Futures Fade Ahead Of ECB Decision During “Extremely Eventful Day” For Europe

Futures Fade Ahead Of ECB Decision During "Extremely Eventful Day" For Europe

US equity futures edged slightly lower on Thursday but rebounded…

Share this:

US equity futures edged slightly lower on Thursday but rebounded off session lows, as China’s worsening property crisis, political chaos in Italy where Mario Draghi rasigned as PM, and Russia’s plans to annex occupied Ukrainian territory all damped global sentiment, which however was offset by news that flows via the Nord Stream 1 pipeline had resumed and oil prices tumbled on fading US gasoline demand and a ramp up in Libyan output. Yes, as Bloomberg succinctly puts it, it has been an "eventful day" for Europe, that includes the resignation of Italian Prime Minister Mario Draghi, an ECB rate decision and the restart of Russian gas flows via the Nord Stream pipeline.

Investors were also waiting for American unemployment claims to gauge their potential impact on Federal Reserve policy tightening and for earnings from companies including AT&T, Philip Morris and Snap. A European Central Bank meeting that’s expected to result in its first rate-hike in more than a decade is also among a flurry of concerns for traders.

S&P 500 contracts were down just 0.1% and those on the Nasdaq 100 little changed as of 715am in New York. The tech-heavy Nasdaq 100 index had gained for a second day on Wednesday, rising to the highest level since June. The Stoxx Europe 600 Index and the euro recouped losses following the resignation of Italy’s Prime Minister Mario Draghi. Treasury yields rose, pushing the 10-year benchmark above 3% and the dollar was flat. Bitcoin slumped after Tesla announced it had sold 75% of its holdings.

In premarket trading, Tesla gained 1.7% after reporting second-quarter results that exceeded analyst expectations. The electric carmaker’s announcement that it had sold most of its bitcoin holdings triggered a selloff in the token and crypto stocks such as Coinbase. Peer Norwegian Cruise Line fell 6.4%. United Airlines slumped 11% after the carrier curbed flying for the rest of this year and lowered growth plans for 2023. Here are some other notable premarket movers:

- Alcoa Corp. (AA US) shares rise as much as 5.5% in US premarket trading after the aluminum producer reported 2Q adjusted Ebitda that topped the average analyst estimate and announced an additional $500 million authorization for future stock repurchases.

- United Airlines (UAL US) shares fall 6.4% in US premarket trading after the company reported adjusted earnings per share for the second quarter that missed the average analyst estimate.

- Carnival (CCL US) drops about 11% in US premarket trading after launching a $1 billion share offering in one of the year’s largest US equity raises to date, as part of a plan to help address its 2023 debt maturities.

- Cryptocurrency- exposed stocks are lower in premarket trading as Bitcoin extends declines after Tesla disclosed that it sold the majority of its holdings of the token during the second quarter.

- Marathon Digital (MARA US) -5%, MicroStrategy (MSTR US) -4%, Coinbase (COIN US) -4.5%, Riot Blockchain (RIOT US) -4.1%

- Las Vegas Sands (LVS US) shares rise 3.8% in premarket trading after the casino and resort company reported revenue for the second quarter that beat the average analyst estimate.

- Qualtrics (XM US) shares slide 4.4% in US postmarket trading after reporting second-quarter results and paring its revenue forecast for the full year. Analysts trimmed price targets on the stock to reflect a more difficult macroeconomic backdrop, while remaining positive on the longer- term prospects

- Keep an eye on Apple (AAPL US) as Morgan Stanley says that the company’s pivot to a subscription-like model creates a clear path to a market capitalization of more than $3 trillion.

“Markets are nervously awaiting the outcome of the July ECB and Fed meetings knowing all too well that these central banks are more than willing to renege on the signals about likely policy moves that they have provided previously,” said Aviral Utkarsh, a multi-asset strategist at NN Investment Partners.

In any case, risk sentiment remains fragile as investors debate whether equities have reached a trough after this year’s selloff amid the war in Ukraine, a slowdown in China and the prospect of a US recession. The resumption of gas exports to Europe through Nord Stream is set to provide some relief for the continent that’s racing to store the fuel before the winter.

Here are some ley Nord Stream 1 news:

- Nord Stream said gas delivery has resumed on Thursday morning, according to DPA. It was also reported that Nord Stream 1 gas pipeline nominations were at 29.3mln kWh/h from 06:00CET, according to the operator. Deliveries are reportedly around pre-maintenance levels of circa 40%

- Nord Stream data shows that gas flows are back to 40% capacity (pre-maintenance amount), according to Bloomberg.

- NEL and OPAL gas grids, connected to Nord Stream 1, show prelim. physical flows into Germany of 9.9mln KWH/H and 12.5mln KWH/H for 05:00-06:00BST.

- Head of German network regulator said gas nominations for Nord Stream 1 for today are still at 30% capacity and this is binding for the next 2 hours, while more changes over the day would be unusual, according to Reuters; German grid has signalled that Nord Stream gas flows have increased in the second hour.

- German Energy Regulator Bundesnetzagentur says real gas flows are above nominations re. Nord Stream 1, pre-maintenance level of 40% capacity could be surpassed today.

- Nord Stream 1 flows are at 29.3mln KWM/H at 07:00-08:00BST, according to the operator; at 29.3mln KWM/H at 08:00-09:00BST, according to the operator; at 29.3mln KWM/H at 09:00-10:00BST, according to the operator.

Meanwhile, US President Joe Biden said he expects to speak to Chinese leader Xi Jinping “within the next 10 days” as Washington considers lifting some tariffs on Chinese imports.

Markets are also assessing earnings to gauge how companies are managing amid the highest inflation in generations and escalating borrowing costs. Many stocks “are still in very distinct downtrends so you can see a rally off maybe an oversold level but really if you are not starting to recover and break into a better uptrend it really remains to be seen if this can continue,” said Cameron Dawson, NewEdge Wealth chief investment officer. “So it’s more a relief at this point and not necessarily a trend change.”

Geopolitics are adding to investors’ skittishness. Russian President Vladimir Putin has warned that unless a spat over sanctioned parts of the Nord Stream pipeline is resolved, flows will be tightly curbed, and some European countries are telling residents to conserve gas.

In Europe, losses for energy, mining and travel stocks outweighed gains in the media and tech industries, pulling the Stoxx Europe 600 Index down 0.2%. Nokia jumped 7.7%, the most in a year, as the Finnish company reported better-than-expected earnings strong demand for its 5G networks from phone carriers. Here are the other notable premarket movers:

- Sartorius AG preferred shares rise as much as 8.9% after the company issued its latest quarterly earnings and reaffirmed its guidance in a sign of strength, according to analysts.

- ASM International shares rise as much as 9.8% in Amsterdam as Jefferies says that the company’s quarterly update delivered “blowout” orders and strong guidance.

- Publicis shares gain as much as 5.6% after reporting strong 1H earnings that notably outperformed consensus estimates.

- Diploma shares jump as much as 5.8% after giving an update for 3Q that analysts described as “strong,” while reiterating annual guidance which was raised in April.

- Italian stocks extended their drop after Prime Minister Mario Draghi resigned, raising the prospect of snap elections. Poste Italiane slides as much as 8.9%, UniCredit -8.5%, Intesa Sanpaolo -7.4%

- SAP shares drop as much as 4.4% after the software company cut its full-year operating profit outlook, citing costs related to exiting Russia and a decline in license revenue.

- HelloFresh stock drops as much as 13% and is on track to post its biggest back-to-back decline on record after reducing full-year adjusted Ebitda guidance, which missed the midpoint of consensus estimates.

- Boliden shares slide as much as 5.5% to underperform the broader mining sector on Thursday, after the company posted 2Q results that analysts said highlighted the impact of higher costs.

Italy’s political turmoil ramped up the pressure on the ECB just before it unveils its new crisis management tool to shield the most vulnerable eurozone members from market speculation. Thursday’s monetary policy decision will end an era of negative rates that helped the region’s economies navigate the global financial crisis, the sovereign debt meltdown and then the 2020 pandemic. If the ECB’s tool is successful in leveling the playing field for countries with higher borrowing costs, and Russia keeps up gas exports, prospects for European markets are “very, very good,” said Andrew Sheets, Morgan Stanley’s chief cross asset strategist.

“The worst scenario would be gas cut off and a weak fragmentation tool from the ECB, because then I think you can see the market hit from both the growth side and the sovereign risk side,” Sheets said in an interview.

Earlier in the session, Asian stocks edged lower as investors assessed lingering risks of an economic downturn while monitoring central bank decisions in Japan and Europe. The MSCI Asia Pacific Index dropped as much as 0.5%, putting it on pace for its first decline in four sessions. Financials were the biggest drag on the gauge, while technology stocks rallied. Shares in Hong Kong and China fell. China’s stock benchmark index extends losses in the last hour of trade, wiping out its gains for the week. CSI 300 Energy Index down 3.5%, the worst performer among sub- gauges; CSI 300 Utilities Index down 3.1%. Tianqi Lithium -6.8% and China Shenhua Energy -5.6% are among the biggest losers on the benchmark CSI 300.

Japanese stocks edged higher after the Bank of Japan kept its monetary policy unchanged -- as expected -- despite more aggressive tightening being undertaken by its global counterparts. The European Central Bank is projected to raise interest rates for the first time since 2011 in a decision due later Thursday. Despite ongoing concerns about an economic slowdown in China and a US recession, some risk-on sentiment returned to Asian markets this week. The regional equity benchmark is still on track for a weekly gain of more than 2% on the back of optimism on US earnings and a weaker dollar. “Everybody’s waiting for earnings disappointments which haven’t necessarily appeared -- there’s a lot of cash on the sidelines,” Sean Darby, chief global equity strategist at Jefferies, said in a Bloomberg TV interview. “The market’s begun to become much more attuned to the fact that actually the Fed can engineer a soft landing.”

In FX, the euro slid after Draghi announced his resignation, erasing earlier gains of as much as 0.5% after Nord Stream AG said flows through Russia’s biggest pipeline to Europe restarted, and was also buoyed by speculation the European Central Bank may consider a rate hike that’s double the planned quarter-point increase at Thursday’s meeting. The Japanese yen fluctuated on the initial rate decision by the Bank of Japan, before weakening marginally after Bank of Japan Governor Haruhiko Kuroda emphasized his commitment to policy easing.

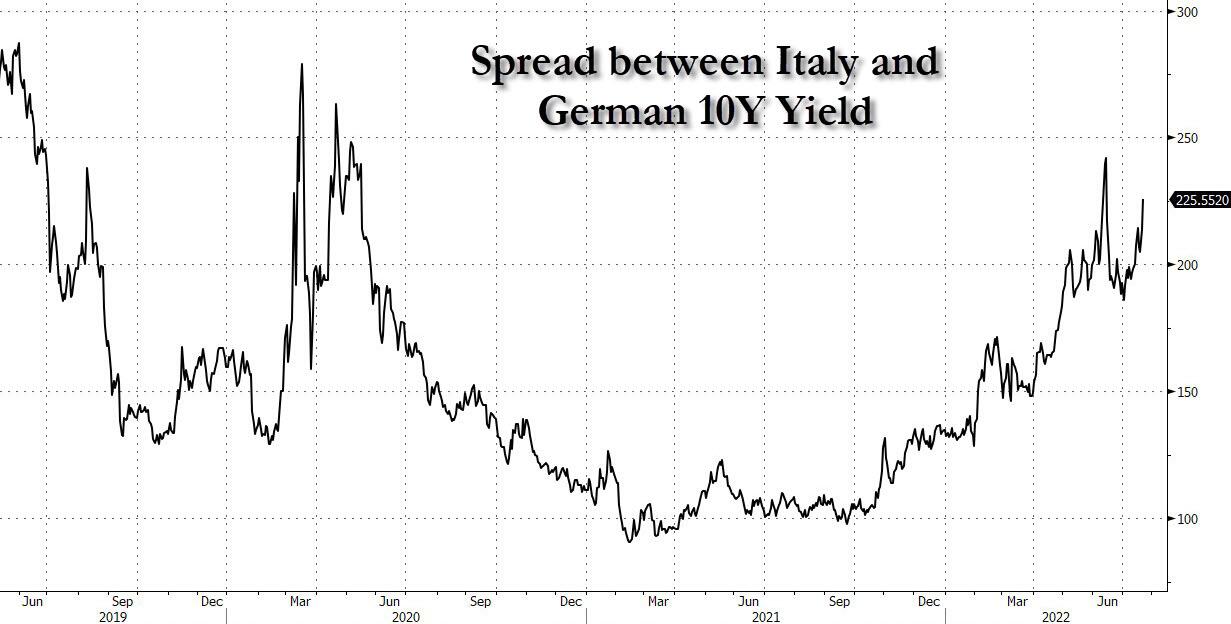

In rates, Italian bonds slumped on news that the coalition was on the brink of collapse on Thursday, with that decline extending after Draghi’s official resignation. Benchmark Italian 10-year yields rose as much as 22 basis points to 3.61%. The spread over equivalent German bonds, a common gauge of risk, rose to 233 basis points.

Treasuries were re slightly cheaper across the curve, with wider losses across gilts weighing ahead of the European Central Bank policy decision at 8:15 a.m. ET. US yields cheaper by up to 1.5bp across intermediates with 10- year yields around 3.05%; gilts lag by 2bp on the sector and Italian bonds by 12bp. Focus is on the sharp underperformance of Italian bonds, which is causing spreads to widen versus bunds amid the prospect of a snap election after Mario Draghi resigned. In the US, supply continues with 10-year TIPS auction, following Wednesday’s strong 20-year bond sale.

In commodities, oil was back below $100 a barrel as growing stockpiles of crude and gasoline tempered fears of a tight market. WTI drifted 4.4% lower to trade near $95.50. Brent falls 4.2% near $102.41. Base metals are mixed; LME zinc falls 2.1% while LME aluminum gains 0%. Spot gold falls roughly $13 to trade near $1,683/oz. Spot silver loses 2% near $18. Bitcoin dropped below $23,000.

To the day ahead now, and the main highlight will be the aforementioned ECB meeting and President Lagarde’s subsequent press conference. Other central bank speakers include BoE Chief economist Pill. Data releases include the US weekly initial jobless claims. Finally, earnings releases include Danaher, AT&T, Philip Morris International, Union Pacific and Blackstone.

Market Snapshot

- S&P 500 futures down 0.2% to 3,952.75

- STOXX Europe 600 down 0.3% to 421.33

- MXAP down 0.1% to 158.36

- MXAPJ little changed at 520.13

- Nikkei up 0.4% to 27,803.00

- Topix up 0.2% to 1,950.59

- Hang Seng Index down 1.5% to 20,574.63

- Shanghai Composite down 1.0% to 3,272.00

- Sensex up 0.3% to 55,537.07

- Australia S&P/ASX 200 up 0.5% to 6,794.28

- Kospi up 0.9% to 2,409.16

- German 10Y yield little changed at 1.31%

- Euro up 0.1% to $1.0194

- Brent Futures down 2.7% to $104.08/bbl

- Gold spot down 0.5% to $1,687.94

- U.S. Dollar Index little changed at 107.05

Top Overnight News from Bloomberg

- The Kremlin is in a dash to hold referendums in Ukrainian territories occupied by its troops to give grounds for President Vladimir Putin to absorb them into Russia as early as September, according to people familiar with the strategy.

- Prime Minister Mario Draghi offered his resignation to Italy’s president, in a move that will raise the prospect of snap elections as soon as early October

- Russia began sending natural gas to Europe through the Nord Stream pipeline system after a pause, bringing relief to a continent whose economy is starting to wobble under the strain of reduced supplies.

- Bank of Japan Governor Haruhiko Kuroda emphasized his determination to stick with rock-bottom interest rates even if it means a weaker yen after the bank’s latest price forecasts left the door open to continued speculation over policy change.

- China’s credit market is now showing stress on an almost daily basis, as a worsening property crisis shatters assumptions about safe borrowers and even Chinese investors turn against troubled debtors

- The European Central Bank is about to raise interest rates for the first time in 11 years, joining peers around the world in confronting a historic spike in inflation after months of standing on the sidelines.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded cautiously following the mixed performance of global counterparts and amid risk events. ASX 200 lacked firm direction as outperformance in tech was offset by weakness in energy and the mining-related sectors despite an increase in quarterly production by several key oil and gold producers. Nikkei 225 eked marginal gains after the BoJ maintained its ultra-easy policy setting but with upside capped given the worsening COVID situation in Japan. Hang Seng and Shanghai Comp. were subdued amid increasing tensions related to a planned visit to Taiwan by US House Speaker Pelosi which spurred warnings from China’s mouthpiece that suggested the mainland's reaction to such a visit would be unprecedented and involve a shocking military response.

Top Asian News

- US President Biden said the military does not think it is a good idea to travel to Taiwan now when questioned about a potential trip by House Speaker Pelosi, while he expects to speak with Chinese President Xi in the next 10 days, according to Reuters.

- US Commerce Secretary Raimondo warned of a deep recession if the US were to be cut off from Taiwan chip manufacturing, according to CNBC.

- China's ambassador to the US Qin said the China-Russia relationship is not an alliance and that the US is blurring the One China policy, while he added the US is bolstering links to Taiwan by sending officials.

- China Global Times' Hu Xijin tweeted earlier that it is certain the mainland's response to US House Speaker Pelosi's visit to Taiwan will be unprecedented and will involve a shocking military response.

- Asian Development Bank lowered Developing Asia growth forecast for 2022 to 4.6% from 5.2% and lowered 2023 growth forecast to 5.2% from 5.3%, while it cut its China 2022 growth forecast to 4.0% from 5.0%, according to Reuters.

European bourses gave up initial upside as Draghi resigns, Euro Stoxx 50 +0.1% however, current performance is more mixed with Nord Stream 1 flowing and earnings factoring. Stateside, futures are directionally in-fitting but with magnitudes more contained thus far awaiting earnings developments. Qatar Airways has ordered 25 Boeing (BA) 737 Max 10 jets.

Top European News

- Italian PM Draghi has tendered his resignation, according to a statement; President Mattarella has asked Draghi to carry on as a caretaker government.; subsequently, Italian President Mattarella will receive the upper and lower house parliamentary speakers this afternoon, according to a statement.

- Italy’s Worsening Political Crisis Adds to Bond, Stock Selloff

- Hungary Unveils Steep Household Energy Cost Hike in Orban U-turn

- Russia Resumes Nord Stream Gas Flow, Bringing Respite for Europe

- Dutch Pension Fund Switch to Steepen Dutch, German 10s30s: ABN

Central Banks

- BoJ kept its policy settings unchanged, as expected, with rates at -0.10% and QQE with yield curve control maintained to target 10yr JGB yields at around 0%. BoJ reiterated it will offer to buy 10yr JGBs at 0.25% every business day unless it is highly likely that no bids will be submitted and repeated its guidance on policy bias that it will take additional easing steps without hesitation as needed with an eye on the pandemic's impact on the economy, as well as kept forward guidance for short- and long-term rates to remain at present or lower levels. Furthermore, it stated that it must be vigilant to financial and currency market moves and their impact on Japan's economy and prices, while it lowered Real GDP growth forecast for the current fiscal year to 2.4% from 2.9%, but raised the Real GDP view for the two years after and increased CPI projections through to FY24.

- BoJ Governor Kuroda says rapid JPY weakening is a negative for the economy; inflation expectations substantial increasing over near-term, gradually mid/long-term; core unlikely to reach 2.0% currently. BoJ Governor Kuroda says no intention to raise interest rates under Yield Curve Control. Won't hesitate to ease monetary policy further if necessary; risks to the economy are skewed to the downside for the time being but will be balanced thereafter

FX

- Yen slides as BoJ and Governor Kuroda retain ultra easy policy and guidance, with latter adding no intention to tweak YCT range, USD/JPY back up near 139.00 from 138.00 low.

- Buck bounces broadly amidst renewed risk aversion with DXY back on 107.000 handle.

- Euro looking towards ECB for support after resignation of Italian PM nullifies partial return of Nord Stream gas flows, EUR/USD sub-1.0200.

- Kiwi reverses course in wake of NZ trade data revealing slowdown in exports and rise in imports to drag balance into deficit from surplus, NZD/USD loses 0.6200+ status.

- Aussie gleans some encouragement from NAB business conditions over confidence and rebound in AUD/NZD cross, AUD/USD off 0.6900+ peak, but holding above 0.6850.

- Loonie and Nokkie undermined by latest retreat in crude prices, USD/CAD over 1.2900 and EUR/NOK hovering around 10.1800.

Fixed Income

- Bonds off lows and braced for a busy pm agenda headlined by the ECB and the 25bp or 50bp hike verdict.

- Bunds back above 151.00 between 150.59-152.02 bounds, Gilts around 114.78 within a 115.11-114.59 range and 10 year T-note at 117-23+ vs 117-31+ peak and 117-18 trough.

- BTPs circa 200 ticks adrift awaiting Italian political developments after second resignation tender by PM Draghi.

Commodities

- WTI and Brent are under pronounced pressure amid multiple potential drivers as Nord Stream 1 resumes and Libya's oil output continues to climb, currently posting losses in excess of USD 4.00/bbl.

- Libya's oil output has recovered to above 700k BPD.

- Spot gold continues to drift after surrendering the USD 1700/oz mark amid renewed USD upside while base metals are mostly tempered amid a sullied risk tone.

US Event Calendar

- 08:30: July Initial Jobless Claims, est. 240,000, prior 244,000; Continuing Claims, est. 1.34m, prior 1.33m

- 08:30: July Philadelphia Fed Business Outl, est. 0.8, prior -3.3

- 10:00: June Leading Index, est. -0.6%, prior -0.4%

DB's Jim Reid concludes the overnight wrap

Today is my last day at work ahead of the wedding. Tomorrow we’ll be travelling back to our home county of Essex, and Saturday is the big day. There are many things I’m looking forward to, including having all our friends and family with us and obviously marrying the love of my life. Another plus is that we should never have to spend as much money on a single day ever again. There are some who’ve implied that marriage is a rather big risk to be playing at my age. But since I couldn’t be happier, I think the only risk would be doing anything else.

Whilst the wedding excitement is building up, markets are also getting excited as today is widely expected to bring the first ECB rate hike in over a decade. And unusually for a major central bank decision, there’s serious doubt about what’s going to happen. On the one hand, the ECB telegraphed explicitly at their last meeting that they would be commencing the hiking cycle with a 25bps hike today. But on the other hand, numerous press reports this week have cited ECB sources suggesting that a 50bp move is on the table as they grapple with the fastest inflation since the single currency’s formation, which was running at +8.6% in June. Market pricing is split as well, with overnight index swaps currently pricing in 35.8bps worth of hikes today, so almost equidistant between 25 and 50. And reflecting that uncertainty, EURUSD implied overnight volatility is at its highest level this morning since the height of the initial wave of the Covid pandemic in March 2020. So we’ve got a big day ahead of us.

The base case from our own European economists is that we’re still set for a 25bps move, and that a deviation by the ECB from their previous guidance could still impose a cost on the credibility of future communications. But the tone is likely to be hawkish regardless of whether they end up going for 25bps or 50bps (link here). The other thing to look out for today will be the details of an anti-fragmentation tool, which our economists are also expecting today. It’s possible that the more dovish Governing Council members concede on a 50bps hike in order to get concessions from the hawks on a stronger anti-fragmentation tool.

The importance of an anti-fragmentation tool came into focus yesterday amidst significant political turmoil in Italy, where the Draghi government is on the verge of collapse after three parties (the League, Forza Italia and the Five Star Movement) failed to back him in a Senate confidence vote. Bear in mind that Draghi had said that he was willing to continue, but wanted his original coalition to commit to reforms. So the latest moves raise the prospect that Draghi could resign again after his attempt last week was rejected by the President, which in turn brings the possibility of early elections into view. Even ahead of the confidence vote, Italian assets had suffered yesterday, with the FTSE MIB down -1.60%, just as the spread of Italian 10yr yields over bunds widened by +8.3bps to of 213bps.

That pessimistic tone in Italy yesterday was echoed across the continent, and the broader STOXX 600 fell -0.21%. But other equity markets were less affected by the volatility in Europe, and in the US the S&P 500 eventually managed to end the day up by +0.59% to reach a fresh one-month high. Tech stocks led that rally, with the NASDAQ up +1.58% and the FANG+ index up +2.22% following the news after the previous day’s close that the decline in Netflix subscribers wasn’t as bad as some had feared. And after the close, we heard from mega-cap Tesla as well, who beat analysts’ earnings estimates and traded just over +1% higher in after-hours trading. CEO Elon Musk expressed some optimism about supply chain issues that have long beleaguered automakers, including falling commodity prices.

For sovereign bonds it was also a day of swings, with Treasuries making gains before moving back into negative territory, and the 10yr yield ended the day up +0.6bps at 3.03%, though the 2s10s curved managed a modest +2.0bp steepening, taking it up to -20.5bps. This morning in Asia however, 10yr yields -1.1bps have reversed those gains and are trading at 3.02% again. Over in Europe, the greater risk-off tone led to a better performance outside of southern Europe, and yields on 10yr bunds (-2.0bps), OATs (-1.5bps) and gilts (-4.0bps) all moved lower on the day.

Staying on Europe, there was some further optimism on the energy side that the Nord Stream pipeline wouldn’t be completely closed in the coming days after the maintenance period ends today. One source of optimism was that grid data showed that gas orders had been made for deliveries today, albeit it’s worth noting that isn’t in itself a guarantee of the fuel being shipped. Natural gas futures themselves remained beneath their recent peaks earlier in the month, closing at €155 per megawatt-hour yesterday after only seeing a modest +0.38% rise on the previous day. So an important one to watch out for today alongside the ECB.

Overnight in Asia, equity markets are struggling this morning amidst the more downbeat newsflow, and a number of major indices including the Hang Seng (-1.37%), the Shanghai Composite (-0.42%) and the CSI (-0.46%) have all lost ground. That comes amidst concern about the growing number of Covid-19 cases in China, with yesterday saw 826 cases reported, which was down from 935 on Tuesday, but that itself was the highest number since May 21. That said, the Nikkei (+0.14%) has managed to eke out a modest gain after recovering from earlier losses, which follows the Bank of Japan’s decision to maintain its ultra-loose monetary policy. They decided to maintain their -0.1% policy rate, as well as the 0.25% yield cap on 10yr JGBs, and in their quarterly projections they raised their core CPI forecasts for fiscal year 2022 to 2.3% (vs. 1.9% previously). Nevertheless, their upgraded forecasts for FY 2023 and FY 2024 were still beneath 2%, at 1.4% and 1.3% respectively. Looking ahead, DM stock futures are seeing that negative tone continuing, with those on the S&P 500 (-0.20%), the NASDAQ 100 (-0.29%) and the DAX (-0.36%) all losing ground.

Elsewhere overnight, President Biden said that he expects to speak with China’s President Xi “within the next ten days”. There’s plenty to potentially discuss, and from an inflation standpoint it’ll be interesting to see if there’s any moves towards tariff reduction by Biden.

Here in the UK, the race to be the next Conservative leader and Prime Minister is now down to a run-off between former Chancellor Rishi Sunak and Foreign Secretary Liz Truss. The two will face a vote of Conservative Party grassroots members over the summer, with the winner to be announced on September 5. That follows the final ballot of MPs yesterday, in which Sunak came first with 137 votes, followed by Truss on 113, with trade minister Penny Mordaunt eliminated with 105. However, Sunak’s lead among MPs doesn’t mean he’s the favourite to win, with a YouGov poll of Conservative members finding that Truss would beat Sunak by 54%-35%.

Also in the UK, data yesterday showed that CPI inflation rose to a 40-year high of +9.4% in June (vs. +9.3% expected), although core inflation fell back a tenth as expected to +5.8%. That comes amidst growing expectations that the BoE will hike by 50bps at their next meeting for the first time since they gained operational independence in 1997. Over in Canada, CPI also rose to +8.1% in June, although this was beneath the +8.4% reading expecting.

To the day ahead now, and the main highlight will be the aforementioned ECB meeting and President Lagarde’s subsequent press conference. Other central bank speakers include BoE Chief economist Pill. Data releases include the US weekly initial jobless claims. Finally, earnings releases include Danaher, AT&T, Philip Morris International, Union Pacific and Blackstone.

Government

Looking Back At COVID’s Authoritarian Regimes

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

Share this:

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

These are the opening two paragraphs of my latest Defining Ideas article, “Looking Back at COVID’s Authoritarian Regimes,” Defining Ideas, March 14, 2024.

Another excerpt:

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

Read the whole thing, which is longer than usual.

(0 COMMENTS) budget deficit coronavirus covid-19 white house fauci trump canadaUncategorized

The hostility Black women face in higher education carries dire consequences

9 Black women who were working on or recently earned their PhDs told a researcher they felt isolated and shut out.

Share this:

Isolated. Abused. Overworked.

These are the themes that emerged when I invited nine Black women to chronicle their professional experiences and relationships with colleagues as they earned their Ph.D.s at a public university in the Midwest. I featured their writings in the dissertation I wrote to get my Ph.D. in curriculum and instruction.

The women spoke of being silenced.

“It’s not just the beating me down that is hard,” one participant told me about constantly having her intelligence questioned. “It is the fact that it feels like I’m villainized and made out to be the problem for trying to advocate for myself.”

The women told me they did not feel like they belonged. They spoke of routinely being isolated by peers and potential mentors.

One participant told me she felt that peer community, faculty mentorship and cultural affinity spaces were lacking.

Because of the isolation, participants often felt that they were missing out on various opportunities, such as funding and opportunities to get their work published.

Participants also discussed the ways they felt they were duped into taking on more than their fair share of work.

“I realized I had been tricked into handling a two- to four-person job entirely by myself,” one participant said of her paid graduate position. “This happened just about a month before the pandemic occurred so it very quickly got swept under the rug.”

Why it matters

The hostility that Black women face in higher education can be hazardous to their health. The women in my study told me they were struggling with depression, had thought about suicide and felt physically ill when they had to go to campus.

Other studies have found similar outcomes. For instance, a 2020 study of 220 U.S. Black college women ages 18-48 found that even though being seen as a strong Black woman came with its benefits – such as being thought of as resilient, hardworking, independent and nurturing – it also came at a cost to their mental and physical health.

These kinds of experiences can take a toll on women’s bodies and can result in poor maternal health, cancer, shorter life expectancy and other symptoms that impair their ability to be well.

I believe my research takes on greater urgency in light of the recent death of Antoinette “Bonnie” Candia-Bailey, who was vice president of student affairs at Lincoln University. Before she died by suicide, she reportedly wrote that she felt she was suffering abuse and that the university wasn’t taking her mental health concerns seriously.

What other research is being done

Several anthologies examine the negative experiences that Black women experience in academia. They include education scholars Venus Evans-Winters and Bettina Love’s edited volume, “Black Feminism in Education,” which examines how Black women navigate what it means to be a scholar in a “white supremacist patriarchal society.” Gender and sexuality studies scholar Stephanie Evans analyzes the barriers that Black women faced in accessing higher education from 1850 to 1954. In “Black Women, Ivory Tower,” African American studies professor Jasmine Harris recounts her own traumatic experiences in the world of higher education.

What’s next

In addition to publishing the findings of my research study, I plan to continue exploring the depths of Black women’s experiences in academia, expanding my research to include undergraduate students, as well as faculty and staff.

I believe this research will strengthen this field of study and enable people who work in higher education to develop and implement more comprehensive solutions.

The Research Brief is a short take on interesting academic work.

Ebony Aya received funding from the Black Collective Foundation in 2022 to support the work of the Aya Collective.

depression pandemicUncategorized

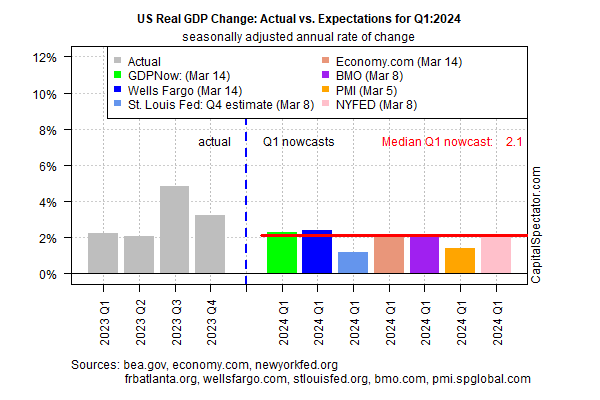

US Economic Growth Still Expected To Slow In Q1 GDP Report

A new round of nowcasts continue to estimate that US economic activity will downshift in next month’s release of first-quarter GDP data. Today’s revised…

Share this:

{kind=link}

A new round of nowcasts continue to estimate that US economic activity will downshift in next month’s release of first-quarter GDP data. Today’s revised estimate is based on the median for a set of nowcasts compiled by CapitalSpectator.com.

Output for the January-through-March period is currently projected to soften to a 2.1% increase (seasonally adjusted annual rate). The estimate reflects a substantially softer rise vs. Q4’s strong 3.2% advance, which in turn marks a downshift from Q3’s red-hot 4.9% increase, according to government data.

{kind=link}

Today’s revised Q1 estimate was essentially unchanged from the previous Q1 nowcast (published on Mar. 7). At this late date in the current quarter, the odds are relatively high that the current median estimate is a reasonable guesstimate for the actual GDP data that the Bureau of Economic Analysis will publish in late-April.

GDP rising at roughly a 2% pace marks another slowdown from recent quarters, but if the current nowcast is correct it suggests that recession risk remains low. The question is whether the slowdown persists into Q2 and beyond. Given the expected deceleration in growth on tap for Q1, the economy may be flirting with a tipping point for recession later in the year. It’s premature to make such a forecast with high confidence, but it’s a scenario that’s increasingly plausible, albeit speculatively so for now.

Yesterday’s release of retail sales numbers for February aligns with the possibility that even softer growth is coming. Although spending rebounded last month after January’s steep decline, the bounce was lowr than expected.

“The modest rebound in retail sales in February suggests that consumer spending growth slowed in early 2024,” says Michael Pearce, Oxford Economics deputy chief US economist.

Reviewing retail spending on a year-over-year basis provides a clearer view of the softer-growth profile. The pace edged up to 1.5% last month vs. the year-earlier level, but that’s close to the slowest increase in the post-pandemic recovery.

Despite emerging signs of slowing growth, relief for the economy in the form of interest-rate cuts may be further out in time than recently expected, due to the latest round of sticky inflation news this week.

“When the Fed is contemplating a series of rate cuts and is confronted by suddenly slower economic growth and suddenly brisker inflation, they will respond to the new news on the inflation side every time,” says Chris Low, chief economist at FHN Financial. “After all, this is not the first time in the past couple of years consumers have paused spending for a couple of months to catch their breath.”

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

recession pandemic economic growth fed recession gdp recovery consumer spending

Key shipping company files for Chapter 11 bankruptcy

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Part 1: Current State of the Housing Market; Overview for mid-March 2024

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Tight inventory and frustrated buyers challenge agents in Virginia

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A