Farmer Mac Reports Second Quarter 2022 Results

Farmer Mac Reports Second Quarter 2022 Results

PR Newswire

WASHINGTON, Aug. 8, 2022

– Outstanding Business Volume of $24.5 Billion –

WASHINGTON, Aug. 8, 2022 /PRNewswire/ — The Federal Agricultural Mortgage Corporation (Farmer Mac; NYSE: AGM and …

Share this:

Farmer Mac Reports Second Quarter 2022 Results

PR Newswire

WASHINGTON, Aug. 8, 2022

- Outstanding Business Volume of $24.5 Billion -

WASHINGTON, Aug. 8, 2022 /PRNewswire/ -- The Federal Agricultural Mortgage Corporation (Farmer Mac; NYSE: AGM and AGM.A), the nation's secondary market provider that increases the availability and affordability of credit for the benefit of rural America, today announced its results for the fiscal quarter ended June 30, 2022.

Second Quarter 2022 Highlights

- Added $1.9 billion of gross business volume, resulting in net growth of $236.0 million

- Net interest income grew $14.3 million year-over-year to $69.4 million

- Net effective spread1 increased 8% from the prior-year period to $60.9 million

- Net income attributable to common stockholders of $39.1 million compared to $25.4 million in second quarter 2021

- Core earnings1 grew 3% year-over-year to $30.7 million, or $2.83 per diluted common share

- 90-day delinquencies were 0.08% across the entire $24.5 billion portfolio as of June 30, 2022

"Farmer Mac delivered another quarter of strong results, generating record core earnings and demonstrating the consistency of our fundamental business model as we continue to successfully execute against our multi-year growth plan," said President & Chief Executive Officer, Brad Nordholm. "These results are again noteworthy given the current economic and market backdrop, where inflationary pressures have created heightened uncertainty across credit markets and high volatility across a broad range of prices, including key agricultural commodities. Our continued strong credit quality, solid capital position, and growing execution capability has enabled Farmer Mac to consistently deliver on our mission to bring even greater efficiencies, and lower costs, in providing financing to lenders for the benefit of their farm and ranch, agribusiness, and rural infrastructure customers. We remain confident in our ability to navigate the current environment and make the necessary investments in our infrastructure to pursue strategic growth opportunities."

_______________

1 Non-GAAP Measure

$ in thousands, except per share amounts | Quarter Ended | ||||

Jun. 30, 2022 | Mar. 31, 2022 | Jun. 30, 2021 | Sequential | YoY | |

Net Change in Business Volume | $235,981 | $628,947 | $334,630 | N/A | N/A |

Net Interest Income (GAAP) | $69,402 | $61,875 | $55,129 | 12 % | 26 % |

Net Effective Spread (Non-GAAP) | $60,946 | $57,839 | $56,551 | 5 % | 8 % |

Diluted EPS (GAAP) | $3.60 | $3.77 | $2.35 | (5) % | 53 % |

Core EPS (Non-GAAP) | $2.83 | $2.37 | $2.77 | 19 % | 2 % |

Second Quarter 2022 Results

Spreads

Net interest income for second quarter 2022 was $69.4 million, a $14.3 million increase compared to $55.1 million in the prior-year period, primarily due to a $7.8 million increase in the fair value of designated financial derivatives, a $4.3 million increase from net new business volume, and a $2.5 million decrease in funding costs. Net interest yield was 1.09% in second quarter 2022 compared to 0.94% in the prior-year period.

Net effective spread, a non-GAAP measure, for second quarter 2022 was $60.9 million, a $4.4 million increase from $56.6 million in the prior-year period. The $4.4 million year-over-year increase in net effective spread was primarily due to a $4.8 million increase from net new business volume, a $0.9 million increase in net coupon yields related to the acquisition of loan servicing rights, and a $0.4 million increase in cash-basis interest income. These factors were partially offset by a $1.4 million increase in non-GAAP funding costs. In percentage terms, net effective spread was 0.99% in second quarter 2022, compared to 1.01% in the prior-year period.

Earnings

Farmer Mac's net income attributable to common stockholders for second quarter 2022 was $39.1 million ($3.60 per diluted common share), compared to $25.4 million ($2.35 per diluted common share) in the prior-year period. The $13.7 million year-over-year increase in net income attributable to common stockholders was due to a $11.3 million after-tax increase in net interest income, a $5.1 million after-tax increase in the fair value of undesignated financial derivatives, and an increase in our release of credit losses of $0.4 million after tax. These factors were partially offset by a $2.5 million after-tax increase in operating expenses and a $0.9 million increase in preferred stock dividends.

Farmer Mac enters into financial derivatives transactions to hedge interest rate risks inherent in its business and carries its financial derivatives at fair value in its consolidated financial statements. The fair value fluctuations of these financial derivatives are not expected to have a cumulative net impact on Farmer Mac's financial condition or results of operations reported with GAAP if the derivatives are held to maturity, as is expected. Therefore, Farmer Mac uses core earnings, a non-GAAP measure that excludes the effects of fair value fluctuations, as a useful alternative measure to understand the business.

Farmer Mac's core earnings for second quarter 2022 were $30.7 million ($2.83 per diluted common share), compared to $30.0 million ($2.77 per diluted common share) in second quarter 2021. The $0.8 million year-over-year increase in core earnings was due to a $3.5 million after-tax increase in net effective spread and an increase in our release of credit losses of $0.4 million after tax. These factors were partially offset by a $2.5 million after-tax increase in operating expenses and a $0.9 million increase in preferred stock dividends.

Business Volume

Farmer Mac's outstanding business volume was $24.5 billion as of June 30, 2022, a net increase of $0.2 billion from March 31, 2022 after taking into account all new business, maturities, sales, and paydowns on existing assets. The net increase was primarily attributable to net increases of $193.0 million in the Rural Infrastructure Finance line of business and $43.0 million in the Agricultural Finance line of business.

The $16.4 million net increase in Farm & Ranch during second quarter 2022 resulted from $1.4 billion of new purchases, commitments, and guarantees, mostly offset by $1.4 billion of scheduled maturities and repayments. Farmer Mac purchased a total of $432.6 million in loans, which was primarily driven by improved borrower economics as well as a competitive, albeit an increasing interest rate environment resulting in demand for intermediate and long-term financing solutions. The $432.6 million in gross Farm & Ranch loan purchases was partially offset by $153.8 million in scheduled maturities and repayments.

Farmer Mac also purchased a total of $0.8 billion in Farm & Ranch AgVantage Securities during second quarter 2022, which primarily reflected the refinancing of maturing securities as well as financial counterparties seeking to add longer term AgVantage securities to manage their asset-liability maturity profile given recent increases in credit spreads and interest rates. The $0.8 billion in gross purchases was more than offset by $1.0 billion in scheduled maturities. Approximately $0.3 billion of the total $0.8 billion in gross purchases reflected purchases that refinanced maturing AgVantage securities and were issued at short-term tenors, which may create some volatility in AgVantage volumes throughout the year.

The $26.6 million net increase in Corporate AgFinance during second quarter 2022 resulted from $107.9 million of new loan purchases, which was offset by $81.4 million of scheduled maturities, repayments, and sales. Farmer Mac purchased a total of $85.4 million in loans, which was offset by $44.3 million in scheduled maturities, repayments, and sales. This net increase in loans was primarily due to Farmer Mac's continued focus to support loans to larger and more complex agribusinesses focused on food and fiber processing, and other supply chain production.

The $165.6 million net increase in Rural Utilities during second quarter 2022 resulted from $326.9 million of new purchases, commitments, and guarantees, which was partially offset by $161.3 million of scheduled maturities and repayments. Farmer Mac purchased a total of $196.5 million in Rural Utilities loans; electric distribution and generation and transmission comprised $161.5 million and telecommunication comprised $35.0 million, which was fueled by a competitive but increasing interest rate environment resulting in demand for long-term financing solutions for planned maintenance and capital expenditures. The $196.5 million in loan purchases was partially offset by $24.4 million in scheduled maturities and repayments.

The $27.4 million net increase in Renewable Energy during second quarter 2022 primarily reflects $35.3 million in loan purchases, partially offset by $7.9 million in repayments.

Credit

As of June 30, 2022, the total allowance for losses was $14.8 million, compared to $16.3 million as of March 31, 2022. The $1.5 million release from the total allowance for losses in second quarter 2022 was comprised of a $1.2 million release from the Rural Infrastructure Finance portfolio and a $0.3 million release from the allowance for the Agricultural Finance portfolio. The $1.2 million release from the allowance for the Rural Infrastructure portfolio was primarily attributable to updated credit loss model forecast assumptions and improvements in risk ratings. The $0.3 million release from the allowance for the Agricultural Finance mortgage loan portfolio was primarily due to a risk rating upgrade on an AgVantage counterparty.

As of June 30, 2022, Farmer Mac's 90-day delinquencies were $20.6 million (0.20% of the Agricultural Finance Mortgage Loan portfolio), compared to $63.1 million (0.70% of the Agricultural Finance Mortgage Loan portfolio) as of June 30, 2021. Across all of Farmer Mac's lines of business, 90-day delinquencies represented 0.08% of total outstanding business volume as of June 30, 2022, compared to 0.28% as of June 30, 2021.

Capital

As of June 30, 2022, Farmer Mac's core capital level was $1.3 billion, $506.3 million above the minimum capital level required by the company's statutory charter. Farmer Mac's Tier 1 capital ratio was 14.7% as of June 30, 2022.

Earnings Conference Call Information

The conference call to discuss Farmer Mac's second quarter 2022 financial results will be held beginning at 4:30 p.m. eastern time on Monday, August 8, 2022, and can be accessed by telephone or live webcast as follows:

Telephone (Domestic): (888) 346-2616

Telephone (International): (412) 902-4254

Webcast: https://www.farmermac.com/investors/events-presentations/

When dialing in to the call, please ask for the "Farmer Mac Earnings Conference Call." The call can be heard live and will also be available for replay on Farmer Mac's website for two weeks following the conclusion of the call.

More complete information about Farmer Mac's performance for second quarter 2022 is in Farmer Mac's Quarterly Report on Form 10-Q for the quarter ended June 30, 2022 filed today with the SEC.

Use of Non-GAAP Measures

In the accompanying analysis of its financial information, Farmer Mac uses the following non-GAAP measures: "core earnings," "core earnings per share," and "net effective spread." Farmer Mac uses these non-GAAP measures to measure corporate economic performance and develop financial plans because, in management's view, they are useful alternative measures in understanding Farmer Mac's economic performance, transaction economics, and business trends. The non-GAAP financial measures that Farmer Mac uses may not be comparable to similarly labeled non-GAAP financial measures disclosed by other companies. Farmer Mac's disclosure of these non-GAAP measures is intended to be supplemental in nature and is not meant to be considered in isolation from, as a substitute for, or as more important than, the related financial information prepared in accordance with GAAP.

Core earnings and core earnings per share principally differ from net income attributable to common stockholders and earnings per common share, respectively, by excluding the effects of fair value fluctuations. These fluctuations are not expected to have a cumulative net impact on Farmer Mac's financial condition or results of operations reported in accordance with GAAP if the related financial instruments are held to maturity, as is expected.

Core earnings and core earnings per share also differ from net income attributable to common stockholders and earnings per common share, respectively, by excluding specified infrequent or unusual transactions that Farmer Mac believes are not indicative of future operating results and that may not reflect the trends and economic financial performance of Farmer Mac's core business. For example, we have excluded from core earnings losses on retirement of preferred stock and the re-measurement of the deferred tax asset.

Farmer Mac uses net effective spread to measure the net spread Farmer Mac earns between its interest-earning assets and the related net funding costs of these assets. Net effective spread differs from net interest income and net interest yield because it excludes: (1) the amortization of premiums and discounts on assets consolidated at fair value that are amortized as adjustments to yield in interest income over the contractual or estimated remaining lives of the underlying assets; (2) interest income and interest expense related to consolidated trusts with beneficial interests owned by third parties, which are presented on Farmer Mac's consolidated balance sheets as "Loans held for investment in consolidated trusts, at amortized cost"; and (3) the fair value changes of financial derivatives and the corresponding assets or liabilities designated in a fair value hedge accounting relationship.

Net effective spread also principally differs from net interest income and net interest yield because it includes: (1) the accrual of income and expense related to the contractual amounts due on financial derivatives that are not designated in hedge accounting relationships ("undesignated financial derivatives"); and (2) the net effects of terminations or net settlements on financial derivatives. More information about Farmer Mac's use of non-GAAP measures is available in "Management's Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations" in Farmer Mac's Annual Report on Form 10-K for the year ended December 31, 2021, filed February 28, 2022 with the SEC.

For a reconciliation of Farmer Mac's net income attributable to common stockholders to core earnings and of earnings per common share to core earnings per share, and net interest income and net interest yield to net effective spread, see "Reconciliations" below.

Forward-Looking Statements

Management's expectations for Farmer Mac's future necessarily involve assumptions and estimates and the evaluation of risks and uncertainties. Various factors or events, both known and unknown, could cause Farmer Mac's actual results to differ materially from the expectations as expressed or implied by the forward-looking statements in this release, including uncertainties about:

- the availability to Farmer Mac of debt and equity financing and, if available, the reasonableness of rates and terms;

- legislative or regulatory developments that could affect Farmer Mac, its sources of business, or agricultural or rural infrastructure industries;

- fluctuations in the fair value of assets held by Farmer Mac and its subsidiaries;

- the level of lender interest in Farmer Mac's products and the secondary market provided by Farmer Mac;

- the general rate of growth in agricultural mortgage and rural utilities indebtedness;

- the effect of economic conditions and geopolitics on agricultural mortgage or rural utilities lending, borrower repayment capacity, or collateral values, including fluctuations in interest rates, changes in U.S. trade policies, fluctuations in export demand for U.S. agricultural products, supply chain disruptions, increases in input costs, labor availability, volatility in commodity prices, and the effects of the conflict between Russia and Ukraine;

- the degree to which Farmer Mac is exposed to interest rate risk resulting from fluctuations in Farmer Mac's borrowing costs relative to market indexes;

- developments in the financial markets, including possible investor, analyst, and rating agency reactions to events involving government-sponsored enterprises, including Farmer Mac;

- the effects of the Federal Reserve's efforts to achieve monetary policy normalization and slow inflation;

- other factors that could hinder agricultural mortgage lending or borrower repayment capacity, including the effects of severe weather and drought, climate change, or fluctuations in agricultural real estate values; and

- the duration, mitigation efforts, spread, severity, and social and economic disruption of the ongoing COVID-19 pandemic and its effects on the business operations of agricultural and rural borrowers, the capital markets, and Farmer Mac's business operations.

Other risk factors are discussed in "Risk Factors" in Part I, Item 1A in Farmer Mac's Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the SEC on February 28, 2022. Considering these potential risks and uncertainties, no undue reliance should be placed on any forward-looking statements expressed in this release. The forward-looking statements contained in this release represent management's expectations as of the date of this release. Farmer Mac undertakes no obligation to release publicly the results of revisions to any forward-looking statements included in this release to reflect new information or any future events or circumstances, except as otherwise required by applicable law. The information in this release is not necessarily indicative of future results.

About Farmer Mac

Farmer Mac is a vital part of the agricultural credit markets and was created to increase access to and reduce the cost of credit for the benefit of American agricultural and rural communities. As the nation's secondary market for agricultural credit, we provide financial solutions to a broad spectrum of the agricultural community, including agricultural lenders, agribusinesses, and other institutions that can benefit from access to flexible, low-cost financing and risk management tools. Farmer Mac's customers benefit from our low cost of funds, low overhead costs, and high operational efficiency. More information about Farmer Mac (including the Annual Report on Form 10-K referenced above) is available on Farmer Mac's website at www.farmermac.com.

* * * *

FEDERAL AGRICULTURAL MORTGAGE CORPORATION AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS (unaudited) | |||

As of | |||

June 30, 2022 | December 31, 2021 | ||

(in thousands) | |||

Assets: | |||

Cash and cash equivalents | $ 909,430 | $ 908,785 | |

Investment securities: | |||

Available-for-sale, at fair value (amortized cost of $4,354,855 and $3,834,714, respectively) | 4,246,012 | 3,836,391 | |

Held-to-maturity, at amortized cost | 45,032 | 44,970 | |

Other investments | 1,537 | 1,229 | |

Total Investment Securities | 4,292,581 | 3,882,590 | |

Farmer Mac Guaranteed Securities: | |||

Available-for-sale, at fair value (amortized cost of $6,679,196 and $6,135,807, respectively) | 6,450,212 | 6,328,559 | |

Held-to-maturity, at amortized cost | 1,689,469 | 2,033,239 | |

Total Farmer Mac Guaranteed Securities | 8,139,681 | 8,361,798 | |

USDA Securities: | |||

Trading, at fair value | 2,275 | 4,401 | |

Held-to-maturity, at amortized cost | 2,430,830 | 2,436,331 | |

Total USDA Securities | 2,433,105 | 2,440,732 | |

Loans: | |||

Loans held for investment, at amortized cost | 8,911,475 | 8,314,096 | |

Loans held for investment in consolidated trusts, at amortized cost | 834,941 | 948,623 | |

Allowance for losses | (12,403) | (14,041) | |

Total loans, net of allowance | 9,734,013 | 9,248,678 | |

Financial derivatives, at fair value | 30,011 | 19,139 | |

Interest receivable (includes $7,664 and $10,418, respectively, related to consolidated trusts) | 177,956 | 177,355 | |

Guarantee and commitment fees receivable | 44,388 | 45,538 | |

Deferred tax asset, net | 25,971 | 15,558 | |

Prepaid expenses and other assets | 129,267 | 45,318 | |

Total Assets | $ 25,916,403 | $ 25,145,491 | |

Liabilities and Equity: | |||

Liabilities: | |||

Notes payable | $ 23,474,095 | $ 22,716,156 | |

Debt securities of consolidated trusts held by third parties | 866,107 | 981,379 | |

Financial derivatives, at fair value | 127,983 | 34,248 | |

Accrued interest payable (includes $6,753 and $9,619, respectively, related to consolidated trusts) | 93,823 | 83,992 | |

Guarantee and commitment obligation | 42,990 | 43,926 | |

Accounts payable and accrued expenses | 97,380 | 79,427 | |

Reserve for losses | 1,677 | 1,950 | |

Total Liabilities | 24,704,055 | 23,941,078 | |

Commitments and Contingencies | |||

Equity: | |||

Preferred stock: | |||

Series C, par value $25 per share, 3,000,000 shares authorized, issued and outstanding | 73,382 | 73,382 | |

Series D, par value $25 per share, 4,000,000 shares authorized, issued and outstanding | 96,659 | 96,659 | |

Series E, par value $25 per share, 3,180,000 shares authorized, issued and outstanding | 77,003 | 77,003 | |

Series F, par value $25 per share, 4,800,000 shares authorized, issued and outstanding | 116,160 | 116,160 | |

Series G, par value $25 per share, 5,000,000 shares authorized, issued and outstanding | 121,327 | 121,327 | |

Common stock: | |||

Class A Voting, $1 par value, no maximum authorization, 1,030,780 shares outstanding | 1,031 | 1,031 | |

Class B Voting, $1 par value, no maximum authorization, 500,301 shares outstanding | 500 | 500 | |

Class C Non-Voting, $1 par value, no maximum authorization, 9,265,842 shares and 9,235,205 shares outstanding, respectively | 9,266 | 9,235 | |

Additional paid-in capital | 127,569 | 125,993 | |

Accumulated other comprehensive (loss)/income, net of tax | (49,484) | 3,853 | |

Retained earnings | 638,935 | 579,270 | |

Total Equity | 1,212,348 | 1,204,413 | |

Total Liabilities and Equity | $ 25,916,403 | $ 25,145,491 | |

FEDERAL AGRICULTURAL MORTGAGE CORPORATION AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF OPERATIONS (unaudited) | |||||||

For the Three Months Ended | For the Six Months Ended | ||||||

June 30, 2022 | June 30, 2021 | June 30, 2022 | June 30, 2021 | ||||

(in thousands, except per share amounts) | |||||||

Interest income: | |||||||

Investments and cash equivalents | $ 11,200 | $ 4,457 | $ 16,916 | $ 9,986 | |||

Farmer Mac Guaranteed Securities and USDA Securities | 57,104 | 42,414 | 96,361 | 84,818 | |||

Loans | 76,632 | 60,214 | 143,879 | 119,708 | |||

Total interest income | 144,936 | 107,085 | 257,156 | 214,512 | |||

Total interest expense | 75,534 | 51,956 | 125,879 | 106,132 | |||

Net interest income | 69,402 | 55,129 | 131,277 | 108,380 | |||

Release of/(provision for) losses | 1,372 | 761 | 1,316 | (152) | |||

Net interest income after release of/(provision for) losses | 70,774 | 55,890 | 132,593 | 108,228 | |||

Non-interest income/(expense): | |||||||

Guarantee and commitment fees | 3,213 | 2,997 | 6,908 | 6,027 | |||

Gains/(losses) on financial derivatives | 3,418 | (3,066) | 19,492 | 1,227 | |||

Gains/(losses) on trading securities | 29 | (62) | (34) | (75) | |||

Release of reserve for losses | 163 | 222 | 273 | 1,166 | |||

Other income | 479 | 435 | 1,154 | 1,018 | |||

Non-interest income | 7,302 | 526 | 27,793 | 9,363 | |||

Operating expenses: | |||||||

Compensation and employee benefits | 11,715 | 9,779 | 25,013 | 21,574 | |||

General and administrative | 7,520 | 6,349 | 14,798 | 12,685 | |||

Regulatory fees | 813 | 750 | 1,625 | 1,500 | |||

Operating expenses | 20,048 | 16,878 | 41,436 | 35,759 | |||

Income before income taxes | 58,028 | 39,538 | 118,950 | 81,832 | |||

Income tax expense | 12,132 | 8,252 | 25,217 | 17,319 | |||

Net income | 45,896 | 31,286 | 93,733 | 64,513 | |||

Preferred stock dividends | (6,792) | (5,842) | (13,583) | (11,111) | |||

Net income attributable to common stockholders | $ 39,104 | $ 25,444 | $ 80,150 | $ 53,402 | |||

Earnings per common share: | |||||||

Basic earnings per common share | $ 3.62 | $ 2.36 | $ 7.43 | $ 4.96 | |||

Diluted earnings per common share | $ 3.60 | $ 2.35 | $ 7.37 | $ 4.93 | |||

Reconciliations

Reconciliations of Farmer Mac's net income attributable to common stockholders to core earnings and core earnings per share are presented in the following tables along with information about the composition of core earnings for the periods indicated:

Reconciliation of Net Income Attributable to Common Stockholders to Core Earnings | |||||

For the Three Months Ended | |||||

June 30, 2022 | March 31, 2022 | June 30, 2021 | |||

(in thousands, except per share amounts) | |||||

Net income attributable to common stockholders | $ 39,104 | $ 41,046 | $ 25,444 | ||

Less reconciling items: | |||||

Gains/(losses) on undesignated financial derivatives due to fair value changes | 2,473 | 1,698 | (3,721) | ||

Gains/(losses) on hedging activities due to fair value changes | 5,916 | 2,024 | (2,097) | ||

Unrealized (losses)/gains on trading assets | (285) | 94 | (61) | ||

Net effects of amortization of premiums/discounts and deferred gains on assets consolidated at fair value | (62) | 20 | 20 | ||

Net effects of terminations or net settlements on financial derivatives | 2,536 | 15,512 | 109 | ||

Income tax effect related to reconciling items | (2,222) | (4,063) | 1,208 | ||

Sub-total | 8,356 | 15,285 | (4,542) | ||

Core earnings | $ 30,748 | $ 25,761 | $ 29,986 | ||

Composition of Core Earnings: | |||||

Revenues: | |||||

Net effective spread(1) | $ 60,946 | $ 57,839 | $ 56,551 | ||

Guarantee and commitment fees(2) | 4,709 | 4,557 | 4,334 | ||

Other(3) | 307 | 514 | 301 | ||

Total revenues | 65,962 | 62,910 | 61,186 | ||

Credit related expense (GAAP): | |||||

Release of losses | (1,535) | (54) | (983) | ||

Total credit related expense | (1,535) | (54) | (983) | ||

Operating expenses (GAAP): | |||||

Compensation and employee benefits | 11,715 | 13,298 | 9,779 | ||

General and administrative | 7,520 | 7,278 | 6,349 | ||

Regulatory fees | 813 | 812 | 750 | ||

Total operating expenses | 20,048 | 21,388 | 16,878 | ||

Net earnings | 47,449 | 41,576 | 45,291 | ||

Income tax expense(4) | 9,909 | 9,024 | 9,463 | ||

Preferred stock dividends (GAAP) | 6,792 | 6,791 | 5,842 | ||

Core earnings | $ 30,748 | $ 25,761 | $ 29,986 | ||

Core earnings per share: | |||||

Basic | $ 2.85 | $ 2.39 | $ 2.79 | ||

Diluted | $ 2.83 | $ 2.37 | $ 2.77 | ||

(1) Net effective spread is a non-GAAP measure. See "Use of Non-GAAP Measures" above for an explanation of net effective spread. See below for a reconciliation of net interest income to net effective spread. | |||||

(2) Includes interest income and interest expense related to consolidated trusts owned by third parties reclassified from net interest income to guarantee and commitment fees to reflect management's view that the net interest income Farmer Mac earns is effectively a guarantee fee on the consolidated Farmer Mac Guaranteed Securities. | |||||

(3) Reflects reconciling adjustments for the reclassification to exclude expenses related to interest rate swaps not designated as hedges and terminations or net settlements on financial derivatives, and reconciling adjustments to exclude fair value adjustments on financial derivatives and trading assets and the recognition of deferred gains over the estimated lives of certain Farmer Mac Guaranteed Securities and USDA Securities. | |||||

(4) Includes the tax impact of non-GAAP reconciling items between net income attributable to common stockholders and core earnings. | |||||

Reconciliation of Net Income Attributable to Common Stockholders to Core Earnings | |||

For the Six Months Ended | |||

June 30, 2022 | June 30, 2021 | ||

(in thousands, except per share amounts) | |||

Net income attributable to common stockholders | $ 80,150 | $ 53,402 | |

Less reconciling items: | |||

Gains/(losses) on undesignated financial derivatives due to fair value changes | 4,171 | (2,026) | |

Gains/(losses) on hedging activities due to fair value changes | 7,940 | (2,368) | |

Unrealized losses on trading assets | (191) | (75) | |

Net effects of amortization of premiums/discounts and deferred gains on assets consolidated at fair value | (42) | 36 | |

Net effects of terminations or net settlements on financial derivatives | 18,048 | 1,274 | |

Income tax effect related to reconciling items | (6,285) | 664 | |

Sub-total | 23,641 | (2,495) | |

Core earnings | $ 56,509 | $ 55,897 | |

Composition of Core Earnings: | |||

Revenues: | |||

Net effective spread(1) | $ 118,785 | $ 110,410 | |

Guarantee and commitment fees(2) | 9,266 | 8,574 | |

Other(3) | 821 | 752 | |

Total revenues | 128,872 | 119,736 | |

Credit related expense (GAAP): | |||

Release of losses | (1,589) | (1,014) | |

Total credit related expense | (1,589) | (1,014) | |

Operating expenses (GAAP): | |||

Compensation and employee benefits | 25,013 | 21,574 | |

General and administrative | 14,798 | 12,685 | |

Regulatory fees | 1,625 | 1,500 | |

Total operating expenses | 41,436 | 35,759 | |

Net earnings | 89,025 | 84,991 | |

Income tax expense(4) | 18,933 | 17,983 | |

Preferred stock dividends (GAAP) | 13,583 | 11,111 | |

Core earnings | $ 56,509 | $ 55,897 | |

Core earnings per share: | |||

Basic | $ 5.24 | $ 5.20 | |

Diluted | $ 5.20 | $ 5.16 | |

(1) Net effective spread is a non-GAAP measure. See "Use of Non-GAAP Measures" above for an explanation of net effective spread. See below for a reconciliation of net interest income to net effective spread. | |||

(2) Includes interest income and interest expense related to consolidated trusts owned by third parties reclassified from net interest income to guarantee and commitment fees to reflect management's view that the net interest income Farmer Mac earns is effectively a guarantee fee on the consolidated Farmer Mac Guaranteed Securities. | |||

(3) Reflects reconciling adjustments for the reclassification to exclude expenses related to interest rate swaps not designated as hedges and terminations or net settlements on financial derivatives, and reconciling adjustments to exclude fair value adjustments on financial derivatives and trading assets and the recognition of deferred gains over the estimated lives of certain Farmer Mac Guaranteed Securities and USDA Securities. | |||

(4) Includes the tax impact of non-GAAP reconciling items between net income attributable to common stockholders and core earnings. | |||

Reconciliation of GAAP Basic Earnings Per Share to Core Earnings Basic Earnings Per Share | |||||||||

For the Three Months Ended | For the Six Months Ended | ||||||||

June 30, | March 31, | June 30, | June 30, | June 30, | |||||

(in thousands, except per share amounts) | |||||||||

GAAP - Basic EPS | $ 3.62 | $ 3.81 | $ 2.36 | $ 7.43 | $ 4.96 | ||||

Less reconciling items: | |||||||||

Gains/(losses) on undesignated financial derivatives due to fair value changes | 0.23 | 0.16 | (0.35) | 0.39 | (0.19) | ||||

Gains/(losses) on hedging activities due to fair value changes | 0.55 | 0.19 | (0.19) | 0.74 | (0.22) | ||||

Unrealized (losses)/gains on trading securities | (0.03) | 0.01 | (0.01) | (0.02) | (0.01) | ||||

Net effects of amortization of premiums/discounts and deferred gains on assets consolidated at fair value | (0.01) | — | — | — | — | ||||

Net effects of terminations or net settlements on financial derivatives | 0.24 | 1.44 | 0.01 | 1.67 | 0.12 | ||||

Income tax effect related to reconciling items | (0.21) | (0.38) | 0.11 | (0.59) | 0.06 | ||||

Sub-total | 0.77 | 1.42 | (0.43) | 2.19 | (0.24) | ||||

Core Earnings - Basic EPS | $ 2.85 | $ 2.39 | $ 2.79 | $ 5.24 | $ 5.20 | ||||

Shares used in per share calculation (GAAP and Core Earnings) | 10,796 | 10,767 | 10,763 | 10,782 | 10,751 | ||||

Reconciliation of GAAP Diluted Earnings Per Share to Core Earnings Diluted Earnings Per Share | |||||||||

For the Three Months Ended | For the Six Months Ended | ||||||||

June 30, | March 31, | June 30, | June 30, | June 30, | |||||

(in thousands, except per share amounts) | |||||||||

GAAP - Diluted EPS | $ 3.60 | $ 3.77 | $ 2.35 | $ 7.37 | $ 4.93 | ||||

Less reconciling items: | |||||||||

Gains/(losses) on undesignated financial derivatives due to fair value changes | 0.23 | 0.16 | (0.34) | 0.38 | (0.18) | ||||

Gains/(losses) on hedging activities due to fair value changes | 0.55 | 0.19 | (0.19) | 0.73 | (0.22) | ||||

Unrealized (losses)/gains on trading securities | (0.03) | 0.01 | (0.01) | (0.02) | (0.01) | ||||

Net effects of amortization of premiums/discounts and deferred gains on assets consolidated at fair value | (0.01) | — | — | — | — | ||||

Net effects of terminations or net settlements on financial derivatives | 0.23 | 1.42 | 0.01 | 1.66 | 0.12 | ||||

Income tax effect related to reconciling items | (0.20) | (0.38) | 0.11 | (0.58) | 0.06 | ||||

Sub-total | 0.77 | 1.40 | (0.42) | 2.17 | (0.23) | ||||

Core Earnings - Diluted EPS | $ 2.83 | $ 2.37 | $ 2.77 | $ 5.20 | $ 5.16 | ||||

Shares used in per share calculation (GAAP and Core Earnings) | 10,864 | 10,887 | 10,838 | 10,876 | 10,829 | ||||

The following table presents a reconciliation of net interest income and net yield to net effective spread for the periods indicated:

Reconciliation of GAAP Net Interest Income/Yield to Net Effective Spread | |||||||||||||||||||

For the Three Months Ended | For the Six Months Ended | ||||||||||||||||||

June 30, 2022 | March 31, 2022 | June 30, 2021 | June 30, 2022 | June 30, 2021 | |||||||||||||||

Dollars | Yield | Dollars | Yield | Dollars | Yield | Dollars | Yield | Dollars | Yield | ||||||||||

(dollars in thousands) | |||||||||||||||||||

Net interest income/yield | $ 69,402 | 1.09 % | $ 61,875 | 1.00 % | $ 55,129 | 0.94 % | $ 131,277 | 1.04 % | $ 108,380 | 0.93 % | |||||||||

Net effects of consolidated trusts | (1,183) | 0.02 % | (1,018) | 0.02 % | (1,337) | 0.02 % | (2,201) | 0.02 % | (2,547) | 0.02 % | |||||||||

Expense related to undesignated financial derivatives | (2,026) | (0.03) % | (994) | (0.02) % | 970 | 0.02 % | (3,020) | (0.02) % | 3,038 | 0.03 % | |||||||||

Amortization of premiums/discounts on assets consolidated at fair value | 65 | — % | (16) | — % | (13) | — % | 49 | — % | (20) | — % | |||||||||

Amortization of losses due to terminations or net settlements on financial derivatives | 725 | 0.01 % | 356 | 0.01 % | 77 | — % | 1,083 | 0.01 % | 180 | — % | |||||||||

Fair value changes on fair value hedge relationships | (6,037) | (0.10) % | (2,364) | (0.04) % | 1,725 | 0.03 % | (8,403) | (0.07) % | 1,379 | 0.01 % | |||||||||

Net effective spread | $ 60,946 | 0.99 % | $ 57,839 | 0.97 % | $ 56,551 | 1.01 % | $ 118,785 | 0.98 % | $ 110,410 | 0.99 % | |||||||||

The following table presents core earnings for Farmer Mac's reportable operating segments and a reconciliation to consolidated net income for the three months ended June 30, 2022:

Core Earnings by Business Segment | |||||||||||||||||

For the Three Months Ended June 30, 2022 | |||||||||||||||||

Agricultural Finance | Rural Infrastructure | Treasury | Corporate | ||||||||||||||

Farm & | Corporate | Rural Utilities | Renewable | Funding | Investments | Reconciling Adjustments | Consolidated | ||||||||||

(in thousands) | |||||||||||||||||

Net interest income | $ 33,670 | $ 6,929 | $ 3,772 | $ 468 | $ 25,845 | $ (1,282) | $ — | $ — | $ 69,402 | ||||||||

Less: reconciling adjustments(1)(2)(3) | (1,080) | — | (39) | — | (7,337) | — | — | 8,456 | — | ||||||||

Net effective spread | 32,590 | 6,929 | 3,733 | 468 | 18,508 | (1,282) | — | 8,456 | — | ||||||||

Guarantee and commitment fees | 4,338 | 43 | 308 | 20 | — | — | — | (1,496) | 3,213 | ||||||||

Other income/(expense)(3) | 161 | 143 | — | — | — | — | 3 | 3,619 | 3,926 | ||||||||

Total revenues | 37,089 | 7,115 | 4,041 | 488 | 18,508 | (1,282) | 3 | 10,579 | 76,541 | ||||||||

Release of/(provision for) losses | 857 | (650) | 1,172 | (8) | — | 1 | — | — | 1,372 | ||||||||

Release of reserve for losses | 111 | — | 52 | — | — | — | — | — | 163 | ||||||||

Operating expenses | — | — | — | — | — | — | (20,048) | — | (20,048) | ||||||||

Total non-interest expense | 111 | — | 52 | — | — | — | (20,048) | — | (19,885) | ||||||||

Core earnings before income taxes | 38,057 | 6,465 | 5,265 | 480 | 18,508 | (1,281) | (20,045) | 10,579 | (4) | 58,028 | |||||||

Income tax (expense)/benefit | (7,991) | (1,357) | (1,105) | (101) | (3,887) | 269 | 4,263 | (2,223) | (12,132) | ||||||||

Core earnings before preferred stock dividends | 30,066 | 5,108 | 4,160 | 379 | 14,621 | (1,012) | (15,782) | 8,356 | (4) | 45,896 | |||||||

Preferred stock dividends | — | — | — | — | — | — | (6,792) | — | (6,792) | ||||||||

Segment core earnings/(losses) | $ 30,066 | $ 5,108 | $ 4,160 | $ 379 | $ 14,621 | $ (1,012) | $ (22,574) | $ 8,356 | (4) | $ 39,104 | |||||||

Total Assets | $ 13,686,589 | $ 1,521,102 | $ 5,632,551 | $ 126,513 | $ — | $ 4,802,159 | $ 147,489 | $ — | 25,916,403 | ||||||||

Total on- and off-balance sheet program assets at principal balance | $ 16,591,999 | $ 1,567,311 | $ 6,172,063 | $ 148,018 | $ — | $ — | $ — | $ — | 24,479,391 | ||||||||

(1) Includes the amortization of premiums and discounts on assets consolidated at fair value, originally included in interest income, to reflect core earnings amounts. | |||||||||||||||||

(2) Includes the reclassification of interest income and interest expense from consolidated trusts owned by third parties to guarantee and commitment fees, to reflect management's view that the net interest income Farmer Mac earns is effectively a guarantee fee. | |||||||||||||||||

(3) Includes the reclassification of interest expense related to interest rate swaps not designated as hedges, which are included in "Gains/(losses) on financial derivatives" on the consolidated financial statements, to determine the effective funding cost for each operating segment. | |||||||||||||||||

(4) Net adjustments to reconcile to the corresponding income measures: core earnings before income taxes reconciled to income before income taxes; core earnings before preferred stock dividends reconciled to net income; and segment core earnings reconciled to net income attributable to common stockholders. | |||||||||||||||||

Supplemental Information

The following table sets forth information about outstanding volume in each of Farmer Mac's lines of business as of the dates indicated:

Outstanding Business Volume | ||||||

On or Off Balance Sheet | As of June 30, 2022 | As of December 31, 2021 | ||||

(in thousands) | ||||||

Agricultural Finance: | ||||||

Farm & Ranch: | ||||||

Loans | On-balance sheet | $ 5,214,307 | $ 4,775,070 | |||

Loans held in consolidated trusts: | ||||||

Beneficial interests owned by third-party investors | On-balance sheet | 834,941 | 948,623 | |||

IO-FMGS(1) | On-balance sheet | 11,561 | 12,297 | |||

USDA Securities | On-balance sheet | 2,429,407 | 2,445,806 | |||

AgVantage Securities | On-balance sheet | 4,995,000 | 4,725,000 | |||

LTSPCs and unfunded commitments | Off-balance sheet | 2,562,467 | 2,587,154 | |||

Farmer Mac Guaranteed Securities | Off-balance sheet | 523,580 | 578,358 | |||

Loans serviced for others | Off-balance sheet | 20,736 | 22,331 | |||

Total Farm & Ranch | $ 16,591,999 | $ 16,094,639 | ||||

Corporate AgFinance: | ||||||

Loans | On-balance sheet | $ 1,149,614 | $ 1,123,300 | |||

AgVantage Securities | On-balance sheet | 352,968 | 367,464 | |||

Unfunded Loan Commitments | Off-balance sheet | 64,729 | 47,070 | |||

Total Corporate AgFinance | $ 1,567,311 | $ 1,537,834 | ||||

Total Agricultural Finance | $ 18,159,310 | $ 17,632,473 | ||||

Rural Infrastructure Finance: | ||||||

Rural Utilities: | ||||||

Loans | On-balance sheet | $ 2,631,694 | $ 2,302,373 | |||

AgVantage Securities | On-balance sheet | 2,986,404 | 3,033,262 | |||

LTSPCs and Unfunded Loan Commitments | Off-balance sheet | 551,210 | 556,837 | |||

Farmer Mac Guaranteed Securities | Off-balance sheet | 2,755 | 2,755 | |||

Total Rural Utilities | $ 6,172,063 | $ 5,895,227 | ||||

Renewable Energy: | ||||||

Loans | On-balance sheet | $ 126,299 | $ 86,763 | |||

Unfunded Loan Commitments | Off-balance sheet | 21,719 | — | |||

Total Renewable Energy | $ 148,018 | $ 86,763 | ||||

Total Rural Infrastructure Finance | $ 6,320,081 | $ 5,981,990 | ||||

Total | $ 24,479,391 | $ 23,614,463 | ||||

(1) An interest-only Farmer Mac Guaranteed Security retained as part of a structured securitization. | ||||||

The following table presents the quarterly net effective spread (a non-GAAP measure) by segment:

Net Effective Spread(1) | |||||||||||||||||||||||||||

Agricultural Finance | Rural Infrastructure Finance | Treasury | |||||||||||||||||||||||||

Farm & Ranch | Corporate | Rural Utilities | Renewable | Funding | Investments | Net Effective | |||||||||||||||||||||

Dollars | Yield | Dollars | Yield | Dollars | Yield | Dollars | Yield | Dollars | Yield | Dollars | Yield | Dollars | Yield | ||||||||||||||

(dollars in thousands) | |||||||||||||||||||||||||||

For the quarter ended: | |||||||||||||||||||||||||||

June 30, 2022(1) | $ 32,590 | 1.05 % | $ 6,929 | 1.87 % | $ 3,733 | 0.27 % | $ 468 | 1.78 % | $ 18,508 | 0.30 % | $ (1,282) | (0.10) % | $ 60,946 | 0.99 % | |||||||||||||

March 31, 2022 | 30,354 | 1.02 % | 7,209 | 1.96 % | 3,159 | 0.23 % | 375 | 1.69 % | 16,738 | 0.28 % | 4 | — % | 57,839 | 0.97 % | |||||||||||||

December 31, 2021 | 28,998 | 0.99 % | 6,321 | 1.84 % | 2,521 | 0.19 % | 356 | 1.53 % | 15,979 | 0.28 % | 158 | 0.01 % | 54,333 | 0.94 % | |||||||||||||

September 30, 2021 | 28,914 | 1.06 % | 7,163 | 1.80 % | 2,067 | 0.16 % | 236 | 1.09 % | 17,386 | 0.31 % | 159 | 0.01 % | 55,925 | 0.99 % | |||||||||||||

June 30, 2021 | 29,163 | 1.06 % | 6,676 | 1.65 % | 1,759 | 0.14 % | 378 | 1.80 % | 18,449 | 0.33 % | 126 | 0.01 % | 56,551 | 1.01 % | |||||||||||||

March 31, 2021 | 26,461 | 0.98 % | 6,921 | 1.67 % | 1,720 | 0.14 % | 249 | 1.28 % | 18,394 | 0.33 % | 114 | 0.01 % | 53,859 | 0.97 % | |||||||||||||

December 31, 2020 | 25,596 | 0.95 % | 6,237 | 1.53 % | 1,838 | 0.15 % | 123 | 1.20 % | 20,585 | 0.37 % | 143 | 0.01 % | 54,522 | 0.98 % | |||||||||||||

September 30, 2020 | 23,735 | 0.89 % | 5,786 | 1.45 % | 2,022 | 0.16 % | 75 | 1.19 % | 20,034 | 0.37 % | 150 | 0.01 % | 51,802 | 0.96 % | |||||||||||||

June 30, 2020 | 21,597 | 0.83 % | 4,997 | 1.36 % | 1,701 | 0.14 % | 47 | 0.93 % | 19,449 | 0.37 % | (1,322) | (0.13) % | 46,469 | 0.89 % | |||||||||||||

(1) Farmer Mac excludes the Corporate segment in the presentation above because the segment does not have any interest-earning assets. | |||||||||||||||||||||||||||

(2) See above for a reconciliation of GAAP net interest income by line of business to net effective spread by line of business for the three months ended June 30, 2022. | |||||||||||||||||||||||||||

The following table presents quarterly core earnings reconciled to net income attributable to common stockholders:

Core Earnings by Quarter Ended | |||||||||||||||||

June | March | December | September | June | March | December | September | June | |||||||||

(in thousands) | |||||||||||||||||

Revenues: | |||||||||||||||||

Net effective spread | $ 60,946 | $ 57,839 | $ 54,333 | $ 55,925 | $ 56,551 | $ 53,859 | $ 54,522 | $ 51,802 | $ 46,469 | ||||||||

Guarantee and commitment fees | 4,709 | 4,557 | 4,637 | 4,322 | 4,334 | 4,240 | 4,652 | 4,659 | 4,943 | ||||||||

Gain on sale of mortgage loans | — | — | 6,539 | — | — | — | — | — | — | ||||||||

Other | 307 | 514 | 241 | 687 | 301 | 451 | 512 | 453 | 1,048 | ||||||||

Total revenues | 65,962 | 62,910 | 65,750 | 60,934 | 61,186 | 58,550 | 59,686 | 56,914 | 52,460 | ||||||||

Credit related expense/(income): | |||||||||||||||||

(Release of)/provision for losses | (1,535) | (54) | (1,428) | 255 | (983) | (31) | 2,973 | 1,200 | 51 | ||||||||

REO operating expenses | — | — | — | — | — | — | — | — | — | ||||||||

Losses/(gains) on sale of REO | — | — | — | — | — | — | 22 | — | — | ||||||||

Total credit related expense/(income) | (1,535) | (54) | (1,428) | 255 | (983) | (31) | 2,995 | 1,200 | 51 | ||||||||

Operating expenses: | |||||||||||||||||

Compensation and employee benefits | 11,715 | 13,298 | 11,246 | 10,027 | 9,779 | 11,795 | 9,497 | 8,791 | 8,087 | ||||||||

General and administrative | 7,520 | 7,278 | 8,492 | 6,330 | 6,349 | 6,336 | 6,274 | 5,044 | 5,295 | ||||||||

Regulatory fees | 813 | 812 | 812 | 750 | 750 | 750 | 750 | 725 | 725 | ||||||||

Total operating expenses | 20,048 | 21,388 | 20,550 | 17,107 | 16,878 | 18,881 | 16,521 | 14,560 | 14,107 | ||||||||

Net earnings | 47,449 | 41,576 | 46,628 | 43,572 | 45,291 | 39,700 | 40,170 | 41,154 | 38,302 | ||||||||

Income tax expense | 9,909 | 9,024 | 9,809 | 9,152 | 9,463 | 8,520 | 8,470 | 8,297 | 8,016 | ||||||||

Preferred stock dividends | 6,792 | 6,791 | 6,792 | 6,774 | 5,842 | 5,269 | 5,269 | 5,166 | 3,939 | ||||||||

Core earnings | $ 30,748 | $ 25,761 | $ 30,027 | $ 27,646 | $ 29,986 | $ 25,911 | $ 26,431 | $ 27,691 | $ 26,347 | ||||||||

Reconciling items: | |||||||||||||||||

Gains/(losses) on undesignated financial derivatives due to fair value changes | $ 2,473 | $ 1,698 | $ (1,213) | $ (1,864) | $ (3,721) | $ 1,695 | $ (1,758) | $ (4,149) | $ 8,700 | ||||||||

Gains/(losses) on hedging activities due to fair value changes | 5,916 | 2,024 | 1,476 | (2,093) | (2,097) | (271) | 3,827 | (5,245) | (2,676) | ||||||||

Unrealized gains/(losses) on trading assets | (285) | 94 | (76) | 36 | (61) | (14) | 223 | (258) | (20) | ||||||||

Net effects of amortization of premiums/discounts and deferred gains on assets consolidated at fair value | (62) | 20 | 71 | 23 | 20 | 16 | (77) | 97 | 35 | ||||||||

Net effects of terminations or net settlements on financial derivatives | 2,536 | 15,512 | (429) | (351) | 109 | 1,165 | 1,583 | 233 | 720 | ||||||||

Issuance costs on the retirement of preferred stock | — | — | — | — | — | — | — | (1,667) | — | ||||||||

Income tax effect related to reconciling items | (2,222) | (4,063) | 36 | 892 | 1,208 | (544) | (798) | 1,957 | (1,419) | ||||||||

Net income attributable to common stockholders | $ 39,104 | $ 41,046 | $ 29,892 | $ 24,289 | $ 25,444 | $ 27,958 | $ 29,431 | $ 18,659 | $ 31,687 | ||||||||

View original content to download multimedia:https://www.prnewswire.com/news-releases/farmer-mac-reports-second-quarter-2022-results-301601780.html

SOURCE Farmer Mac

Government

Young People Aren’t Nearly Angry Enough About Government Debt

Young People Aren’t Nearly Angry Enough About Government Debt

Authored by The American Institute for Economic Research,

Young people sometimes…

Share this:

Authored by The American Institute for Economic Research,

Young people sometimes seem to wake up in the morning in search of something to be outraged about. We are among the wealthiest and most educated humans in history. But we’re increasingly convinced that we’re worse off than our parents were, that the planet is in crisis, and that it’s probably not worth having kids.

I’ll generalize here about my own cohort (people born after 1981 but before 2010), commonly referred to as Millennials and Gen Z, as that shorthand corresponds to survey and demographic data. Millennials and Gen Z have valid economic complaints, and the conditions of our young adulthood perceptibly weakened traditional bridges to economic independence. We graduated with record amounts of student debt after President Obama nationalized that lending. Housing prices doubled during our household formation years due to zoning impediments and chronic underbuilding. Young Americans say economic issues are important to us, and candidates are courting our votes by promising student debt relief and cheaper housing (which they will never be able to deliver).

Young people, in our idealism and our rational ignorance of the actual appropriations process, typically support more government intervention, more spending programs, and more of every other burden that has landed us in such untenable economic circumstances to begin with. Perhaps not coincidentally, young people who’ve spent the most years in the increasingly partisan bubble of higher education are also the most likely to favor expanded government programs as a “solution” to those complaints.

It’s Your Debt, Boomer

What most young people don’t yet understand is that we are sacrificing our young adulthood and our financial security to pay for debts run up by Baby Boomers. Part of every Millennial and Gen-Z paycheck is payable to people the same age as the members of Congress currently milking this system and miring us further in debt.

Our government spends more than it can extract from taxpayers. Social Security, which represents 20 percent of government spending, has run an annual deficit for 15 years. Last year Social Security alone overspent by $22.1 billion. To keep sending out checks to retirees, Social Security goes begging to the Treasury Department, and the Treasury borrows from the public by issuing bonds. Bonds allow investors (who are often also taxpayers) to pay for some retirees’ benefits now, and be paid back later. But investors only volunteer to lend Social Security the money it needs to cover its bills because the (younger) taxpayers will eventually repay the debt — with interest.

In other words, both Social Security and Medicare, along with various smaller federal entitlement programs, together comprising almost half of the federal budget, have been operating for a decade on the principle of “give us the money now, and stick the next generation with the check.” We saddle future generations with debt for present-day consumption.

The second largest item in the budget after Social Security is interest on the national debt — largely on Social Security and other entitlements that have already been spent. These mandatory benefits now consume three quarters of the federal budget: even Congress is not answerable for these programs. We never had the chance for our votes to impact that spending (not that older generations were much better represented) and it’s unclear if we ever will.

Young Americans probably don’t think much about the budget deficit (each year’s overspending) or the national debt (many years’ deficits put together, plus interest) much at all. And why should we? For our entire political memory, the federal government, as well as most of our state governments, have been steadily piling “public” debt upon our individual and collective heads. That’s just how it is. We are the frogs trying to make our way in the watery world as the temperature ticks imperceptibly higher. We have been swimming in debt forever, unaware that we’re being economically boiled alive.

Millennials have somewhat modest non-mortgage debt of around $27,000 (some self-reports say twice that much), including car notes, student loans, and credit cards. But we each owe more than $100,000 as a share of the national debt. And we don’t even know it.

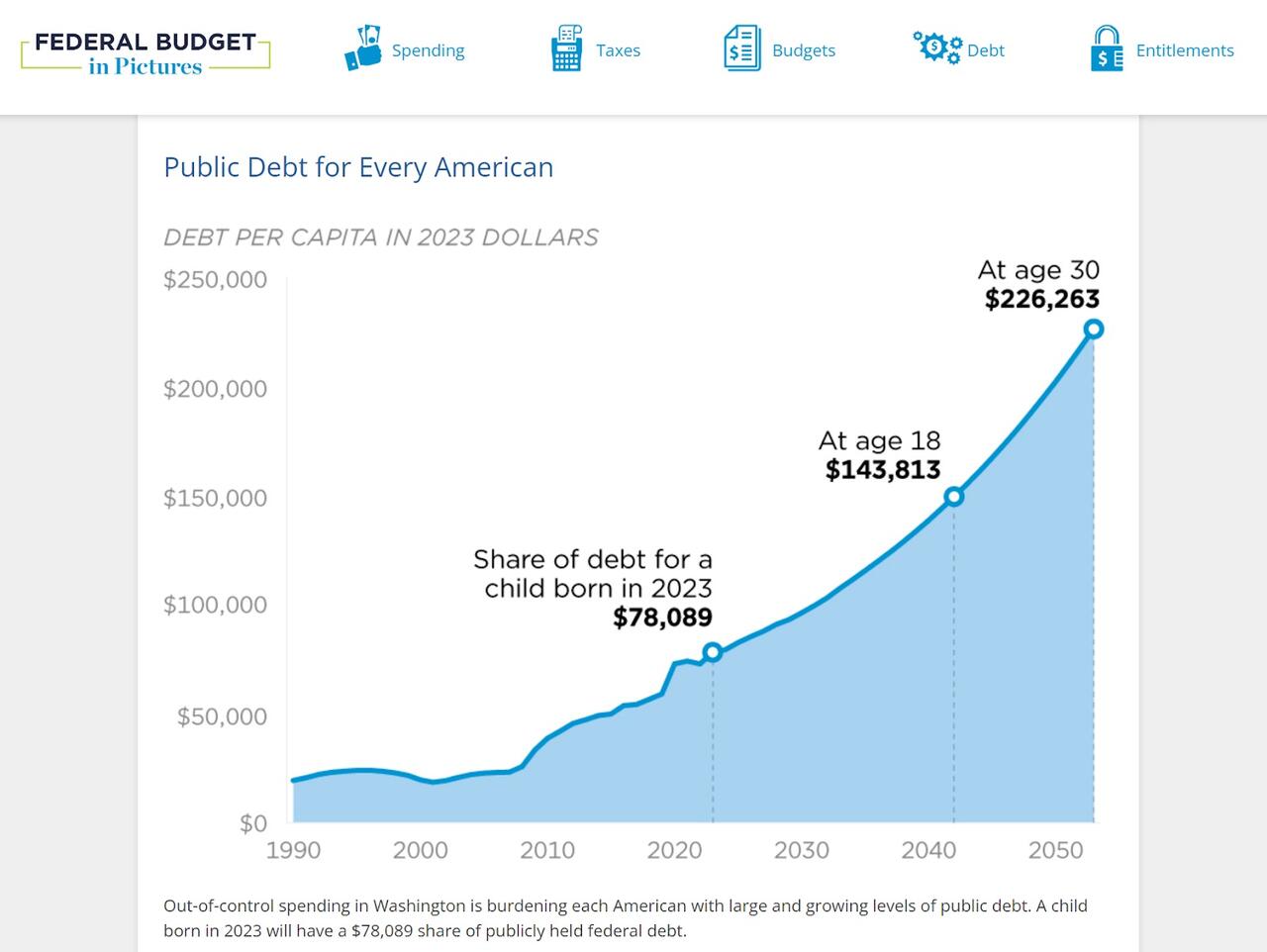

When Millennials finally do have babies (and we are!) that infant born in 2024 will enter the world with a newly minted Social Security Number and $78,089 credit card bill for Granddad’s heart surgery and the interest on a benefit check that was mailed when her parents were in middle school.

Headlines and comments sections love to sneer at “snowflakes” who’ve just hit the “real world,” and can’t figure out how to make ends meet, but the kids are onto something. A full 15 percent of our earnings are confiscated to pay into retirement and healthcare programs that will be insolvent by the time we’re old enough to enjoy them. The Federal Reserve and government debt are eating the economy. The same interest rates that are pushing mortgages out of reach are driving up the cost of interest to maintain the debt going forward. As we learn to save and invest, our dollars are slowly devalued. We’re right to feel trapped.

Sure, if we’re alive and own a smartphone, we’re among the one percent of the wealthiest humans who’ve ever lived. Older generations could argue (persuasively!) that we have no idea what “poverty” is anymore. But with the state of government spending and debt…we are likely to find out.

Despite being richer than Rockefeller, Millennials are right to say that the previous ways of building income security have been pushed out of reach. Our earning years are subsidizing not our own economic coming-of-age, but bank bailouts, wars abroad, and retirement and medical benefits for people who navigated a less-challenging wealth-building landscape.

Redistribution goes both ways. Boomers are expected to pass on tens of trillions in unprecedented wealth to their children (if it isn’t eaten up by medical costs, despite heavy federal subsidies) and older generations’ financial support of the younger has had palpable lifting effects. Half of college costs are paid by families, and the trope of young people moving back home is only possible if mom and dad have the spare room and groceries to make that feasible.

Government “help” during COVID-19 resulted in the worst inflation in 40 years, as the federal government spent $42,000 per citizen on “stimulus” efforts, right around a Millennial’s average salary at that time. An absurd amount of fraud was perpetrated in the stimulus to save an economy from the lockdown that nearly ruined it. Trillions in earmarked goodies were rubber stamped, carelessly added to young people’s growing bill. Government lenders deliberately removed fraud controls, fearing they couldn’t hand out $800 billion in young people’s future wages away fast enough. Important lessons were taught by those programs. The importance of self-sufficiency and the dignity of hard work weren’t top of the list.

Boomer Benefits are Stagnating Hiring, Wages, and Investment for Young People

Even if our workplace engagement suffered under government distortions, Millennials continue to work more hours than other generations and invest in side hustles and self employment at higher rates. Working hard and winning higher wages almost doesn’t matter, though, when our purchasing power is eaten from the other side. Buying power has dropped 20 percent in just five years. Life is $11,400/year more expensive than it was two years ago and deficit spending is the reason why.

We’re having trouble getting hired for what we’re worth, because it costs employers 30 percent more than just our wages to employ us. The federal tax code both requires and incentivizes our employers to transfer a bunch of what we earned directly to insurance companies and those same Boomer-busted federal benefits, via tax-deductible benefits and payroll taxes. And the regulatory compliance costs of ravenous bureaucratic state. The price paid by each employer to keep each employee continues to rise — but Congress says your boss has to give most of the increase to someone other than you.

Federal spending programs that many people consider good government, including Social Security, Medicare, Medicaid, and health insurance for children (CHIP) aren’t a small amount of the federal budget. Government spends on these programs because people support and demand them, and because cutting those benefits would be a re-election death sentence. That’s why they call cutting Social Security the “third rail of politics.” If you touch those benefits, you die. Congress is held hostage by Baby Boomers who are running up the bill with no sign of slowing down.

Young people generally support Social Security and the public health insurance programs, even though a 2021 poll by Nationwide Financial found 47 percent of Millennials agree with the statement “I will not get a dime of the Social Security benefits I have earned.”

In the same survey, Millennials were the most likely of any generation to believe that Social Security benefits should be enough to live on as a sole income, and guessed the retirement age was 52 (it’s 67 for anyone born after 1959 — and that’s likely to rise). Young people are the most likely to see government guarantees as a valid way to live — even though we seem to understand that those promises aren’t guarantees at all.

Healthcare costs tied to an aging population and wonderful-but-expensive growth in medical technologies and medications will balloon over the next few years, and so will the deficits in Boomer benefit programs. Newly developed obesity drugs alone are expected to add $13.6 billion to Medicare spending. By 2030, every single Baby Boomer will be 65, eligible for publicly funded healthcare.

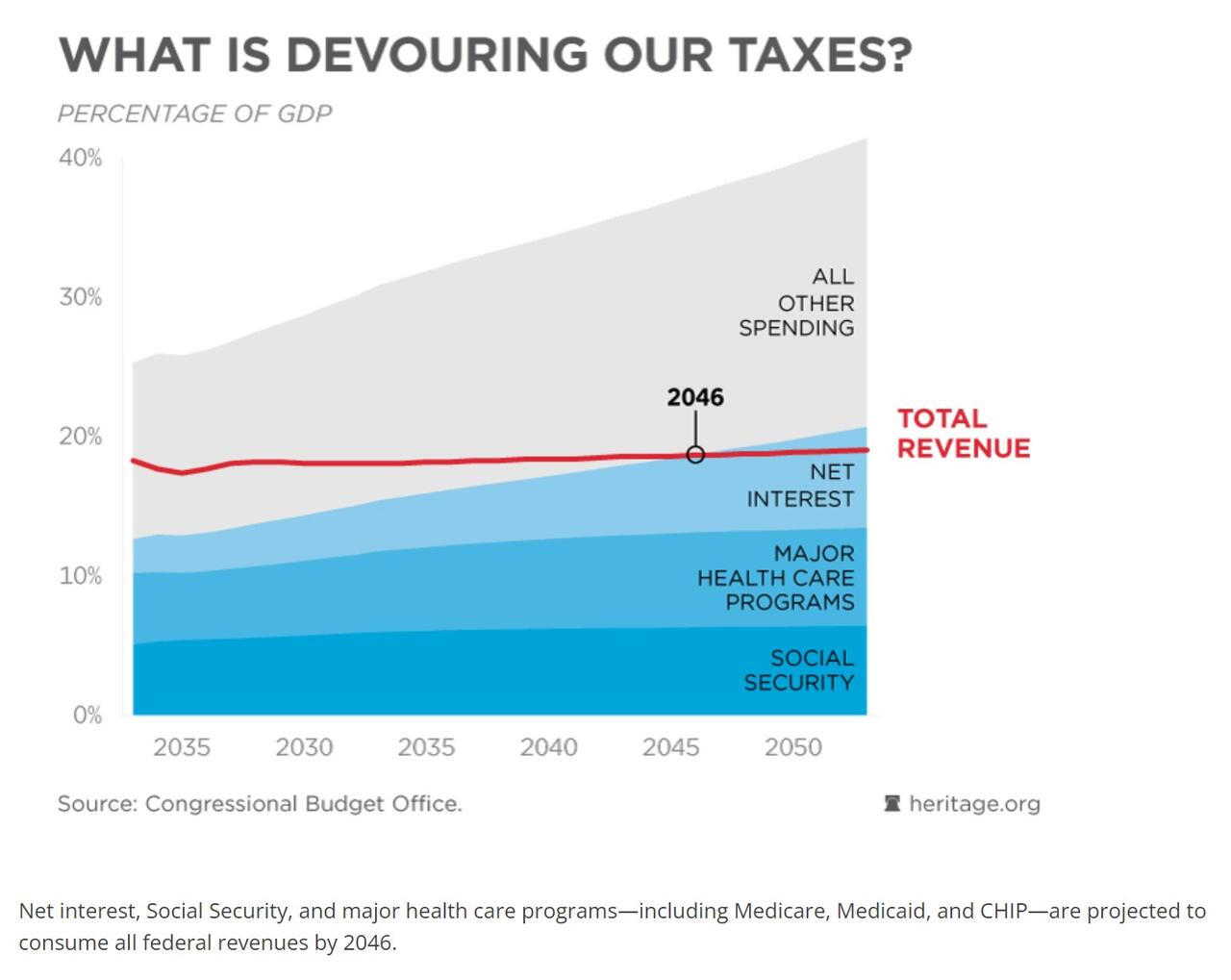

The first Millennial will be eligible to claim Medicare (assuming the program exists and the qualifying age is still 65, both of which are improbable) in 2046. As it happens, that’s also the year that the Boomer benefits programs (which will then be bloated with Gen Xers) and the interest payments we’re incurring to provide those benefits now, are projected to consume 100 percent of federal tax revenue.

Government spending is being transferred to bureaucrats and then to the beneficiaries of government spending who are, in some sense, your diabetic grandma who needs a Medicare-paid dialysis treatment, but in a much more immediate sense, are the insurance companies, pharma giants, and hospital corporations who wrote the healthcare legislation. Some percentage of every college graduate’s paycheck buys bullets that get fired at nothing and inflating the private investment portfolios of government contractors, with dubious, wasteful outcomes from the prison-industrial complex to the perpetual war machine.

No bank or nation in the world can lend the kind of money the American government needs to borrow to fulfill its obligations to citizens. Someone will have to bite the bullet. Even some of the co-authors of the current disaster are wrestling with the truth.

Forget avocado toast and streaming subscriptions. We’re already sensing it, but we haven’t yet seen it. Young people are not well-informed, and often actively misled, about what’s rotten in this economic system. But we are seeing the consequences on store shelves and mortgage contracts and we can sense disaster is coming. We’re about to get stuck with the bill.

Spread & Containment

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

Two years ago, we first said that it’s only a matter…

Share this:

Two years ago, we first said that it's only a matter of time before the Fed admits it is unable to rsolve the so-called "last mile" of inflation and that as a result, the old inflation target of 2% is no longer viable.

At some point Fed will concede it has no control over supply. That's when we will start getting leaks of raising the inflation target

— zerohedge (@zerohedge) June 21, 2022

Then one year ago, we correctly said that while everyone was paying attention elsewhere, the inflation target had already been hiked to 2.8%... on the way to even more increases.

The new inflation target has been set to 2.8%. The rest is just narrative fill for the next 2 years. https://t.co/X1xYkecyPy

— zerohedge (@zerohedge) February 21, 2023

And while the Fed still pretends it can one day lower inflation to 2% even as it prepares to cut rates as soon as June, moments ago Goldman published a note from its economics team which had to balls to finally call a spade a spade, and concluded that - as party of the Fed's next big debate, i.e., rethinking the Neutral rate - both the neutral and terminal rate, a polite euphemism for the inflation target, are much higher than conventional wisdom believes, and that as a result Goldman is "penciling in a terminal rate of 3.25-3.5% this cycle, 100bp above the peak reached last cycle."

There is more in the full Goldman note, but below we excerpt the key fragments:

We argued last cycle that the long-run neutral rate was not as low as widely thought, perhaps closer to 3-3.5% in nominal terms than to 2-2.5%. We have also argued this cycle that the short-run neutral rate could be higher still because the fiscal deficit is much larger than usual—in fact, estimates of the elasticity of the neutral rate to the deficit suggest that the wider deficit might boost the short-term neutral rate by 1-1.5%. Fed economists have also offered another reason why the short-term neutral rate might be elevated, namely that broad financial conditions have not tightened commensurately with the rise in the funds rate, limiting transmission to the economy.

Over the coming year, Fed officials are likely to debate whether the neutral rate is still as low as they assumed last cycle and as the dot plot implies....

...Translation: raising the neutral rate estimate is also the first step to admitting that the traditional 2% inflation target is higher than previously expected. And once the Fed officially crosses that particular Rubicon, all bets are off.

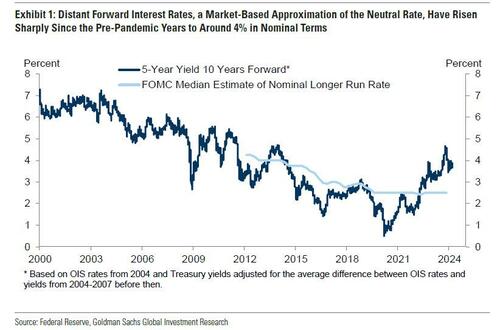

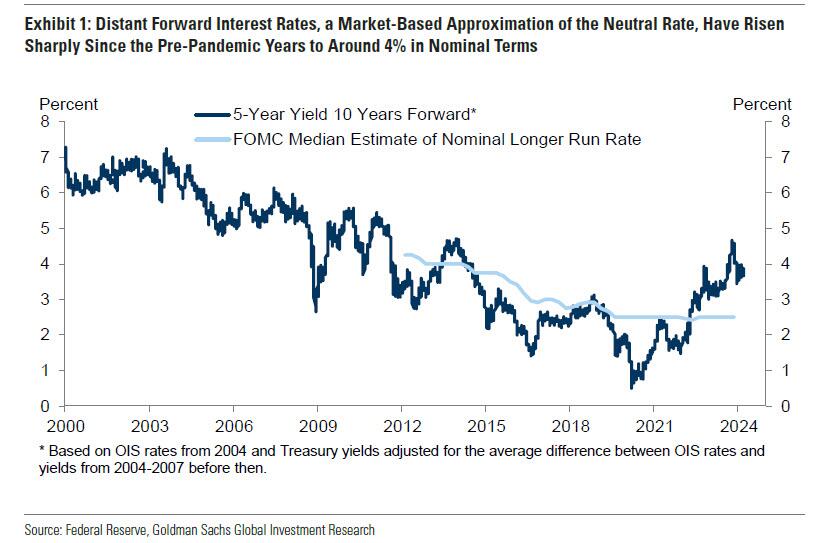

... Their thinking is likely to be influenced by distant forward market rates, which have risen 1-2pp since the pre-pandemic years to about 4%; by model-based estimates of neutral, whose earlier real-time values have been revised up by roughly 0.5pp on average to about 3.5% nominal and whose latest values are little changed; and by their perception of how well the economy is performing at the current level of the funds rate.

The bank's conclusion:

We expect Fed officials to raise their estimates of neutral over time both by raising their long-run neutral rate dots somewhat and by concluding that short-run neutral is currently higher than long-run neutral. While we are fairly confident that Fed officials will not be comfortable leaving the funds rate above 5% indefinitely once inflation approaches 2% and that they will not go all the way back to 2.5% purely in the name of normalization, we are quite uncertain about where in between they will ultimately land.

Because the economy is not sensitive enough to small changes in the funds rate to make it glaringly obvious when neutral has been reached, the terminal or equilibrium rate where the FOMC decides to leave the funds rate is partly a matter of the true neutral rate and partly a matter of the perceived neutral rate. For now, we are penciling in a terminal rate of 3.25-3.5% this cycle, 100bps above the peak reached last cycle. This reflects both our view that neutral is higher than Fed officials think and our expectation that their thinking will evolve.

Not that this should come as a surprise: as a reminder, with the US now $35.5 trillion in debt and rising by $1 trillion every 100 days, we are fast approaching the Minsky Moment, which means the US has just a handful of options left: losing the reserve currency status, QEing the deficit and every new dollar in debt, or - the only viable alternative - inflating it all away. The only question we had before is when do "serious" economists make the same admission.

Meanwhile, nothing changes: total US debt jumps $57BN on March 15, to a record $34.543 trillion.

— zerohedge (@zerohedge) March 19, 2024

Three ways this ends: inflate it away, QE it all, or reserve status collapse

They now have.

And while we have discussed the staggering consequences of raising the inflation target by just 1% from 2% to 3% on everything from markets, to economic growth (instead of doubling every 35 years at 2% inflation target, prices would double every 23 years at 3%), and social cohesion, we will soon rerun the analysis again as the implications are profound. For now all you need to know is that with the US about to implicitly hit the overdrive of dollar devaluation, anything that is non-fiat will be much more preferable over fiat alternatives.

Much more in the full Goldman note available to pro subs in the usual place.

Spread & Containment

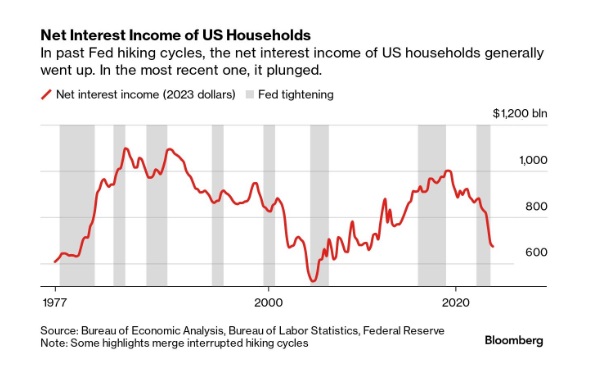

Household Net Interest Income Falls As Rates Spike

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical…

Share this:

{kind=link}

{kind=link}

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical anomaly was both surprising and contradicted our priors.

10 Key Points:

- Historical Anomaly: This is the first time in the last fifty years that a Federal Reserve rate hike cycle has led to a significant drop in household net interest income.

- Interest Expense Increase: Since the Fed began raising rates in March 2022, Americans’ annual interest expenses on debts like mortgages and credit cards have surged by nearly $420 billion.

- Interest Income Lag: The increase in interest income during the same period was only about $280 billion, resulting in a net decline in household interest income, a departure from past trends.

- Consumer Debt Influence: The recent rate hikes impacted household finances more because of a higher proportion of consumer credit, which adjusts more quickly to rate changes, increasing interest costs.

- Banks and Savers: Banks have been slow to pass on higher interest rates to depositors, and the prolonged period of low rates before 2022 may have discouraged savers from actively seeking better returns.

- Shift in Wealth: There’s been a shift from interest-bearing assets to stocks, with dividends surpassing interest payments as a source of unearned income during the pandemic.

- Distributional Discrepancy: Higher interest rates benefit wealthier individuals who own interest-earning assets, whereas lower-income earners face the brunt of increased debt servicing costs, exacerbating economic inequality.

- Job Market Impact: Typically, Fed rate hikes affect households through the job market, as businesses cut costs, potentially leading to layoffs or wage suppression, though this hasn’t occurred yet in the current cycle.

- Economic Impact: The distribution of interest income and debt servicing means that rate increases transfer money from those more likely to spend (and thus stimulate the economy) to those less likely to increase consumption, potentially dampening economic activity.

- No Immediate Relief: Expectations for the Fed to reduce rates have diminished, indicating that high-interest expenses for households may persist.

Google’s A.I. Fiasco Exposes Deeper Infowarp

Greenback Surges after BOJ Hikes and Ends YCC and RBA Delivers a Dovish Hold

Young People Aren’t Nearly Angry Enough About Government Debt

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

Manufacturing and construction vs. the still-inverted yield curve

When words make you sick

Student loan borrowers may finally get answers to loan forgiveness issues

TikTok Ban Obscures Chinese Stock Gold Rush

You can strike gold and silver investment opportunities at Costco

Bolsonaro Indicted By Brazilian Police For Falsifying Covid-19 Vaccine Records

-

Spread & Containment7 days ago

Spread & Containment7 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex