Futures, Global Stocks Extend Gains To End Volatile Week

Futures, Global Stocks Extend Gains To End Volatile Week

S&P index futures ticked higher on Friday, alongside European and Asian stocks, and building on Thursday’s strong gains as bullish investor sentiment got a boost from strong global.

Share this:

S&P index futures ticked higher on Friday, alongside European and Asian stocks, and building on Thursday's strong gains as bullish investor sentiment got a boost from strong global PMI surveys while reflation fears faded. Oil climbed while treasury yields and the dollar were little changed. Dow e-minis were up 150 points, or 0.4%, S&P 500 e-minis were up 18 points, or 0.43%, and Nasdaq 100 e-minis were up 51 points, or 0.4%.

Wall Street’s rebounded on Thursday following a three-day slump after data showed the fewest weekly jobless claims since the recession in 2020. The risk recovery was led by FAAMG gigacaps as inflation fears appear to have now peaked, putting the Nasdaq on course to snap a four-week losing streak as worries over higher interest rates weighed on the tech-heavy index.

“We believe there is still an upside story to be told,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “Beneficiaries of reflation, like financials and energy, still have ‘catch up’ potential, while the relative near-term case for mega-cap tech is less clear.”

The S&P 500 and the Dow were headed for second straight weekly declines, after a volatile week, with euphoria cooling as minutes from the latest Federal Reserve meeting flagged the possibility of a debate at some point on scaling back stimulus measures. Still, better-than-forecast jobless claims data on Thursday buoyed sentiment. Here are some of the biggest Friday movers in the US:

- Tesla shares dropped after Bank of America cut its price target from $900 to $700.

- AT&T shares rose 1.4% after an upgrade to buy at both UBS and New Street Research following company’s deal with Discovery to spin off its media business.

- Datadog shares gain 3.3% premarket after the software company is upgraded to overweight from equalweight at Morgan Stanley, which says the company is serving a critical role in helping companies switch to cloud operating models.

- Virgin Galactic shares gained 3.3% after being upgraded to buy from neutral at UBS, which says the “price is right” for the space tourism company.

- Deere & Co gained 2.4% after the farm equipment manufacturer raised its full-year profit forecast.

- Foot Locker gains 3.4% premarket after reporting comparable sales and earnings for the first quarter that beat the average analyst estimate.

- Palo Alto Networks’ growth outlook is not fully-reflected in the cyber security firm’s shares, analysts say after the group raised its earnings forecasts alongside quarterly results Thursday. The stock gains 6% premarket

- Buckle shares rise 9% premarket after the retailer reported first quarter net sales that more than doubled from the prior year period

Bitcoin hovered around $40,000, pausing its attempt to recover from this week’s massive plunge. Cryptocurrency-related stocks Coinbase Global, Riot Blockchain and Marathon Digital Holdings firmed 0.7% and 2%.

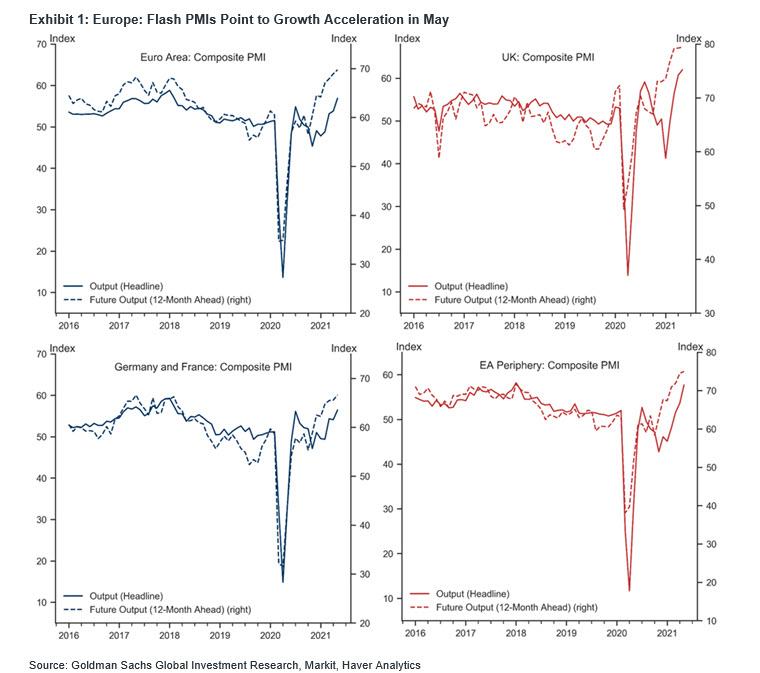

European equities rebounded from a modest loss and were near their best levels of the day, up 0.5% as all sectors gained, led higher by consumer products, autos and travel & leisure names. The FTSE MIB outperformed marginally. Euro zone business growth accelerated at its fastest pace in over three years in May, as a strong resurgence in the bloc’s reopening service industry added to the impetus from an already-booming manufacturing sector, a survey showed on Friday.

With more businesses reopening, Markit’s flash Composite Purchasing Managers’ Index climbed to 56.9 from April’s final reading of 53.8. That was its highest level since February 2018 and comfortably above the 50 mark separating growth from contraction, as well as the more modest increase to 55.1 predicted in a Reuters poll.

“May’s increase in the euro zone Composite PMI reflects the further lifting of virus restrictions in many parts of the region and suggests that the economic recovery is now underway,” said Jessica Hinds at Capital Economics. In Germany, Europe’s largest economy, services activity rose by the most in nearly a year, helped by a loosening of restrictions. But supply bottlenecks in manufacturing led to production problems at a growing number of factories. The lifting of a lockdown in France unleashed a business boom there, with activity surging past expectations to set the stage for an economic rebound.

Here are some of the biggest European movers today:

- Richemont shares advance as much as 6.4% to a record after fiscal FY results impressed investors, with analysts predicting the Cartier owner will continue benefiting from pent-up demand for jewels as consumers splash out in the pandemic aftermath.

- Travis Perkins rises as much as 3.3%, hitting the highest intraday since December 2019. The building materials distributor’s sale of its plumbing and heating business will allow it to focus on its core growth drivers with its end- markets in good health, analysts say.

- PKO advances as much as 3.8% after Poland’s de facto leader Jaroslaw Kaczynski said the next chief executive officer of the state-controlled lender will be picked from among members of its current management.

- Card Factory tumbles as much as 16% after the U.K. retailer said it plans to use its “best efforts” to raise net equity proceeds of GBP70m to help with prepayments of bank loans.

Earlier in the session, Asian stocks rose capping a weekly gain, as a recovery in the technology sector helped lift shares in Japan and Taiwan. Chipmakers TSMC and Samsung Electronics were among the biggest boosts to the MSCI Asia Pacific Index, lifted by a tech-driven rebound in the U.S. overnight. A drop in U.S. initial jobless claims shifted investor focus back to prospects for a global economic recovery. A gauge of Asian tech stocks was poised for a weekly gain of over 2.5%, clawing back a sizable chunk of its 5.9% slide last week amid fears of inflation sparked by rising commodities prices. “With inflation fears ebbing, equity markets may resume rallying,” Oanda Asia Pacific analyst Jeffrey Halley wrote in a note. “I do not believe the inflation story is over, but I do accept it may be over for now. It shall return, but of one thing I am sure, we do not yet know if it will be transitory or sticky, for the first time in over 20 years.” Taiwan’s tech-heavy benchmark gained to cap a weekly advance of 3%, bouncing back after last week’s 8.4% tumble. Japanese stocks rose, helped by government approval of two additional coronavirus vaccines as well as gains in electronics makers. Indian equities also traded notable higher, helping offset losses in China and underperformance in Hong Kong. Tencent fell as much as 4.2%, dragging down a regional gauge of communications companies, after the internet giant announced plans to sharply increase spending to fend off competition.

Offsetting broader Asian bullishness, Chinese stocks fell, with broad-based declines led by financial and health care stocks. The CSI 300% Index closed down 1%, reversing an earlier rise of 0.6%. Still, the benchmark clocked its second straight week of gains with a 0.5% increase, as investors see shares bottoming out following a technical correction. Financial stocks had their worst day since April 30 while health care shares slid, dragged down by vaccine makers. Materials extended their declines to a third day, the longest streak in two months, reflecting lingering concern over the government’s pledge to curb commodity prices. Chongqing Zhifei Biological Products was the biggest drag on the main gauge, followed by financial service provider East Money Information, Walvax Biotechnology and China Merchants Bank. The earnings recovery story is not sufficient for a strong market rebound in the near term, while the peaking of China’s credit and business cycles will put downward pressure on market sentiment starting this quarter, Daiwa analyst Patrick Pan wrote in a note Thursday. Friday’s drop in stocks came as Chinese bonds advanced, with the yield on 10-year government bonds set for its lowest in more than eight months. Separately, foreign investors sold a net 578 million yuan of A shares via the trading link with Hong Kong, after an outflow of 1.5 billion yuan the previous day. In Hong Kong, Tencent shares fell 3.4%, most since April 7, after the conglomerate’s planned investment ramp-up prompted brokerage CICC to lower its earnings estimates. The Hang Seng Index closed little changed ahead of an announcement Friday of the details of a wide-ranging overhaul of Hong Kong’s equity benchmark

Japanese stocks rose to complete a weekly gain after a rally on Wall Street and a government panel’s approval of two coronavirus vaccines helped pull the market further back from the brink of a technical correction. Electronics makers and service providers were the biggest boosts to the Topix, which capped a weekly advance of 1.1%. Fast Retailing Co. and Tokyo Electron Ltd. gave the most support to the Nikkei 225 Stock Average, helping to pare its drop from a February peak to 7.1%. “Japanese stocks are tracking U.S. equities higher” and Applied Materials’ earnings are helping chip stocks, said Tetsuo Seshimo, a fund manager at Saison Asset Management Co. in Tokyo. Also, “Moderna and AstraZeneca vaccine approval overnight is helping support the Japanese equity markets.” Moderna is considering making its Covid-19 vaccine in Asia and may seek production contracts or license agreements with Japanese companies, the Nikkei reported, citing an interview with Chief Executive Officer Stephane Bancel. A government panel in Japan has approved the use of Moderna and AstraZeneca’s vaccines

In FX, the Bloomberg Dollar Spot Index hovered and the greenback traded mixed versus its Group-of-10 peers. The euro was little changed versus the dollar; it earlier fell and German bonds advanced, sending the 10-year yield to the lowest since Tuesday, after manufacturing PMI for Europe’s powerhouse missed the median estimate. The pound reversed a rally that had followed better- than-expected than U.K. retail sales data, only to recover shortly after PMI data (U.K. retail sales rose 9.2% m/m in April; est. +4.5%; U.K. May Flash Composite PMI 62 vs est 61.9). Australia’s dollar slid under weight of leveraged selling and iron ore’s third-straight decline; the nation’s bonds extended gains, aided by a rally in N.Z. debt that kicked off after the RBNZ kept QE unchanged amid strong long-end auction demand.

In rates, Treasuries were slightly cheaper across the curve with the 10Y Treasury yield near flat at 1.625%, in line with gilts and ~1bp cheaper vs bunds; most curve spreads marginally steeper, within a basis point of Thursday’s close. Long-end lags, with 30-year yields cheaper by around 1bp. Bunds outperforming after May manufacturing PMI fell more than expected. Asia-session futures flows included curve flattener via block trades in TY and US contracts. China’s bonds extended gains, with the yield on 10-year government bonds declining to the lowest level since September, as interbank borrowing costs declined. The yield on 10-year Chinese sovereign bonds fall 2bps to 3.07% after touching 3.06%, the lowest since September; Futures on the notes jump 0.3% to highest since August.

In commodities, Brent oil trimmed its biggest weekly decline since March. Brent oil was heading for the biggest weekly decline since March, with the market bracing for the prospect of more Iranian crude flows as the nation inches closer to a revived nuclear deal. Gold was unchanged trading at $1,878/oz. Copper slipped 0.3% to $10,019 a tonne on the LME, down 2.1% on the week. "It's the potential risk of Chinese authorities clamping down on prices that seems to be the catalyst for the turnaround this week," said Ole Hansen, head of commodity strategy at Saxo Bank in Copenhagen. "The turnaround you could argue was overdue. The market had almost gone vertical during the past month and so we seem to be entering a consolidation phase right now." Hansen said a further leg of the correction could take LME copper down to about $9,600 a tonne.

Aluminium gained 1.3% to $2,428 a tonne as a consultancy forecast that almost 1 million tonnes of smelting capacity in drought-hit Yunnan province in southwest China could be shut temporarily owing to restrictions on electricity supply.

To the day ahead now, and the main highlight will be the release of the aforementioned flash PMIs from Europe and the US. Other releases include UK retail sales for April, US existing home sales for April, and the Euro Area’s advance consumer confidence reading for May. From central banks, we’ll hear from ECB President Lagarde, and the Fed’s Kaplan, Bostic, Barkin and Daly. There’s also an earnings release from Deere & Company.

Market Snapshot

- S&P 500 futures up 0.24% to 4,164.00

- STOXX Europe 600 +0.27% to 443.10

- German 10Y yield fell 1.4 bps to -0.122%

- Euro little changed at $1.2224

- MXAP up 0.3% to 204.49

- MXAPJ up 0.2% to 684.44

- Nikkei up 0.8% to 28,317.83

- Topix up 0.5% to 1,904.69

- Hang Seng Index little changed at 28,458.44

- Shanghai Composite down 0.6% to 3,486.56

- Sensex up 1.4% to 50,270.60

- Australia S&P/ASX 200 up 0.2% to 7,030.26

- Kospi down 0.2% to 3,156.42

- Brent Futures down 0.6% to $65.50/bbl

- Gold spot little changed at $1,877.20

- U.S. Dollar Index little changed at 89.747

Top Overnight News from Bloomberg

- One-day swings of 31%. A slump amid a jump in U.S. inflation. Ever more critical regulatory scrutiny. Bitcoin delivered all of these in the past few days, undermining its claimed role as a portfolio hedge rivaling gold

- Japan’s key inflation indicator showed prices falling for a ninth straight month in April in stark contrast with some other developed nations and supporting the view that the Bank of Japan will keep its stimulus in place for the foreseeable future

- Brent oil was heading for the biggest weekly decline since March, with the market bracing for the prospect of more Iranian crude flows as the nation inches closer to a revived nuclear deal

- The U.S. called for a global minimum corporate tax of at least 15%, less than the 21% rate it has proposed for the overseas earnings of U.S. businesses -- a level that some nations had argued was excessive

- Demand at a key Federal Reserve facility used to control short-term rates surged Thursday to the highest in more than four years, accommodating a barrage of cash in search of a home

- The number of U.K. cases of a worrying coronavirus variant from India more than doubled for a second week as authorities also monitor a new mutation of the virus, adding fresh doubt to U.K. plans to fully unlock the economy

- Japan’s second-largest pension fund said it expects to post the best returns since 2001 on the back of the global equity market’s rally and is looking to expand sustainable investing

- Canadian officials escalated efforts to cool the nation’s booming housing market, moving ahead with tighter mortgage qualification rules after the central bank issued a fresh warning against buyers taking on too much debt.

- The U.S. called for a global minimum corporate tax of at least 15%, less than the 21% rate it has proposed for the overseas earnings of U.S. businesses

A quick look at global markets courtesy of Newsquawk

Asian equity markets were mixed after failing to sustain the early momentum from the constructive mood on Wall Street, where all major indices finished higher amid a tech-led rebound and as concerns regarding future Fed taper discussions abated. ASX 200 (+0.2%) was initially lifted by outperformance in tech but then faltered due to weakness in the commodity-related sectors, in particular energy names, amid prospects of a return of Iranian oil supply following yesterday's comments from Iranian President Rouhani who suggested an agreement was reached in Vienna for world powers to lift all major sanctions although they are still discussing the final details. Nikkei 225 (+0.8%) took impetus from its US counterparts but with gains capped after soft CPI data and mixed COVID-related headlines including reports that Japan is said to be mulling extending the virus state of emergency in Tokyo and Osaka. Furthermore, Japan approved the Moderna and AstraZeneca COVID-19 vaccines today but may wait before administering the AstraZeneca vaccines due to blood clot concerns. Hang Seng (Unch.) and Shanghai Comp. (-0.6%) gave back early gains with underperformance in the mainland amid China’s ongoing frictions including with the EU after the latter voted to freeze its investment deal with China until Beijing lifts sanctions on EU officials, while MSCI also stated that it is to delete four more securities from the MSCI China All Shares Indexes at the close on June 9th if it doesn't receive OFAC guidance. Finally, 10yr JGBs eventually eked marginal gains as the risk momentum in Asia petered out although gains were limited with price action confined to within this week’s tight range of around 11 ticks and following mixed results at 20yr JGB auction.

Top Asian News

- RBI Eases India Government Finances With $14 Billion Payout

- India Central Bank to Transfer INR991.2B Surplus to Government

- China Resources Said to Consider $2 Billion Supermarket IPO

- North Korea Strategy Tops Agenda at Biden-Moon Summit Friday

Major bourses in Europe are mostly modestly higher but off best levels (Euro Stoxx 50 +0.4%) following a lukewarm cash open and as Flash PMIs painted a mixed picture. Key themes for the releases were price pressures emanating from demand outpacing supply, with the latter also hindered by shortages. US equity futures meanwhile consolidate with broad-based gains in early European hours following yesterday’s rebound. Back to Europe, the non-Euro bourses lag peers, with the FTSE 100 (Unch) the underperformer as a decline in yields, lower oil, a pull-back in base metals and a firmer Sterling prove to be headwinds for the index, although strong retail sales and PMIs have cushioned the downside. Sectors in Europe are mostly in the green aside from financials amid the lower yield environment, whilst Autos reside as the current winner with BMW (+0.8%) providing positive vibes for the sector after guiding a positive impact of around EUR 1bln as it expects the European Commission to significantly reduce its antitrust allegations against the Co. All-in-all it is difficult to discern a particular theme from a sectoral standpoint. In terms of some individual movers, Richemont (+4.7%) is firmer post earnings after topping forecasts and declaring a dividend. Meanwhile, Lufthansa (-6%) is the Stoxx 600 laggard after its second-largest shareholder KB Holding (12% stake), is reportedly looking to offload over half of its stake at a discount.

Top European News

- Wealth Fund That Quadrupled Profit Now Pivots With Bet on Europe

- BlueBay Sees ‘Incredible Value’ in Europe’s Riskiest Bank Bonds

- UniCredit to Skip Legacy Bond Coupon Payment Due Next Week

- Euro-Area Recovery Boosted by Services as Industry Loses Steam

In FX, the Buck remains fundamentally, technically and even psychologically weak as the DXY languishes below 90.000, but the index is trying resist another bout of selling pressure that could yet culminate in further depreciation given bearish external factors. The DXY just slipped to a marginal new cycle low at 89.646 vs 89.686 on Wednesday and 89.689 the day before having weathered an earlier attack when the Pound got a belated boost via significantly stronger than expected UK retail sales data and the Euro from really flash French PMIs, though both short-lived at the time. Meanwhile, another lacklustre session for APAC bourses overnight has left the likes of the Yen and Franc with an underlying safe-haven bid to the detriment of the Greenback against the backdrop of firmer bonds and flatter curves ahead of the US Markit PMIs, existing home sales and yet more Fed speak from hawk Kaplan no less than 4 times, plus Barkin and Daly.

- AUD/NZD/CAD - Not quite all change again, but another swing in the pendulum as the Aussie, Kiwi and Loonie hand back gains vs their US counterpart following firm rebounds yesterday. Aud/Usd is pivoting 0.7750 again with the latest downturn in base metal and other commodity prices overshadowing a decent retail sales beat, while Nzd/Usd has retreated through 0.7200 regardless of a pick-up in NZ credit card spending and Usd/Cad is hovering above 1.2050 in advance of Canadian retail sales.

- GBP/JPY/CHF/EUR - Sterling has benefited from a 2nd wind regardless of mixed UK PMIs, or perhaps on reflection of the marked acceleration in manufacturing activity to retest resistance above 1.4200 and circa 0.8600 against the Dollar and Euro respectively. Similarly, the Yen is having another look at offers into an effective twin top vs its US rival (108.57 and 108.56 from this Wednesday and last Wednesday respectively) standing in the way of 108.50, but could be stymied by decent option expiry interest between 108.60-45 in 1.2 bn). Elsewhere, the Franc is nestling just shy of 0.8950 and fresh multi-month peaks in wake of a sharp rebound in Swiss ip, while the Euro is still striving to establish a solid platform on the 1.2200 handle following the aforementioned eye-catching French PMIs vs somewhat contrasting German prelim prints compared to consensus and all round beats in the pan Eurozone readings. However, Eur/Usd may also be capped or held back by option expiries into the NY cut given 1.3 bn rolling off at the 1.2200 strike.

In commodities, WTI and Brent front-month futures were initially choppy within USD 1.5/bbl ranges following the prior day’s declines, induced by the simmering down in geopolitical tensions on a couple of fronts. Firstly, Iranian nuclear deal discussions are seemingly nearing an accord whereby the US has reportedly agreed to lift several sanctions against Iran, including restrictions on oil exports. Sources via EnergyIntel suggest that Iran is preparing to hike oil exports to maximum capacity in the upcoming months – in-fitting with reports over the week. According to reports citing the Iranian National Oil Co, the most optimistic scenario suggests that Iran could ramp up production to almost 4mln BPD in three months. Talks are to resume next week, with a possible official announcement also on the cards. “While any announcement confirming the lifting of sanctions would likely hit sentiment further, we believe that this will be short-lived, given that the supply and demand balance remains supportive,” ING said. OPEC+ members will also have to consider any deal when tweaking output quotas as Iran, Venezuela, and Libya is currently exempt from the output restrictions – with the group also poised to meet at the start of June. ING believes that the oil market can handle Iranian oil alongside OPEC+ supply, "We are assuming that Iranian supply returns to 3mln BPD by 4Q21". Sticking with geopolitics, Israel and Hamas have announced a ceasefire mediated by Egypt, whilst offshore platforms in the vicinity are restarting operations as a result. However, source reports earlier in the week suggested that there are concerns that another militant group might provoke the situation even after the two sides agree to a ceasefire in principle. WTI resides just under USD 63/bbl (vs low USD 61.56/bbl), and Brent trades sub-USD 66/bbl (vs low 64.57/bbl). Elsewhere, precious metals have been mirroring Dollar action and have remained within overnight ranges, with spot gold on either side of USD 1,875/oz and spot silver around USD 27.75/bbl. Over to base metals, Chinese iron and coke futures bore the brunt of the losses overnight in a continued move sparked by the Chinese Cabinet’s verbal intervention earlier this week. LME copper is also on the decline and has dipped back below USD 10,000/t as China’s crackdown on price manipulation seeps into LME.

US Event Calendar

- 9:45am: May Markit US Services PMI, est. 64.4, prior 64.7

- 9:45am: May Markit US Manufacturing PMI, est. 60.2, prior 60.5

- 9:45am: May Markit US Composite PMI, prior 63.5

- 10am: April Existing Home Sales MoM, est. 1.0%, prior -3.7%

- 12:15pm: Fed’s Kaplan, Bostic and Barkin Speak at Technology Conference

- 1:30pm: Fed’s Daly Speaks on Wage Dynamics

DB's Jim Ried concludes the overnight wrap

Well after 14 months I’m going to London this morning for the first time since WFH was instigated. Not to the office though but to have an injection in my knee in an attempt to delay microfracture surgery until the end of the golf season. Had you told me back in January 2020 that by May 2021 that I wouldn’t have been in London for 14 months I would have been very concerned about the mortgage payments and I certainly wouldn’t be about to embark on a fresh (but last ever) building works. As an interesting anecdote, we’re finding that it’s a real struggle to get basic building material in the UK at the moment. There is a huge building boom coupled with a global shortage of raw materials. Even basic items like breeze blocks are on a long lead time. We haven’t yet pulled the trigger and it’s tempting to leave it 6-12 months to allow things to calm down.

Such bottlenecks will certainly continue to be the main speed limiters on growth over the next few months as economies increasingly reopen. We’ll get the latest news on the global recovery today with the flash PMIs for May. The April readings were pretty strong on both sides of the Atlantic, with the Euro Area composite PMI at 53.8, the highest since July, while the US composite PMI was the highest on record at 63.5. Expectations going into today have the Euro Area composite PMI climbing to 55.1, with the UK, Germany and France all seeing roughly 2pt increases from last month. On the other hand, the US services and manufacturing PMIs are expected to fall back 0.3pts and 0.4pts to 64.4 and 60.2 respectively. A reminder that our equity strategist is watching carefully for the sign that the ISM is trending back down in the US as that’s his signal for a 6-10% summer correction. The flash PMI number today will give us a few clues on this growth momentum.

Overnight we’ve already seen the PMI readings out of Japan, which actually showed the composite PMI falling to 48.1, down from 51.0 last month and beneath the 50-mark that separates expansion from contraction. Services (45.7) fared worse than manufacturing (52.5), reflecting the recent surge in Covid-19 cases and the extension of restrictions across more regions to deal with that. Australia had a much better performance however, with their composite PMI coming in at 58.1 (vs. 58.9 last month), marking the 9th consecutive month of expansion.

Elsewhere overnight, equity markets have had another mixed performance, with the Nikkei advancing +0.62%, whereas the Hang Seng (-0.30%), the Shanghai Comp (-0.84%) and the KOSPI (-0.29%) have all moved lower. However, the main news is that a ceasefire came into effect 2am local time between Israel and Hamas, bringing an end to the 11-day conflict there that’s seen the worst fighting there since 2014. Meanwhile in the US, S&P 500 futures are pointing +0.09% higher.

These moves follow what was a decent recovery for markets yesterday after a fairly poor start to the week. The S&P 500 (+1.06%) and the MSCI World Index (+1.07%) both advanced after a run of 3 successive declines, helped by decent US jobs data and an improving picture on the pandemic. But to be honest, we can’t help but feel a sense of déjà vu here, as last week both indices saw the same pattern of losses on Monday, Tuesday and Wednesday, before rising again on Thursday and Friday. So if we get another day in the green today we’ll know this is Groundhog Week. Time to get that great Bill Murray film out again.

As mentioned, the mood was helped by positive US data that showed initial jobless claims for the week through May 15 falling to a post-pandemic low of 444k (vs. 450k expected). So a sign of continued improvement in the labour market following last month’s distinctly underwhelming jobs report, and raising hopes that the April report will hopefully prove a blip rather than a trend. Furthermore, Treasury yields fell back and investors marginally downgraded the pace of Fed hikes over the coming years, which helped tech stocks in particular as the NASDAQ (+1.77%) and the FANG+ (+2.38%) outpaced the broader market. Recent cyclical winners were weaker as the drop in yields saw US banks (-0.40%) lag. European equities similarly bounced back strongly with the STOXX 600 up +1.27%, though energy stocks had a weaker performance on both sides of the Atlantic. This was against the backdrop of a 3rd consecutive decline in oil prices that saw Brent crude (-2.33%) and WTI (-2.07%) lose further ground, thanks to Iranian President Rouhani saying that a broad outline had been reached to end oil sanctions. That said, it wasn’t all bad news for commodities, with gold prices up another +0.41% to a 4-month high.

Another asset class that bounced back yesterday was cryptocurrencies, with Bitcoin recovering +4.55% yesterday to move back above $40,000, even if this still left it well beneath its level a week ago. The moves were seen across the sphere of crypto assets, with Ethereum (+9.27%), XRP (+5.51%) and Litecoin (+4.52%) all managing to claw back some of the previous day’s losses. The recovery in cryptocurrencies took a slight hit midday in the US, when the Treasury Department announced that the Biden administration is proposing to improve tax compliance in the nascent market by requiring businesses that “receive cryptoassets with a fair-market value of more than $10,000” to “...be reported on.” This matches the current requirement for dollar transactions. The news caused an -8% drawdown for bitcoin intraday before it regained the majority of those losses by the end of the day. Ahead of the Treasury announcement, Marion Laboure on my team published a note on the issue yesterday, called “Trendy is the Last Stage Before Tacky”, in which she points out that throughout history, governments have not been inclined to give up their monetary monopolies, and as cryptocurrencies begin to seriously compete with regular currencies, regulators and policymakers will crack down. You can read her note here.

In sovereign bond markets yesterday, yields on 10yr US Treasuries fell back -4.6bps to 1.625%, which was actually (and surprisingly) the biggest one-day decline in yields for a month. The drop was driven by inflation expectations as the 10yr breakeven fell (-4.3bps) for a 3rd straight day, having lost -11.4bps over that period – the largest three day drop since early-September 2020. The drop comes after the 10yr breakeven rate hit 8-year highs on Monday. For Europe it was a more divergent picture between core and periphery however, with 10yr bund yields up +0.1bps, whereas southern European countries including Italy (-6.0bps), Greece (-5.9bps) and Spain (-3.6bps) saw reasonable declines.

In terms of the pandemic, a Japanese government panel approved the use of the Moderna and AstraZeneca vaccines, with the two joining the Pfizer/BioNTech vaccine that’s already been approved there. However, it was reported by NTV that the government was also considering an extension of the state of emergency beyond May 31 in areas including Tokyo and Osaka. Separately, Bloomberg reported that the G7 countries would discuss an international system of recognising vaccination certificates, which would help the resumption of global travel again. G7 health ministers are due to meet at Oxford University on 3-4 June, before the leaders gather in Cornwall from 11-13 June. This comes following news late yesterday that EU negotiators have agreed to a plan that would allow travellers to get out of quarantine procedures if they show proof of vaccination. The member states still have to have a formal vote on the plan, which is expected to allow similar guidance for vaccinated visitors from non-EU nations. Lastly, Moderna started to export vaccine doses out of the US, with domestic demand waning. Even so, various US states, including New York and Maryland, have introduced lottery tickets as incentives to getting shots in an effort to increase overall vaccine uptake.

There wasn’t a great deal of other data yesterday, though German producer prices were up by +5.2% year-on-year in April (vs. +5.1% expected), which marked the fastest pace of growth in nearly a decade. Otherwise the Conference Board’s leading economic index in the US was up +1.6% (vs. +1.3% expected).

To the day ahead now, and the main highlight will be the release of the aforementioned flash PMIs from Europe and the US. Other releases include UK retail sales for April, US existing home sales for April, and the Euro Area’s advance consumer confidence reading for May. From central banks, we’ll hear from ECB President Lagarde, and the Fed’s Kaplan, Bostic, Barkin and Daly. There’s also an earnings release from Deere & Company.

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentSpread & Containment

Another beloved brewery files Chapter 11 bankruptcy

The beer industry has been devastated by covid, changing tastes, and maybe fallout from the Bud Light scandal.

Share this:

{kind=link}

{kind=link}

Before the covid pandemic, craft beer was having a moment. Most cities had multiple breweries and taprooms with some having so many that people put together the brewery version of a pub crawl.

It was a period where beer snobbery ruled the day and it was not uncommon to hear bar patrons discuss the makeup of the beer the beer they were drinking. This boom period always seemed destined for failure, or at least a retraction as many markets seemed to have more craft breweries than they could support.

Related: Fast-food chain closes more stores after Chapter 11 bankruptcy

The pandemic, however, hastened that downfall. Many of these local and regional craft breweries counted on in-person sales to drive their business.

And while many had local and regional distribution, selling through a third party comes with much lower margins. Direct sales drove their business and the pandemic forced many breweries to shut down their taprooms during the period where social distancing rules were in effect.

During those months the breweries still had rent and employees to pay while little money was coming in. That led to a number of popular beermakers including San Francisco's nationally-known Anchor Brewing as well as many regional favorites including Chicago’s Metropolitan Brewing, New Jersey’s Flying Fish, Denver’s Joyride Brewing, Tampa’s Zydeco Brew Werks, and Cleveland’s Terrestrial Brewing filing bankruptcy.

Some of these brands hope to survive, but others, including Anchor Brewing, fell into Chapter 7 liquidation. Now, another domino has fallen as a popular regional brewery has filed for Chapter 11 bankruptcy protection.

Image source: Shutterstock

Covid is not the only reason for brewery bankruptcies

While covid deserves some of the blame for brewery failures, it's not the only reason why so many have filed for bankruptcy protection. Overall beer sales have fallen driven by younger people embracing non-alcoholic cocktails, and the rise in popularity of non-beer alcoholic offerings,

Beer sales have fallen to their lowest levels since 1999 and some industry analysts

"Sales declined by more than 5% in the first nine months of the year, dragged down not only by the backlash and boycotts against Anheuser-Busch-owned Bud Light but the changing habits of younger drinkers," according to data from Beer Marketer’s Insights published by the New York Post.

Bud Light parent Anheuser Busch InBev (BUD) faced massive boycotts after it partnered with transgender social media influencer Dylan Mulvaney. It was a very small partnership but it led to a right-wing backlash spurred on by Kid Rock, who posted a video on social media where he chastised the company before shooting up cases of Bud Light with an automatic weapon.

Another brewery files Chapter 11 bankruptcy

Gizmo Brew Works, which does business under the name Roth Brewing Company LLC, filed for Chapter 11 bankruptcy protection on March 8. In its filing, the company checked the box that indicates that its debts are less than $7.5 million and it chooses to proceed under Subchapter V of Chapter 11.

"Both small business and subchapter V cases are treated differently than a traditional chapter 11 case primarily due to accelerated deadlines and the speed with which the plan is confirmed," USCourts.gov explained.

Roth Brewing/Gizmo Brew Works shared that it has 50-99 creditors and assets $100,000 and $500,000. The filing noted that the company does expect to have funds available for unsecured creditors.

The popular brewery operates three taprooms and sells its beer to go at those locations.

"Join us at Gizmo Brew Works Craft Brewery and Taprooms located in Raleigh, Durham, and Chapel Hill, North Carolina. Find us for entertainment, live music, food trucks, beer specials, and most importantly, great-tasting craft beer by Gizmo Brew Works," the company shared on its website.

The company estimates that it has between $1 and $10 million in liabilities (a broad range as the bankruptcy form does not provide a space to be more specific).

Gizmo Brew Works/Roth Brewing did not share a reorganization or funding plan in its bankruptcy filing. An email request for comment sent through the company's contact page was not immediately returned.

bankruptcy pandemic social distancing

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Wendy’s has a new deal for daylight savings time haters

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Catastrophic Risk: Investing and Business Implications

When Military Rule Supplants Democracy

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Wealth Inequality by Age in the Post‑Pandemic Era

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges