Futures Fall Ahead Of Key Inflation Print On Impeachment Wednesday

Futures Fall Ahead Of Key Inflation Print On Impeachment Wednesday

The dollar rebounded from Tuesday’s selloff, as global markets dropped with S&P futures down 8 points, or 0.2%, to 3,786 trading in a narrow 20 point range since Friday,.

Share this:

The dollar rebounded from Tuesday's selloff, as global markets dropped with S&P futures down 8 points, or 0.2%, to 3,786 trading in a narrow 20 point range since Friday, as investors focused on comments from the Federal Reserve and European Central Bank about the outlook for monetary stimulus. The outlook for Federal Reserve bond purchases was in focus after two Fed officials said there was no rush to start tapering given the pandemic is still raging. Boosting risk sentiment, U.S. yields dropped following a strong auction, easing concerns of an imminent inflation surge.

Exxon Mobil added 0.9% after J.P. Morgan upgraded the stock to “overweight”, its first outright “buy” recommendation for the oil major in seven years, saying cuts in capital spending had put it on track for a stronger performance. The upgrade follows similar upgrades from Goldman and Morgan Stanley. General Motors added another 3% in premarket trading on top of Tuesday’s 6% jump after the automaker announced its entry into the growing electric delivery vehicle business. Regeneron Pharmaceuticals climbed 3.5% in light trading as the U.S. government said it would buy 1.25 million additional doses of the company’s COVID-19 antibody cocktail for about $2.63 billion.

On Tuesday, Wall Street’s main indexes ended marginally higher on Tuesday on a boost from economy-linked financials, energy and materials stocks, while the small-cap Russell 2000, sensitive to domestic outlook, closed at an all-time high.

"Inflation is the key number for us to watch today," said Marija Veitmane, senior multi-asset strategist at State Street Global Markets. “The market is very relaxed about it and should we get high inflation that would be a big pressure. The 10-year is probably the key variable to watch. If you have a very strong positive surprise then you will probably start thinking about the Fed being a bit more aggressive in their intervention and pushing yields lower,” she said.

This will tie in closely to the biggest question facing markets today: when will the Fed start to taper? In recent days, several Fed policymakers, including Loretta Mester, Esther George, James Bullard and Eric Rosengren, pushed back against the idea of the Fed tapering its asset purchases any time soon as yields broke out sharply higher. These comments, along with a well-received auction of 10-year Treasuries, eased concern that the Fed might be headed for a repeat of the so-called taper tantrum in 2013 and pushed the 10-year Treasury down from the 10-month high of 1.187% reached in the previous session.

On Tuesday, James Bullard said getting through the pandemic remains the policy priority, a sentiment that was echoed by Boston Fed chief Eric Rosengren.

“Coordinated comments from Fed governors” are helping to deflate bond yields, said Deutsche Bank's Jim Reid in a note to clients. “We’ve only had seven business days this year and we’ve already had a full 360-degree tapering debate played out by the Fed.”

Politics also takes the center stage again today with investors set to closely follow events in Washington, where the House of Representatives will vote to impeach President Donald Trump for the second time over the storming of the U.S. Capitol last week. The House vote may may be supported by a dozen or more Republicans, including No. 3 GOP leader Liz Cheney. The move comes after Mike Pence refused to use the 25th Amendment to remove Trump from office. Here's a chronology of the events (per Bloomberg).

- The debate begins shortly after 9 a.m. and voting will end by 5 p.m.

- The matter would then go to the Senate for a trial, which probably wouldn't occur before Jan. 20. It would take at least 17 Republicans along with all Democrats for a guilty verdict, an almost impossible order. But Mitch McConnell may be swayed that way, Axios reported.

Looking at global markets, the MSCI world equity index was up 0.1%, edging back towards record highs.

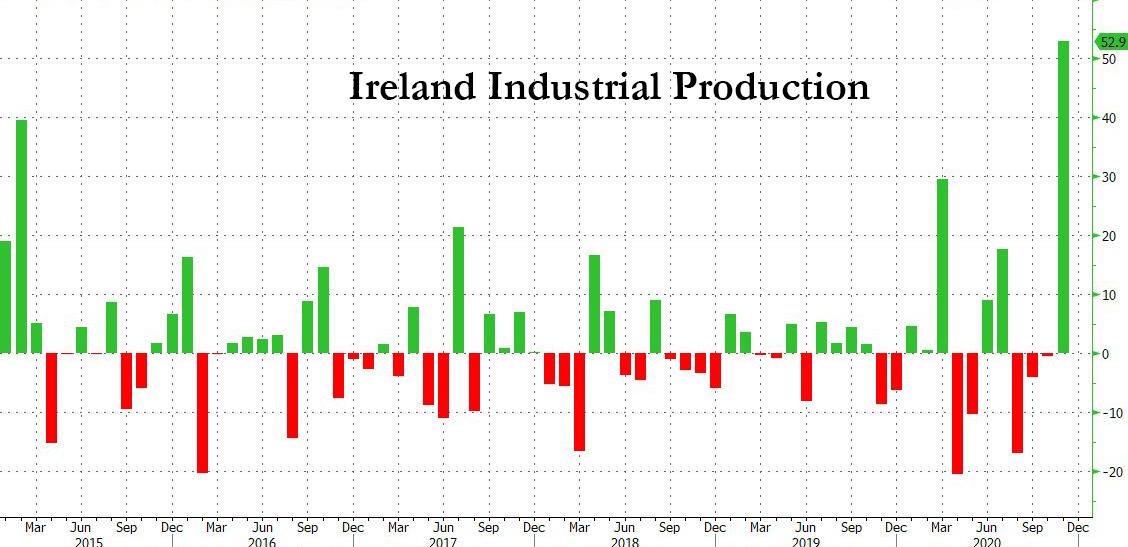

MSCI’s main European Index was down by a similar amount. European shares opened lower and struggled to make gains, with the pan-European STOXX 600 down 0.1% on the day, with banks leading the drop. The banking subindex was down 1.3% while oil and gas companies trimmed gains of above 1% to trade 0.2% higher after Angela Merkel warned that the country may need to extend its lockdown until Easter. Among the day’s winners, French grocer Carrefour SA rallied 10% after Alimentation Couche-Tard Inc., the convenience-store giant that owns the Circle K chain, said it’s exploring a transaction. Telefonica SA also jumped 10% after American Tower Corp. said it would buy telecommunication towers in Europe and Latin America from the company. November industrial production data was better than expected, on the back of a ridiculous 53% surge in Irish industrial production.

European Central Bank President Christine Lagarde pushed back about economic pessimism, saying that the ECB’s December projections for a rebound are “still very clearly plausible”, so long as COVID-19 restrictions in Europe can be lifted from the second quarter of the year.

Earlier in the session, Asian stock headed for another record close amid a broad risk-on rally in global markets on hopes of an economic recovery. Technology stocks contributed the most to the MSCI Asia Pacific Index’s gain as Lenovo Group surged 9.7% in Hong Kong. That’s after its board approved a preliminary proposal to list shares on the Shanghai Stock Exchange through the issuance of Chinese depositary receipts. Taiwan’s equity benchmark climbed 1.7% to lead the advance in Asia. Malaysian stocks were among the other top performers as investors snapped up local shares following a two-day slide of 1.3% in the benchmark on new emergency and lockdown measures. Tech names powered gains in Japan as well, where the Nikkei 225 hit a record in dollar terms. Meanwhile, equity benchmarks in China and New Zealand declined. Among industry groups, a gauge of energy shares was the best performer in the region -- rallying more than 2% -- as oil prices were set for the longest winning streak in almost two years. Asia’s stock gains came as Treasury yields continued their retreat from a 10-month high.

In rates, Treasuries were steady with long-end yields marginally richer as gilts, bunds outperform on the day. Early Asia session saw a wave of futures-buying -- supported by short-covering and unwinds -- that temporarily extended the advance spurred by Tuesday’s strong 10-year note auction. Treasury 10-year yields were around 1.12% after dropping as low as 1.105% during peak Asia rally; bunds outperform by 2.5bp despite packed issuance slate with focus on German, Portuguese debt sales and an expected 10-year Spanish note syndication. Today the coupon auction cycle concludes with $24b 30-year bond sale, and several Fed speakers are slated.

The yield curve, which had reached the steepest since May 2017 on expectations for big fiscal stimulus under a new Democratic administration, narrowed overnight but started to creep up in the European session, at 97.5 basis points.

“We believe the potential for fiscal stimulus, along with a normalization of economic activity as the vaccine rollout ramps up, justify slightly higher US Treasury yields,” UBS strategists wrote in a note to clients. “To acknowledge this, we have raised our 10- and 30- year US Treasury yield forecasts by 0.1 percentage points this year to 1.0% and 1.7%, respectively, by end-December,” they said. They do not expect the run-up in yields to go much further than that, because central banks remain accommodative and the Fed has signalled a tolerance for higher inflation.

Speaking of the bond market, today's inflation data is unlikely to have much of an impact with the headline number expected to have ticked higher to 1.3% in December, while the core reading is likely to remain at 1.6%.

In FX, the U.S. dollar recently broke its downward trend with a three-day winning streak, then resumed falling on Tuesday. On Wednesday the Bloomberg Dollar Spot Index reversed an early drop as the dollar rose versus most Group-of-10 peers, even as U.S. yields stayed slightly lower. The euro inched lower, to trade below $1.22, while the pound was the top G-10 performer, gaining a second day, after traders pushed back back expectations for a rate cut this week. Sweden’s krona led declines after the Riksbank announced it will start a transition to a fully self-financed FX reserve. The yen advanced after earlier falling to 103.53 day low while the Aussie headed lower, spurred by a drop in iron-ore futures and a weaker-than-expected yuan fix. Over the period Feb. 2021 until Dec. 2023, the Riksbank will purchase foreign currency with Swedish kronor in an amount averaging SEK 5 billion per month, it said in a statement.

In commodities, oil prices steadied after an early jump when industry data showed a bigger-than-expected drop in inventories and investors shrugged off the impact of the pandemic. Brent was last trading at $56.7, down from 10 month high of $57.5 hit earlier in the session. Bitcoin edged up, but at $34,255 was still around 18% down from the record high of $42,000 it reached on Friday last week .

Looking at the day ahead, Expected data include mortgage applications and inflation

Market Snapshot

- S&P 500 down 0.2% to 3,782

- MXAP up 0.5% to 208.93

- MXAPJ up 0.5% to 697.37

- Nikkei up 1% to 28,456.59

- STOXX Europe 600 up 0.2% to 409.48

- Topix up 0.4% to 1,864.40

- Hang Seng Index down 0.2% to 28,235.60

- Shanghai Composite down 0.3% to 3,598.65

- Sensex up 0.02% to 49,527.64

- Australia S&P/ASX 200 up 0.1% to 6,686.60

- Kospi up 0.7% to 3,148.29

- Brent futures little changed at $56.55/bbl

- Gold spot little changed at $1,855.78

- U.S. Dollar Index up 0.1% to 90.20

- German 10Y yield fell 2.7 bps to -0.495%

- Euro down 0.2% to $1.2186

- Italian 10Y yield rose 8.5 bps to 0.539%

- Spanish 10Y yield fell 2.4 bps to 0.086%

Top Overnight News

- The ECB’s latest projections for economic growth in the euro area are still “very clearly plausible” despite the resurgent coronavirus and latest lockdowns, President Christine Lagarde said

- The ECB will maintain favorable monetary conditions as long as needed and is closely watching the impact of foreign exchange rates on inflation, governing council member Francois Villeroy de Galhau says

- Trump’s impeachment appeared inevitable in a vote Democrats anticipated would come Wednesday with the resolution’s sponsors claiming broad support from Democrats and public backing from several Republicans, including Liz Cheney, the No. 3 House GOP leader and daughter of former Vice President Dick Cheney

- The government of Italian Prime Minister Giuseppe Conte is at risk of collapsing as a junior ally prepared to abandon the coalition as early as Wednesday, just as the administration seeks to push through measures to battle the pandemic and boost the economy

- Two months after Donald Trump issued an executive orderbanning U.S. investments in Chinese military-linked companies –- and more than a day after it took effect -- the financial industry is still struggling to figure out what it can and can’t do under the new rules

- Some of the world’s biggest banks are urging a U.S. judge not to immediately terminate Libor after a group of borrowers filed suit claiming the benchmark was the work of a “price-fixing cartel”

- Excess cash held by banks in the euro-area rose to yet another record, a symptom of exceptionally loose monetary conditions that are bolstering investor appetite for bonds in the bloc

A quick look at global markets courtesy of Newsquawk

Asian equity markets mostly lacked firm direction as bourses took their cue from the rangebound session in the US where tech losses were offset by cyclicals and with participants tentative ahead of the start of earnings season. ASX 200 (+0.1%) and Nikkei 225 (+1.0%) were mixed for most of the session with weakness seen across most sectors in Australia although the declines in the index were eventually reversed by strength in commodity names as energy stocks mirrored the outperformance stateside after WTI crude prices extended above USD 53.00/bbl, while the Japanese benchmark outperformed led by a rally in power names and miners which helped Tokyo shrug-off detrimental currency inflows and reports that Japan could announce an emergency in 7 additional prefectures. Hang Seng (-0.2%) and Shanghai Comp. (-0.3%) were indecisive after the PBoC continued with its tepid liquidity efforts which reports suggested shows an intent to keep policy appropriate and not take a sharp turn this year, while participants also digested mixed loans and financing data from China in which New Yuan Loans topped estimates but Aggregate Financing disappointed which is the broadest measure of Chinese credit growth. Finally, 10yr JGBs were steady amid the indecisive risk tone and after the recent reversal of the bear steepening in USTs, while the 5yr JGB auction also contributed to the humdrum picture as the results showed a slightly weaker b/c and lowest accepted price.

Top Asian News

- Sequoia-Backed Cloud Firm Is Said to Weigh $500 Million IPO

- Japan Expands Virus Emergency to Cover 60% of Economy

- Saudis Curb Oil Supply to Some Buyers After Pledged Cut

- China Vaccine Faces First Global Test as Indonesia Starts Shots

European indices trade relatively choppy (Euro Stoxx 50 -0.2%) following a mixed APAC session whereby indices treaded water at first before dipping into the red; albeit the breadth of the losses is modest thus far. Meanwhile, US equity futures have also drifted into negative territory in tandem with their counterparts across the pond amid a lack of fresh macro catalysts to latch onto ahead of the US entrance. Broader European sectors are mixed with no clear risk bias to be derived. Delving deeper into the sectors, some of the performances experienced are driven by stock-specific news for sector-heavyweights: Telecoms stand as the outperformer as Telefonica (+9.6%) lifts the sector amid news that American Towers is to purchase Telxius from Telefonica for around EUR 7.7bln in which the Spanish telecom name will use to reduce debt. Consumer Staples are propped up after Carrefour (+9.2%) was approached by Canadian convenience store group Alimentation Couche-Tard regarding a takeover deal which would form a joint entity valued at over USD 50bln, for which the Canadian company reportedly offered Carrefour EUR 20/shr vs share price of around EUR 17/shr at the time. Meanwhile, the Energy sector loses steam, but still remains in positive territory as it tracks price action in the crude complex. On the other end of the spectrum, Travel & Leisure resides as a laggard amid the ongoing COVID-19 woes. In terms of other individual movers, Germany’s ProSiebenSat (-5.8%) is pressured by reports KKR is said to be expected to sell a 4.7% stake priced at around EUR 13.42/shr via accelerated bookbuilding. Meanwhile, Just Eat Takeaway (-4.3%) shares yield despite reporting an increase in revenue on the back of lockdowns as the group warned it will need to invest heavily to keep up current momentum as the rollout of vaccines may prompt orders to deplete.

Top European News

- Lagarde Says ECB Economic Outlook Still Valid Despite Lockdowns

- Italy Coalition Risks Collapse, Threatening Battle Against Virus

- Navalny to Return to Russia Sunday Despite Prison Threat

- London Financiers Cling to Hopes for Post-Brexit Access to EU

In FX, the Dollar is trying to regain a foothold after what proved to be a ‘turnaround Tuesday’ in terms of its recovery efforts, as the DXY fell short of the prior day’s high when in the ascendency and ultimately failed to ‘close’ above the low before losing grip of the 90.000 level, albeit briefly and marginally. The index is now flitting between 89.922-90.259 with a loss of momentum via several Fed commentators indicating little inclination to slow the pace of asset purchases, while the UST yield backdrop is less supportive after a strong 10 year auction prompted broad short covering in futures and some particularly large blocked purchases. However, upcoming US inflation data has the potential to reinflate the Buck and rekindle QE taper talk from today’s array of Fed officials that are scheduled either side of the Beige Book, and the last leg of this week’s issuance could spark a resumption of bear-steepening given less concession for the Usd 24 bn 30 year offering.

- EUR - Not the biggest G10 mover or most volatile, but under the microscope following an attempt to reclaim 1.2200+ status vs the Greenback that faded and 2 ECB speakers reiterating that FX rates are being watched in context of the negative effects, including on prices and the wider economic impact – see Headline Feed at 8.47GMT and 9.11GMT for comments from Villeroy and President Lagarde respectively. Eur/Usd is now hovering around the bottom of a 1.2223-1.2172 range awaiting the outcome of Italy’s coalition showdown, with little reaction to weaker than forecast Italian or Eurozone ip along the way.

- GBP - In contrast to the Euro and most other majors, the Pound has picked up where it left off yesterday, as Cable extended its rebound to touch 1.3700 and Eur/Gbp tests 0.8900 bids/support in wake of BoE Governor Bailey’s latest reservations about going down the negative rate path. However, Sterling faces a formidable hurdle at the current 2021 peak against the Dollar circa 1.2704, not to mention the bleak fundamental outlook caused by the latest UK national lockdown.

- JPY/CHF/CAD/NZD/AUD - All softer vs their US counterpart, with the Yen heading back down towards 104.00 after meeting resistance just ahead of 103.50, as Japan looks to widen COVID-19 restrictions across more prefectures and further reports suggest an economic downgrade by the BoJ. Similarly, the Franc looks vulnerable approaching 0.8900 having crested 0.8850, the Loonie is nearer 1.2750 than 1.2700, the Kiwi back below 0.7200 after a brief boost from ANZ revising its RBNZ forecast up from a NIRP call previously and the Aussie is under 0.7750 again.

- SCANDI/EM- The Sek is still underperforming relative to the Nok even though the latter has lost some traction from oil, with the former only just keeping its head above 10.1000 vs the Eur in wake of changes to the Riksbank’s currency reserves financing arrangements. Elsewhere, the Rub continues to watch Brent moves, while assessing any impact from the Russian Finance Ministry resuming FX purchases from Friday through February 4th.

In commodities, WTI and Brent front-month futures have drifted off best levels in early European trade, with the complex continuing to feel underlying support from the voluntary excess cuts pledged by Saudi whilst a tenser geopolitical landscape coupled with a softer Buck and a larger-than-expected drawdown in Private Inventories also keep prices near their recent levels, albeit markets are still eyeing demand impacts from the COVID-19 resurgence. Kicking off with supply side developments, yesterday’s Private Inventory report printed a larger than expected draw of 5.8mln bbls (vs exp -2.3mln bbl), while distillate fuel stocks also came in at a larger draw than forecasts. Markets will be awaiting the weekly EIA numbers later in the session whereby headline crude stocks are seen drawing by 2.26mln bbls. On the geopolitical front, reports via Sky News Arabia suggested that Iran has conducted a naval missile exercise in the Gulf of Oman, located at the mouth of the Strait of Hormuz where around a fifth of global oil passes through (according to 2018 data). This reported exercise comes against the backdrop of heightened tensions between Iran and the outgoing Trump administration in which the former previously threatened to disrupt oil shipments through the Strait of Hormuz if the US attempts to “strangle” its economy. As a reminder, in 2019, four vessels were attacked just outside the Strait, whilst earlier this month, Iran seized a South-Korean-flagged tanker and detained its crew in the Gulf. Moving onto the demand side of the equation, the first of the trio of monthly oil market reports - the EIA STEO - cut its forecast for 2021 world oil demand growth by 220k BPD to a 5.56mln BPD YY increase and sees 2022 world oil demand to hit 101.08mln BPD, up by 3.31mln BPD from 2021. Further, the EIA forecasts Brent crude oil spot prices to average USD 53bbl in both 2021 and 2022 compared with an average of USD 42/bbl in 2020. The agency did caveat that “the January STEO remains subject to heightened levels of uncertainty because responses to COVID-19 continue to evolve.” Looking ahead, tomorrow sees the release of the OPEC MOMR followed by the IEA’s take on Friday. Currently, Brent Mar resides just below USD 57/bbl having waned off its USD 57.40 high (vs USD 56.70 low), whilst WTI hit a peak of USD 53.90/bbl (vs low 53.29/bbl) before drifting lower. Elsewhere, spot gold and spot silver have given up their earlier gains as the Dollar recoups some lost ground, with the former now around USD 1850/oz (vs high USD 1863/oz). Finally, turning to base metals, LME copper has drifted off best levels as the Buck gains traction despite the mild gains seen across stock markets. Nickel prices meanwhile gained in Shanghai amid worries about supply disruptions in its top ore producers Philippines and New Caledonia.

US Event Calendar

- 8:30am: US CPI MoM, est. 0.4%, prior 0.2%; US CPI YoY, est. 1.3%, prior 1.2%

- US CPI Ex Food and Energy MoM, est. 0.1%, prior 0.2%; CPI Ex Food and Energy YoY, est. 1.6%, prior 1.6%

- 8:30am: Real Avg Hourly Earning YoY, prior 3.2%; Real Avg Weekly Earnings YoY, prior 4.7%

- 2pm: Monthly Budget Statement, est. $143.5b deficit, prior $145.3b deficit; 2pm: U.S. Federal Reserve Releases Beige Book

DB's Jim Reid concludes the overnight wrap

This morning we are launching our latest monthly survey. There is a big focus on whether you think there are bubbles in financial markets (and where) and also on whether there will be a taper tantrum in markets this year. In addition there are covid, vaccine and other market related questions. We nearly broke through a 1000 responses last month for the first time and while I expect January to be quieter I’m grateful for the continued support we are getting for this survey. Many thanks. The link is here and it will be open until Friday morning.

The big theme yesterday was a big intraday swing in rates as the European session saw yields rise everywhere but with this more than reversing late in the US session. The rally back seemed to start just ahead of the latest Treasury auction and accelerated on better than expected results. Early in the US trading day, US Treasury yields had climbed a further +3.9bps to 1.185%, their highest level since March before dropping -5.6bps to finish the day down -1.7bps at 1.129%. They are fairly flat in Asian trading as we type. US yields likely also fell due to the coordinated comments from Fed governors George, Bullard and Rosengren who all indicated that tapering was not imminent. We’ve only had 7 business days this year and we’ve already had a full 360 degree tapering debate played out by the Fed.

Fed Reserve president George, considered one of the more hawkish central bank officials, says it is “too soon to speculate” on when monetary policy support should be pulled back and that the Fed is not likely to react even if inflation rises just over 2%. Taken together with Fed governor Rosengren’s comments about not expecting “the US economy to reach a sustained 2% inflation rate” over the next two years it was an evening for market participants to reassess their views on a potential tapering schedule.

There was a similar pause in the recent relentless steepening of the US yield curve. The 2s10s slope dropped -1.5bps on the day after initially rising above 100bps for the first time in more than 3 years early in the US session prior to the Fed comments and the Treasury auction. Even if we didn’t hold above +100bps, it seems a long time ago now we were shouting from the rooftops about the inverted yield curve!

Though much of the market’s focus is understandably remaining on the US, Italian BTPs were a notable underpeformer yesterday, with their spread over bunds widening +5.8bps (+8.5bp in yield) in their biggest daily spread move higher since late October. The moves come on the back of heightened political instability and speculation over a potential government collapse, since there have been threats from former Prime Minister Matteo Renzi to withdraw the support of his Italia Viva party from the governing coalition led by PM Conte, because of disagreements over the government’s economic recovery plan. Matteo Renzi will apparently decide today on whether to topple the current government by withdrawing his ministers with a press conference scheduled at 530pm local time after his decision has been made. Amidst this speculation, it’s worth remembering that in the last 160 years, Italy has actually had 131 governments, so on average that’s just under 15 months each. Indeed, the current coalition has been going for 16 months now, so it’s already beaten the average length! We showed this in our chart of the day yesterday (link here), in what is probably the longest graph we’ll likely ever use (in length of page terms), with the lesson being that political risk in Italy is a perennial problem that the market regularly has to face even if the most likely outcome to any change of government is relatively sanguine in this instance. See Clemente’s latest blog for more on the potential scenarios here.

Elsewhere in Europe, the rates moves were in a similar direction to Italy, albeit more subdued, with yields on 10yr bunds (+2.9bps), OATs (+3.6bps) and gilts (+4.3bps) all moving higher even if the US late move will probably reverse much of this at the open this morning. Equity markets in the US were fairly flat on the surface with the S&P 500 just above unchanged at +0.04%. There was a good amount of sector rotation though, led in particular by cyclicals such as Autos (+4.79%), Energy (3.50%) – on the back of gains in the oil market – and Banks (1.53%). Pandemic-winners such as Media (-1.64%), Biotech (-1.23%) and Software (-0.99%) were the largest laggards as the reopening trade worked yesterday. The Russell 2000 Index of US small-caps rose another +1.77% to reach a fresh all-time high. As previewed above, Brent crude oil prices (+1.64%) reached their highest levels since the pandemic began.

In Europe, the STOXX 600 managed to eke out a +0.05% gain, even as the FTSE 100 (-0.65%) and the DAX (-0.08%) both lost ground. The sector rotation somewhat mirrored that of the US, where Autos (+1.73%) and Banks (+1.49%) were in favour, however here defensives – such as Utilities (-1.49%) and Consumer Products (-0.85%) – were the underperformers.

Turning to Asia now and a quick refresh of our screens shows that most markets are moving higher with the Nikkei (+1.05%), Shanghai Comp (+0.11%) and Kospi (+1.00%) all up. The Hang Seng is trading flattish. Meanwhile, futures on the S&P 500 are up +0.17%. Elsewhere, Brent crude oil prices are up +1.24% likely on news that Saudi Arabia slashed crude oil supplies to at least nine refiners in Asia and Europe after the kingdom volunteered to cut its production by 1 million barrels a day for February and March. According to the news, Saudi Aramco will supply less crude as part of long-term contracts next month, giving some Asian processors as much as 20%-30% less than they had sought. Bitcoin’s decline has also resumed this morning with the crypto currency being down -5.06% to $32,957 as we type.

In other news, Bloomberg has reported overnight that President-elect Joe Biden will seek a deal with Republicans on another round of Covid-19 relief, rather than attempting to get a package through without their support. This means that Biden’s talked about multitrillion-dollar economic package could now come in stages and a smaller initial package will likely have features that cater to some of the priorities favoured by Senate Republican leader Mitch McConnell. Elsewhere, the House voted overnight to demand that VP Pence invoke the Constitution’s 25th Amendment to remove Donald Trump from office, a largely symbolic move leading up to a vote today to impeach the President for a second time.

In terms of the latest on the coronavirus, a report from the Bild newspaper in Germany said that Chancellor Merkel had told her party’s lawmakers that Germany could need another 8-10 weeks of lockdown measures, and that the arrival of the UK variant could make things particularly hard. Elsewhere, even as the UK remains one of the leaders in getting people vaccinated the somber news on the virus spread is continuing. The UK has 3,363 patients on mechanical ventilation now, the highest since the pandemic began. The previous peak was set on April 12 2020 at 3,301.

Notwithstanding the short-term lockdown and virus gloom, with optimism on the recovery growing beyond Q1, there were some notable moves in inflation expectations yesterday, with 5y5y forward inflation swaps for the Euro Area rising 3.2bps to 1.36%, their highest in over a year. That follows the release yesterday of an interview by Isabel Schnabel of the ECB’s Executive Board, in which she played down the importance of any near-term increase in inflation, and also warned against tightening policy too soon. This effect was also seen in individual countries, with German 10yr breakevens rising above 1% for the first time since last February, while Italy’s reached a 2-year high of 0.97%.

Staying on central bank speak, sterling was the strongest performing G10 currency yesterday on the back of headlines that the Bank of England were pushing back on negative rate speculation. In particular, Governor Bailey said that "there are a lot of issues" with negative rates, which followed a more supportive speech from MPC member Tenreyro the day before. By the close, sterling had strengthened +1.08% against the US dollar, which itself was the weakest-performing currency in the G10, with the dollar index snapping a run of 4 successive gains to end the session -0.41% lower (down a further -0.12% this morning).

There weren’t a great deal of data releases yesterday, though we did get the JOLTS job openings from the US, which showed that job openings fell to 6.527m in November (vs. 6.45m expected), which was a smaller-than-expected decline. It’s worth noting that this measure lags the monthly jobs reports however, where the December number showed a -140k fall in nonfarm payrolls, which was the first decline since the height of the pandemic in March and April. Otherwise, the NFIB’s small business optimism index for December fell to 95.9 (vs. 100.2 expected), which is its lowest level in 7 months.

To the day ahead now, and data releases from the US include the December CPI release as well as December’s monthly budget statement. Meanwhile from Europe, we’ll get Euro Area and Italian industrial production for November. From central banks, we’ll hear from ECB President Lagarde and the ECB’s Villeroy, along with Fed Vice Chair Clarida and the Fed’s Bullard, Brainard and Harker. In addition, the Federal Reserve will be releasing their Beige Book.

Uncategorized

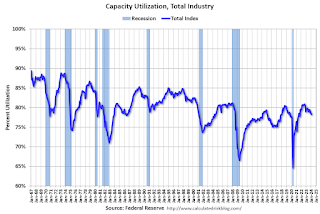

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

International

Fuel poverty in England is probably 2.5 times higher than government statistics show

The top 40% most energy efficient homes aren’t counted as being in fuel poverty, no matter what their bills or income are.

Share this:

The cap set on how much UK energy suppliers can charge for domestic gas and electricity is set to fall by 15% from April 1 2024. Despite this, prices remain shockingly high. The average household energy bill in 2023 was £2,592 a year, dwarfing the pre-pandemic average of £1,308 in 2019.

The term “fuel poverty” refers to a household’s ability to afford the energy required to maintain adequate warmth and the use of other essential appliances. Quite how it is measured varies from country to country. In England, the government uses what is known as the low income low energy efficiency (Lilee) indicator.

Since energy costs started rising sharply in 2021, UK households’ spending powers have plummeted. It would be reasonable to assume that these increasingly hostile economic conditions have caused fuel poverty rates to rise.

However, according to the Lilee fuel poverty metric, in England there have only been modest changes in fuel poverty incidence year on year. In fact, government statistics show a slight decrease in the nationwide rate, from 13.2% in 2020 to 13.0% in 2023.

Our recent study suggests that these figures are incorrect. We estimate the rate of fuel poverty in England to be around 2.5 times higher than what the government’s statistics show, because the criteria underpinning the Lilee estimation process leaves out a large number of financially vulnerable households which, in reality, are unable to afford and maintain adequate warmth.

Energy security

In 2022, we undertook an in-depth analysis of Lilee fuel poverty in Greater London. First, we combined fuel poverty, housing and employment data to provide an estimate of vulnerable homes which are omitted from Lilee statistics.

We also surveyed 2,886 residents of Greater London about their experiences of fuel poverty during the winter of 2022. We wanted to gauge energy security, which refers to a type of self-reported fuel poverty. Both parts of the study aimed to demonstrate the potential flaws of the Lilee definition.

Introduced in 2019, the Lilee metric considers a household to be “fuel poor” if it meets two criteria. First, after accounting for energy expenses, its income must fall below the poverty line (which is 60% of median income).

Second, the property must have an energy performance certificate (EPC) rating of D–G (the lowest four ratings). The government’s apparent logic for the Lilee metric is to quicken the net-zero transition of the housing sector.

In Sustainable Warmth, the policy paper that defined the Lilee approach, the government says that EPC A–C-rated homes “will not significantly benefit from energy-efficiency measures”. Hence, the focus on fuel poverty in D–G-rated properties.

Generally speaking, EPC A–C-rated homes (those with the highest three ratings) are considered energy efficient, while D–G-rated homes are deemed inefficient. The problem with how Lilee fuel poverty is measured is that the process assumes that EPC A–C-rated homes are too “energy efficient” to be considered fuel poor: the main focus of the fuel poverty assessment is a characteristic of the property, not the occupant’s financial situation.

In other words, by this metric, anyone living in an energy-efficient home cannot be considered to be in fuel poverty, no matter their financial situation. There is an obvious flaw here.

Around 40% of homes in England have an EPC rating of A–C. According to the Lilee definition, none of these homes can or ever will be classed as fuel poor. Even though energy prices are going through the roof, a single-parent household with dependent children whose only income is universal credit (or some other form of benefits) will still not be considered to be living in fuel poverty if their home is rated A-C.

The lack of protection afforded to these households against an extremely volatile energy market is highly concerning.

In our study, we estimate that 4.4% of London’s homes are rated A-C and also financially vulnerable. That is around 171,091 households, which are currently omitted by the Lilee metric but remain highly likely to be unable to afford adequate energy.

In most other European nations, what is known as the 10% indicator is used to gauge fuel poverty. This metric, which was also used in England from the 1990s until the mid 2010s, considers a home to be fuel poor if more than 10% of income is spent on energy. Here, the main focus of the fuel poverty assessment is the occupant’s financial situation, not the property.

Were such alternative fuel poverty metrics to be employed, a significant portion of those 171,091 households in London would almost certainly qualify as fuel poor.

This is confirmed by the findings of our survey. Our data shows that 28.2% of the 2,886 people who responded were “energy insecure”. This includes being unable to afford energy, making involuntary spending trade-offs between food and energy, and falling behind on energy payments.

Worryingly, we found that the rate of energy insecurity in the survey sample is around 2.5 times higher than the official rate of fuel poverty in London (11.5%), as assessed according to the Lilee metric.

It is likely that this figure can be extrapolated for the rest of England. If anything, energy insecurity may be even higher in other regions, given that Londoners tend to have higher-than-average household income.

The UK government is wrongly omitting hundreds of thousands of English households from fuel poverty statistics. Without a more accurate measure, vulnerable households will continue to be overlooked and not get the assistance they desperately need to stay warm.

Torran Semple receives funding from Engineering and Physical Sciences Research Council (EPSRC) grant EP/S023305/1.

John Harvey does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

european uk pandemicUncategorized

Southwest and United Airlines have bad news for passengers

Both airlines are facing the same problem, one that could lead to higher airfares and fewer flight options.

Share this:

Airlines operate in a market that's dictated by supply and demand: If more people want to fly a specific route than there are available seats, then tickets on those flights cost more.

That makes scheduling and predicting demand a huge part of maximizing revenue for airlines. There are, however, numerous factors that go into how airlines decide which flights to put on the schedule.

Related: Major airline faces Chapter 11 bankruptcy concerns

Every airport has only a certain number of gates, flight slots and runway capacity, limiting carriers' flexibility. That's why during times of high demand — like flights to Las Vegas during Super Bowl week — do not usually translate to airlines sending more planes to and from that destination.

Airlines generally do try to add capacity every year. That's become challenging as Boeing has struggled to keep up with demand for new airplanes. If you can't add airplanes, you can't grow your business. That's caused problems for the entire industry.

Every airline retires planes each year. In general, those get replaced by newer, better models that offer more efficiency and, in most cases, better passenger amenities.

If an airline can't get the planes it had hoped to add to its fleet in a given year, it can face capacity problems. And it's a problem that both Southwest Airlines (LUV) and United Airlines have addressed in a way that's inevitable but bad for passengers.

Image source: Kevin Dietsch/Getty Images

Southwest slows down its pilot hiring

In 2023, Southwest made a huge push to hire pilots. The airline lost thousands of pilots to retirement during the covid pandemic and it needed to replace them in order to build back to its 2019 capacity.

The airline successfully did that but will not continue that trend in 2024.

"Southwest plans to hire approximately 350 pilots this year, and no new-hire classes are scheduled after this month," Travel Weekly reported. "Last year, Southwest hired 1,916 pilots, according to pilot recruitment advisory firm Future & Active Pilot Advisors. The airline hired 1,140 pilots in 2022."

The slowdown in hiring directly relates to the airline expecting to grow capacity only in the low-single-digits percent in 2024.

"Moving into 2024, there is continued uncertainty around the timing of expected Boeing deliveries and the certification of the Max 7 aircraft. Our fleet plans remain nimble and currently differs from our contractual order book with Boeing," Southwest Airlines Chief Financial Officer Tammy Romo said during the airline's fourth-quarter-earnings call.

"We are planning for 79 aircraft deliveries this year and expect to retire roughly 45 700 and 4 800, resulting in a net expected increase of 30 aircraft this year."

That's very modest growth, which should not be enough of an increase in capacity to lower prices in any significant way.

United Airlines pauses pilot hiring

Boeing's (BA) struggles have had wide impact across the industry. United Airlines has also said it was going to pause hiring new pilots through the end of May.

United (UAL) Fight Operations Vice President Marc Champion explained the situation in a memo to the airline's staff.

"As you know, United has hundreds of new planes on order, and while we remain on path to be the fastest-growing airline in the industry, we just won't grow as fast as we thought we would in 2024 due to continued delays at Boeing," he said.

"For example, we had contractual deliveries for 80 Max 10s this year alone, but those aircraft aren't even certified yet, and it's impossible to know when they will arrive."

That's another blow to consumers hoping that multiple major carriers would grow capacity, putting pressure on fares. Until Boeing can get back on track, it's unlikely that competition between the large airlines will lead to lower fares.

In fact, it's possible that consumer demand will grow more than airline capacity which could push prices higher.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic stocks

Key shipping company files for Chapter 11 bankruptcy

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Part 1: Current State of the Housing Market; Overview for mid-March 2024

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex