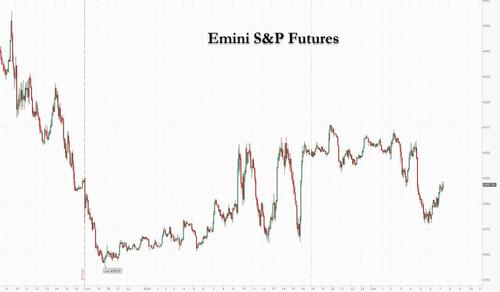

Futures Flat As Yen Discombobulation Extends To Record 13th Day

Futures Flat As Yen Discombobulation Extends To Record 13th Day

After some jerky rollercoaster moves in Monday’s illiquid trading session,…

Share this:

After some jerky rollercoaster moves in Monday's illiquid trading session, which jerked both higher and lower before closing modestly in the green, US futures resumed their volatility and at last check were trading flat after earlier in the session rising and falling; Nasdaq futures retreated 0.1%. as investors weighed the risks to economic growth from hawkish Federal Reserve comments. Stocks in Europe dropped as markets reopened after the Easter holiday, while bonds around the globe slumped as investors weighed the prospect of aggressive policy action to curb inflation. Asian stocks also dropped as did oil, while the dollar extended its gains . Treasuries extended declines, with the 10-year yield hitting a fresh three-year peak north of 2.90%. German and U.K. 10-year yields climbed to the highest since 2015 as bonds across Europe plunged.

The grotesque farce that is MMT came one step closer to total collapse as the yen dropped for a record 13th day, its longest-losing streak in at least half a century with the credibility of the BOJ - that central bank that launched MMT, QE and NIRP - now hanging by a thread. It wasn't all bad news however, because with the yen losing more of its purchasing power, Japanese stocks gained.

Disruptions to supply chains from China’s lockdowns and to commodity flows from the war are keeping pressure on central banks to rein in runaway prices at a time when global growth is tipped to slow. The World Bank cut its forecast for global economic expansion this year on Russia’s invasion.

Meanwhile, investors - already betting on an almost half-point Federal Reserve rate increase next month - continue monitoring comments from policy makers as prospects of monetary tightening weigh on the sentiment. St Louis Fed President James Bullard said the central bank needs to move quickly to raise interest rates to around 3.5% this year with multiple half-point hikes and that it shouldn’t rule out rate increases of 75 basis points. The last increase of such magnitude was in 1994.

“The Bullard comments really encapsulate the quandary that many of the world’s central banks have found themselves in,” said Jeffrey Halley, a senior markets analyst at Oanda. “Luckily, they have plenty of excuses in the shape of the pandemic and the Ukraine war. Central banks can now play catchup, hike aggressively and run the risk of recessions. Getting the pain over and done may be the least worst option.”

Over in Ukraine, President Volodymyr Zelenskiy said Monday that Russian forces had begun the campaign to conquer the Donbas region in Ukraine’s east. Here are all the latest news and headlines over Ukraine:

- Russia's Belgorod provincial Governor said a village near the Ukrainian border was struck by Ukraine, according to RIA. However, Sputnik noted that no casualties were reported.

- Russian Foreign Minister Lavrov says another stage of its operation is beginning

- Russian Defence Ministry is calling on Ukrainian and foreign fighters to leave the metallurgical plant in Mauripol without arms and ammunition today, via Reuters; adding, the US and other Western countries do everything to drag out the Ukrainian military operation.

- White House said US President Biden will hold a call with allies and partners on Tuesday to discuss continued support for Ukraine and efforts to hold Russia accountable, according to Reuters.

- French Finance Minister Le Maire says an embargo on Russian oil is being worked on, adds that we have always said with President Macron that we want such an embargo, via Reuters; aims to convince the EU on such an embargo in the coming weeks.

- Russia's Gazprom has not booked gas transit capacity via Yamal-Europe pipeline for May.

In premarket trading, Zendesk rose 4.1% in premarket trading after a report about the software company hiring a new adviser to explore a potential sale. NXP Semiconductors dropped 2.5% in premarket trading after Citi cut the stock to neutral from buy, saying in note that its thesis on margin expansion has played out. Other notable premarket movers include:

- Amazon (AMZN US) could be active as Barclays analyst Ross Sandler is upbeat on it heading into 1Q results and sees gross merchandise value (GMV) accelerating on a 1-yr basis in 2Q.

- Netgear (NTGR US) dropped 11% in extended trading Monday after reporting preliminary net revenue for the first quarter that trailed the average analyst estimate.

- Super Micro Computer (SMCI US) climbed 15% after the maker of server and storage systems reported fiscal 3Q preliminary profit and sales that beat the average analyst estimate.

- Acadia (ACAD US) shares declined in postmarket after it said Phase 2 clinical trial of the efficacy and safety of ACP-044 for acute pain following bunion removal surgery didn’t meet the primary endpoint.

- WeWork (WE US) advanced in postmarket trading Monday as coverage starts with an overweight rating and $10 price target at Piper Sandler, which highlights that the co-working company is on track to achieve profitability by late 2023 or early 2024.

European stocks slumped with the Stoxx 600 dropping 1.1% led lower by healthcare and media shares as traders returned from a lengthy Easter holiday, with technology stocks also underperforming; the energy sub-index the only sector gaining in Europe in Tuesday trading as investors digest the recent rally in crude prices. Meanwhile in Russia equities fell for a second day with the benchmark MOEX Index dropping as Russia’s military pressed on with its offensive in southern and eastern Ukraine, with President Volodymyr Zelenskiy saying Moscow had launched a new campaign focused on conquering the Donbas region. The MOEX dropped as much as 3.2%, adding to declines of 3.4% on Monday with Lukoil, Sberbank and Gazprom leading losses. Here are some of Europe's biggest movers:

- TotalEnergies rises as much as 3.6% to the highest level since the end of last month after reporting higher refining margins, as well as better liquids and gas prices

- Spectris gains as much as 6.3% after the firm said it will sell its Omega Engineering business to Arcline Investment Management for $525m, and also announced a GBP300m buyback program

- Carrefour climbs as much as 3% as Berenberg upgrades to buy from hold, saying that higher inflation is making the food retail sector more challenging, but will also reveal outperformers

- Virbac advances as much as 11% after the French maker of veterinary products raised the top end of its sales growth forecast. Oddo upgraded the stock to outperform.

- Food delivery shares lead European tech lower as U.S. Treasury yields touch new highs following a hawkish comment from a Federal Reserve President, Just Eat Takeaway -4.5%; Delivery Hero -2.5%

- European consumer staples and luxury stocks fall as markets reopen after a 4-day break, with higher inflation and looming interest-rate hikes at the forefront of investor worries

- L’Oreal, which reports 1Q sales after the market close today, slumps as much as 4.1%; LVMH decreases as much as 1.9%, Hermes down as much as 4%

- Wizz Air drops as much as 6.1% after being downgraded to reduce at HSBC, with the broker saying the low-cost airline’s decision to not hedge its fuel prior to the outbreak of the Ukraine war could bite

- Adevinta falls as much as 9.8% after Bank of America downgraded to underperform from neutral on Thursday, due to the classifieds business’s large exposure to the automotive sector

- Elior and SSP Group shares retreat after both are downgraded to hold from buy at Deutsche Bank on downside risks; Elior down as much as 3.7%, SSP as much as 6.1%

Earlier in the session, Hong Kong technology names declined on ongoing concerns over regulation. China dropped as investors assessed measures to tackle economic headwinds from Covid-led lockdowns.

Asian stocks declined for a third day, as continued concerns over China’s regulatory crackdowns and the prospect of aggressive monetary-policy tightening by the Federal Reserve weighed on sentiment. The MSCI Asia Pacific Index fell as much as 0.6%, with Chinese technology shares including Tencent and Alibaba the biggest drags after Beijing announced a “clean-up” of the video industry. Hong Kong stocks were the worst performers around the region as trading resumed after Easter holidays, while equities rose in Japan and South Korea. The People’s Bank of China on Monday announced measures to help businesses hit by Covid-19, as the latest economic data started to show the impact of extended lockdowns.

Investors are awaiting further easing with the release of China’s loan prime rates on Wednesday, after the central bank last week announced a smaller-than-expected cut in the reserve requirement for banks. Whether policy support measures will “flow significantly into the economy will be on watch,” and market participants may “want to see signs of recovery before taking on more risks in that aspect,” said Jun Rong Yeap, a strategist at IG Asia Pte. Hawkish Fed member James Bullard raised the possibility of a 75 basis-point hike in interest rates. Concerns of inflation and moves by the Fed and other central banks to fight it have driven the recent global equity selloff, with the Asian benchmark down about 11% this year.

In China, markets are also awaiting the release of banks’ benchmark lending rates on Wednesday after the People’s Bank of China reduced the reserve requirement ratio for most banks Friday but refrained from cutting interest rates. The latest policy measures “have really highlighted easing is required,” Gareth Nicholson, Nomura chief investment officer and head of discretionary portfolio management, said on Bloomberg Television. “The markets don’t believe enough has been done and they’re going to have to step it up.”

Japanese equities gained, rebounding after two days of losses as the continued weakening of the yen bolstered exporters. Electronics and auto makers were the biggest boosts to the Topix, which rose 0.8%. Tokyo Electron and Advantest were the largest contributors to a 0.7% rise in the Nikkei 225. The yen extended declines to a 13th straight day, its longest losing streak on record, falling through 128 per dollar.

Australian stocks also advanced, with the S&P/ASX 200 index rising 0.6% to close at 7,565.20 as trading resumed following Easter holidays. The energy and materials sectors gained the most. Cleanaway was among the biggest gainers, climbing the most since April 2021 after a media report said KKR has been preparing an offer for the Australian waste management company. City Chic Collective was the biggest decliner, falling to its lowest since December 2020. In New Zealand, the S&P/NZX 50 index fell 0.5% to 11,835.88.

In rates, Treasuries slipped, with yields rising by as much as 6bps in the long end of the curv, however they traded off session lows reached during European morning as those markets reopened after a four-day holiday. Yields beyond the 5-year are higher by 3bp-4bp, 10-year by 3.3bp at 2.89% after rising above 2.90% earlier; U.K. and most euro-zone 10-year yields are higher by at least 5bp, correcting spreads vs U.S. created Monday when those markets were closed. The yield curve continues to steepen; 7- to 30-year yields reached new YTD highs, nearly 3% for 30-year. Japanese government bonds were mixed. Focal points for U.S. session are corporate new-issue calendar expected to include more financial offerings and comments by Chicago Fed President Evans.

In FX, the Bloomberg Dollar Spot Index was little changed, after earlier rising to its highest since July 2020, and the dollar fell against almost all of its Group-of-10 peers. Commodity-related currencies and the Swedish krona were the best performers while the Japanese currency fell versus all of its G-10 peers. The yen extended its longest-losing streak in at least half a century, and touched 128.45 per dollar, its weakest level since May 2002, amid concerns over further widening in yield differentials. The euro reversed an Asia session loss even amid another round of bearish option bets in the front-end due to political risks. Bunds extended a slump, underperforming Treasuries, before a five-year debt sale and as money markets increased ECB tightening wagers. The Australian dollar surged against the yen to levels last seen almost seven year ago. RBA minutes said quicker inflation and a pickup in wage growth have moved up the likely timing of the first interest-rate increase since 2010. The New Zealand dollar also advanced; RBNZ Governor Orr reiterated the central bank’s aggressive rate stance. The pound was little changed and gilts slid, sending the U.K. 10-year yield to the highest since 2015 as money markets bet on a faster BOE policy tightening path.

In commodities, crude futures declined. WTI trades within Monday’s range, falling 1.5% to trade around $106. Brent falls 1.5% to ~$111. Most base metals trade in the green; LME copper rises 1.4%, outperforming peers. Spot gold is down 0.1% to $1,977/oz.

Bitcoin was flat and holding steady at the bottom of the sessions USD 40.6-41.2k parameters.

Looking at the day ahead, data is light with US March building permits, housing starts, and Canada March existing home sales. The IMF will also release their 2022 World Economic Outlook.

Market Snapshot

- S&P 500 futures up 0.3% to 4,401.75

- STOXX Europe 600 down 0.8% to 456.07

- MXAP down 0.4% to 171.55

- MXAPJ down 0.3% to 570.60

- Nikkei up 0.7% to 26,985.09

- Topix up 0.8% to 1,895.70

- Hang Seng Index down 2.3% to 21,027.76

- Shanghai Composite little changed at 3,194.03

- Sensex up 0.5% to 57,438.93

- Australia S&P/ASX 200 up 0.6% to 7,565.21

- Kospi up 1.0% to 2,718.89

- German 10Y yield little changed at 0.91%

- Euro up 0.2% to $1.0808

- Brent Futures down 0.7% to $112.40/bbl

- Brent Futures down 0.7% to $112.40/bbl

- Gold spot up 0.1% to $1,979.91

- U.S. Dollar Index little changed at 100.73

Top Overnight News from Bloomberg

- Record numbers of U.K. business leaders expect operating costs to soar this year as inflation proves more sticky than thought, according to a survey by Deloitte

- French President Emmanuel Macron led his rival Marine Le Pen 55.5% to 44.5% ahead of the run-off presidential election set for April 24, according to a polling average calculated by Bloomberg on April 19. The gap between them has widened from the 8.2 percentage points recorded on April 15

- Nationalist leader Marine Le Pen never led in the three campaigns she’s run for France’s top job, but a protectionist stance on economic issues in recent years has allowed her to reach some voters who traditionally backed left- wing candidates

- China’s central bank announced a spate of measures to help an economy which has been hit by lockdowns to control the current Covid outbreak, but the focus on boosting credit likely means the chances for broad-based easing are shrinking

A more detailed breakdown courtesy of Newsquawk

Asia-Pac stocks saw a mixed performance as more markets reopened and trade picked up from the holiday lull. ASX 200 gained on return from the extended weekend, led by strength in commodity-related sectors and top-weighted financials. Nikkei 225 briefly reclaimed the 27k level as continued currency depreciation underscored the Fed and BoJ policy divergence. Hang Seng was pressured as it took its first opportunity to react to the PBoC’s underwhelming policy decisions and with tech hit after Shanghai's market regulator summoned 12 e-commerce platforms including Meituan on price gouging during COVID outbreaks. Shanghai Comp was choppy as participants mulled over the latest virus-related developments including an increase in Shanghai deaths and the lockdown of five districts in the steel producing hub of Tangshan, although policy support pledges from the PBoC and NDRC ultimately provided a cushion.

Top Asian News

- Japan’s Stepped-Up Warnings Fail to Stem Yen’s Slide Past 128

- China’s Promises to Support Covid-Hit Economy Fail to Impress

- China Tech Stocks Slump on Didi Delisting Plan, Regulation Woes

- Sri Lanka Officially Requests Rapid IMF Funds Amid Crisis

European bourses are negative on the session but were choppy and rangebound for much of the morning before dropping further amid renewed yield upside, Euro Stoxx 50 -1.4%. Stateside, US futures have given up their initial positive performance and are now lower across the board, ES -0.3%, and the NQ -0.4% lags given yield action; session is focused on Fed speak and earnings with NFLX due. Truist Financial Corp (TFC) Q1 2022 (USD): Adj. EPS 1.23 (exp. 1.10), Revenue 5.32bln (exp. 5.47bln)

Top European News

- Stellantis Idles One of Russia’s Last Auto Plants Left Running

- Commodities Trader Gunvor Doubled Profits on Hot Gas Market

- European Gas Falls to Lowest Since Russian Invasion of Ukraine

- Credit Suisse’s Top China Banker Tu Steps Aside for New Role

FX:

- USD/JPY breezes through more option barriers and disregards more chat from Japanese officials about demerits of Yen weakness; pair pulls up just pips shy of 128.50.

- DXY tops 101.000 in response before pulling back as Europeans return from long Easter break.

- Aussie outperforms as RBA minutes highlight more recognition about inflationary environment externally and internally.

- Kiwi next best G10 currency as RBNZ Governor Orr underlines that policy is being weighted towards anchoring inflation expectations; AUD/USD hovers under 0.7400 and NZD/USD around 0.6750

- Euro trying to hold near 1.0800 where 1.3bln option expiry interest rolls off at the NY cut, Pound regains 1.3000 plus status and Loonie pivots 1.2600 on the eve of Canadian CPI.

- Yuan close to 6.4000 ahead of Chinese LPR rate verdict on Wednesday amidst heightened easing expectations.

Fixed income:

- EU bonds correct lower after long Easter holiday weekend then pick up the baton to push US Treasuries even lower; Bunds giving up 154.00 and dropping to a 153.58 trough in short order and USTs lower to the tune of 7 ticks.

- Decent demand for German Bobls, but high price in terms of yield and a larger retention - limited relief seen in the benchmark, given broader action.

- Benchmark 10 year cash rates approaching new psychological marks of 1.0%, 2.0% and 3.0% in Bunds, Gilts and T-notes respectively.

Commodities

- Crude benchmarks are softer after yesterday's firmer session, which was driven by Libya supply concerns, currently moving in tandem with broader equity performance awaiting fresh geopolitical developments.

- Currently, WTI and Brent are modestly above session lows which reside sub USD 106/bbl and USD 111/bbl respectively.

- OPEC+ produced 1.45mln BPD below targets during March, via Reuters citing a report; compliance 157% (132% in February).

- Spot gold and silver are contained with the yellow metal pivoting USD 1975/oz while copper derives further impetus from Peru protest activity.

- MMG said protesters at the Las Bambas copper mine alleged a failure to comply with social investment commitments, while it rejected the allegations and noted that Las Bambas will be unable to continue copper output as of April 20th.

US Event Calendar

- 08:30: March Building Permits MoM, est. -2.4%, prior -1.9%, revised -1.6%

- 08:30: March Housing Starts MoM, est. -1.6%, prior 6.8%

- 08:30: March Building Permits, est. 1.82m, prior 1.86m, revised 1.87m

- 08:30: March Housing Starts, est. 1.74m, prior 1.77m

Central Bank Speakers

- 12:05: Fed’s Evans Speaks to Economic Club of New York

DB's Tim Wessel concludes the overnight wrap

Welcome back to another holiday-shortened week for many markets. What it lacks in tier one data releases, it makes up for with heavy hitting central bank speakers and a core European Presidential election. We’re also wading into the thick of earnings season, while the on-running war in Ukraine has the potential to tip markets in any direction at the speed of a headline.

Starting with the central bankers, President Lagarde and Chair Powell will sit on an IMF panel to discuss the global economy in the last Fed communications before their May meeting blackout period. The Fed has primed markets for a +50bp hike in May, and pricing has obliged, with futures placing a 98.1% probability of a +50bp rise, along with +246bps of tightening for the entire year. Governor Bailey won’t miss out on the action and is also delivering an address Thursday. Other Fed regional Presidents will speak throughout the week, with the Fed’s Beige Book due Wednesday. The IMF, meanwhile, will release their global outlook later today. As a reminder, DB Research updated our World Outlook earlier this month, where we are calling for recessions in the US and the euro area within the next two years. Plenty more in the link here.

US earnings season will diversify beyond the financials-heavy slate from last week. Today is a nice microcosm of the change up, showcasing earnings from Johnson & Johnson, Halliburton, Hasbro, Lockheed Martin, Netflix, and IBM.

On data the rest of the week, we’ll receive German PPI and Canadian CPI Wednesday, along with global PMIs Friday. US housing data dot the rest of the week, as we unravel the competing threads of tight inventories, heightened demand, and supply constraints, against higher mortgage rates on housing activity.

Finally, the second round of the French Presidential election is this coming Sunday. Politico’s latest polling aggregates still have incumbent President Macron outpacing Marine Le Pen by around 9% in Sunday’s runoff. Our Europe team has their takeaways from the first round here.

The ECB’s April meeting garnered top billing during the EMR’s long weekend (our Euro econ team’s full review here). Overlaid on an inflationary backdrop, the Governing Council is weighing the downside risk to growth against the upside risk to inflation stemming from the recent conflict. While uncertainty pervades, the latter risks are more pressing, which drove their decision to signal net APP purchases would end in Q3, paving the way for policy rate liftoff later this year. Our economists expect the last APP net purchases will occur in July, with the risk skewed toward June, with a +25bp liftoff in September. Markets have +11.8bps of hikes priced by July, +35.6bps by September, and +64.4bps of hikes through 2022.

There was no new tool to address market fragmentation, though the ECB signaled imperfect policy transmission would not stand in the way of lifting rates and a new tool would be created if need be. 10yr BTP spreads were -5.0bps tighter to bunds over the week, and +3.3bps wider the day of the meeting.

Elsewhere, as mentioned, a suite of US financials reported. Looking through the releases, it seems most FICC trading desks benefitted from the quarter of volatility and higher rates are set to improve margins. However, the prospect of an economic slowdown or potential exposures to war fallout cloud the outlook. S&P 500 financials were -2.65% lower on the week.

Taking a longer view of last week, sovereign yields marched higher on the back of tighter expected monetary policy, and the yield curve’s recent sharp steepening continued. 10yr Treasury and bund yields respectively increased +12.8bps (+12.9bps Thursday, +2.5bps yesterday) and +13.5bps (+7.6bps Thursday) with continued heightened volatility. Real yields drove most of the gains in the US (+10.2bps for the week, +4.6bps Thursday, -1.0bps yesterday), ending the week at -0.09%, the highest level since early 2020. 10yr real yields are now +101.7bps higher this year, having had their climb only briefly interrupted by Russia’s invasion of Ukraine. The 2s10s Treasury curve steepened +19.1bps (+2.5bps Friday, +2.9bps yesterday).

There were not many positives to hang onto in Ukraine last week. Negotiation progress turned sour, President Biden labeled Russia’s invasion a ‘genocide’, and the US upped the provision of heavy weaponry to Ukraine, which was met with a diplomatic warning from Russia. The EU also pledged additional aid, while Finland began the process of applying for NATO membership and Sweden is reportedly considering the same. On the ground, Russian forces continued their eastern offensive, surrounding Ukrainian defenders of the port city Mariupol.

Along with the drag on sentiment, the International Energy Agency warned the full disruption to Russian oil supply had yet to bind, with as much as 3 million barrels of oil per day coming offline starting in May. Brent crude futures therefore climbed +8.7% (+2.68% Thursday, +1.31% yesterday), and closed yesterday at $113.16/bbl, their highest level in three weeks.

The S&P 500 fell -2.13% (-1.21% Thursday, -0.02% yesterday in a very quiet session) while the STOXX 600 managed to lose just -0.2% after a +0.7% rally Thursday into the holiday. In the S&P, energy (+3.53%) outperformed given the oil spike, while large cap stocks underperformed on the valuation hit wrought by rising yields, with FANG+ falling -4.81% (-3.16% Thursday, +0.25% yesterday).

Asian equity markets are ambivalent about returning after a long holiday, with the Hang Seng (-2.80%) leading regional losses. Mainland Chinese stocks are faring better, with the CSI dipping -0.38% while the Shanghai Composite is -0.03% lower. This, following the PBOC announcing yesterday increased financial support for industries, businesses, and people affected by Covid-19. Elsewhere, the Nikkei (+0.12%) and the Kospi (+0.90%) are up. Outside of Asia, S&P 500 (+0.20%) and Nasdaq (+0.28%) futures are both trading higher.

The RBA minutes overnight signaled they are not too far from joining the global tightening cycle, as they expect inflation to further increase above target.

The yen extended its depreciation streak against the US dollar, falling -0.58% to 127.73 per dollar, the weakest level since May 2002, as diverging monetary policy paths take their toll.

Oil prices and 10yr Treasury yields are little changed overnight; brent futures are +0.19% higher, while 10yr Treasury yields are -1.5bps lower.

To the day ahead, data is light on top of the aforementioned earnings, with US March building permits, housing starts, and Canada March existing home sales. The IMF will also release their 2022 World Economic Outlook.

Spread & Containment

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

Uncategorized

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Authored by Sam Bourgi via CreditNews.com,

Homeownership…

Share this:

Authored by Sam Bourgi via CreditNews.com,

Homeownership is one of the key pillars of the American dream. But for many families, the idyllic fantasy of a picket fence and backyard barbecues remains just that—a fantasy.

Thanks to elevated mortgage rates, sky-high house prices, and scarce inventory, millions of American families have been locked out of the opportunity to buy a home in many cities.

To shed light on America’s housing affordability crisis, Creditnews Research ranked the 50 most populous cities by the percentage of neighborhoods within reach for the typical married-couple household to buy a home in.

The study reveals a stark reality, with many cities completely out of reach for the most affluent household type. Not only that, the unaffordability has radically worsened in recent years.

Comparing how affordability has changed since Covid, Creditnews Research discovered an alarming pattern—indicating consistently more unaffordable housing in all but three cities.

Fortunately, there’s still hope for households seeking to put down roots in more affordable cities—especially for those looking beyond Los Angeles, New York, Boston, San Jone, and Miami.

The typical American family has a hard time putting down roots in many parts of the country. In 11 of the top 50 cities, at least 50% of neighborhoods are out of reach for the average married-couple household. The affordability gap has widened significantly since Covid; in fact, no major city has reported an improvement in affordability post-pandemic.

Sam Bourgi, Senior Analyst at Creditnews

Key findings

-

The most unaffordable cities are Los Angeles, Boston, St. Louis, and San Jose; in each city, 100% of neighborhoods are out of reach for for married-couple households earning a median income;

-

The most affordable cities are Cleveland, Hartford, and Memphis—in these cities, the typical family can afford all neighborhoods;

-

None of the top 50 cities by population saw an improvement in affordable neighborhoods post-pandemic;

-

California recorded the biggest spike in unaffordable neighborhoods since pre-Covid;

-

The share of unaffordable neighborhoods has increased the most since pre-Covid in San Jose (70 percentage points), San Diego (from 57.8 percentage points), and Riverside-San Bernardino (51.9 percentage points);

-

Only three cities have seen no change in housing affordability since pre-Covid: Cleveland, Memphis, and Hartford. They’re also the only cities that had 0% of unaffordable neighborhoods before Covid.

Cities with the highest share of unaffordable neighborhoods

With few exceptions, the most unaffordable cities for married-couple households tend to be located in some of the nation’s most expensive housing markets.

Four cities in the ranking have an unaffordability percentage of 100%—indicating that the median married-couple household couldn’t qualify for an average home in any neighborhood.

The following are the cities ranked from the least affordable to the most:

-

Los Angeles, CA: Housing affordability in Los Angeles has deteriorated over the last five years, as average incomes have failed to keep pace with rising property values and elevated mortgage rates. The median household income of married-couple families in LA is $117,056, but even at that rate, 100% of the city’s neighborhoods are unaffordable.

-

St. Louis, MO: It may be surprising to see St. Louis ranking among the most unaffordable housing markets for married-couple households. But a closer look reveals that the Mound City was unaffordable even before Covid. In 2019, 98% of the city’s neighborhoods were unaffordable—way worse than Los Angeles, Boston, or San Jose.

-

Boston, MA: Boston’s housing affordability challenges began long before Covid but accelerated after the pandemic. Before Covid, married couples earning a median income were priced out of 90.7% of Boston’s neighborhoods. But that figure has since jumped to 100%, despite a comfortable median household income of $172,223.

-

San Jose, CA: Nestled in Silicon Valley, San Jose has long been one of the most expensive cities for housing in America. But things have gotten far worse since Covid, as 100% of its neighborhoods are now out of reach for the average family. Perhaps the most shocking part is that the median household income for married-couple families is $188,403—much higher than the national average.

-

San Diego, CA: Another California city, San Diego, is among the most unaffordable places in the country. Despite boasting a median married-couple household income of $136,297, 95.6% of the city’s neighborhoods are unaffordable.

-

San Francisco, CA: San Francisco is another California city with a high married-couple median income ($211,585) but low affordability. The percentage of unaffordable neighborhoods for these homebuyers stands at 89.2%.

-

New York, NY: As one of the most expensive cities in America, New York is a difficult housing market for married couples with dual income. New York City’s share of unaffordable neighborhoods is 85.9%, marking a 33.4% rise from pre-Covid times.

-

Miami, FL: Partly due to a population boom post-Covid, Miami is now one of the most unaffordable cities for homebuyers. Roughly four out of five (79.4%) of Miami’s neighborhoods are out of reach price-wise for married-couple families. That’s a 34.7% increase from 2019.

-

Nashville, TN: With Nashville’s population growth rebounding to pre-pandemic levels, the city has also seen greater affordability challenges. In the Music City, 73.7% of neighborhoods are considered unaffordable for married-couple households—an increase of 11.9% from pre-Covid levels.

-

Richmond, VA: Rounding out the bottom 10 is Richmond, where 55.9% of the city’s 161 neighborhoods are unaffordable for married-couple households. That’s an 11.9% increase from pre-Covid levels.

Cities with the lowest share of unaffordable neighborhoods

All the cities in our top-10 ranking have less than 10% unaffordable neighborhoods—meaning the average family can qualify for a home in at least 90% of the city.

Interestingly, these cities are also outside the top 15 cities by population, and eight are in the bottom half.

The following are the cities ranked from the most affordable to the least:

-

Hartford, CT: Hartford ranks first with the percentage of unaffordable neighborhoods at 0%, unchanged since pre-Covid times. Married couples earning a median income of $135,612 can afford to live in any of the city’s 16 neighborhoods. Interestingly, Hartford is the smallest city to rank in the top 10.

-

Memphis, TN: Like Hartford, Memphis has 0% unaffordable neighborhoods, meaning any married couple earning a median income of $101,734 can afford an average homes in any of the city’s 12 neighborhoods. The percentage of unaffordable neighborhoods also stood at 0% before Covid.

-

Cleveland, OH: The Midwestern city of Cleveland is also tied for first, with the percentage of unaffordable neighborhoods at 0%. That means households with a median-couple income of $89,066 can qualify for an average home in all of the city’s neighborhoods. Cleveland is also among the three cities that have seen no change in unaffordability compared to 2019.

-

Minneapolis, MN: The largest city in the top 10, Minneapolis’ share of unaffordable neighborhoods stood at 2.41%, up slightly from 2019. Married couples earning the median income ($149,214) have access to the vast majority of the city’s 83 neighborhoods.

-

Baltimore, MD: Married-couple households in Baltimore earn a median income of $141,634. At that rate, they can afford to live in 97.3% of the city’s 222 neighborhoods, making only 2.7% of neighborhoods unaffordable. That’s up from 0% pre-Covid.

-

Louisville, KY: Louisville is a highly competitive market for married households. For married-couple households earning a median wage, only 3.6% of neighborhoods are unaffordable, up 11.9% from pre-Covid times.

-

Cincinnati, OH: The second Ohio city in the top 10 ranks close to Cleveland in population but has a much higher median married-couple household income of $129,324. Only 3.6% of the city’s neighborhoods are unaffordable, up slightly from pre-pandemic levels.

-

Indianapolis, IN: Another competitive Midwestern market, only 4.4% of Indianapolis is unaffordable, making the vast majority of the city’s 92 neighborhoods accessible to the average married couple. Still, the percentage of unaffordable neighborhoods before Covid was less than 1%.

-

Oklahoma City, OK: Before Covid, Oklahoma City had 0% neighborhoods unaffordable for married-couple households earning the median wage. It has since increased to 4.69%, which is still tiny compared to the national average.

-

Kansas City, MO: Kansas City has one of the largest numbers of neighborhoods in the top 50 cities. Its married-couple residents can afford to live in nearly 95% of them, making only 5.6% of neighborhoods out of reach. Like Indiana, Kansas City’s share of unaffordable neighborhoods was less than 1% before Covid.

The biggest COVID losers

What's particularly astonishing about the current housing market is just how quickly affordability has declined since Covid.

Even factoring in the market correction after the 2022 peak, the price of existing homes is still nearly one-third higher than before Covid. Mortgage rates have also more than doubled since early 2022.

Combined, the rising home prices and interest rates led to the worst mortgage affordability in more than 40 years.

Against this backdrop, it’s hardly surprising that unaffordability increased in 47 of the 50 cities studied and remained flat in the other three. No city reported improved affordability in 2024 compared to 2019.

The biggest increases are led by San Jose (70 percentage points), San Diego (57.8 percentage points), Riverside-San Bernardino (51.9 percentage points), Sacramento (43 percentage points), Orlando (37.4 percentage points), Miami (34.7 percentage points), and New York City (33.4 percentage points).

The following cities in our study are ranked by the largest percentage point change in unaffordable neighborhoods since pre-Covid:

Uncategorized

Your financial plan may be riskier without bitcoin

It might actually be riskier to not have bitcoin in your portfolio than it is to have a small allocation.

Share this:

{kind=link}

{kind=link}

{kind=link}

This article originally appeared in the Sound Advisory blog. Sound Advisory provide financial advisory services and are specialize in educating and guiding clients to thrive financially in a bitcoin-powered world. Click here to learn more.

“Belief is a wise wager. Granted that faith cannot be proved, what harm will come to you if you gamble on its truth and it proves false? If you gain, you gain all; if you lose, you lose nothing. Wager, then, without hesitation, that He exists.”

- Blaise Pascal

Blaise Pascal only lived to age 39 but became world-famous for many contributions in the fields of mathematics, physics, and theology. The above quote encapsulates Pascal’s wager—a philosophical argument for the Christian belief in the existence of God.

The argument's conclusion states that a rational person should live as though God exists. Even if the probability is low, the reward is worth the risk.

Pascal’s wager as a justification for bitcoin? Yes, I’m aware of the fallacies: false dichotomy, appeal to emotion, begging the question, etc. That is not the point. The point is that binary outcomes instigate extreme results, and the game theory of money suggests that it’s a winner-take-all game.

The Pascalian investor: A rational approach to bitcoin

Humanity’s adoption of “the best money over time” mimics a series of binary outcomes—A/B tests.

Throughout history, inferior forms of money have faded as better alternatives emerged (see India’s failed transition to a gold standard). And if bitcoin is trying to be the premier money of the future, it will either succeed or it won’t.

“If you ain’t first, you’re last.” -Ricky Bobby, Talladega Nights, on which monies succeed over time.

So, we can look at bitcoin success similarly to Pascal’s wager—let’s call it Satoshi’s wager. The translated points would go something like this:

- If you own bitcoin early and it becomes a globally valuable money, you gain immensely. ????

- If you own bitcoin and it fails, you’ve lost that value. ????

- If you don’t own bitcoin and it goes to zero, no pain and no gain. ????

- If you don’t own bitcoin and it succeeds, you will have missed out on the significant financial revolution of our lifetimes and fall comparatively behind. ????

If bitcoin is successful, it will be worth far more than it is today and have a massive impact on your financial future. If it fails, the losses are only limited to your exposure. The most that you could lose is the money that you invested.

It is hypothetically possible that bitcoin could be worth 100x more than it is today, but it can only possibly lose 1x its value as it goes to zero. The concept we’re discussing here is asymmetric upside - significant gains with relatively limited downside. In other words, the potential rewards of the investment outweigh the potential risks.

Bitcoin offers an asymmetric upside that makes it a wise investment for most portfolios. Even a small allocation provides potential protection against extreme currency debasement.

Salt, gasoline, and insurance

“Don’t over salt your steak, pour too much gas on the fire, or buy too much insurance.”

A little bit goes a long way, and you can easily overdo it. The same applies when looking at bitcoin in the context of a financial plan.

Bitcoin’s asymmetric upside gives it “insurance-like” qualities, and that insurance pays off very well in times of money printing. This was exemplified in 2020 when bitcoin's value increased over 300% in response to pandemic money printing, far outpacing stocks, gold, and bonds.

Bitcoin offers a similar asymmetric upside today. Bitcoin's supply is capped at 21 million coins, making it resistant to inflationary debasement. In contrast, the dollar's purchasing power consistently declines through unrestrained money printing. History has shown that societies prefer money that is hard to inflate.

If recent rampant inflation is uncontainable and the dollar system falters, bitcoin is well-positioned as a successor. This global monetary A/B test is still early, but given their respective sizes, a little bitcoin can go a long way. If it succeeds, early adopters will benefit enormously compared to latecomers. Of course, there are no guarantees, but the potential reward justifies reasonable exposure despite the risks.

Let’s imagine Nervous Nancy, an extremely conservative investor. She wants to invest but also take the least risk possible. She invests 100% of her money in short-term cash equivalents (short-term treasuries, money markets, CDs, maybe some cash in the coffee can). With this investment allocation, she’s nearly certain to get her initial investment back and receive a modest amount of interest as a gain. However, she has no guarantees that the investment returned to her will purchase the same amount as it used to. Inflation and money printing cause each dollar to be able to purchase less and less over time. Depending on the severity of the inflation, it might not buy anything at all. In other words, she didn’t lose any dollars, but the dollar lost purchasing power.

Now, let’s salt her portfolio with bitcoin.

99% short-term treasuries. 1% bitcoin.

With a 1% allocation, if bitcoin goes to zero overnight, she’ll have only lost a penny on the dollar, and her treasury interest will quickly fill the gap. Not at all catastrophic to her financial future.

However, if the hypothetical hyperinflationary scenario from above plays out and bitcoin grows 100x in purchasing power, she’s saved everything. Metaphorically, her entire dollar house burned down, and “bitcoin insurance” made her whole. Powerful. A little bitcoin salt goes a long way.

(When protecting against the existing system, it’s important to remember that you need to get your bitcoin out of the system. Keeping bitcoin on an exchange or with a counterparty will do you no good if that entity fails. If you view bitcoin as insurance, it’s essential to keep your bitcoin in cold storage and hold your keys. Otherwise, it’s someone else’s insurance.)

When all you have a hammer, everything looks like a…

A construction joke:

There are only three rules to construction: 1.) Always use the right tool for the job! 2.) A hammer is always the right tool! 3.) Anything can be a hammer!

Yeah. That’s what I thought, too. Slightly funny and mostly useless.

But if you spend enough time swinging a hammer, you’ll eventually realize it can be more than it first appears. Not everything is a nail. A hammer can tear down walls, break concrete, tap objects into place, and wiggle other things out. A hammer can create and destroy; it builds tall towers and humbles novice fingers. The use cases expand with the skill of the carpenter.

Like hammers, bitcoin is a monetary tool. And a 1-5% allocator to the asset typically sees a “speculative insurance” use case - valid. Bitcoin is speculative insurance, but it is not only speculative insurance. People invest and save in bitcoin for many different reasons.

I’ve seen people use bitcoin to pursue all of the following use cases:

- Hedging against a financial collapse (speculative insurance)

- Saving for family and future (long-term general savings and safety net)

- Growing a downpayment for a house (medium-term specific savings)

- Shooting for the moon in a manner equivalent to winning the lottery (gambling)

- Opting out of government-run, bank-controlled financial systems (financial optionality)

- Making a quick buck (short-term trading)

- Escaping a hostile country (wealth evacuation)

- Locking away wealth that can’t be confiscated (wealth preservation)

- As a means to influence opinions and gain followers (social status)

- Fix the money and fix the world (mission and purpose)

Keep this in mind when taking other people’s financial advice. They are often playing a different game than you. They have different goals, upbringings, worldviews, family dynamics, and circumstances. Even though they might use the same hammer as you, it could be for a completely different job.

Wrapping Up

A massive allocation to bitcoin may seem crazy to some people, yet perfectly reasonable to others. The same goes for having a 1% allocation.

But, given today’s macroeconomic environment and bitcoin’s trajectory, I find very few use cases where 0% bitcoin makes sense. By not owning bitcoin, you implicitly say that you are 100% certain it will fail and go to zero. Given its 14-year history so far, I’d recommend reducing your confidence. Nobody is 100% right forever. A little salt goes a long way. Your financial plan may be riskier without bitcoin. Diversify accordingly.

“We must learn our limits. We are all something, but none of us are everything.” - Blaise Pascal.

bonds pandemic stocks bitcoin link goldContact

Office: (208)-254-0142

Ste. 205

Eagle, ID 83616

Check the background of your financial professional on FINRA's BrokerCheck.The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Some of this material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named representative, broker - dealer, state - or SEC - registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

Copyright 2024 FMG Suite.

Sound Advisory, LLC (“SA”) is a registered investment advisor offering advisory services in the State of Idaho and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training. The information on this site is not intended as tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment-making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, Sound Advisory LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

SA does not warrant that the information on this site will be free from error. Your use of the information is at your sole risk. Under no circumstances shall SA be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided on this site, even if SA or an SA authorized representative has been advised of the possibility of such damages. Information contained on this site should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

The Question You Should Ask Whenever You’re Wrong

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Health Officials: Man Dies From Bubonic Plague In New Mexico

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International6 days ago

International6 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges