First Citizens BancShares Reports Fourth Quarter 2022 Earnings

PR Newswire

RALEIGH, N.C., Jan. 26, 2023

RALEIGH, N.C., Jan. 26, 2023 /PRNewswire/ -- First Citizens BancShares, Inc. ("BancShares") (NASDAQ: FCNCA) reported earnings for the fourth quarter and year-to-date period ended December 31, 2022.

Chairman and CEO Frank B. Holding, Jr. commented on the financial results for the quarter and year ended December 31, 2022: "First Citizens delivered solid financial results in 2022 marked by strong top line growth, low credit losses and well controlled expenses. Since the completion of our merger with CIT on January 3, 2022, we have successfully integrated our two companies and are now focused on capitalizing on opportunities to create positive operating leverage by growing revenues and optimizing our operations. We continued to execute on our capital strategy in the fourth quarter, completing our stock repurchase plan while still exceeding our CET 1 target. Looking ahead, we believe that we will have the ability to resume share buybacks in the second half of this year. We have also remained diligent in positioning ourselves to meet the regulatory requirements of a new large financial institution."

Holding added: "We are pleased with the performance of our lines of business during the year, achieving robust loan growth in the General Bank and in Industry Verticals and Business Capital within the Commercial Bank. Despite a challenging environment for deposits driven by unprecedented quantitative tightening, we experienced modest growth in noninterest checking accounts and only experienced a slight decline in deposits during the year. During the fourth quarter, deposits grew at an annualized rate of 8.4% driven by growth in our Direct Bank."

Holding concluded: "While we acknowledge concerns in the broader economy, and although we experienced an increase in nonaccrual loans during the fourth quarter, overall credit quality remains strong, and we are not seeing signs of significant loan portfolio deterioration. We enter 2023 with solid capital and liquidity positions and we believe that we are well positioned to continue to build customer relationships and grow our balance sheet profitably. And last but not least, I want to thank all of our associates for working so hard in 2022 on merger integration and to support our stockholders, customers and communities."

FINANCIAL HIGHLIGHTS

For the fourth quarter, net income available to common stockholders was $243 million, or $16.67 per diluted common share, compared to $303 million, or $19.25 per diluted common share in the third quarter of 2022. Fourth quarter results were impacted by the strategic decision to exit $1.2 billion of Bank Owned Life Insurance policies. The surrender of the policies resulted in a tax charge of $55 million. Favorable market conditions prompted us to exit this long-term, illiquid asset and, as we receive proceeds from the surrender, it increases our capital and liquidity positions while at the same time allowing us to invest in highly liquid assets at higher yields. During the fourth quarter, we repurchased 472,586 shares of Class A common stock for a total cost of $398 million. For the year, we repurchased 1,500,000 shares of Class A common stock for a total cost of $1.2 billion.

Fourth quarter adjusted net income available to common stockholders was $306 million, or $20.94 per diluted common share, as compared to $326 million, or $20.77 per diluted common share in the third quarter. The following bullets highlight significant changes in the components of net income and adjusted net income between the third and fourth quarters (see the supporting tables for a reconciliation of GAAP net income to adjusted net income):

Net interest income - Reported

Net interest income totaled $802 million compared to $795 million in the third quarter. The $7 million increase was primarily due to a higher yield on earning assets and loan growth, partially offset by higher funding costs and average balances.

Net interest margin was 3.36%, a decrease of 4 basis points compared to the third quarter. The yield on earning assets increased by 49 basis points while the cost of funding them increased by 53 basis points. The cost of funding earning assets increased due to higher rates paid on interest-bearing deposits and borrowings as well as a mix shift between noninterest-bearing and interest-bearing deposits.

Noninterest income and expense - Reported

Noninterest income totaled $429 million compared to $433 million in the third quarter, a decrease of $4 million. Rental income on operating lease equipment increased $5 million on a gross basis driven by continued improvement in utilization and a higher lease rate. Noninterest income from fee generating lines of business including service charges on deposit accounts, factoring and insurance commissions, card services and fee income and other service charges increased $8 million. Other noninterest income declined by $17 million, spread among various accounts.

Noninterest expense totaled $760 million for both the third and fourth quarters. While the total was unchanged over the prior quarter, there was a $6 million increase in marketing costs related to the Direct Bank and a $3 million increase in net occupancy expense due to increased repairs and utilities costs. These were offset by a $4 million decline in maintenance and depreciation expense on operating lease equipment, a $4 million decline in merger-related expenses and a $1 million decline in other operating expenses spread among various accounts.

Noninterest income and expense - Adjusted

Adjusted noninterest income totaled $290 million compared to $288 million in the third quarter, an increase of $2 million. The combination of higher rental income discussed above and a $4 million decline in depreciation and maintenance expense on operating lease equipment resulted in a $9 million increase in adjusted rental income on operating lease equipment. Noninterest income from fee generating lines of business including service charges on deposit accounts, factoring and insurance commissions, card services and fee income and other service charges increased $8 million. Other noninterest income declined by $15 million, spread among various accounts.

Adjusted noninterest expense totaled $590 million compared to $577 million in the third quarter, an increase of $13 million primarily due to the $6 million increase in marketing costs related to the Direct Bank, the $3 million increase in net occupancy expense noted above and a $4 million increase in other operating expenses spread among various accounts.

Credit

Provision for credit losses totaled $79 million compared to $60 million in the third quarter, an increase of $19 million. The increase was primarily due to an increase in net charge-offs and a reserve build in the quarter. The increase in allowance for credit losses over the prior quarter was due to changes in reserves on individually evaluated loans, loan growth and continued deterioration in the economic outlook, partially offset by a change in portfolio mix.

Net charge-offs totaled $24 million or a ratio of 0.14% of average loans, compared to $18 million or a ratio of 0.10% of average loans during the third quarter.

Nonaccrual loans as a percentage of total loans increased this quarter to 0.89% from 0.65%. The increase in nonaccrual loans was driven primarily by our non-owner occupied commercial real estate portfolio and more specifically related to general office exposure in the Commercial Bank segment.

Balance Sheet

Loans totaled $70.8 billion, an increase of $1.0 billion, or 5.6% on an annualized basis due to strong growth in our branch network, Mortgage and Business Capital, partially offset by declines in Commercial Services and Real Estate Finance.

Deposits totaled $89.4 billion, an increase of $1.9 billion, or 8.4% on an annualized basis. Interest-bearing deposits increased $3.5 billion driven primarily by the $2.5 billion of growth in the Direct Bank and the addition of $0.7 billion in brokered deposits.

Borrowings decreased $1.7 billion during the quarter, replaced by interest-bearing deposits to support our asset growth.

EARNINGS CALL DETAILS

BancShares will host a conference call and webcast to discuss the company's financial results on Thursday, January 26, 2023, at 9 a.m. Eastern time.

To access this call, dial:

United States: 1-844-200-6205 Canada: 1-833-950-0062 All other locations: 1-929-526-1599

Access code: 836216

The fourth quarter 2022 earnings presentation and this news release are available on the company's website at ir.firstcitizens.com, and the conference call will be webcast live at this same location.

A replay of the call will be available until Thursday, February 16, 2023, by calling 1-866-813-9403 (United States), 1-226-828-7578 (Canada) or +44-204-525-0658 (all other locations) and referencing access code 724723. A webcast archive of the conference call will be available through February 16, 2023, at ir.firstcitizens.com.

ABOUT FIRST CITIZENS BANCSHARES

First Citizens BancShares, Inc. (NASDAQ: FCNCA), a top 20 U.S. financial institution with more than $100 billion in assets, is the financial holding company for First-Citizens Bank & Trust Company ("First Citizens Bank"). First Citizens Bank helps personal, business, commercial and wealth clients build financial strength that lasts. Founded in 1898 and headquartered in Raleigh, N.C., First Citizens is the largest family-controlled bank in the United States, providing a unique legacy of strength, stability and long-term thinking that has spanned generations. First Citizens Bank offers an array of general banking services including a network of 500-plus branches in 22 states; commercial banking expertise delivering best-in-class lending, leasing and other financial services coast to coast; and a nationwide direct bank. Discover more at firstcitizens.com.

FORWARD-LOOKING STATEMENTS

This communication contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 regarding the financial condition, results of operations, business plans and future performance of BancShares. Words such as "anticipates," "believes," "estimates," "expects," "predicts," "forecasts," "intends," "plans," "projects," "targets," "designed," "could," "may," "should," "will," "potential," "continue", "aims" or other similar words and expressions are intended to identify these forward-looking statements. These forward-looking statements are based on BancShares' current expectations and assumptions regarding BancShares' business, the economy, and other future conditions.

Because forward-looking statements relate to future results and occurrences, they are subject to inherent risks, uncertainties, changes in circumstances and other risk factors that are difficult to predict. Many possible events or factors could affect BancShares' future financial results and performance and could cause the actual results, performance or achievements of BancShares to differ materially from any anticipated results expressed or implied by such forward-looking statements. Such risks and uncertainties include, among others, general competitive, economic, political, geopolitical events (including the military conflict between Russia and Ukraine) and market conditions, the impacts of the global COVID-19 pandemic on BancShares' business and customers, the financial success or changing conditions or strategies of BancShares' customers or vendors, fluctuations in interest rates, actions of government regulators, including the recent and projected interest rate hikes by the Board of Governors of the Federal Reserve Board (the "Federal Reserve"), the potential impact of decisions by the Federal Reserve on BancShares' capital plans, adverse developments with respect to U.S. or global economic conditions, including the significant turbulence in the capital or financial markets, the impact of the current inflationary environment, the impact of implementation and compliance with current or proposed laws, regulations and regulatory interpretations, the availability of capital and personnel, the timing and authorization of any future repurchases of our Class A common under potential share repurchase programs and the failure to realize the anticipated benefits of BancShares' previous acquisition transaction(s), including the recently completed transaction with CIT, which acquisition risks include (1) disruption from the transaction, or recently completed mergers, with customer, supplier or employee relationships, (2) the possibility that the amount of the costs, fees, expenses and charges related to the transaction may be greater than anticipated, including as a result of unexpected or unknown factors, events or liabilities, (3) reputational risk and the reaction of the parties' customers to the transaction, (4) the risk that the cost savings and any revenue synergies from the transaction may not be realized or take longer than anticipated to be realized and (5) difficulties experienced in the integration of the businesses.

Except to the extent required by applicable laws or regulations, BancShares disclaims any obligation to update forward-looking statements or to publicly announce the results of any revisions to any of the forward-looking statements included herein to reflect future events or developments. Additional factors which could affect the forward-looking statements can be found in BancShares' Annual Report on Form 10-K for the fiscal year ended December 31, 2021, and its other filings with the Securities and Exchange Commission (the "SEC").

NON-GAAP MEASURES

Certain measures in this release and supporting tables, including those referenced as "Adjusted", are "Non-GAAP", meaning they are not presented in accordance with generally accepted accounting principles in the U.S. ("GAAP") and also are not codified in U.S. banking regulations currently applicable to BancShares. BancShares believes that Non-GAAP financial measures, when reviewed in conjunction with GAAP financial information, can provide transparency about or an alternative means of assessing its operating results and financial position to its investors, analysts and management. Non-GAAP measures should be considered a supplement to, and not a substitute for, financial measures prepared in accordance with GAAP. The Non-GAAP measures are reconciled to the most directly comparable GAAP measure, in the Non-GAAP reconciliation table(s) at the end of this earnings release, and notable items are summarized in a separate table.

Dollars in millions, except per share data

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Summary Financial Data & Key Metrics

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Results of Operations:

Net interest income

$

802

795

357

2,946

1,390

Provision (benefit) for credit losses

79

60

(5)

645

(37)

Net interest income after provision for credit losses

723

735

362

2,301

1,427

Noninterest income

429

433

114

2,136

508

Noninterest expense

760

760

323

3,075

1,234

Income before income taxes

392

408

153

1,362

701

Income tax expense

135

93

30

264

154

Net income

257

315

123

1,098

547

Preferred stock dividends

14

12

4

50

18

Net income available to common stockholders

$

243

303

119

1,048

529

Adjusted net income available to common stockholders(1)

306

326

126

1,201

509

Pre-tax, pre-provision net revenue (PPNR)(1)

471

468

148

2,007

664

Per Share Information:

Diluted earnings per common share (EPS)

$

16.67

19.25

12.09

67.40

53.88

Adjusted diluted earnings per common share (EPS)(1)

20.94

20.77

12.82

77.24

51.88

Book value per common share

605.36

597.75

447.95

605.36

447.95

Tangible book value per common share (TBV)(1)

571.89

564.97

410.74

571.89

410.74

Key Performance Metrics:

Return on average assets (ROA)

0.93 %

1.16 %

0.84 %

1.01 %

1.00 %

Adjusted ROA(1)

1.15

1.24

0.89

1.15

0.96

PPNR ROA(1)

1.70

1.72

1.01

1.84

1.21

Adjusted PPNR ROA(1)

1.81

1.86

1.08

1.64

1.16

Return on average common equity (ROE)

11.05

12.49

10.96

11.15

12.84

Adjusted ROE(1)

13.89

13.47

11.63

12.78

12.36

Return on average tangible common equity (ROTCE)(1)

11.70

13.17

12.00

11.78

14.12

Adjusted ROTCE(1)

14.71

14.20

12.72

13.50

13.60

Efficiency ratio

61.74

61.91

68.52

60.50

64.98

Adjusted efficiency ratio(1)

54.08

53.32

66.31

56.40

65.11

Net interest margin (NIM)(2)

3.36

3.40

2.58

3.14

2.66

Select Balance Sheet Items at Period End:

Total investment securities

$

19,369

18,841

13,110

19,369

13,110

Total loans and leases

70,781

69,790

32,372

70,781

32,372

Total operating lease equipment, net

8,156

7,984

—

8,156

—

Total deposits

89,408

87,553

51,406

89,408

51,406

Total borrowings

6,645

8,343

1,784

6,645

1,784

Loan to deposit ratio

79.17 %

79.71 %

62.97 %

79.17 %

62.97 %

Noninterest-bearing deposits to total deposits

27.87 %

30.37 %

41.64 %

27.87 %

41.64 %

Capital Ratios at Period End: (3)

Total risk-based capital ratio

13.18 %

13.46 %

14.35 %

13.18 %

14.35 %

Tier 1 risk-based capital ratio

11.06

11.36

12.47

11.06

12.47

Common equity Tier 1 ratio

10.08

10.37

11.50

10.08

11.50

Tier 1 leverage capital ratio

9.06

9.31

7.59

9.06

7.59

Asset Quality at Period End:

Nonaccrual loans to total loans and leases

0.89 %

0.65 %

0.37 %

0.89 %

0.37 %

Allowance for credit losses (ACL) to loans and leases

1.30

1.26

0.55

1.30

0.55

Net charge-off ratio

0.14

0.10

-0.01

0.12

0.03

(1) Denotes a non-GAAP measure. Refer to the non-GAAP reconciliation subsequently included in these materials for a reconciliation to the most directly comparable GAAP measure. "Adjusted" items exclude the impact of Notable Items.

(2) Calculated net of average credit balances of factoring clients.

(3) Capital ratios for the current quarter are preliminary pending completion of quarterly regulatory filings.

Dollars in millions, except share and per share data

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Income Statement (unaudited)

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Interest income

Interest and fees on loans

$

892

785

328

2,953

1,295

Interest on investment securities

92

90

39

354

145

Interest on deposits at banks

56

31

4

106

11

Total interest income

1,040

906

371

3,413

1,451

Interest expense

Deposits

176

78

8

335

33

Borrowings

62

33

6

132

28

Total interest expense

238

111

14

467

61

Net interest income

802

795

357

2,946

1,390

Provision (benefit) for credit losses

79

60

(5)

645

(37)

Net interest income after provision for credit losses

723

735

362

2,301

1,427

Noninterest income

Rental income on operating lease equipment

224

219

—

864

—

Fee income and other service charges

45

44

11

163

42

Wealth management services

35

35

33

142

129

Service charges on deposit accounts

23

21

26

100

95

Factoring commissions

26

24

—

104

—

Cardholder services, net

26

25

22

102

87

Merchant services, net

8

8

7

35

33

Insurance commissions

13

11

4

47

16

Realized gain on sale of investment securities available for sale, net

—

—

—

—

33

Fair value adjustment on marketable equity securities, net

2

(2)

3

(3)

34

Bank-owned life insurance

7

8

1

32

3

Gain on sale of leasing equipment, net

2

2

—

15

—

Gain on acquisition

—

—

—

431

—

Gain on extinguishment of debt

—

1

—

7

—

Other noninterest income

18

37

7

97

36

Total noninterest income

429

433

114

2,136

508

Noninterest expense

Depreciation on operating lease equipment

88

87

—

345

—

Maintenance and other operating lease expenses

47

52

—

189

—

Salaries and benefits

352

351

193

1,396

759

Net occupancy expense

50

47

30

194

117

Equipment expense

55

55

30

216

119

Professional fees

13

13

7

57

20

Third-party processing fees

26

27

16

103

60

FDIC insurance expense

5

5

4

31

14

Marketing

21

15

3

53

10

Merger-related expenses

29

33

9

231

29

Intangible asset amortization

6

5

3

23

12

Other noninterest expense

68

70

28

237

94

Total noninterest expense

760

760

323

3,075

1,234

Income before income taxes

392

408

153

1,362

701

Income tax expense

135

93

30

264

154

Net income

$

257

315

123

1,098

547

Preferred stock dividends

14

12

4

50

18

Net income available to common stockholders

$

243

303

119

1,048

529

Basic earnings per common share

$

16.69

19.27

12.09

67.47

53.88

Diluted earnings per common share

$

16.67

19.25

12.09

67.40

53.88

Weighted average common shares outstanding (basic)

14,590,387

15,711,976

9,816,405

15,531,924

9,816,405

Weighted average common shares outstanding (diluted)

14,607,426

15,727,993

9,816,405

15,549,944

9,816,405

Dollars in millions

BancShares

BancShares

BancShares

Balance Sheet (unaudited)

12/31/22

9/30/22

12/31/21

Assets

Cash and due from banks

$

518

481

338

Interest-earning deposits at banks

5,025

6,172

9,115

Investment in marketable equity securities

95

92

98

Investment securities available for sale

8,995

9,088

9,203

Investment securities held to maturity

10,279

9,661

3,809

Assets held for sale

60

21

99

Loans and leases

70,781

69,790

32,372

Allowance for credit losses

(922)

(882)

(178)

Loans and leases, net of allowance for credit losses

69,859

68,908

32,194

Operating lease equipment, net

8,156

7,984

—

Premises and equipment, net

1,456

1,410

1,233

Goodwill

346

346

346

Other intangible assets

140

145

19

Other assets

4,369

5,002

1,855

Total assets

$

109,298

109,310

58,309

Liabilities

Deposits:

Noninterest-bearing

$

24,922

26,587

21,405

Interest-bearing

64,486

60,966

30,001

Total deposits

89,408

87,553

51,406

Credit balances of factoring clients

995

1,147

—

Borrowings:

Short-term borrowings

2,186

3,128

589

Long-term borrowings

4,459

5,215

1,195

Total borrowings

6,645

8,343

1,784

Other liabilities

2,588

2,434

381

Total liabilities

99,636

99,477

53,571

Stockholders' equity

Preferred stock

881

881

340

Common stock:

Class A - $1 par value

14

14

9

Class B - $1 par value

1

1

1

Additional paid in capital

4,109

4,506

—

Retained earnings

5,392

5,160

4,378

Accumulated other comprehensive loss

(735)

(729)

10

Total stockholders' equity

9,662

9,833

4,738

Total liabilities and stockholders' equity

$

109,298

109,310

58,309

Dollars in millions, except share per share data

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Notable Items (1)

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Noninterest income

Rental income on operating lease equipment (2)

$

(135)

(139)

—

(534)

—

Realized gain on sale of investment securities available for sale, net

—

—

—

—

(33)

Fair value adjustment on marketable equity securities, net

(2)

2

(3)

3

(34)

Gain on sale of leasing equipment, net

(2)

(2)

—

(15)

—

Gain on acquisition

—

—

—

(431)

—

Gain on extinguishment of debt

—

(1)

—

(7)

—

Other noninterest income (3)

—

(5)

—

(11)

—

Impact on adjusted noninterest income

(139)

(145)

(3)

(995)

(67)

Noninterest expense

Depreciation on operating lease equipment (2)

(88)

(87)

—

(345)

—

Maintenance and other operating lease expenses (2)

(47)

(52)

—

(189)

—

Merger-related expenses

(29)

(33)

(9)

(231)

(29)

Intangible asset amortization

(6)

(5)

(3)

(23)

(12)

Other noninterest expense (4)

—

(6)

—

18

—

Impact on adjusted noninterest expense

(170)

(183)

(12)

(770)

(41)

CECL Day 2 provision and reserve for unfunded commitments

—

—

—

(513)

—

Impact on adjusted pre-tax income

31

38

9

288

(26)

Income tax impact (5) (6)

(32)

15

2

135

(6)

Impact on adjusted net income

$

63

23

7

153

(20)

Impact on adjusted diluted EPS

$

4.27

1.52

0.73

9.84

(2.00)

(1) Notable items include income and expense for infrequent transactions and certain recurring items (typically noncash) that Management believes should be excluded from adjusted measures (non-GAAP) to enhance understanding of operations and comparability to historical periods. Management utilizes both GAAP and adjusted measures (non-GAAP) to analyze the Company's performance. Refer to the Non-GAAP reconciliation table(s) at the end of this earnings release for a reconciliation of Non-GAAP measures to the most directly comparable GAAP measures.

(2) Depreciation and maintenance and other operating lease expenses are reclassified from noninterest expense to a reduction of rental income on operating lease equipment. There is no net impact to earnings for this notable item as adjusted noninterest income and expense are reduced by the same amount. Adjusted rental income on operating lease equipment (non-GAAP) is net of depreciation and maintenance expense for operating lease equipment. Management believes this measure enhances comparability to banking peers, primarily due to the extent of our rail and other equipment rental activities. Refer to the Non-GAAP reconciliation table(s) at the end of this earnings release for a reconciliation of Non-GAAP measures to the most directly comparable GAAP measure.

(3) Primarily includes the following: 3Q22- contract settlement with a rail customer; YTD22- contract settlement with rail customer and gain on sale of other assets.

(4) Primarily includes the following: 3Q22- impairment of a call center facility; YTD22- impairment of a call center facility and termination of two post retirement benefit plans.

(5) Includes $55 million of tax expense related to the early surrender of BOLI policies. During 4Q22, management decided to early surrender $1.2 billion of BOLI policies. This triggered a taxable gain of $160 million and resulted in tax expense of $55 million.

(6) The income tax impact includes tax discrete items and changes in the estimated annualized effective tax rate.

Dollars in millions, except share and per share data

Condensed Income Statement (unaudited) - Adjusted for Notable Items (1)

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Interest income

$

1,040

906

371

3,413

1,451

Interest expense

238

111

14

467

61

Net interest income

802

795

357

2,946

1,390

Provision (benefit) for credit losses

79

60

(5)

132

(37)

Net interest income after provision for credit losses

723

735

362

2,814

1,427

Noninterest income

290

288

111

1,141

441

Noninterest expense

590

577

311

2,305

1,193

Income before income taxes

423

446

162

1,650

675

Income tax expense

103

108

32

399

148

Net income

$

320

338

130

1,251

527

Preferred stock dividends

14

12

4

50

18

Net income available to common stockholders

$

306

326

126

1,201

509

Basic earnings per common share

$

20.97

20.79

12.82

77.33

51.88

Diluted earnings per common share

$

20.94

20.77

12.82

77.24

51.88

Weighted average common shares outstanding (basic)

14,590,387

15,711,976

9,816,405

15,531,924

9,816,405

Weighted average common shares outstanding (diluted)

14,607,426

15,727,993

9,816,405

15,549,944

9,816,405

(1) The GAAP income statements and notable items are included previously in this communication. The condensed adjusted income statements above (non-GAAP) exclude the impacts of notable items. Refer to the Non-GAAP reconciliation table(s) at the end of this earnings release for a reconciliation of Non-GAAP measures to the most directly comparable GAAP measure.

Dollars in millions

BancShares

BancShares

BancShares

Loans & Leases by Class (end of period)

12/31/22

9/30/22

12/31/21

Loans & Leases by Class

Commercial

Commercial construction

$

2,804

2,752

1,238

Owner-occupied commercial mortgages

14,473

14,053

12,099

Non-owner-occupied commercial mortgages

9,902

9,683

3,041

Commercial and industrial

24,105

24,288

5,937

Leases

2,171

2,184

271

Total commercial

$

53,455

52,960

22,586

Consumer

Residential mortgage

$

13,309

12,910

6,088

Revolving mortgage

1,951

1,923

1,818

Consumer auto

1,414

1,385

1,332

Consumer other

652

612

548

Total consumer

$

17,326

16,830

9,786

Total loans and leases

$

70,781

69,790

32,372

Less: Allowance for credit losses

(922)

(882)

(178)

Total loans and leases, net of allowance for credit losses

$

69,859

68,908

32,194

BancShares

BancShares

BancShares

Deposits by Type (end of period)

12/31/22

9/30/22

12/31/21

Noninterest-bearing demand

$

24,922

26,587

21,405

Checking with interest

16,202

16,118

12,694

Money market

21,040

21,818

10,590

Savings

16,634

14,722

4,236

Time

10,610

8,308

2,481

Total deposits

$

89,408

87,553

51,406

Dollars in millions

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Credit Quality & Allowance

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Nonaccrual loans

$

627

454

121

627

121

Ratio of nonaccrual loans to total loans

0.89 %

0.65 %

0.37 %

0.89 %

0.37 %

Charge-offs

$

39

33

9

146

36

Recoveries

(15)

(15)

(9)

(67)

(26)

Net charge-offs

$

24

18

—

79

10

Net charge-off ratio

0.14 %

0.10 %

(0.01) %

0.12 %

0.03 %

Allowance for credit losses to loans ratio

1.30 %

1.26 %

0.55 %

1.30 %

0.55 %

Allowance for credit losses - beginning

$

882

850

183

178

225

Initial PCD ACL

—

—

—

272

—

Day 2 provision, excluding provision for unfunded commitments

—

—

—

454

—

Provision (benefit) for credit losses

64

50

(5)

97

(37)

Net charge-offs

(24)

(18)

—

(79)

(10)

Allowance for credit losses - ending

$

922

882

178

922

178

Dollars in millions

Average Balance Sheet

BancShares QTD 12/31/22

BancShares QTD 09/30/22

BancShares QTD 12/31/21

Avg Balance

Income/ Expense

Yield/Rate

Avg Balance

Income/ Expense

Yield/Rate

Avg Balance

Income/ Expense

Yield/Rate

Loans and leases (1) (2)

$ 69,290

$ 892

5.09 %

$ 67,733

$ 785

4.58 %

$ 32,488

$ 328

3.98 %

Total investment securities

18,876

92

1.95

19,119

90

1.88

11,424

39

1.39

Interest-earning deposits at banks

6,193

56

3.60

5,685

31

2.17

10,690

4

0.15

Total interest-earning assets (2)

$ 94,359

$ 1,040

4.36 %

$ 92,537

$ 906

3.87 %

$ 54,602

$ 371

2.69 %

Operating lease equipment, net (including held for sale)

$ 8,049

$ 7,981

$ —

Cash and due from banks

500

489

337

Allowance for credit losses

(886)

(851)

(184)

All other non-interest-earning assets

7,770

7,831

3,361

Total assets

$ 109,792

$ 107,987

$ 58,116

Interest-bearing deposits:

Checking with interest

$ 15,985

$ 13

0.24 %

$ 16,160

$ 7

0.14 %

$ 11,994

$ 2

0.05 %

Money market

21,200

60

1.13

22,993

32

0.55

10,358

3

0.09

Savings

15,831

69

1.73

13,956

28

0.78

4,140

—

0.03

Time deposits

9,516

34

1.42

8,436

11

0.54

2,517

3

0.62

Total interest-bearing deposits

62,532

176

1.12

61,545

78

0.50

29,009

8

0.11

Borrowings:

Securities sold under customer repurchase agreements

514

—

0.27

617

1

0.16

650

1

0.16

Short-term FHLB borrowings

2,080

20

3.72

1,188

8

2.57

—

—

—

Short-term borrowings

2,594

20

3.04

1,805

9

1.74

650

1

0.16

Federal Home Loan Bank borrowings

2,818

28

3.85

1,784

11

2.45

645

1

1.28

Senior unsecured borrowings

906

4

2.03

898

5

2.00

—

—

—

Subordinated debt

1,051

9

3.38

1,054

8

3.21

497

3

3.34

Other borrowings

25

1

6.57

67

—

4.51

75

1

1.25

Long-term borrowings

4,800

42

3.42

3,803

24

2.59

1,217

5

2.12

Total borrowings

7,394

62

3.28

5,608

33

2.32

1,867

6

1.44

Total interest-bearing liabilities

$ 69,926

$ 238

1.35 %

$ 67,153

$ 111

0.65 %

$ 30,876

$ 14

0.19 %

Noninterest-bearing deposits

$ 26,510

$ 26,877

$ 22,229

Credit balances of factoring clients

1,174

1,089

—

Other noninterest-bearing liabilities

2,561

2,369

378

Stockholders' equity

9,621

10,499

4,633

Total liabilities and stockholders' equity

$ 109,792

$ 107,987

$ 58,116

Net interest income

$ 802

$ 795

$ 357

Net interest spread (2)

3.01 %

3.22 %

2.50 %

Net interest margin (2)

3.36 %

3.40 %

2.58 %

(1) Loans and leases include non-PCD and PCD loans, nonaccrual loans and held for sale. Interest income on loans and leases includes accretion income and loan fees.

(2) The balance and rate presented is calculated net of average credit balances of factoring clients.

Note: Certain items above do not precisely recalculate as presented due to rounding.

Dollars in millions

Average Balance Sheet

BancShares YTD 12/31/22

BancShares YTD 12/31/21

Avg Balance

Income/

Expense

Yield/Rate

Avg Balance

Income/

Expense

Yield/Rate

Loans and leases (1) (2)

$ 66,634

$ 2,953

4.41 %

$ 32,860

$ 1,295

3.91 %

Total investment securities

19,166

354

1.85

10,611

145

1.37

Interest-earning deposits at banks

7,726

106

1.38

8,349

11

0.13

Total interest-earning assets(2)

$ 93,526

$ 3,413

3.63 %

$ 51,820

$ 1,451

2.78 %

Operating lease equipment, net (including held for sale)

$ 7,982

$ —

Cash and due from banks

512

350

Allowance for credit losses

(875)

(202)

All other non-interest-earning assets

7,788

3,015

Total assets

$ 108,933

$ 54,983

Interest-bearing deposits:

Checking with interest

$ 16,323

$ 29

0.15 %

$ 11,258

$ 6

0.05 %

Money market

23,949

125

0.52

9,708

10

0.10

Savings

14,193

117

0.82

3,847

1

0.03

Time deposits

9,133

64

0.70

2,647

16

0.63

Total interest-bearing deposits

63,598

335

0.53

27,460

33

0.12

Borrowings:

Securities sold under customer repurchase agreements

590

1

0.19

660

1

0.20

Short-term FHLB borrowings

824

28

3.30

—

—

—

Short-term borrowings

1,414

29

2.00

660

1

0.20

Federal Home Loan Bank borrowings

1,414

43

2.96

648

8

1.28

Senior unsecured borrowings

1,348

25

1.87

—

—

—

Subordinated debt

1,056

33

3.15

498

15

3.35

Other borrowings

64

2

3.22

80

4

1.23

Long-term borrowings

3,882

103

2.64

1,226

27

2.12

Total borrowings

5,296

132

2.47

1,886

28

1.45

Total interest-bearing liabilities

$ 68,894

$ 467

0.68 %

$ 29,346

$ 61

0.21 %

Noninterest-bearing deposits

$ 26,318

$ 20,798

Credit balances of factoring clients

1,153

—

Other noninterest-bearing liabilities

2,292

378

Stockholders' equity

10,276

4,461

Total liabilities and stockholders' equity

$ 108,933

$ 54,983

Net interest income

$ 2,946

$ 1,390

Net interest spread (2)

2.95 %

2.57 %

Net interest margin (2)

3.14 %

2.66 %

(1) Loans and leases include non-PCD and PCD loans, nonaccrual loans and held for sale. Interest income on loans and leases includes accretion income and loan fees.

(2) The balance and rate presented is calculated net of average credit balances of factoring clients.

Note: Certain items above do not precisely recalculate as presented due to rounding.

Dollars in millions, except share and per share data

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Non-GAAP Reconciliations

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Net income and EPS

Net income (GAAP)

a

$

257

315

123

1,098

547

Preferred stock dividends

14

12

4

50

18

Net income available to common stockholders (GAAP)

b

243

303

119

1,048

529

Total notable items, after income tax

c

63

23

7

153

(20)

Adjusted net income (non-GAAP)

d = (a+c)

320

338

130

1,251

527

Adjusted net income available to common stockholders (non-GAAP)

e = (b+c)

$

306

326

126

1,201

509

Weighted average common shares outstanding

Basic

f

14,590,387

15,711,976

9,816,405

15,531,924

9,816,405

Diluted

g

14,607,426

15,727,993

9,816,405

15,549,944

9,816,405

EPS (GAAP)

Basic

b/f

$

16.69

19.27

12.09

67.47

53.88

Diluted

b/g

16.67

19.25

12.09

67.40

53.88

Adjusted EPS (non-GAAP)

Basic

e/f

$

20.97

20.79

12.82

77.33

51.88

Diluted

e/g

20.94

20.77

12.82

77.24

51.88

Noninterest income and expense

Noninterest income

h

$

429

433

114

2,136

508

Impact of notable items, before income tax

(139)

(145)

(3)

(995)

(67)

Adjusted noninterest income

i

$

290

288

111

1,141

441

Noninterest expense

j

$

760

760

323

3,075

1,234

Impact of notable items, before income tax

(170)

(183)

(12)

(770)

(41)

Adjusted noninterest expense

k

$

590

577

311

2,305

1,193

Provision (benefit) for credit losses

Provision (benefit) for credit losses

$

79

60

(5)

645

(37)

Plus: Day 2 provision for credit losses

—

—

—

(513)

—

Adjusted provision (benefit) for credit losses

$

79

60

(5)

132

(37)

PPNR

Net income (GAAP)

a

$

257

315

123

1,098

547

Plus:

Provision (benefit) for credit losses

79

60

(5)

645

(37)

Income tax expense (benefit)

135

93

30

264

154

PPNR (non-GAAP)

l

$

471

468

148

2,007

664

Plus: total notable items, before income tax

31

38

9

(225)

(26)

Adjusted PPNR (non-GAAP)

m

$

502

506

157

1,782

638

Note: Certain items above do not precisely recalculate as presented due to rounding.

Dollars in millions, except share and per share data

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Non-GAAP Reconciliations (continued)

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

ROA

Net income (GAAP)

a

$

257

315

123

1,098

547

Annualized net income

n = a annualized

1,020

1,250

488

1,098

547

Adjusted net income (non-GAAP)

d

320

338

130

1,251

527

Annualized adjusted net income

p = d annualized

1,270

1,341

516

1,251

527

Average assets

o

109,792

107,987

58,116

108,933

54,983

ROA

n/o

0.93 %

1.16 %

0.84 %

1.01 %

1.00 %

Adjusted ROA

p/o

1.15 %

1.24 %

0.89 %

1.15 %

0.96 %

PPNR ROA

PPNR (non-GAAP)

l

$

471

468

148

2,007

664

Annualized PPNR

q = l annualized

1,868

1,858

589

2,007

664

Adjusted PPNR (non-GAAP)

m

502

506

157

1,782

638

Annualized PPNR

r = m annualized

1,992

2,009

622

1,782

638

PPNR ROA

q/o

1.70 %

1.72 %

1.01 %

1.84 %

1.21 %

Adjusted PPNR ROA

r/o

1.81 %

1.86 %

1.08 %

1.64 %

1.16 %

ROE and ROTCE

Annualized net income available to common stockholders

s = b annualized

$

964

1,202

472

1,048

529

Annualized adjusted net income available to common stockholders

t = e annualized

$

1,214

1,293

500

1,201

509

Average stockholders' equity (GAAP)

$

9,621

10,499

4,633

10,276

4,461

Less: average preferred stock

881

881

340

878

340

Average common stockholders' equity (non-GAAP)

u

$

8,740

9,618

4,293

9,398

4,121

Less: average goodwill

346

346

350

346

350

Less: average other intangible assets

143

148

21

156

25

Average tangible common equity (non-GAAP)

v

$

8,251

9,124

3,922

8,896

3,746

ROE

s/u

11.05 %

12.49 %

10.96 %

11.15 %

12.84 %

Adjusted ROE

t/u

13.89 %

13.47 %

11.63 %

12.78 %

12.36 %

ROTCE

s/v

11.70 %

13.17 %

12.00 %

11.78 %

14.12 %

Adjusted ROTCE

t/v

14.71 %

14.20 %

12.72 %

13.50 %

13.60 %

Tangible common equity to tangible assets

Stockholders' equity (GAAP)

w

$

9,662

9,833

4,738

9,662

4,738

Less: preferred stock

881

881

340

881

340

Common equity (non-GAAP)

x

$

8,781

8,952

4,398

8,781

4,398

Less: goodwill

346

346

346

346

346

Less: other intangible assets

140

145

19

140

19

Tangible common equity (non-GAAP)

y

$

8,295

8,461

4,033

8,295

4,033

Total assets (GAAP)

z

109,298

109,310

58,309

109,298

58,309

Tangible assets (non-GAAP)

aa

108,812

108,819

57,944

108,812

57,944

Total equity to total assets

w/z

8.84 %

9.00 %

8.13 %

8.84 %

8.13 %

Tangible common equity to tangible assets (non-GAAP)

y/aa

7.62 %

7.78 %

6.96 %

7.62 %

6.96 %

Note: Certain items above do not precisely recalculate as presented due to rounding.

Dollars in millions, except share and per share data

BancShares

BancShares

BancShares

BancShares

BancShares

QTD

QTD

QTD

YTD

YTD

Non-GAAP Reconciliations (continued)

12/31/22

9/30/22

12/31/21

12/31/22

12/31/21

Book value and tangible book value per common share

Common shares outstanding at period end

bb

14,506,200

14,976,127

9,816,405

14,506,200

9,816,405

Book value per share

x/bb

$

605.36

597.75

447.95

605.36

447.95

Tangible book value per share

y/bb

$

571.89

564.97

410.74

571.89

410.74

Efficiency ratio

Net interest income

cc

$

802

795

357

2,946

1,390

Efficiency ratio (GAAP)

j / (h + cc)

61.74 %

61.91 %

68.52 %

60.50 %

64.98 %

Adjusted efficiency ratio (non-GAAP)

k / (i + cc)

54.08 %

53.32 %

66.31 %

56.40 %

65.11 %

Rental income on operating lease equipment

Rental income on operating lease equipment

$

224

219

—

864

—

Less:

Depreciation on operating lease equipment

88

87

—

345

—

Maintenance and other operating lease expenses

47

52

—

189

—

Adjusted rental income on operating lease equipment

89

80

—

330

—

Note: Certain items above do not precisely recalculate as presented due to rounding.

Vetted by HousingWire | Our editors independently review the products we recommend. When you buy through our links, we may earn a commission.

Real estate is a vibrant, dynamic and competitive industry. From the thrill of a sale to the pursuit of new leads, it keeps you on your toes. That said, it can also be incredibly isolating, and it can be hard to stay motivated. As a way to deal with this, many agents and brokers seek out professional mentorship as a means to gain insight and level up their performance. Across the country, the best real estate coaches serve as valuable mentors who can help agents and brokers achieve the success they deserve.

“It’s really hard for independent business owners to get unbiased advice from themselves,” says Kyle Scott, President of SERHANT. Ventures. “So they need unbiased experts to work with that will help them grow their business — someone who has been there, who has done it, and who is able to see their business from both the 35,000-foot view and down in the weeds.”

A quick internet search will prove that real estate coaching programs are plentiful. Whether you’re looking to expand your team or client network or figure out how to delegate work so you can focus on the tasks you do best, a real estate coaching program could be a valuable launchpad. But when it comes to choosing the right one for your unique needs, there’s a lot to consider. Here, we highlight some of the best real estate coaches in the industry and their programs.

An unbiased view is worth millions. Often, we turn to our closest friends and family for guidance. Unfortunately, they’re usually not familiar with the ins and outs of the real estate industry and can’t provide you with the relevant feedback you need. As a result, many independent contractors rely on themselves, which generally doesn’t work either.

You can’t advise yourself, you’re too close to it. A coach works best for someone who is actually looking to grow their business, someone who is looking to put in the time and the energy to make a difference in achieving more income this year.

Hire a coach if you want to start taking your business to the next level for any reason — you want to make more money, have more freedom with your time, or stop riding the ins and outs of the commission cycle.President of SERHANT. Ventures

1. Sell It Like Serhant

Key Facts

Grown throughout the pandemic, the Sell It Like Serhant program has been carefully adapted to the current market. It follows a weekly and bi-weekly platform featuring one-on-one virtual coaching from Serhant’s proprietary video platform. After a half-hour or hour-long group meeting every week or every other week, participants follow actionable steps to help them grow their business. Thus far, more than 22,000 enrollees in 128 countries have been through the Sell It Like Serhant program.

What We Love

Serhant offers daily office hours so participants can pop into virtual sessions to ask questions or get expert advice between their regularly scheduled sessions. A community platform also allows participants to pass referrals to each other. Thus far, it seems to have worked: To date, participating agents have closed over $250 million of referral deals.

Pricing

There are different membership tiers, depending on the level of guidance you need. The introductory Real Estate Core Course starts at $497. Prices are higher for a more specific course or one with 1:1 coaching.

Who’s it Best For?

If you’re looking to build a memorable personal brand, SERHANT. is the way to go. “The number one differentiator about our program is we understand that as a real estate agent, you have one job: to generate leads,” says SERHANT. Ventures President Kyle Scott. “Our number one focus is helping you build a clear, compelling, memorable personal brand and put your lead generation on autopilot. So that way, you can do what you do best, which is build relationships and close deals.”

Visit Sell It Like Serhant

2. Tom Ferry International

Key Facts

For good reason, Ferry International refers to itself as the real estate industry’s leading coaching and training company. Focused on Ferry’s “8 Levels of Performance,” the programs are a staple of real estate coaching. Their new group coaching sessions cover various aspects of real estate sales.

Prospecting Bootcamp is a 14-hour program comprised of seven two-hour group coaching sessions, and includes a peer-to-peer collaboration space. It involves independent work pulled from training videos and downloadable resources.

Recruitment Roadmap consists of hour-long sessions each week for ten weeks. Completed over Zoom and through the Tom Ferry video platform, each group coaching program offers a high level of specialization.

Finally, their Fast Track program offers 12 interactive group coaching sessions designed to help new agents build the necessary skills to succeed — like mastering listing presentations and handling objections.

What we love

If you’re looking for the gold standard of real estate coaching, Tom Ferry has the goods to back up the bravado. Because of their many years in the biz, Tom Ferry has a huge base of coaches, which means there are plenty of options to find the program best suited for your specific needs.

Pricing

Tom Ferry’s Prospecting Bootcamp and Fast Track coaching programs cost $999 but can be broken down into three monthly payments. The Recruitment Roadmap group coaching costs $1,499 but can be split into three monthly payments of $500. Consider their free coaching consultation if you want to dip your toes in the water. Check out their customer reviews, where several coaching program alums rave about the program.

Who’s it Best For?

If you thrive in a group setting that allows you to feed off the energy of others, Tom Ferry might be right for you. Their group coaching programs are new and more affordable alternatives to often costly 1:1 coaching fees.

Visit Tom Ferry

3. Tim and Julie Harris

Key Facts

The dynamic duo of real estate coaching, Tim and Julie Harris are a major name in the industry. Under their business, Harris Real Estate Coaching, their programs are divided into three tiers: Premier, Premier Plus, and VIP, all of which rely on a user-friendly online platform.

Pricing

Premier platform costs $197 per month, but a 30-day free trial is available. Premier Plus costs $599 per month, while VIP costs $999 per month. Of course, their wildly successful podcast is a great free resource to tap into, as well as Tim and Julie’s many written contributions to HousingWire.

Who’s it Best For?

If you’re constantly on the go, the ability to access the course from any device is a major asset.

4. Candy Miles-Crocker

Key Facts

Newbies are welcome at Candy Miles Crocker’s program. Known as the “Real Life Realtor,” she’s the brain behind Real Life Real Estate Training. With a variety of courses in her offerings, including a plethora of self-paced online courses, Miles-Crocker gives new agents a leg-up on the rest.

What we love

Miles-Crocker is still an active agent, working with clients to close deals. Her 20+ years of experience practicing in Washington, D.C., Virginia and Maryland have helped her build “systems, strategies and scripts” that she shares with her coaching clients.

Pricing

The CORE Essentials Blueprint program retails for $1,597. Smaller, more specific courses, such as The Buyer Presentation, are priced at $347. While all pricing isn’t listed on her website, Miles-Crocker also offers a free course that includes her 6-point system for growth.

Who’s it Best For?

Miles-Crocker’s courses could be beneficial if you are new to agent life or looking to get your business reorganized. She even has one specifically for your first 30 days as a real estate agent.

5. Ashley Harwood

Key Facts

Boston-based Ashley Harwood inspires introverts with her convincing, heartfelt and high-touch approach to practicing real estate. Her very human, very relatable Move Over Extroverts coaching approach is the perfect antidote for cheerleader-style coaches that urge you to door-knock, chase down divorce leads or become a social media superstar.

What we love

Harwood is a licensed agent coaching agents week-in and week-out at no less than three Keller-Williams offices in the great Boston metro. We love her humanity, inspiring videos, and her latest enterpise — The Quiet Success Club. Inspired by Susan Cain’s New York Times bestseller Quiet, about the power of introverts, Harwood brings together a community of like-minded real estate agents wanting a more client-centric approach to succeeding as an agent.

Pricing

Join The Quiet Success Club for $45 per month (paid monthly) or get two months free when you pay for an annual subscription (for $450). The club is currently offering founding member pricing for $25 per month or $250, but it’s a limited-time offer available only under April 30, 2024. Or get a lifetime membership to Harwood’s suite of courses, called IntrovertU, for a one-time cost of $997.

Who’s it Best For?

Introverts, of course! While you may not count yourself as one, if you read Susan Cain’s book, you may unearth your more introverted traits — like recharging your battery by being alone. Ok, even if you don’t bask in solitude, Harwood promises a calming community where agents can be themselves, be seen, and where they don’t have to be the loudest voice in her mastermind group, purposefully (and quietly) designed to teach successful lead generation and other strategies.

6. Levi Lascsak

If you’re looking to improve your social media game, Levi Lascsak is the YouTube master. The author of Passive Prospecting specializes in helping real estate professionals embrace the video platform, and he does so in jam-packed, 2-day virtual events. Discover how he earned over $4 million in gross commission income as a new agent.

What we love

Lascsak’s social media marketing skills are top-of-the-line. While he may not be part of the traditional world of real estate coaching, Lascak’s ability to relate to younger audiences is an asset that Millennial and Gen Z agents might appreciate.

Pricing

The live, 2-day events are available at a discount for $47. But as you can expect, he’s got endless information available for free on YouTube.

Who’s it best for?

If you’re a digital native looking to pack a bunch of education into a short period, a Lascsak course is particularly beneficial.

7. Jess Lenouvel

Key Facts

Promising to help agents scale from six to seven figures, The Listings Lab founder Jess Lenouvel is the author of More Money, Less Hustle. A strong example of a coach with a significant understanding of social media, Lenouvel hosts vibrant live events that hype up the audience and prepare them to take their career to the next level.

What we Love

Lenouvel emphasizes the significant power of mindset to achieve one’s goals. She understands how quickly the market shifts and emphasizes staying on top of trends to succeed.

Lenouvel’s live events focus on messaging. For those looking to solidify their brand and develop a clear, concise message, her events might be what you need.

8. Buffini & Company

Key Facts

Another giant of the real estate coaching industry, Buffini & Company is one of the largest coaching and training companies in the United States. They have two major coaching programs: The Leadership Coaching program includes three monthly coaching calls, free admission to a 2-day conference, and curriculums and training led by Brian Buffini. There are also bi-monthly coaching sessions and a monthly web series with a live Q&A.

Buffini & Company also performs a REALstrengths profile — an in-depth personality assessment. In the One2One Coaching program, there are two coaching calls per month, a monthly marketing kit, the REALStrengths profile, and as with the SERHANT. program, Buffini features the Buffini Referral Network, allowing participants to send and receive referrals with other agents.

What We Love

Buffini coaches aren’t independent contractors. Instead, they’re full-time employees who go through intense training. Thus far, they’ve conducted 1.7 million coaching calls and more than one million hours of coaching.

Pricing

The Leadership Coaching program costs $1,499 a month. Private coaching, referred to as One2One Coaching, costs $549 per month. Two tiers of Referral Maker courses are available from $45 to $149 each per month.

Who’s it Best For?

Team spirit is the name of the game for Buffini’s Leadership Coaching program. If you’re a team leader looking to improve your coaching skills and assist your team in leveling up, the Leadership Coaching program might be right for you. If you want a more personalized path as a solo agent, the One2One Coaching program may be a better fit.

9. Vanda Martin

Key Facts

A popular name in the real estate coaching industry, Vanda Martin’s VIP Coaching Program follows three components: coaching, content, and community. Martin doesn’t shy away from mistakes – instead, she emphasizes avoiding indecision that puts you behind the pack.

What we love

Positive vibes are plentiful in Martin’s world, and her energy is tangible. Just check out her Instagram videos.

Pricing

Martin’s pricing isn’t listed.

Who’s it best for?

If you’re looking for a female leader who emphasizes loving your job and building habits that will take you to a greater level of success, Martin’s ability to convey those feelings is clear. Just check out the endless testimonials on her website.

9. Tat Londono

Key Facts

Tatiana Londono is the founder and CEO of Londono Realty Group Inc. The author of Real Estate Unfiltered, she offers a variety of programming that ranges from free templates to intensive coaching sessions. The Millionaire Realtor Membership provides weekly input from Londono, while the intensive Millionaire Real Estate Agent Coaching Program focuses on building 12-month objectives using a custom success action plan. It uses live programming and workshops with Londono herself, as well as an exclusive online community and referral network for members.

What we love

Londono’s keen sense of social media and her posts are a masterclass in how to boost your engagement on platforms like TikTok and Instagram. Don’t miss her takes on Taylor Swift’s real estate portfolio.

Londono’s programs specifically target agents who are looking to scale their business. If you’re struggling with lead generation or want to increase the number of views you’re racking up on social media, Londono is a valuable source within the industry.

10. Steve Shull

Key Facts

Steve Shull’s Performance Coaching focuses on using consistent execution to achieve your goals. With options ranging from 1:1 private coaching to small group coaching for 10 to 20 agents, the groups have 30-minute Zoom calls three times a day, but the number of sessions you choose to attend is up to you. Several self-directed courses are also available on the website, focusing on topics ranging from mindset to time blocking.

What we love

If you’re not positive you want to make the investment, Performance Coaching allows a 14-day free trial of daily accountability calls.

Pricing

Small group coaching costs $6,000 a year, and while 1:1 coaching prices aren’t listed online, you should prepare for a hefty price tag.

Who’s it Best For?

If you have a specific area you’re looking to improve upon, Performance Coaching offers coaches with unique areas of expertise, ranging from CRMs to business strategy. Tailoring your program to your greatest areas of weakness can help you become a more well-rounded agent.

11. Aaron Novello

Key Facts

Aaron Novello of Elite Real Estate Coaching has several programs tailor-made for agents looking to hone their craft. A Masterclass in Systems works to teach agents how to scale their real estate business, organize their team, and use programming like Follow Up Boss to manage their business.

The Role Play Mastermind is for agents looking to prepare themselves for tough discussions by working with a role-play partner for 15 to 30 minutes, five days a week. The group coaching option includes a variety of scripts Novello used to close on homes, as well as mindset guides, skill sheets, and expert guidance from experts in the field.

What we love

Novello’s exclusive accountability group allows active members and former coaching clients to share everything from guidance to motivation. If you’re looking to save money, Novello also has a free podcast available on YouTube.

If you struggle with having difficult conversations and are looking for solid templates to guide you, Novello’s Role Play Mastermind is a solid investment. The group coaching option emphasizes taking the educational portion and putting it into practice in the real world rather than just watching videos.

12. Krista Mashore Coaching

Key Facts

Filled with energy and known for popping up in the press, Krista Mashore is the mind behind Unstoppable Agent, her 3-day mastery class. It includes over 15 hours of coaching, group workshops, breakout sessions, and skill-building workshops to provide you with the skills to implement digital marketing successfully into your real estate business.

What we love

A positive attitude counts for a lot, and Mashore’s personality is a key component of the success of her course.

Pricing

Mashore’s accessibility is another one of her program’s best assets. Her 3-day class is currently priced at $47, but pricing occasionally varies.

Who’s it best for?

If you crave energy and enthusiasm, Krista Mashore has the goods. She’s also an expert on working in today’s low-inventory market, which is ideal for someone struggling with the current housing shortage. But she’s also got a good sense of humor, which shines through in her social media presence.

The full picture: The best real estate coaches for 2024

Hiring a top real estate coach goes far beyond just expanding your skills. While growing and educating yourself as you navigate your career is essential, hiring a coach is all about seeking to achieve more. Whether you’re looking to boost lead generation, build a solid personal brand, or make more commission income, having the input of a seasoned expert is a priceless step in the right direction. As you can see through the endless reviews and testimonials on coaches’ websites, agents who want to scale their business and take their profits to a higher level often seek the outside guidance of a coach. While the cost of hiring someone may be significant, the return on investment is equally as monumental.

Real estate coaching programs vary in price significantly. Most cost over $500 per month, with others charging several thousand dollars per month. “Oftentimes, it is the case that you get what you pay for,” said Kyle Scott, President of SERHANT. Ventures.

However, prices can also vary depending on the specific niche of real estate coaching you’re focusing on. The more specificity you’re seeking, the higher the financial investment. Of course, self-led courses are likely to cost much less.

Does your career feel stalled right now? Are you ready to take your career to the next level, but you’re not sure where to start? In a down market, you can channel your time and energy into actively improving your business skills so that you’ll be sufficiently prepared for when the market changes.

“When things pick up again, you’re ready to capture the climbing market,” says Scott. “If that’s the case, then the best time to embrace coaching is now. At the same time, a thriving market presents agents with new challenges, ranging from having to turn away business or being unable to service your existing business in a way you’re proud of,” Scott noted. “In that type of market, a real estate coach can help you determine what kind of junior agent or assistant would serve you best. How do I figure out how to manage my business in a way that I can keep up with the volume?”

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-March 2024

A brief excerpt: This 2-part overview for mid-March provides a snapshot of the current housing market.

This 2-part overview for mid-March provides a snapshot of the current housing market.

I always like to start with inventory, since inventory usually tells the tale!

...

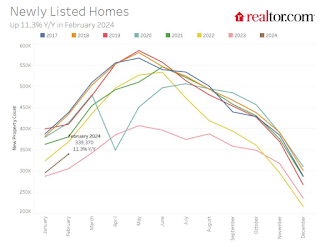

Here is a graph of new listing from Realtor.com’s February 2024 Monthly Housing Market Trends Report showing new listings were up 11.3% year-over-year in February. This is still well below pre-pandemic levels. From Realtor.com:

However, providing a boost to overall inventory, sellers turned out in higher numbers this February as newly listed homes were 11.3% above last year’s levels. This marked the fourth month of increasing listing activity after a 17-month streak of decline.

Note the seasonality for new listings. December and January are seasonally the weakest months of the year for new listings, followed by February and November. New listings will be up year-over-year in 2024, but we will have to wait for the March and April data to see how close new listings are to normal levels.

There are always people that need to sell due to the so-called 3 D’s: Death, Divorce, and Disease. Also, in certain times, some homeowners will need to sell due to unemployment or excessive debt (neither is much of an issue right now).

And there are homeowners who want to sell for a number of reasons: upsizing (more babies), downsizing, moving for a new job, or moving to a nicer home or location (move-up buyers). It is some of the “want to sell” group that has been locked in with the golden handcuffs over the last couple of years, since it is financially difficult to move when your current mortgage rate is around 3%, and your new mortgage rate will be in the 6 1/2% to 7% range.

But time is a factor for this “want to sell” group, and eventually some of them will take the plunge. That is probably why we are seeing more new listings now.

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45%…

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45% of US respondents in 2023, according to the latest Harris Poll data. That’s exactly the same as the previous year.

Pharma’s highest point was in February 2021 — as Covid vaccines began to roll out — with a 62% positive US perception, and helping the industry land at an average 55% positive sentiment at the end of the year in Harris’ 2021 annual assessment of industries. The pharma industry’s reputation hit its most recent low at 32% in 2019, but it had hovered around 30% for more than a decade prior.

Rob Jekielek

“Pharma has sustained a lot of the gains, now basically one and half times higher than pre-Covid,” said Harris Poll managing director Rob Jekielek. “There is a question mark around how sustained it will be, but right now it feels like a new normal.”

The Harris survey spans 11 global markets and covers 13 industries. Pharma perception is even better abroad, with an average 58% of respondents notching favorable sentiments in 2023, just a slight slip from 60% in each of the two previous years.

Pharma’s solid global reputation puts it in the middle of the pack among international industries, ranking higher than government at 37% positive, insurance at 48%, financial services at 51% and health insurance at 52%. Pharma ranks just behind automotive (62%), manufacturing (63%) and consumer products (63%), although it lags behind leading industries like tech at 75% positive in the first spot, followed by grocery at 67%.

The bright spotlight on the pharma industry during Covid vaccine and drug development boosted its reputation, but Jekielek said there’s maybe an argument to be made that pharma is continuing to develop innovative drugs outside that spotlight.

“When you look at pharma reputation during Covid, you have clear sense of a very dynamic industry working very quickly and getting therapies and products to market. If you’re looking at things happening now, you could argue that pharma still probably doesn’t get enough credit for its advances, for example, in oncology treatments,” he said.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.