Uncategorized

Four Banking Stocks That Aren’t Getting Crushed Amid Financial Sector Volatility

U.S. banks have been navigating a minefield of tumultuous conditions throughout much of the year, leading to a greater concern … Read more

Share this:

U.S. banks have been navigating a minefield of tumultuous conditions throughout much of the year, leading to a greater concern regarding the overall well-being of the American banking sector.

Investors have shrugged their attention away from JPMorgan Chase’s (NYSE:JPM) rescue efforts of First Republic Bank (OTCMKTS:FRCB), after the bank announced that it would buy out the disgruntled regional bank for $10.6 billion in a statement during the first week of May 2023.

This comes at a crucial time, as Wall Street analysts are begging to understand where the American banking sector may be heading following the collapse of Silicon Valley Bank (OTCMKTS:SIVBQ) in March this year, which narrowly caused an air of concern among depositors after the news broke headlines.

Regional Lenders Are Struggling

While JPMorgan’s efforts didn’t herald the end of a possible banking crisis, investors are gearing their focus towards smaller regional lenders that have seen shares plummeting in recent weeks.

Given the current economic uncertainty, shares of the California-based lender, Pacific Western Bank (NASDAQ:PACW) or PacWest, have shed more than 70% since the start of the year. Despite the negativity, PacWest CEO Paul Taylor has reassured investors that the bank’s business structure has until thus far remained “fundamentally sound.”

Other regional lenders, including First Horizon (NYSE:FHN) and TD Bank (NYSE:TD), have in recent weeks also called off a $13 billion deal, which would have merged to become America’s sixth-largest bank. First Horizon has lost close to 40% of its share value since the start of May.

Tough economic conditions have put Wall Street on high alert, as bank shares have struggled to shake off pandemic-era declines. The KBW Bank Index, which tracks leading American lenders, has declined 26% this year already, with a near 6% decline between May 1 and May 9.

Taking into consideration broader economic headwinds, investors are still recuperating from the Federal Reserve’s aggressive monetary tightening, after the central bank raised its base interest rate for the tenth consecutive time by 25 basis points on May 3, 2023.

While it looks as if the Fed could hold off on their monetary cycle, for now at least, after the Bureau of Labor Statistics reported cooler-than-expected inflation data for April, with prices rising 4.9%, compared to Wall Street estimates of 5%, other challenges caused by the U.S. fast-approaching deadline to raise the debt ceiling could pose yet another hurdle.

Banking Stocks That Remain Uncrushed

There is however a slight sense of positivity for investors looking to climb into the American banking and finance sector. Yet, it’s undeniable that major risks associated with the banking sector such as cyclicality, loan losses, and interest rate risks, remain among the biggest concerns for investors right now.

For those investors that do however consider taking up their position of investing in some of America’s biggest lenders, the risks associated remain staggeringly high.

However, investing in banks is a committed long-term option, although some analysts claim that the coming months could see banking stocks rally as they shrug off the recent economic turmoil. Even with stocks sliding across the board, some big-bank names continue to hold their steam as investors and economists hold their breath for a potential soft landing.

JPMorgan Chase

Although conditions have not been the most promising for even America’s biggest lenders this year, JPMorgan Chase holds a steady performance, with six out of 13 analysts recommending JPM as a Strong Buy and four recommending it as a Buy.

Furthermore, the bank has forecasted an annual revenue growth rate of 3.55%, outpacing the U.S. Banks Diversified average revenue growth rate of 3.02%. Still, the bank will be unable to beat the overall U.S. Market average forecast revenue growth rate of 8.79%.

JPMorgan now holds more than $3 trillion in combined assets, and although its balance sheet has been rocked by tough economic headwinds, overall stock performance has held out relatively well considering how things have unfolded over the last several months.

So far, year-to-date (YTD) growth has been mild at 0.95%, and shares have gained a mediocre 6.6% between April and May. The bank is expected to make $12 billion in stock buybacks this year, which could in the near-term help boost its earnings per share (EPS).

Fifth Third Bancorp

Among regional banks, Fifth Third Bancorp (NASDAQ:FITB) has remained a stalwart on the back of the bankrupt Silicon Valley Bank, which helped accelerate its growth, both in its earnings and share performance after the news broke.

Although FITB nosedived at the collapse of SVB, along with other major names such as JPMorgan and Bank of America, it proved to remain buoyant with access to $102 billion in liquidity sources.

During the first week of May, FITB managed to regain 4.45% of its share price, after sliding 2.20% during April. While volatility remains high, and investors share skepticism over the bank’s overall well-being amid a looming banking crisis and ongoing recession talk, Fifth Third helped shed more color on its conditions following its Q1 2023 earnings report.

Both its consumer and commercial deposit segment remains relatively healthy, with the bank reporting a 71% of retail stable per liquidity coverage ratio (LCR). Even more, the bank claimed that nearly 88% of its deposits are FDIC insured, and the bank has limited exposure to other liabilities such as commercial real estate.

The bank features a mix of consumer customers, with 69% of them being digitally active, Their seemingly progressive banking sales incentives programs have managed to pay off, with more than 80% current balances being primarily from customers that have been with the bank for more than five years.

There’s nothing special to mention about FITB, and while share performance has been all over the board since the start of the year, being stagnant in volatile conditions can sometimes be a good thing as well.

Wells Fargo

Another American heavyweight is Wells Fargo (NYSE:WFC), which currently holds an average brokerage recommendation (ABR) of 1.90, this is on a 1 to 5 scale, on a Strong Buy to Strong Sell scale. Based on brokerage and analysts’ recommendations, Wells Fargo holds a steady position amid volatility in the wider banking sector.

WFC earnings prospects have remained largely unchanged, and this could be an indication for the stock to perform in line with the broader market in the near term.

During the height of the SVB collapse, WFC fell sharply by 17%, but over the long-term stretch of YTD performance, stocks are down close to 8%, still relatively lower than what many expected.

Over the past month or so, investors have yet again seen growing potential in WFC, as the stock has steadily climbed by 0.52%, closely approaching its peak in May 2023 of $40.39 per share.

Furthermore, its balance sheet sees positive improvement, with the bank reporting a 5% increase in year-over-year revenue ending March 2023. Total net income is also up by 31% for the same recorded period.

There’s a good chance that WFC could see slight fluctuations in the coming months, but the bank’s diverse loan book, which holds a steady amount of loan advance to consumers and commercial players, has ensured investors that it remains a buoyant banking heavyweight.

Citizens Financial Group

The turmoil and self-off of First Republic to JPMorgan have meant meager tumult for Citizen Financial Group (NYSE:CFG), yet in an earlier Argu analysis in April, analysts held CFG at a Buy, with a price target of $47.00 per share, slightly down from its previous price target of $52.00 per share.

Even before this rating by Argus, the bank has marked 13 buy ratings and six hold ratings and only has one sell rating.

On the financial side of things, both revenue and net income have improved year-over-year, seeing steady increases of 19.37% and 21.67%, respectively for the period ending March 2023. The company has also boosted its assets by 22%, marking $222 billion in assets for the same recorded period.

The Providence, Rhode Island-headquartered bank did, however, see its number of regional deposits dip between December 31, 2022, and March 31, 2022, which fell by $8.5 billion during this period.

Although Citizens First isn’t the only bank that recorded a decline in deposits, U.S. Bancorp noticed a decline of $20 billion in deposits during the same recorded period.

While there is still a lot of uncertainty looming overhead, coming to terms with that CFG could be a sink or swim scenario in the near term could help investors solidify their position with Citizens First.

What’s The Verdict?

While there are a lot of risks currently bubbling at the surface, it’s hard to give a definitive answer on whether or not the banking sector is a good place for investors to park their cash. There’s still too much uncertainty looming overhead, and despite other economic indicators showing improvement, the banking sector remains roiled with volatility.

Ultimately, investing in big banks could be the stalemate that investors need to expose themselves to different segments of the market, yet this should be done through extreme caution and consideration.

Taking into account the events of the last few months, there’s both certainty and uncertainty that makes up the census of whether banking stocks are the right pick right now.

Bear in mind, that however, conditions may swing, bank stocks remain a long-term investing option, and investors should consider their options against broader economic conditions while navigating their options against the backdrop of historic performance data, and how well these banks can hold out against wider market and economic declines.

recession pandemic nasdaq stocks fed federal reserve real estate recessionUncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

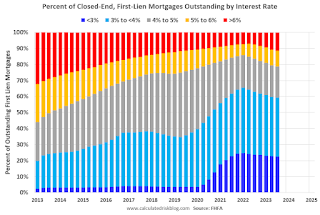

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Uncategorized

‘Bougie Broke’ – The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming…

Share this:

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

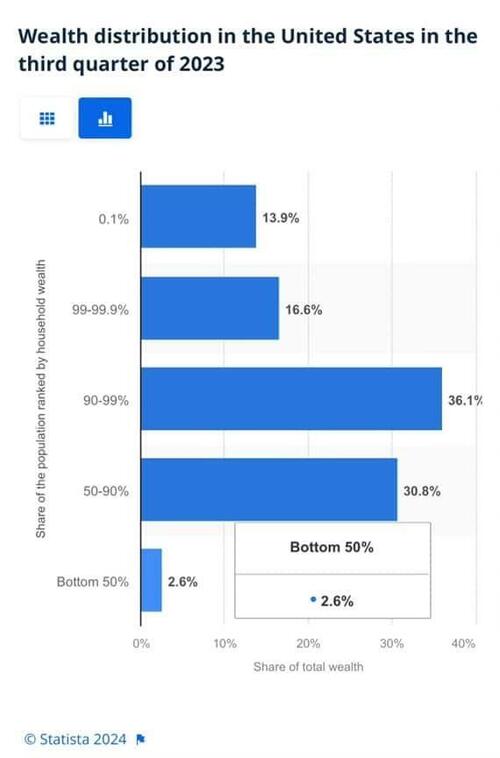

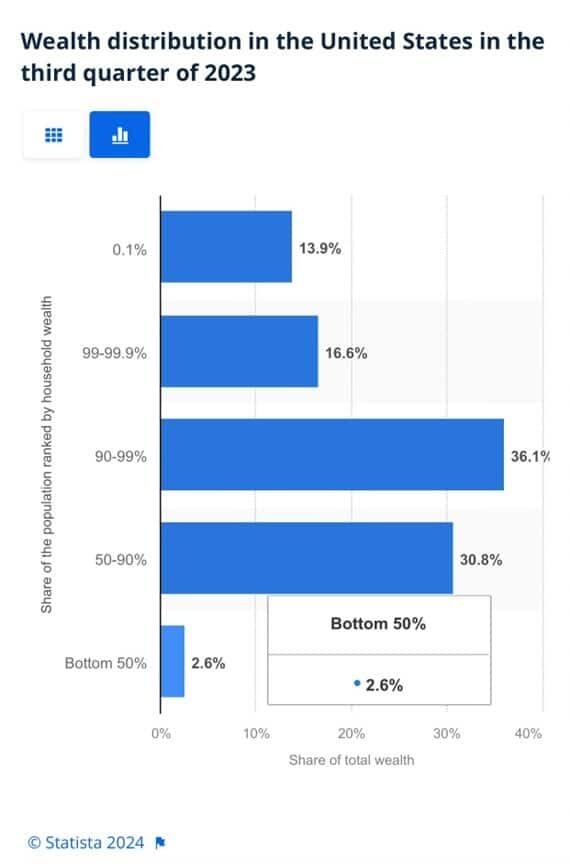

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

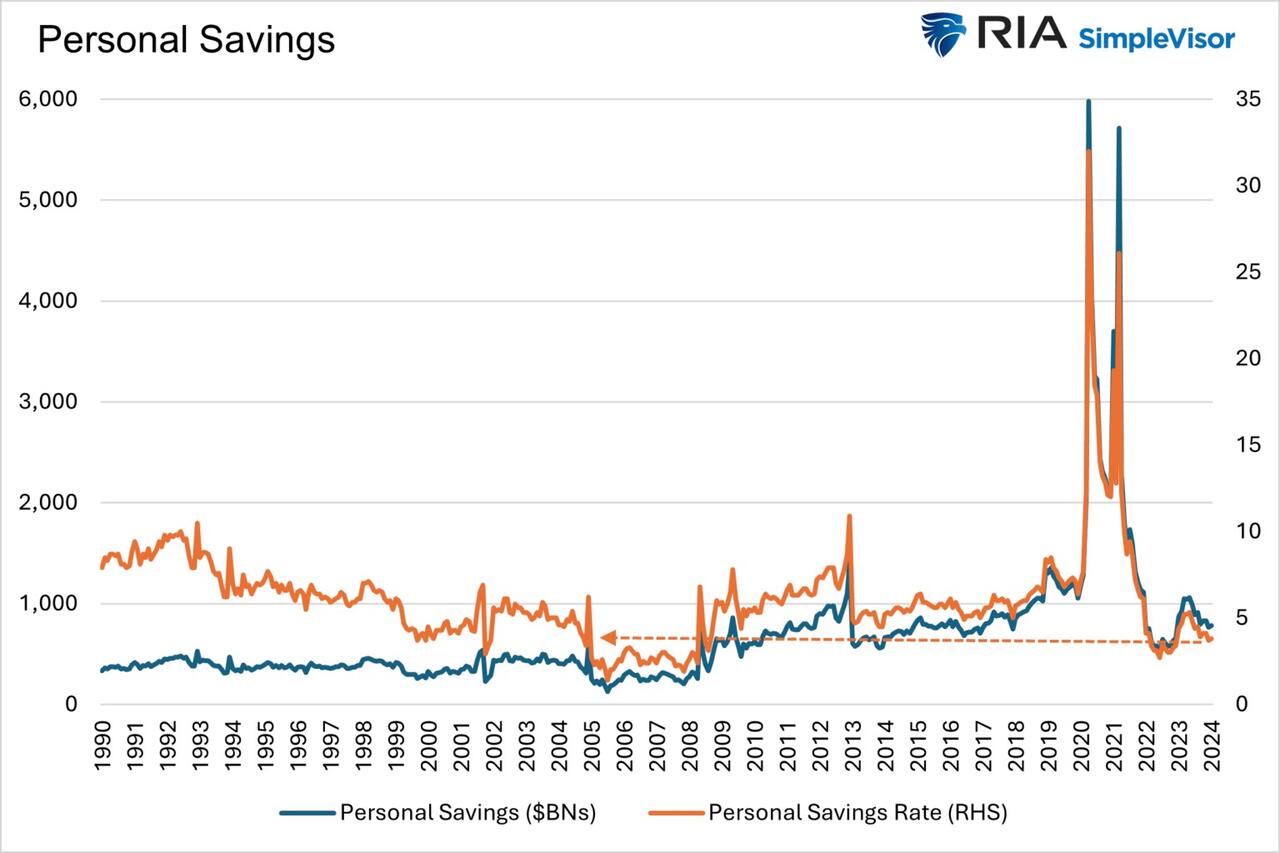

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

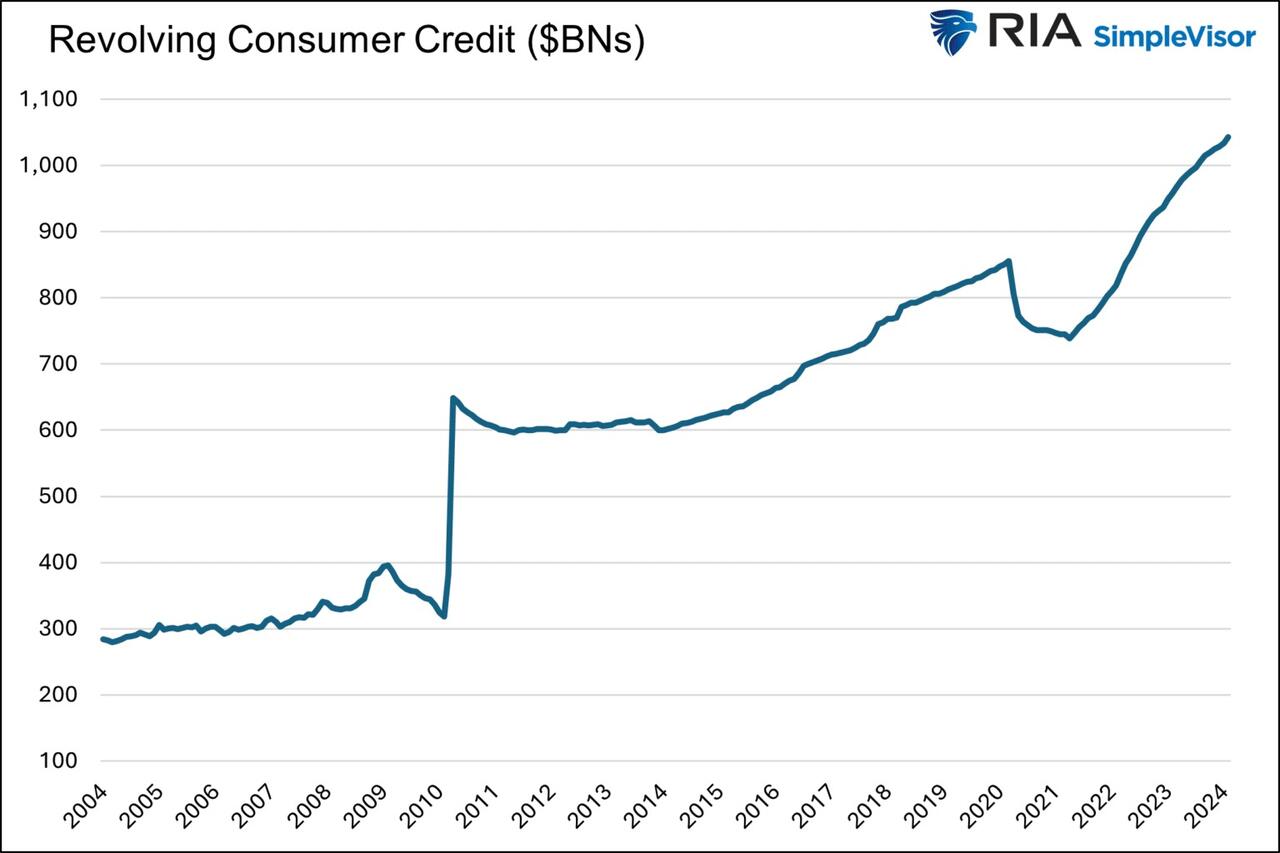

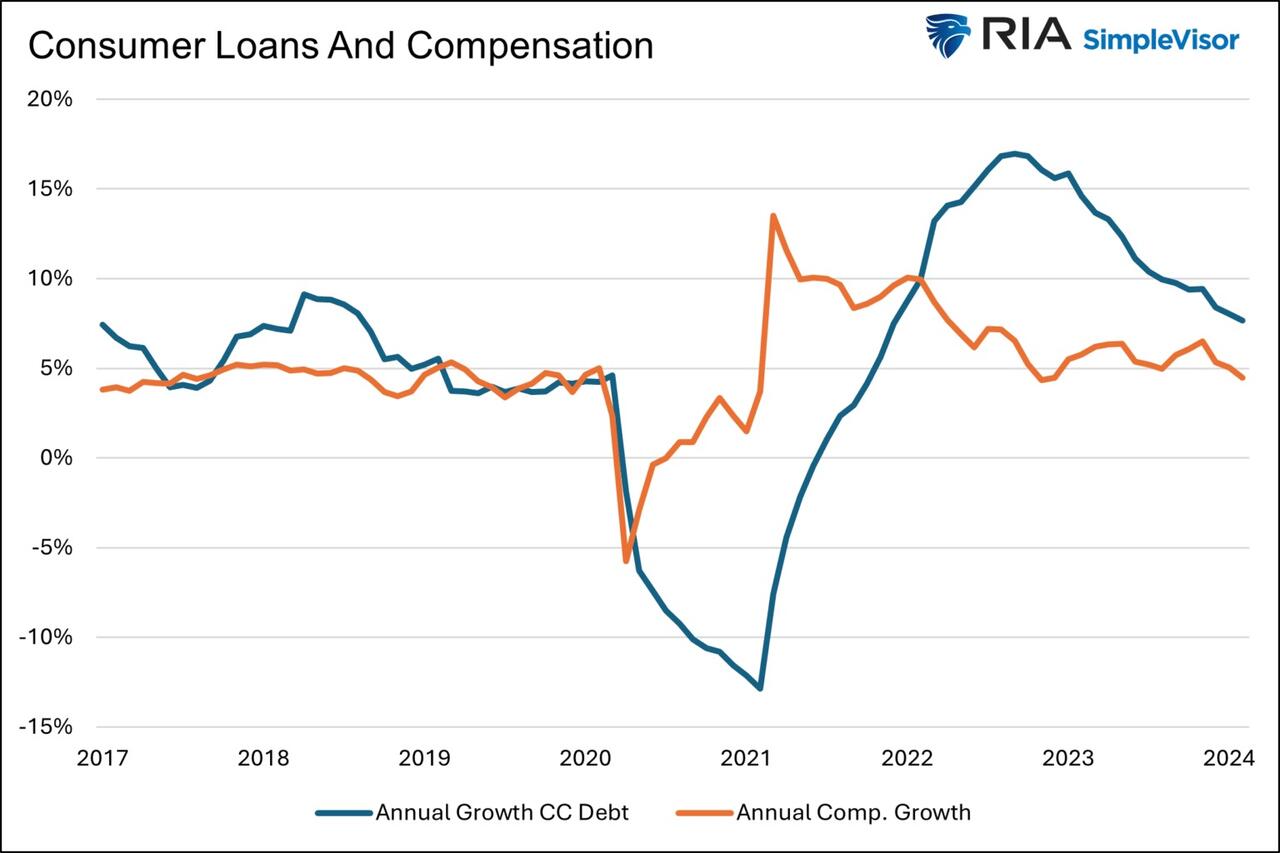

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

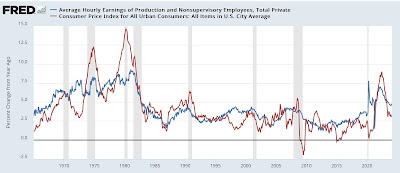

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

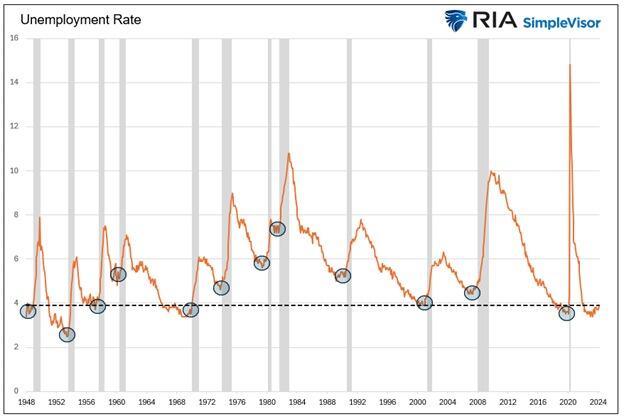

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

Uncategorized

The most potent labor market indicator of all is still strongly positive

– by New Deal democratOn Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently…

Share this:

{kind=link}

{kind=link}

- by New Deal democrat

On Monday I examined some series from last Friday’s Household survey in the jobs report, highlighting that they more frequently than not indicated a recession was near or underway. But I concluded by noting that this survey has historically been noisy, and I thought it would be resolved away this time. Specifically, there was strong contrary data from the Establishment survey, backed up by yesterday’s inflation report, to the contrary. Today I’ll examine that, looking at two other series.

{kind=link}

Q4 Update: Delinquencies, Foreclosures and REO

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

Aging at AACR Annual Meeting 2024

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

‘Bougie Broke’ – The Financial Reality Behind The Facade

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges