Fed Losing Control As Consumers’ Inflation Expectations Hit New All Time High

Fed Losing Control As Consumers’ Inflation Expectations Hit New All Time High

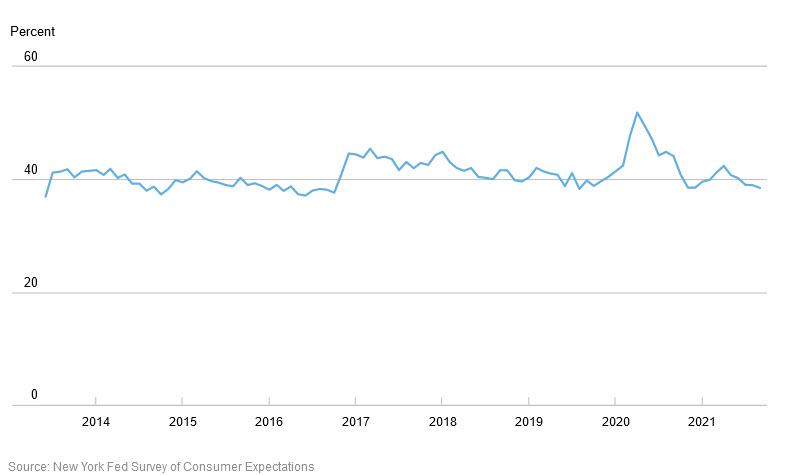

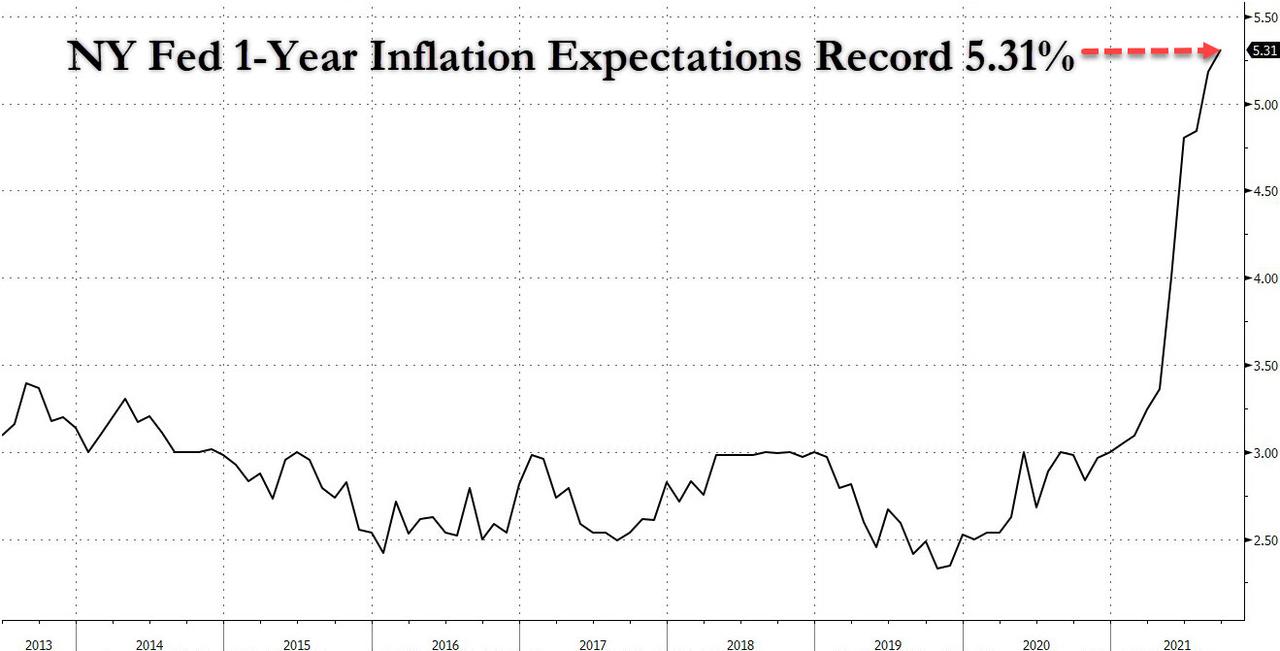

Another month, another record high in consumer inflation expectations.

While central banks, tenured economists and the financial media are doing everything in…

Share this:

Another month, another record high in consumer inflation expectations.

While central banks, tenured economists and the financial media are doing everything in their propaganda power to convince ordinary Americans (who don't have the privilege of charging their Federal Reserve debit card when shopping at the grocery store) that the current phase of galloping inflation - to avoid the far more dreaded "h" word - is merely transitory, the shocking reality on the ground is that the Fed has effectively lost control over near-term inflation expectations, as the NY Fed's latest survey of consumer expectations reveals.

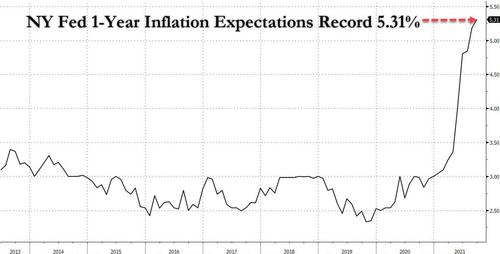

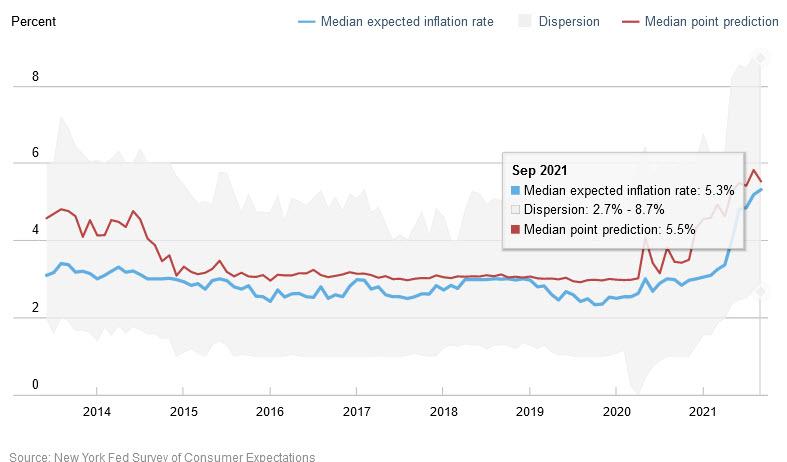

According to the September installment of this closely watched survey, consumer inflation expectations for one year ahead hit a fresh all-time high for this series of 5.31, up from 5.18 in August. "Median short-term (one-year-ahead) inflation expectations increased by 0.1 percentage point in September to 5.3%, the eleventh consecutive monthly increase and a new series high since the inception of the survey in 2013" the NY Fed said without a trace of irony even as its economists plead with the public that this spike will last at most a few more months, hence "transitory."

But while the median 1 Year expected inflation rate was a "modest" 5.3%, the upper end of the 25%/75% dispersion range was a mindblowing 8.7%, meaning that at least 25% of respondents see inflation surging to nearly double digits!

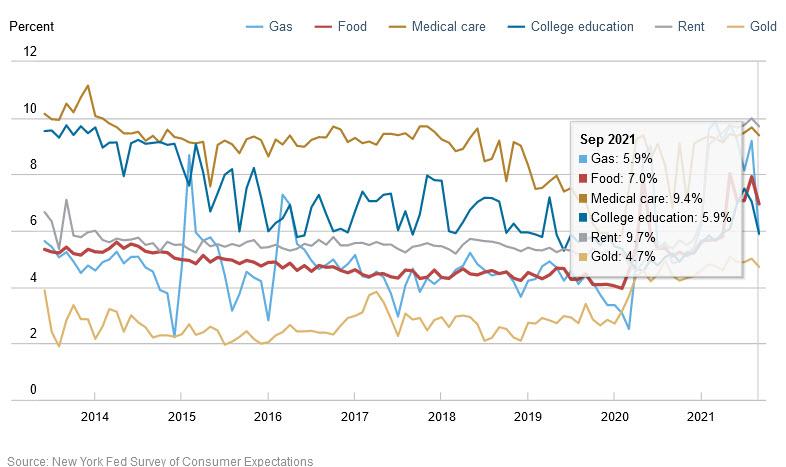

The Fed survey showed that Americans are expecting higher rates of price increases for virtually all items, like rent and food, that make up a big chunk of the consumer-price basket, and can’t be substituted. Looking at a breakdown of inflation expectations by component, over the next year consumers expect gasoline prices to rise 5.9% (expect this number to surge with oil hitting a 7 year high); food prices to rise 7%; the price of a college education to rise 5.9%; rent prices to rise 9.7%; medical care to increase by 9.4%. Curiously, the price of gold is expected to rise 4.7% (down from 5.0% last month) after being in the 2% range for much of the past decade.

There were a few silver linings: expectations that wages will keep pace with the acceleration in prices reversed from last month's drop, and the median one-year-ahead expectation for earnings growth rose 0.4 percentage point to 2.9%, reversing the August drop, with respondents over the age of 40 largely driving the decline. There was a modest improvement in labor market conditions too, with the mean perceived probability of losing one’s job in the next 12 months decreased from 12.45% to 11.09%.

Going back to inflation, unfortunately it was not just 1-year expectations that hit new all time highs: consumers' median inflation expectations for the three-year horizon also jerked higher with the median 3-Year inflation expectation surging to 4.19% from 4.0% in August, which was also the highest reading in series history!

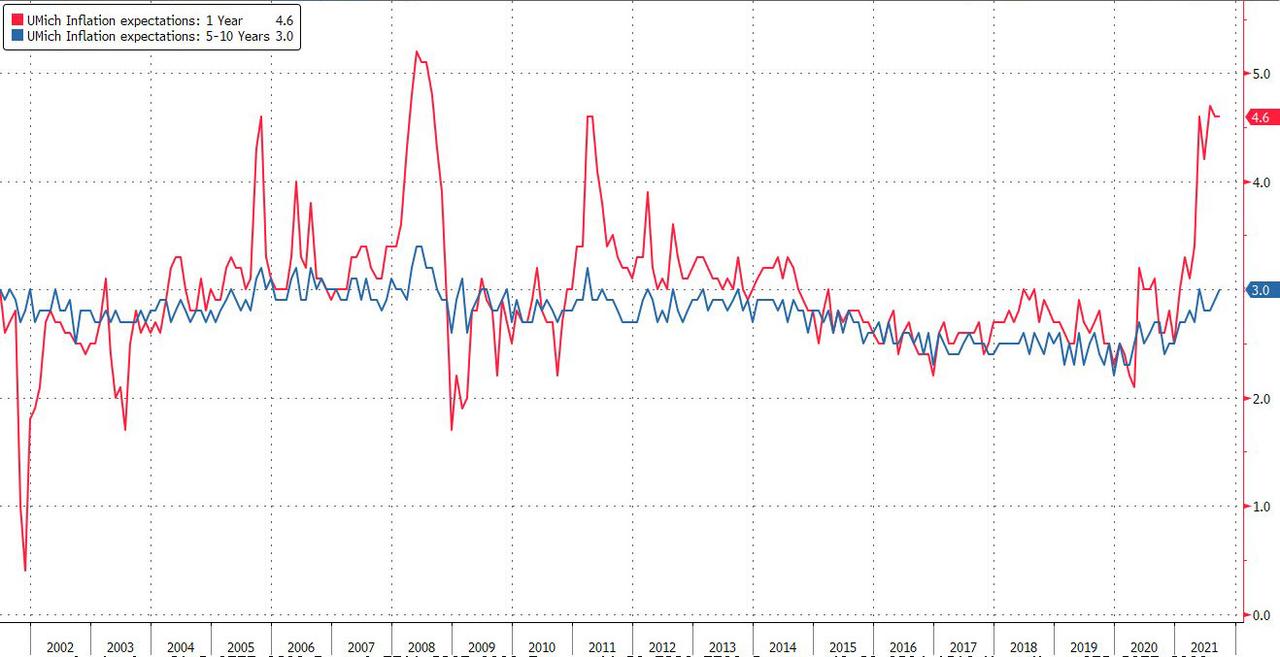

Remarkably, both the Fed's 1-Year and 3-Year inflation expectations are now above those observed most recently in the UMich consumer sentiment survey, where the 1Y expectations were flat at 4.6% while the 5-10 inflation expectations rose to 3.0%. Expect both numbers to rise in coming months.

Well aware that it would get substantial criticism for deanchoring inflation expectations - as the charts above clearly show - the report authors write that inflation expectations remain "anchored." How do they reconcilte this ludicrous claim with the data which is clearly showing that expectations are anything but anchored through 3 years ahead? Simple: by moving the goal posts of course: "longer-term (5-year ahead) inflation expectations still appear to be as well anchored as they were two years ago, before the start of the pandemic."

In other words, yes, inflation will surge for 3 years, probably 4, but on year 4 at end of the 12th month, all shall be well, and 5 year inflation will be back to normal. Said otherwise, we may have soaring inflation but it's only for the next 5 years.

We doubt this will be a comfort to anyone except those who can use their Fed debit card to charge all purchases for the next 5 years.

Some other observations from the report:

- Median year-ahead home price change expectations decreased by 0.4 percentage point in September to 5.5%, the fourth consecutive monthly decrease. The decrease was driven mostly by respondents who live in the “West” and “Northeast” Census regions.

- Expectations about year-ahead price changes decreased for all the commodities considered in the survey. The median one-year-ahead expected change in the price of gas decreased sharply from 9.2% to 5.9%. The median one-year-ahead expected change in the cost of a college education and in the price of food decreased by 1.1 and 0.9 percentage points, to 5.9% and 7.0%, respectively. Finally, the median one-year-ahead expected change in the cost of medical care and in the cost of rent each fell 0.3 percentage point to 9.4% and 9.7%, respectively.

Labor Market

- Median one-year-ahead expected earnings growth rebounded in September, increasing 0.4 percentage point to 2.9%, substantially above its 12-month trailing average of 2.2%. The decrease was driven mostly by respondents over the age of 40 and respondents without a bachelor’s degree.

- Mean unemployment expectations—or the mean probability that the U.S. unemployment rate will be higher one year from now—increased 0.8 percentage point to 35.8%, slightly above its 12-month trailing average of 35.7%.

- The mean perceived probability of losing one’s job in the next 12 months decreased from 12.5% to 11.1%. The decrease was more pronounced among respondents below the age of 40 and those with less than $50,000 in household income. The mean probability of leaving one’s job voluntarily in the next 12 months also decreased, from 20.0% to 18.9%. The decrease was more pronounced among respondents above the age of 60, those with no more than a high school diploma, and those with more than $100,000 in household income.

- The mean perceived probability of finding a job (if one’s current job was lost) rose to 55.2% from 54.9% in August. Despite the increase, the September reading remains below its pre-pandemic levels.

Household Finance

- The median expected growth in household income remained unchanged at its series high of 3.0% in September.

- The median household spending growth expectations was unchanged at 5.0%, remaining above its 12-month trailing average of 4.3%.

- Perceptions of credit access compared to a year ago were mixed, with fewer respondents finding it easier to obtain credit now than a year ago, but also fewer respondents finding it harder to obtain credit now than a year ago. Similarly, expectations about future credit availability were mixed, with fewer respondents expecting it will be easier or harder to obtain credit in the year ahead.

- The average perceived probability of missing a minimum debt payment over the next three months increased by 0.3 percentage point to 9.9%, but remains just below its 12-month trailing average of 10.1%.

- The median expectation regarding a year-ahead change in taxes (at current income level) decreased by 0.3 percentage point to 4.3%.

- Median year-ahead expected growth in government debt decreased to 14.4%, from 15.1% in August.

- The mean perceived probability that the average interest rate on saving accounts will be higher 12 months from now decreased to 27.3%, from 27.4% in August.

- Perceptions about households’ current financial situations compared to a year ago deteriorated slightly, with more respondents reporting being financially worse off than they were a year ago. In contrast, respondents were more optimistic about their households’ financial situations in the year ahead, with more respondents expecting their financial situation to improve a year from now.

- The mean perceived probability that U.S. stock prices will be higher 12 months from now decreased by 0.5 percentage points to 38.5%.

Finally, one for the market: perhaps sensing that risk-killing stagflation pressures are rising, the mean perceived probability that U.S. stock prices will be higher 12 months from now dropped again to 3.85%, from 39.0%, tied for the lowest in 2021.

Source: NY Fed

Spread & Containment

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now…

Share this:

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

{kind=link}

{kind=link}

{kind=link}

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemployment

Walmart launches clever answer to Target’s new membership program

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Wendy’s has a new deal for daylight savings time haters

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Catastrophic Risk: Investing and Business Implications

When Military Rule Supplants Democracy

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Redefining Poverty: Towards a Transpartisan Approach

The Digest #187

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 day ago

Walmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges