Futures Flat Ahead Of ECB, Powell Doubleheader

Futures Flat Ahead Of ECB, Powell Doubleheader

US stock futures traded flat, erasing modest earlier gains and losses in the overnight session…

Share this:

US stock futures traded flat, erasing modest earlier gains and losses in the overnight session as investors remained cautious while watching for signs of a softening in the Federal Reserve’s policy. Nasdaq 100 futures were little changed by 7:15 a.m. in New York after earlier gaining as much as 0.6%. S&P 500 contracts were up less than 0.1%, at 3,983.75 after hitting 3,996 overnight and following small gains in Estoxx50. The underlying index notched its biggest gain in a month on Wednesday which was sparked by yet another short squeeze, and is attempting to rebound following three straight weeks of declines that were fueled by fading bets on a Fed policy pivot and as investors braced for the impact of a potential economic contraction. Crude oil futures managed a feeble, +0.5% bounce after falling 5.7% Wednesday. The dollar reversed earlier gains helping lift the badly beaten EUR and JPY higher.

Among notable movers in premarket trading, American Eagle Outfitters slumped as much 16% after the retailer reported results for a quarter that Citigroup analysts described as “rough,” while also pausing its quarterly cash dividend. GameStop jumped as much as 12% in US premarket trading after the announcement of a partnership with cryptocurrency exchange FTX US, though the gaming company reported net sales for the second quarter that missed estimates. Here are some other notable premarket movers:

- Asana gains 18% in premarket trading after the software company boosted its revenue guidance for the full year. Separately, the company said CEO Dustin Moskovitz bought $350 million of shares in a private placement.

- Moderna (MRNA US) gains 2.2% in premarket trading after Deutsche Bank upgraded the stock to buy from hold after its “solid” second quarter earnings beat and the “welcome” late- July news of additional fall 2022 orders from the US.

- Apple (AAPL US) shares were steady in premarket trading as analysts say the biggest takeaway from the company’s product event was its pricing strategy, with the iPhone maker opting not to raise average prices for its latest smartphone and watch models.

- Keep an eye on Intel (INTC US) as the stock is started with a hold rating and $32 price target at Stifel, which cites uncertainty over the chipmaker’s turnaround strategy. Stifel also started Nvidia (NVDA US) with a hold recommendation and AMD (AMD US) with a buy rating.

- Chipmakers may also be in focus after TSMC, the world’s largest supplier of made-to-order chips, said sales rose 59% in August from a year earlier. In the US, watch equipment stocks such as Applied Materials (AMAT US), KLA (KLAC US), Lam Research (LRCX US), Entegris (ENTG US), Teradyne (TER US), and MKS Instruments (MKSI US)

Sentiment improved on Wednesday after Fed Vice Chair Lael Brainard warned that “two-sided” risks will eventually emerge from tightening monetary policy -- remarks that were considered to have a more dovish tone than some other recent Fed comments. Focus on Thursday will be on a speech by Chair Jerome Powell, who is scheduled to speak just after a monetary policy decision by the European Central Bank.

Still, strategists warn that risks to a sustained rally are growing. “Sentiment is very depressed and markets are oversold,” Frederique Carrier, head of investment strategy at RBC Wealth Management, said on Bloomberg TV. “It’s possible that there is a rally, but as long as the Fed is increasing interest rates, it’s very difficult for the upside to be very strong.”

As central banks are walking a tightrope, moving sharply to tackle price pressures while remaining leery of sparking a damaging economic contraction in the process, today we get a central bank doubleheader with the ECB expected to hike rates by 75bps at 8:15am, while Jerome Powell speaks at a monetary conference at 9:10am ET. The Euro is holding around parity against the dollar ahead of the ECB, where money markets price in around 65bp of rate hikes for the meeting, with most economists expecting a 75bp rate hike. The focal point of US session after ECB is Powell participation in moderated discussion at a monetary policy conference.

“What we are seeing in Europe is very, very concerning, what is happening there is the worst energy crisis we have seen since the oil embargo in 70s,” Ryan Lemand, Securrency Capital advisor to the board, said on Bloomberg Television. “Europe will face a recession, one of the worst recessions it will have faced and I don’t think risky assets are pricing this in correctly.”

Fed officials reiterated their determination to get inflation under control. Vice Chair Lael Brainard said interest rates will need to rise to restrictive levels, while cautioning risks would become more two-sided in the future. The Fed’s Beige Book report said US economic expansion prospects were weak, while adding that price growth showed signs of decelerating.

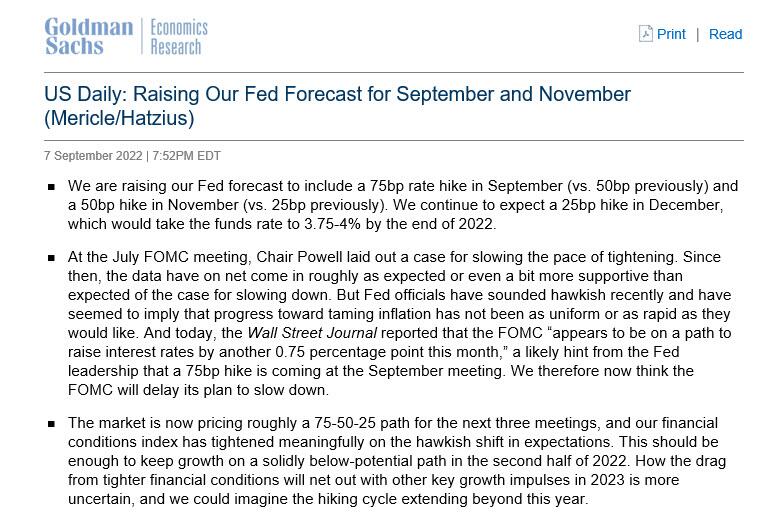

Goldman economists lifted their forecast for the pace of Fed interest rate increases, expecting the Fed to hike by 75 basis points this month and 50 basis points in November, up from previous forecasts of 50 basis points and 25 basis points respectively. They are tipping a 25 basis points move in December.

Deutsche Bank AG strategists also said that elevated “late-cycle earnings,” higher valuations and the risk of a recession limit the fundamental case for a sustained rally in US stocks. In their worst case scenario, they see the S&P 500 slumping to 3,000 points in the event of a recession -- almost 25% below its latest close. However, their base case still calls for equities to rise by year end.

In Europe, the Stoxx 50 rose 0.1%, surrendering most of an initial 0.6% advance as retailers slumped after a profit warning from Primark-owner Associated British Foods Plc. The FTSE 100 outperformed peers, adding 0.4%, IBEX lags, dropping 0.2%. Insurance, banks and miners are the strongest-performing sectors. Here are the biggest European movers:

- Genus shares jump as much as 16%, the most since May 2019, after Peel Hunt upgraded the firm to buy, saying its business was “back on the front foot” after publishing FY earnings

- SBB shares jumped as much as 11% during early trading in Stockholm after signing a letter of intent to sell SEK9 billion worth of properties to an unidentified institutional investor

- European semiconductor stocks rise on Thursday, after chipmaking bellwether TSMC reported an acceleration in sales in August and Apple launched a new lineup of devices

- Ocado shares advance as much as 4.4% after being upgraded to equal-weight from underweight at Barclays, which says the risks are now “more evenly balanced” for the online grocer

- Alleima gains as much as 6.1% after Danske Bank initiated coverage of the shares with a buy recommendation, where it sees “plenty of value,” also expecting it to benefit from a cyclical recovery

- Munters shares rise as much as 7.6% after Nordea upgraded the Swedish climate and cooling manufacturer to buy on “surging order intake,” raising adjusted Ebita estimates for 2023 and 2024

- Energean shares rise as much as 15% after it increased medium-term financial targets in its 1H report and a quarterly dividend helped by what Peel Hunt called “robust operational performance”

- Atos shares tumble to the lowest level since 1993 after Goldman Sachs downgrades the French tech firm to sell from neutral, citing low visibility and a long path to recovery

- Darktrace shares plunge as much as 35%, the most on record, after M&A talks with Thoma Bravo collapsed, with the suitor not intending to make an offer for the UK cybersecurity company

- AB Foods shares drop as much as 8.6% after the Primark owner said it expects FY23 adjusted operating profit and adjusted earnings per share to be lower than this financial year

- Somfy fell as much as 13% after the French maker of windows and doors warned of a possible pullback in consumer spending after its 1H results were hurt by a slowdown in growth

Earlier in the session, Asian stocks rebounded from their lowest level in more than two years as oil prices eased and the region’s suppliers to Apple Inc. climbed after the US company unveiled new lineups for its iPhones and watches. The MSCI Asia Pacific Index rose as much as 1.3%, snapping a five-day slump, as technology and industrial shares advanced. Japan gained along with Australia and Taiwan, while China dropped as Chengdu extended a week-long lockdown in most downtown areas after Covid-19 cases increased. Asian stocks regained some footing amid a rout that still has the market on course for its fourth-straight week of losses. A two-day retreat in long-term US Treasury yields and Wednesday’s plunge in oil prices helped lift sentiment that had been hurt by concerns over a hawkish Federal Reserve.

“Markets have started to price in a less aggressive Fed, while falling oil and other commodity prices have also helped to ease profit-margin pressures for Asian companies,” Soo Hai Lim, head of Asia ex-China equities at Barings, wrote in a note. “In the longer term, we believe the performance of individual Asian markets will be driven by country-specific growth factors.” Asian stocks are down more than 4% this month amid an outflow of funds from the region. Still, some investors believe that attractive valuations will lure money back and spur a rebound. Read: ‘Massive Discount’ Has Robeco Eyeing 2003-Like Asia Stock Bounce

Japanese stocks gained, with the Topix climbing the most since July 20, after a rally in US shares and a weak yen boosted exporters. The Topix rose 2.2% to 1,957.62 at the 3pm close in Tokyo, while the Nikkei 225 advanced 2.3% to 28,065.28. Toyota Motor contributed the most to the Topix’s gain, increasing 2.3%. Out of 2,169 stocks in the index, 1,947 rose and 161 fell, while 61 were unchanged. Shares also climbed after Japanese GDP data showed the economy grew at a faster pace last quarter than earlier estimates. “Japanese stocks look attractive to dollar-denominated investors in the short term,” said Tetsuo Seshimo, portfolio manager at Saison Asset Management. “It makes it easier to buy when there’s a bit of a risk-on mood.”

Australian stocks gained most in ten weeks on RBA Lowe's comments. The S&P/ASX 200 index rose 1.8% to close at 6,848.70, staging an afternoon rally after the RBA’s chief signaled a potential end to outsized interest rate hikes. Mining and banking shares provided the biggest boost to the benchmark. Reserve Bank Governor Philip Lowe said the case for a slower pace of tightening becomes stronger as the cash rate moves higher. The central bank delivered a fourth straight half-point hike this week to take the cash rate to 2.35%. Energy shares declined as oil fell to a near eight-month low before steadying, with investors assessing the outlook for demand as China pushes on with its Covid Zero policy and central banks tighten monetary policy. In New Zealand, the S&P/NZX 50 index rose 1.1% to 11,677.93

Indian stocks rose, snapping two sessions of declines, as a drop in crude oil prices below $90 per barrel raised optimism of lower import costs and softer consumer prices. The S&P BSE Sensex gained 1.1% to 59,688, its highest level in three weeks, while the NSE Nifty 50 Index advanced 1%. ICICI Bank contributed the most to the Sensex, which had 24 of 30 member shares ending higher. Fourteen of 19 sectoral sub-indexes compiled by BSE Ltd. advanced, led by a gauge of banks. Price of Brent crude, a major import for India, hovered around $88 per barrel, their lowest level since early February

In FX, the pound pared a decline as UK Prime Minister Liz Truss outlined plans to provide relief on rising energy costs to British households and businesses, which she said is expected to curb inflation. There has been widespread speculation that the government’s aid proposals will require further debt sales to fund it that could drive up bond yields. Short-end gilts steadied after rallying Wednesday on bets the plan would calm inflation. Other notable movers:

- A dollar gauge was steady as traders assessed comments from Federal Reserve officials on their commitment to fighting inflation.

- The euro was little changed against the dollar. On European bond markets, two-year German yields rose by around 5 basis points, while the Italian two-year yield fell by one basis point. Market pricing for the following ECB meetings picked up slightly. Just one jumbo rate hike from the European Central Bank may not cut it for euro bulls looking for a sustainable move above parity with the dollar

- The yen gave up an earlier modest advance to trade below 144 per dollar after senior Japanese officials met for the first time since June to discuss markets but said their stance remained the same

- The Australian dollar slumped and Australian sovereign bonds jumped after Reserve Bank Governor Philip Lowe signaled a potential end to outsized interest-rate increases. Australian dollar underperformed all its Group-of-10 peers

In rates, Treasuries steadied after rallying as Australia’s central bank chief signaled a potential end to outsized policy moves; they were slightly richer from belly out to the long-end of the curve with price action light ahead of ECB policy rate decision at 8:15am ET. US yields were richer by up to 2bp across belly of the curve with 2s5s, 2s10s spreads both flatter by around 2bp on the day as front-end underperforms; 10-year yields around 3.25% with bunds and gilts lagging by 3bp and 2bp in the sector after an earlier rally spurred by RBA signaling a potential end to outsized interest-rate increases, making it an outlier in G-10. Bunds yield curve bear-flattens with 2-year yield up 3.6bps to around 1.12%, underperforming USTs and gilts. Both 10-year and 2-year gilts yields trade around 3% as traders gear for details of the new economic package from Truss. Futures gained during Asia session after RBA’s dovish policy pivot, following Aussie bonds higher before fading slightly over London morning. IG dollar issuance slate includes Mitsubishi HC $500m 5Y; six borrowers priced $10b on Wednesday, follows Tuesday’s massive $33b over 44 tranches. Three-month dollar Libor +4.17bp to 3.23571%.

In commodities, oil trimmed a sharp slide this week sparked by demand risks from monetary tightening and China’s Covid travails -- the megacity of Chengdu extended a weeklong lockdown in most downtown areas. Gold added $1 to ~$1,719. Most base metals trade in the green; LME aluminum rises 1.4%, outperforming peers. LME nickel lags, dropping 1.3%.

Bitcoin trades relatively flat just above USD 19,000 whilst Ethereum remains north of USD 1,600.

To the day ahead now, and the ECB policy decision will be the main highlight, along with President Lagarde’s press conference. Otherwise, we’ll also hear from Fed Chair Powell and the Fed’s Evans and Kashkari. Finally, data releases include the weekly initial jobless claims from the US.

Market Snapshot

- S&P 500 futures down 0.1% to 3,975.00

- STOXX Europe 600 little changed at 412.42

- MXAP up 1.0% to 152.06

- MXAPJ up 0.3% to 498.31

- Nikkei up 2.3% to 28,065.28

- Topix up 2.2% to 1,957.62

- Hang Seng Index down 1.0% to 18,854.62

- Shanghai Composite down 0.3% to 3,235.59

- Sensex up 0.8% to 59,518.06

- Australia S&P/ASX 200 up 1.8% to 6,848.67

- Kospi up 0.3% to 2,384.28

- German 10Y yield little changed at 1.59%

- Euro down 0.2% to $0.9984

- Gold spot down 0.1% to $1,717.37

- U.S. Dollar Index little changed at 109.81

Top Overnight News from Bloomberg

- With the greenback supercharged by expectations of higher-for- longer US interest rates, traders are struggling to pick the bottom for Asian currencies

- The European Union may need additional stimulus measures if the economic downturn worsens, according to the bloc’s economy chief, who warned that the coming winter could be “one of the worst in history”

- Investors are bracing for details of UK Prime Minister Liz Truss’s new economic package, with some warning that a new wave of debt issuance to fund the spending risks roiling debt markets and pressuring the battered pound

- Inflation in Hungary accelerated to the highest level since 1998 in August as food prices increased by almost a third, according to stats office data. Consumer prices rose an annual 15.6% in August after 13.7% growth in July

- Russian Deputy Finance Minister Timur Maksimov said the government plans to resume sales of its bonds, known as OFZs, as early as this month, Interfax reports

A more detailed look at global markets

Asia-Pacific stocks were mostly positive after the relief rally on Wall St where a lower yield environment and declines in oil prices underpinned risk appetite, although Chinese markets underperformed on COVID woes. ASX 200 was positive with tech and gold miners leading the advances across nearly all sectors aside from energy after the recent fall in oil. Nikkei 225 surged towards the 28,000 level with sentiment lifted following the larger-than-expected upward revisions to Q2 GDP. Hang Seng and Shanghai Comp underperformed their regional peers after the megacity of Chengdu extended its lockdown in most areas and Shenzhen also temporarily lowered its entry quota for Hong Kong travellers amid a resource squeeze from the ongoing outbreak.

Top Asian News

- China Health Authority encourages people to stay put during China National Day holidays (Oct 1st-7th), and to avoid travel outside their cities, via Reuters. China Transport Ministry Official said daily average travel for mid-Autumn festival expected to drop 32% Y/Y.

- RBA Governor Lowe said further rate rises will be required but they are not on a preset path and said the case for a slower pace of rate hikes becomes stronger as the level of the Cash Rate increases. Lowe also commented that demand has to grow more slowly to bring it back in line with supply and there is a significant demand element to higher inflation, while he added it is very possible that wage growth does not pick up much further and said quantitative tightening is not on the agenda.

- Japanese top currency diplomat Kanda said MoF, BoJ, and FSA meeting produced no statement this time as basic understanding on FX remains unchanged from the prior meeting. Japanese top currency diplomat Kanda agreed at the meeting on the need to watch markets with a strong sense of urgency, will not rule out any step, and are ready to take action in the FX market; BoJ and Govt are extremely worried about the recent JPY moves.

- Japan Deputy Chief Cabinet Secretary said it is watching FX moves with high sense of urgency, ready to take necessary steps if recent FX moves continue. When asked about potential intervention, said he would not comment on specific market views. Will make decisions at the appropriate time regarding both economic sentiment and inflation when asked about supplementary budget

European bourses trade with a directionless bias on ECB day after waning off best levels, and following a mixed APAC handover. European sectors are now mixed (vs mostly firmer at the open), with defensives making their way up the ranks. Stateside, US equity futures are portraying a similar tentativeness as their European counterparts, with the main contracts trading on either side of the flat mark but holding onto yesterday’s gains.

Top European News

- Primark Drags Down AB Foods Outlook as Energy Costs Rise

- Commerzbank Says Profit Target Remains Despite Energy Crisis

- Euro Holding Parity Needs Uber-Hawkish Meet: ECB Cheat Sheet

- Sampo Plans Dual Listing in Stockholm to Boost Liquidity

- Zurich Cuts Swimming Pool Temperatures to Save Energy

FX

- DXY pulled back further from Wednesday’s new y-t-d and multi-year peak before finding support just under 109.500.

- The EUR briefly popped over parity and the JPY pared more losses from its worst levels in around 24 years vs the USD.

- The Kiwi and Aussie both have cause to underperform given a deceleration in NZ manufacturing sales, bleak Australian trade data and remarks from RBA Governor Lowe.

Fixed Income

- Bunds and Gilts sit far from best levels between 145.82-144.71 and 106.84-105.75 parameters.

- Conversely, US Treasuries are treading water ahead of jobless claims and Fed chair Powell, albeit also off overnight peaks

Commodities

- WTI and Brent front-month futures trade volatile with two-way action seen in the European morning.

- JPMorgan believes OPEC+ will need to cut another 1mln BPD to stabilise the market.

- Spot gold holds onto yesterday’s gains north of USD 1,700/oz, but under the USD 1,726.79/oz high set on Tuesday

- Base metals are mostly firmer but the upside is capped by China’s COVID woes, nonetheless, 3M LME copper is supported by reports that Workers at Chile's Escondida copper mine voted to strike over safety concerns.

- Russian Finance Minister considers it reasonable to build reserves in gold and Yuan, according to Tass.

US Event Calendar

- 08:30: Aug. Continuing Claims, est. 1.44m, prior 1.44m

- 08:30: Sept. Initial Jobless Claims, est. 235,000, prior 232,000

- 15:00: July Consumer Credit, est. $32b, prior $40.2b

Central Banks

- 09:10: Powell Speaks at Monetary Policy Conference

- 12:00: Fed’s Evans speaks on economy, policy at DuPage forum

- 14:20: Fed’s Kashkari Makes Introductory Remarks at Labor Market...

DB's Jim Reid concludes the overnight wrap

Readers could be forgiven for losing track of the various themes in markets right now, after a volatile 24 hours that’s seen oil prices crash to their lowest level in months, the dollar reach another multi-decade high, a WSJ article that cemented expectations for another 75bps Fed hike this month, but an S&P 500 that relentlessly marched higher all day to close +1.83%. Indeed even as the likelihood rose that we could see a more rapid pace of near-term hikes, both equities and sovereign bonds rallied yesterday, since the commodity declines raised hopes that central banks could afford to slow up on rate hikes when we get to 2023. Today could put that narrative under pressure however, as there’s a decent chance we’ll see the largest ECB hike in their history, and we’re also set to hear from Fed Chair Powell in his last appearance before the next FOMC meeting.

Running through those specific moves, oil prices took a significant tumble yesterday as concerns about the strength of global demand continued to fester. Indeed, Brent crude (-5.55%) closed beneath $90/bbl for the first time since early February, before Russia’s invasion of Ukraine began, whilst WTI fell -5.69% to $81.85/bbl. Brent futures are back up c.+1% this morning in Asia. One factor behind the declines has been the continued pursuit of the zero-Covid strategy in China, and we got confirmation yesterday that Chengdu (population 21 million) would be extending its lockdown in most of the city. Even European Gas (-10.82%) fell and is now down -28.47% from the intra-day peak on Monday as the market digested the latest NS1 closure announced after the close on Friday. Since then we’re actually down -14.78%. How much of this is a demand destruction story this week and how much is a “we now have peak bad news on European gas supplies” is one to debate.

On the commodities topic, at 12:00 London time today I’ll be speaking on a client call on the outlook for commodities, China and inflation. It’s hosted by DB’s metals and mining team, and I’ll be joined by their head Liam Fitzpatrick, our chief China economist Yi Xiong, and our head of Asian property equity research, Lucia Kwong. Industrial commodities have come under heavy pressure in recent months since peaking earlier this year, so is this the end of the bullish mining and commodities trade, or a cyclical blip within a larger structural uptrend? For further details on the call and how to register, click here.

The continued decline in oil prices has been welcome news from an inflation perspective, and US gasoline prices are now down by nearly a quarter since their peak in mid-June. And in turn, the prospect that central banks don’t need to hike rates as aggressively if inflation is subdued (rightly or wrong) helped both equities and bonds to stage a strong rally over yesterday’s session. For instance, the S&P 500 (+1.84% yesterday) is now on track to end a run of three consecutive weekly declines, where only the Energy (-1.15%) sector ended in the red and every other sector gained at least +1%, a broad-based gain. Germany’s DAX (+0.35%) also recovered from its initial losses of more than -1% to move higher on the day. In the meantime, yields on 10yr Treasuries (-8.6bps), bunds (-6.1bps), OATs (-7.7bps) and BTPs (-11.4bps) all declined, which makes a change from the awful run that sovereign bonds have been on over recent weeks. As we go to print, we are another -3.6bps lower on the 10yr USTs but less than a basis point lower for 2yrs.

Indeed, when it comes to the next couple of weeks, it looks as though the series of bumper rate hikes is set to continue. There was a noticeable reaction in Fed funds futures yesterday after the WSJ’s Nick Timiraos published an article saying that Chair Powell’s pledge to tackle inflation “appears to have put the central bank on a path” to a 75bps hike. Remember it was Timiraos’ article back in June that was seen as setting the stage for the first 75bps hike of this cycle (rather than 50bps as previously expected), so his articles do carry weight in markets. That was apparent in futures, which are now pricing in +69.5bps worth of hikes for the September meeting, which is the most hawkish markets have been on September since the last meeting in July. Fed speakers continued to weigh in yesterday. Notably, Fed Vice Chair Brainard noted the Fed’s commitment to bring inflation under order, and the risks of inflation expectations moving higher, while at the same time paying heed to the two-sided risks of over-doing tightening. In short, her remarks didn’t do anything to discourage markets from pricing a larger hike in September and from pricing in lower yields out the curve. As noted, Fed Chair Powell will follow up at a conference later this morning.

Speaking of rate hikes, the focus today will be on the ECB’s latest decision, where the consensus among both market pricing and economists is that they’ll follow the Fed’s moves in June and July and similarly hike by a bumper 75bps. Our own economists at DB are also expecting a 75bps move, and if realised this would be the largest ECB hike since the formation of the single currency, so a historic move. In our economists’ view, the factors tipping the balance towards a larger hike are the upside inflation surprises (hitting a record +9.1% in August), along with the significant minority of Governing Council members publicly calling for 75bps to be on the table. You can see their full preview here.

Staying on this theme, overnight, the Reserve Bank of Australia (RBA) Governor Philip Lowe reiterated that further rate rises are required to cool inflation while signalling that the hikes could be smaller in the coming months. Comments from the Governor indicated that he is hopeful that the central bank can navigate the narrow path to a soft landing despite badly misreading the growing inflation crisis. Aussie yields are around -15bps lower across the curve with two-thirds of the move coming after Lowe's speech. So a big reaction.

Another focus today will be the UK once again, as new PM Truss is set to announce the government’s plan on energy bills in the House of Commons. According to media reports, that will involve bills being frozen around their current levels, rather than rising in October in line with the increase in the energy price cap. However, there was a tough market backdrop yesterday, as sterling fell to its weakest intraday level against the US Dollar since 1985, hitting $1.1406 at one point before recovering to end the day at $1.1533. To be fair, a good chunk of sterling’s recent weakness has been down to dollar strength, with the dollar index currently up by +14.72% YTD, leaving it on track for its biggest annual gain since 1981, when it strengthened +15.8%. But when it came to yesterday, it was certainly a story of sterling weakness, as it fell -0.89% against the Euro too.

Asian equity markets are mixed this morning following Wall Street’s solid rebound overnight. As I type, the Nikkei (+2.05%) is leading gains across the region with the Kospi (+0.55%) also trading in positive territory. Over in mainland China, stocks are slightly down with the Shanghai Composite (-0.08%) and CSI (-0.04%) both struggling for direction on the extension of a lockdown in the city of Chengdu while the Hang Seng (-0.53%) is slipping in early trade. US stock futures are little changed with contracts on the S&P 500 (+0.06%) and NASDAQ 100 (+0.09%) marginally higher after yesterday’s rally.

Early this morning, the final estimate of Japan’s GDP showed that the economy expanded an annualised +3.5% in the second quarter (+2.9% expected) up from the initial reading of +2.2% growth as the removal of local Covid-19 restrictions boosted consumer and business spending. Separately, Australia recorded a record drop in its trade surplus, narrowing to A$8.7 bn in July from A$17.7 bn a month before mainly due to declining iron ore and coal exports. At the same time, exports in July declined -10.0% (-8.0% expected) from the month before while imports rose +5%.

Back to yesterday and the theme of hawkish central banks continued (notwithstanding the Aussie news this morning), as the Bank of Canada hiked by 75bps, whilst outlining their view that “the policy interest rate will need to rise further.” Meanwhile on the data side, we heard that the Euro Area economy grew faster than previously thought in Q2, with a +0.8% expansion (vs. +0.6% previous estimate). Finally, German industrial production in July contracted by a smaller-than-expected -0.3% (vs. -0.6% expected).

To the day ahead now, and the ECB policy decision will be the main highlight, along with President Lagarde’s press conference. Otherwise, we’ll also hear from Fed Chair Powell and the Fed’s Evans and Kashkari. Finally, data releases include the weekly initial jobless claims from the US.

Government

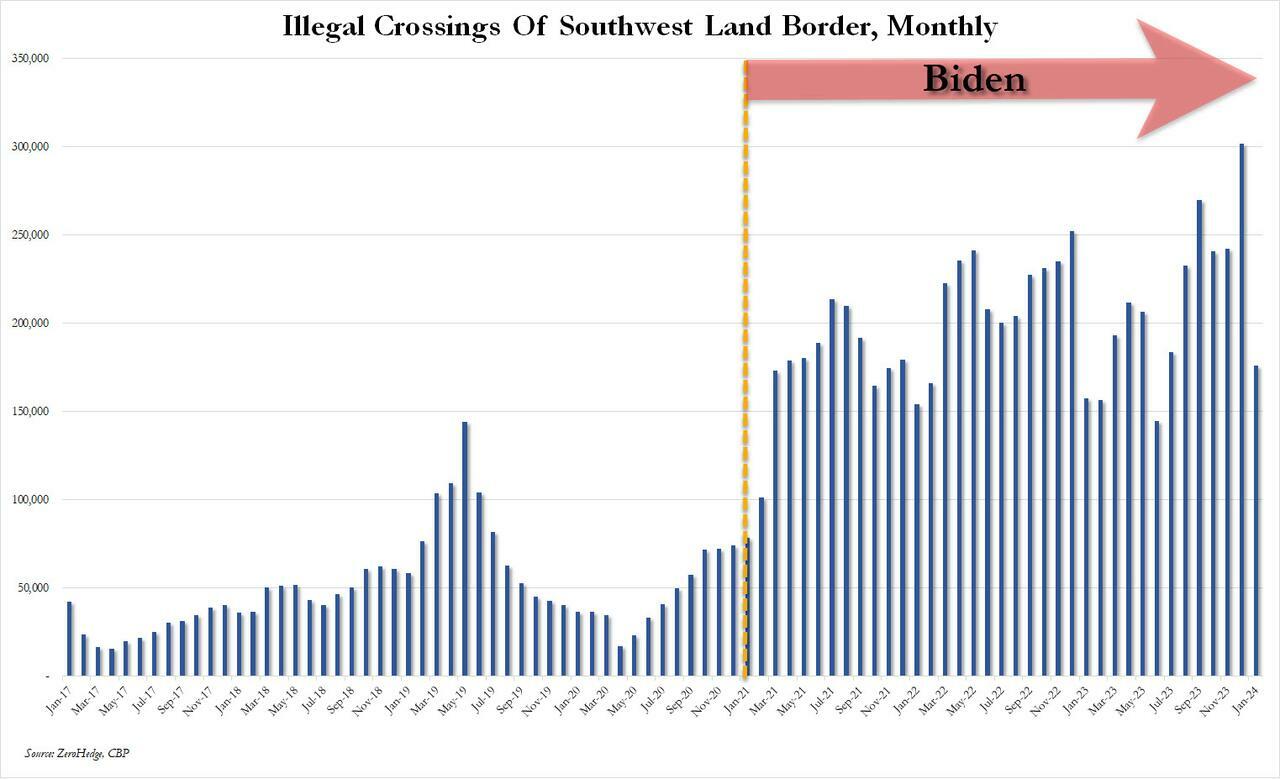

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While "Waiting" For Deporation, Asylum

Over the past several…

Share this:

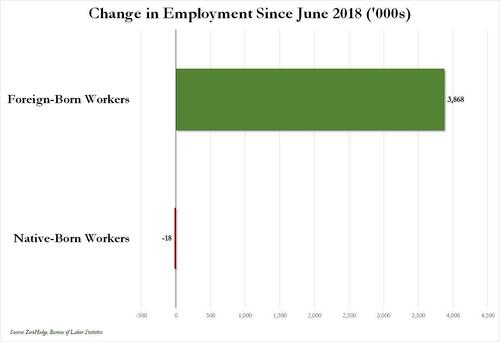

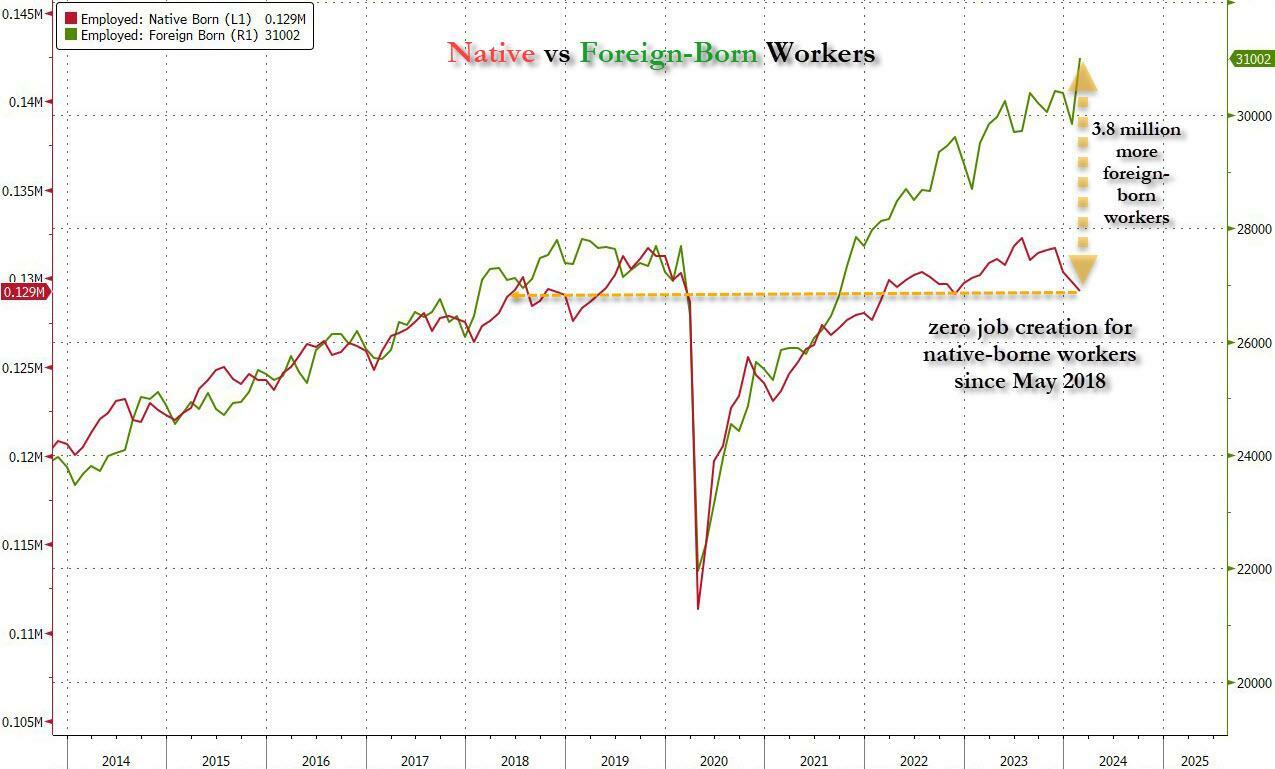

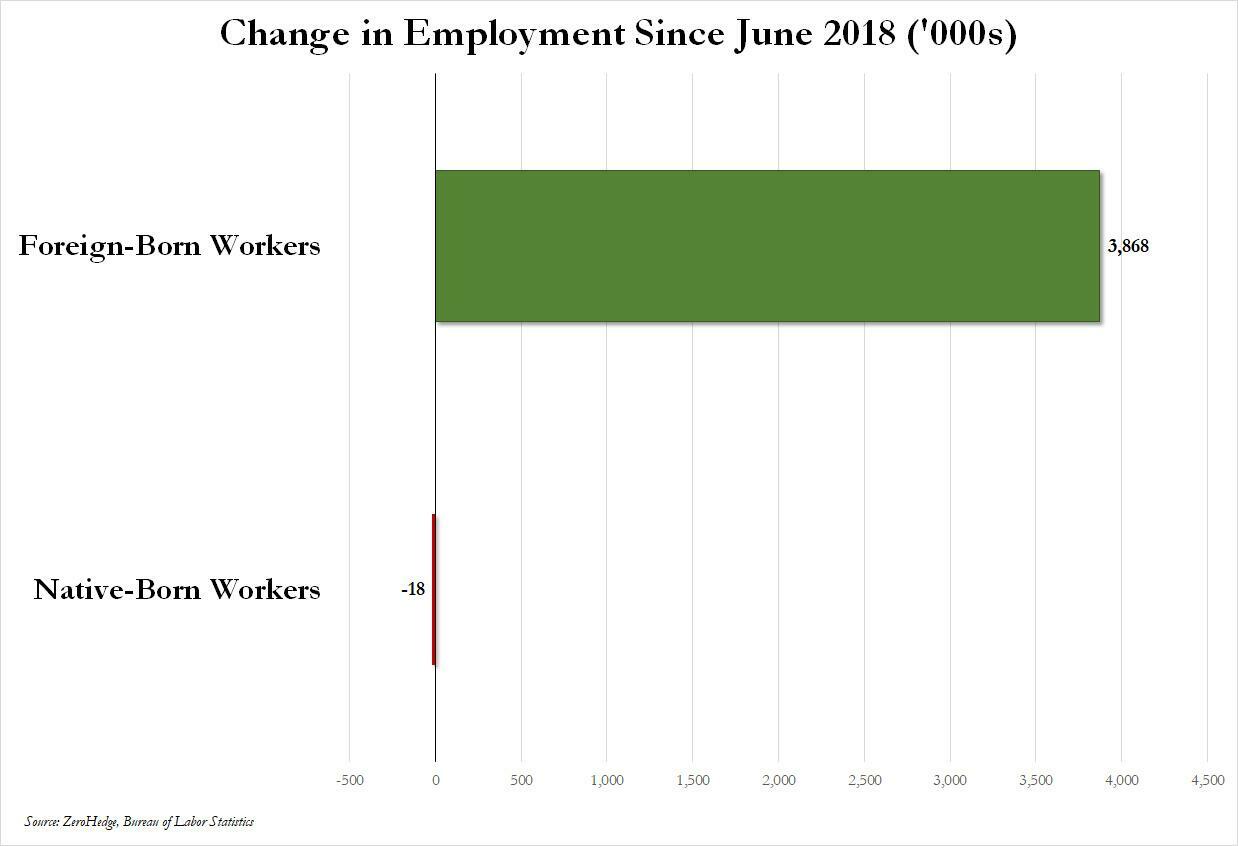

Over the past several months we've pointed out that there has been zero job creation for native-born workers since the summer of 2018...

... and that since Joe Biden was sworn into office, most of the post-pandemic job gains the administration continuously brags about have gone foreign-born (read immigrants, mostly illegal ones) workers.

And while the left might find this data almost as verboten as FBI crime statistics - as it directly supports the so-called "great replacement theory" we're not supposed to discuss - it also coincides with record numbers of illegal crossings into the United States under Biden.

In short, the Biden administration opened the floodgates, 10 million illegal immigrants poured into the country, and most of the post-pandemic "jobs recovery" went to foreign-born workers, of which illegal immigrants represent the largest chunk.

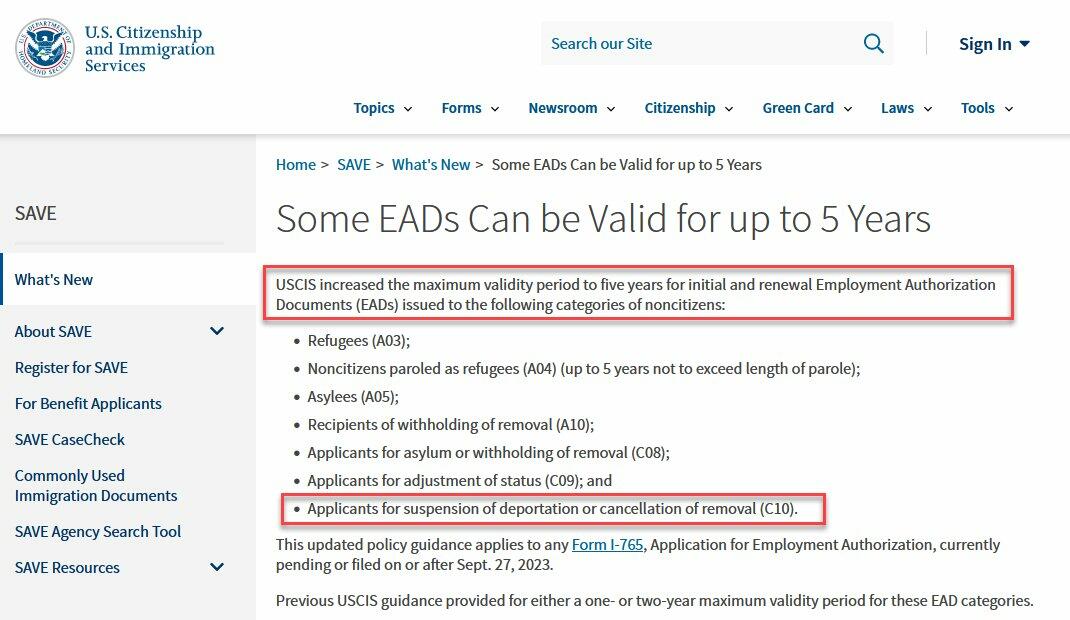

'But Tyler, illegal immigrants can't possibly work in the United States whilst awaiting their asylum hearings,' one might hear from the peanut gallery. On the contrary: ever since Biden reversed a key aspect of Trump's labor policies, all illegal immigrants - even those awaiting deportation proceedings - have been given carte blanche to work while awaiting said proceedings for up to five years...

... something which even Elon Musk was shocked to learn.

Wow, learn something new every day https://t.co/8MDtEEZGam

— Elon Musk (@elonmusk) March 10, 2024

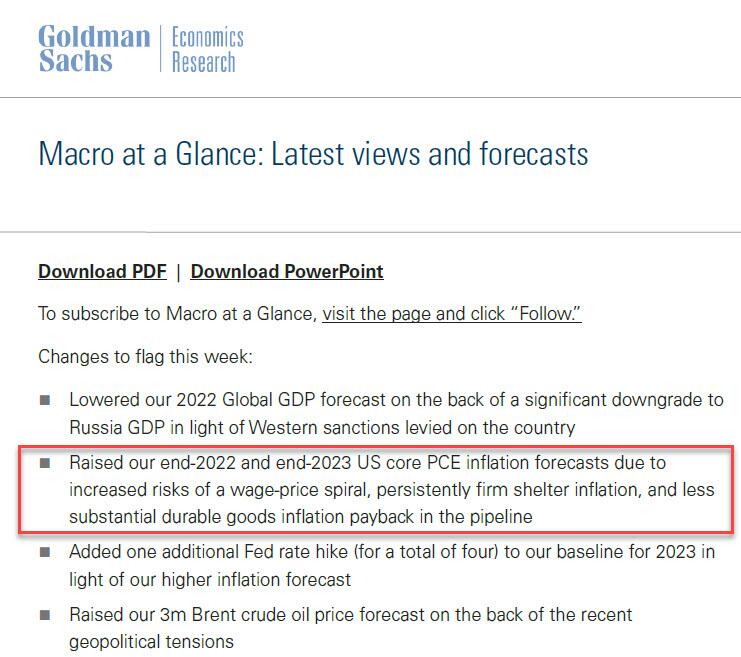

Which leads us to another question: recall that the primary concern for the Biden admin for much of 2022 and 2023 was soaring prices, i.e., relentless inflation in general, and rising wages in particular, which in turn prompted even Goldman to admit two years ago that the diabolical wage-price spiral had been unleashed in the US (diabolical, because nothing absent a major economic shock, read recession or depression, can short-circuit it once it is in place).

Well, there is one other thing that can break the wage-price spiral loop: a flood of ultra-cheap illegal immigrant workers. But don't take our word for it: here is Fed Chair Jerome Powell himself during his February 60 Minutes interview:

PELLEY: Why was immigration important?

POWELL: Because, you know, immigrants come in, and they tend to work at a rate that is at or above that for non-immigrants. Immigrants who come to the country tend to be in the workforce at a slightly higher level than native Americans do. But that's largely because of the age difference. They tend to skew younger.

PELLEY: Why is immigration so important to the economy?

POWELL: Well, first of all, immigration policy is not the Fed's job. The immigration policy of the United States is really important and really much under discussion right now, and that's none of our business. We don't set immigration policy. We don't comment on it.

I will say, over time, though, the U.S. economy has benefited from immigration. And, frankly, just in the last, year a big part of the story of the labor market coming back into better balance is immigration returning to levels that were more typical of the pre-pandemic era.

PELLEY: The country needed the workers.

POWELL: It did. And so, that's what's been happening.

Translation: Immigrants work hard, and Americans are lazy. But much more importantly, since illegal immigrants will work for any pay, and since Biden's Department of Homeland Security, via its Citizenship and Immigration Services Agency, has made it so illegal immigrants can work in the US perfectly legally for up to 5 years (if not more), one can argue that the flood of illegals through the southern border has been the primary reason why inflation - or rather mostly wage inflation, that all too critical component of the wage-price spiral - has moderated in in the past year, when the US labor market suddenly found itself flooded with millions of perfectly eligible workers, who just also happen to be illegal immigrants and thus have zero wage bargaining options.

None of this is to suggest that the relentless flood of immigrants into the US is not also driven by voting and census concerns - something Elon Musk has been pounding the table on in recent weeks, and has gone so far to call it "the biggest corruption of American democracy in the 21st century", but in retrospect, one can also argue that the only modest success the Biden admin has had in the past year - namely bringing inflation down from a torrid 9% annual rate to "only" 3% - has also been due to the millions of illegals he's imported into the country.

We would be remiss if we didn't also note that this so often carries catastrophic short-term consequences for the social fabric of the country (the Laken Riley fiasco being only the latest example), not to mention the far more dire long-term consequences for the future of the US - chief among them the trillions of dollars in debt the US will need to incur to pay for all those new illegal immigrants Democrat voters and low-paid workers. This is on top of the labor revolution that will kick in once AI leads to mass layoffs among high-paying, white-collar jobs, after which all those newly laid off native-born workers hoping to trade down to lower paying (if available) jobs will discover that hardened criminals from Honduras or Guatemala have already taken them, all thanks to Joe Biden.

Spread & Containment

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

The crisis in NHS dentistry is driving increasing numbers abroad for treatment. Here are some of their stories.

Share this:

It’s a hot summer day in the Turkish city of Antalya, a Mediterranean resort with golden beaches, deep blue sea and vibrant nightlife. The pool area of the all-inclusive resort is crammed with British people on sun loungers – but they aren’t here for a holiday. This hotel is linked to a dental clinic that organises treatment packages, and most of these guests are here to see a dentist.

From Norwich, two women talk about gums and injections. A man from Wales holds a tissue close to his mouth and spits blood – he has just had two molars extracted.

The dental clinic organises everything for these dental “tourists” throughout their treatment, which typically lasts from three to 15 days. The stories I hear of what has caused them to travel to Turkey are strikingly similar: all have struggled to secure dental treatment at home on the NHS.

“The hotel is nice and some days I go to the beach,” says Susan*, a hairdresser in her mid-30s from Norwich. “But really, we aren’t tourists like in a proper holiday. We come here because we have no choice. I couldn’t stand the pain.”

This is Susan’s second visit to Antalya. She explains that her ordeal started two years earlier:

I went to an NHS dentist who told me I had gum disease … She did some cleaning to my teeth and gums but it got worse. When I ate, my teeth were moving … the gums were bleeding and it was very painful. I called to say I was in pain but the clinic was not accepting NHS patients any more.

The only option the dentist offered Susan was to register as a private patient:

I asked how much. They said £50 for x-rays and then if the gum disease got worse, £300 or so for extraction. Four of them were moving – imagine: £1,200 for losing your teeth! Without teeth I’d lose my clients, but I didn’t have the money. I’m a single mum. I called my mum and cried.

Susan’s mother told her about a friend of hers who had been to Turkey for treatment, then together they found a suitable clinic:

The prices are so much cheaper! Tooth extraction, x-rays, consultations – it all comes included. The flight and hotel for seven days cost the same as losing four teeth in Norwich … I had my lower teeth removed here six months ago, now I’ve got implants … £2,800 for everything – hotel, transfer, treatments. I only paid the flights separately.

In the UK, roughly half the adult population suffers from periodontitis – inflammation of the gums caused by plaque bacteria that can lead to irreversible loss of gums, teeth, and bone. Regular reviews by a dentist or hygienist are required to manage this condition. But nine out of ten dental practices cannot offer NHS appointments to new adult patients, while eight in ten are not accepting new child patients.

Some UK dentists argue that Britons who travel abroad for treatment do so mainly for cosmetic procedures. They warn that dental tourism is dangerous, and that if their treatment goes wrong, dentists in the UK will be unable to help because they don’t want to be responsible for further damage. Susan shrugs this off:

Dentists in England say: ‘If you go to Turkey, we won’t touch you [afterwards].’ But I don’t worry because there are no appointments at home anyway. They couldn’t help in the first place, and this is why we are in Turkey.

‘How can we pay all this money?’

As a social anthropologist, I travelled to Turkey a number of times in 2023 to investigate the crisis of NHS dentistry, and the journeys abroad that UK patients are increasingly making as a result. I have relatives in Istanbul and have been researching migration and trading patterns in Turkey’s largest city since 2016.

In August 2023, I visited the resort in Antalya, nearly 400 miles south of Istanbul. As well as Susan, I met a group from a village in Wales who said there was no provision of NHS dentistry back home. They had organised a two-week trip to Turkey: the 12-strong group included a middle-aged couple with two sons in their early 20s, and two couples who were pensioners. By going together, Anya tells me, they could support each other through their different treatments:

I’ve had many cavities since I was little … Before, you could see a dentist regularly – you didn’t even think about it. If you had pain or wanted a regular visit, you phoned and you went … That was in the 1990s, when I went to the dentist maybe every year.

Anya says that once she had children, her family and work commitments meant she had no time to go to the dentist. Then, years later, she started having serious toothache:

Every time I chewed something, it hurt. I ate soups and soft food, and I also lost weight … Even drinking was painful – tea: pain, cold water: pain. I was taking paracetamol all the time! I went to the dentist to fix all this, but there were no appointments.

Anya was told she would have to wait months, or find a dentist elsewhere:

A private clinic gave me a list of things I needed done. Oh my God, almost £6,000. My husband went too – same story. How can we pay all this money? So we decided to come to Turkey. Some people we know had been here, and others in the village wanted to come too. We’ve brought our sons too – they also need to be checked and fixed. Our whole family could be fixed for less than £6,000.

By the time they travelled, Anya’s dental problems had turned into a dental emergency. She says she could not live with the pain anymore, and was relying on paracetamol.

In 2023, about 6 million adults in the UK experienced protracted pain (lasting more than two weeks) caused by toothache. Unintentional paracetamol overdose due to dental pain is a significant cause of admissions to acute medical units. If left untreated, tooth infections can spread to other parts of the body and cause life-threatening complications – and on rare occasions, death.

In February 2024, police were called to manage hundreds of people queuing outside a newly opened dental clinic in Bristol, all hoping to be registered or seen by an NHS dentist. One in ten Britons have admitted to performing “DIY dentistry”, of which 20% did so because they could not find a timely appointment. This includes people pulling out their teeth with pliers and using superglue to repair their teeth.

In the 1990s, dentistry was almost entirely provided through NHS services, with only around 500 solely private dentists registered. Today, NHS dentist numbers in England are at their lowest level in a decade, with 23,577 dentists registered to perform NHS work in 2022-23, down 695 on the previous year. Furthermore, the precise division of NHS and private work that each dentist provides is not measured.

The COVID pandemic created longer waiting lists for NHS treatment in an already stretched public service. In Bridlington, Yorkshire, people are now reportedly having to wait eight-to-nine years to get an NHS dental appointment with the only remaining NHS dentist in the town.

In his book Patients of the State (2012), Argentine sociologist Javier Auyero describes the “indignities of waiting”. It is the poor who are mostly forced to wait, he writes. Queues for state benefits and public services constitute a tangible form of power over the marginalised. There is an ethnic dimension to this story, too. Data suggests that in the UK, patients less likely to be effective in booking an NHS dental appointment are non-white ethnic groups and Gypsy or Irish travellers, and that it is particularly challenging for refugees and asylum-seekers to access dental care.

This article is part of Conversation Insights

The Insights team generates long-form journalism derived from interdisciplinary research. The team is working with academics from different backgrounds who have been engaged in projects aimed at tackling societal and scientific challenges.

In 2022, I experienced my own dental emergency. An infected tooth was causing me debilitating pain, and needed root canal treatment. I was advised this would cost £71 on the NHS, plus £307 for a follow-up crown – but that I would have to wait months for an appointment. The pain became excruciating – I could not sleep, let alone wait for months. In the same clinic, privately, I was quoted £1,300 for the treatment (more than half my monthly income at the time), or £295 for a tooth extraction.

I did not want to lose my tooth because of lack of money. So I bought a flight to Istanbul immediately for the price of the extraction in the UK, and my tooth was treated with root canal therapy by a private dentist there for £80. Including the costs of travelling, the total was a third of what I was quoted to be treated privately in the UK. Two years on, my treated tooth hasn’t given me any more problems.

A better quality of life

Not everyone is in Antalya for emergency procedures. The pensioners from Wales had contacted numerous clinics they found on the internet, comparing prices, treatments and hotel packages at least a year in advance, in a carefully planned trip to get dental implants – artificial replacements for tooth roots that help support dentures, crowns and bridges.

In Turkey, all the dentists I speak to (most of whom cater mainly for foreigners, including UK nationals) consider implants not a cosmetic or luxurious treatment, but a development in dentistry that gives patients who are able to have the procedure a much better quality of life. This procedure is not available on the NHS for most of the UK population, and the patients I meet in Turkey could not afford implants in private clinics back home.

Paul is in Antalya to replace his dentures, which have become uncomfortable and irritating to his gums, with implants. He says he couldn’t find an appointment to see an NHS dentist. His wife Sonia went through a similar procedure the year before and is very satisfied with the results, telling me: “Why have dentures that you need to put in a glass overnight, in the old style? If you can have implants, I say, you’re better off having them.”

Most of the dental tourists I meet in Antalya are white British: this city, known as the Turkish Riviera, has developed an entire economy catering to English-speaking tourists. In 2023, more than 1.3 million people visited the city from the UK, up almost 15% on the previous year.

Read more: NHS dentistry is in crisis – are overseas dentists the answer?

In contrast, the Britons I meet in Istanbul are predominantly from a non-white ethnic background. Omar, a pensioner of Pakistani origin in his early 70s, has come here after waiting “half a year” for an NHS appointment to fix the dental bridge that is causing him pain. Omar’s son had been previously for a hair transplant, and was offered a free dental checkup by the same clinic, so he suggested it to his father. Having worked as a driver for a manufacturing company for two decades in Birmingham, Omar says he feels disappointed to have contributed to the British economy for so long, only to be “let down” by the NHS:

At home, I must wait and wait and wait to get a bridge – and then I had many problems with it. I couldn’t eat because the bridge was uncomfortable and I was in pain, but there were no appointments on the NHS. I asked a private dentist and they recommended implants, but they are far too expensive [in the UK]. I started losing weight, which is not a bad thing at the beginning, but then I was worrying because I couldn’t chew and eat well and was losing more weight … Here in Istanbul, I got dental implants – US$500 each, problem solved! In England, each implant is maybe £2,000 or £3,000.

In the waiting area of another clinic in Istanbul, I meet Mariam, a British woman of Iraqi background in her late 40s, who is making her second visit to the dentist here. Initially, she needed root canal therapy after experiencing severe pain for weeks. Having been quoted £1,200 in a private clinic in outer London, Mariam decided to fly to Istanbul instead, where she was quoted £150 by a dentist she knew through her large family. Even considering the cost of the flight, Mariam says the decision was obvious:

Dentists in England are so expensive and NHS appointments so difficult to find. It’s awful there, isn’t it? Dentists there blamed me for my rotten teeth. They say it’s my fault: I don’t clean or I ate sugar, or this or that. I grew up in a village in Iraq and didn’t go to the dentist – we were very poor. Then we left because of war, so we didn’t go to a dentist … When I arrived in London more than 20 years ago, I didn’t speak English, so I still didn’t go to the dentist … I think when you move from one place to another, you don’t go to the dentist unless you are in real, real pain.

In Istanbul, Mariam has opted not only for the urgent root canal treatment but also a longer and more complex treatment suggested by her consultant, who she says is a renowned doctor from Syria. This will include several extractions and implants of back and front teeth, and when I ask what she thinks of achieving a “Hollywood smile”, Mariam says:

Who doesn’t want a nice smile? I didn’t come here to be a model. I came because I was in pain, but I know this doctor is the best for implants, and my front teeth were rotten anyway.

Dentists in the UK warn about the risks of “overtreatment” abroad, but Mariam appears confident that this is her opportunity to solve all her oral health problems. Two of her sisters have already been through a similar treatment, so they all trust this doctor.

The UK’s ‘dental deserts’

To get a fuller understanding of the NHS dental crisis, I’ve also conducted 20 interviews in the UK with people who have travelled or were considering travelling abroad for dental treatment.

Joan, a 50-year-old woman from Exeter, tells me she considered going to Turkey and could have afforded it, but that her back and knee problems meant she could not brave the trip. She has lost all her lower front teeth due to gum disease and, when I meet her, has been waiting 13 months for an NHS dental appointment. Joan tells me she is living in “shame”, unable to smile.

In the UK, areas with extremely limited provision of NHS dental services – known as as “dental deserts” – include densely populated urban areas such as Portsmouth and Greater Manchester, as well as many rural and coastal areas.

In Felixstowe, the last dentist taking NHS patients went private in 2023, despite the efforts of the activist group Toothless in Suffolk to secure better access to NHS dentists in the area. It’s a similar story in Ripon, Yorkshire, and in Dumfries & Galloway, Scotland, where nearly 25,000 patients have been de-registered from NHS dentists since 2021.

Data shows that 2 million adults must travel at least 40 miles within the UK to access dental care. Branding travel for dental care as “tourism” carries the risk of disguising the elements of duress under which patients move to restore their oral health – nationally and internationally. It also hides the immobility of those who cannot undertake such journeys.

The 90-year-old woman in Dumfries & Galloway who now faces travelling for hours by bus to see an NHS dentist can hardly be considered “tourism” – nor the Ukrainian war refugees who travelled back from West Sussex and Norwich to Ukraine, rather than face the long wait to see an NHS dentist.

Many people I have spoken to cannot afford the cost of transport to attend dental appointments two hours away – or they have care responsibilities that make it impossible. Instead, they are forced to wait in pain, in the hope of one day securing an appointment closer to home.

‘Your crisis is our business’

The indignities of waiting in the UK are having a big impact on the lives of some local and foreign dentists in Turkey. Some neighbourhoods are rapidly changing as dental and other health clinics, usually in luxurious multi-storey glass buildings, mushroom. In the office of one large Istanbul medical complex with sections for hair transplants and dentistry (plus one linked to a hospital for more extensive cosmetic surgery), its Turkish owner and main investor tells me:

Your crisis is our business, but this is a bazaar. There are good clinics and bad clinics, and unfortunately sometimes foreign patients do not know which one to choose. But for us, the business is very good.

This clinic only caters to foreign patients. The owner, an architect by profession who also developed medical clinics in Brazil, describes how COVID had a major impact on his business:

When in Europe you had COVID lockdowns, Turkey allowed foreigners to come. Many people came for ‘medical tourism’ – we had many patients for cosmetic surgery and hair transplants. And that was when the dental business started, because our patients couldn’t see a dentist in Germany or England. Then more and more patients started to come for dental treatments, especially from the UK and Ireland. For them, it’s very, very cheap here.

The reasons include the value of the Turkish lira relative to the British pound, the low cost of labour, the increasing competition among Turkish clinics, and the sheer motivation of dentists here. While most dentists catering to foreign patients are from Turkey, others have arrived seeking refuge from war and violence in Syria, Iraq, Afghanistan, Iran and beyond. They work diligently to rebuild their lives, careers and lost wealth.

Regardless of their origin, all dentists in Turkey must be registered and certified. Hamed, a Syrian dentist and co-owner of a new clinic in Istanbul catering to European and North American patients, tells me:

I know that you say ‘Syrian’ and people think ‘migrant’, ‘refugee’, and maybe think ‘how can this dentist be good?’ – but Syria, before the war, had very good doctors and dentists. Many of us came to Turkey and now I have a Turkish passport. I had to pass the exams to practise dentistry here – I study hard. The exams are in Turkish and they are difficult, so you cannot say that Syrian doctors are stupid.

Hamed talks excitedly about the latest technology that is coming to his profession: “There are always new materials and techniques, and we cannot stop learning.” He is about to travel to Paris to an international conference:

I can say my techniques are very advanced … I bet I put more implants and do more bone grafting and surgeries every week than any dentist you know in England. A good dentist is about practice and hand skills and experience. I work hard, very hard, because more and more patients are arriving to my clinic, because in England they don’t find dentists.

While there is no official data about the number of people travelling from the UK to Turkey for dental treatment, investors and dentists I speak to consider that numbers are rocketing. From all over the world, Turkey received 1.2 million visitors for “medical tourism” in 2022, an increase of 308% on the previous year. Of these, about 250,000 patients went for dentistry. One of the most renowned dental clinics in Istanbul had only 15 British patients in 2019, but that number increased to 2,200 in 2023 and is expected to reach 5,500 in 2024.

Like all forms of medical care, dental treatments carry risks. Most clinics in Turkey offer a ten-year guarantee for treatments and a printed clinical history of procedures carried out, so patients can show this to their local dentists and continue their regular annual care in the UK. Dental treatments, checkups and maintaining a good oral health is a life-time process, not a one-off event.

Many UK patients, however, are caught between a rock and a hard place – criticised for going abroad, yet unable to get affordable dental care in the UK before and after their return. The British Dental Association has called for more action to inform these patients about the risks of getting treated overseas – and has warned UK dentists about the legal implications of treating these patients on their return. But this does not address the difficulties faced by British patients who are being forced to go abroad in search of affordable, often urgent dental care.

A global emergency

The World Health Organization states that the explosion of oral disease around the world is a result of the “negligent attitude” that governments, policymakers and insurance companies have towards including oral healthcare under the umbrella of universal healthcare. It as if the health of our teeth and mouth is optional; somehow less important than treatment to the rest of our body. Yet complications from untreated tooth decay can lead to hospitalisation.

The main causes of oral health diseases are untreated tooth decay, severe gum disease, toothlessness, and cancers of the lip and oral cavity. Cases grew during the pandemic, when little or no attention was paid to oral health. Meanwhile, the global cosmetic dentistry market is predicted to continue growing at an annual rate of 13% for the rest of this decade, confirming the strong relationship between socioeconomic status and access to oral healthcare.

In the UK since 2018, there have been more than 218,000 admissions to hospital for rotting teeth, of which more than 100,000 were children. Some 40% of children in the UK have not seen a dentist in the past 12 months. The role of dentists in prevention of tooth decay and its complications, and in the early detection of mouth cancer, is vital. While there is a 90% survival rate for mouth cancer if spotted early, the lack of access to dental appointments is causing cases to go undetected.

The reasons for the crisis in NHS dentistry are complex, but include: the real-term cuts in funding to NHS dentistry; the challenges of recruitment and retention of dentists in rural and coastal areas; pay inequalities facing dental nurses, most of them women, who are being badly hit by the cost of living crisis; and, in England, the 2006 Dental Contract that does not remunerate dentists in a way that encourages them to continue seeing NHS patients.

The UK is suffering a mass exodus of the public dentistry workforce, with workers leaving the profession entirely or shifting to the private sector, where payments and life-work balance are better, bureaucracy is reduced, and prospects for career development look much better. A survey of general dental practitioners found that around half have reduced their NHS work since the pandemic – with 43% saying they were likely to go fully private, and 42% considering a career change or taking early retirement.

Reversing the UK’s dental crisis requires more commitment to substantial reform and funding than the “recovery plan” announced by Victoria Atkins, the secretary of state for health and social care, on February 7.

The stories I have gathered show that people travelling abroad for dental treatment don’t see themselves as “tourists” or vanity-driven consumers of the “Hollywood smile”. Rather, they have been forced by the crisis in NHS dentistry to seek out a service 1,500 miles away in Turkey that should be a basic, affordable right for all, on their own doorstep.

*Names in this article have been changed to protect the anonymity of the interviewees.

For you: more from our Insights series:

GP crisis: how did things go so wrong, and what needs to change?

Insomnia: how chronic sleep problems can lead to a spiralling decline in mental health

To hear about new Insights articles, join the hundreds of thousands of people who value The Conversation’s evidence-based news. Subscribe to our newsletter.

Diana Ibanez Tirado receives funding from the School of Global Studies, University of Sussex.

pound pandemic treatment therapy spread recovery iran brazil european europe uk germany ukraine world health organizationInternational

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

{kind=link}

{kind=link}

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canada

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

February Employment Situation

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Walmart joins Costco in sharing key pricing news

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex