easing of fears about higher interest rates would typically help the non-interest bearing asset.

Looking at the day ahead, investors will be assessing July PPI data along with weekly initial jobless claims and continuing claims. Following a busy week, there are no Fed speakers scheduled for today, but there will be a monetary policy decision from the Bank of Mexico. In terms of earnings, Walt Disney, China Mobile, Deutsche Telekom, AirBnB, Doordash, and Baidu are all reporting as we approach the end of earnings season. Also investors are sure to look at OPEC’s monthly oil market report for signals on where pricing is going.

Market Snapshot

S&P 500 futures little changed at 4,440.75

MXAP down 0.3% to 200.51

MXAPJ down 0.4% to 661.42

Nikkei down 0.2% to 28,015.02

Topix little changed at 1,953.55

Hang Seng Index down 0.5% to 26,517.82

STOXX Europe 600 little changed at 474.54

Shanghai Composite down 0.2% to 3,524.74

Sensex up 0.5% to 54,824.32

Australia S&P/ASX 200 little changed at 7,588.19

Kospi down 0.4% to 3,208.38

Brent Futures little changed at $71.42/bbl

Gold spot up 0.1% to $1,754.09

U.S. Dollar Index little changed at 92.90

German 10Y yield fell 0.3 bps to -0.462%

Euro little changed at $1.1741

Top Overnight News from Bloomberg

Money-market traders are starting to get nervous that the debt- ceiling battle will go down to the wire, even though the U.S. government has created some breathing room for now

China is halting private equity funds from raising money to invest in residential property developments, turning off the spigot on one of the last stable funding resorts for the struggling sector

Rishi Sunak promised the U.K. won’t see a return to the austerity policies of last decade and that he is “united” with Prime Minister Boris Johnson over plans to rebuild the economy after the pandemic

The International Energy Agency cut forecasts for global oil demand “sharply” for the rest of this year as the resurgent pandemic hits major consumers, and predicted a new surplus in 2022

A member of a Tokyo Metropolitan Government coronavirus advisory panel of experts said it was now impossible to control the spread of Covid-19 in the capital

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac equities traded saw a mixed session with a downside bias and a cautious tone after a Wall Street closed mostly higher; cyclicals and value continued to show outperformance and tech failed to sustain a bid despite lower Treasury yields on the back of cooling CPI. The DJIA outperformed while the NDX lagged, and the VIX fell beneath 16 for the first time since early July. Back to APAC, the ASX 200 (+0.1%) gave up its earlier gains as Australia’s COVID woes deepen, with areas in Sydney tightening restrictions and Canberra tipped to enter a lockdown. The Nikkei 225 (-0.2%) was initially kept afloat by its manufacturing sector, although a firmer JPY and cautious risk tone capped upside. The KOSPI (-0.4%) remained on guard as North Korea did not respond to South Korea’s calls for a third straight day, in the run-up to annual military drills between Washington and Seoul. Elsewhere, the Hang Seng (-0.5%) and Shanghai Comp (-0.2%) traded downbeat amid reports of further sectorial crackdowns, this time the insurance and aesthetic medicines sectors, whilst peak growth and COVID concerns simmer in the background for China.

Top Asian News

Tokyo Virus Situation Is Out of Control, Panel Expert Says

Volatility Sneaks Back Into Emerging Markets Amid Fed Angst

Masks and Rules Return to Shanghai Banks Preparing for the Worst

Beijing Capital Said to Mull Sale of $1 Billion New Zealand Unit

European equities (Eurostoxx 50 +0.2%) trade mixed/flat amid a lack of fresh macro impulses for the region. The lead from Asia was predominantly downbeat with pressure observed in Chinese bourses amid further regulatory crackdowns, this time with the insurance and aesthetic medicines sectors in the sights of the government. Stateside, US futures trade in close proximity to the unchanged mark with very mild underperformance in the NQ (-0.1%) vs. ES (U/C) in a minor continuation of yesterday’s underperformance. Sectors in Europe are mixed with Insurance names top of the pile following earnings from Aviva (+4.4%) and Zurich Insurance (+3.7%) who both sit at the top of their respective indices. Telecom names are also firmer on the session amid gains in Deutsche Telekom (+2.9%) after the Co. raised guidance alongside Q2 earnings. To the downside, Basic Resources are the clear laggard (when looking at the Stoxx 600 BR Index), however, this is more a by-product of the Stoxx 600 Basic Resource index not adjusting for Rio Tinto trading ex-div rather than any systemic underperformance in the sector (nb. other miners trade with much shallower losses than the index). In terms of individual movers, Ageon (+7.3%) is the best performer in the Stoxx 600 after delivering strong Q2 results. Deliveroo (+4.7%) also trade firmer on the session as the Co. looks to claw back some of yesterday’s earnings-inspired losses. Competitor, Delivery Hero (-4.5%) trades softer on the session despite raising guidance alongside Q2 results as concerns linger over how long it will take the Co. to make a profit amid recent investments.

Top European News

Aviva to Hand Investors $5.6 Billion Following Asset Sales

U.K. Economy Sees Faster Growth in June as Lockdown Eases

U.K. City Center Offices Drawing Just 18% of Staff, Study Finds

Poland Defies U.S. and EU by Passing Contentious Media Law

In FX, the Dollar is mixed and tightly bound against major counterparts, with the DXY holding just off Wednesday's post-US inflation data low (92.800) and now looking towards pipeline prices to see what kind of pressures are building, but perhaps more pertinently at the latest snapshot of the labour market via jobless claims to find out whether there has been further progress following last month’s healthy BLS report. The index is hovering below 93.000 within a 92.962-845 range and inside w-t-d extremes (93.195-92.718) after more taper talk from Fed officials, but no scheduled speakers today leaving the stage clear for long bond issuance once the aforementioned data is out of the way.

AUD/CAD/NZD - It’s marginal, but the Aussie, Loonie and Kiwi are underperforming after taking advantage of the Greenback’s loss of momentum yesterday. Aud/Usd has drifted back down from 0.7377 or so overnight as COVID-19 restrictions are tightened further in Sydney and the capital Canberra prepares to join the list of big cities entering lockdown, according to local media reports. Meanwhile, Usd/Cad is back above 1.2500 against the backdrop of ongoing volatility in crude plus unusually large option expiries between 1.2495 and the big figure (1.6 bn) and the Kiwi has retreated through 0.7050 even though Q3 NZ inflation expectations revealed a jump in the 12 month outlook and firmer 2 year projection to underscore already odds-on pricing for RBNZ tightening next week.

EUR/JPY/CHF/GBP - The Euro is still breathing a huge sigh of relief following its recovery from the clutches of a new y-t-d low, albeit thanks to others in the main if not entirely. However, Eur/Usd remains top heavy around 1.1750 and faces a string of big option expiries beyond the half round number (from 1.1775-90, through 1.1795-00 to 1.1810-15 in 1.6 bn, 1.6 bn and 2 bn respectively). Elsewhere, the Yen has rebounded over 110.50 again, but could also be stymied by option expiry interest given 1.4 bn rolling off at 110.35-30, the Franc has pared losses from sub-0.9240 to hover nearer 0.9200 and the Pound is consolidating above 1.3850 with more direction derived from outside influences and external factors than very mixed UK data. From a technical perspective, Cable sits almost equidistant from 21 and 50 DMAs that come in at 1.3832 and 1.3894 today.

SCANDI/EM - Moderately positive risk sentiment and Brent maintaining its recovery momentum are more likely drivers behind the Sek and Nok revival to post fresh weekly peaks vs the Eur rather than unchanged Swedish money market CPIF forecasts over 1 and 5 year horizons. Meanwhile, the Try and Mxn will be hoping for some independent inspiration from the CBRT and Banxico as the former rebounds further from worst levels with the aid of better than anticipated Turkish ip data in the interim. Note, previews for both policy meetings are available in the Research Suite.

In commodities, crude benchmarks have been contained around the unchanged mark for the entirety of the European and APAC sessions, as such ranges are narrow and currently around USD 0.50/bbl for both WTI and Brent. As price action has been minimal, we do reside in close proximity to the highs of yesterday’s session, printed just after the European cash equity close, as the complex derived support from the White House’s initial commentary which implied no immediate/sudden pressure on OPEC+, following the earlier statements. This morning, the main event has been the IEA MOMR which looks for oil demand to rise by 5.3mln BPD in 2021 and by an additional 3.2mln BPD in 2022; however, they reduced their demand outlook for the remainder of 2021 due to the worsening COVID-19 situation. No price reaction on the release. Separately, at 11:50BST today the equivalent report from OPEC is scheduled for release. Moving to metals, spot gold and silver print modest divergence but ranges are minimal and fresh newsflow for the complex has been very slim; the schedule ahead has the US PPI release which will be scrutinised for any further inflation updates after yesterday’s CPI release. Elsewhere, copper prices are supported but near familiar levels as we continue to await BHP/Escondida updates after yesterday’s prelim. wage agreement; however, this still needs to be ratified by the unions members to remove the risk of strike action.

US Event Calendar

8:30am: U.S. Initial Jobless Claims, Aug. 7, est. 375k, prior 385k; Continuing Claims, July 31, est. 2900k, prior 2930k

8:30am: U.S. PPI Final Demand MoM, July, est. 0.6%, prior 1.0%; PPI Final Demand YoY, July, est. 7.2%, prior 7.3%

8:30am: U.S. PPI Ex Food and Energy MoM, July, est. 0.5%, prior 1.0%; PPI Ex Food and Energy YoY, July, est. 5.6%, prior 5.6%

DB's Jim Reid concludes the overnight wrap

There was a bit of an everything-rally yesterday as equities hit another record high even as bonds rallied on slightly moderating (but still high) US inflation data, and a strong 10yr auction. The S&P rose +0.25%, and has now traded in a less than 0.34% range in each of the last 4 sessions. The confirmation of the US infrastructure package saw the construction & engineering (+3.08%), transportation (+1.85%) and materials (+1.42%) industries outperform yesterday. In Europe, the STOXX 600 (+0.42%) reached a new high for an eighth straight session with cyclicals largely driving the increase. It is the longest such run of gains since June.

The obvious highlight of the day was US inflation data from July which showed headline CPI rising +0.5%, in line with expectations and leaving year-over-year change steady at 5.4% (5.3% expected). Core inflation rose by +0.3% (+0.4% expected), which was the softest reading since March. The goods readings moderated substantially due to supply/demand imbalances easing, particularly in the much watched areas of autos. The reopening-sensitive categories (autos, insurance, lodging, airfare, restaurants) made up just 13% of the overall monthly increase, after being over 50% of the previous 3 inflation prints. So moderation here but while yesterday’s US CPI print was a fraction below expectations, the last 4 months has still been a remarkable period for inflation beats. As my CoTD from yesterday (link here) showed, in the last 4 months of prints, the cumulative monthly beat has been 1.1pp for both headline and core relative to consensus expectations on Bloomberg. That level of expectation beats dwarfs what we have seen over the last 24 years of data, especially for core.

This data was followed by a bevy of Fed speakers, with the normally hawkish Governor Bostic speaking for the second time this week. He mirrored Governor Mester’s speech from the day before, saying “we have seen inflation rise above 2% as the economy recovers from the pandemic downturn. But most of that rise is fueled by forces that should recede over time. So, I expect price inflation to average close to our target over the longer term.” He also again affirmed that the Fed is more focused on the job market, saying that “The committee will no longer preemptively raise interest rates in response to a ‘hot’ labor market because of fear that inflation will eventually be a result.” Fed Governor George (non-voter this year) agreed with Bostic’s view from earlier in the week that the Fed ought to start reducing monetary stimulus, saying that “substantial” progress has been made. Lastly, Governor Kaplan actually laid out a timeline for investors saying he “would be in favour of announcing a plan at the September meeting and beginning tapering in October.”

After the three previous CPI readings saw a greater than 5bps move in Treasuries on the day, yesterday’s reading saw a much tamer response. US 10yr yields fell -1.9bps, their first retreat in the last 6 sessions. The drop was due to real yields falling, which overcame a slight increase in inflation expectations (+1.4bps). A successful 10 year auction after US lunchtime helped continue the rally after a pre-CPI sell off.

Germany’s final inflation data was in-line yesterday morning, with July CPI coming in at +0.9% m/m and +3.8% y/y, which saw 10yr bund yields fall marginally (-0.7bps). Overall, other European sovereign bonds underperformed bunds yesterday with yields on OATs (+0.1bps) and BTPs (+1.8bps) slightly higher. Staying with fixed income, the start of August has seen credit issuance explode in the US, with 48 dollar transactions being brought to market between IG and HY in the first two days of this week. There were an additional 8 US high-grade deals priced yesterday, which takes their overall issuance to $41bn this week so far, well ahead of the $25-30bn expected. It seems corporates are taking advantage of the lower Treasury yields and are either refinancing more expensive debt or are pulling forward autumn bond sales.

Following the late Tuesday night vote to move forward on the planned $3.5 trillion “human infrastructure” package, which includes funding for healthcare, higher education, paid family leave, climate policy among other Democratic initiatives, President Biden sought to get ahead of some the criticism surrounding potential inflation. The President said “If your primary concern right now is the cost of living, you should support this plan …A vote against this plan is a vote against lowering the cost of health care, housing, child care, and elder care and prescription drugs for American families.” The passage of this bill will take a good amount of shepherding as two moderate Senate Democrats have already said they agreed to discuss the bill, but do not support the $3.5 trillion price tag. At the same time, Democratic House members have said the $3.5tn is as low as they would want to go to enact consequential change. This will get picked up again in September when all members return, but this bill along with the bipartisan infrastructure package make up nearly the entirety of Biden’s domestic policy platform.

Overnight, China’s State Council and the Communist Party’s Central Committee have jointly released a statement saying that authorities would “actively” work on legislation in areas including national security, technology and monopolies while adding that law enforcement will be strengthened in sectors ranging from food and drugs to big data and artificial intelligence. In addition to this, China’s banking and insurance watchdog has ordered companies and local agencies to curb improper marketing and pricing practices, and step up user privacy protection. The agency said that it is encouraging for companies to address these issues voluntarily and said those that failed to comply would face “severe punishment.” Chinese stocks are weaker on the back of this with the the CSI (-0.61%) and Shanghai Comp (-0.12%) both in the red, while the Hang Seng (-0.10%) and Kospi (-0.13%) have also seen modest falls. The Nikkei (+0.15%) is the exception. Outside of Asia, futures on the S&P 500 are unchanged while yields on 10y USTs are up +1.4bps to 1.346%.

On the pandemic, there was good news yesterday from the UK with fewer than 1% of UK school students and teachers testing positive for Covid-19 in June, which was significantly lower than last Autumn according to a study by the ONS. This is seen as an optimistic sign for those who want to convince parents and health ministers that it is safe to send kids back to school when term starts next month. Meanwhile, the US continues to have diverging policies around schools. Yesterday, California mandated that all teachers and school personnel be vaccinated or be subjected to weekly testing, while in Florida the Governor banned school districts from instituting a mask mandate. This comes as Moderna announced plans to double the size of its under-12 vaccine trial to nearly 13,275, after a request from the US regulators for additional safety data. Bloomberg has reported overnight that the US FDA might clear vaccines from Moderna and Pfizer/BioNTech for booster doses as soon as today for people with compromised immune systems. Meanwhile, even as the Olympics have ended, cases continue to rise in Japan and the government is considering increasing the radius of its state of emergency to additional areas outside of Tokyo and keeping it in force through September, rather than ending it this month.

To the day ahead now and we will get our first look at UK Q2 GDP and the June industrial and manufacturing production data as well as the Euro Area June industrial production. Over in the US, investors will be assessing July PPI data along with weekly initial jobless claims and continuing claims. Following a busy week, there are no Fed speakers scheduled for today, but there will be a monetary policy decision from the Bank of Mexico. In terms of earnings, Walt Disney, China Mobile, Deutsche Telekom, AirBnB, Doordash, and Baidu are all reporting as we approach the end of earnings season. Also investors are sure to look at OPEC’s monthly oil market report for signals on where pricing is going.

Simple blood test could predict risk of long-term COVID-19 lung problems

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to…

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to suffer “long-haul” lung problems. That finding could help doctors better personalize treatments for individual patients.

Credit: UVA Health

UVA Health researchers have discovered a potential way to predict which patients with severe COVID-19 are likely to recover well and which are likely to suffer “long-haul” lung problems. That finding could help doctors better personalize treatments for individual patients.

UVA’s new research also alleviates concerns that severe COVID-19 could trigger relentless, ongoing lung scarring akin to the chronic lung disease known as idiopathic pulmonary fibrosis, the researchers report. That type of continuing lung damage would mean that patients’ ability to breathe would continue to worsen over time.

“We are excited to find that people with long-haul COVID have an immune system that is totally different from people who have lung scarring that doesn’t stop,” said researcher Catherine A. Bonham, MD, a pulmonary and critical care expert who serves as scientific director of UVA Health’s Interstitial Lung Disease Program. “This offers hope that even patients with the worst COVID do not have progressive scarring of the lung that leads to death.”

Long-Haul COVID-19

Up to 30% of patients hospitalized with severe COVID-19 continue to suffer persistent symptoms months after recovering from the virus. Many of these patients develop lung scarring – some early on in their hospitalization, and others within six months of their initial illness, prior research has found. Bonham and her collaborators wanted to better understand why this scarring occurs, to determine if it is similar to progressive pulmonary fibrosis and to see if there is a way to identify patients at risk.

To do this, the researchers followed 16 UVA Health patients who had survived severe COVID-19. Fourteen had been hospitalized and placed on a ventilator. All continued to have trouble breathing and suffered fatigue and abnormal lung function at their first outpatient checkup.

After six months, the researchers found that the patients could be divided into two groups: One group’s lung health improved, prompting the researchers to label them “early resolvers,” while the other group, dubbed “late resolvers,” continued to suffer lung problems and pulmonary fibrosis.

Looking at blood samples taken before the patients’ recovery began to diverge, the UVA team found that the late resolvers had significantly fewer immune cells known as monocytes circulating in their blood. These white blood cells play a critical role in our ability to fend off disease, and the cells were abnormally depleted in patients who continued to suffer lung problems compared both to those who recovered and healthy control subjects.

Further, the decrease in monocytes correlated with the severity of the patients’ ongoing symptoms. That suggests that doctors may be able to use a simple blood test to identify patients likely to become long-haulers — and to improve their care.

“About half of the patients we examined still had lingering, bothersome symptoms and abnormal tests after six months,” Bonham said. “We were able to detect differences in their blood from the first visit, with fewer blood monocytes mapping to lower lung function.”

The researchers also wanted to determine if severe COVID-19 could cause progressive lung scarring as in idiopathic pulmonary fibrosis. They found that the two conditions had very different effects on immune cells, suggesting that even when the symptoms were similar, the underlying causes were very different. This held true even in patients with the most persistent long-haul COVID-19 symptoms. “Idiopathic pulmonary fibrosis is progressive and kills patients within three to five years,” Bonham said. “It was a relief to see that all our COVID patients, even those with long-haul symptoms, were not similar.”

Because of the small numbers of participants in UVA’s study, and because they were mostly male (for easier comparison with IPF, a disease that strikes mostly men), the researchers say larger, multi-center studies are needed to bear out the findings. But they are hopeful that their new discovery will provide doctors a useful tool to identify COVID-19 patients at risk for long-haul lung problems and help guide them to recovery.

“We are only beginning to understand the biology of how the immune system impacts pulmonary fibrosis,” Bonham said. “My team and I were humbled and grateful to work with the outstanding patients who made this study possible.”

Findings Published

The researchers have published their findings in the scientific journal Frontiers in Immunology. The research team consisted of Grace C. Bingham, Lyndsey M. Muehling, Chaofan Li, Yong Huang, Shwu-Fan Ma, Daniel Abebayehu, Imre Noth, Jie Sun, Judith A. Woodfolk, Thomas H. Barker and Bonham. Noth disclosed that he has received personal fees from Boehringer Ingelheim, Genentech and Confo unrelated to the research project. In addition, he has a patent pending related to idiopathic pulmonary fibrosis. Bonham and all other members of the research team had no financial conflicts to disclose.

The UVA research was supported by the National Institutes of Health, grants R21 AI160334 and U01 AI125056; NIH’s National Heart, Lung and Blood Institute, grants 5K23HL143135-04 and UG3HL145266; UVA’s Engineering in Medicine Seed Fund; the UVA Global Infectious Diseases Institute’s COVID-19 Rapid Response; a UVA Robert R. Wagner Fellowship; and a Sture G. Olsson Fellowship in Engineering.

To keep up with the latest medical research news from UVA, subscribe to the Making of Medicine blog at http://makingofmedicine.virginia.edu.

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

These are the themes that emerged when I invited nine Black women to chronicle their professional experiences and relationships with colleagues as they earned their Ph.D.s at a public university in the Midwest. I featured their writings in the dissertation I wrote to get my Ph.D. in curriculum and instruction.

“It’s not just the beating me down that is hard,” one participant told me about constantly having her intelligence questioned. “It is the fact that it feels like I’m villainized and made out to be the problem for trying to advocate for myself.”

The women told me they did not feel like they belonged. They spoke of routinely being isolated by peers and potential mentors.

One participant told me she felt that peer community, faculty mentorship and cultural affinity spaces were lacking.

Participants also discussed the ways they felt they were duped into taking on more than their fair share of work.

“I realized I had been tricked into handling a two- to four-person job entirely by myself,” one participant said of her paid graduate position. “This happened just about a month before the pandemic occurred so it very quickly got swept under the rug.”

Why it matters

The hostility that Black women face in higher education can be hazardous to their health. The women in my study told me they were struggling with depression, had thought about suicide and felt physically ill when they had to go to campus.

Other studies have found similar outcomes. For instance, a 2020 study of 220 U.S. Black college women ages 18-48 found that even though being seen as a strong Black woman came with its benefits – such as being thought of as resilient, hardworking, independent and nurturing – it also came at a cost to their mental and physical health.

Several anthologies examine the negative experiences that Black women experience in academia. They include education scholars Venus Evans-Winters and Bettina Love’s edited volume, “Black Feminism in Education,” which examines how Black women navigate what it means to be a scholar in a “white supremacist patriarchal society.” Gender and sexuality studies scholar Stephanie Evans analyzes the barriers that Black women faced in accessing higher education from 1850 to 1954. In “Black Women, Ivory Tower,” African American studies professor Jasmine Harris recounts her own traumatic experiences in the world of higher education.

What’s next

In addition to publishing the findings of my research study, I plan to continue exploring the depths of Black women’s experiences in academia, expanding my research to include undergraduate students, as well as faculty and staff.

I believe this research will strengthen this field of study and enable people who work in higher education to develop and implement more comprehensive solutions.

The Research Brief is a short take on interesting academic work.

Ebony Aya received funding from the Black Collective Foundation in 2022 to support the work of the Aya Collective.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}