Futures Flat Ahead Of FOMC Minutes

Futures Flat Ahead Of FOMC Minutes

Global stocks were stuck in a holding pattern on Wednesday at record high levels, with US equity futures unchanged from Tuesday’s close, as investors awaited details of the latest FOMC minutes. The 10-year..

Share this:

Global stocks were stuck in a holding pattern on Wednesday at record high levels, with US equity futures unchanged from Tuesday's close, as investors awaited details of the latest FOMC minutes. The 10-year Treasury yield reversed an earlier loss, while the dollar paused after a four-day slide.

While COVID case numbers rose in several parts of the world and geopolitical tensions between China and Taiwan and between Russia and Ukraine ensured it was by no means a fairytale, markets had a Goldilocks feel again with MSCI’s 50-country world index grinding out a sixth day of gains. Futures on the S&P 500 and Nasdaq 100 fluctuated after the underlying gauges retreated overnight as volume on U.S. exchanges dwindled below 10 billion shares for the first time this year.

The IMF raised its global growth forecast to 6% this year from 5.5% on Tuesday, reflecting a rapidly brightening outlook for the U.S. economy. If realized, that would be the fastest the world economy has grown since 1976, albeit after the steepest annual downturn of the post-war era last year when the COVID pandemic brought commerce to a near stand-still at times. “Even with high uncertainty about the path of this pandemic, a way out of this health economic crisis is increasingly visible,” IMF Chief Economist Gita Gopinath said.

Expectations for continued central-bank support and the strongest world expansion in at least four decades have driven stock benchmarks to unprecedented heights. Concerns about higher borrowing costs destabilizing the market have eased, with bond yields subsiding as traders pull their more-aggressive positioning for Fed policy tightening. Minutes of the last Fed rates meeting later Wednesday may provide more clues on the outlook.

"We continue to expect equity prices and U.S. long-term yields to increase further over the coming months, as real growth and inflation data picks up especially in the U.S.,” said Xavier Chapard, a global macro strategist at Credit Agricole SA. “In the short term they could remain range-bound as a lot of good news is in the prices."

The Stoxx Europe 600 index edged lower 0.1% one day after hitting an all time high. The Stoxx 600 Technology Index falls as much as 1.2%, retreating after reaching the highest level in more than 20 years on Tuesday, with chip equipment makers pausing and high-flying pandemic winners also lower. Here are some of the biggest European movers today courtesy of Bloomberg:

- EDF shares surge as much as 10% following a report that the French government could spend EU10b on buying out minority shareholders. Given the current state-ownership level, the EU10b figure would suggest a price for minority holders of almost EU20/share, Citi wrote in a note.

- Carnival jumps as much as 4.8% after the sector is boosted by the U.S. Centers for Disease Control and Prevention saying cruises could resume by mid-summer with restrictions. In a statement Tuesday before the CDC update, Carnival Cruise Line said it may have “no choice” but to move ships outside of U.S. ports.

- Atos rises as much as 4.8%, recouping some of its 14% slump over the past two sessions, as Exane pondered the scenario of a deal with French IT services peer Capgemini. The broker wrote that Atos and Capgemini valuations are “at extremes,” and Atos’s struggling share price suggests investors could be open to an “alternative strategic solution.”

- Prosus declinee as much as 5.1% after the internet investor said it would reduce its stake in Chinese online giant Tencent to just under 29% from 31% through a share sale that will raise as much as $14.6b.

- Flutter Entertainment falls as much as 3.9% following a share placing at a discount to Tuesday’s close. Drop also comes after Fox was reported to have filed a suit against the gaming company over its stake in FanDuel.

- Amundi SA gained as much as 3.3% after agreeing to buy Societe Generale SA’s fund management arm Lyxor.

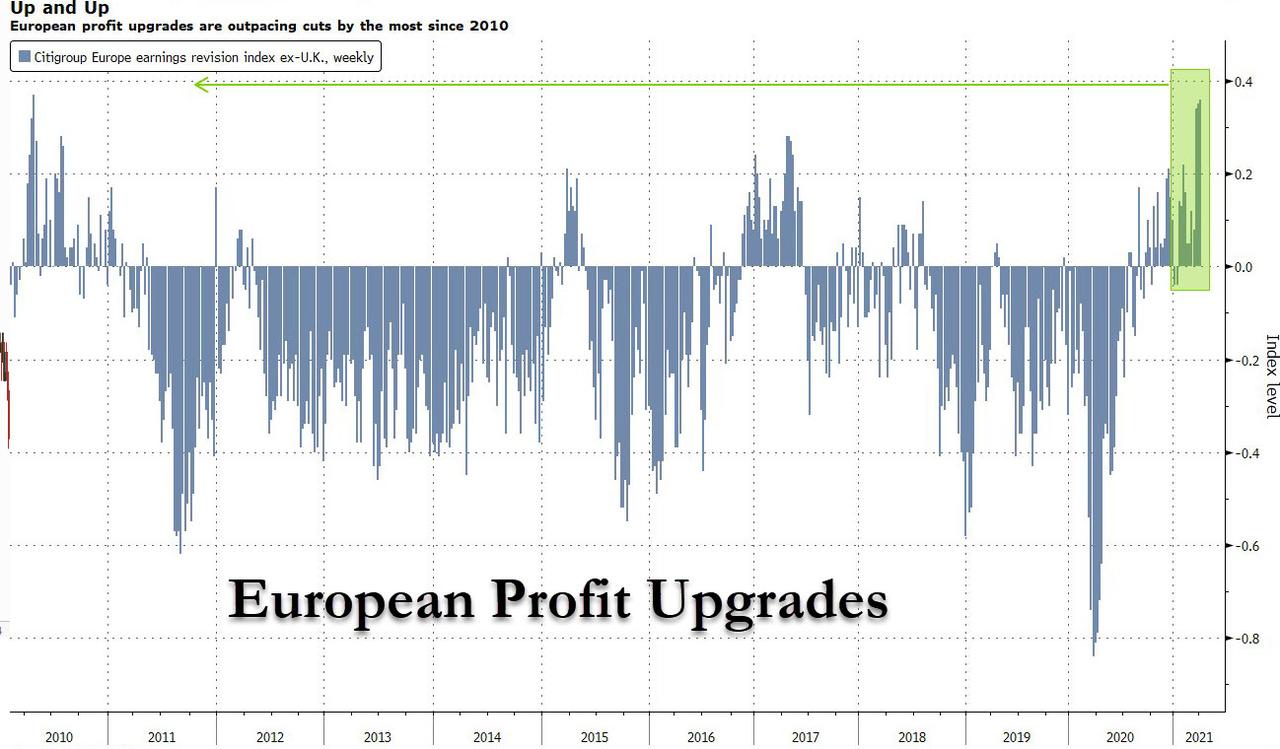

As Bloomberg shows, validating the bullish European picture, profit upgrades are outpacing cuts by the most since 2010.

Earlier in the session, MSCI’s index of Asia-Pacific shares had started on a firm footing, going as high as 208.46 points, a level last seen on March 18. However, it succumbed to selling pressure and ended flat as China’s blue-chip CSI300 index dipped 1% and Hong Kong eased 0.9%. Eventually, Asian stocks were little changed overall as Thailand and Hong Kong led declines while most major equity benchmarks advanced. By sector, communications services firms were the biggest drag on the MSCI Asia Pacific Index while gains in materials makers provided support.

Geopolitical tensions in the region added to the jitters. Taiwan’s foreign minister said on Wednesday it will fight to the end if China attacks, adding that the United States saw a danger that this could happen amid mounting Chinese military pressure, including aircraft carrier drills, near the island. Other Asian markets managed to stay positive. Japan’s Nikkei closed higher; Australian shares rose 0.6% and South Korea’s KOSPI added 0.3%.

Chinese stocks dropped for a second session, dragged lower by liquor firms after a popular fund reduced its stake in a distiller.

The benchmark CSI 300 Index fell 0.7% to close at 5,103.74 points, the lowest in a week. The decline added to a 0.4% drop on Tuesday after the gauge posted its biggest weekly gain since mid-February last week. Sichuan Swellfun fell 3.8%, extending its two-day decline to 6.2%, after the E Fund Small and Mid Cap Fund, managed by star manager Zhang Kun, trimmed its holdings to just 0.6% of total shares outstanding, according to regulatory filings. That compares with 2.9% at the end of 2020. The shift comes after one of Zhang’s funds returned 95% last year largely due to bets on baijiu makers, a strategy that drew a large investor following. Peers of the firm also fell, including Kweichow Moutai’s 3.1% loss, the most in a month. Meanwhile, Wuliangye and Luzhou Laojiao dropped by at least 4.9%. The Hang Seng China Enterprises Index in Hong Kong dropped, with heavyweights including China Pacific Insurance and Tencent Holdings among those contributing most to the fall.

Thailand’s key SET Index posted its biggest drop since Feb. 22 amid a domestic surge in coronavirus infections. Hotel and restaurant shares led the decline, with Prime Minister Prayuth Chan-Ocha hinting that tougher restrictions on entertainment venues were likely in an effort to fight the virus spread.

Equity markets in India, the Philippines and New Zealand advanced, among others, with some global stock benchmarks hovering around all-time highs. Indian stocks climbed after central bank policy makers pledged to maintain an accommodative stance for as long as necessary, amid a new wave of coronavirus infections. India’s central bank announced it would buy one trillion rupees of govt bonds in the secondary market during the fiscal year that began on April 1 under an acquisition program, the Reserve Bank of India Governor Shaktikanta Das said.

The S&P BSE Sensex climbed 0.9% to 49,661.76 in Mumbai, while the NSE Nifty 50 Index advanced by a similar magnitude. All but one of 19 sector sub-indexes compiled by BSE Ltd. gained, led by a gauge of automobile makers. The Reserve Bank of India monetary policy committee held the benchmark repurchase rate at a record low of 4% -- a decision predicted by all 30 economists surveyed by Bloomberg. The central bank also pledged to buy 1 trillion rupees ($13.5 billion) of bonds this quarter to cap borrowing costs and support an economy facing a resurgence of coronavirus infections. “This will have a trickle-down effect on other instruments, including stocks,” said Deepak Jasani, head of retail research at HDFC Securities Ltd. A new wave of Covid cases has prompted the return of localized lockdowns in a number of key states, raising concerns over business recovery. India crossed 100,000 new daily infections on Sunday, with wealthiest state Maharashtra emerging as the epicenter. “Localized and regional lockdowns could dampen the recent improvement in demand conditions and delay the return of normalcy,” RBI Governor Shaktikanta Das said.

In rates, Treasury futures held small gains, leaving yields slightly richer across the curve vs Tuesday’s close. 10-year yields hovered around 1.65%, lower by less than 1bp, trailing bunds and gilts by ~1bp; gilts saw duration demand from real-money accounts. Minutes of March 17 FOMC meeting, slated for 2pm ET release, will be searched for any commentary on tapering, as markets continue to price in an earlier start to rate hikes than Fed policy makers project. The five-year Treasury yield especially is seen as a major barometer of the faith investors have in the Fed’s message that it doesn’t expect to raise U.S. interest rates until 2024. Europe’s bond yields also eased, with southern European debt markets stabilising after a selloff the previous session as traded braced for a 50-year bond from Italy. The European Central Bank meanwhile will release monthly data on its conventional asset purchases and a bi-monthly breakdown of its PEPP pandemic emergency bond purchases which it has vowed to increase to keep borrowing costs low.

FX markets also saw subdued trading, with the dollar traded mixed versus G-10 peers and most pairs trading in narrow ranges. The euro hovered in a 30 pips range versus the dollar. The pound steadied after falling to its lowest level versus the dollar since April 1 amid concerns over the U.K.’s vaccine rollout. Australian and New Zealand dollars led G-10 losses as the greenback strengthened but remained within recent ranges; the Aussie had earlier inched higher after the IMF boosted its forecast for Australia’s GDP to 4.5% this year.

"A large share of the hopes of a U.S. growth boom supported by state aid and rapid vaccination progress has already been priced in," Commerzbank FX and EM analyst Esther Reichelt wrote in a note to clients. “Further and more pronounced USD gains would only be justified if this boom also caused rising inflation rates to which the Fed would have to react with higher interest rates."

In commodities, Brent crude futures were nudging lower at $62.67 a barrel. U.S. crude was up at $59.51 and both gold and copper were off at $1,736.4 an ounce and 8,980 a tonne respectively.

Looking at today's calendar, all eyes will be on minutes of the U.S. Federal Reserve’s March policy meeting when they are published later. The upcoming earnings season is expected to show S&P profit growth of 24.2% from a year earlier, according to Refinitiv data, and investors will be watching to see whether corporate results further confirm recent positive economic data.

Market Snapshot

- S&P 500 futures little changed at 4,065.25

- STOXX Europe 600 little changed at 435.41

- MXAP little changed at 207.18

- MXAPJ down 0.3% to 691.53

- Nikkei up 0.1% to 29,730.79

- Topix up 0.7% to 1,967.43

- Hang Seng Index down 0.9% to 28,674.80

- Shanghai Composite little changed at 3,479.63

- Sensex up 1.1% to 49,761.51

- Australia S&P/ASX 200 up 0.6% to 6,928.02

- Kospi up 0.3% to 3,137.41

- Brent Futures down 0.5% to $62.43/bbl

- Gold spot down 0.4% to $1,737.15

- U.S. Dollar Index little changed at 92.29

- German 10Y yield fell 1.2 bps to -0.328%

- Euro little changed at $1.1887

Top Overnight News from Bloomberg

- The ECB would be able to start unwinding its emergency bond- buying program if the economy develops in line with expectations, Governing Council member Klaas Knot told Reuters in an interview

- Germany, Italy, Spain and Ireland all saw business activity rise last month and France halted its contraction, according to IHS Markit’s latest survey of purchasing managers

- Billionaire investor Mike Novogratz said he’s bought Facebook Inc. stock to benefit from crypto’s ascent and is also shorting the five-year Treasury as a hedge against policy makers pulling back monetary support

- Rising demand for everything from soybeans to steel has sent the cost of hauling dry goods soaring more than 50% this year

- The Swedes are learning that their once pioneering vision for a central bank digital currency might take a lot longer to enact than initially thought.

A quick look at global markets courtesy of Newsquawk

Asian equity markets traded mixed following on from the flat performance on Wall St where most major indices consolidated after recently hitting fresh record highs and with a lack of solid macro drivers, as well as the looming FOMC Minutes ensuring a non-committal tone. ASX 200 (+0.6%) was positive as outperformance in real estate, gold miners and tech kept the index afloat but with gains limited by pressure in industrials and the largest-weighted financials sector, while Nikkei 225 (+0.1%) briefly gave back its early gains as the index succumbed to the JPY strength although there was also plenty of focus on Toshiba shares which were so far untraded with a glut of buy orders after reports of a USD 20bln buyout proposal from CVC Capital. KOSPI (+0.3%) remained positive following preliminary earnings from Samsung Electronics which reported Q1 operating profit rose 44% Y/Y to KRW 9.3tln as expected and with LG Electronics topping forecasts for its preliminary quarterly operating profit and revenue. However, the gains were only marginal as concerns of a 4th wave of the pandemic were stoked after daily infections increased by the most in three months and with by-elections taking place in Seoul and Busan which are a bellwether for next year’s Presidential Elections. Hang Seng (-0.9%) and Shanghai Comp. (-0.1%) were subdued after continued PBoC liquidity inaction and with the former suffering from holiday blues on return from the extended weekend as it gets its first opportunity to digest the recent reports of the PBoC instructing banks to curtail lending. Finally, 10yr JGBs were flat as they took a breather from yesterday’s gains but with prices kept afloat by the flimsy picture in Japanese stocks and with the BoJ also present in the market for JPY 710bln of JGBs with the majority in the belly, while it also offered to buy JPY 125bln of corporate bonds with 1yr-3yr maturities from April 12th.

Top Asian News

- SoftBank-Backed Policybazaar Said to Plan IPO Filing Next Month

- Australia Opposition Urges Review of RBA, Fiscal-Monetary Policy

- China Vows to Hold Successful Olympics, Dismisses Boycott Threat

- Steel’s Storming Rally Pauses as China Steps Up Mill Scrutiny

European equities have maintained the mixed picture portrayed at the cash open (Euro Stoxx 50 -0.1%) following the similar performance seen in APAC markets. US equity futures meanwhile remain contained in sideways trade with the RTY narrowly lagging peers, although the depth of the price action is shallow as participants await upcoming catalysts. Back to Europe, a snapshot of the bourses' performances sees the core markets faring better than the periphery, with the UK's FTSE 100 (+0.8%) outpacing peers with the early aid of a softer sterling, whilst heavyweight BP (+2.7%) and mining giants continue to underpin the index. The SMI meanwhile resides in the red as pharma behemoths Novartis (-1%) and Roche (-0.8%) keep upside capped - with the former weighed on by a cancer research deal with Artios whereby the Co. will pay as much as USD 20mln initially but this could rise to a ceiling of USD 1.3bln. Subsequently, the downside in the Cos is exerting pressure on the broader healthcare sector which stands as the underperformer thus far. Sectors, in general, are mixed with no clear cyclical/defensive bias. Tech stands as the laggard despite favourable yield play and light news flow, with potential follow-through emanating from earning updates via Samsung Electronics and LG Electronics which saw both companies weaker in the aftermath. Elsewhere, the Real Estate sector is propped up as UK housing names are faring well - with Persimmon (+3%), Taylor Wimpey (+2.9%), and Barratt Developments (+2.0%) all towards the top of the UK benchmark. Travel & Leisure meanwhile continues to bear the brunt of lockdown woes, albeit Carnival (+4.3%) bucks the trend ahead of results despite extending its pause in cruises from US ports. In terms of individual movers, EDF (+8.5%) is bolstered by reports that the French state (cited by union sources) reportedly said the buyback of shares in EDF, held by minority shareholders, is seen at EUR 10bln in restructuring project. On the flip side Flutter Entertainment (-3.0%) trades at the foot of the Stoxx 600 as Fox filed an arbitration claim against the Co. as part of a dispute over the FanDuel platform. Shell (+0.5%) sees some modest gains following its Q1 update, whereby the giant said Adjusted Earnings are expected to be positive in Q1, but the Texas deep freeze and adverse currency effects are seen knocking off some USD 240mln from earnings. Finally, Credit Suisse (-0.6%) is back under pressure as sources close to Credit Suisse said the group not ruling out further management alterations as a result of the Archegos situation, Furthermore, reports state that the Co. could report losses related to Greensill of some CHF 1.4bln.

Top European News

- Italy Is Said to Be Under Pressure to Delay Euronext-Borsa Deal

- France Pushes Back Against Mooted $12 Billion EDF Delisting

- Polish Coalition May Collapse Over EU Plan, Kaczynski Says

- Euro-Area Companies Return to Broad Growth on Vaccine Optimism

In FX, the Pound has been in the spotlight again and under pressure as Cable retreated through 1.3800 amidst what looked like further short covering and technical retracement in Eur/Gbp rather than anything negative or bearish for Sterling specifically. Indeed, the cross extended its rebound to circa 150 pips from Monday’s low before petering out around 0.8624 and ahead of several recent tops from late March below 0.8650 that could be pivotal in terms of the overall bear trend that has seen Eur/Gbp decline from 0.9085 on January 6 having already fallen sharply from 0.9230 less than a month before that (December 11 to be precise). Meanwhile, Cable met some underlying bids into 1.3770 and above a pivot point at 1.3760 that is guarding 1.3750 ahead of the April 1 base just below, and is back on the 1.3800 handle irrespective of minor downward tweaks to the final UK services and composite PMIs.

- AUD/CAD/NZD/DXY - The non-US Dollars are bearing the brunt of relative stability in the Greenback and some other factors, like a worrying 3rd COVID-19 wave spreading across Canada and wavering risk sentiment amidst ongoing uncertainty over the AZN vaccine, but with the Aussie also unwinding some of its gains vs the Kiwi and Loonie treading cautiously into trade data plus Ivey PMIs. Aud/Usd and Nzd/Usd are both still pivoting half round numbers at 0.7650 and 0.7050 respectively, but Aud/Nzd has lost a bit of momentum after reaching 1.0875 and Usd/Cad is probing 1.2600 following no breach of the big figure below since March 22. However, the Buck remains mixed overall and the index is capped below 92.500 awaiting US data, FOMC minutes and Fed speakers within a 92.413-246 range that also incorporates potentially key chart levels in the form of 200 and 21 DMAs (at 92.380 and 92.304).

- CHF/EUR/JPY - All narrowly mixed vs the Dollar, but the Franc marginally outperforming either side of 0.9300 as the Euro tests technical resistance at 1.1889 (200 DMA) in wake of broadly firmer than forecast and/or flash Eurozone services and composite PMIs plus hawkish-leaning PEPP talk from ECB’s Knot, and the Yen slips back after running out of steam into 109.50. At this stage, decent option expiry interest in Eur/Usd and Usd/Jpy looks too far from spot to influence direction, but for the record 1.1 bn rolls off at the 1.1850 strike, 1.2 bn between 1.1835-30 and 1.4 bn at 109.00.

- EM - No respite for the Rub via latest RIA reports quoting the Foreign Ministry stating that Russia and the US are in talks about the former taking part in a climate summit, while the Try remains weak despite a dip in oil prices after Turkey’s opposition leader urged President Erdogan to call a snap election, according to Al Arabiya, and regardless of the latter expressing a determination to get CPI back down to sub-10%. Elsewhere, the Inr emerged softer following the RBI’s anticipated on hold rate verdicts as it also maintained an accommodative stance and extended its on tap TLTRO by a further 6 months and provided an extra Inr 500 bn in liquidity to all domestic financial institutions for new loans.

In commodities, WTI and Brent front month futures have seen a choppy session thus far after giving up APAC gains and some more in early European hours before reversing ahead of the US entrance, with the benchmarks currently firmer to the tune of 0.7% apiece at the time of writing at around USD 59.75/bbl (vs low 58.80/bbl) and USD 63.20/bbl (vs high 62.20/bbl). There have not been any specific headlines to drive price action although participants continue to weigh the recent fundamental drivers; namely, OPEC and COVID among others. Aside from the ongoing COVID-related demand risks, the supply-side sees uncertainty on the Iranian front as nuclear deal talks are underway this week following the first round of talks yesterday - which seemed to be sanguine, although Iran sticks to its stance that key sanctions need to be lifted for any developments. Talks are poised to resume on Friday with eyes on any potential rollback of Iranian sanctions, namely oil-related - although this is not expected. Moving on, the EIA STEO yesterday raised its 2021 world oil demand growth forecast by 180k BPD and cut the 2022 world oil demand growth forecast by 180k BPD, whilst also cutting US production forecasts for both years. Yesterday also saw the release of the weekly Private Inventory data, which showed a larger-than-expected draw in the headline figure, however, refined products saw large builds - traders will be eyeing the DoE's today with the headline forecasting a draw of 1.436mln bbls. Elsewhere, spot gold and silver are uneventful within recent ranges around USD 1,740/oz and USD 25/oz respectively as Dollar action is tracked. Turning to base metals, LME copper is softer and back below USD 9,000/t with traders citing rising inventories alongside softening demand in China. Dalian iron ore meanwhile closed the session higher by almost 2% with follow-through from record steel prices cited as a factor despite the recent curbs in China's top steel-making city of Tangshan. On this front, the city's government has asked domestic steel mills to conduct environmental assessments related to the production and processes, and mills who are unable to do so may face production halts or fines.

US Event Calendar

- 7am: April MBA Mortgage Applications, prior -2.2%

- 8:30am: Feb. Trade Balance, est. -$70.5b, prior -$68.2b

- 2pm: March FOMC Meeting Minutes

- 3pm: Feb. Consumer Credit, est. $2.8b, prior - $1.32b

Central Banks

- 9am: Fed’s Evans Discusses Economic Outlook

- 11am: Fed’s Kaplan Takes Part in Panel Discussion

- 12pm: Fed’s Barkin Discusses Monetary Policy and the Economy

- 1pm: Fed’s Daly Discusses U.S. Economic Outlook

- 2pm: March FOMC Meeting Minutes

DB's Jim Reid concludes the overnight wrap

Although it was a pretty quiet day in terms of newsflow, the momentum behind risk assets largely continued for the most part over the last 24 hours, as investors continued to bet on an economic rebound over the coming months in light of the very strong data in recent weeks. Equity indices remained around their recent record highs, with the S&P 500 reaching a new intraday high in spite of a late selloff that saw the index close down -0.10% to record its first loss in four session. Furthermore, as Europe caught up following Monday’s holiday, the STOXX 600 (+0.70%) surpassed its previous all-time high back in February 2020, and the MSCI World index (+0.11%) similarly hit a new record. And on top of all that, equity volatility continued to remain subdued around its lowest levels since the pandemic began, while Bloomberg’s index of US financial conditions eased to its most accommodative level since late-2018.

While those data points would all suggest some pretty benign conditions right now as equities hover around record highs, it’s worth pointing out a note from DB’s Binky Chadha and our asset allocation team from earlier this week, who write that they’re expecting a significant consolidation in equities (-6% to -10%) as growth peaks over the next 3 months (link here).Historically speaking, the team’s report notes how equities have traded closely with indicators of cyclical macro growth such as the ISMs, which in turn typically peak around a year after the recession ends, so around the point we now appear to be. So although they expect equities to continue to be well-supported by the acceleration in macro growth over the very near term, they expect that pullback as growth peaks in the next few months, before equities rally back once again towards the end of the year given our baseline for a Goldilocks economic outlook of strong growth and contained inflation pressures.

Looking back at yesterday’s moves in more depth, the small pullback in US equities was fairly subdued overall, as the S&P 500 and Dow Jones (-0.29%) only saw modest declines from Monday’s record high. Tech stocks outperformed slightly, with the NASDAQ closing just a touch better than the broader S&P, with a -0.05% loss, while semiconductors & semiconductor equipment (-1.11%) were the worst-performing of the S&P’s 24 industry groups. The exception to this were the megacap tech stocks however, and the NYSE FANG+ (+0.65%) outperformed in its 7th successive advance, even if this still leaves the index nearly 8% down from its peak in mid-February. Banks (-0.23%) were another laggard, and were under pressure against the backdrop of further declines in Treasury yields, even as this proved supportive for the broader equity market. And the underlying strength in a consumer-led economic recovery was still seen as consumer services (+1.37%), consumer durables (+0.83%) and food & beverages (+0.53%) were among the best performing industry groups.

Compared to equities, sovereign bonds saw a much more divergent performance on either side of the Atlantic, although again this could in part be explained by Europe not being open on Monday. Yields on 10yr Treasuries fell -4.4bps to 1.656%, their lowest closing level in almost two weeks, and the bulk of this decline could be explained by lower inflation expectations (-3.8bps) rather than real rates (-0.7bps). For Europe it was a different story however, as yields on 10yr bunds (+1.2bps), OATs (+1.8bps) and BTPs (+6.2bps) all moved higher, and in the reverse of the US, inflation expectations were driving the move higher. 10yr German, Italian and Spanish breakevens all rose to their highest closing levels since 2018, and yesterday saw 5y5y forward inflation swaps for the Euro Area rise another +1.5bps, putting them at 1.56%, their highest level since early 2019.

Overnight in Asia, markets are a bit directionless this morning given the subdued newsflow with the Hang Seng (-0.65%) and Shanghai Comp (-0.53%) losing ground while the Nikkei (+0.28%), Kospi (+0.24%) and Asx (+0.42%) have all moved higher. In addition, the Reserve Bank of India announced that they’d be keeping their repo rate unchanged at 4%, in line with expectations. Elsewhere, futures are indicating that US and European indices will continue to hover around their recent records, with those on the S&P (+0.04%) pointing to a small gain, while in Europe those on the Stoxx 50 (-0.13%) and Dax (-0.10%) are indicating a modest pullback.

Oil prices rebounded somewhat yesterday as Iran described the first round of talks in Vienna on restoring the 2015 nuclear deal had been “constructive”. However, the main Iranian negotiator Abbas Araghchi said that Iran had rejected a proposal from the US to release $1bn of frozen Iranian oil revenues that would be offered in return for the suspension of production of 20% enriched uranium. A European official noted that it is important that some level of progress was made prior to the end of May, given a 90-day deadline that Iran and International Atomic Energy Agency agreed to in late February which allowed the continuity of inspections data. Diplomats will be meeting again to continue the talks on Friday. Elsewhere in crude, the US Energy Information Administration cut their oil production forecast to 11.04mn barrels/day this year – down from last month’s forecast of 11.15mn. Production will still be increasing modestly year-over-year however.This comes just as OPEC+ has indicated they will turn back on their taps by rolling back cuts over the coming months. After all the news flow, Brent Crude rose +0.95% and WTI rose +1.16%.

Turning to the pandemic, the main news yesterday was that President Biden announced that the new deadline for states to make all adults eligible for Covid-19 vaccinations is April 19th. This is two weeks earlier than previously planned, yet all but two states are already set to meet that timeline. California is currently planning on fully reopen their economy – the largest in the US – as of June 15 as long as the conditions continue to improve and vaccination rates remain high. On the topic of vaccinations, the White House again came out against any sort of “vaccine passport” issued by the federal government, nothing that they did not want them “used against people unfairly.” However Press Secretary Psaki noted that the administration will be circulating guidance for private-sector solutions that have been floated.

On the AstraZeneca vaccine, the EMA said that their ongoing review should be finalised by tomorrow, and we also heard that a trial of the AstraZeneca shot in children ages 6-17 has been paused while a review by the UK’s MHRA takes place on the blood clot incidents, although Oxford noted that no safety issues arose in the children’s trial so far. Staying here in the UK, the 7-day average of confirmed cases fell to 3,256, which is its lowest since mid-September, back when the levels of testing were a fraction of their current levels, and the country is also set to begin the rollout of the Moderna vaccine today. Nevertheless, Prime Minister Johnson said that it is not yet clear that non-essential travel will be allowed to resume safely by May 17 and the UK government asked Britons to wait a little while longer on planning foreign travel over the summer holidays. Finally in emerging markets, the newsflow was rather less positive, with India seeing a record 115,736 cases, and in Brazil a record number of daily fatalities were reported, at 4,195.

Yesterday saw the IMF release their latest World Economic Outlook, in which they upgraded their global growth forecast for 2021 to +6.0% (vs. +5.5% in January), along with their 2022 forecast to +4.4% (vs. +4.2% in Jan). Both the advanced and emerging market economies saw upgrades, though it was the advanced economies that saw the bulk of the upward revisions, with the US forecast for the next 2 years now at +6.4% in 2021 and +3.5% in 2022 (vs. +5.1% and +2.5% in Jan respectively). Their inflation forecasts saw modest upgrades too, with their forecasts now seeing consumer prices in the advanced economies rising by +1.6% in 2021 and +1.7% in 2022.

In terms of other data out yesterday, US job openings rose to a 2-year high of 7.367m in February, well above the 6.9m reading expected, while the quits rate that is typically a good leading indicator for wage growth remained steady at 2.3%. The other main release came from the Euro Area, where the unemployment rate for February remained at an upwardly-revised 8.3% (vs. 8.1% expected).

To the day ahead now, and data releases include the March services and composite PMIs from Europe, along with US February data on the trade balance and consumer credit. From central banks, the main highlight will be the release of the FOMC’s minutes from their March meeting, though there’ll also be remarks from the Fed’s Evans, Kaplan, Barkin and Daly.

Uncategorized

Economic Earthquake Ahead? The Cracks Are Spreading Fast

Economic Earthquake Ahead? The Cracks Are Spreading Fast

Authored by Brandon Smith via Alt-Market.us,

One of my favorite false narratives…

Share this:

Authored by Brandon Smith via Alt-Market.us,

One of my favorite false narratives floating around corporate media platforms has been the argument that the American people “just don’t seem to understand how good the economy really is right now.” If only they would look at the stats, they would realize that we are in the middle of a financial renaissance, right? It must be that people have been brainwashed by negative press from conservative sources…

I have to laugh at this notion because it’s a very common one throughout history – it’s an assertion made by almost every single political regime right before a major collapse. These people always say the same things, and when you study economics as long as I have you can’t help but throw up your hands and marvel at their dedication to the propaganda.

One example that comes to mind immediately is the delusional optimism of the “roaring” 1920s and the lead up to the Great Depression. At the time around 60% of the U.S. population was living in poverty conditions (according to the metrics of the decade) earning less than $2000 a year. However, in the years after WWI ravaged Europe, America’s economic power was considered unrivaled.

The 1920s was an era of mass production and rampant consumerism but it was all fueled by easy access to debt, a condition which had not really existed before in America. It was this illusion of prosperity created by the unchecked application of credit that eventually led to the massive stock market bubble and the crash of 1929. This implosion, along with the Federal Reserve’s policy of raising interest rates into economic weakness, created a black hole in the U.S. financial system for over a decade.

There are two primary tools that various failing regimes will often use to distort the true conditions of the economy: Debt and inflation. In the case of America today, we are experiencing BOTH problems simultaneously and this has made certain economic indicators appear healthy when they are, in fact, highly unstable. The average American knows this is the case because they see the effects everyday. They see the damage to their wallets, to their buying power, in the jobs market and in their quality of life. This is why public faith in the economy has been stuck in the dregs since 2021.

The establishment can flash out-of-context stats in people’s faces, but they can’t force the populace to see a recovery that simply does not exist. Let’s go through a short list of the most faulty indicators and the real reasons why the fiscal picture is not a rosy as the media would like us to believe…

The “miracle” labor market recovery

In the case of the U.S. labor market, we have a clear example of distortion through inflation. The $8 trillion+ dropped on the economy in the first 18 months of the pandemic response sent the system over the edge into stagflation land. Helicopter money has a habit of doing two things very well: Blowing up a bubble in stock markets and blowing up a bubble in retail. Hence, the massive rush by Americans to go out and buy, followed by the sudden labor shortage and the race to hire (mostly for low wage part-time jobs).

The problem with this “miracle” is that inflation leads to price explosions, which we have already experienced. The average American is spending around 30% more for goods, services and housing compared to what they were spending in 2020. This is what happens when you have too much money chasing too few goods and limited production.

The jobs market looks great on paper, but the majority of jobs generated in the past few years are jobs that returned after the covid lockdowns ended. The rest are jobs created through monetary stimulus and the artificial retail rush. Part time low wage service sector jobs are not going to keep the country rolling for very long in a stagflation environment. The question is, what happens now that the stimulus punch bowl has been removed?

Just as we witnessed in the 1920s, Americans have turned to debt to make up for higher prices and stagnant wages by maxing out their credit cards. With the central bank keeping interest rates high, the credit safety net will soon falter. This condition also goes for businesses; the same businesses that will jump headlong into mass layoffs when they realize the party is over. It happened during the Great Depression and it will happen again today.

Cracks in the foundation

We saw cracks in the narrative of the financial structure in 2023 with the banking crisis, and without the Federal Reserve backstop policy many more small and medium banks would have dropped dead. The weakness of U.S. banks is offset by the relative strength of the U.S. dollar, which lures in foreign investors hoping to protect their wealth using dollar denominated assets.

But something is amiss. Gold and bitcoin have rocketed higher along with economically sensitive assets and the dollar. This is the opposite of what’s supposed to happen. Gold and BTC are supposed to be hedges against a weak dollar and a weak economy, right? If global faith in the dollar and in the U.S. economy is so high, why are investors diving into protective assets like gold?

Again, as noted above, inflation distorts everything.

Tens of trillions of extra dollars printed by the Fed are floating around and it’s no surprise that much of that cash is flooding into the economy which simply pushes higher right along with prices on the shelf. But, gold and bitcoin are telling us a more honest story about what’s really happening.

Right now, the U.S. government is adding around $600 billion per month to the national debt as the Fed holds rates higher to fight inflation. This debt is going to crush America’s financial standing for global investors who will eventually ask HOW the U.S. is going to handle that growing millstone? As I predicted years ago, the Fed has created a perfect Catch-22 scenario in which the U.S. must either return to rampant inflation, or, face a debt crisis. In either case, U.S. dollar-denominated assets will lose their appeal and their prices will plummet.

“Healthy” GDP is a complete farce

GDP is the most common out-of-context stat used by governments to convince the citizenry that all is well. It is yet another stat that is entirely manipulated by inflation. It is also manipulated by the way in which modern governments define “economic activity.”

GDP is primarily driven by spending. Meaning, the higher inflation goes, the higher prices go, and the higher GDP climbs (to a point). Eventually prices go too high, credit cards tap out and spending ceases. But, for a short time inflation makes GDP (as well as retail sales) look good.

Another factor that creates a bubble is the fact that government spending is actually included in the calculation of GDP. That’s right, every dollar of your tax money that the government wastes helps the establishment by propping up GDP numbers. This is why government spending increases will never stop – It’s too valuable for them to spend as a way to make the economy appear healthier than it is.

The REAL economy is eclipsing the fake economy

The bottom line is that Americans used to be able to ignore the warning signs because their bank accounts were not being directly affected. This is over. Now, every person in the country is dealing with a massive decline in buying power and higher prices across the board on everything – from food and fuel to housing and financial assets alike. Even the wealthy are seeing a compression to their profit and many are struggling to keep their businesses in the black.

The unfortunate truth is that the elections of 2024 will probably be the turning point at which the whole edifice comes tumbling down. Even if the public votes for change, the system is already broken and cannot be repaired without a complete overhaul.

We have consistently avoided taking our medicine and our disease has gotten worse and worse.

People have lost faith in the economy because they have not faced this kind of uncertainty since the 1930s. Even the stagflation crisis of the 1970s will likely pale in comparison to what is about to happen. On the bright side, at least a large number of Americans are aware of the threat, as opposed to the 1920s when the vast majority of people were utterly conned by the government, the banks and the media into thinking all was well. Knowing is the first step to preparing.

The second step is securing your own financial future – that’s where physical precious metals can play a role. Diversifying your savings with inflation-resistant, uninflatable assets whose intrinsic value doesn’t rely on a counterparty’s promise to pay adds resilience to your savings. That’s the main reason physical gold and silver have been the safe haven store-of-value assets of choice for centuries (among both the elite and the everyday citizen).

* * *

As the world moves away from dollars and toward Central Bank Digital Currencies (CBDCs), is your 401(k) or IRA really safe? A smart and conservative move is to diversify into a physical gold IRA. That way your savings will be in something solid and enduring. Get your FREE info kit on Gold IRAs from Birch Gold Group. No strings attached, just peace of mind. Click here to secure your future today.

Uncategorized

Wendy’s teases new $3 offer for upcoming holiday

The Daylight Savings Time promotion slashes prices on breakfast.

Share this:

Daylight Savings Time, or the practice of advancing clocks an hour in the spring to maximize natural daylight, is a controversial practice because of the way it leaves many feeling off-sync and tired on the second Sunday in March when the change is made and one has one less hour to sleep in.

Despite annual "Abolish Daylight Savings Time" think pieces and online arguments that crop up with unwavering regularity, Daylight Savings in North America begins on March 10 this year.

Related: Coca-Cola has a new soda for Diet Coke fans

Tapping into some people's very vocal dislike of Daylight Savings Time, fast-food chain Wendy's (WEN) is launching a daylight savings promotion that is jokingly designed to make losing an hour of sleep less painful and encourage fans to order breakfast anyway.

Image source: Wendy's.

Promotion wants you to compensate for lost sleep with cheaper breakfast

As it is also meant to drive traffic to the Wendy's app, the promotion allows anyone who makes a purchase of $3 or more through the platform to get a free hot coffee, cold coffee or Frosty Cream Cold Brew.

More Food + Dining:

- Taco Bell menu tries new take on an American classic

- McDonald's menu goes big, brings back fan favorites (with a catch)

- The 10 best food stocks to buy now

Available during the Wendy's breakfast hours of 6 a.m. and 10:30 a.m. (which, naturally, will feel even earlier due to Daylight Savings), the deal also allows customers to buy any of its breakfast sandwiches for $3. Items like the Sausage, Egg and Cheese Biscuit, Breakfast Baconator and Maple Bacon Chicken Croissant normally range in price between $4.50 and $7.

The choice of the latter is quite wide since, in the years following the pandemic, Wendy's has made a concerted effort to expand its breakfast menu with a range of new sandwiches with egg in them and sweet items such as the French Toast Sticks. The goal was both to stand out from competitors with a wider breakfast menu and increase traffic to its stores during early-morning hours.

Wendy's deal comes after controversy over 'dynamic pricing'

But last month, the chain known for the square shape of its burger patties ignited controversy after saying that it wanted to introduce "dynamic pricing" in which the cost of many of the items on its menu will vary depending on the time of day. In an earnings call, chief executive Kirk Tanner said that electronic billboards would allow restaurants to display various deals and promotions during slower times in the early morning and late at night.

Outcry was swift and Wendy's ended up walking back its plans with words that they were "misconstrued" as an intent to surge prices during its most popular periods.

While the company issued a statement saying that any changes were meant as "discounts and value offers" during quiet periods rather than raised prices during busy ones, the reputational damage was already done since many saw the clarification as another way to obfuscate its pricing model.

"We said these menuboards would give us more flexibility to change the display of featured items," Wendy's said in its statement. "This was misconstrued in some media reports as an intent to raise prices when demand is highest at our restaurants."

The Daylight Savings Time promotion, in turn, is also a way to demonstrate the kinds of deals Wendy's wants to promote in its stores without putting up full-sized advertising or posters for what is only relevant for a few days.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemicUncategorized

Inside The Most Ridiculous Jobs Report In Recent History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In Recent History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Walmart launches clever answer to Target’s new membership program

Wendy’s has a new deal for daylight savings time haters

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Catastrophic Risk: Investing and Business Implications

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Gather ’round the crystal ball: A multi-commodity outlook from PDAC 2024

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 hours ago

Walmart launches clever answer to Target’s new membership program

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex