Uncategorized

Futures Dip After Shock RBA Rate Hike As Fed Meeting Begins

Futures Dip After Shock RBA Rate Hike As Fed Meeting Begins

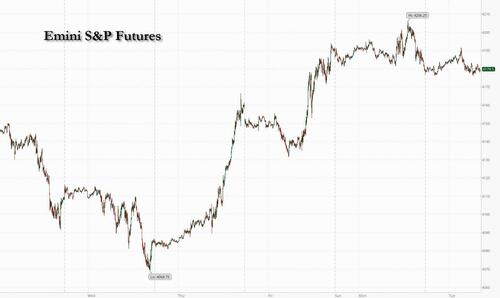

US index futures saw modest declines on Tuesday as investors braced for this week’s…

Share this:

US index futures saw modest declines on Tuesday as investors braced for this week’s Federal Reserve meeting where policymakers are expected to deliver another rate increase, and then pause the hiking cycle. S&P 500 contracts slid 0.1% as of 8:00 a.m. ET after earlier swinging between small gains and losses. Nasdaq 100 futures traded little changed. Both benchmarks closed steady on Monday after data showed that US factory activity contracted for a sixth-straight month in April, the longest such stretch since 2009.

In premarket trading, Chegg fell over 40% after the online education company warned that ChatGPT was threatening growth of its homework-help services. Sprouts Farmers Market gained 8% after the grocer published better-than-expected results and guidance. Uber rallied as much as 11% after the ride-hailing firm reported earnings and revenue that beat analysts’ estimates. Shares of peer Lyft also rose 2.9%. Here are the other notable premarket movers:

- Arista Networks falls as much as 8.8% as analysts said the cloud networking company’s first-quarter results and forecast for the second-quarter were strong, but flagged a lack of visibility for the second half of the year, especially regarding the company’s “cloud titan” customers.

- LendingTree plunges 22% after the firm cut its revenue guidance for the full year, missing the average of analysts’ estimates.

- MGM Resorts dips 1%, set to slip from their highest level in more than a year, after the entertainment resort operator gave an update for the first quarter. Analysts noted that the company flagged a slightly sparser events calendar for its Las Vegas business.

- Oramed gained as much as 2% after US conservative media entrepreneur Ben Shapiro took a stake of more than 4% in the struggling Israeli pharma company and was named to its board.

- Penn Entertainment rises 3.8% after Roth MKM upgrades the casino and gaming company to buy from neutral, anticipating that better-than-expected property margins in the first quarter will prompt investors to reevaluate their 2023 projections.

- Pfizer gains as much as 2.8% after the drugmaker reported revenue for the first quarter that beat the average of analysts’ estimates.

- SoFi Technologies Inc. dips 1.1% after Wedbush downgraded the online lender to neutral from outperform noting that there may be “downside risk to its gain on sale margins and fair value marks of its loan portfolio.”.

- Sprouts Farmers Market jumps as much as 8% after the grocery-store operator’s first-quarter results beat estimates, as did guidance for the second quarter. Analysts are positive on the company’s strategy and margin performance.

- Stag Industrial gains 7% after S&P Dow Jones Indices said that the real estate investment trust will replace Axon Enterprise in the S&P MidCap 400, effective before the market opens on May 4.

Global sentiment was subdued ahead of tomorrow's (final) 25bps rate hike by the Fed, especially after Australia unexpectedly hiked rates showing central banks remain in inflation-fighting mode, and renewing concerns about a deeper US economic slowdown.

JPMorgan strategists predicted stocks would remain under pressure for the rest of the year as monetary tightening cools the economy and earnings weaken after a strong first quarter. Still, a deal on Monday for JPMorgan to acquire the troubled First Republic Bank boosted optimism that the recent banking turmoil “could well be in the rear-view mirror,” said Michael Hewson, chief analyst at CMC Markets in London (narrator: it's not).

“This would be extremely welcome to jittery markets at a time when yields are rising again and recent economic data suggests that central bank may well have to continue to raise rates,” he said.

And while the rescue of First Republic Bank drew a line for now under US banking turbulence, investors now fear lending will be crimped, slowing an economy already under pressure from the most aggressive rate-hike campaign in decades. Euro-zone data reinforced these fears, showing banks had curbed lending more than anticipated.

“The banking crisis appears to have been dealt with, now it’s again all about inflation,” said Fahad Kamal, chief investment officer at SG Kleinwort Hambros Bank Limited. “Markets are wobbly because of the dichotomy between reasonably strong data and weak forward expectations, as there is concern over what may happen to corporate earnings due to the delayed effects of monetary policy.”

Attention now turns to the Fed, whose two-day policy meeting kicks off Tuesday. The central bank is expected to raise rates by a quarter percentage point and potentially signal a willingness to hold off on further increases. Focus is also on policymakers in Washington after Treasury Secretary Janet Yellen said the government might run out of money to pay its bills as early as June. Investors will also watch US JOLTS job openings, factory and durable goods orders today. Earnings will also garner attention, with more than 35 S&P 500 firms slated to report Tuesday, including Starbucks and Uber Technologies. Apple Inc.’s report is due Thursday.

European stocks traded in the red after coming back from Monday's holiday following a busy day of corporate earnings, economic data and central bank policy speculation. The Stoxx 600 is down 0.3% with real estate, energy and media the worst performing sectors. Banks have outperformed, led by HSBC after the UK lender announced a new $2 billion share buyback plan. Here are the biggest European movers:

- HSBC shares rise as much as 6.1% in London, the most since November, after the bank’s quarterly profit topped expectations on better trading revenue, lower costs and fewer provisions

- Persimmon gains as much as 6.5% alongside other UK homebuilders, boosted by a report in The Times that the UK government is working on a new policy to support first-time buyers

- Logitech gains as much as 7.2%, the most since October, after the Swiss manufacturer of computer peripherals beat analyst estimates in quarterly sales for the first time in a year

- Electrolux rises as much as 10% to later pare some gains after Bloomberg reported that China’s Midea Group is exploring a potential acquisition of the Swedish home appliance company

- Kambi shares gain as much as 11%, the most in nearly a year, after the Swedish online betting services firm announced a multi-year sportsbook deal with US gambling firm Bally’s

- BP drops as much as 5.6% after the energy giant slowed the pace of share buybacks after a sharp drop in quarterly profit; while earnings beat estimates, cash flow momentum is likely to weaken

- Pearson falls as much as 7.3% Chegg, an American firm providing online guidance for students preparing tests, saw shares plummeting in US postmarket trading after it warned of AI competition

- Evolution falls as much as 5.4% after the Swedish online gambling firm was downgraded to neutral from buy at Citi, which in note says there is now limited upside scope shares in the coming months

- Ams-OSRAM falls as much as 8.8% after the chipmaker’s 2Q sales forecast missed expectations, with a downturn in the semiconductor industry continuing to hit demand for its products

- Traton falls as much as 2.1%, reversing initial gains, after raised margin guidance from the German truckmaker failed to impress. After strong 1Q performance, “all eyes” are on 2H demand, Citi says

Earlier in the session, Asian stocks were little changed, with investors digesting a slew of economic data from China for clues on the strength of the nation’s recovery, as most of the region’s markets resumed trading after a holiday. The MSCI Asia Pacific Index swung in a narrow range, with declines in industrials and consumer staples moderating gains in utilities stocks. Hong Kong equities also fluctuated, while key gauges rose in South Korea and were mixed in Japan. The Hang Seng China Enterprises Index wiped out an early gain of 2.1% as traders assessed China’s shrinking manufacturing activity. The official manufacturing purchasing managers’ index unexpectedly fell to 49.2 in April from 51.9 in March. Mainland markets are shut through Wednesday.

“Data brought back risks that China’s recovery is losing steam, and built the case for further policy support,” Saxo Capital Markets strategists wrote in a note. On the other hand, “travel demand during the Golden Week has started on a positive note,” they said. Investors also awaited the Federal Reserve’s rate decision scheduled for Wednesday. The US central bank is widely expected to hike interest rates again.

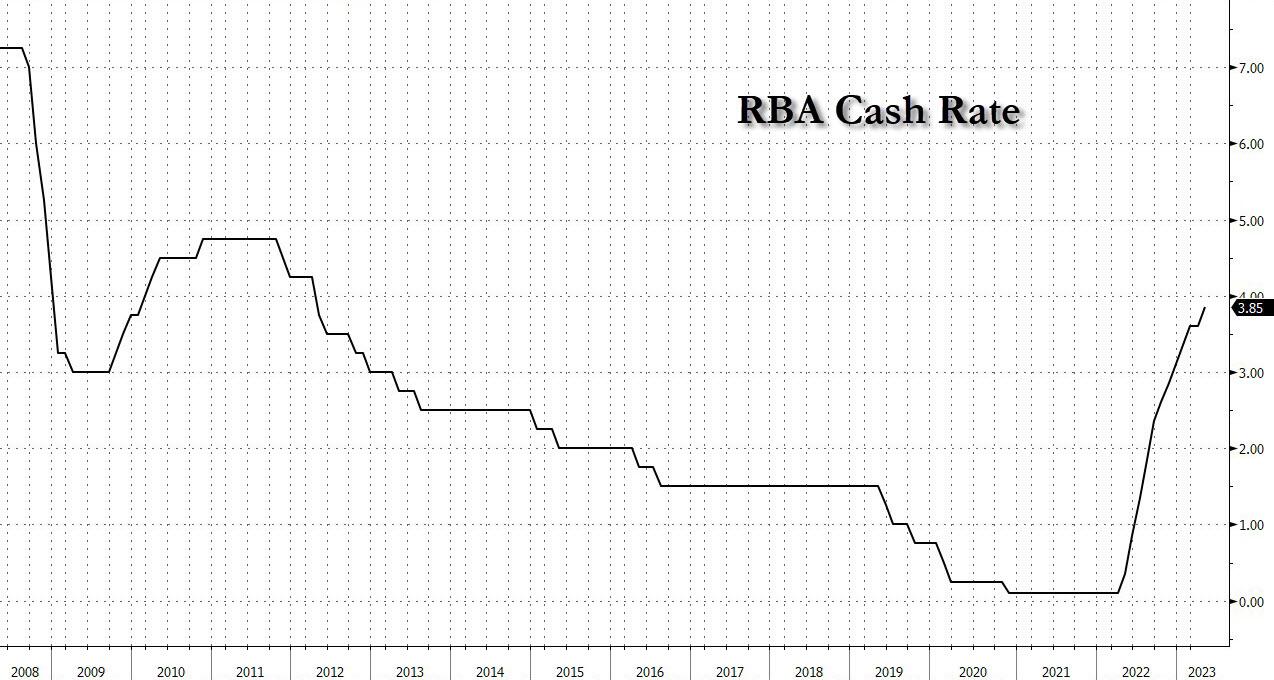

Australian stocks fell after the country’s central bank unexpectedly raised interest rates by a quarter-percentage point and signaled further policy tightening ahead. The S&P/ASX 200 index fell 0.9% to close at 7,267.40; the Aussie and bond yields surged. “A potential higher terminal rate is a risk and negative for equities,” said Matthew Haupt, a fund manager at Wilson Asset Management in Sydney. “It’s becoming a credibility issue now, these shocks to markets, and we need to add discount due to policy uncertainty,” he said. Read: RBA Shock Hike Spurs Strategist Clash About Global Rate Bets In New Zealand, the S&P/NZX 50 index rose 0.3% to 12,037.81.

Japanese stocks ended mixed in thin trading as investors geared up for a US rate decision and a domestic holiday this week. The Topix Index fell 0.1% to end at 2,075.53, while the Nikkei advanced 0.1% to 29,157.95. Toyota Motor Corp. contributed the most to the Topix Index’s decline, decreasing 0.5%. Out of 2,160 stocks in the index, 768 rose and 1,257 fell, while 135 were unchanged. “Although the yen has weakened after the BOJ decision and interest rates have fallen, making it easier to take risks,” the holiday-shortened week and the upcoming FOMC meeting make it hard to take a position, said Hiroshi Matsumoto, a senior client portfolio manager at Pictet Asset Management. Japan’s financial markets will be closed Wednesday through Friday for holidays.

India’s benchmark stocks gauge gained for the eighth straight session, supported by foreign buying while banks led earnings outperformance. The S&P BSE Sensex rose 0.4% to 61,354.71 in Mumbai on Tuesday, its highest close since Dec. 20, while the NSE Nifty 50 Index advanced 0.5%. The Sensex is now trading at 14-day RSI of 71, a level that some traders see as overbought, for the first time since it peaked all-time high in early December. However, India VIX Index - a measure of volatility expectations - continues to trade near its lowest level in three years. Banks in India, including top lenders such as HDFC Bank and Kotak Mahindra have reported strong earnings for the March quarter amid sustained loan growth. Out of 21 Nifty companies, which have so far reported earnings, 11 have matched or exceeded average analyst expectations, while eight have trailed. Two companies didn’t have comparable estimates. Tata Steel will be releasing its numbers later Tuesday. Infosys contributed the most to the Sensex’s gain, increasing 2%. Out of 30 shares in the Sensex index, 16 rose, while 14 fell.

In FX, the Bloomberg Dollar Spot Index is up 0.1% while the Australian dollar was the clear outperformer among the G-10s, jumping with local yields after the Reserve Bank unexpectedly resumed policy tightening. AUD/USA climbed as much as 1.3% to 0.6717 while Australia’s 3-year yield rose as much as 25bps to 3.26%, the highest since March. The RBA lifted the cash rate by 25 basis points to 3.85% while economists expected the rate to be left unchanged after data last week showed growth in consumer prices slowed more than expected in the first quarter. “The RBA is clearly still focused on inflation and feels it is still too high,” said Nick Twidale, chief executive Asia Pacific at FP Markets. “You’ve got to look to get long Aussie for the short to medium term, and it’s much more preferable to do it on the crosses than the dollar because we have so much uncertainty coming up with the Federal Reserve”

In rates, treasuries were richer across the curve, paring a portion of Monday’s sharp rate-lock driven selloff (courtesy of FB's massive $8.5 billion new bond offering) as stock futures extended a retreat from Monday’s highs. During Asia session the Reserve Bank of Australia hiked its benchmark rate by 25bp to 3.85%, saying inflation remained too high and further tightening may be required. US yields are richer by 1bp to 4bp across the curve with gains led by intermediates, tightening the 2s5s30s fly by 3bp on the day; 10-year yields around 3.53%, lower by 4bps vs Monday’s close. Bund futures gapped lower but have pared some of that drop after the ECB bank lending survey and euro-area CPI data supported the view that the central bank will slow the pace of rate hikes this week. German 10-year yields are still up 5bps on the day. US session features 10am data raft including JOLTS job openings — which sparked gains last month — and factory orders.

In commodities, crude futures decline with WTI falling 0.4% to trade near $75.40. Spot gold is flat around $1,981.

Bitcoin is modestly firmer though is yet to convincingly extend above the USD 28k mark and as such remains well within the parameters of recent action.

Now looking at the day ahead, in the US we will get the March JOLTS report, factory orders, and April total vehicle sales. Meanwhile in Europe the main datapoints are the UK April Nationwide house price index, German March retail sales, and a bevy of Italian releases including April CPI, budget balance, new car registrations, manufacturing PMI, and March PPI. Additionally, this morning we will learn the Eurozone April CPI and March M3 level. In terms of central banks, we will get the important Eurozone bank lending survey. On earnings we will hear from Pfizer, HSBC, AMD, Starbucks, BP, Uber, Marriott, and Ford amongst others.

Market Snapshot

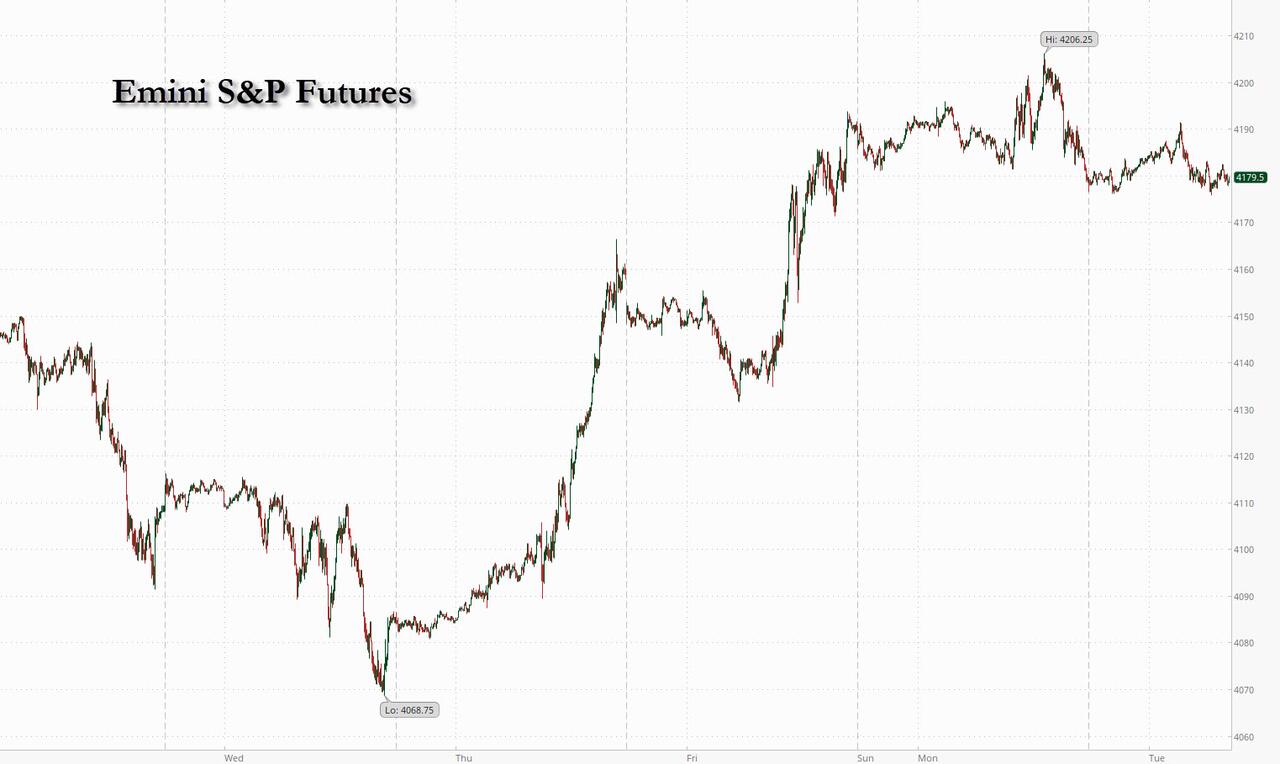

- S&P 500 futures down 0.1% to 4,180.00

- MXAP little changed at 160.56

- MXAPJ little changed at 515.64

- Nikkei up 0.1% to 29,157.95

- Topix down 0.1% to 2,075.53

- Hang Seng Index up 0.2% to 19,933.81

- Shanghai Composite up 1.1% to 3,323.28

- Sensex up 0.5% to 61,424.73

- Australia S&P/ASX 200 down 0.9% to 7,267.40

- Kospi up 0.9% to 2,524.39

- STOXX Europe 600 down 0.3% to 465.62

- German 10Y yield little changed at 2.34%

- Euro little changed at $1.0972

- Brent Futures down 0.4% to $79.03/bbl

- Gold spot down 0.1% to $1,981.44

- U.S. Dollar Index little changed at 102.16

Top Overnight News

- Australia’s RBA catches markets off guard with a surprise 25bp rate hike to 3.85% (most assumed they would stay on hold for an extended period) as the central bank warns that further increases may be required as inflation is still too elevated. RTRS

- Europe’s CPI for April ran hot at +7% on the headline (up from +6.9% in Mar and higher than the Street’s +6.9% forecast) while core ticked down only slightly (+5.6%, inline with the Street but off just fractionally from +5.7% in March). BBG

- ECB’s latest bank lending survey reveals a “further substantial tightening in credit standards for loans to firms and for house purchases” (“pace of net tightening in credit standards remained at the highest level since the euro area sovereign debt crisis in 2011”) while “demand for loans decreased strongly”. ECB

- BlackRock will begin selling failed banks’ municipal securities today, starting with an auction of about $50 million of taxable bonds, according to people familiar with the matter. BBG

- The FDIC said in its report that switching to a “targeted coverage” approach, where business accounts get more coverage than the current cap, would be the best option for financial stability. Such a change, however, would require congressional action. Other options include maintaining coverage as is, or switching to cover all deposits, the FDIC said. BBG

- Morgan Stanley may axe about 3,000 jobs this quarter, people familiar said, roughly 5% of its workforce, excluding advisers and people supporting them in the wealth management business. The banking and trading group is expected to be hit hard. In other banking woes, hundreds of Credit Suisse AT1 bondholders sued the Swiss regulator over their $1.7 billion loss. BBG

- Janet Yellen warned the Treasury may run out of cash at the start of June and Joe Biden invited lawmakers to a May 9 meeting to discuss raising the debt ceiling. The market is unsure about the timing. T-bill yields rose yesterday and pricing shows growing concern about a default in June. But the highest yields are in late July and August, with rates now above 5%. BBG

- Investors warn of First Republic aftershocks. Attendees at Milken financial conference fear credit crunch and sharper slowdown after banking turmoil. “There is a little bit of a tendency to kind of breathe a sigh of relief on mornings like this,” David Hunt, chief executive of $1.2tn asset manager PGIM, told Milken attendees digesting the First Republic rescue. “Actually, we’re just starting the implications for the US economy.” FT

- JPMorgan was the only bank with the appetite to buy substantially all of First Republic at a competitive price, including mortgages that other banks didn’t want. That was a priority for the FDIC because it removed uncertainty over any assets left behind that it would have to sell. WSJ

- Chegg Inc. plummeted 42% after warning that the ChatGPT tool is threatening growth of its homework-help services, one of the most notable market reactions yet to signs that generative AI is upending industries.

- Banks in the euro zone curbed lending more than anticipated after borrowing costs jumped and turmoil gripped the financial sector, reinforcing calls for the European Central Bank to slow the pace of its interest-rate hikes.

- HSBC shares rose after the Asia- focused lender announced a fresh plan to return money to shareholders after reporting first-quarter results that beat estimates.

- Morgan Stanley is preparing a fresh round of job cuts amid a renewed focus on expenses as recession fears delay a rebound in dealmaking.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded with a slight positive bias as many of the regional participants returned to the market from the long weekend albeit with gains capped ahead of this week's upcoming risk events. ASX 200 was pressured after the RBA surprised markets with a 25bps rate increase, while the central bank's language remained hawkish with the Board expecting some further tightening of monetary policy will be needed. Nikkei 225 was indecisive and pulled back after briefly touching its highest level since January last year. Hang Seng initially surged on reopening from the holiday weekend and was led higher by strength in tech and casino stocks with the latter buoyed after a jump in Macau gaming revenue, although the index later faded most of its gains while the mainland remained shut for golden week.

Top Asian News

- Japanese, South Korean and Chinese finance ministers and central bank governors said they recognise the importance of strengthening economic and trade relations, while they fully support the implementation of the Regional Comprehensive Economic Partnership agreement. However, they also noted that despite close economic relations, they have observed a recent slowdown in economic relations, according to Reuters.

- US President Biden and Philippines President Marcos affirmed the importance of maintaining peace and stability across the Taiwan Strait, while President Biden confirmed the US will send a presidential trade and investment mission to the Philippines, according to Reuters.

- RBA unexpectedly hiked the Cash Rate Target by 25bps to 3.85% (exp. pause), while it stated that the Board expects some further tightening of monetary policy will be needed and remains resolute in its determination to return inflation to target and will do what is necessary to achieve that. RBA stated that inflation in Australia has passed its peak, but at 7% is still too high and it will be some time yet before it is back in the target range. Furthermore, it stated some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but will depend upon how the economy and inflation evolve.

European stocks mostly decline after a long weekend, Euro Stoxx 50 -0.2%, with traders keeping an eye on various upcoming risk events; US equity futures hold a downward bias, ES -0.1%. In earnings, HSBC +4.5% beat expectations while BP -4.5% missed on revenue and guided towards lower Q2 refining margins. Stateside, futures are modestly softer but have picked up off lows as the European session progresses with the focus remaining firmly on the Fed, debt ceiling and earnings.

Top European News

- ECB bank lending survey - Q1 2023; net 27% of EZ banks reported tightening of lending standards for companies, 38% reported fall in demand for credit from companies. Banks indicated that their credit standards for loans or credit lines to enterprises tightened further substantially in the first quarter of 2023. Firms’ net demand for loans fell strongly in the first quarter of 2023. The decline in net demand was stronger than expected by banks in the previous quarter and the strongest since the global financial crisis.. Click here for more detail & newsquawk analysis.

- UK Foreign Secretary Cleverly says a meeting with China's Vice President Han Zheng is likely.

- Ukraine Latest: Russia Seen Buying Foreign Currency Reserves

- European Stocks Slip Amid Earnings, Data Before Rates Decisions

- HSBC Shares Rise After Lender Announces $2 Billion Share Buyback

- Vitol Says EU Gas Market to Stay Tight Until 2026 Supply Boost

FX

- Aussie outperforms as RBA hikes and delivers hawkish guidance against expectations for another pause, AUD/USD probes 0.6700 and the top end of 1.5 bn expiry options, AUD/NZD back above 1.0800 even though NZD/USD hovers just shy of 0.6200 ahead of jobs data.

- DXY pivots 102.000 awaiting US factory orders and JOLTS job openings.

- Euro fades from 1.1000+ vs Buck amidst decent expiries and as the ECB lending survey reveals substantially tighter credit conditions.

- Pound fails to retain 1.2500 handle against Dollar despite an upwardly revised final UK manufacturing PMI.

Fixed Income

- US Treasuries bounce from post-manufacturing ISM lows as attention turns to factory orders and JOLTs, T-note nearer upper end of 114-28+/114-15 band after decent block purchase at 114-24

- Bunds and Gilts remain weak in corrective trade after the long weekend, but off worst levels between 134.35-135.34 and 100.37-101.18 respective ranges

- EZ debt takes note of ECB BLS showing tighter credit standards, but UK bonds largely shrug off the upgrade to final manufacturing PMI.

- For reference, the morning's ECB Bank Lending Survey saw a modest dovish adjustment to market pricing while the subsequent Flash HICP figures sparked little sustained reaction

Commodities

- WTI and Brent futures see choppy trade amid a cautious market environment, whilst BP anticipates elevated oil prices due to OPEC+ production restrictions, strengthening Chinese demand, and tight supply/demand balances.

- Metals trade mixed, with spot gold lower in a tight range, and base metals initially gaining but now showing mixed performance as the DXY gains ground.

Geopolitics

- Japan scrambled a jet fighter following a suspected Chinese drone spotted between Yonaguni island and Taiwan on Tuesday, according to the Japanese Defence Ministry.

- Russian Defence Ministry says steps have been taken to speed up weapons production, via Tass.

US Event Calendar

- April Wards Total Vehicle Sales, est. 15.1m, prior 14.8m

- 10:00: March Factory Orders, est. 1.2%, prior -0.7%

- 10:00: March Factory Orders Ex Trans, prior -0.3%

- 10:00: March Durable Goods Orders, est. 3.2%, prior 3.2%

- 10:00: March -Less Transportation, est. 0.3%, prior 0.3%

- 10:00: March Cap Goods Ship Nondef Ex Air, prior -0.4%

- 10:00: March Cap Goods Orders Nondef Ex Air, est. -0.4%, prior -0.4%

- 10:00: March JOLTs Job Openings, est. 9.74m, prior 9.93m

DB's Jim Reid concludes the overnight wrap

So welcome to a belated start to May in Europe after a surprisingly dull April. Indeed it’s quite ironic that a month which culminated in the second largest US bank failure in history was also the least volatile for global assets since the pre-pandemic days by at least one measure. In less than 2 months, SVB’s place as the second largest US bank failure was eclipsed yesterday as First Republic Bank was seized by the FDIC. Shortly thereafter a deal was brokered for JPM to buy the embattled regional lender. However, at the same time we’ve just closed an April where in our monthly performance review only 5 out of 38 assets in our study moved by more than 3% in either direction for the first time since pre-pandemic days and the VIX fell back to November 2021 levels mid-month. See Henry’s monthly performance review here for more on this.

Even with the FRC situation resolved (see more below), this week’s FOMC meeting – which concludes on Wednesday – will likely include continued discussion of the banking system going forward. However the details of that discussion may not be revealed until the minutes are released later this month. The main focus of the Fed tomorrow will be on whether they give any hints of forward guidance at all. Our base case is that the FOMC will maintain a hawkish bias and signal that a June hike is on the table, but with no pre-commitment to act on it. One important note will be how much Fed Chair Powell previews the very important Senior Loan Officer Survey that comes out next week. The Chair will be aware of the results. See our economists’ preview of the FOMC here.

The also very important European bank lending survey comes out this morning so that will play a part in Thursday’s ECB decision where our economists expect +25bps but with finely balanced risks versus a +50bps hike. In terms of the ECB hiking, the market sees it as a bit more clear cut as it prices in just over a 25bps hike (+28bps) and 50bps of hikes by the June meeting. We get the Eurozone CPI print today which may also have an influence, but the regional prints last week didn’t suggest any big hawkish surprises. The median Bloomberg estimate is a +0.7% m/m increase, after a 0.9% rise in March. See our economists’ preview of the ECB meeting here.

When that central bank excitement is over, attention will turn to another payrolls’ Friday. DB expects +150k with consensus at +180k and +236k last month. JOLTS today is arguably a better gauge of US labour market tightness but is always a month behind. Claims (Thursday) is one to watch given the recent flirtation with 18-month highs even if we’re still at historically low levels. Another notable piece of US data will come from productivity numbers on Thursday, as inflationary and wage pressures remain strong. Our economists expect +0.6% growth in productivity (v +1.7% in Q4) and a +3.4% reading for unit labour costs, an increase from +3.2% in Q4.

Additionally, the ISM services tomorrow is important following the marginal upside surprise in manufacturing yesterday. Our US economists expect a 52.1 reading for services tomorrow (51.2 last month). The US April ISM manufacturing reading yesterday was stronger than expected while remaining contractionary, coming in at 47.1 (46.8 expected). That was up 0.8pts from last month’s cycle lows, and is on the back of higher prices paid (53.2 vs 49.2 last month), higher new orders (45.7 vs 44.3 last month), and stronger employment. The employment portion of the survey rebounded into expansionary territory – albeit just at 50.2 – after being down at 46.9 in March. Elsewhere, US construction spending in March rose 0.3% m/m (0.1% expected).

Moving on to earnings, the key highlights of the week will continue to be tech earnings, including Apple on Thursday. The company will round out what has been a string of above-expectation results from the rest of the big tech pack last week. These boosted American large cap indices while small caps have struggled a bit more of late. The key earnings and data releases are in the day-by-day calendar at the end.

Now to a US session yesterday where virtually all of Europe was on holiday. The main story of the day, as referenced above, was First Republic officially being seized by regulators on Monday morning and then sold to JPMorgan. This followed speculation of assets sales last week as well as reports of multiple bidding banks materialising over the weekend. JPMorgan will now have acquired the two largest US bank failures of all-time, having acquired Washington Mutual back in 2008. JPM’s stock gained +2.14% yesterday, and was one of only 2 members in the KBW index (-1.78%) to finish higher on the day. The two worst performing stocks in the index were Citizens Financial (-6.85%) and PNC (-6.33%) who were among the known bidders for First Republic.

The weakness in overall bank shares followed news that the FDIC wanted to overhaul the deposit insurance system, citing new technological challenges and high concentrations of uninsured depositors in specific “pockets” of the banking system. The plan would see business accounts treated separately and have a higher coverage cap than individuals. This would require congressional approval. Questions still remain on how the Deposit Insurance Fund will be replenished and who should foot that bill, and so there is likely to be more response from the government in the coming weeks and months amid discussions of the impending debt ceiling deadline.

Outside of the First Republic news, the US equity session was fairly quiet with attention on the busy upcoming macro calendar. The S&P 500 traded in a 0.5% range and finished just -0.04% lower on the day with a good deal of dispersion under the surface. Exactly half of the 24 GICS level 2 industry groups in the index were higher on the day with little discernible factor bias as growth industries like biotech (+0.85%) and semiconductors (+1.52%) did well as did cyclicals such as transports (+1.50%). However some of the worst performers were also cyclicals such as energy (-1.26%), consumer retail (-1.93%), and autos (-0.98%).

With the First Republic deal taking a slice out of the overall risk premium built into markets, as well as pre-positioning ahead of the FOMC there was a big selloff in rates. This came despite a risk-on tone and was also potentially aided by a large day of corporate issuance in the US, as corporate blackout periods have concluded for some of the bigger issuers. Overall, 10yr US Treasury yields were +14.6bps higher at 3.56%, with 2yr yields +13.4bps higher at 4.14%. Fed futures are pricing in a near certainty of a hike in 2 days (95%) and a 1-in-5 chance of an additional hike in June, before 50bps of cuts come through by year-end.

There was a bit of a rally in treasuries in the last hour or so of trading following US Treasury Secretary Yellen telling US lawmakers that the US could hit the debt ceiling as early as June 1. 10yr yields came in about 3bps following the announcement. Markets are still pricing more risk later into the summer but the White House took a step toward coming to a resolution with Republicans in the House yesterday. President Biden has invited congressional leaders from both parties to the White House on May 9.

In Asia, as we go to print the RBA have surprised the market by hiking +25bps after many expected a continued pause. The surprise is reflected in 3yr yields rising +22bps after the decision. At this stage it looks like a hawkish hike. In terms of equities in the region the Nikkei 225 is trading largely flat, up a modest +0.06% ahead of the Japanese public holidays for the rest of the week. The Hang Seng is up +0.12%, and set to secure a fourth consecutive day of gains after Hong Kong GDP for Q1 grew 2.7% year-on-year (vs 0.5% expected). Onshore Chinese markets are closed and are set to reopen on Thursday after a four-day public holiday that started on Monday, whilst the Korean Kospi relatively outperformed up +0.62%. US equity futures are pretty flat along with Treasury yields.

Now looking at the day ahead, in the US we will get the March JOLTS report, factory orders, and April total vehicle sales. Meanwhile in Europe the main datapoints are the UK April Nationwide house price index, German March retail sales, and a bevy of Italian releases including April CPI, budget balance, new car registrations, manufacturing PMI, and March PPI. Additionally, this morning we will learn the Eurozone April CPI and March M3 level. In terms of central banks, we will get the important Eurozone bank lending survey. On earnings we will hear from Pfizer, HSBC, AMD, Starbucks, BP, Uber, Marriott, and Ford amongst others.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire