Spread & Containment

Futures Flat On Last Day Of Best Quarter In 22 Years

Futures Flat On Last Day Of Best Quarter In 22 Years

Share this:

There was some sound and fury in a very illiquid overnight session, which ended up signifying nothing, and futures were little changed from their Monday closing ramp as markets puts a close to the best quarter for stocks since 1998.

The MSCI world equity index was up about 0.1% in early trading after Asian shares rose on strong data from the U.S. housing market and Chinese factories. European shares continued the rally. S&P futures fluctuated and the dollar index strengthened to a one-month high amid concern that new virus infections could slow the pace of business re-openings.

Overnight sentiment fizzled after Australia's Victoria state said it would shutter 10 areas in the metropolis of Melbourne. Arizona also ordered a number of establishments including gyms to close for 30 days and New Jersey halted plans for indoor dining. However, this latest gloom was quickly forgotten shortly after Europe reopened and the magical overnight futures levitation kicked in right on schedule.

"Renewed shutdowns of economic activity would bring additional market volatility," said Kristina Hooper, the chief global market strategist at Invesco in New York. "But importantly, we do not expect the same draconian shut-down measures as seen earlier in the year."

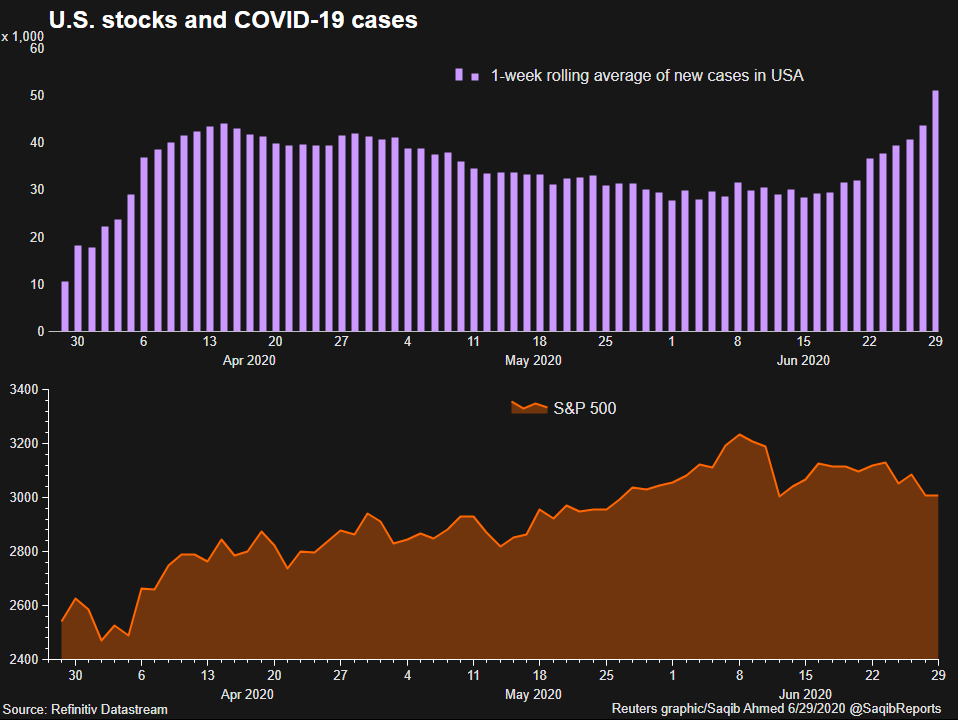

After new cases of the coronavirus trended lower in May, they climbed again in June, denting investors’ enthusiasm that the U.S. economy would recovery relatively quickly from the crisis. Investor enthusiasm had been driven in part by recent economic data that were better than expected.

A spike in virus infections in Southern and Western states last week spooked investors. Florida, Texas, California and Arizona, which were the top four states with the most new cases, account for nearly a third of U.S. economic output. California’s government on Sunday ordered bars in several counties to close due to the coronavirus rebound, while San Francisco put plans to reopen businesses on hold.

Los Angeles has become a new epicenter in the pandemic as coronavirus cases and hospitalizations surge there despite California Governor Gavin Newsom’s orders requiring bars to close and residents to wear masks in nearly all public spaces. The World Health Organization (WHO) will “read carefully” a Chinese study on a new flu virus found in pigs, a spokesman said, adding that the findings underscored the importance of influenza surveillance during the current pandemic.

“Asset markets are looking beyond COVID stats,” said Neil Jones, head of FX sales at Mizuho Bank. “There’s some expectation of containment and then, further down the line, an expectation of some form of measure to combat the virus.”

Anyway, back to markets, where Uber climbed in pre-market trading after reports that the company is in talks to buy Postmates as a consolation prize after it failed to acquire Grub Hub. Boeing, which idiotically surged yesterday on trials of the 737 MAX airplane which nobody will want to fly in, slipped after one of its biggest European customers scrapped its $10.6 billion purchase deal.

European shares edged up, with the Euro STOXX 600 up 0.1% in early trading having been relatively range-bound for the past two weeks. Germany’s DAX was up 0.3%. London’s FTSE 100 was down 0.6%. Britain’s economy shrank by the most since 1979 in early 2020 as households slashed their spending, according to official data that included the first few days of the lockdown. Annual inflation in the Euro area accelerated to 0.3% in June from a four-year low of 0.1% in May, beating forecasts for no change and supporting the European Central Bank’s expectation that a negative reading may be avoided.

Earlier in the session, Asian stocks gained, led by materials and communications, after falling in the last session. The Topix gained 0.6%, with EJ HD and DVX rising the most. The Shanghai Composite Index rose 0.8%, with Xinjiang Yilu Wanyuan Industrial Investment and Chengtun Mining posting the biggest advances. China’s parliament passed national security legislation for Hong Kong in response to last year’s pro-democracy protests. The United States, Britain and other Western governments have said the legislation erodes the autonomy the city was granted at its 1997 handover. Market reaction was limited.

While the latest stronger than expected Chinese PMI print added to reopening optimism...

... some investors are questioning the rally that has carried global stock benchmarks higher. The MSCI All Country World Index is up about 18% this quarter and just 10% below its February record high, the biggest advance in a decade. Yet the World Health Organization warned that the worst of the coronavirus pandemic is still to come. As a result, investors are parsing an array of factors that could weigh on stocks in the months ahead, including potential delays in reopening parts of the U.S. economy and sky-high stock valuations.

The S&P 500’s strongest quarterly performance since the fourth quarter of 1998 — during the dot-com boom — was driven by gains in April and May, followed by an overall flat June after Wall Street gave back gains in the second half of the month.

In FX, the dollar advanced against all its Group-of-10 peers amid quarter-end positioning and as investors tracked a resurgence in coronavirus infections. The dollar got a boost while the Aussie swung to a loss as the Australia’s second-most populous state imposed a lockdown in some areas for four weeks, while also diverting flights for a shorter period; other risk-sensitive currencies reacted in a similar fashion.

“I would expect overall dollar demand to continue as we go into July,” Mizuho’s Neil Jones said. “If there’s a summer lull then we may see a dollar sell-off into the elections but as we run up to the end of the year I would expect to see a resurgence of dollar demand,” he added.

The euro was down around 0.3% against the dollar, at $1.1208, while the Australian and New Zealand dollars also edged down. The Australian and New Zealand dollars are set to end the best quarter against the greenback since the financial crisis; Sweden’s krona and Norway’s krone are heading for their best quarter against the euro in a decade or more.

In rates, Treasuries were steady ahead of a slew of Fed speakers. European peripheral spreads widened as Bunds popped through Monday’s best levels, however Italian bonds advanced as a sale of 10-year debt saw the highest oversubscription rate since 2012. Copper rose above $6,000 a ton for the first time since January.

In commodities, oil prices slipped as traders took profits after sharp gains the previous session and Libya’s state oil company flagged progress in talks to resume exports, potentially boosting supply. Prices then recovered partially. WTI was down 0.6% at $39.15 a barrel, having hit as low as $39.00, while Brent crude slipped 0.6% to $41.16 per barrel.

Looking at today's calendar, expected data include Chicago PMI. FedEx reports earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 3,045.75

- STOXX Europe 600 down 0.3% to 358.75

- MXAP up 0.7% to 157.99

- MXAPJ up 0.7% to 513.21

- Nikkei up 1.3% to 22,288.14

- Topix up 0.6% to 1,558.77

- Hang Seng Index up 0.5% to 24,427.19

- Shanghai Composite up 0.8% to 2,984.67

- Sensex up 0.5% to 35,128.74

- Australia S&P/ASX 200 up 1.4% to 5,897.88

- Kospi up 0.7% to 2,108.33

- German 10Y yield fell 0.8 bps to -0.478%

- Euro down 0.2% to $1.1221

- Brent futures down 0.7% to $41.44/bbl

- Italian 10Y yield rose 0.6 bps to 1.17%

- Spanish 10Y yield unchanged at 0.47%

- Brent futures down 1.2% to $41.22/bbl

- Gold spot down 0.1% to $1,771.15

- U.S. Dollar Index up 0.18% to 97.70

Top Overnight News

- China’s top legislative body approved a landmark national security law for Hong Kong, a sweeping attempt to quell dissent that drew fresh U.S. retaliation and could endanger the city’s appeal as a financial hub

- Boris Johnson will confirm his commitment to spending billions of pounds on infrastructure to rebuild the coronavirus-ravaged U.K. economy in a major speech on Tuesday, arguing that balancing the books must wait until recovery is secure

- Bets that the Federal Reserve will implement yield-curve control sooner rather than later are showing up in positioning data and the curve itself

- Germany is paving the way for a green bond revolution in Europe by announcing it will sell its first government-backed securities later this year

- Some of Germany’s furloughed workers are beginning to return to work full time, according to a survey by the Ifo Institute

- Prices in the euro area rose 0.3% in June from a year ago, according to preliminary data, versus a 0.2% estimate, as economies across the bloc allowed more businesses to reopen

- France risks losing control of its debts unless the government overhauls its long- term fiscal policy, according to the national auditor

Asian equity markets traded higher as the region took its cue from the firm performance on Wall St which was attributed to several factors including technical buying in the S&P 500 around the 3000 level and encouraging comments by Fed Chair Powell who suggested the US economy entered an important new phase sooner than expected and that recent economic data offers some positive signs, while better than expected Chinese PMI figures also contributed to the overnight optimism. ASX 200 (+1.4%) was lifted from the open with upside in Australia led by firm gains in energy and strength in the top weighted financials sector, with industrials also inspired by the outperformance of their counterparts stateside after Boeing shares soared by double digits as it began 737 MAX test flights. Nikkei 225 (+1.3%) was underpinned as recent favourable currency moves helped participants overlook the soft data which showed the weakest Industrial Production since March 2009 and highest Unemployment Rate in 3 years. Hang Seng (+0.5%) and Shanghai Comp. (+0.8%) were also positive after Chinese Manufacturing PMI and Non-Manufacturing PMI both topped estimates, but with gains capped following another PBoC liquidity drain and after China’s legislature reportedly passed the Hong Kong security bill as expected. Finally, 10yr JGBs traded lower to test support at the 152.00 level as the gains in riskier assets sapped haven demand which also resulted in the 40yr yield rising to its highest since March last year, while weaker results at the 2yr JGB auction further weighed on prices.

Top Asian News

- BOJ’s Bond Purchases Signal Japan’s Curve to Steepen Further

- CAR Inc Surges 17%, Sparks Speculation of Progress in Stake Sale

- BOJ Widens Buying Ranges for Bonds Due Up to 10 Yrs in July Plan

Another day of volatile price action across the equity-sphere but European bourses are ultimately negative [Euro Stoxx -0.1%] as the risk appetite seen during APAC hours petered out on month/quarter and HY-end, where Citi’s month-end model shows a relatively strong signal for a rotation out of European and Japanese stocks into bonds, specifically US, Asian and Canadian. Furthermore, markets could also be bracing for a rise in COVID case-counts as the weekend effect dissipates. Add to that the passage of the Hong Kong security law which is likely to face international pushback, namely from the US, UK and the EU, albeit the latter two have previously signalled a more balanced approach to the situation given their preferability for a Chinese partnership. It’s also worth bearing in mind that Germany will take the EU presidency from tomorrow and have previously hinted at the tougher stance against China. For refence, Eurex suffered an outage overnight for several hours. Nonetheless, European stocks saw a bout of buying immediately after the cash open – somewhat mimicking yesterday’s actions – before gains again subsided. Sectors are now mixed after earlier flow rotated into defensives from cyclicals shortly after the open. The detailed breakdown sees Tech holding its position in the green on the back of Micron’s (+4% pre-mkt) after-market earnings in which guidance was upgraded – thus propping up European peers STMicroelectronics (+1.8%), Dialog Semiconductor (+1.9%), Micro Focus (+0.8%) and Infineon (+0.3%). Banks are on the other end of the spectrum amid lower yields and after Wells Fargo (-1.8%), the fourth largest bank State-side, opted to cut its Q3 dividend when it reports earnings on July 14th. In terms of individual movers, Wirecard (+96%) shares feel some reprieve after UK FCA lifted restrictions on the Co’s UK arm. Meanwhile, Novartis (-1.0%), the likely culprit for losses in the Healthcare sector, remains pressured after the Canadian federal court dismissed a plea by drug makers, including Co., challenging the government’s new regulation aimed at lowering prices of patented drugs.

Top European News

- Shell to Write Down Up to $22 Billion as Virus Hits Big Oil

- Boris Johnson Vows ‘New Deal’ to Rebuild Britain After Virus

- Hedge Funds Score Big Gains on Dividend Bets That Hurt Banks

In FX, the Dollar may yet succumb to bearish rebalancing flows around daily fixes, but more pronounced weakness in major currency rivals is keeping the index afloat around 97.500 and close to a new 97.774 peak amidst waning risk appetite on the final day of June, Q2 and the first half of 2020. Moreover, the Greenback has maintained momentum following Monday’s positive US data (pending home sales) and a slightly more upbeat economic assessment via the text of a speech to be delivered by Fed chair Powell to the House later today.

- NOK/NZD/AUD - Another downturn in crude prices has undermined the Norwegian Krona’s revival, while the Kiwi and Aussie have pulled back from overnight highs after the latter failed to sustain post-Chinese PMI gains on reports that 10 sectors of Melbourne are returning to lockdown and some suburbs may be on the verge of being ordered to stay at home. Eur/Nok has rebounded from sub-10.9000 towards 10.9500, Nzd/Usd has lost grip of the 0.6400 handle and Aud/Usd is back below 0.6850 after fading ahead of 0.6900 where a hefty 1.4 bn option expiry resides.

- GBP/EUR/CAD - Also weaker vs the Buck, as Cable languishes below 1.2300 in wake of weaker than expected UK Q1 GDP awaiting further BoE commentary via Haldane and Cunliffe, while the Euro is only just holding up above 1.1200 and the 100 DMA (1.1205) in the midst of big expiries either side of the round number, and with Eur/Usd one of the only exceptions to the modest sell Dollar for portfolio mantra over month/quarter/half year end. Elsewhere, the Loonie is trying to keep its head above 1.3700 in advance of Canadian GDP for April and the first full month of COVID-19 contagion.

- CHF/JPY - Relative G10 ‘outperformers’ or at least showing more resilience than others due to underlying safe-haven demand and for the Yen in particular reports of RHS Usd/Jpy interest that is seen gathering pace, if not peaking in the run up to 4 pm London time. However, a weaker than forecast Swiss KOF survey has offset a rebound in retail sales, while Japanese ip missed consensus and the jobless rate hit a 3 year high.

- EM - Some respite for the Rand via SA Q1 GDP contracting considerably less than anticipated, as Usd/Zar pares back from nearly 17.4000, albeit still higher in line with peers against the backdrop of fragile risk sentiment and broad Dollar strength. Conversely, the Rouble is still underperforming and jittery on the last day of voting for/against the new Russian convention before Wednesday’s national holiday, with Usd/Rub hovering just shy of 70.9000, and Eur/Pln is firmer following a surprise rebound in Polish CPI.

In commodities, A downbeat session thus far for the oil complex as stocks hold onto losses as with global economies re-imposing some targeted lockdowns amid local flare-ups in COVID-19 cases, with Australia’s Victoria state the latest to re-introduce stay-at-home orders across 10 postcodes. Negativity also arises from the passage of the Hong Kong Security Bill, poised to be implemented tomorrow. WTI Aug resides near session lows, just north of the USD 39/bbl mark (vs. high 39.80/bbl), whilst Brent Sep trades on either side of USD 41.50/bbl, off its USD 41.80/bbl high. Looking ahead, price action will likely be dictated by COVID-related headlines in the absence of anti-China flare-ups over the National Security Bill ahead of the weekly Private Inventory numbers . Elsewhere, spot gold remains within recent ranges between USD 1768-1774/oz as markets eye portfolio rebalancing. Copper prices meanwhile gained overnight amid broader upside in APAC stocks and with supply concerns still on trader’s minds.

US Event Calendar

- 9am: S&P CoreLogic CS 20-City MoM SA, est. 0.5%, prior 0.47%; CS 20-City YoY NSA, est. 3.8%, prior 3.92%;

- 9:45am: MNI Chicago PMI, est. 45, prior 32.3

- 10am: Conf. Board Consumer Confidence, est. 91.4, prior 86.6; Expectations, prior 96.9; Present Situation, prior 71.1

Central Bank Speakers

- 11am: Fed’s Williams Speaks on Central Banking in the Age of Covid

- 11:05am: Fed’s Brainard Discusses a Decade of Dodd- Frank

- 12:30pm: Powell and Mnuchin Speak Before House Financial Panel

- 2pm: Fed’s Bostic and Kashkari Takes Part in Panel on Diversity

DB's Jim Reid concludes the overnight wrap

Welcome to the last day of the first half of 2020. We’ll have our usual month, quarter and YTD (H1) performance review out tomorrow. As H1 draws to a close, equity markets yesterday resolutely looked past the negative headlines from the US and abroad on the coronavirus, choosing to focus on some better than expected economic data. However it’s quite clear from yesterday that there will be hiccups to come in terms of re-openings. In New York City, Mayor de Blasio said that the city might slow the restart of indoor dining, which is currently scheduled to be reopened from July 6, given the spread seen elsewhere. Concurrently, the New York Times reported that Broadway would remain closed for the N this year, with other large cultural venues such as the Metropolitan Museum and Lincoln Center likely to delay opening until later in the summer even if the city gives them a green light. Over in Florida, cases continued to grow, with the state seeing a further 3.7% increase (weekly average of 5.5%), and parts of the state are now indicating they will make mask wearing mandatory. Florida’s slight drop in case growth was seen elsewhere in US. Cases rose by 1.5% overall, compared to the 1.6% weekly average, but the weekend effect was clearly seen in some states. Arizona saw cases rise by 0.8%, but cited a clerical error, where one lab didn’t submit a report to the state’s record keepers. This compounded by the lower testing capacity that we have seen across the US over the weekend likely means there will be a sharp revision in the next couple of days.

Our US Chief Economist, Matthew Luzzetti, released a new video yesterday where he assesses whether the recent deterioration in covid trends across many states led to a retrenchment in economic activity even prior to official rollback of reopenings. A link to video and report are here.

Looking elsewhere, reports continued to be concerning, with Iran reporting its highest number of daily fatalities since the outbreak began, with 162 new deaths in 24 hours. New cases in India continue to grow rapidly, at roughly 3.8% per day on average over the past month, while South America as a whole is now seeing over 40,000 new cases per day with the largest countries yet to see a meaningful drop in new cases. However reported fatalities remain relatively contained given caseloads in those regions. With around 280 fatalities per 1 million residents, Chile, Brazil, and Peru are well below the US (388), UK (642), and Italy (575), however they do trail Germany (108) and Canada (225).

Even against this worrisome virus backdrop, global equity markets rallied following a rather lackluster start to the day as economic data from the US came in stronger than expected and turned the session around. The S&P 500 closed up +1.47%, which as it stands puts the index just one day away from its strongest quarterly performance on a total returns basis since Q4 1998. And that comes after a first quarter that was the worst since Q4 2008, so it’s fair to say we’ve had an eventful few months in financial markets. There may have been some quarter-end rebalancing at work as well given the over +0.5% move in the last 10 minutes of US trading - typical of quarter end type price action. Tech stocks just slightly underperformed, with the NASDAQ up +1.20%, while the Dow Jones climbed +2.32% as Boeing surged +14.43% (best S&P performer on the day) following the weekend announcement that the Federal Aviation Administration had approved some test flights for the 737 Max. Europe lagged slightly as it missed the afternoon rally in New York. The Stoxx 600 gained +0.44%, even while some of the individual bourses were higher. The DAX (+1.18%), IBEX (+1.39%) and FTSEMIB (+1.69%) all outperformed the index.

Other risk assets also benefited from the sudden turn in sentiment yesterday, including commodities. Oil prices recovered from their losses earlier in the session to move higher, with Brent (+1.68%) and WTI (+3.14 %) both advancing, while copper rose +0.77% to a 5-month high as well. Over in fixed income, yields on 10yr Treasuries fell a further -1.8bps to 0.623%, which is their lowest level in over 6 weeks. And in the UK, yields on both 2yr and 5yr gilts fell to a record low as they inched deeper into negative territory.

Asian markets have followed Wall Street’s lead this morning with the Nikkei (+1.67%), Hang Seng (+0.89%), Shanghai Comp (+0.58%), Kospi (+1.74%) and ASX (+1.39%) all up. Meanwhile, futures on the S&P 500 are up a more modest +0.22%.

In terms of the main headlines overnight, China’s NPC has passed the new Hong Kong security law, expected to become effective from July 1. The SCMP has reported that Hong Kong’s Basic Law committee is expected to meet immediately to discuss insertion into Annex III of the city’s mini-constitution. Xinhua, the official state news agency, is expected to publish the details at some point today, marking the first time the law will be fully disclosed to the public.

Prior to that, US Commerce Secretary Wilbur Ross said that regulations affording preferential treatment to Hong Kong over China, including the availability of export license exceptions, are to be suspended while adding “further actions to eliminate differential treatment are also being evaluated”. He also said, “with the Chinese Communist Party’s imposition of new security measures on Hong Kong, the risk that sensitive U.S. technology will be diverted to the People’s Liberation Army or Ministry of State Security has increased, all while undermining the territory’s autonomy.”

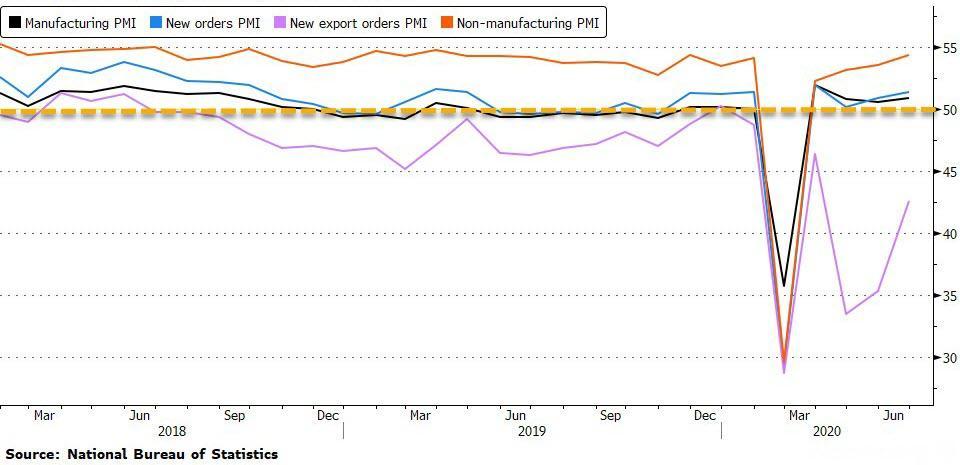

Meanwhile, we’ve also had the latest PMIs out of China which surprised to the upside. The manufacturing PMI rose to 50.9 (vs. 50.5 expected and 50.6 last month) while the non-manufacturing PMI printed at 54.4 (vs. 53.6 expected and 53.6 last month) which left the composite at 54.2 (vs. 53.4 last month). Encouragingly, there was a broad improvement in the details for the manufacturing PMI with output, new orders and new export orders all rising from last month.

The other overnight story has come from here in the UK, with Bloomberg reporting that PM Johnson will announce £5bn of accelerated spending today in roads, schools and hospitals while promising to publish a strategy for further capital spending in the fall. The report further added that in a briefing note about the speech, Johnson’s office has said decisions over increasing taxes or cutting services to pay for the debt will have to wait. The report also added that UK’s Chancellor Sunak is poised to make an economic statement next week.

Back to yesterday. When referencing the EU Recovery plan in a joint press conference with President Macron, Chancellor Merkel made it clear the “talks won’t fail because of us, but there will be no new proposal.” This is not necessarily a negative coming from the two biggest proponents of an extensive continent-wide recovery proposal, as the President of the European Council, Charles Michel, is the one trying to craft a compromise proposal based on the original Merkel-Macron plan. All 27 EU members will convene in Brussels on July 17 to continue hammering out the details of the nearly €750bn plan. Ahead of their press conference, continental sovereign bonds were steady yesterday, with yields on 10yr bunds (+1.2bps), OATs (+0.5bps) and BTPs (+0.6bps) seeing relatively little movement.

While we’re on Europe, it’s worth mentioning a couple of ECB headlines in the light of the recent German constitutional court ruling on their asset purchases. One was a letter from ECB President Lagarde to an MEP which said that the ECB Governing Council had received a request earlier this month from the Bundesbank President “to authorise the disclosure by the Deutsche Bundesbank of non-public documents that show how the ECB has assessed and continues to assess the proportionality of the PSPP and of all its instruments of monetary policy.” It said that the Governing Council had accommodated the request and authorised them to disclose these to the German government, who in turn can share the documents with the German Parliament. This followed a report from FAZ earlier in the day that German finance minister Scholz had told the Bundestag President that the Bundesbank was “permitted to continue to participate in the implementation and execution” of the PSPP since the demands of the German constitutional court had been fulfilled.

Staying with Europe, yesterday our UK team put out a note looking at the state of play in the Brexit negotiations (link here ), and whether there’s room for a deal in the remaining time before the end of the year. Their view is that although the UK has said it wants to complete a deal by the end of the summer, the bar for this remains high. And with a deal also needing time for ratification, it could be that late October/early November becomes the real deadline. On balance, they still see a deal as the more likely outcome, with space for compromise in many of the key areas slowly emerging.

Looking at yesterday’s data releases, in Germany the EU-harmonised CPI reading rose to +0.8% in June, which was above expectations for a +0.6% reading, and up from its nearly-four year low of +0.5% back in May. Meanwhile the European Commission’s economic sentiment indicator for the Euro Area rose to 75.7 (vs. 80.0 expected), which was the second successive increase from April’s low, but still well below the 103.4 reading recorded back in February. And over in the US the data surprised to the upside, with pending home sales rebounding by +44.3% month-on-month in May, well above the +19.3% rebound expected, while the Dallas Fed manufacturing activity also beat expectations to rise to -6.1 (vs. -21.4 expected).

To the day ahead now, and one of the main highlights will be the appearance of Fed Chair Powell and US Treasury Secretary Mnuchin before the House Financial Services Committee. Otherwise, central bank speakers include the BoE’s Haldane and Cunliffe, the Fed’s Williams and Kashkari, and the ECB’s Schnabel and de Guindos. In terms of data, we’ll get the flash June CPI reading for the Euro Area, along with the preliminary June CPI for France and Italy as well. Otherwise, there’ll be Canada’s GDP for April, and from the US we have the Conference Board’s consumer confidence reading for June and the MNI Chicago PMI for June.

International

Four Years Ago This Week, Freedom Was Torched

Four Years Ago This Week, Freedom Was Torched

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare…

Share this:

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare quotes the soothsayer’s warning Julius Caesar about what turned out to be an impending assassination on March 15. The death of American liberty happened around the same time four years ago, when the orders went out from all levels of government to close all indoor and outdoor venues where people gather.

It was not quite a law and it was never voted on by anyone. Seemingly out of nowhere, people who the public had largely ignored, the public health bureaucrats, all united to tell the executives in charge – mayors, governors, and the president – that the only way to deal with a respiratory virus was to scrap freedom and the Bill of Rights.

And they did, not only in the US but all over the world.

The forced closures in the US began on March 6 when the mayor of Austin, Texas, announced the shutdown of the technology and arts festival South by Southwest. Hundreds of thousands of contracts, of attendees and vendors, were instantly scrapped. The mayor said he was acting on the advice of his health experts and they in turn pointed to the CDC, which in turn pointed to the World Health Organization, which in turn pointed to member states and so on.

There was no record of Covid in Austin, Texas, that day but they were sure they were doing their part to stop the spread. It was the first deployment of the “Zero Covid” strategy that became, for a time, official US policy, just as in China.

It was never clear precisely who to blame or who would take responsibility, legal or otherwise.

This Friday evening press conference in Austin was just the beginning. By the next Thursday evening, the lockdown mania reached a full crescendo. Donald Trump went on nationwide television to announce that everything was under control but that he was stopping all travel in and out of US borders, from Europe, the UK, Australia, and New Zealand. American citizens would need to return by Monday or be stuck.

Americans abroad panicked while spending on tickets home and crowded into international airports with waits up to 8 hours standing shoulder to shoulder. It was the first clear sign: there would be no consistency in the deployment of these edicts.

There is no historical record of any American president ever issuing global travel restrictions like this without a declaration of war. Until then, and since the age of travel began, every American had taken it for granted that he could buy a ticket and board a plane. That was no longer possible. Very quickly it became even difficult to travel state to state, as most states eventually implemented a two-week quarantine rule.

The next day, Friday March 13, Broadway closed and New York City began to empty out as any residents who could went to summer homes or out of state.

On that day, the Trump administration declared the national emergency by invoking the Stafford Act which triggers new powers and resources to the Federal Emergency Management Administration.

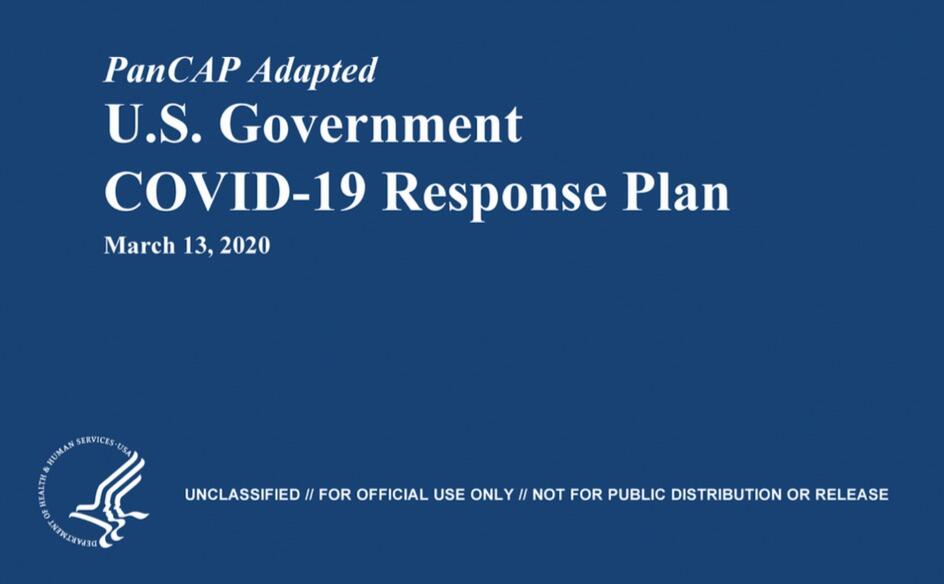

In addition, the Department of Health and Human Services issued a classified document, only to be released to the public months later. The document initiated the lockdowns. It still does not exist on any government website.

The White House Coronavirus Response Task Force, led by the Vice President, will coordinate a whole-of-government approach, including governors, state and local officials, and members of Congress, to develop the best options for the safety, well-being, and health of the American people. HHS is the LFA [Lead Federal Agency] for coordinating the federal response to COVID-19.

Closures were guaranteed:

Recommend significantly limiting public gatherings and cancellation of almost all sporting events, performances, and public and private meetings that cannot be convened by phone. Consider school closures. Issue widespread ‘stay at home’ directives for public and private organizations, with nearly 100% telework for some, although critical public services and infrastructure may need to retain skeleton crews. Law enforcement could shift to focus more on crime prevention, as routine monitoring of storefronts could be important.

In this vision of turnkey totalitarian control of society, the vaccine was pre-approved: “Partner with pharmaceutical industry to produce anti-virals and vaccine.”

The National Security Council was put in charge of policy making. The CDC was just the marketing operation. That’s why it felt like martial law. Without using those words, that’s what was being declared. It even urged information management, with censorship strongly implied.

The timing here is fascinating. This document came out on a Friday. But according to every autobiographical account – from Mike Pence and Scott Gottlieb to Deborah Birx and Jared Kushner – the gathered team did not meet with Trump himself until the weekend of the 14th and 15th, Saturday and Sunday.

According to their account, this was his first real encounter with the urge that he lock down the whole country. He reluctantly agreed to 15 days to flatten the curve. He announced this on Monday the 16th with the famous line: “All public and private venues where people gather should be closed.”

This makes no sense. The decision had already been made and all enabling documents were already in circulation.

There are only two possibilities.

One: the Department of Homeland Security issued this March 13 HHS document without Trump’s knowledge or authority. That seems unlikely.

Two: Kushner, Birx, Pence, and Gottlieb are lying. They decided on a story and they are sticking to it.

Trump himself has never explained the timeline or precisely when he decided to greenlight the lockdowns. To this day, he avoids the issue beyond his constant claim that he doesn’t get enough credit for his handling of the pandemic.

With Nixon, the famous question was always what did he know and when did he know it? When it comes to Trump and insofar as concerns Covid lockdowns – unlike the fake allegations of collusion with Russia – we have no investigations. To this day, no one in the corporate media seems even slightly interested in why, how, or when human rights got abolished by bureaucratic edict.

As part of the lockdowns, the Cybersecurity and Infrastructure Security Agency, which was and is part of the Department of Homeland Security, as set up in 2018, broke the entire American labor force into essential and nonessential.

They also set up and enforced censorship protocols, which is why it seemed like so few objected. In addition, CISA was tasked with overseeing mail-in ballots.

Only 8 days into the 15, Trump announced that he wanted to open the country by Easter, which was on April 12. His announcement on March 24 was treated as outrageous and irresponsible by the national press but keep in mind: Easter would already take us beyond the initial two-week lockdown. What seemed to be an opening was an extension of closing.

This announcement by Trump encouraged Birx and Fauci to ask for an additional 30 days of lockdown, which Trump granted. Even on April 23, Trump told Georgia and Florida, which had made noises about reopening, that “It’s too soon.” He publicly fought with the governor of Georgia, who was first to open his state.

Before the 15 days was over, Congress passed and the president signed the 880-page CARES Act, which authorized the distribution of $2 trillion to states, businesses, and individuals, thus guaranteeing that lockdowns would continue for the duration.

There was never a stated exit plan beyond Birx’s public statements that she wanted zero cases of Covid in the country. That was never going to happen. It is very likely that the virus had already been circulating in the US and Canada from October 2019. A famous seroprevalence study by Jay Bhattacharya came out in May 2020 discerning that infections and immunity were already widespread in the California county they examined.

What that implied was two crucial points: there was zero hope for the Zero Covid mission and this pandemic would end as they all did, through endemicity via exposure, not from a vaccine as such. That was certainly not the message that was being broadcast from Washington. The growing sense at the time was that we all had to sit tight and just wait for the inoculation on which pharmaceutical companies were working.

By summer 2020, you recall what happened. A restless generation of kids fed up with this stay-at-home nonsense seized on the opportunity to protest racial injustice in the killing of George Floyd. Public health officials approved of these gatherings – unlike protests against lockdowns – on grounds that racism was a virus even more serious than Covid. Some of these protests got out of hand and became violent and destructive.

Meanwhile, substance abuse rage – the liquor and weed stores never closed – and immune systems were being degraded by lack of normal exposure, exactly as the Bakersfield doctors had predicted. Millions of small businesses had closed. The learning losses from school closures were mounting, as it turned out that Zoom school was near worthless.

It was about this time that Trump seemed to figure out – thanks to the wise council of Dr. Scott Atlas – that he had been played and started urging states to reopen. But it was strange: he seemed to be less in the position of being a president in charge and more of a public pundit, Tweeting out his wishes until his account was banned. He was unable to put the worms back in the can that he had approved opening.

By that time, and by all accounts, Trump was convinced that the whole effort was a mistake, that he had been trolled into wrecking the country he promised to make great. It was too late. Mail-in ballots had been widely approved, the country was in shambles, the media and public health bureaucrats were ruling the airwaves, and his final months of the campaign failed even to come to grips with the reality on the ground.

At the time, many people had predicted that once Biden took office and the vaccine was released, Covid would be declared to have been beaten. But that didn’t happen and mainly for one reason: resistance to the vaccine was more intense than anyone had predicted. The Biden administration attempted to impose mandates on the entire US workforce. Thanks to a Supreme Court ruling, that effort was thwarted but not before HR departments around the country had already implemented them.

As the months rolled on – and four major cities closed all public accommodations to the unvaccinated, who were being demonized for prolonging the pandemic – it became clear that the vaccine could not and would not stop infection or transmission, which means that this shot could not be classified as a public health benefit. Even as a private benefit, the evidence was mixed. Any protection it provided was short-lived and reports of vaccine injury began to mount. Even now, we cannot gain full clarity on the scale of the problem because essential data and documentation remains classified.

After four years, we find ourselves in a strange position. We still do not know precisely what unfolded in mid-March 2020: who made what decisions, when, and why. There has been no serious attempt at any high level to provide a clear accounting much less assign blame.

Not even Tucker Carlson, who reportedly played a crucial role in getting Trump to panic over the virus, will tell us the source of his own information or what his source told him. There have been a series of valuable hearings in the House and Senate but they have received little to no press attention, and none have focus on the lockdown orders themselves.

The prevailing attitude in public life is just to forget the whole thing. And yet we live now in a country very different from the one we inhabited five years ago. Our media is captured. Social media is widely censored in violation of the First Amendment, a problem being taken up by the Supreme Court this month with no certainty of the outcome. The administrative state that seized control has not given up power. Crime has been normalized. Art and music institutions are on the rocks. Public trust in all official institutions is at rock bottom. We don’t even know if we can trust the elections anymore.

In the early days of lockdown, Henry Kissinger warned that if the mitigation plan does not go well, the world will find itself set “on fire.” He died in 2023. Meanwhile, the world is indeed on fire. The essential struggle in every country on earth today concerns the battle between the authority and power of permanent administration apparatus of the state – the very one that took total control in lockdowns – and the enlightenment ideal of a government that is responsible to the will of the people and the moral demand for freedom and rights.

How this struggle turns out is the essential story of our times.

CODA: I’m embedding a copy of PanCAP Adapted, as annotated by Debbie Lerman. You might need to download the whole thing to see the annotations. If you can help with research, please do.

* * *

Jeffrey Tucker is the author of the excellent new book 'Life After Lock-Down'

Government

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Mandating COVID-19…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Mandating COVID-19 vaccination was a mistake due to ethical and other concerns, a top government doctor warned Dr. Anthony Fauci after Dr. Fauci promoted mass vaccination.

“Coercing or forcing people to take a vaccine can have negative consequences from a biological, sociological, psychological, economical, and ethical standpoint and is not worth the cost even if the vaccine is 100% safe,” Dr. Matthew Memoli, director of the Laboratory of Infectious Diseases clinical studies unit at the U.S. National Institute of Allergy and Infectious Diseases (NIAID), told Dr. Fauci in an email.

“A more prudent approach that considers these issues would be to focus our efforts on those at high risk of severe disease and death, such as the elderly and obese, and do not push vaccination on the young and healthy any further.”

Employing that strategy would help prevent loss of public trust and political capital, Dr. Memoli said.

The email was sent on July 30, 2021, after Dr. Fauci, director of the NIAID, claimed that communities would be safer if more people received one of the COVID-19 vaccines and that mass vaccination would lead to the end of the COVID-19 pandemic.

“We’re on a really good track now to really crush this outbreak, and the more people we get vaccinated, the more assuredness that we’re going to have that we’re going to be able to do that,” Dr. Fauci said on CNN the month prior.

Dr. Memoli, who has studied influenza vaccination for years, disagreed, telling Dr. Fauci that research in the field has indicated yearly shots sometimes drive the evolution of influenza.

Vaccinating people who have not been infected with COVID-19, he said, could potentially impact the evolution of the virus that causes COVID-19 in unexpected ways.

“At best what we are doing with mandated mass vaccination does nothing and the variants emerge evading immunity anyway as they would have without the vaccine,” Dr. Memoli wrote. “At worst it drives evolution of the virus in a way that is different from nature and possibly detrimental, prolonging the pandemic or causing more morbidity and mortality than it should.”

The vaccination strategy was flawed because it relied on a single antigen, introducing immunity that only lasted for a certain period of time, Dr. Memoli said. When the immunity weakened, the virus was given an opportunity to evolve.

Some other experts, including virologist Geert Vanden Bossche, have offered similar views. Others in the scientific community, such as U.S. Centers for Disease Control and Prevention scientists, say vaccination prevents virus evolution, though the agency has acknowledged it doesn’t have records supporting its position.

Other Messages

Dr. Memoli sent the email to Dr. Fauci and two other top NIAID officials, Drs. Hugh Auchincloss and Clifford Lane. The message was first reported by the Wall Street Journal, though the publication did not publish the message. The Epoch Times obtained the email and 199 other pages of Dr. Memoli’s emails through a Freedom of Information Act request. There were no indications that Dr. Fauci ever responded to Dr. Memoli.

Later in 2021, the NIAID’s parent agency, the U.S. National Institutes of Health (NIH), and all other federal government agencies began requiring COVID-19 vaccination, under direction from President Joe Biden.

In other messages, Dr. Memoli said the mandates were unethical and that he was hopeful legal cases brought against the mandates would ultimately let people “make their own healthcare decisions.”

“I am certainly doing everything in my power to influence that,” he wrote on Nov. 2, 2021, to an unknown recipient. Dr. Memoli also disclosed that both he and his wife had applied for exemptions from the mandates imposed by the NIH and his wife’s employer. While her request had been granted, his had not as of yet, Dr. Memoli said. It’s not clear if it ever was.

According to Dr. Memoli, officials had not gone over the bioethics of the mandates. He wrote to the NIH’s Department of Bioethics, pointing out that the protection from the vaccines waned over time, that the shots can cause serious health issues such as myocarditis, or heart inflammation, and that vaccinated people were just as likely to spread COVID-19 as unvaccinated people.

He cited multiple studies in his emails, including one that found a resurgence of COVID-19 cases in a California health care system despite a high rate of vaccination and another that showed transmission rates were similar among the vaccinated and unvaccinated.

Dr. Memoli said he was “particularly interested in the bioethics of a mandate when the vaccine doesn’t have the ability to stop spread of the disease, which is the purpose of the mandate.”

The message led to Dr. Memoli speaking during an NIH event in December 2021, several weeks after he went public with his concerns about mandating vaccines.

“Vaccine mandates should be rare and considered only with a strong justification,” Dr. Memoli said in the debate. He suggested that the justification was not there for COVID-19 vaccines, given their fleeting effectiveness.

Julie Ledgerwood, another NIAID official who also spoke at the event, said that the vaccines were highly effective and that the side effects that had been detected were not significant. She did acknowledge that vaccinated people needed boosters after a period of time.

The NIH, and many other government agencies, removed their mandates in 2023 with the end of the COVID-19 public health emergency.

A request for comment from Dr. Fauci was not returned. Dr. Memoli told The Epoch Times in an email he was “happy to answer any questions you have” but that he needed clearance from the NIAID’s media office. That office then refused to give clearance.

Dr. Jay Bhattacharya, a professor of health policy at Stanford University, said that Dr. Memoli showed bravery when he warned Dr. Fauci against mandates.

“Those mandates have done more to demolish public trust in public health than any single action by public health officials in my professional career, including diminishing public trust in all vaccines.” Dr. Bhattacharya, a frequent critic of the U.S. response to COVID-19, told The Epoch Times via email. “It was risky for Dr. Memoli to speak publicly since he works at the NIH, and the culture of the NIH punishes those who cross powerful scientific bureaucrats like Dr. Fauci or his former boss, Dr. Francis Collins.”

Government

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Trump "Clearly Hasn’t Learned From His COVID-Era Mistakes", RFK Jr. Says

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President…

Share this:

{kind=link}

{kind=link}

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President Joe Biden claimed that COVID vaccines are now helping cancer patients during his State of the Union address on March 7, but it was a response on Truth Social from former President Donald Trump that drew the ire of independent presidential candidate Robert F. Kennedy Jr.

{kind=link}

During the address, President Biden said: “The pandemic no longer controls our lives. The vaccines that saved us from COVID are now being used to help beat cancer, turning setback into comeback. That’s what America does.”

President Trump wrote: “The Pandemic no longer controls our lives. The VACCINES that saved us from COVID are now being used to help beat cancer—turning setback into comeback. YOU’RE WELCOME JOE. NINE-MONTH APPROVAL TIME VS. 12 YEARS THAT IT WOULD HAVE TAKEN YOU.”

An outspoken critic of President Trump’s COVID response, and the Operation Warp Speed program that escalated the availability of COVID vaccines, Mr. Kennedy said on X, formerly known as Twitter, that “Donald Trump clearly hasn’t learned from his COVID-era mistakes.”

“He fails to recognize how ineffective his warp speed vaccine is as the ninth shot is being recommended to seniors. Even more troubling is the documented harm being caused by the shot to so many innocent children and adults who are suffering myocarditis, pericarditis, and brain inflammation,” Mr. Kennedy remarked.

“This has been confirmed by a CDC-funded study of 99 million people. Instead of bragging about its speedy approval, we should be honestly and transparently debating the abundant evidence that this vaccine may have caused more harm than good.

“I look forward to debating both Trump and Biden on Sept. 16 in San Marcos, Texas.”

Mr. Kennedy announced in April 2023 that he would challenge President Biden for the 2024 Democratic Party presidential nomination before declaring his run as an independent last October, claiming that the Democrat National Committee was “rigging the primary.”

Since the early stages of his campaign, Mr. Kennedy has generated more support than pundits expected from conservatives, moderates, and independents resulting in speculation that he could take votes away from President Trump.

Many Republicans continue to seek a reckoning over the government-imposed pandemic lockdowns and vaccine mandates.

President Trump’s defense of Operation Warp Speed, the program he rolled out in May 2020 to spur the development and distribution of COVID-19 vaccines amid the pandemic, remains a sticking point for some of his supporters.

Operation Warp Speed featured a partnership between the government, the military, and the private sector, with the government paying for millions of vaccine doses to be produced.

President Trump released a statement in March 2021 saying: “I hope everyone remembers when they’re getting the COVID-19 Vaccine, that if I wasn’t President, you wouldn’t be getting that beautiful ‘shot’ for 5 years, at best, and probably wouldn’t be getting it at all. I hope everyone remembers!”

President Trump said about the COVID-19 vaccine in an interview on Fox News in March 2021: “It works incredibly well. Ninety-five percent, maybe even more than that. I would recommend it, and I would recommend it to a lot of people that don’t want to get it and a lot of those people voted for me, frankly.

“But again, we have our freedoms and we have to live by that and I agree with that also. But it’s a great vaccine, it’s a safe vaccine, and it’s something that works.”

On many occasions, President Trump has said that he is not in favor of vaccine mandates.

An environmental attorney, Mr. Kennedy founded Children’s Health Defense, a nonprofit that aims to end childhood health epidemics by promoting vaccine safeguards, among other initiatives.

Last year, Mr. Kennedy told podcaster Joe Rogan that ivermectin was suppressed by the FDA so that the COVID-19 vaccines could be granted emergency use authorization.

He has criticized Big Pharma, vaccine safety, and government mandates for years.

Since launching his presidential campaign, Mr. Kennedy has made his stances on the COVID-19 vaccines, and vaccines in general, a frequent talking point.

“I would argue that the science is very clear right now that they [vaccines] caused a lot more problems than they averted,” Mr. Kennedy said on Piers Morgan Uncensored last April.

“And if you look at the countries that did not vaccinate, they had the lowest death rates, they had the lowest COVID and infection rates.”

Additional data show a “direct correlation” between excess deaths and high vaccination rates in developed countries, he said.

President Trump and Mr. Kennedy have similar views on topics like protecting the U.S.-Mexico border and ending the Russia-Ukraine war.

COVID-19 is the topic where Mr. Kennedy and President Trump seem to differ the most.

Former President Donald Trump intended to “drain the swamp” when he took office in 2017, but he was “intimidated by bureaucrats” at federal agencies and did not accomplish that objective, Mr. Kennedy said on Feb. 5.

Speaking at a voter rally in Tucson, where he collected signatures to get on the Arizona ballot, the independent presidential candidate said President Trump was “earnest” when he vowed to “drain the swamp,” but it was “business as usual” during his term.

John Bolton, who President Trump appointed as a national security adviser, is “the template for a swamp creature,” Mr. Kennedy said.

Scott Gottlieb, who President Trump named to run the FDA, “was Pfizer’s business partner” and eventually returned to Pfizer, Mr. Kennedy said.

Mr. Kennedy said that President Trump had more lobbyists running federal agencies than any president in U.S. history.

“You can’t reform them when you’ve got the swamp creatures running them, and I’m not going to do that. I’m going to do something different,” Mr. Kennedy said.

During the COVID-19 pandemic, President Trump “did not ask the questions that he should have,” he believes.

President Trump “knew that lockdowns were wrong” and then “agreed to lockdowns,” Mr. Kennedy said.

He also “knew that hydroxychloroquine worked, he said it,” Mr. Kennedy explained, adding that he was eventually “rolled over” by Dr. Anthony Fauci and his advisers.

MaryJo Perry, a longtime advocate for vaccine choice and a Trump supporter, thinks votes will be at a premium come Election Day, particularly because the independent and third-party field is becoming more competitive.

Ms. Perry, president of Mississippi Parents for Vaccine Rights, believes advocates for medical freedom could determine who is ultimately president.

She believes that Mr. Kennedy is “pulling votes from Trump” because of the former president’s stance on the vaccines.

“People care about medical freedom. It’s an important issue here in Mississippi, and across the country,” Ms. Perry told The Epoch Times.

“Trump should admit he was wrong about Operation Warp Speed and that COVID vaccines have been dangerous. That would make a difference among people he has offended.”

President Trump won’t lose enough votes to Mr. Kennedy about Operation Warp Speed and COVID vaccines to have a significant impact on the election, Ohio Republican strategist Wes Farno told The Epoch Times.

President Trump won in Ohio by eight percentage points in both 2016 and 2020. The Ohio Republican Party endorsed President Trump for the nomination in 2024.

“The positives of a Trump presidency far outweigh the negatives,” Mr. Farno said. “People are more concerned about their wallet and the economy.

“They are asking themselves if they were better off during President Trump’s term compared to since President Biden took office. The answer to that question is obvious because many Americans are struggling to afford groceries, gas, mortgages, and rent payments.

“America needs President Trump.”

Multiple national polls back Mr. Farno’s view.

As of March 6, the RealClearPolitics average of polls indicates that President Trump has 41.8 percent support in a five-way race that includes President Biden (38.4 percent), Mr. Kennedy (12.7 percent), independent Cornel West (2.6 percent), and Green Party nominee Jill Stein (1.7 percent).

A Pew Research Center study conducted among 10,133 U.S. adults from Feb. 7 to Feb. 11 showed that Democrats and Democrat-leaning independents (42 percent) are more likely than Republicans and GOP-leaning independents (15 percent) to say they have received an updated COVID vaccine.

The poll also reported that just 28 percent of adults say they have received the updated COVID inoculation.

The peer-reviewed multinational study of more than 99 million vaccinated people that Mr. Kennedy referenced in his X post on March 7 was published in the Vaccine journal on Feb. 12.

It aimed to evaluate the risk of 13 adverse events of special interest (AESI) following COVID-19 vaccination. The AESIs spanned three categories—neurological, hematologic (blood), and cardiovascular.

The study reviewed data collected from more than 99 million vaccinated people from eight nations—Argentina, Australia, Canada, Denmark, Finland, France, New Zealand, and Scotland—looking at risks up to 42 days after getting the shots.

Three vaccines—Pfizer and Moderna’s mRNA vaccines as well as AstraZeneca’s viral vector jab—were examined in the study.

Researchers found higher-than-expected cases that they deemed met the threshold to be potential safety signals for multiple AESIs, including for Guillain-Barre syndrome (GBS), cerebral venous sinus thrombosis (CVST), myocarditis, and pericarditis.

A safety signal refers to information that could suggest a potential risk or harm that may be associated with a medical product.

The study identified higher incidences of neurological, cardiovascular, and blood disorder complications than what the researchers expected.

President Trump’s role in Operation Warp Speed, and his continued praise of the COVID vaccine, remains a concern for some voters, including those who still support him.

Krista Cobb is a 40-year-old mother in western Ohio. She voted for President Trump in 2020 and said she would cast her vote for him this November, but she was stunned when she saw his response to President Biden about the COVID-19 vaccine during the State of the Union address.

“I love President Trump and support his policies, but at this point, he has to know they [advisers and health officials] lied about the shot,” Ms. Cobb told The Epoch Times.

“If he continues to promote it, especially after all of the hearings they’ve had about it in Congress, the side effects, and cover-ups on Capitol Hill, at what point does he become the same as the people who have lied?” Ms. Cobb added.

“I think he should distance himself from talk about Operation Warp Speed and even admit that he was wrong—that the vaccines have not had the impact he was told they would have. If he did that, people would respect him even more.”

Four Years Ago This Week, Freedom Was Torched

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

The next pandemic? It’s already here for Earth’s wildlife

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Vaccine-skeptical mothers say bad health care experiences made them distrust the medical system

Survey Shows Declining Concerns Among Americans About COVID-19

Chinese migration to US is nothing new – but the reasons for recent surge at Southern border are

As the pandemic turns four, here’s what we need to do for a healthier future

A major cruise line is testing a monthly subscription service

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International4 days ago

International4 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International4 days ago

International4 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges