Futures, Global Markets Tumble As Central Bankers Plan To Push World Into Coordinated Recession

Futures, Global Markets Tumble As Central Bankers Plan To Push World Into Coordinated Recession

Market sentiment has only deteriorated after…

Share this:

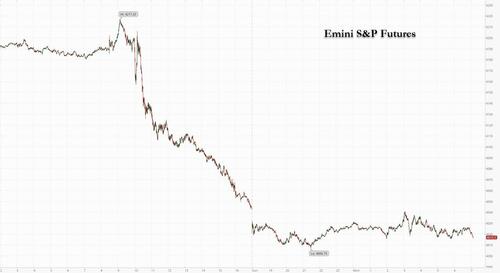

Market sentiment has only deteriorated after Friday's sharp post-Powell/ECB dump, and investors started the week with the bear market rally in tatters after the world’s biggest central banks huddled around a simple message in Jackson Hole this weekend: they are ready to fight runaway inflation with higher interest rates, even if it does some damage (in other words they want to crush demand, even as Biden's debt relief plan and Inflation Reduction Plan hopes to stimulate demand). Powell quashed the idea of an early dovish Fed pivot (ensuring a much more forceful one later once all EMs fully blow up on the back of the soaring USD) and also said on Friday that the road ahead will “bring some pain to households and businesses” in the US, an “unfortunate cost of bringing down inflation” while ECB's Isabel Schnabel said she and her colleagues had “little choice” but to continue tightening even if Europe’s economy tips into recession, which is becoming increasingly likely. As expected, Senator Liz Warren said she was worried the central bank will tilt the US economy into a recession, but for now Biden still thinks that soaring inflation polls worse than recession and/or global depression.

In any case, Powell’s signal of higher-for-longer interest rates rocked market on Friday and then followed through in Asia and Europe on Monday, sinking stocks and equity futures. S&P 500 futures slipped 1% as of 715 a.m. New York time, while Nasdaq futures tumbled 1.3%, as swaps traders boosted their expectation for where the Fed rate will be a year from now to 3.82%, from 3.68% a week ago.

Some more dismal data: the S&P 500 just posted its worst week since July and virtually all members tumbled Friday. Major indexes dipped below their 100-day price averages, which could indicate the potential for more losses. And the one-month percentage price change for all major indexes is negative. As Bloomberg puts it, the message is clear: interest rates will stay higher for some time, reducing the possibility of a soft landing.

Amid the rate back-up, 2Y Treasury yields rose to the highest since 2007, stopping just shy of 3.50%...

... as Bonds in Europe also tumbled with Germany’s 10-year yield rising above 1.5% after a string of European Central Bank officials also stressed over the weekend the need to act more forcefully to quash record inflation, effectively assuring that Europe will be pushed into recession or worse. The Bloomberg Dollar Spot Index pushed toward the record hit last month as investors sought a haven from spiking volatility. Commodity-linked currencies as well as the yen, the pound and the offshore yuan were under pressure. Bitcoin broke below the $20,000 level some view as a marker of a deeper slide in investor sentiment. Gold retreated, but oil made gains on supply risks.

In premarket trading, markets are honing in on the possibility of an economic slowdown: cyclical companies such as Freeport McMoran, Dow, Nucor and Ford are among the bigger decliners while shares of major US technology and internet stocks such as Tesla and Amazon.com also sharply lower with the group on track to extend a sharp selloff from Friday. Apple and Amazon each fall 1.3%, Nvidia 1.2%, Meta Platforms -1.1%, Microsoft -1%, Alphabet -1%.

- Cryptocurrency-exposed stocks may be active on Monday after Bitcoin extended its drop below $20,000 as part of a wider market retreat, amid concern about the Federal Reserve’s rate- hike path. Keep an eye on Marathon Digital (MARA US), MicroStrategy (MSTR US), Coinbase (COIN US), Bit Digital (BTBT US), Ebang (EBON US), Riot Blockchain (RIOT US), and Silvergate Capital (SI US)

- VBI Vaccines (VBIV US) is down 9.7% in US premarket trading after entering into a sales agreement for possible offering of up to $125 million in shares from time to time via Jefferies on Friday.

- Watch Walmart (WMT US) stock as the retailer proposed to buy all of the shares in its South African unit Massmart it doesn’t already own for 62 rand apiece, a 53% premium to the last closing price.

- Minerva Neurosciences (NERV US) shares rise 2.6% in US premarket trading after gaining more than 150% last week as it applied to the FDA for approval of its schizophrenia drug candidate and Point72 Asset Management disclosed an 8.8% passive stake in the stock.

“We maintain our view that the Fed will raise rates by another 100 basis points by year-end, with risks for more if inflation does not slow in line with our forecasts,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “With rates likely to stay higher for longer, our base case is for further volatility, earnings downgrades, and higher-than-expected default rates over the course of the next year.”

European equities also tumbled on Monday, adding to last week’s selloff amid concerns about the economic impact from further central bank tightening, which officials embraced in Jackson Hole. The Stoxx Europe 600 slid 1.2% with technology stocks underperforming as bond yields rose. Utilities also fell after comments from French Prime Minister Elisabeth Borne over the weekend heightened unease that a windfall tax could be imposed on “super profits.” UK markets were shut for a holiday. The benchmark has slumped to the lowest since July 21, breaking below its 50-day moving average, as worries about a downturn intensified after central bank officials said they are ready to follow through with higher interest rates, even if it does some damage. The region already faces a flurry of other headwinds, such as the prospects of gas rationing and political turmoil in Italy and the UK. Here are some of the biggest European movers today:

- Utilities are among the worst performing sub-sectors in Europe after comments from French Prime Minister Elisabeth Borne over the weekend heightened windfall tax concerns on “super profits”

- Technology stocks underperform all other sectors in the Stoxx 600 after central bank officials signaled they’re ready to follow through with higher interest rates, and as bond yields rose

- Bavarian Nordic falls as much as 15% after White House monkeypox coordinator Robert Fenton said after market close on Friday that the US has nearly all the monkeypox vaccines it needs

- Cryptocurrency-exposed stocks suffer on Monday after Bitcoin extended its drop below $20,000 as part of a wider market retreat, amid concern about the Federal Reserve’s rate- hike path

- BW LPG shares fall as much as 13.2% after the Norwegian LPG published 2Q results. Analysts note a soft report with a miss on adjusted Ebitda, and some exposure to prices on the 3Q spot market

- SAS shares slide as much as 17% after DNB cut its PT for the ailing Scandinavian airliner to SEK0.05 from SEK0.10, seeing “significant dilution” on the back of its Chapter 11 proceedings

Tech firms led losses for Asian equities, while progress in the US-China delisting spat helped to cushion Chinese stocks. Emerging-market stocks dropped and a gauge of major developing-nation currencies slumped by the most in more than two months.

In FX, the Bloomberg Dollar Spot Index rose to six-week high as the greenback advanced versus all of its Group-of-10 peers, and pushed toward the record hit last month as investors sought a haven from spiking volatility. The euro fell a second day but remained in its recent $0.99-1.00 range. The euro is trading close to its cycle lows, yet options show that bearish sentiment for the common currency is becoming steadily lower. The yen tumbled as much as 1% back toward the 140 per dollar level as the impact of hawkish Federal Reserve comments at Jackson Hole weighed on Japan’s currency. Signs from the option market suggested a renewed bias toward yen weakness on the part of asset managers, who boosted their net-short position by the most on record in the week to Aug. 23. Australia’s dollar fell for a second day as momentum accounts price in a more hawkish Fed after Jerome Powell’s speech at Jackson Hole. Sovereign bonds declined. Australian retailers powered further ahead in July, suggesting cashed-up households are coping well with rapid interest-rate increases. The yuan weakened to fresh two-year lows after Powell signaled higher-for-longer interest rates, prompting China’s central bank to set a stronger-than-expected fixing to cap the currency’s drop. South Korea’s won led declines, falling 1.4%, while the Thai baht slipped 1%. “The market has not been hawkish enough on the Fed’s path,” says Stephen Chiu, chief Asia FX & rates strategist at Bloomberg Intelligence in Hong Kong. “Last week’s deluge of Fed speakers including Powell basically told the market to retune their view. But we believe still not enough hawkishness is priced in. So the dollar may continue to rise versus Asian currencies.” Bank of Korea Governor Rhee Chang-yong said he would join the Fed in focusing on inflation if prices remain out of control, keeping the door open for another outsized rate hike

In rates, Treasuries remained under pressure but are off the cheapest levels of the session; the US 2-Year yield, sensitive to expectations around Fed policy, hit 3.47% in Asian trading, the highest since the global financial crisis. The 10-year yield climbed to about 3.10%. UK markets are closed for bank holiday. US yields higher by 4bp-8bp, 10-year by ~6bp at 3.10%, with most euro-zone 10-year yields higher on the day by at least 9bp. 2-year rose as much as 8.4bp to 3.48%, highest since 2007, exceeding its June 14 high by about 3bp. In early US trading, swaps referencing Fed meeting dates once again give higher than 50% odds to another 75bp rate hike at September meeting. European bonds lead the selloff following hawkish rhetoric from ECB officials over the weekend. while paring odds of rate cuts in 2023. IG credit issuance remains moribund, with lull expected to last through US Labor Day holiday Sept. 6.

Bitcoin tumbled below $20,000 amid broader tightening fears; in addition, Reuters reported that the Monetary Authority of Singapore is considering further measures to reduce the harm to consumers from cryptocurrency trading and MAS will issue public consultation on new measures by October.

In commodities, gold retreated, but oil made gains on supply risks. WTI and Brent contracts have been choppy on the first trading day of the week; gains are capped by risk aversion. Spot gold remains pressured under its 21 DMA (1,766/oz), 50 DMA (1,763/oz) and 10 DMA (1,749/oz). Copper declined in APAC hours, whilst the LME is closed today due to the UK bank holiday. Meanwhile, European natural gas prices plunged the most since March after Germany said its gas stores are filling up faster than planned ahead of winter.

It's a quiet start to the week, with just the Dallas Fed report due at 10:30am.

Market Snapshot

- S&P 500 futures down 0.8% to 4,025.25

- STOXX Europe 600 down 1.0% to 421.91

- MXAP down 2.2% to 157.01

- MXAPJ down 1.9% to 515.30

- Nikkei down 2.7% to 27,878.96

- Topix down 1.8% to 1,944.10

- Hang Seng Index down 0.7% to 20,023.22

- Shanghai Composite up 0.1% to 3,240.73

- Sensex down 1.2% to 58,132.18

- Australia S&P/ASX 200 down 2.0% to 6,965.49

- Kospi down 2.2% to 2,426.89

- German 10Y yield lup 13 bps to 1.52%

- Euro down 0.4% to $0.9924

- Brent futures up 0.2% to $101.24/bbl

- Gold spot down 0.9% to $1,721.81

- US Dollar Index up 0.53% to 109.38

Top Overnight News from Bloomberg

- Top officials from the world’s biggest central banks coalesced around a simple message in Jackson Hole this weekend: They are ready to follow through with higher interest rates, even if it does some damage

- Federal Reserve Chair Jerome Powell’s stern message at Jackson Hole has made it clear for Bank of Japan Governor Haruhiko Kuroda that the weaker yen, a major source of concern for Japan’s economy, won’t be going away anytime soon

- The ECB is prepared to at least repeat the half-point increase in interest rates it delivered last month, with an even bigger move not to be excluded as inflation nears yet another record. That’s the message from ECB officials who joined the Federal Reserve’s annual Jackson Hole symposium, which wrapped up Saturday

- The rally that’s bolstered risk assets over the past month was just a blip in a bear market that’s likely to worsen from here. That’s the view of investors who seem to be finally getting the message that a resolutely hawkish Federal Reserve and central bank peers are planning to raise interest-rates at all costs to combat the hottest inflation in a generation

- German Power for next year, the European benchmark, broke through 1,000 euros ($993) for the first time as the region’s energy crisis intensifies

- Poland’s central bank may end or at least pause its series of interest-rate increases as early as the next week’s policy meeting, Governor Adam Glapinski said, adding that a turning point is near

- The Swedish Debt Office has decided to wind up a strategic position in the Swedish krona against the euro as “major changes” have occurred in the global economy, which has altered the conditions for the position in terms of cost and risk

- Swedish housing prices will continue falling until the middle of next year as the share of household income that goes toward mortgage interest payments is set to double, economists at the Nordic region’s largest bank said in a new forecast

- China is enforcing lockdown restrictions in areas around Beijing more intensively, and will mass test the nearby port city of Tianjin, stepping up its quest to wipe out Covid-19 ahead of a key meeting of the Communist Party’s top leaders

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks took their cue from Friday's sell-off on Wall St amid higher yields and following hawkish central bank rhetoric from Jackson Hole including from Fed Chair Powell. ASX 200 was pressured as underperformance in tech led the declines across all sectors and with better-than-expected Retail Sales doing little to brighten the mood. Nikkei 225 gapped beneath the 28K level and shed around 800 points despite a weaker currency and reports of a potential further easing of COVID restrictions. Hang Seng and Shanghai Comp declined at the open although losses in the mainland were stemmed after Sichuan resumed power to most industries and participants digested a deluge of earnings releases, while the US and China reached a preliminary agreement on audit inspections. Agricultural Bank of China (1288 HK) - H1 2022 (CNY): net profit 128.95bln vs. prev. Y/Y 122.3bln. Will support local government efforts to complete construction of properties.

Top Asian News

- Chinese authorities informed the US Department of Agriculture that Chinese customs will suspend meat imports transported by Tyson Fresh Meat (TSN) from Monday after its pig trotters failed inspection, according to Global Times.

- Huaqiangbei, China has been ordered to shut between Monday and Thursday to contain a new COVID outbreak, via SCMP.

- Moody's affirms China at A1, maintains Stable outlook. Driven by assessment that core strengths of the credit profile are likely to remain in the medium-term.

European bourses are under pressure amid the weekend's central bank hawkishness, Euro Stoxx 50 -1.5%; note, FTSE 100 away for a Bank Holiday. US futures are similarly subdued, ES -1.0%, in tandem with Europe as specific updates are somewhat limited ahead of a packed week of data. Qualcomm (QCOM) - USD 991mln fine against the Co. which was rejected by an EU court will not be appealed by EU antitrust regulator, according to Reuters sources

Top European News

- UK Tory leadership frontrunner Truss is reportedly mulling cutting the 20% VAT by 5% across the board to help ease the cost-of-living pressures under a nuclear option, while other options include a more modest 2.5% reduction, according to a source cited by The Telegraph. Furthermore, Truss is under renewed pressure to outline the cost-of-living support with Tory MPs voicing increasing concerns regarding the impact of higher energy prices on households and small businesses, according to FT.

- A senior economist warned that UK Foreign Secretary and Tory leadership front runner Truss's plan to cut tens of billions of pounds in VAT would crash public finances, according to The Times citing the Institute of Fiscal Studies Director.

- UK corner shops are calling for government support to offset energy costs and have warned that thousands risk going out of business if the government doesn’t provide support, according to FT.

- Goldman Sachs sees the UK economy entering a recession in Q4 and said the recession will be mild, while it lowered its 2022 GDP forecast to 3.5% from 3.7% and the 2023 GDP forecast to 0.6% from 1.1%.

- S&P affirmed Austria at AA+; Outlook revised to Stable from Positive.

Central Banks

- ECB’s Schnabel said both the likelihood and the cost of current high inflation becoming entrenched in expectations are uncomfortably high and said that central banks need to act forcefully in this environment, according to Reuters.

- ECB’s Villeroy said a significant rate increase is needed in September and that they should get rates to neutral by year-end with neutral somewhere between 1.00%-2.00%, according to Reuters.

- ECB’s Kazaks said the ECB should discuss 50bps and 75bps hikes in September and that a 50bps rate increase is the least the bank should do, while he added that Euro zone recession risk is substantial and a technical recession is likely, according to Reuters.

- ECB’s Rehn said its action time for the ECB with a weak Euro a key point and that a ‘significant’ hike in interest rates is needed in September, while he added it is too early to publicly discuss quantitative tightening, according to Bloomberg.

- SNB’s Jordan said there is no need to adjust the definition of price stability or broaden SNB’s mandate, while he added they are prepared to act decisively if price stability is at threat and that unconventional monetary policy instruments are likely to continue to have an important part to play in Switzerland, according to Reuters.

- BoJ Governor Kuroda reiterated the view regarding transitory inflation in Japan in which he stated they have 2.4% inflation but is almost wholly caused by rising international commodity and food prices, while they expect inflation to approach 2% or 3% by year-end but decelerate again to 1.5% next year.

- BoK Governor Rhee said it is premature to say inflation has peaked and that rates will increase until it is clear that inflation is falling. Rhee also commented they will intervene in FX markets if speculative forces are seen and that the KRW’s movement is in line with EUR and other major currencies, while he noted that a weakening KRW from the rally in USD is a bad factor for inflation and that BoK policy tightening is unlikely to end before the Fed, according to Reuters.

FX

- DXY printed a fresh YTD peak just shy of 109.50 overnight as APAC players reacted to the Jackson Hole Symposium, but the index then pulled back below 109.

- G10s are pressured to varying degrees but EUR/USD has been trimming losses though remains under parity as the DXY wanes.

- JPY is the clear laggard as the widening FOMC-BoJ pricing lifted USD/JPY to test 139.00 to the upside, ahead of the YTD peak at 139.39.

- The Yuan was in focus in APAC hours as USD/CNH topped 6.9000 before finding resistance around 6.9300.

Fixed Income

- EGBs slump following weekend Central Bank updates from ECB officials which follow on from and continue the tone of Friday's hawkish sources

- At worst, Bunds lower by over 200 ticks while USTs have stabilised somewhat near lows of 116.26+ with yield curves elevated but somewhat mixed directionally.

Commodities

- WTI and Brent contracts have been choppy on the first trading day of the week; gains are capped by risk aversion.

- Spot gold remains pressured under its 21 DMA (1,766/oz), 50 DMA (1,763/oz) and 10 DMA (1,749/oz).

- Copper declined in APAC hours, whilst the LME is closed today due to the UK bank holiday.

- Austrian Chancellor Nehammer called for an EU-wide cap on power prices and said they must decouple the price of electricity from the gas price and bring it closer to actual production costs, while he added that they must finally stop the madness that is occurring in energy markets and cannot let Russian President Putin determine the European power price, according to Reuters.

- US temporarily waived truck driver hours of service rules to transport fuel to Illinois, Indiana, Michigan and Wisconsin following the unanticipated shutdown of BP’s Whiting refinery, according to Reuters.

- Ukraine PM Shmyhal said Ukraine will permit merchant sailors to leave Ukraine if they receive approval from their local military administrative body, according to Reuters.

- UN Coordinator for the Black Sea Grain Initiative said Ukrainian silos are still stocked with millions of tonnes from previous harvests and that much more grains need to shift to provide room for the new harvest, according to Reuters.

US Event Calendar

- 10:30: Aug. Dallas Fed Manf. Activity, est. -12.7, prior -22.6

- 14:15: Fed’s Brainard speaks at a FedNow workshop

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Spread & Containment

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now…

Share this:

{kind=link}

{kind=link}

{kind=link}

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

{kind=link}

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Wendy’s has a new deal for daylight savings time haters

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Catastrophic Risk: Investing and Business Implications

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Mortgage rates fall as labor market normalizes

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

Walmart launches clever answer to Target’s new membership program

-

International2 days ago

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex