Uncategorized

Futures Extend Slump To 3rd Day As Tech Rout Accelerates, Yields Rise, Oil Surges

Futures Extend Slump To 3rd Day As Tech Rout Accelerates, Yields Rise, Oil Surges

Global markets dropped, US futures extended their slump…

Share this:

Global markets dropped, US futures extended their slump into a third day and the Nasdaq 100 was on course for its first weekly loss of 2023, while Treasuries extended a selloff as wagers for more hawkish monetary policy mounted. Oil rose after Russia said it will cut output. Nasdaq futures were down 1.1% by 730 a.m. ET after the tech-heavy index lost 0.9% during the previous session, bringing this week’s declines to 1.5%. Nasdaq futs have broken below the support level of the rising channel since the start of the year.

The tech benchmark is still up over 13% year-to-date, but expectations of interest rates staying higher for longer - at least for a few more days - after a blowout US payrolls report and concerns about inflation pressures are weighing on sentiment. Investors will be closely watching the US inflation report next Tuesday for clues on the Fed’s monetary policy outlook.

S&P futures were also down, off by 0.6% and trading near session lows, and at the lowest level since the Golden Cross earlier this week. Treasury yields held gains across the curve after investors inverted the TSY yield curve by the most since the early 1980s, a sign of flagging confidence in the economy’s ability to withstand additional Federal Reserve hikes. The dollar reversed earlier losses when the yen surged after a report that Japan's Prime Minister Fumio Kishida had picked the hawkish Kazuo Ueda as the next head of the BOJ.

In premarket trading, Lyft tumbled as much as 35% after the ride-hailing company said it would prioritize lower prices to attract more customers, a move it expects to shrink future profits. Expedia Group was lower in premarket trading after reporting a fourth-quarter miss driven by bad weather. Here are some other notable premarket movers"

- BuzzFeed and SoundHound AI lead fellow artificial intelligence-related stocks lower in US premarket trading. The group is poised to extend losses from Thursday. AI-related stocks falling in premarket trading: BuzzFeed -10%, SoundHound AI -6%, BigBear.ai -3.5% and C3.ai Inc. -4%

- Expedia Group dips 2.3% after the US online travel agency reported a fourth-quarter miss, driven by bad weather. That said, a surge in January bookings sparks optimism around recovery in 2023, with some analysts raising price targets.

- PayPal shares slip 0.4%, erasing earlier gains, as analysts weighed the payment company’s miss on fourth-quarter total payment volume against better-than-expected EPS guidance, with some looking for more evidence of growth to justify further gains in the stock.

- Cloudflare rises 7.3% after the infrastructure software company gave a 2023 revenue forecast that beat the average analyst estimate. Analysts raised their price targets and said that the guidance will allay some investor concerns.

- Bloom Energy shares jumped 7.4% as analysts nudged their price targets higher on the power generation equipment maker, noting the company’s fourth-quarter revenue beat estimates.

- News Corp. shares drop 2.8% in US postmarket on Thursday after the media company reported adjusted earnings per share for the second quarter that missed the average analyst estimate and said it will cut 5% of its staff this year, or about 1,250 positions.

Stocks are heading for their first weekly decline in three after a chorus of Fed speakers reinforced the need to keep raising rates for longer, following a strong payrolls report, quashing the optimism that spurred a powerful rally in January. Next week’s inflation update from the US offers a relevant potential inflection point in the Treasury yield curve, according to Benjamin Jeffery and Ian Lyngen, strategists at BMO Capital Markets “Our expectations are that the market takes away sufficient angst regarding the prevailing inflation trend to press the inversion trade even further,” they wrote in a note.

Investors have become increasingly jittery about a hawkish policy tilt are paying close attention to official comments and economic data for clues on the rates trajectory. In Japan, reports of a surprise nomination for Kazuo Ueda to take helm at the Bank of Japan sparked a jump in the yen. It pared gains later as Ueda said the BOJ’s stimulus should stay in place.

"The momentum this week is building towards realizing that Powell’s last speech is actually not dovish and that translates on Treasuries yield and the Nasdaq,” said John Plassard, investment specialist at Mirabaud, confirming once again that price action sets the daily narrative. Investors initially brushed off the Fed chief’s warning on Tuesday that borrowing costs may need to peak higher than previously expected, and instead focused on his outlook that 2023 will be a year of significant declines in inflation.

And speaking of deflation, next week’s CPI data will mark a turning point for the equity rally at a time when investors are swapping stocks for bonds amid the specter of a recession, according to Bank of America strategists. US equity funds saw their first redemptions in three weeks, according to BofA’s note citing EPFR Global data. Bank of America strategist Michael Hartnett said that while it was “so very tempting” to believe that last week’s blowout US jobs report for January indicated the economy could avoid a contraction, the consumer-price data on Tuesday will be “vital” for clues on when the Federal Reserve would start easing up on monetary policy. Hartnett reiterated his 4,200 "sell" level.

In Europe, stocks were also lower with the Stoxx 600 down 1.1% and on course to snap a three day winning streak. Retailers, travel and consumer products are the worst-performing sectors. Here are some of the biggest European movers.

- Adidas shares drop as much as 12%, the most since March 2020, after the sportswear group warned that the fallout from the dispute with rapper and former partner Ye might lead to a €700 million operating loss in 2023

- Roche voting shares fall as much as 7.9% on news that an unnamed shareholder plans to sell a 2.5% stake in the Swiss pharmaceutical company

- HelloFresh falls as much as 8.9% as the meal-kit delivery firm is cut to underweight from neutral at JPMorgan

- Standard Chartered declines as much as 7% after First Abu Dhabi Bank reiterates that it’s not evaluating a possible offer for the London-based lender

- Schibsted slides as much as 5.7% after results, trimming a recent rally, after the Norwegian firm failed to offer Ebitda guidance at a group level

- Thule falls as much as 18%, the most since September, after the Swedish outdoor and bicycle equipment maker said it would replace its CEO

- Enel shares gain as much as 3.5%, the most since Jan. 4, after the Italian utility reported full-year revenue and adjusted Ebitda that beat estimates

- Saab jumps as much as 11% to a record after reporting a strong full-year performance

- Neobo Fastigheter AB rises as much as 56% on its first day of trading, bucking a trend in the real estate market that’s recently been in the limelight for its struggles

- Nobia gains as much as 5.6% after the Swedish kitchen interiors manufacturer reported in-line numbers in its 4Q report

- Iveco soars as much as 15%, the steepest gain on record, after the company reported 4Q results that Mediobanca (neutral) said are strong and “far above” consensus across the board

Earlier in the session, Asian stocks were poised for a second weekly decline as worries about a more hawkish Federal Reserve weighed on sentiment, while a pullback in China’s reopening rally also dragged the region’s equities. The MSCI Asia Pacific Index fell as much as 1.1% on Friday, with losses driven by consumer discretionary and communication service shares. The Hang Seng Index declined the most among benchmarks, led by Chinese technology stocks, while gauges for South Korea and Australia also fell. Onshore Chinese shares continued to retreat from their highs as traders await fresh impetus, with a mild pick-up in inflation — seen as reflecting improving demand — doing little to support share prices. Meanwhile, Japanese stocks edged higher as strong earnings from chipmakers providing a boost. However, Nikkei futures slipped after a report said Kazuo Ueda will be nominated as the Bank of Japan’s next governor. The Asian stock benchmark was poised to drop more than 1% this week, extending its slide from a late-January high. Global investors are starting to price in the prospect of higher interest rates, following a strong US jobs report last week and a string of hawkish comments by Fed officials. “Some investors are ramping up bets that we could see a whole lot more Fed tightening, but overnight index swaps are still pricing in easing by the end of the year,” said Edward Moya, senior market analyst at Oanda. “If inflation ends up being hotter-than-expected, the Fed will most likely go back to the hawkish playbook and signal more work needs to be done.”

Stocks in India declined for a second week in three amid rising wagers for further rate hikes by the global central banks, while an extension of a selloff in Adani Group shares weighed on investor sentiment. The S&P BSE Sensex fell 0.2% to 60,682.70 in Mumbai on Friday, stretching its weekly decline to 0.3%, while the NSE Nifty 50 Index declined by by a similar measure. The Reserve Bank of India raised its key lending rate by 25 basis points as expected to 6.50% earlier this week. The rate-setting panel said it remains open to further hikes if the inflation accelerates. US Federal Reserve as well as the Reserve Bank of India seem to be using a “firmer tone” regarding inflation containment, and “both sounded quite determined to hike rates again if data points favor the same,” according to Joseph Thomas, head of research at Emkay Wealth Management. Nine out of BSE Ltd.’s 20 sector-gauges fell on Friday, led by metal companies, which were also among worst performers for the week as worries over global growth and monetary tightening hurt stocks across Asia. Reliance Industries contributed the most to the Sensex’s decline on Friday, decreasing 0.8%. Out of 30 shares in the Sensex index, 14 rose, while 16 fell. Adani Group stocks capped another week of losses as a review by MSCI Inc. spurred concern about passive outflows from shares already reeling from the rout triggered by US short seller Hindenburg Research’s scathing report.

In FX, the dollar edged higher against its Group-of-10 peers as traders awaited Tuesday’s key inflation data to assess the outlook for Federal Reserve rate hikes. The gauge is set for a 0.3% gain this week as traders lifted bets on peak Federal Reserve policy rate after a slew of officials reiterated the need to hike rates further to quash inflation. In Japan, the yen initially jumped on media reports of a surprise nomination for Kazuo Ueda to take helm at the Bank of Japan — suggesting investors saw the move as hawkish. The currency later pared gains after Ueda said it’s important to keep BOJ easing for now

In rates, US treasuries extended losses over the London session, following wider selloff in bunds and gilts as money markets ramped up expectations that the ECB will raise the deposit rate to 3.75% by September. Front-end-led selloff in core rates pushed German 2-year yield 8bps higher to 2.77%, the highest since 2008. US yields cheaper by 3bp to 4.5bp across the curve with losses led by intermediates, cheapening the 2s5s10s spread by 1.5bp on the day; 10-year yields up to around 3.70% are near cheapest levels of the day with bunds and gilts lagging by 3bp and 4.5bp in the sector. Bear-flattening move in German curves have knocked 2s10s, 5s30s spreads tighter by 1bp and 2.5bp vs Thursday’s close.

In commodities, oil prices surged after Russian Deputy Prime Minister Alexander Novak said the country will cut output in March by 500,000 barrels per day. Russia did not consult with OPEC+ on its March oil production reduction, it was an independent decision, according to a source cited by Reuters. Subsequently, Russia's Kremlin says Russia held talks with some OPEC+ members on its decision to cut its oil output. OPEC+ will not boost supply in reaction to the Russian cut, according to delegates cited by Reuters. Brent crude futures have added 2.6% to trade around $86.70. Spot gold is little changed around $1,864.

To the day ahead now, and data releases include UK GDP for Q4, Italian industrial production for December, and in the US there’s the University of Michigan’s preliminary consumer sentiment index for February. From central banks, we’ll hear from the Fed’s Waller and Harker, the ECB’s Schnabel and de Cos, and BoE chief economist Pill.

Market Snapshot

- S&P 500 futures down 0.7% to 4,062.25

- MXAP down 0.8% to 166.52

- MXAPJ down 1.1% to 542.42

- Nikkei up 0.3% to 27,670.98

- Topix little changed at 1,986.96

- Hang Seng Index down 2.0% to 21,190.42

- Shanghai Composite down 0.3% to 3,260.67

- Sensex down 0.2% to 60,701.20

- Australia S&P/ASX 200 down 0.8% to 7,433.66

- Kospi down 0.5% to 2,469.73

- STOXX Europe 600 down 0.6% to 459.65

- German 10Y yield little changed at 2.36%

- Euro down 0.2% to $1.0718

- Brent Futures up 2.8% to $86.83/bbl

- Gold spot up 0.1% to $1,863.42

- U.S. Dollar Index little changed at 103.29

Top Overnight News from Bloomberg

- Japanese Prime Minister Fumio Kishida will nominate Kazuo Ueda, a professor and former Bank of Japan board member, to take the helm of the BOJ from April, according to local media reports, in a surprise move that sparked a jump in the yen

- Russia’s partners in the OPEC+ oil coalition signaled they won’t boost output to fill in for cutbacks announced by Moscow

- The UK avoided a recession last year by the narrowest of margins after the cost- of-living crisis and industrial action hit the economy during December

- The UK’s trade deficit with the European Union widened to a record in the final quarter of 2022 as imports from the bloc jumped

- Banks in the euro zone will return another €36.6 billion ($39.2 billion) in long-term funding to the European Central Bank after the terms of the programs were toughened to help the fight against inflation

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly negative after the losses on Wall St where the major indices wiped out initial gains and virtually spent the entire session on the back foot with sentiment hampered and recession fears stoked amid the deepest 2s/10s yield inversion since the 1980s. ASX 200 was dragged lower as underperformance in tech led the declines seen in almost all sectors and after the latest RBA Statement on Monetary Policy reaffirmed that further rate hikes will be needed. Nikkei 225 bucked the trend amid an overload of earnings releases and softer PPI data, although advances were capped as participants second-guess who will succeed BoJ Governor Kuroda. Hang Seng and Shanghai Comp. were lower with Hong Kong pressured by weakness in the property and tech industries, while frictions lingered as the US seeks to take action against Chinese entities linked to the surveillance balloon and reportedly aims to curtail technology investment in China.

Top Asian News

- RBA Statement on Monetary Policy noted that the board's priority is to return inflation to the target and that the board expects further increases in rates will be needed, while it is mindful that a considerable adjustment to interest rates has already been made and that monetary policy affects activity and inflation with a lag and through different channels. RBA also stated there are considerable uncertainties surrounding the outlook, and so around the level of interest rates needed to achieve the Board’s objectives.

- Singapore Backtracks on Grab’s Lawmaker Hire After Outcry

- Adani Stocks Decline as MSCI Action Raises Concern Over Outflows

European bourses are under pressure, Euro Stoxx 50 -1.2%, in a continuation of APAC/US trade that was exacerbated by the latest geopolitical developments re. Romanian airspace. Sectors are predominantly in the red with the exception of Energy given benchmark pricing while Retail names post marked underperformance amid heavy losses in Adidas. Stateside, futures are directionally in-fitting with Europe given broader geopolitics-induced action though with marked NQ -1.0% underperformance as yields pick up globally.

Top European News

- UK Treasury officials are in discussions to speed up Solvency II reforms and are considering whether to pursue a two-stage implementation, according to FT.

- ECB's Vujcic says core inflation is too high and ECB needs to see a sustained decline in the core rate. Not the time to discuss terminal, once the peak is reached will need to hold there for some time. Even if headline inflation fell below core, policy would need to remain restrictive.

- ECB TLTRO.III February 10th window repayment figure (EUR): 36.6bln vs exp. 60-320bln (prev. 62.75bln).

- Russian Federation Central Bank Key Rate (Feb) 7.50% vs. Exp. 7.5% (Prev. 7.5%); if pro-inflationary risks intensify will consider the necessity of hikes.

- Roche Foundation Buys Shares as Family Voting Stake Falls to 65%

- Jupiter’s Mid-Cap Fund Sinks Below £1 Billion AUM After 62% Fall

- UK Trade Deficit With EU Hits Record as Brexit Curtails Exports

- Russia to Cut Oil Output in Retaliation for West’s Sanctions

- Brent Oil Jumps Above $86 After Russia Says It Plans Output Cut

BOJ

- Japanese gov't is reportedly likely to nominate Kazuo Ueda as the new BoJ Governor, via Nikkei; to nominate Himino as the new Deputy. Japanese gov't initially approached BoJ deputy Amamiya as a possible successor but was met with a firm refusal. Click here for more detail.

- Touted BoJ Governor nominee Ueda said the BoJ's monetary policy is appropriate and they need to continue easy policy, speaking on NTV; when asked if he will be nominated as the next BoJ Governor, says nothing has been decided. Adds, it is important to make decisions logically and explain them clearly.

- Japan's government is to present the nominees for the BoJ leadership on February 14th at 02:00GMT/21:00EST, while the ruling and opposition parties are considering holding a hearing on the nominees in the lower house on February 24th, according to officials cited by Reuters. Subsequently confirmed by PM Kishida

Geopolitics

- "Ukrainian commander in chief Zaluzhny says 2 Russian kalibr missiles entered Moldovan and NATO-member Romanian airspace on their way to targets in Ukraine", via The Economists' Carroll; subsequently, Romania says it cannot confirm at this point that a Russian missile crossed its airspace though Moldova confirms it entered Moldovan airspace.

- Most recently, Romania's Defence Ministry says Russian missile did not reach Romanian airspace, but crossed Moldovan airspace.

- Ukrainian Energy Minister says Russian attacks hit power facilities in six regions, emergency shutdowns reported in many regions.

- French President Macron said he doesn't rule out sending fighter jets to Ukraine but added that it is not a priority for now, according to Reuters.

- Brazil reportedly bowed to US pressure and agreed to delay Iranian warships from docking in Rio de Janeiro until after President Lula meets with US President Biden, according to sources cited by Reuters.

FX

- JPY soared on reports that Ueda will be the gov'ts nomination for BoJ Governor, with USD/JPY dropping to 129.82 from 131.55; however, Ueda announcing he is happy with easy policy saw this unwind back towards 131.00.

- Amidst this, the DXY was pushed down to 102.89 though has since been revitalised by the above Ueda commentary and geopolitics, taking the index to a session peak of 103.50.

- More broadly, GBP and EUR initially benefitted from the above gyrations, but have since succumbed to the USD's strength and thus have been below 1.21 and 1.07 respectively.

- SEK continues to extend post-Riksbank while NOK benefited from very hot CPI which adds to conviction to the calls for more policy tightening than flagged by Governor Bache at the last gathering.

- PBoC set USD/CNY mid-point at 6.7884 vs exp. 6.7885 (prev. 6.7905)

- Banxico hiked rates by 50bps in a unanimous decision (exp. 25bps hike) and said for the next policy meeting, the upward adjustment to the reference rate could be of a lower magnitude.

Fixed Income

- Core benchmarks came under JGB-led pressure on the initial Ueda reports, sending Bunds, Gilts and USTs to 135.88, 104.07 and 112.29+ lows.

- However, this pressure has since eased a touch for EGBs given risk gyrations though USTs remain at session lows as the initial JGB-induced move was less pronounced stateside.

Commodities

- WTI and Brent are bolstered following Novak announcing that Russia is to cut oil production by 500k BPD in March.

- Currently, the benchmarks are firmer by circa. USD 2/bbl, though they have eased slightly from best levels as the USD lifts alongside the risk tone slipping somewhat.

- MMG (1208 HK) said the Las Bambas copper mine in Peru secured critical supplies that have enabled production to continue at a reduced rate and the property remains secure but transport disruptions continue and critical supplies remain low. Furthermore, it warned that if the situation of critical supplies persists, it would be forced to commence a period of care and maintenance.

- Damage assessment and repairs are taking place in Turkey's Ceyhan oil terminal and exports from BTC could begin on Sunday, according to a Turkish official and industry source cited by Reuters.

- Spot gold is modestly firmer and seemingly torn between geopolitical-induced haven appeal, though perhaps impacted by JPY action, and the associated pick up in the USD, as such the yellow metal is at the mid-point of USD 1852-1877/oz parameters.

US Event Calendar

- 10:00: Feb. U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

- 10:00: Feb. U. of Mich. 1 Yr Inflation, est. 4.0%, prior 3.9%

- 10:00: Feb. U. of Mich. Expectations, est. 63.1, prior 62.7

- 10:00: Feb. U. of Mich. Current Conditions, est. 68.5, prior 68.4

- 10:00: Feb. U. of Mich. Sentiment, est. 65.0, prior 64.9

- 14:00: Jan. Monthly Budget Statement, est. -$55b, prior $118.7b

DB's Jim Reid concludes the overnight wrap

Although the S&P 500 is still above where it was before the FOMC last Wednesday, it does feel like more challenging markets for both risk and rates have been developing since the payrolls number two days later.

After the strong 10yr auction on Wednesday, a weak 30-yr auction last night pushed yields higher across the curve in the last few hours of the session. US 30yr UST yields were up +5.5bps on the day and around 10bps off their pre-auction lows. This pulled up 10yr Treasury yields, which prior to the auction were down slightly, to close +4.8bps higher on the day at 3.658% and slightly up (+0.76 bps) this morning in Asia. There were bigger moves at the front end, with the 2yr yield up +6.1bps to 4.482%, and came as investors modestly raised their estimates of the Fed’s terminal rate. For instance, Fed funds futures are now expecting a 5.153% rate in July, up +1.5bps from the previous day, although still -0.05bps beneath its recent closing high on Monday.

The only silver lining from the poor 30 year auction was that it prevented the 2s10s curve from closing at its most inverted for 42 years. It moved as low as -87.2bps at one point before closing at -82.8bps as the back end got dragged up by the weak auction. Regardless of the brief respite, these curve levels are very extreme and at levels where a recession has always followed within months. Long-time readers will know that the 2s10s is my favourite US recession lead indicator. Critics might argue that some cycles have taken a lot longer to roll over than others after the initial inversion which means you can't rely on the curve for timings.

However, the lead time tightens up considerably when we only count it as a signal when the yield curve inverts for 3 months. In this cycle it first (briefly) inverted at the end of March last year but then only inverted on a sustained basis since the start of last July. After the 3 months rule has been triggered in the last 70 years, 8 out of 9 recessions have occurred between 8-19 months later. In this cycle that would take us to a range between March 2023 and February 2024.

The deeper curve inversion hurt US equities after a bright start in the first half of the session but the market didn't recover any poise in the last few hours of trading even as we steepened back. In the end, over 77% of the S&P 500 finished lower as the index posted a -0.88% loss. The large move higher in long-term yields weighed on tech stocks, which was one of the sectors that was keeping the index afloat in the morning. It was the first back-to-back -1.0% days for the S&P 500 since mid-December. Tesla remained an outperformer (+3.0%). Its share price now stands at nearly double its intraday low back on January 6, albeit down -49.98% from its all-time peak on November 4th. On the other hand, Alphabet fell a further -4.39% yesterday, following on from its -7.68% decline on Wednesday. Outside of Tesla and BorgWarner keeping the Autos sector above water (+2.44%), defensives like Food & Beverage (+0.01%) were the only industry group higher on the day.

Whilst US markets were fairly soft, European assets had a much stronger day thanks to some good news on the inflation side. First, we had the delayed German CPI figures for January, which showed inflation unexpectedly falling to 9.2% (vs. 10.0% expected) on the EU-harmonised definition. That’s a 5-month low, and is also the third consecutive decline since its peak of 11.6% back in October. The data might need to settle down a bit after the benchmark revisions though for economists to get the best view on trends. Second, European natural gas futures fell to a fresh 17-month low yesterday of €52.77 per megawatt-hour, which is another positive story for European consumers and should help sustain the recent downturn in inflation.

Against that backdrop, Euro sovereigns outperformed their counterparts elsewhere, with yields on 10yr bunds (-5.9bps), OATs (-6.1bps) and BTPs (-11.2bps) all seeing a decent decline on the day. It was a similar story for equities too, with the STOXX 600 (+0.62%) hitting a 10-month high and Germany’s DAX (+0.72%) reaching a one-year high.

The main exception to this European outperformance came from Sweden, which followed the Riksbank’s latest policy decision. This was the first meeting with the new Governor at the helm, and although the 50bps hike was expected, they also announced that QT would be starting from April and indicated that the policy rate would “probably be raised further during the spring.” That triggered a massive reaction among Swedish assets, with the Krona strengthening +2.36% against the US Dollar, whilst yields on 10yr Swedish government bonds were up by +23.0bps on the day.

Asian equity markets are mostly trading in the red following the second consecutive overnight losses on Wall Street. Across the region, the Hang Seng (-1.79%) is the biggest underperformer with the CSI (-0.72%), the Shanghai Composite (-0.60%) and the KOSPI (-0.59%) slipping in morning trading. Meanwhile, the S&P/ASX 200 (-0.67%) is also losing ground after the Reserve Bank of Australia (RBA) released its quarterly Statement on Monetary Policy (SoMP) in which it indicated that inflation remains high and flagged further interest rate hikes ahead. Elsewhere, the Nikkei (+0.22%) is bucking the regional downward trend. Outside of Asia, US stock futures are printing fresh losses with contracts tied to the S&P 500 (-0.17%) and NASDAQ 100 (-0.26%) both slightly down.

In early morning data, consumer prices in China (+2.1% y/y) rose at the fastest pace in three months in January, in line with market expectations and up from a +1.8% increase seen in December on the back of a spending surge over the Lunar New year festival. At the same time, factory gate prices (-0.8% y/y) dropped more than the anticipated -0.5% decline while extending the -0.7% drop in the preceding month. The mixed data highlights a staggered economic recovery in the world’s second largest economy even as it relaxed its stringent Covid-19 policy earlier this year. Meanwhile, Japan’s producer prices advanced (+9.5% y/y) in January (vs +9.7% expected), lower than the upwardly revised gain of +10.5% in December 2022.

There wasn’t much other data of note yesterday, but we did get the latest weekly initial jobless claims for the US, covering the week ending February 4th. Interestingly, they marked the first time this year that the number had surprised to the upside of consensus with a 196k reading (vs. 190k expected). Even so, the 4-week moving average still fell to its lowest level since April, at just 189.25k.

To the day ahead now, and data releases include UK GDP for Q4, Italian industrial production for December, and in the US there’s the University of Michigan’s preliminary consumer sentiment index for February. From central banks, we’ll hear from the Fed’s Waller and Harker, the ECB’s Schnabel and de Cos, and BoE chief economist Pill.

Uncategorized

The most potent labor market indicator of all is still strongly positive

– by New Deal democratOn Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently…

Share this:

- by New Deal democrat

On Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently than not indicated a recession was near or underway. But I concluded by noting that this survey has historically been noisy, and I thought it would be resolved away this time. Specifically, there was strong contrary data from the Establishment survey, backed up by yesterday’s inflation report, to the contrary. Today I’ll examine that, looking at two other series.

Uncategorized

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

US futures are trading modestly in positive territory and just shy of…

Share this:

US futures are trading modestly in positive territory and just shy of all time highs, after swinging between gains and losses as Europe trades higher and Asia closed weaker after US markets shrugged of a higher core CPI print and focused on the more constructive disinflation components (Super core 47bps vs 85bps). As of 7:50am, S&P futures traded +0.1% while Nasdaq futures were modestly red; earlier, Germany's DAX hit 18K for first time, while EuroStoxx50 hit 5K for first time in 24 years.

Overnight newsflow was relatively quiet outside of early results from Japan’s wage negotiations which showed majority of companies agreeing to unions demands: previously, BOJ's Ueda said wage negotiations were critical in deciding when to phase out its big stimulus program while Japan PM Kishida noted in Parliament that Japan has not emerged out of deflation, pushing back some expectations of BOJ exiting negative rates next week. UK Jan Industrial Production printed softer, Jan GPD/Manf Production in-line, and EZ Industrial Production printed weaker as well. Donald Trump clinched the Republican presidential nomination, setting up a combative election race with President Joe Biden. Elsewhere, US TSY 10Y yields are trading 1bp higher at 4.17% while bond yields across Europe ticked lower; the Bloomberg dollar index is fractionally lower, WTI crude is +$1.05 at $78.65, and bitcoin just hit a new all time high above $73,000.

In premarket trading, Nvidia shares rose again after the chipmaker rallied 7.2% and added $153 billion in market value on Tuesday. Tesla slipped after Wells Fargo downgraded the stock to underweight from equal-weight. Dollar Tree slumped after reporting fourth-quarter sales and profit that missed Wall Street’s expectations. The retailer also announced plans to close about 600 Family Dollar stores in the first half of the fiscal year.

- Beauty Health soars 21% after the skin-care company reported fourth-quarter sales that topped consensus estimates. The company named Marla Beck as CEO after a stint as interim CEO that began in November.

- Clover Health rises 9% after the Medicare Advantage insurer reported revenue for the fourth quarter that beat the average analyst estimate.

- Dollar Tree slumps 6% after issuing an annual sales outlook that fell short of the average analyst estimate at the midpoint of the forecast range.

- Eli Lilly rises about 1% after teaming up with Amazon.com Inc. to expand its nascent business of selling weight-loss drugs directly to patients.

- Petco (WOOF) rises 3% after the company reported comparable sales for the fourth quarter that topped the consensus estimate. Petco also said Ron Coughlin has stepped down as CEO/Chairman.

- Tesla (TSLA) falls 2% after Wells Fargo cuts the recommendation on the EV maker’s stock to underweight, saying there are fresh risks to EV volumes as price cuts are not having as much impact as before.

- ZIM Integrated Shipping (ZIM) falls 4% after the marine shipping company reported its fourth-quarter results and gave an outlook.

Traders held onto Fed rate cut bets for this year even after US inflation came in higher than expected on Tuesday. Futures are pricing in nearly 70% odds that the central bank will start easing in June and enact at least three quarter-point cuts over the course of 2024. Policymakers next gather March 19-20, where investors will key into the Federal Open Market Committee’s quarterly forecasts for rates, including whether fresh employment and inflation figures have prompted any changes.

“It’s going to be hard for the Fed not to be hawkish in the next meeting as the fight against inflation clearly isn’t won yet,” said Justin Onuekwusi, chief investment officer at wealth manager St. James’s Place. “That print does make you sit up and be alert of the risk inflation remain stubbornly high and that has massive feed-across right across portfolios. Markets may be underestimating impact of sticky inflation as they are still aggressively pricing a June rate cut.”

European stocks rise with the Stoxx 600 hovering near a record high and the Stoxx 50 breaching 5,000 for the first time in 24 years. Retail shares are leading gains after positive updates from Zalando and Inditex. Utilities and banks also outperform. Here are some of the biggest movers on Wednesday:

- Zalando shares jump as much as 18%, the most in five years, after results that analysts describe as positive, with a beat on adjusted ebit for 2023 and updated targets for growth through 2028. RBC analysts say they are confident in the German company’s ability to capture growth as consumer demand recovers.

- Inditex shares climbed as much as 5.2% to a fresh record high after the Zara parent reported what analysts called strong results thanks to continued robust demand for its clothing collections. The Spanish retailer plans to increase its annual dividend by 28% to €1.54 per share. H&M and the broader retail index also gain.

- BNP Paribas rises as much as 3.4% after the lender forecast higher-than-expected profit and stepped up cost savings measures.

- Balfour Beatty shares gain as much as 10%, its biggest intraday gain since August 2022, after the construction and infrastructure group reported full-year adjusted earnings per share that came ahead of consensus expectations. Additionally, the company announced a share buyback of £100 million for 2024. Liberum noted the strength in the company’s Gammon Construction joint venture, with Jardine Matheson.

- E.On shares jump as much as 7%, most in more than a year, after it reported a positive update according to Jefferies, with outlook ahead of consensus. Company also announced CFO Marc Spieker will assume role of COO and Nadia Jakobi is set to become CFO.

- Keywords Studios shares gain as much as 13%, the most since May 2020, after the company maintained FY goals issued in January, offering reassurance in a video game industry marked by layoffs at bellwethers including Sony and Electronic Arts. Keywords provides external technical support to video-game makers.

- Vallourec shares gain 9.8% after ArcelorMittal said it’s buying a stake in the tubular steel company from Apollo Global Management for about €955 million. Analysts highlight the deal triggers M&A speculation around Vallourec, and Oddo BHF expects ArcelorMittal to launch a takeover bid once the six-month lock-up period expires.

- Adidas shares fall as much as 4.1% as a lack of a full-year guidance upgrade from the sportswear maker disappointed some analysts, even as results were in line with January’s pre-released figures. The focus turns to the German firm’s growth outlook for the first quarter, and whether it will indeed see a pick-up in trading in the second half of the year.

- Solvay drops as much as 5.2% after guidance for lower Ebitda in 2024. Analysts note that the chemicals company’s commitment to a stable or growing divided may offset negatives from falling Ebitda. Investors will focus on the soda ash price assumptions, Morgan Stanley said.

- Geberit falls as much as 4.8% after the Swiss maker of building materials missed earnings estimates. The stock had rallied ahead of the earnings, gaining almost 8% from the start of February through Tuesday.

- Stadler Rail shares fall 3.3% after the Swiss train manufacturer’s sales and operating margins came in lower than estimates. The company’s 2024 outlook also weighs on sentiment, according to Vontobel.

The European Central Bank is also poised to start rate cuts soon, with Governing Council member Martins Kazaks saying on Wednesday reductions could come “within the next few meetings.” Bank of France Governor Francois Villeroy de Galhau said borrowing costs may be cut in the spring, with June more likely than April for a first move.

In FX, the Bloomberg Spot Index slips to reverse modest earlier gains while the yen was the weakest of the G-10 currencies, falling 0.2% versus the greenback to 148.05; the krone led G-10 gains. “BOJ Governor Kazuo Ueda clearly indicated yesterday that wages were the last piece of information needed before the central bank could decide whether to end its negative interest rate policy next week, said David Forrester, a senior FX strategist at Credit Agricole CIB in Singapore. “So the partial tally of the spring wage negotiations this Friday will be a decisive factor for the BOJ and the JPY in the coming week.” The pound was flat.

In rates, treasuries edged lower, with US 10-year yields rising 1bps to 4.16%. Gilts fall after data showed the UK economy rebounded in January. UK 10-year yields rise 2bps to 3.96%. Gilts lag across core European rates as market digests an offering of 30-year inflation-linked debt and a wave of domestic data. US session includes 30-year bond reopening, following soft reception for Tuesday’s 10-year sale. Treasury auction cycle concludes with $22b 30-year bond reopening after $39b 10-year reopening tailed by 0.9bp, while Monday’s 3-year new issue stopped through by 1.3bp. WI 30-year yield at ~4.320% is roughly 4bp richer than February refunding, which stopped through by 2bp in a strong auction

In commodities, oil advanced after four days of losses as an industry report pointed to shrinking US crude stockpiles, offsetting wavering OPEC cuts. WTI rose 1.5% to trade near $78.70. Spot gold adds 0.2%. and trades near all time highs.

Bitcoin rises 3% to a record high above $73,000 with Ethereum (+2.7%) also catching wind.

To the day ahead now, and data releases include UK GDP and Euro Area industrial production for January. Central bank speakers include the ECB’s Cipollone and Stournaras. And in the US, there’s a 30yr Treasury auction taking place.

Market Snapshot

- S&P 500 futures little changed at 5,176.25

- STOXX Europe 600 little changed at 506.38

- MXAP down 0.3% to 176.21

- MXAPJ down 0.3% to 540.31

- Nikkei down 0.3% to 38,695.97

- Topix down 0.3% to 2,648.51

- Hang Seng Index little changed at 17,082.11

- Shanghai Composite down 0.4% to 3,043.84

- Sensex down 1.0% to 72,924.23

- Australia S&P/ASX 200 up 0.2% to 7,729.44

- Kospi up 0.4% to 2,693.57

- German 10Y yield little changed at 2.30%

- Euro little changed at $1.0929

- Brent Futures little changed at $81.99/bbl

- Gold spot up 0.0% to $2,158.75

- US Dollar Index little changed at 102.93

Top Overnight News

- US President Biden secured enough votes to clinch the Democratic presidential nomination and Donald Trump secured enough delegates to win the Republican nomination, according to Reuters.

- Eli Lilly (LLY) is partnering with Amazon Pharmacy (AMZN) to deliver prescriptions sold through direct-to-consumer website.

- Some of Japan’s biggest companies, including Toyota, Nissan, and Nippon Steel, hand out large wage hikes to their workers (the biggest increases in decades), paving the way for a BOJ rate hike next week. FT

- China is scrapping a string of infrastructure projects in indebted regions as it struggles to reconcile a need to save money with this year’s target for economic growth. FT

- Chinese state media has touted President Xi Jinping as a market-friendly reformer on par with the paramount leader Deng Xiaoping, in an apparent attempt to dispel skepticism over the country’s growth outlook. BBG

- The European Central Bank will lower borrowing costs in the spring, with June more likely than April for a first move, Bank of France Governor Francois Villeroy de Galhau said. BBG

- Putin says Russia is willing to resolve the Ukraine war “by peaceful means”, but insists Moscow would require security guarantees to do so. BBG

- Donald Trump and Joe Biden have both secured enough delegates to clinch their respective party nominations, cementing a November rematch. The 2024 election is expected to be one of the most expensive on record. BBG

- US crude stockpiles fell by 5.5 million barrels last week, the API is said to have reported, registering the first decline in seven weeks if confirmed by the EIA. Gasoline and distillate supplies also dropped. BBG

- Global dividends hit a record $1.66 trillion last year, according to Janus Henderson. Payouts were up 5%, with almost half the growth coming from the banking sector. It’s the third annual record for dividends and the fund manager expects another all-time high this year. BBG

- Hedge funds are unwinding short Treasury futures bets at a rapid clip, a sign that basis-trade positions are diminishing. This is probably due to asset managers pivoting into investment-grade credit. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as early momentum from the tech-led gains on Wall St was offset by Chinese developer default concerns and as participants digested Japanese wage hike announcements. ASX 200 was led higher by consumer stocks after China's MOFCOM released an interim proposal to remove tariffs on Australian wine although the advances in the index were limited by losses in the mining sector as iron ore prices continued to tumble. Nikkei 225 swung between gains and losses with initial strength reversed amid firm wage hike announcements. Hang Seng and Shanghai Comp. were varied and price action was contained within relatively narrow ranges with the Hong Kong benchmark kept afloat by strength in auto names and tech, while the mainland was pressured amid developer default fears and with the US House set to vote later on the TikTok crackdown bill.

Top Asian News

- Country Garden Holdings (2007 HK) onshore bondholders said they have not received a coupon payment due on Tuesday, while the developer said funds for a CNY 96mln coupon payment due on Tuesday were not fully in place and it plans to do its best to raise money for payment within a 30-day grace period, according to Reuters.

- TikTok US executives told headquarters recently that a ban wasn't an imminent risk, according to WSJ citing sources. However, it was separately reported that the US House plans to vote on the TikTok crackdown bill today at around 10:00EDT (14:00GMT).

European bourses, Stoxx600 (+0.2%), are modestly firmer, though with overall trade rangebound in what has been an uneventful session. The IBEX 35 (+1.3%) outperforms, led higher by post-earning strength in Inditex (+4.2%). European sectors are mixed; Retail outperforms, propped up by gains in Zalando (+13.5%) and Inditex. Autos is found at the foot of the pile, hampered by a poor Volkswagen (-0.8%) update. US equity futures (ES U/C, NQ -0.2%, RTY +0.1%) are trading around the unchanged mark, with slight underperformance in the NQ, paring back some of the strength seen in the prior session.

Top European News

- ECB's Villeroy noted broad agreement in the ECB to start cutting rates in spring as the battle against inflation is being won, while he noted the risk of waiting too long before loosening monetary policy and unduly hurting the economy is now “at least equal” to acting too soon and letting inflation rebound, according to an interview with Le Figaro; In another batch of comments: Says the ECB is winning the battle against inflation; will remain vigilant on inflation but victory is within sight; Spring rate cut remains probably; more likely to cut rates in June than April.

- ECB's Kazaks says ECB rate cut decision will come in the next few meetings; uncertainty remains high, and tensions in the labour market is still high.

- Citi expects BoE to start cutting rates in June (vs prev forecast of August).

Japan

- Japan Chief Cabinet Secretary Hayashi said it is important for wage hikes to spread to mid-sized and small companies, while he added they are seeing strong momentum for wage hikes. It was also reported that Toyota, Nissan, Panasonic, Hitachi & Nippon Steel were among the companies that have responded to unions' wage hike demands in full.

- Japanese PM Kishida says will call for pay hikes exceeding last year at small and mid-sized firms during the meeting with labour union and management; Japan not yet emerging out of deflation.

- BoJ Governor Ueda says BoJ will consider tweaking negative rates, YCC, and other monetary easing tools if the sustained achievement of price target comes into sight. We must scrutinize whether positive wage-inflation cycle merges in deciding whether conditions for phasing out stimulus are falling into place. This year's wage talks is critical in deciding timing on exit from stimulus. Unions have demanded higher pay, seeing many corporate management making offers that will stream in today and beyond. Will scrutinize the wage talk outcomes, as well as other data and information from hearings when making policy decisions.

- Japanese PM Adviser Yata says wage hikes this year likely to exceed last year's; Must continue pay rises next year and thereafter to defeat deflation; must broaden pay hikes to workers nationwide and in every prefecture. When asked if solid wage offers could trigger end to NIRP in march, Yata says government will not meddle with the BoJ's independent policy-making.

- BoJ is reportedly to mull ending all ETF purchases if price goal is in sight; likely to keep buying bonds to keep market stable and to intervene in the event of sharp yield upside, according to Bloomberg sources.

- Japan's Business Lobby Keidanren Head Tokura says wage increases indicated in the preliminary survey of big firms' wage talks are likely to exceed last years levels.

- Early signs of a strong outcome in this year's annual wage talks have heightened changes the BoJ will end its negative interest rate policy next week, according to Reuters sources; "There seems to be enough factors that justify a March policy shift".

FX

- Marginal upside for the USD which has seen DXY kiss the 103 mark in quiet trade. If the level is cleared, yesterday's 103.17 will come into view.

- Uneventful price action for EUR with ECB comments unable to shift the dial. As such, the pair is sticking to a 1.09 handle and within yesterday's 1.0902-43 range.

- GBP is steady vs. the USD and stuck on a 1.27 handle as in-line GDP metrics failed to inspire price action. For now, yesterday's 1.2746-1.2823 range holds.

- JPY is marginally softer vs. the USD but with losses tempered by reports that the BoJ could end ETF purchases. Today's 147.24-89 range sits within yesterday's 146.62-148.18 parameters. More broadly, focus is on in

- AUD is holding up vs. the USD despite falling iron ore prices, with AUD/USD maintaining 0.66 status and within yesterday's 0.6596-0.6627 range. Likewise, NZD/USD is unable to break out of yesterday's 0.6133-6184 range. RBNZ's Conway later today could help to decide direction.

- PBoC set USD/CNY mid-point at 7.0930 vs exp. 7.1775 (prev. 7.0963).

Fixed Income

- Gilts are the relative laggards, at lows of 99.68, with the paper unreactive to the UK's GDP data (which was broadly in-line). The downside can be attributed to Gilts paring some of Tuesday's outperformance following the labour data and a strong DMO sale.

- USTs are essentially unchanged in a quieter session for the US (on paper) after Tuesday's marked CPI moves and a soft 10yr auction, despite the marked concession built in by the post-CPI reaction. Currently holds near session lows at 111-04.

- Bunds are slightly firmer after Tuesday's marked US CPI-induced pressure. Specifics are relatively light thus far, but focus will be on the ECB Operational Framework Review (tentatively due today). Currently, Bunds hold around 133.24, with the peak for today at 133.27.

- Italy sells EUR 7.25bln vs exp. EUR 6-7.25bln 2.95% 2027, 3.50% 2031, 3.25% 2038 BTP Auction and EUR 1.25bln vs exp. EUR 1-1.25bln 4.0% 2031 BTP Green.

- Germany sells EUR 3.738bln vs exp. EUR 4.5bln 2.20% 2034 Bund: b/c 2.29x (prev. 2.10x), average yield 2.31% (prev. 2.38%) & retention 16.9% (prev. 17.5%)

Commodities

- Crude is firmer, taking impetus from Tuesday's bullish private inventory data, with specifics light in the session thus far; Brent holds near session highs at +1.1%.

- Flat trade in gold and a mild upward bias in silver with the Dollar steady, calendar light, and with the ongoing geopolitical landscape potentially providing a modest underlying bid; XAU trades in a tight USD 2,155.86-2,161.66/oz range.

- Base metals are mixed with copper prices outperforming following reports that top Chinese copper smelters have reportedly reached an agreement to take action to curb falling fees.

- Azerbaijan oil production stood at 476k BPD in Feb (prev. 474k BPD in Jan), according to the Energy Ministry.

- Top Chinese copper smelters have reportedly reached an agreement to take action to curb falling fees, according to Reuters sources; smelters to cut output at loss-making plants.

- BP (BP/ LN) and ADNOC suspend USD 2bln talks to take Israel-based Newmed private, via Bloomberg.

Geopolitics: Middle East

- CIA Director Burns said there is "still a possibility" of a Gaza ceasefire deal but added that many complicated issues are still to be worked through.

- US may urge partners and allies to fund a privately run operation to send aid by sea to Gaza that could begin before a much larger US military effort, according to sources cited by Reuters.

- US Central Command announced that Houthis fired a close-range ballistic missile from Yemen toward USS Laboon in the Red Sea on March 12th but it did not impact the vessel, while CENTCOM forces and a coalition vessel successfully engaged and destroyed two unmanned aerial systems launched from Yemen.

Geopolitics: Other

- Ukrainian Army Chief Syrskyi and Ukraine's Defence Minister Umerov held a phone call with US Defense Secretary Austin on weapons delivery to Ukraine, according to Reuters.

- A fire at oil refinery in Ryazan region extinguished, according to the governor cited by Reuters.

US event calendar

- 07:00: March MBA Mortgage Applications 7.1%, prior 9.7%

Government Agenda

- 4 p.m: US President Joe Biden delivers remarks in Milwaukee, Wisconsin on how his investments are rebuilding communities and creating jobs

- 11.15 a.m: US Secretary of State Antony Blinken meets with EU foreign affairs chief Josep Borrell

DB's Jim Reid concludes the overnight wrap

Next stop on the global tour is Singapore as I'm about to board the plane from Melbourne here this evening. My vaguely fascinating fact about Singapore is that my grandfather was a civil engineer there in the 1920s and 1930s and helped build much of its rapid development at the time. He was Scottish and met my Dutch grandmother there and got married without speaking each other's language and being able to understand each other. My wife says she's done the same thing! His brother owned a very successful industrial company on the island and lost all his wealth and his company after the 1929 stock market crash. My entire family were eventually left penniless after the 1930s crash and then WWII. 90 years later and my kids have had the same impact on me!

I'm looking forward to landing in the pretty standard 35 degree heat that Singapore always seems to have on landing. Talking of the heat, even with another hot US inflation print, risk assets put in another strong performance yesterday, with both the S&P 500 (+1.12%) and Europe’s STOXX 600 (+1.00%) driven by strong tech gains (sound familiar?). The highs in the main indices came despite the latest US CPI report for February, which saw inflation come in strongly for a second month running, and led to growing fears that the last phase of getting inflation back to target would be the hardest. But despite the persistence of inflation, investors were remarkably unphased for the most part, and they continue to see a June rate cut as the most likely outcome.

In terms of the details of the report, headline CPI came in at a 6-month high of +0.44%, which meant the year-on-year measure actually ticked up a bit to +3.2% (vs. +3.1% expected). Alongside that, core CPI was at +0.36%, which also meant annual core CPI was also above expectations at +3.8% (vs. +3.7% expected). Some of the blame was placed on shelter inflation, which was up by a monthly +0.43%. But even if you looked at core CPI excluding shelter, it was still up by +0.30%, so it’s difficult to say that shelter was the whole story behind the ongoing persistence. See our US economists’ reaction to the print here.

For the Fed, there must be some concern even if markets show little of this. For instance, if you look at core CPI on a 3-month annualised basis, it rose to +4.2%, so it’s getting harder to explain this away as just one month of bad data. Bear in mind that this is pretty high by historic standards as well, and apart from the post-Covid inflation, 3m core CPI hasn’t been that high since 1991. Alongside that, there was evidence that the inflation was coming from the stickier categories in the consumer basket. In fact the Atlanta Fed’s sticky CPI series is now up by +5.1% on a 3m annualised basis, the fastest it’s been since April 2023. So the concern for markets will be that inflation is showing some signs of rebounding, or at the very least stabilising at above-target levels.

When it comes to the Fed, the report led investors to dial back the rate cuts priced this year by -6.1bps, and futures now see 85bps of cuts by the December meeting. There was also a bit more doubt creeping into the chance of a cut by June, with 78% now priced in, down from 86% the previous day. But even with this slightly hawkish repricing, June is still considered the most likely timing for the first cut, which helped to support risk assets even though the print was above expectations. For the Fed, the most important question now will be how this affects the PCE measure of inflation, which is what they officially target. We won’t find that out until March 29th (Good Friday), but we should get a bit more info from the PPI report tomorrow, which has several components that feed into PCE.

The report led to a selloff for US Treasuries, with the 2yr yield (+5.0bps) up to 4.59%, whilst the 10yr yield (+5.4bps) rose to 4.15%. The 10yr yield had peaked at 4.17% intra-day shortly after the latest 10yr Treasury auction which saw slightly soft demand, with bonds issued +0.9bps above the pre-sale yield.

The fixed income selloff was echoed in Europe too, even if the overall performance was better there, with yields on 10yr bunds (+2.7bps) and OATs (+1.6bps) rising by a smaller amount. At the same time, markets remain confident of an ECB cut by June (priced at 91% vs 95% the day before). This is consistent with the latest ECB commentary, with Austria’s Holzmann (strong hawk) saying that a June cut was more likely than April, while France’s Villeroy suggested that “there’s a very broad agreement” to cut rates by the June meeting.

Yesterday’s main outperformer in the rates space were 10yr gilts (-2.5bps), which came after the UK labour market data was a bit weaker than expected over the three months to January. Notably, wage growth slowed to an 18-month low of +5.6% (vs. +5.7 expected), and the unemployment rate ticked up to 3.9% (vs. 3.8% expected).

Although sovereign bonds struggled yesterday for the most part, there was a much better performance for equities. In the US, the S&P 500 (+1.12%) closed at a new record, with tech stocks and the Magnificent 7 (+2.88%) leading the advance. Nvidia was +7.16% higher. Likewise in Europe, the STOXX 600 (+1.00%) hit an all-time high, and there were new records for the DAX (+1.23%) and the CAC 40 (+0.84%) as well. That said, gains more moderate outside of tech, with the equal-weighted S&P 500 up by +0.26%, while the small-cap Russell 2000 (-0.02%) narrowly lost ground for a 3rd consecutive day.

This backdrop was mostly positive for other risk assets. US HY credit spread fell -6bps, closing just 3bps above their 2-year low reached in late February. Meanwhile, Bitcoin posted a new intra-day high just shy of $73,000, surpassing the market cap of silver. Marion Laboure and Cassidy Ainsworth-Grace's new report this morning discusses the upcoming halving event's impact on Bitcoin prices, along with the Dencun upgrade scheduled for Ethereum today (link here).

Asian equity markets are mixed this morning with the Hang Seng (+0.26%) and the KOSPI (+0.11%) edging higher while the Nikkei (-0.36%) continues to drift back from last week's all time highs. Elsewhere, stocks in mainland China are also seeing losses with the CSI (-0.59%) and the Shanghai Composite (-0.26%) dragged lower by property developers as Country Garden Holdings Co. missed a 96-million-yuan ($13 million) coupon payment on a yuan bond for the first time. Outside of Asia, US stock futures are struggling to gain momentum with those on the S&P 500 (-0.03%) and NASDAQ 100 (-0.06%) flat. In early morning data, the unemployment rate in South Korea unexpectedly dropped to +2.6% in February from January's 3.0% level (v/s +3.0% consensus expectation).

Although the CPI release was the main data focus yesterday, there was also the NFIB’s small business optimism index from the US. That f ell to a 9-month low in February of 89.4 (vs. 90.5 expected). And there were also further signs of softening in the labour market, as the share planning to increase employment was down to a net +12, the lowest since May 2020 at the height of the Covid-19 pandemic. Likewise, the share of firms with positions they weren’t able to fill hit a three-year low of 37%.

To the day ahead now, and data releases include UK GDP and Euro Area industrial production for January. Central bank speakers include the ECB’s Cipollone and Stournaras. And in the US, there’s a 30yr Treasury auction taking place.

Uncategorized

Bougie Broke The Financial Reality Behind The Facade

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive…

Share this:

{kind=link}

{kind=link}

{kind=link}

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

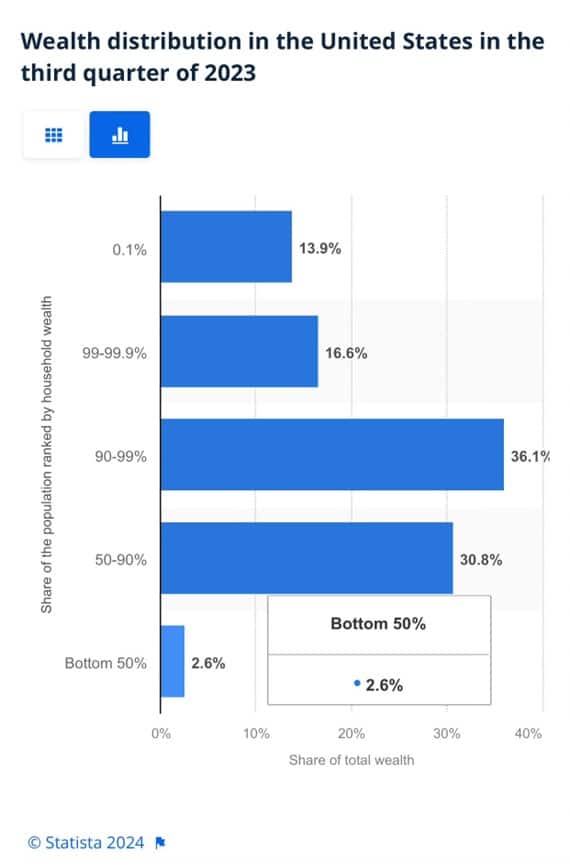

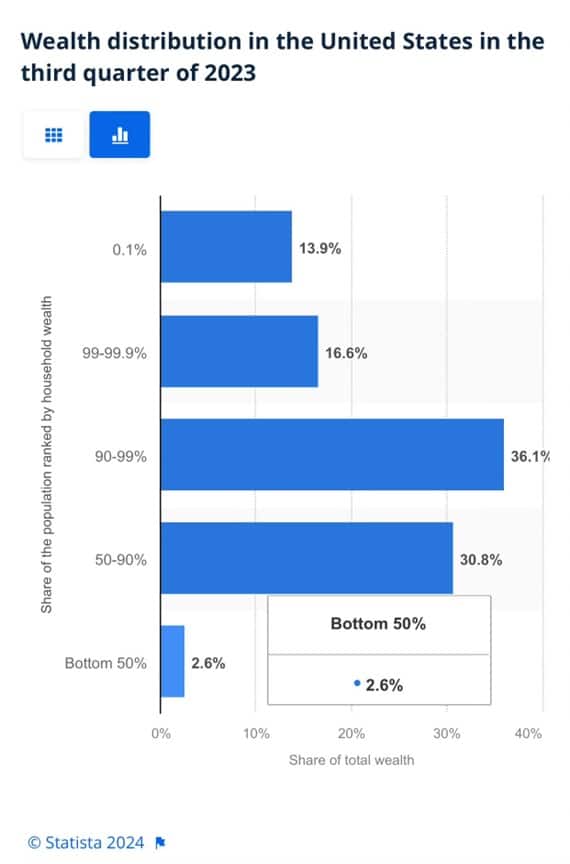

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

{kind=link}

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

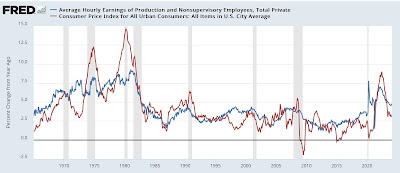

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

The post Bougie Broke The Financial Reality Behind The Facade appeared first on RIA.

recession unemployment pandemic economic recovery stimulus fed recession recovery interest rates unemployment stimulus

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

Aging at AACR Annual Meeting 2024

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges