Earnings Season Shocker: FAAMG Earnings Grew By 2% While EPS For The Other 495 S&P Companies Plunged 38%

Earnings Season Shocker: FAAMG Earnings Grew By 2% While EPS For The Other 495 S&P Companies Plunged 38%

Share this:

Goldman, which over the weekend turned incrementally more bullish on the economy and hiked its GDP forecast as it now expects that a covid vaccine will be discovered and widely distributed in Q1 2021, resulting in what Goldman believes will be a sharp jump in consumption in the first half of next year (whether that actually happens in a country where more than half refuse to get vaccinated is a different story completely), has done a post-mortem on Q2 earnings season and also found some more "good news."

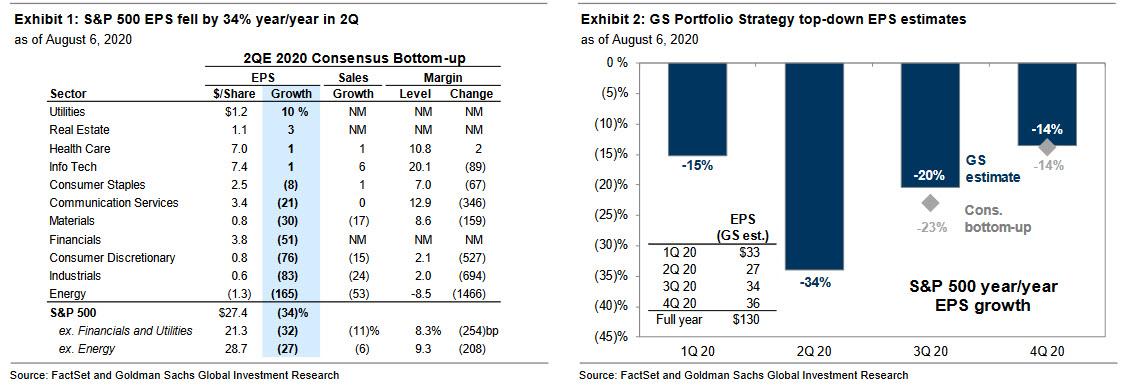

First, after expecting a 60% plunge in EPS in Q2, Goldman's David Kostin was delighted to report that S&P 500 EPS declined by "only" 34% year/year, well above both consensus expectations for a -45% decline, and Goldman's own forecast of a nearly double drop.

Some more details on soon to be concluded Q2 earnings season: with 445 companies representing 88% of S&P 500 market cap having reported, 58% of firms beat consensus EPS expectations by more than a standard deviation of estimates. This beat rate is well above the long-term average of 47% and nearly matches the previous record high from 2009 post-Financial Crisis. However, as even Kostin concedes, this only happened because consensus bottom-up earnings estimates were drastically cut ahead of 2Q earnings season. As a result of low expectations, companies that beat EPS estimates have only outperformed the market by 36 bp on average during the day following reports, below the historical average of 110 bp.

Aggressive estimate cuts aside, Goldman notes that strict cost management helped S&P 500 margins decline by less than expected, read lower input costs as well as aggressive layoffs.

Company managements across a variety of industries highlighted this theme in their earnings transcripts, ranging from employment and wages (e.g. DAL, KSU, HST) to discretionary expenditures (e.g., ALLE, GM). Both COGS and SG&A expenses as a share of revenues came in below consensus expectations, contributing to positive margin surprises in the quarter.

Kostin then suggests that the composition of the S&P 500 helps explain why 2Q results were stronger than what we expected based on the state of the economy.The US economy contracted by 10% year/year in the second quarter, setting a post-war record. Based on the historical relationship, S&P 500 EPS would have been expected to decline by roughly 60%. However, the shock to economic growth has had a particularly pronounced impact on small firms compared with large firms. The relatively strong balance sheets and elevated profit margins of large-cap stocks helped insulate their profits in 2Q.

And here is the first big surprise: while S&P 500 EPS fell by 34%, Russell 2000 EPS declined by 97%. Looking forward, small businesses continue to face elevated risk from the pandemic. As an example. a recent survey by GS 10,000 Small Businesses survey found that 84% of PPP loan recipients expected to exhaust funding by the first week of August. Further small business weakness could threaten the recoveries of both the US labor market and large-cap revenue growth.

But while small business remain crushed, large businesses are flourishing, and nowhere is this more evident than in the following fascinating observation from Goldman:

The strength of technology broadly and specifically the market-leading FAAMG stocks has also helped S&P 500 earnings fare better than what the economic environment would normally indicate. Info Tech is the largest S&P 500 sector by earnings weight (27% in 2Q) and actually grew earnings by 1% in the quarter, led by strong results within Semiconductors. Excluding Info Tech, S&P 500 EPS fell by 41% in 2Q. The five largest stocks in the S&P 500 (FB, AMZN, AAPL, MSFT, and GOOGL, or “FAAMG”) account for 16% of S&P 500 EPS, and each of those companies beat consensus sales and EPS estimates by more than one standard deviation in the quarter.

The punchline: In aggregate, FAAMG EPS grew by 2% year/year in 2Q compared with an aggregate decline of -38% for the other 495 S&P 500 companies: "The FAAMG stocks benefit from secular trends expedited by the coronavirus, such as cloud spending and e-commerce, and continue to capture an increasing share of their respective market."

In other words, for the "Big 5" techs, the pandemic shutdowns were precisely what the doctor ordered to not only crush what's left of their small and medium enterprise competition, but to boost their own WFH-based earnings.

Earnings shocker aside, Goldman used this unexpected strength in earnings (of really just a handful of companies), to lift its 2020 S&P 500 EPS estimate from $115 to $130 (-21% growth vs. 2019), and adds that of the $15 increase, $11 reflects better 2Q earnings results.

On a quarterly basis, we now expect year/year S&P 500 EPS growth of -20% in 3Q (vs. -30% previously) and -14% in 4Q (vs. -17% previously). High-frequency activity indicators, such as consumer spending measures, have improved since April, but softened in July as virus case counts have surged. Our estimates compare with consensus forecasts of -23% and -14%. Excluding Financials and Utilities, we forecast S&P 500 full-year 2020 sales growth of -4% and net profit margins of 9.1% (-157 bp). However, most investors are looking beyond 2020 and to the outlook for earnings in 2021 and 2022.

The better-than-expected Q2 results also gave Goldman confidence in its above-consensus 2021 EPS estimate of $170, which is largely driven by the bank's above-consensus 2021 economic forecast:

Our economists’ estimates for real US GDP growth in 2020 (-5.0%) and 2021 (+5.6%) are above both Blue Chip consensus and the median from the FOMC’s Summary of Economic Projections. We forecast S&P 500 sales growth of +10% and net profit margins of 10.9% (+181 bp) in 2021. Consensus has already started to revise 2021 EPS estimates higher. At the start of earnings season, bottom-up estimates implied 2021 EPS of $162, but that has increased to $165 today.

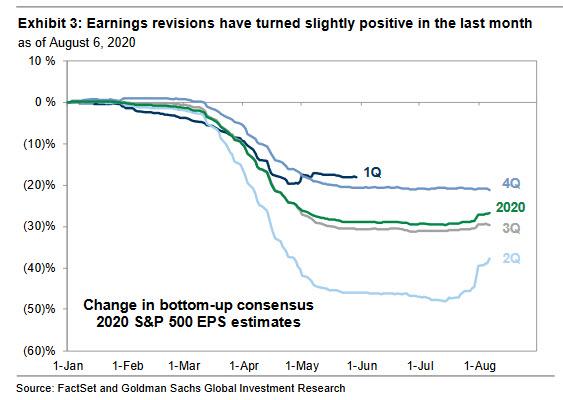

The bank also notes that revisions have been most positive in Energy, Consumer Discretionary, Materials, and Info Tech, and "while positive consensus EPS revisions are rare, they typically occur as the economy emerges from recessions."

Finally, Kostin admits that the US election and a reversal of the 2017 corporate tax cut pose substantial downside risks to both the S&P 500 EPS and the bank's earnings forecast. Even a best case scenario, however, means that it will take nearly two years for earnings to fully recovery: "While we expect aggregate S&P 500 earnings to reach 2019 levels by the end of 2021, we do not expect every sector to recover this quickly. Based on our top-down earnings model. we forecast Info Tech (+10% 2019-2022 CAGR) and Health Care (+10%) earnings will surpass 2019 levels by the end of 2021. However, we expect a more gradual earnings growth in cyclical sectors."

Uncategorized

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

NY Fed Finds Medium, Long-Term Inflation Expectations Jump Amid Surge In Stock Market Optimism

One month after the inflation outlook tracked…

Share this:

One month after the inflation outlook tracked by the NY Fed Consumer Survey extended their late 2023 slide, with 3Y inflation expectations in January sliding to a record low 2.4% (from 2.6% in December), even as 1 and 5Y inflation forecasts remained flat, moments ago the NY Fed reported that in February there was a sharp rebound in longer-term inflation expectations, rising to 2.7% from 2.4% at the three-year ahead horizon, and jumping to 2.9% from 2.5% at the five-year ahead horizon, while the 1Y inflation outlook was flat for the 3rd month in a row, stuck at 3.0%.

The increases in both the three-year ahead and five-year ahead measures were most pronounced for respondents with at most high school degrees (in other words, the "really smart folks" are expecting deflation soon). The survey’s measure of disagreement across respondents (the difference between the 75th and 25th percentile of inflation expectations) decreased at all horizons, while the median inflation uncertainty—or the uncertainty expressed regarding future inflation outcomes—declined at the one- and three-year ahead horizons and remained unchanged at the five-year ahead horizon.

Going down the survey, we find that the median year-ahead expected price changes increased by 0.1 percentage point to 4.3% for gas; decreased by 1.8 percentage points to 6.8% for the cost of medical care (its lowest reading since September 2020); decreased by 0.1 percentage point to 5.8% for the cost of a college education; and surprisingly decreased by 0.3 percentage point for rent to 6.1% (its lowest reading since December 2020), and remained flat for food at 4.9%.

We find the rent expectations surprising because it is happening just asking rents are rising across the country.

At the same time as consumers erroneously saw sharply lower rents, median home price growth expectations remained unchanged for the fifth consecutive month at 3.0%.

Turning to the labor market, the survey found that the average perceived likelihood of voluntary and involuntary job separations increased, while the perceived likelihood of finding a job (in the event of a job loss) declined. "The mean probability of leaving one’s job voluntarily in the next 12 months also increased, by 1.8 percentage points to 19.5%."

Mean unemployment expectations - or the mean probability that the U.S. unemployment rate will be higher one year from now - decreased by 1.1 percentage points to 36.1%, the lowest reading since February 2022. Additionally, the median one-year-ahead expected earnings growth was unchanged at 2.8%, remaining slightly below its 12-month trailing average of 2.9%.

Turning to household finance, we find the following:

- The median expected growth in household income remained unchanged at 3.1%. The series has been moving within a narrow range of 2.9% to 3.3% since January 2023, and remains above the February 2020 pre-pandemic level of 2.7%.

- Median household spending growth expectations increased by 0.2 percentage point to 5.2%. The increase was driven by respondents with a high school degree or less.

- Median year-ahead expected growth in government debt increased to 9.3% from 8.9%.

- The mean perceived probability that the average interest rate on saving accounts will be higher in 12 months increased by 0.6 percentage point to 26.1%, remaining below its 12-month trailing average of 30%.

- Perceptions about households’ current financial situations deteriorated somewhat with fewer respondents reporting being better off than a year ago. Year-ahead expectations also deteriorated marginally with a smaller share of respondents expecting to be better off and a slightly larger share of respondents expecting to be worse off a year from now.

- The mean perceived probability that U.S. stock prices will be higher 12 months from now increased by 1.4 percentage point to 38.9%.

- At the same time, perceptions and expectations about credit access turned less optimistic: "Perceptions of credit access compared to a year ago deteriorated with a larger share of respondents reporting tighter conditions and a smaller share reporting looser conditions compared to a year ago."

Also, a smaller percentage of consumers, 11.45% vs 12.14% in prior month, expect to not be able to make minimum debt payment over the next three months

Last, and perhaps most humorous, is the now traditional cognitive dissonance one observes with these polls, because at a time when long-term inflation expectations jumped, which clearly suggests that financial conditions will need to be tightened, the number of respondents expecting higher stock prices one year from today jumped to the highest since November 2021... which incidentally is just when the market topped out during the last cycle before suffering a painful bear market.

Spread & Containment

A major cruise line is testing a monthly subscription service

The Cruise Scarlet Summer Season Pass was designed with remote workers in mind.

Share this:

While going on a cruise once meant disconnecting from the world when between ports because any WiFi available aboard was glitchy and expensive, advances in technology over the last decade have enabled millions to not only stay in touch with home but even work remotely.

With such remote workers and digital nomads in mind, Virgin Voyages has designed a monthly pass that gives those who want to work from the seas a WFH setup on its Scarlet Lady ship — while the latter acronym usually means "work from home," the cruise line is advertising as "work from the helm.”

Related: Royal Caribbean shares a warning with passengers

"Inspired by Richard Branson's belief and track record that brilliant work is best paired with a hearty dose of fun, we're welcoming Sailors on board Scarlet Lady for a full month to help them achieve that perfect work-life balance," Virgin Voyages said in announcing its new promotion. "Take a vacation away from your monotonous work-from-home set up (sorry, but…not sorry) and start taking calls from your private balcony overlooking the Mediterranean sea."

Shutterstock

This is how much it'll cost you to work from a cruise ship for a month

While the single most important feature for successful work at sea — WiFi — is already available for free on Virgin cruises, the new Scarlet Summer Season Pass includes a faster connection, a $10 daily coffee credit, access to a private rooftop, and other member-only areas as well as wash and fold laundry service that Virgin advertises as a perk that will allow one to concentrate on work

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The pass starts at $9,990 for a two-guest cabin and is available for four monthlong cruises departing in June, July, August, and September — each departs from ports such as Barcelona, Marseille, and Palma de Mallorca and spends four weeks touring around the Mediterranean.

Longer cruises are becoming more common, here's why

The new pass is essentially a version of an upgraded cruise package with additional perks but is specifically tailored to those who plan on working from the ship as an opportunity to market to them.

"Stay connected to your work with the fastest at-sea internet in the biz when you want and log-off to let the exquisite landscape of the Mediterranean inspire you when you need," reads the promotional material for the pass.

Amid the rise of remote work post-pandemic, cruise lines have been seeing growing interest in longer journeys in which many of the passengers not just vacation in the traditional sense but work from a mobile office.

In 2023, Turkish cruise line operator Miray even started selling cabins on a three-year tour around the world but the endeavor hit the rocks after one of the engineers declared the MV Gemini ship the company planned to use for the journey "unseaworthy" and the cruise ship line dealt with a PR scandal that ultimately sank the project before it could take off.

While three years at sea would have set a record as the longest cruise journey on the market, companies such as Royal Caribbean (RCL) (both with its namesake brand and its Celebrity Cruises line) have been offering increasingly long cruises that serve as many people’s temporary homes and cross through multiple continents.

stocks pandemic testingInternational

This is the biggest money mistake you’re making during travel

A retail expert talks of some common money mistakes travelers make on their trips.

Share this:

{kind=link}

Travel is expensive. Despite the explosion of travel demand in the two years since the world opened up from the pandemic, survey after survey shows that financial reasons are the biggest factor keeping some from taking their desired trips.

Airfare, accommodation as well as food and entertainment during the trip have all outpaced inflation over the last four years.

Related: This is why we're still spending an insane amount of money on travel

But while there are multiple tricks and “travel hacks” for finding cheaper plane tickets and accommodation, the biggest financial mistake that leads to blown travel budgets is much smaller and more insidious.

This is what you should (and shouldn’t) spend your money on while abroad

“When it comes to traveling, it's hard to resist buying items so you can have a piece of that memory at home,” Kristen Gall, a retail expert who heads the financial planning section at points-back platform Rakuten, told Travel + Leisure in an interview. “However, it's important to remember that you don't need every souvenir that catches your eye.”

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

According to Gall, souvenirs not only have a tendency to add up in price but also weight which can in turn require one to pay for extra weight or even another suitcase at the airport — over the last two months, airlines like Delta (DAL) , American Airlines (AAL) and JetBlue Airways (JBLU) have all followed each other in increasing baggage prices to in some cases as much as $60 for a first bag and $100 for a second one.

While such extras may not seem like a lot compared to the thousands one might have spent on the hotel and ticket, they all have what is sometimes known as a “coffee” or “takeout effect” in which small expenses can lead one to overspend by a large amount.

‘Save up for one special thing rather than a bunch of trinkets…’

“When traveling abroad, I recommend only purchasing items that you can't get back at home, or that are small enough to not impact your luggage weight,” Gall said. “If you’re set on bringing home a souvenir, save up for one special thing, rather than wasting your money on a bunch of trinkets you may not think twice about once you return home.”

Along with the immediate costs, there is also the risk of purchasing things that go to waste when returning home from an international vacation. Alcohol is subject to airlines’ liquid rules while certain types of foods, particularly meat and other animal products, can be confiscated by customs.

While one incident of losing an expensive bottle of liquor or cheese brought back from a country like France will often make travelers forever careful, those who travel internationally less frequently will often be unaware of specific rules and be forced to part with something they spent money on at the airport.

“It's important to keep in mind that you're going to have to travel back with everything you purchased,” Gall continued. “[…] Be careful when buying food or wine, as it may not make it through customs. Foods like chocolate are typically fine, but items like meat and produce are likely prohibited to come back into the country.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemic france

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Is the National Guard a solution to school violence?

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Vaccine-skeptical mothers say bad health care experiences made them distrust the medical system

Are Voters Recoiling Against Disorder?

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

Survey Shows Declining Concerns Among Americans About COVID-19

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex