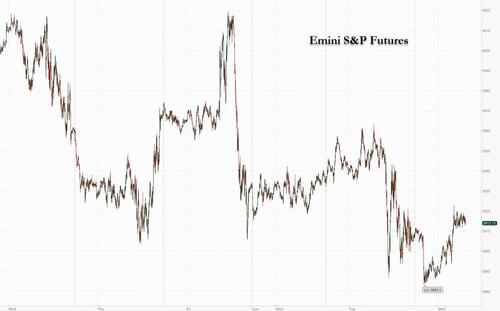

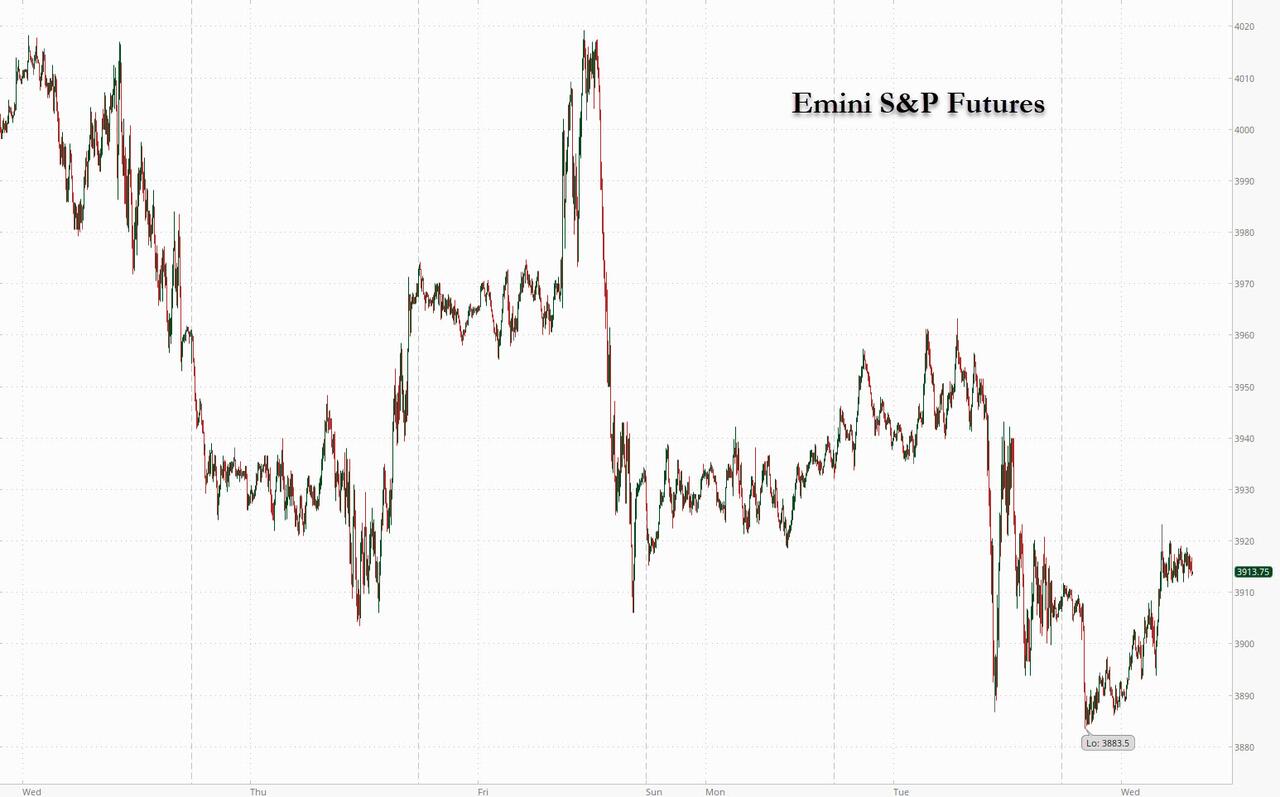

Futures Flat, Dollars Steamrolls To New Record Highs Ahead Of Fed Speaker Barrage

S&P futures swung in illiquid overnight trading, first sliding below the key 3,900 level after the Japan open, only to recover all losses after Europe opened, with the dollar storming to new record highs and steamrolling all FX competitors as traders braced for a slew of hawkish Fed speakers to assess the path of monetary policy and its impact on the economy. S&P 500 futures edged 0.1% higher at 7:15 a.m. in New York after the underlying benchmark fell six out of the last seven sessions, while Nasdaq 100 futures rose 0.3%, as both European and Asian market slumped. The Bloomberg Dollar index hit a new record high as the Yen plunge below 144 for the first time since 1998 and the Chinese yuan flirted with the key 7.00 level. Bitcoin recovered modestly after tumbling to new 2022 lows and oil erased a decline after Russian President Vladimir Putin underlined that his country won’t supply oil and fuel if price caps on the country’s exports are introduced..

In premarket trading, UiPath tumbled 21% after the application software company gave weaker-than-expected third-quarter revenue forecast. Meanwhile, Gitlab gained 3% in US premarket trading after second-quarter earnings. While analysts were broadly positive on the software development platform’s increased revenue guidance, especially given a tough backdrop, Piper Sandler flagged “noise” around a deceleration in billings. Here are the other notable premarket movers:

Coupa Software (COUP US) rises about 12% in premarket trading on Wednesday after boosting its full-year earnings guidance and posting better-than-expected second-quarter results, helped by strong billings in North America. While analysts were positive about the results, they remained cautious about softness in Europe.

Keep an eye on shares in US utilities and energy suppliers, incuding PG&E (PCG US), Edison International (EIX US) and Sempra Energy (SRE US) amid a deepening power crisis in California, where a heat wave is piling pressure on the US state’s power grid.

Watch US digital health companies, as Truist initiates coverage on 16 firms, with a positive view on the industry overall. Progyny (PGNY US), Privia Health (PRVA US), Accolade (ACCD US), Agilon (AGL US) and R1 RCM (RCM US) all started with buy ratings.

Watch Petco (WOOF US) stock as it was initiated with an outperform rating and $17 PT at RBC, with the broker saying near-term risks are reflected in the shares and the long-term picture is positive for the pet health company.

Keep an eye on Guidewire (GWRE US) as RBC Capital Markets says that the software company has reported a “mixed” quarter amid macroeconomic headwinds with “muted” guidance.

Alvotech (ALVO US) stock may be in focus as it was initiated with an equal-weight rating at Morgan Stanley, with broker flagging “many knowns” and a wide range of possible outcomes of the biotech’s US launch of its lead product, the biosimilar Humira.

Newell Brands (NWL US) fell 4.6% in US postmarket trading on Tuesday after the consumer-products company cut its normalized earnings per share guidance for the full year. The firm has “limited” visibility and is buffeted by macroeconomic pressures, Morgan Stanley says.

On today's calendar, no less than four Fed officials including Vice Chair Lael Brainard and Cleveland President Loretta Mester are set to speak before the release of the US Beige book later this afternoon. Richmond President Thomas Barkin already said rates must stay high until inflation eases. Investors will closely monitor their comments for clues about the pace of interest rate hikes in the face of slowing growth and still-elevated inflation. The consumer-price index reading due next week will also be paramount for the Fed’s September decision. Bets on another 75 basis points Fed interest-rate hike to tackle high inflation have spurred a selloff in Treasuries, while traders are bracing for a European Central Bank rates decision due on Thursday, with the potential for a similar-size move.

Aside from tightening monetary settings and an apparently unstoppable dollar, markets are also contending with a debilitating energy crisis in Europe and Covid lockdowns in China. Concerns are growing about the outlook for company earnings given the various global economic headwinds and a rebound seen in equity markets since mid-June is fading.

The S&P 500 rose too much in July and is overvalued by about 10% compared to macroeconomic fundamentals, according to Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. He expects the Federal Reserve to hike rates by 75 basis points even if inflation declined in August. “The current wait-and-see mode of the US market should be short-lived,” he said. “We expect another leg down in the S&P 500 into the fourth quarter before we find a bottom.”

“At this point, we see no positive triggers to keep the rally going, while there are rising risks moving into autumn amid a gloomier economic backdrop,” Amundi SA Chief Investment Officer Vincent Mortier and his deputy, Matteo Germano, wrote in a note. “To cope with this environment, we believe investors should adjust their asset allocation stances.”

Europe’s Stoxx 600 Index fell 0.4%, with tumbling miners leading the declines; IBEX outperforms, adding 0.4%, FTSE 100 lags, dropping 0.7%. Banks, miners and retailers are the worst-performing sectors.

Earlier in the session, Asiun stocks were pressured amid spillover selling from Wall St owing to the higher yield environment and as participants digested the latest Chinese trade data. ASX 200 weakened from the open with the index dragged lower by the energy and mining-related sectors and with somewhat mixed GDP data not doing much to spur risk appetite. Hang Seng and Shanghai Comp were subdued amid the ongoing COVID woes and following the softer than expected Chinese trade data in which all metrics missed forecasts.

Japanese stocks also fell as the yen slumped to a level that leaves it on track for its worst year on record, prompting government warnings and putting traders on edge as volatility rises. The Topix Index fell 0.6% to 1,915.65 as of market close Tokyo time, while the Nikkei declined 0.7% to 27,430.30. Sony Group Corp. contributed the most to the Topix Index decline, decreasing 2.3%. Out of 2,169 stocks in the index, 492 rose and 1,610 fell, while 67 were unchanged. While currency weakness is generally seen as favorable for exporters, rapid depreciation raises input costs and can complicate business decisions. “With the yen this weak, it’s difficult for the stock market to rally,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Limited.

In Australia, the S&P/ASX 200 index fell 1.4% to close at 6,729.30, dragged by declines in banks and mining shares. Energy-related shares fell after oil retreated to the lowest level since January on concern a global slowdown will cut demand in Europe and the US just as China’s Covid Zero strategy hurts consumption. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,548.30.

In India, key equity indexes dropped on Wednesday, tracking a selloff in Asia, with companies such as ICICI Bank and Reliance Industries putting pressure on the market. The S&P BSE Sensex closed 0.3% lower at 59,028.91 in Mumbai, while the NSE Nifty 50 Index fell 0.2%, extending its decline for a second day. Still, all but five of the 19 sector sub-gauges compiled by BSE Ltd. gained, led by an index of basic material companies. Automobile stocks were the worst performers. However, the broader market, including mid- and small-cap companies, gained as basic material stocks advanced on the back of recent decline in commodity prices. The S&P BSE MidCap Index fell as much as 0.5%, before closing higher by an equal measure and climbing to its highest level since Jan. 17.

In FX, the Bloomberg dollar index surged to a fresh record as strong US data and hawkish comments from a Federal Reserve official reinforced aggressive tightening bets. The Bloomberg Dollar Spot Index gained as much as 0.4% fuelling weakness among all of its Group-of-10 peers.

Fed’s Richmond President Thomas Barkin said in an interview with the Financial Times that the central bank must raise interest rates to a level that restrains economic activity and keep them there until policy makers are “convinced” that rampant inflation is subsiding.

The yen fell to a fresh 24-year low, prompting Japan’s top spokesman Hirokazu Matsuno to say he’s concerned about recent rapid, one-sided moves in the yen and the country would need to take “necessary action” if these movements continue. But despite this verbal intervention, “markets appear quite happy with testing their tolerance” and 145.00 might be the line in the sand, Francesco Pesole, a strategist at ING Groep NV wrote in a note. USD/JPY rose as high as 144.99. The Bank of Japan said it would boost scheduled bond purchases as Japan’s benchmark 10- year yield hit 0.24% -- approaching the 0.25% upper limit of the BOJ’s tolerated trading band

GBP/USD fell 0.4% to 1.1471 erasing gains made after reports of Prime Minister Liz Truss’s energy support package. The pound has managed to “discount much of the bad news but that does not mean that it will bound higher anytime soon,” Steve Barrow, a strategist at Standard Bank wrote in a note.

AUD/USD lost 0.2% to 0.6722; a drop below the July 14 low of 0.6682 would take it to the lowest since 2020

In rates,Treasuries hold gains, reversing some of Tuesday’s declines, amid a bull-steepening rally in gilts where 2-year yields are richer by around 25bp on the day as BOE speakers discuss inflation outlook amid proposed government action. US yields richer by 2bp to 4bp across the curve with gains led by front-end, steepening 2s10s spread by around 1bp; 10-year yields at 3.33%, richer by 2.5bp and underperforming bunds and gilts in the sector by 3.5bp and 6bp.Sharp bull-steepening in gilts follows dovish comments from BOE’s Tenreyro; UK 2s10s, 5s30s spreads widen 8bp and 7bp into the front-end led rally.Fed speaker slate includes Vice Chair Brainard on the economic outlook; Chair Powell has an appearance scheduled for Thursday; August CPI report to be released Sept. 13 falls during the blackout period.IG dollar issuance slate includes IFC $2b 3Y SOFR and IADB 7Y SOFR; more than $35b priced Tuesday with issuers paying just over 10bps in concessions on deals 2.8x covered, and at least three borrowers stood down.

WTI crude drifts 0.6% higher to trade near $87.38 after Putin said Russia won’t supply oil, fuel or gas if price caps are introduced; gold adds about ~$3 to $1,705. Bitcoin prices slipped overnight to under USD 19,000 whilst Ethereum tested 1,500 to the downside; and gold recovered to trade above $1,700 an ounce.

To the day ahead now, and there’s plenty on the central bank side, as the Bank of Canada announce their latest policy decision and the Fed release their Beige Book. We’ll also hear from Bank of England Governor Bailey, as well as the BoE’s Pill, Mann and Tenreyro as they testify before the Treasury Select Committee. In addition, there are scheduled remarks Fed officials, including Vice Chair Brainard, Vice Chair Barr, and Mester and Barkin. Otherwise, data releases include German industrial production and Italian retail sales for July.

Market Snapshot

S&P 500 futures up 0.1% to 3,915.00

STOXX Europe 600 down 0.5% to 412.19

MXAP down 1.3% to 150.62

MXAPJ down 1.2% to 496.50

Nikkei down 0.7% to 27,430.30

Topix down 0.6% to 1,915.65

Hang Seng Index down 0.8% to 19,044.30

Shanghai Composite little changed at 3,246.29

Sensex down 0.2% to 59,092.96

Australia S&P/ASX 200 down 1.4% to 6,729.34

Kospi down 1.4% to 2,376.46

Brent Futures down 0.3% to $92.56/bbl

Gold spot up 0.1% to $1,703.64

U.S. Dollar Index little changed at 110.31

German 10Y yield little changed at 1.59%

Euro up 0.1% to $0.9916

Brent Futures down 0.3% to $92.57/bbl

Top Overnight News from Bloomberg

The Federal Reserve must raise interest rates to a level that restrains economic activity and keep them there until policy makers are “convinced” that rampant inflation is subsiding, Fed Richmond President Thomas Barkin said in an interview with the Financial Times

All 31 economists surveyed by Bloomberg expect Bank of Canada policy makers led by Governor Tiff Macklem to raise the benchmark overnight rate by at least 50 basis points, and most say it will be 75 basis points

The ECB’s interest-rate hikes may fail to fully filter through into markets without a shift in its policies. Interest-rate rises are already struggling to be reflected across money markets because there’s too much cash chasing scarce high-quality securities, depressing their yields

The euro-area economy expanded by more than initially estimated in the second quarter, with the revision revealing greater support from consumer and government spending. Output rose 0.8% from the previous three months -- stronger than an earlier reading of 0.6%

“Give us turbines and we’ll turn on Nord Stream tomorrow, but they won’t give us anything,” President Vladimir Putin said at the Eastern Economic Forum in Vladivostok

The European Commission recommends member states cap the price of electricity from producers like wind farms, nuclear and coal plants at EU200 per MWh, the Financial Times reported, citing a draft of proposals it has seen

The yen has slumped to a level that leaves it on track for its worst year on record, prompting the strongest warnings to date from senior Japanese government officials aimed at stemming the slide

The world’s original and longest-running experiment in negative interest rates will finally end this week as Denmark raises borrowing costs in tandem with the euro zone. The move is likely as the ECB delivers a large hike on Thursday, because Danish monetary policy often shadows such moves to protect the krone’s peg to the single currency

Developed economies are taking a hit from the dollar’s appreciation to multi-decade highs in ways that were once more familiar to their emerging-market peers

China’s export growth slowed in August and imports stagnated, a sign of a darkening global economic picture and weak domestic growth hit by Covid lockdowns and a property slump. Exports in US dollar terms expanded 7.1% last month from a year earlier, far weaker than economists had predicted

China sent its most powerful signal yet on its discomfort with the yuan’s weakness by setting its reference rate for the currency with the strongest bias on record

A more detailed look at global markets courtesy of Newsquawk

Asia stocks were pressured amid spillover selling from Wall St owing to the higher yield environment and as participants digested the latest Chinese trade data. ASX 200 weakened from the open with the index dragged lower by the energy and mining-related sectors and with somewhat mixed GDP data not doing much to spur risk appetite. Nikkei 225 declined despite a further weakening in the JPY as the recent rapid currency depreciation raised further questions surrounding the BoJ’s dovish resolve. Hang Seng and Shanghai Comp were subdued amid the ongoing COVID woes and following the softer than expected Chinese trade data in which all metrics missed forecasts.

Top Asian News

Japanese Chief Cabinet Secretary Matsuno believes relaxation of border control measures could be an advantage with the weak JPY, while they are concerned by recent rapid, one-sided currency moves and are ready to take appropriate action on FX market moves if necessary, according to Reuters.

Japanese Finance Minister Suzuki, when asked about the chance of currency intervention, says will take necessary steps, according to Reuters.

Japan's former MOF FX head Watanabe said there is no need for Japan to intervene in the currency market to stem the yen's declines and that Japan intervening solo in the FX market would be meaningless as current FX moves are driven by broad dollar gains, while he noted that intervening solo would be a waste of money as markets would know Tokyo has limited to how much reserves it can tap to continue with such actions. Wakatabe also stated that USD/JPY is overshooting somewhat now and may briefly reach 145 later this month but such increases likely won't last long, while he doesn't think the BoJ will raise rates just to stem JPY's declines.

Xi, Putin to Meet for First Time Since Russia’s War in Ukraine

China’s Xi Has Broad Support for Continued Rule, Envoy Says

Korean Won Still Near 13-Year Low After Central Bank Warning

Vietnam Wins Rating Upgrade From Moody’s on stronger Growth

China State-Backed Expo Pulls Ukraine Trade Event at Last Minute

Goldman Sachs, BNP Paribas at Odds Over Asia Earnings Outlook

European bourses have trimmed the losses seen at the open, but still trade mostly lower. European sectors are mostly lower after opening with a mild defensive bias – that bias has since eased somewhat, with some cyclicals making their way up the ranks. Stateside, US equity futures were softer in early trade, but to a lesser extent than peers across the pond, and have since mostly moved into the green as yields ease

Top European News

UK PM Truss spoke with US President Biden with Truss said to be looking forward to working with Biden to tackle shared challenges, particularly extreme economic problems from Russian President Putin's war, while they discussed domestic issues and agreed on the importance of protecting the Good Friday Agreement, according to Downing Street.

UK PM Truss will not activate the emergency Article 16 override provision in the Northern Ireland protocol in the coming weeks and pulling away from an early confrontation with the EU over Brexit, according to FT citing the PM's allies.

BoE Governor Bailey noted that we have had volatile markets in the last six weeks, still seeing extreme volatility in energy markets. On the UK exchange rate, said there are dollar-specific factors in play; said the Fed is more focussed on bringing demand shock under control. Bailey added a review of the Bank's mandate would not be a recognition that the BoE regime is failing.

BoE Chief Economist Pill said he does not want to comment on fiscal stimulus without seeing the details. He expects headline inflation to decline in the short-term. Pill emphasised the importance of BoE inflation target as an anchor, not considering new regime.

BoE's Mann said trade, financial flows, and GBP may have heightened role in the next year. Mann added that more forceful bank rate moves open door for policy to be on hold or a reversal later. She added that short-term inflation spikes are getting increasingly embedded in domestic prices.

BoE's Tenreyro said demand is already weakening, and added when close to equilibrium rate, gradual hikes allow BoE to react before it tightens too far into contractionary territory. "Even without rate increases in August, rates were at a sufficient level to return inflation to target over the medium-term."

FX

DXY maintains bullish momentum but remained under 110.50 throughout most of the European session in a 110.17-69 range (at the time of writing).

JPY underperforms with USD/JPY extending above 144.00 despite a slew of verbal intervention by Japanese officials, whilst the Yuan shrugged off another firm CNY fixing by the PBoC.

EUR, and CHF are all trading mid-range vs the USD whilst the NZD, AUD, and CAD track risk sentiment.

Fixed Income

Debt futures are hovering just below best levels having extended rebounds to fresh intraday highs in the run up to UK and German auctions that saw solid demand.

Bunds sit under their 145.24 peak (+44 ticks vs -33 ticks at one stage), Gilts skirt 106.00 from 106.11 (+38 ticks vs -59 ticks at the Liffe low).

10yr T-note holds closer to 115-27 than 115-13+ following some hefty block purchases (two 10k clips in particular)

Commodities

WTI and Brent futures have been bouncing off worst levels after printing multi-month lows.

Spot gold fluctuates on either side of USD 1,700/oz, driven largely by bond yields.

Base metals are mostly lower with upside hampered by disappointing Chinese trade data overnight.

Indian PM Modi said keen to boost ties with Russia; said Russia and India can work closely on coking coal supply.

US Event Calendar

07:00: Sept. MBA Mortgage Applications, prior -3.7%

08:30: July Trade Balance, est. -$70.2b, prior -$79.6b

14:00: U.S. Federal Reserve Releases Beige Book

Fed Speakers

09:00: Fed’s Barkin Speaks at MIT

10:00: Fed’s Mester speaks at MNI virtual event

12:40: Fed’s Brainard Discusses the Economic Outlook

14:00: Fed’s Barr Speaks on Financial System Fairness and Safety

DB's Jim Reid concludes the overnight wrap

The air of feral fog will lift from our house this morning as the kids go back to school. Only about 12-50 years, depending on the debts we collectively leave to our children, until they leave home. After the summer she's had looking after them I'm slightly worried my wife will leave first. A big fingers crossed she doesn't.

On this theme, today I've just launched a back-to-school survey as part of our regular monthly series. This month we ask whether you think Europe will make it through winter without gas rationing, whether you are thinking about using less energy, at recession probabilities, whether the next big move in bonds and equities will be up or down, your inflation expectations and which if any central banks are likely to make a policy error and in which direction. All help filling it in very much appreciated as usual. See here for the survey.

Yesterday I released my latest chartbook, which also has a back-to-school vibe as we review where we are on important issues facing global markets and the economy over the coming months. Among the charts, we look at how August was the worst month for European bonds in decades, why inflation isn’t going away over the medium-to-longer term, the latest on the European energy crisis, and also briefly examine the upcoming Italian election and the Chinese property sector’s troubles. As ever, it’s full of big easy-to-read figures and titles that explain our biases. Here’s the link. ***

With different asset classes swinging between gains and losses over the last 24 hours, it’s been difficult to point to a single factor behind the various moves. On the one hand, investors remain cautious about the growing array of risks on the horizon, ranging from the European energy situation to Chinese lockdowns to hawkish central banks. But on the other hand, the latest ISM services index for August added to the recent run of US data releases that’s pointed to an improving outlook, suggesting that the Fed can afford to be more aggressive in raising rates, which in turn led to a sharp selloff in Treasuries that leaves them on track for their 6th consecutive weekly decline.

In terms of the details of that ISM print, the headline measure unexpectedly rose in August to a 4-month high of 56.9 (vs. 55.3 expected), with improvements in the new orders and employment components as well. That follows in the footsteps of the ISM manufacturing reading last Thursday that was similarly better than expected, the weekly initial jobless claims that fell for a 3rd week running, and the Conference Board’s consumer confidence measure that hit a 3-month high in August. Now all this might be a last hurrah before our long expected 2023 recession, but there’s no doubt that recent data has been more positive than expected, and is coming alongside some other tailwinds of note like falling gasoline prices.

Given the stronger data, there were growing expectations (again) that the Fed might hike by 75bps in a couple of weeks’ time, with the hike priced in for September up by +2.9bps to 68.0bps. Treasury yields surged across the curve in response (with also a small catch-up after being closed on Monday), with some of the increase likely exacerbated by a banner day for corporate debt issuance ahead of the next Fed meeting (not to mention ahead of the next crucial CPI print), with the 10yr yield up +16.0bps on the day to 3.35%, and the 30yr yield (+15.6bps) even hitting a post-2014 high of 3.50%. That was driven by a rise in real yields, with the 10yr real yield (+15.0bps) rising to a post-2019 high of 0.87%. This morning in Asia, yields on the 10yr USTs are fairly stable. Bear in mind that it was less than -1% in early March after Russia invaded Ukraine, so we’ve seen an incredible shift in real borrowing costs over the last 6 months.

With US real yields reaching new heights, the dollar index advanced +0.62% to reach its strongest level in over two decades. However, it was bad news for equities and the S&P 500 (-0.41%) built on its run of 3 consecutive weekly declines to close at a 7-week low. The more interest-sensitive sectors were particularly affected, and the NASDAQ (-0.74%) and the FANG+ index (-1.50%) saw even larger declines, while there was a clear preference for defensive sectors with real estate (+1.02%) and utilities (+0.22%) outperforming the rest of the pack. Over in Europe there was a moderately better performance however, with the STOXX 600 up +0.24%, and the German Dax (+0.87%) recovering somewhat from the previous day’s heavy losses. Futures are weak this morning though with contracts on the S&P 500 (-0.52%), NASDAQ 100 (-0.53%) and DAX (-1.15%) lower.

When it comes to the energy situation, there wasn’t much respite yesterday as we look forward to Friday’s meeting of EU energy ministers. Natural gas futures in Europe fell by -2.47% to €240 per megawatt-hour, and German power prices for next year were also down -6.02% to €536 per megawatt-hour. But relative to their levels from last year they are still incredibly elevated. One piece of news we did get was from German Chancellor Scholz, who said that when it came to a cap on power prices, “If we have our way, it will take weeks rather than months”. In the meantime, European sovereign bonds lost further ground, with yields on 10yr bunds (+7.4bps), OATs (+3.5bps) and BTPs (+3.3bps) all moving higher.

Here in the UK, Liz Truss was appointed as the new Prime Minister yesterday, succeeding Boris Johnson after three years in the job. In her initial speech in front of Downing Street, she said that action would be taken on the energy crisis this week, so that’s one to keep an eye out for, with reports across the press (as we previewed yesterday) indicating that bills will be frozen around current levels rather than going up in October. That came as gilts strongly underperformed their continental counterparts yesterday, with 10yr yields up by +15.7bps to 3.09%, which is their highest closing level since 2011. Interestingly however, there was a major steepening in the yield curve, with 2yr yields down -2.0bps as investors reacted to the prospect of lower short-term inflation in light of the potential freeze on bills.

Asian equity markets are weak this morning with the Hang Seng (-1.65%) leading losses followed by the Kospi (-1.50%) and the Nikkei (-0.95%). Over in Mainland China, the Shanghai Composite (-0.05%) and the CSI (-0.08%) are wavering between gains and losses in early trade.

The latest trade data coming out of China this morning showed exports growing at a slower pace in August (+7.1% y/y) against market forecast of a +13.0% increase and compared to July’s +18.0% rise as global demand continued to soften. At the same time, imports rose only +0.3%, falling short of expectations for a +1.1% gain. Elsewhere, Australia’s GDP expanded +0.9% in the second quarter, in-line with market expectations as consumers kept spending while energy exports boomed. The growth figure for the previous quarter (+0.7%) was downwardly revised though.

In FX news, the Japanese yen (-0.90%) this morning slid to a fresh 24-year low of 144.09 against the US dollar. Widening rate differential is the main reason for yen’s depreciation while yesterday’s better than expected US data probably also pushed the yen weaker. Separately, the People’s Bank of China (PBOC) fixed the yuan at 6.9160 to the dollar, its strongest bias on record and the 11th successive increase as the authorities continue to fight the global trend of a strong dollar against virtually every currency.

In energy markets, oil prices are trading lower in Asian trade with Brent futures down -1.45% at $91.48/bbl as the demand could remain under pressure amid China's Covid-19 lockdowns.

There wasn’t a great deal of other data yesterday, though in Europe we did get the German and UK construction PMIs for August, which were both in contractionary territory at 42.6 and 49.2 respectively. German factory orders in July also contracted by a faster-than-expected -1.1% (vs. -0.7% expected). Otherwise in the US, the final composite and services PMI for August painted quite a different picture to the ISM numbers, with the final services PMI revised down to 43.7 (vs. flash 44.1) and the final composite PMI revised down to 44.6 (vs. flash 45).

To the day ahead now, and there’s plenty on the central bank side, as the Bank of Canada announce their latest policy decision and the Fed release their Beige Book. We’ll also hear from Bank of England Governor Bailey, as well as the BoE’s Pill, Mann and Tenreyro as they testify before the Treasury Select Committee. In addition, there are scheduled remarks Fed officials, including Vice Chair Brainard, Vice Chair Barr, and Mester and Barkin. Otherwise, data releases include German industrial production and Italian retail sales for July.

The New Mexico Department of Health, in a statement, said that a man in Lincoln County “succumbed to the plague.” The man, who was not identified, was hospitalized before his death, officials said.

They further noted that it is the first human case of plague in New Mexico since 2021 and also the first death since 2020, according to the statement. No other details were provided, including how the disease spread to the man.

The agency is now doing outreach in Lincoln County, while “an environmental assessment will also be conducted in the community to look for ongoing risk,” the statement continued.

“This tragic incident serves as a clear reminder of the threat posed by this ancient disease and emphasizes the need for heightened community awareness and proactive measures to prevent its spread,” the agency said.

A bacterial disease that spreads via rodents, it is generally spread to people through the bites of infected fleas. The plague, known as the black death or the bubonic plague, can spread by contact with infected animals such as rodents, pets, or wildlife.

The New Mexico Health Department statement said that pets such as dogs and cats that roam and hunt can bring infected fleas back into homes and put residents at risk.

Officials warned people in the area to “avoid sick or dead rodents and rabbits, and their nests and burrows” and to “prevent pets from roaming and hunting.”

“Talk to your veterinarian about using an appropriate flea control product on your pets as not all products are safe for cats, dogs or your children” and “have sick pets examined promptly by a veterinarian,” it added.

“See your doctor about any unexplained illness involving a sudden and severe fever, the statement continued, adding that locals should clean areas around their home that could house rodents like wood piles, junk piles, old vehicles, and brush piles.

The plague, which is spread by the bacteria Yersinia pestis, famously caused the deaths of an estimated hundreds of millions of Europeans in the 14th and 15th centuries following the Mongol invasions. In that pandemic, the bacteria spread via fleas on black rats, which historians say was not known by the people at the time.

Other outbreaks of the plague, such as the Plague of Justinian in the 6th century, are also believed to have killed about one-fifth of the population of the Byzantine Empire, according to historical records and accounts. In 2013, researchers said the Justinian plague was also caused by the Yersinia pestis bacteria.

But in the United States, it is considered a rare disease and usually occurs only in several countries worldwide. Generally, according to the Mayo Clinic, the bacteria affects only a few people in U.S. rural areas in Western states.

Recent cases have occurred mainly in Africa, Asia, and Latin America. Countries with frequent plague cases include Madagascar, the Democratic Republic of Congo, and Peru, the clinic says. There were multiple cases of plague reported in Inner Mongolia, China, in recent years, too.

Symptoms

Symptoms of a bubonic plague infection include headache, chills, fever, and weakness. Health officials say it can usually cause a painful swelling of lymph nodes in the groin, armpit, or neck areas. The swelling usually occurs within about two to eight days.

The disease can generally be treated with antibiotics, but it is usually deadly when not treated, the Mayo Clinic website says.

“Plague is considered a potential bioweapon. The U.S. government has plans and treatments in place if the disease is used as a weapon,” the website also says.

According to data from the U.S. Centers for Disease Control and Prevention, the last time that plague deaths were reported in the United States was in 2020 when two people died.

Vetted by HousingWire | Our editors independently review the products we recommend. When you buy through our links, we may earn a commission.

Real estate is a vibrant, dynamic and competitive industry. From the thrill of a sale to the pursuit of new leads, it keeps you on your toes. That said, it can also be incredibly isolating, and it can be hard to stay motivated. As a way to deal with this, many agents and brokers seek out professional mentorship as a means to gain insight and level up their performance. Across the country, the best real estate coaches serve as valuable mentors who can help agents and brokers achieve the success they deserve.

“It’s really hard for independent business owners to get unbiased advice from themselves,” says Kyle Scott, President of SERHANT. Ventures. “So they need unbiased experts to work with that will help them grow their business — someone who has been there, who has done it, and who is able to see their business from both the 35,000-foot view and down in the weeds.”

A quick internet search will prove that real estate coaching programs are plentiful. Whether you’re looking to expand your team or client network or figure out how to delegate work so you can focus on the tasks you do best, a real estate coaching program could be a valuable launchpad. But when it comes to choosing the right one for your unique needs, there’s a lot to consider. Here, we highlight some of the best real estate coaches in the industry and their programs.

An unbiased view is worth millions. Often, we turn to our closest friends and family for guidance. Unfortunately, they’re usually not familiar with the ins and outs of the real estate industry and can’t provide you with the relevant feedback you need. As a result, many independent contractors rely on themselves, which generally doesn’t work either.

You can’t advise yourself, you’re too close to it. A coach works best for someone who is actually looking to grow their business, someone who is looking to put in the time and the energy to make a difference in achieving more income this year.

Hire a coach if you want to start taking your business to the next level for any reason — you want to make more money, have more freedom with your time, or stop riding the ins and outs of the commission cycle.President of SERHANT. Ventures

1. Sell It Like Serhant

Key Facts

Grown throughout the pandemic, the Sell It Like Serhant program has been carefully adapted to the current market. It follows a weekly and bi-weekly platform featuring one-on-one virtual coaching from Serhant’s proprietary video platform. After a half-hour or hour-long group meeting every week or every other week, participants follow actionable steps to help them grow their business. Thus far, more than 22,000 enrollees in 128 countries have been through the Sell It Like Serhant program.

What We Love

Serhant offers daily office hours so participants can pop into virtual sessions to ask questions or get expert advice between their regularly scheduled sessions. A community platform also allows participants to pass referrals to each other. Thus far, it seems to have worked: To date, participating agents have closed over $250 million of referral deals.

Pricing

There are different membership tiers, depending on the level of guidance you need. The introductory Real Estate Core Course starts at $497. Prices are higher for a more specific course or one with 1:1 coaching.

Who’s it Best For?

If you’re looking to build a memorable personal brand, SERHANT. is the way to go. “The number one differentiator about our program is we understand that as a real estate agent, you have one job: to generate leads,” says SERHANT. Ventures President Kyle Scott. “Our number one focus is helping you build a clear, compelling, memorable personal brand and put your lead generation on autopilot. So that way, you can do what you do best, which is build relationships and close deals.”

Visit Sell It Like Serhant

2. Tom Ferry International

Key Facts

For good reason, Ferry International refers to itself as the real estate industry’s leading coaching and training company. Focused on Ferry’s “8 Levels of Performance,” the programs are a staple of real estate coaching. Their new group coaching sessions cover various aspects of real estate sales.

Prospecting Bootcamp is a 14-hour program comprised of seven two-hour group coaching sessions, and includes a peer-to-peer collaboration space. It involves independent work pulled from training videos and downloadable resources.

Recruitment Roadmap consists of hour-long sessions each week for ten weeks. Completed over Zoom and through the Tom Ferry video platform, each group coaching program offers a high level of specialization.

Finally, their Fast Track program offers 12 interactive group coaching sessions designed to help new agents build the necessary skills to succeed — like mastering listing presentations and handling objections.

What we love

If you’re looking for the gold standard of real estate coaching, Tom Ferry has the goods to back up the bravado. Because of their many years in the biz, Tom Ferry has a huge base of coaches, which means there are plenty of options to find the program best suited for your specific needs.

Pricing

Tom Ferry’s Prospecting Bootcamp and Fast Track coaching programs cost $999 but can be broken down into three monthly payments. The Recruitment Roadmap group coaching costs $1,499 but can be split into three monthly payments of $500. Consider their free coaching consultation if you want to dip your toes in the water. Check out their customer reviews, where several coaching program alums rave about the program.

Who’s it Best For?

If you thrive in a group setting that allows you to feed off the energy of others, Tom Ferry might be right for you. Their group coaching programs are new and more affordable alternatives to often costly 1:1 coaching fees.

Visit Tom Ferry

3. Tim and Julie Harris

Key Facts

The dynamic duo of real estate coaching, Tim and Julie Harris are a major name in the industry. Under their business, Harris Real Estate Coaching, their programs are divided into three tiers: Premier, Premier Plus, and VIP, all of which rely on a user-friendly online platform.

Pricing

Premier platform costs $197 per month, but a 30-day free trial is available. Premier Plus costs $599 per month, while VIP costs $999 per month. Of course, their wildly successful podcast is a great free resource to tap into, as well as Tim and Julie’s many written contributions to HousingWire.

Who’s it Best For?

If you’re constantly on the go, the ability to access the course from any device is a major asset.

4. Candy Miles-Crocker

Key Facts

Newbies are welcome at Candy Miles Crocker’s program. Known as the “Real Life Realtor,” she’s the brain behind Real Life Real Estate Training. With a variety of courses in her offerings, including a plethora of self-paced online courses, Miles-Crocker gives new agents a leg-up on the rest.

What we love

Miles-Crocker is still an active agent, working with clients to close deals. Her 20+ years of experience practicing in Washington, D.C., Virginia and Maryland have helped her build “systems, strategies and scripts” that she shares with her coaching clients.

Pricing

The CORE Essentials Blueprint program retails for $1,597. Smaller, more specific courses, such as The Buyer Presentation, are priced at $347. While all pricing isn’t listed on her website, Miles-Crocker also offers a free course that includes her 6-point system for growth.

Who’s it Best For?

Miles-Crocker’s courses could be beneficial if you are new to agent life or looking to get your business reorganized. She even has one specifically for your first 30 days as a real estate agent.

5. Ashley Harwood

Key Facts

Boston-based Ashley Harwood inspires introverts with her convincing, heartfelt and high-touch approach to practicing real estate. Her very human, very relatable Move Over Extroverts coaching approach is the perfect antidote for cheerleader-style coaches that urge you to door-knock, chase down divorce leads or become a social media superstar.

What we love

Harwood is a licensed agent coaching agents week-in and week-out at no less than three Keller-Williams offices in the great Boston metro. We love her humanity, inspiring videos, and her latest enterpise — The Quiet Success Club. Inspired by Susan Cain’s New York Times bestseller Quiet, about the power of introverts, Harwood brings together a community of like-minded real estate agents wanting a more client-centric approach to succeeding as an agent.

Pricing

Join The Quiet Success Club for $45 per month (paid monthly) or get two months free when you pay for an annual subscription (for $450). The club is currently offering founding member pricing for $25 per month or $250, but it’s a limited-time offer available only under April 30, 2024. Or get a lifetime membership to Harwood’s suite of courses, called IntrovertU, for a one-time cost of $997.

Who’s it Best For?

Introverts, of course! While you may not count yourself as one, if you read Susan Cain’s book, you may unearth your more introverted traits — like recharging your battery by being alone. Ok, even if you don’t bask in solitude, Harwood promises a calming community where agents can be themselves, be seen, and where they don’t have to be the loudest voice in her mastermind group, purposefully (and quietly) designed to teach successful lead generation and other strategies.

6. Levi Lascsak

If you’re looking to improve your social media game, Levi Lascsak is the YouTube master. The author of Passive Prospecting specializes in helping real estate professionals embrace the video platform, and he does so in jam-packed, 2-day virtual events. Discover how he earned over $4 million in gross commission income as a new agent.

What we love

Lascsak’s social media marketing skills are top-of-the-line. While he may not be part of the traditional world of real estate coaching, Lascak’s ability to relate to younger audiences is an asset that Millennial and Gen Z agents might appreciate.

Pricing

The live, 2-day events are available at a discount for $47. But as you can expect, he’s got endless information available for free on YouTube.

Who’s it best for?

If you’re a digital native looking to pack a bunch of education into a short period, a Lascsak course is particularly beneficial.

7. Jess Lenouvel

Key Facts

Promising to help agents scale from six to seven figures, The Listings Lab founder Jess Lenouvel is the author of More Money, Less Hustle. A strong example of a coach with a significant understanding of social media, Lenouvel hosts vibrant live events that hype up the audience and prepare them to take their career to the next level.

What we Love

Lenouvel emphasizes the significant power of mindset to achieve one’s goals. She understands how quickly the market shifts and emphasizes staying on top of trends to succeed.

Lenouvel’s live events focus on messaging. For those looking to solidify their brand and develop a clear, concise message, her events might be what you need.

8. Buffini & Company

Key Facts

Another giant of the real estate coaching industry, Buffini & Company is one of the largest coaching and training companies in the United States. They have two major coaching programs: The Leadership Coaching program includes three monthly coaching calls, free admission to a 2-day conference, and curriculums and training led by Brian Buffini. There are also bi-monthly coaching sessions and a monthly web series with a live Q&A.

Buffini & Company also performs a REALstrengths profile — an in-depth personality assessment. In the One2One Coaching program, there are two coaching calls per month, a monthly marketing kit, the REALStrengths profile, and as with the SERHANT. program, Buffini features the Buffini Referral Network, allowing participants to send and receive referrals with other agents.

What We Love

Buffini coaches aren’t independent contractors. Instead, they’re full-time employees who go through intense training. Thus far, they’ve conducted 1.7 million coaching calls and more than one million hours of coaching.

Pricing

The Leadership Coaching program costs $1,499 a month. Private coaching, referred to as One2One Coaching, costs $549 per month. Two tiers of Referral Maker courses are available from $45 to $149 each per month.

Who’s it Best For?

Team spirit is the name of the game for Buffini’s Leadership Coaching program. If you’re a team leader looking to improve your coaching skills and assist your team in leveling up, the Leadership Coaching program might be right for you. If you want a more personalized path as a solo agent, the One2One Coaching program may be a better fit.

9. Vanda Martin

Key Facts

A popular name in the real estate coaching industry, Vanda Martin’s VIP Coaching Program follows three components: coaching, content, and community. Martin doesn’t shy away from mistakes – instead, she emphasizes avoiding indecision that puts you behind the pack.

What we love

Positive vibes are plentiful in Martin’s world, and her energy is tangible. Just check out her Instagram videos.

Pricing

Martin’s pricing isn’t listed.

Who’s it best for?

If you’re looking for a female leader who emphasizes loving your job and building habits that will take you to a greater level of success, Martin’s ability to convey those feelings is clear. Just check out the endless testimonials on her website.

9. Tat Londono

Key Facts

Tatiana Londono is the founder and CEO of Londono Realty Group Inc. The author of Real Estate Unfiltered, she offers a variety of programming that ranges from free templates to intensive coaching sessions. The Millionaire Realtor Membership provides weekly input from Londono, while the intensive Millionaire Real Estate Agent Coaching Program focuses on building 12-month objectives using a custom success action plan. It uses live programming and workshops with Londono herself, as well as an exclusive online community and referral network for members.

What we love

Londono’s keen sense of social media and her posts are a masterclass in how to boost your engagement on platforms like TikTok and Instagram. Don’t miss her takes on Taylor Swift’s real estate portfolio.

Londono’s programs specifically target agents who are looking to scale their business. If you’re struggling with lead generation or want to increase the number of views you’re racking up on social media, Londono is a valuable source within the industry.

10. Steve Shull

Key Facts

Steve Shull’s Performance Coaching focuses on using consistent execution to achieve your goals. With options ranging from 1:1 private coaching to small group coaching for 10 to 20 agents, the groups have 30-minute Zoom calls three times a day, but the number of sessions you choose to attend is up to you. Several self-directed courses are also available on the website, focusing on topics ranging from mindset to time blocking.

What we love

If you’re not positive you want to make the investment, Performance Coaching allows a 14-day free trial of daily accountability calls.

Pricing

Small group coaching costs $6,000 a year, and while 1:1 coaching prices aren’t listed online, you should prepare for a hefty price tag.

Who’s it Best For?

If you have a specific area you’re looking to improve upon, Performance Coaching offers coaches with unique areas of expertise, ranging from CRMs to business strategy. Tailoring your program to your greatest areas of weakness can help you become a more well-rounded agent.

11. Aaron Novello

Key Facts

Aaron Novello of Elite Real Estate Coaching has several programs tailor-made for agents looking to hone their craft. A Masterclass in Systems works to teach agents how to scale their real estate business, organize their team, and use programming like Follow Up Boss to manage their business.

The Role Play Mastermind is for agents looking to prepare themselves for tough discussions by working with a role-play partner for 15 to 30 minutes, five days a week. The group coaching option includes a variety of scripts Novello used to close on homes, as well as mindset guides, skill sheets, and expert guidance from experts in the field.

What we love

Novello’s exclusive accountability group allows active members and former coaching clients to share everything from guidance to motivation. If you’re looking to save money, Novello also has a free podcast available on YouTube.

If you struggle with having difficult conversations and are looking for solid templates to guide you, Novello’s Role Play Mastermind is a solid investment. The group coaching option emphasizes taking the educational portion and putting it into practice in the real world rather than just watching videos.

12. Krista Mashore Coaching

Key Facts

Filled with energy and known for popping up in the press, Krista Mashore is the mind behind Unstoppable Agent, her 3-day mastery class. It includes over 15 hours of coaching, group workshops, breakout sessions, and skill-building workshops to provide you with the skills to implement digital marketing successfully into your real estate business.

What we love

A positive attitude counts for a lot, and Mashore’s personality is a key component of the success of her course.

Pricing

Mashore’s accessibility is another one of her program’s best assets. Her 3-day class is currently priced at $47, but pricing occasionally varies.

Who’s it best for?

If you crave energy and enthusiasm, Krista Mashore has the goods. She’s also an expert on working in today’s low-inventory market, which is ideal for someone struggling with the current housing shortage. But she’s also got a good sense of humor, which shines through in her social media presence.

The full picture: The best real estate coaches for 2024

Hiring a top real estate coach goes far beyond just expanding your skills. While growing and educating yourself as you navigate your career is essential, hiring a coach is all about seeking to achieve more. Whether you’re looking to boost lead generation, build a solid personal brand, or make more commission income, having the input of a seasoned expert is a priceless step in the right direction. As you can see through the endless reviews and testimonials on coaches’ websites, agents who want to scale their business and take their profits to a higher level often seek the outside guidance of a coach. While the cost of hiring someone may be significant, the return on investment is equally as monumental.

Real estate coaching programs vary in price significantly. Most cost over $500 per month, with others charging several thousand dollars per month. “Oftentimes, it is the case that you get what you pay for,” said Kyle Scott, President of SERHANT. Ventures.

However, prices can also vary depending on the specific niche of real estate coaching you’re focusing on. The more specificity you’re seeking, the higher the financial investment. Of course, self-led courses are likely to cost much less.

Does your career feel stalled right now? Are you ready to take your career to the next level, but you’re not sure where to start? In a down market, you can channel your time and energy into actively improving your business skills so that you’ll be sufficiently prepared for when the market changes.

“When things pick up again, you’re ready to capture the climbing market,” says Scott. “If that’s the case, then the best time to embrace coaching is now. At the same time, a thriving market presents agents with new challenges, ranging from having to turn away business or being unable to service your existing business in a way you’re proud of,” Scott noted. “In that type of market, a real estate coach can help you determine what kind of junior agent or assistant would serve you best. How do I figure out how to manage my business in a way that I can keep up with the volume?”

Former Secretary of State Mike Pompeo said in a new interview that he’s not ruling out accepting a White House position if former President Donald Trump is reelected in November.

“If I get a chance to serve and think that I can make a difference ... I’m almost certainly going to say yes to that opportunity to try and deliver on behalf of the American people,” he told Fox News, when asked during a interview if he would work for President Trump again.

“I’m confident President Trump will be looking for people who will faithfully execute what it is he asked them to do,” Mr. Pompeo said during the interview, which aired on March 8. “I think as a president, you should always want that from everyone.”

He said that as a former secretary of state, “I certainly wanted my team to do what I was asking them to do and was enormously frustrated when I found that I couldn’t get them to do that.”

Mr. Pompeo, a former U.S. representative from Kansas, served as Central Intelligence Agency (CIA) director in the Trump administration from 2017 to 2018 before he was secretary of state from 2018 to 2021. After he left office, there was speculation that he could mount a Republican presidential bid in 2024, but announced that he wouldn’t be running.

President Trump hasn’t publicly commented about Mr. Pompeo’s remarks.

In 2023, amid speculation that he would make a run for the White House, Mr. Pompeo took a swipe at his former boss, telling Fox News at the time that “the Trump administration spent $6 trillion more than it took in, adding to the deficit.”

“That’s never the right direction for the country,” he said.

In a public appearance last year, Mr. Pompeo also appeared to take a shot at the 45th president by criticizing “celebrity leaders” when urging GOP voters to choose ahead of the 2024 election.

2024 Race

Mr. Pompeo’s interview comes as the former president was named the “presumptive nominee” by the Republican National Committee (RNC) last week after his last major Republican challenger, former South Carolina Gov. Nikki Haley, dropped out of the 2024 race after failing to secure enough delegates. President Trump won 14 out of 15 states on Super Tuesday, with only Vermont—which notably has an open primary—going for Ms. Haley, who served as President Trump’s U.S. ambassador to the United Nations.

On March 8, the RNC held a meeting in Houston during which committee members voted in favor of President Trump’s nomination.

“Congratulations to President Donald J. Trump on his huge primary victory!” the organization said in a statement last week. “I’d also like to congratulate Nikki Haley for running a hard-fought campaign and becoming the first woman to win a Republican presidential contest.”

Earlier this year, the former president criticized the idea of being named the presumptive nominee after reports suggested that the RNC would do so before the Super Tuesday contests and while Ms. Haley was still in the race.

Also on March 8, the RNC voted to name Trump-endorsed officials to head the organization. Michael Whatley, a North Carolina Republican, was elected the party’s new national chairman in a vote in Houston, and Lara Trump, the former president’s daughter-in-law, was voted in as co-chair.

“The RNC is going to be the vanguard of a movement that will work tirelessly every single day to elect our nominee, Donald J. Trump, as the 47th President of the United States,” Mr. Whatley told RNC members in a speech after being elected, replacing former chair Ronna McDaniel. Ms. Trump is expected to focus largely on fundraising and media appearances.

President Trump hasn’t signaled whom he would appoint to various federal agencies if he’s reelected in November. He also hasn’t said who his pick for a running mate would be, but has offered several suggestions in recent interviews.

In various interviews, the former president has mentioned Sen. Tim Scott (R-S.C.), Texas Gov. Greg Abbott, Rep. Elise Stefanik (R-N.Y.), Vivek Ramaswamy, Florida Gov. Ron DeSantis, and South Dakota Gov. Kristi Noem, among others.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}

{kind=link}

Uncategorized3 weeks ago

Uncategorized3 weeks ago

International6 days ago

International6 days ago

Uncategorized4 weeks ago

Uncategorized4 weeks ago

Uncategorized3 weeks ago

Uncategorized3 weeks ago

Uncategorized4 weeks ago

Uncategorized4 weeks ago

International6 days ago

International6 days ago

Uncategorized4 weeks ago

Uncategorized4 weeks ago

Uncategorized3 weeks ago

Uncategorized3 weeks ago