Futures Fall From Record As Traders Ignore Latest Vaccine News, Seek New Catalysts

Futures Fall From Record As Traders Ignore Latest Vaccine News, Seek New Catalysts

Tyler Durden

Wed, 12/02/2020 – 07:58

US index futures dropped and European shares edged lower as investors struggled to find fresh catalysts to exten

Share this:

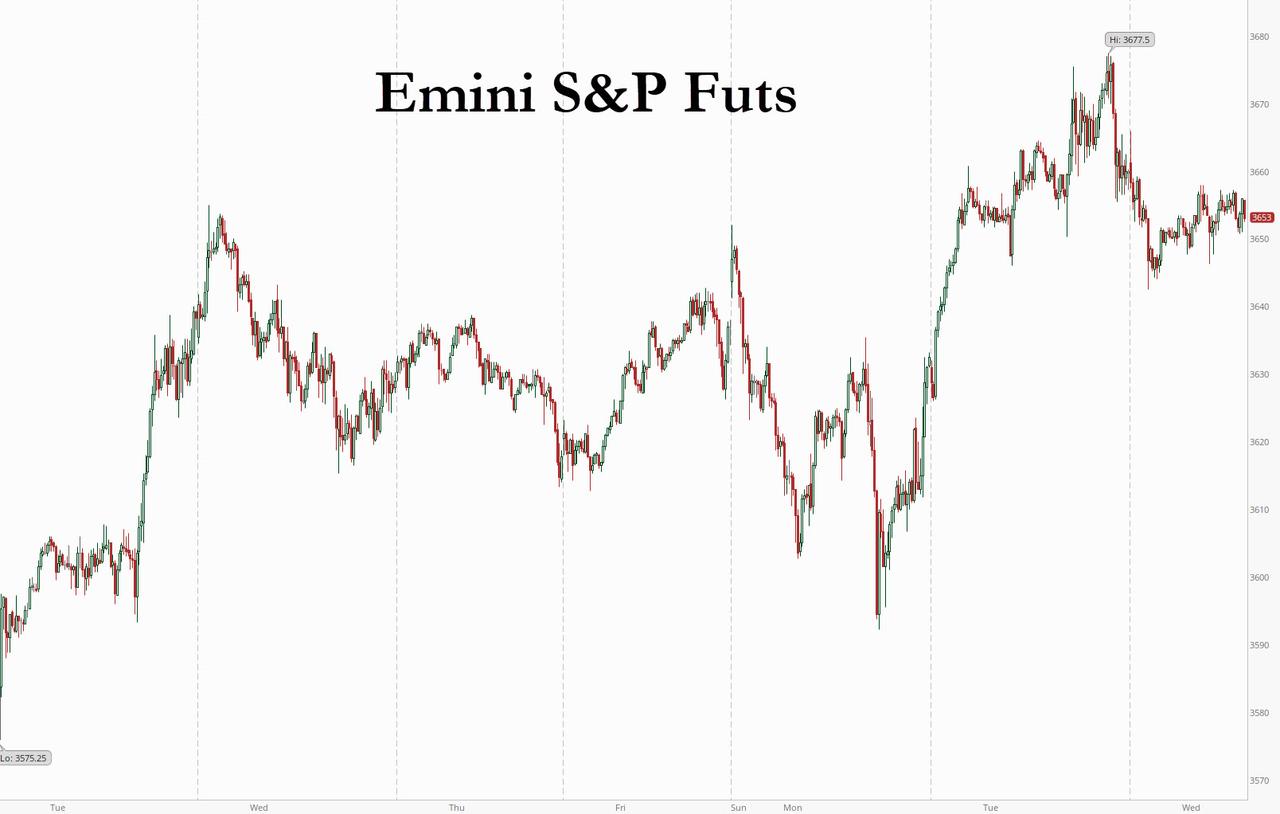

US index futures dropped and European shares edged lower as investors struggled to find fresh catalysts to extend their buying of stocks after the market has fully priced in an improved health outlook on vaccine optimism, while waiting for the latest ADP private payrolls report. Treasury yields modestly faded Tuesday surge which was sparked by renewed fiscal stimulus optimism, while the dollar rebounded from a 2.5 year low. At 7:30 a.m. ET, Dow E-minis fell 111 points, or 0.36% and S&P 500 E-minis dropped 11.25 points, or 0.31%. Nasdaq 100 E-minis declined 29.50 points, or 0.24%.

Among individual stocks, Salesforce.com dropped about 4.5% as it agreed to buy workplace messaging app Slack Technologies Inc in a $27.7 billion deal as it bets on an extended run for remote working. Moderna shares fell in the pre-market to as low as $135.52, down from earlier trading that saw prices as high as $151.47, after Merck said it had sold its direct holding in Moderna in the first half of the fourth quarter. Pfizer climbed after its Covid-19 shot was cleared for deployment in the U.K. as soon as next week while shares in BioNTech surged by more than 8% before trimming gains.

In the latest positive vaccine news, overnight Britain approved Pfizer and BioNTech's COVID-19 vaccine, jumping ahead of the United States and Europe to become the first country to formally endorse a shot it said should reach the most vulnerable people early next week. The two drug firms and competitor Moderna have also sought emergency use approval from European regulators this week, while U.S. health officials have announced plans to start vaccinating Americans as early as mid-December, once regulatory approvals are in place.

"Early vaccines will help bolster the reflation and normalcy trade, which has been the key macro theme in driving equity markets," said Neil MacKinnon, global macro strategist at VTB Capital. "Equity bulls will be hoping that the vaccine news is not an example of ‘buy the rumor, sell the fact’,” he added, saying there was a risk stock markets have already been "priced to perfection."

The MSCI index of global stocks inched up 0.4% to keep it near an all-time high set in the previous session. "General risk sentiment is unchanged - perhaps there’s a bit of consolidation today but that’s understandable given where we’ve come from since November," said Derek Halpenny, EMEA head of research for global markets at MUFG. The dollar lost more than 2.5% of its value in November.

Despite the positive vaccine news, European stocks failed to add to their recent surge. The Stoxx Europe 600 Index erased declines of as much as 0.5%, before dipping again, and trading down 0.3% last with automakers and travel shares leading declines while defensive sectors, such as real estate, utilities, healthcare gained.

Earlier in the session, Asian markets were mixed; shares in China recovered from early losses and rose 0.12%. China’s No. 2 smartphone maker Xiaomi Corp. dropped the most ever after disclosing a share sale. The offshore yuan erased gains after president-elect Joe Biden told the New York Times he won’t soon remove tariffs on Chinese goods. Tokyo stocks were little changed after setting a new 29-year high. Softbank Group shares fell 0.66% after Bloomberg News said the tech investor is winding down its options trades on companies including Amazon.com Inc and Facebook Inc.

As Bloomberg notes, after vaccine breakthroughs fueled record monthly gains for global stocks in November, markets appear to have priced in an improved health outlook, and investors are turning some of their attention to bonds. One of the year’s biggest spikes in Treasury yields on Tuesday has spurred speculation about the potential impact of rising rates on stocks and corporate debt.

"The question is how much is already priced in, and is the upside therefore limited?” Esty Dwek, head of global market strategy at Natixis Investment Managers Solutions, wrote in a report. “The outlook is one of improvement and leaving behind the chaos of the pandemic. Still, a number of risks remain."

Markets were also buoyed on Tuesday after top U.S. Senate Republican Mitch McConnell said that Congress should include new coronavirus stimulus in a $1.4 trillion spending bill aimed at heading off a government shutdown in the midst of the pandemic. Joe Biden told the New York Times his priority is getting a generous aid package through Congress even before he takes office in January.

Also on Tuesday Fed Chair Powell again cautioned lawmakers that the U.S. economy remains in a damaged and uncertain state during testimony at a Tuesday hearing before the Senate Banking Committee. Perhaps boosted by his comments, congressional efforts to pass additional coronavirus relief in the U.S. pushed ahead Tuesday as House Speaker Nancy Pelosi presented a fresh Democratic proposal and Senate Majority Leader Mitch McConnell floated a revision of his smaller plan to fellow Republicans.

In rates, Treasuries held small gains following Tuesday's rout although yields remained within a basis point of Tuesday’s closing levels. Yields were lower by about 1bp at long end with the curve slightly flatter; 10-year around 0.92% after touching 0.936% Tuesday, the cheapest in two weeks. Yields on euro zone government bonds edged up to their highest in three weeks at -0.51% before weakening to -0.525% at 1153 GMT.

In FX, The dollar edged off 2-1/2 year lows against the euro and a basket of major currencies hit earlier on Wednesday. The pound was under some pressure, with doubts remaining over whether Britain can agree a trade deal with the European Union. Sterling fell 0.6% to $1.3342. UK blue-chip stocks were up 0.2%.

In commodities, oil prices dropped after OPEC and its allies left markets in limbo by postponing a formal meeting to decide whether to lift output in January. Brent crude futures fell 0.44% to $47.21 per barrel, while U.S. crude was down 0.74% at $44.22 per barrel. Oil has raced up nearly 30% over the last month. Gold rose for a second day, while bitcoin traded just above $19,000.

As pandemic-led restrictions continue to pose a threat to the labor market recovery, investors will keep a close eye on November’s private payrolls data, which is due at 8:15 a.m. ET. The U.S. House of Representatives is expected to pass legislation later on Wednesday that could prevent some Chinese companies from listing their shares on U.S. exchanges unless they adhere to U.S. auditing standards, congressional aides said.The bill would give Chinese companies like Alibaba , tech firm Pinduoduo Inc. and oil giant PetroChina Co Ltd. three years to comply with U.S. rules before being removed from U.S. markets.

Looking at today's calendar, we get the November ADP employment change at 8:15am ET and Fed Chair Powell appearance before House panel. ECB Board member Philip Lane is due to speak as part of the Thomson Reuters Global Investment Summit at 1400 GMT, ahead of a Dec. 10 ECB policy meeting which is expected to increase and extend the central bank’s Pandemic Emergency Purchase Programme.

Market Snapshot

- S&P 500 futures down 0.1% to 3,656.25

- STOXX Europe 600 down 0.05% to 391.72

- MXAP up 0.3% to 191.55

- MXAPJ up 0.3% to 631.40

- Nikkei up 0.05% to 26,800.98

- Topix up 0.3% to 1,773.97

- Hang Seng Index down 0.1% to 26,532.58

- Shanghai Composite down 0.07% to 3,449.38

- Sensex down 0.05% to 44,635.22

- Australia S&P/ASX 200 up 0.03% to 6,590.20

- Kospi up 1.6% to 2,675.90

- Brent futures down 0.1% to $47.36/bbl

- Gold spot up 0.5% to $1,824.21

- U.S. Dollar Index little changedat 91.36

- German 10Y yield rose 1.2 bps to -0.516%

- Euro down 0.1% to $1.2058

- Italian 10Y yield rose 4.8 bps to 0.563%

- Spanish 10Y yield unchanged at 0.12%

Top Overnight News from Bloomberg

- President Trump has discussed with advisers whether to grant pre-emptive pardons to his children, to his son-in-law and to his personal lawyer Rudolph W. Giuliani, and talked with Mr. Giuliani about pardoning him as recently as last week, according to two people briefed on the matter

- President-elect Joe Biden told the New York Times he’d leave the phase-one trade deal with China in place while he conducts a full review of U.S. policy toward its Asian rival in consultation with key allies

- One of the year’s biggest spikes in Treasury yields has investors mapping out the impact of rising rates on markets ranging from stocks to corporate bonds

- The U.K. became the first western country to approve a Covid-19 vaccine, with its regulator clearing Pfizer Inc. and BioNTech SE’s shot ahead of decisions in the U.S. and European Union

- European Central Bank policy maker Martins Kazaks said an expansion of the institution’s emergency bond-buying program by 500 billion euros ($603 billion) would be “reasonable” and he’s ready to support an extension until mid 2022

- German car and parts makers’ expectations have regressed during each of the last four months in the Ifo Institute’s monthly survey, sending the economic think tank’s index into negative territory in November

A quick look at global markets courtesy of NewsSquawk

In Asia, stocks lacked firm direction as momentum faded from the record-setting performance on Wall St, where the S&P 500 and Nasdaq printed fresh all-time highs after a resumption of COVID-19 relief discussions and weak data spurred stimulus hopes, while US futures pulled back after-hours with DJIA futures retreating further away from 30k. ASX 200 (Unch.) was indecisive after underperformance in healthcare and tech was offset by gains in the mining sectors and with better than expected GDP data failing to spur risk appetite as although Q/Q growth topped estimates at 3.3% vs. Exp. 2.6%, the economy still contracted by 3.8% from the prior year. Nikkei 225 (+0.1%) traded rangebound and ignored a predominantly weaker currency, while KOSPI (+1.6%) outperformed amid strength in chipmakers and with shares in index heavyweight Samsung Electronics rallying to unprecedented levels. Hang Seng (-0.1%) and Shanghai Comp. (Unch) conformed to the humdrum mood after the PBoC drained CNY 110bln of liquidity and amid lingering concerns regarding US-China tensions, as well as the worsening COVID-19 situation in Hong Kong. Finally, 10yr JGBs fell below the key 152.00 level as they tracked the downturn in T-notes but with further losses stemmed by the uninspiring mood for regional stocks and with the BoJ present in the market for nearly JPY 1.1tln of JGBs in up to 5yr maturities.

Top Asian News

- Specter of Cashless Gambling Drives Junket Operators from Macau

- Thai Court Rejects Petition to Disqualify Premier Amid Protests

- Philippines Adds to Global Debt Binge With Another Bond Deal

European markets kicked the session off lower across the board but have since trimmed/nursed losses with the region now seeing a mixed picture (Euro Stoxx 50 -0.2%) following the uninspiring APAC handover. The main news of the morning has been UK's approval of the Pfizer/BioNTech COVID-19 vaccine, a move touted in UK press over the weekend, with the vaccine to be rolled out as soon as next week, with sources over the weekend suggesting the first jab to be administered on December 7th. On this front, it is worth keeping in mind the challenges posed by the logistics of supply and distribution, whereby "The companies have developed specially designed, temperature-controlled thermal shippers utilizing dry ice to maintain temperature conditions of -70°C±10°C. They can be used be as temporary storage units for 15 days by refilling with dry ice", according to the official PFE/BNTX release. Nonetheless, the news sparked little in the way of a sustained reaction across European and US equity futures, with US FDA and EU EMA reviews expected later this month. On that note, EU lawmakers called the UK approval "problematic" as it was too fast - something to keep an eye on to gauge the bloc's risk profile with regards to accelerated approvals. Sectors in Europe are mostly in the red having had had a downbeat open, but energy has recouped lost ground on account of price action in the complex whilst healthcare is supported. Elsewhere, Travel & Leisure was faring well at the open but the optimism has since waned. Overall, a clear risk profile cannot be derived from sectors. Looking at individual movers, G4S (+7%) top the charts following a revised offer from Gardaworld who upped the price to GBP 2.35 per G4S shares vs. the prior offer of GBP 1.90. G4S has until December 16th to digest the terms and respond. Meanwhile, Rolls-Royce (+1.0%) sees tailwinds after signing an aerospace engineering partnership with Indian giant Infosys. Finally, Tesco (-1.5%) shares are on the backfoot as the Co. is to repay the UK govt GBP 585mln of business rates relief received in the wake of the pandemic, whilst adding the latest estimates in October was that COVID would cost Co. GBP 725mln this year, well in excess of the rates relief received.

Top European News

- U.K. Debates Carbon Cut as High as 69% to Show Climate Ambition

- The U.K. Has Approved a Vaccine. Here’s What Happens Next

- Covid-19 Testing for Most of a Nation Backfires on Slovak Leader

In FX, the Pound was riding high alongside fellow majors against downtrodden Dollar before an update on Brexit trade talks from chief EU negotiator Barnier pulled the rug from Cable and pushed Eur/Gbp back above 0.9000. In short, far from entering the final phase towards a deal, the 2 sides remain apart on the 3 main sticking points and an agreement is still in the balance. Moreover, his briefing to envoys also conceded that is uncertain whether the gaps can be bridged as EU officials are said to be getting increasingly nervous about the prospect of reaching an accord, albeit with one source in Brussels suggesting that a deal can still be done in December, next month or (presumably) later in 2021. Cable is now a full point down from best levels circa 1.3440 and the cross is hovering near the top of a 0.9045-0.8965 range.

- DXY - For all intents and purposes, the Buck appears to have stopped the rot by virtue of the aforementioned relapse in Sterling, as other G10 currencies suffered contagion, like the Euro to lift the index from 91.103 to 91.426. However, the Greenback remains fragile overall ahead of ADP, the 2nd part of Fed chair Powell’s Congressional testimonies and 2 speeches from Williams before the latest Beige Book prepared for next month’s FOMC.

- AUD/NZD/CAD - Mixed GDP data and the ongoing rift with China may be keeping the Aussie capped into 0.7400 vs its US counterpart, but Aud/Nzd has bounced from recent lows nearer the 1.0400 mark as the Kiwi stalls in the high 0.7300 zone against its US peer following remarks from RBNZ Governor Orr flagging risks to the economic recovery and outlook, while reiterating that the LSAP, FLP and OCR can all be adjusted to meet the Bank’s mandate. Meanwhile, some stability in crude prices is keeping the Loonie afloat between 1.2915-50 parameters awaiting OPEC+ tomorrow.

- JPY/CHF/EUR - Little respite for the underperforming Yen irrespective of fading risk sentiment and bear-steepening in US Treasuries abating somewhat, as Usd/Jpy pivots 104.50 in a moderately firmer 104.23-72 band. Elsewhere, the Franc is straddling 0.9000 against the Dollar, but thankfully for the SNB unable to keep pace with the Euro following its outsized gains yesterday given more deflationary than expected Swiss CPI. Indeed, Eur/Chf is elevated within a 1.0852-71 band even though Eur/Usd has run in to resistance just shy of 1.2100, albeit partly in sympathy with the Pound as noted above. Note also, aside from the obvious psychological factors surrounding the next round number, a prior high from September 2017 (1.2092) may be hampering the single currency in addition to a key Fib retracement level only a few pips above (1.2103 represents a 76.4% correction of the move from 1.2555 to 1.0638 - mid-February 2018 peak to this year’s low).

-

SCANDI/EM/PM - The Sek and Nok seem more in thrall with Eur excesses than the general risk tone or somewhat confusing Norwegian current account developments as the surplus widened in Q3, but only after a huge downward revision to the prior quarter. Conversely, EMs are trading mixed with the Zar underperforming regardless of Xau extending its recovery rally beyond another chart hurdle in the form of the 10 DMA (after breaching the 200 DMA on Tuesday).

In commodities, WTI and Brent front month futures have recouped earlier losses which were seen in wake of OPEC indecision coupled with a surprise build of 4.1mln bbl (vs. Exp. -2.4mln bbls) in private inventories last night. The recovery in futures commenced in APAC hours but gained traction following the UK vaccine approval announcement, albeit in the context of yesterday's sell-off, the recovery is somewhat tame. In terms of where we stand on OPEC, ministers are to meet again today in an attempt to hash out differences over the producers' next move - with three options reportedly on the table. 1) An extension of current cuts by three months (Saudi's preference), 2) output to be raised from January but by a smaller volume than the 2mln BPD under the DoC (Russia's preference), and 3) hiking output under the original plan. Furthermore, the compliance mechanism seems to be an issue with the UAE, whereby sources noted that kingdom is willing to back the 7.7mln BPD extension but contingent on assurances of improved compliance. Note UAE also reportedly called for an extension of 7.2mln BPD cuts. WTI Jan trades on either side of USD 44.50/bbl (vs. low 43.92/bbl) and Brent Feb on either side of USD 47.50/bbl (vs. low ~ 46.85/bbl). Elsewhere, precious metals have been bolstered post-vaccine approval amid reflationary play and despite the firmer Buck. Spot gold also surpassed the 10DMA (~ 1820/oz) flagged by technicians ahead of USD 1850/oz psychological mark and the 21 DMA at USD 1859/oz. Spot silver meanwhile continues to make headway above USD 24/oz. Elsewhere, Dalian iron ore futures gained as much as 3.5% amid rosy steel demand prospects, whilst LME copper is subdued amid the firmer Buck and mixed equity picture.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 3.9%

- 8:15am: ADP Employment Change, est. 430,000, prior 365,000

- 2pm: U.S. Federal Reserve Releases Beige Book

Central Banks

- 10am: Powell Appears Before House Finance Panel

- 1pm: Fed’s Williams Holds Press Briefing

- 2pm: U.S. Federal Reserve Releases Beige Book

DB's Jim Reid concludes the overnight wrap

Risk assets got December off to a very strong start yesterday, as both the S&P 500 (+1.13%) and the NASDAQ composite (+1.28%) shrugged off the rising number of pandemic cases to reach fresh all-time highs. 21 of the 24 S&P 500 industry groups rose yesterday, and there was not a clear driver of the rally which was led by a mix of growth and cyclical names. Tech hardware (+2.65%), Media (+2.27%), Autos (+1.96%) and Banks (+1.95%) all led the way, Energy (+0.44%) had been doing well early in the session before oil prices reversed on further OPEC+ meeting worries. The overall equity strength was seen in Europe too, where the STOXX 600 (+0.65%), the DAX (+0.69%) and the FTSE 100 (+1.89%) had all moved higher by the close.

With equities reaching all-time highs, there was a major selloff in sovereign bond markets as investors rotated out of safer assets, and yields on 10yr US Treasuries were up +8.7bps to 0.926% by the close. The moves offered support for those of us saying the Covid crisis is more likely to lead to inflation than deflation in the coming years (although maybe not in 2021), since US 10-year breakevens rose to 1.82% yesterday, their highest closing level since May 2019. European sovereigns witnessed a similar selloff, and yields on 10yr bunds (+4.3bps), OATs (+3.7bps) and gilts (+4.2bps) all moving higher yesterday. Nevertheless, Greek bonds continued their relative outperformance however, with the spread of their 10yr yields over bunds falling to a post-sovereign debt crisis low yesterday of 1.185%.

Overnight the New York Times has reported that President-elect Joe Biden won’t immediately remove the phase 1 tariffs on China and will conduct a full review of the existing trade deal with China. Biden further said that when dealing with China it is all about “leverage,” and “in my view, we don’t have it yet.” This news is weighing on Asian bourses as most of them have erased part of their early gains. Currently, the Nikkei (+0.04%) and Shanghai Comp (+0.02%) are flattish while the Kospi (+1.47%) is up and the Hang Seng (-0.20%) is down. Futures on the S&P 500 are down -0.26% and European equivalents are pointing to a weaker open.

Fed Chair Powell spoke yesterday before the Senate Banking Committee and again tried to urge lawmakers that while economic indicators are improving, the outlook for the economy continues to see risks. The Fed chair noted that the “recent news on the vaccine front is very positive for the medium term,” but added that “significant challenges and uncertainties remain, including timing, production and distribution, and efficacy across different groups.” Powell also both congratulated the CARES act for helping to support the economy while also stressing the fact that more fiscal stimulus may be needed, especially in a winter that is sure to see more small business closures if case counts do not get under control quickly. Treasury Secretary Mnuchin shared the Fed Chair’s desire to get more fiscal stimulus and urged Congress to “pass something quickly”.

This came just ahead of reports that House Speaker Pelosi and Senate Majority Leader McConnell had new proposals for fresh stimulus. Pelosi’s plan has been sent to Secretary Mnuchin and the Republican leadership, while Senator McConnell is circulating his plan among Republicans to gauge support. President-elect Biden has called on Congress to get a “robust package” passed in the lame duck session, though indicated that this would be just the start. Neither plan had been released but you may recall that McConnell previously supported a $500 billion package, while President Trump indicated he is willing to back a bigger bill. Any legislation would have to get past a Democratic-controlled House, where Pelosi has called for a $2.4 trillion plan.

Risk appetite was further supported yesterday by some very strong readings in the global manufacturing PMIs, where all of the major economies reported decent numbers. In the Euro Area, the final PMI was revised up from the flash reading to 53.8 (vs. flash 53.6), the UK saw a revision up to 55.6 (vs. flash 55.2), and the US remained in line with the flash number at 56.7. Furthermore, as we mentioned in yesterday’s edition, China’s PMI was above expectations as well at 54.9. So all of the world’s major economies have their manufacturing PMIs in the 50s, which is in expansionary territory, and that’s even with the increase in restrictions that have come into place with Covid case numbers on the rise.

Speaking of Covid, UK MPs voted by 291-78 yesterday in favour of the new tiered system of restrictions for England. And the 78 voting against the measures included 55 from Prime Minister Johnson’s own Conservative Party, which reflects the fact that there’s increasing disquiet against further prolonged restrictions. Nevertheless, Johnson also told the House of Commons that if the Pfizer/BioNTech vaccine was approved, then it could start to be administered before Christmas, which raises the prospect that life could return closer to normal early next year.

Staying with vaccines, Pfizer/BioNTech have said that they have sought regulatory clearance for their Covid-19 vaccine in the EU with BioNTech adding that it could start shipping the first doses “within hours” after approval. Meanwhile, CNN has reported overnight that the US will see the first shipments of this vaccine delivered by December 15 while Moderna’s vaccine will arrive a week later.

In New York City, older residents and those with underlying health conditions were advised to remain at home and not have people over. This came as city hospitalisations rose by 242 yesterday, the largest one day rise since April. In better news, Dr Fauci said that US residents without co-existing conditions or elevated risks will get access to vaccines by April. He went on to say that, if Americans embrace vaccination to a high enough degree, herd immunity could be reached over the summer. The comments came in an online news conference with Colorado governor Polis. Overnight, Bloomberg has reported that the US CDC new guidance will cut quarantine time for individuals exposed to the coronavirus by as much as half. Across the other side of world, the Nikkei reported that Japan won’t require visitors to get vaccinated before arriving for next year’s Summer Olympics.

On Brexit, with just over 4 weeks to go until the end of the transition period, the chief political commentator of Times Radio reported yesterday that the trade talks had finally entered the so-called tunnel, which are intensified negotiations in the late-stage of talks. He said that “Neither side formally confirming tunnel status yet. No10 never recognise the term, but also not denying it.” There is some chatter that a deal as early as later this week could be on the cards. I say early but in reality this is very late in the day but the early refers to how soon that is to now! On the flip side there were also reports suggesting negotiators were bemused by reports that talks had entered a so called tunnel so no-one knows where we are apart from the two sides who are probably confused themselves! The EU’s chief negotiator is set to brief diplomats from the bloc’s 27 member states today on the progress of the negotiations. So expect more headlines and perhaps some more clarity on the state of negotiations.

Elsewhere in Europe, data yesterday showed the flash estimate of CPI inflation in the Euro Area remained at -0.3% for the 3rd month running in November, a tenth below expectations. However as in the US, inflation expectations have been on the up over the last week, with five-year forward five-year inflation swaps for the Euro Area now at a 3-month high of 1.23%. And on top of this, the dollar’s slide meant that the euro closed above $1.20 for the first time since April 2018. See here for why DB think the Euro rise continues.

To the day ahead now, and we’ll hear from Fed Chair Powell and Treasury Secretary Mnuchin again as they appear before the House Financial Services Committee. Otherwise, there’ll also be remarks from the Fed’s Williams and the BoE’s Haskel, and the Federal Reserve will be releasing its Beige Book. Elsewhere, data highlights include the Euro Area unemployment rate and German retail sales for October, while from the US we’ll get the ADP’s November report of private payrolls.

Uncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

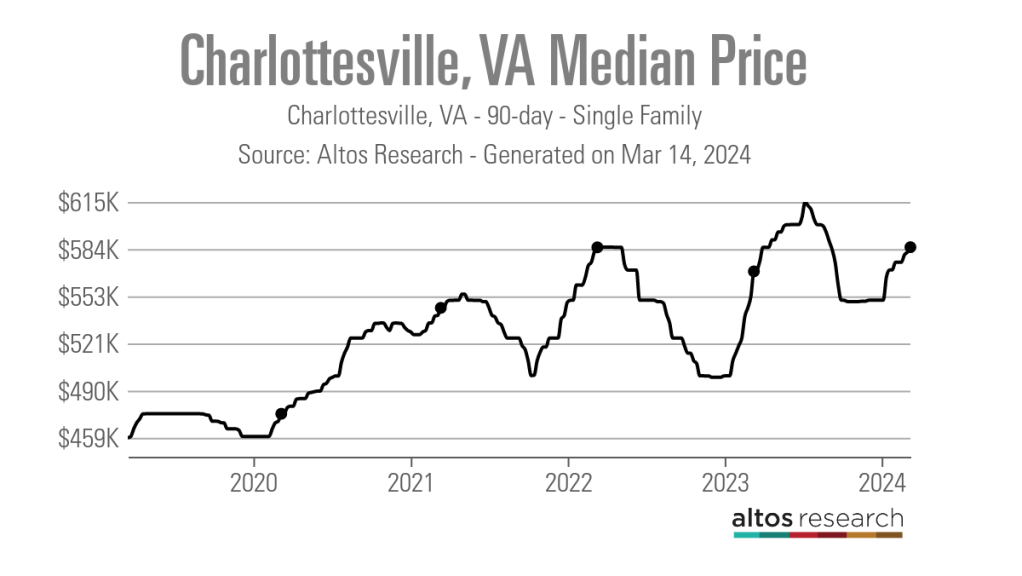

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest ratesInternational

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

{kind=link}

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges