Dr. Fauci’s “biodefense-related research”

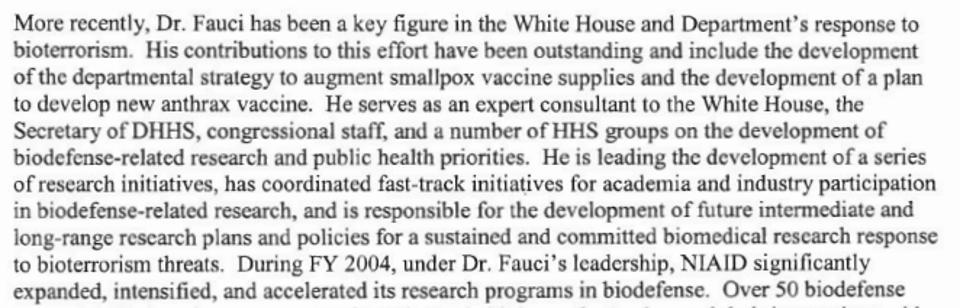

Dr. Kingston’s 2004 letter regarding Dr. Fauci explains some background for his proposed raise:

“More recently, Dr. Fauci has been a key figure in the White House and Department’s response to bioterrorism. His contributions to this effort have been outstanding and include the development of the departmental strategy to augment smallpox vaccine supplies and the development of a plan to develop new anthrax vaccine. He serves as an expert consultant to the White House, the Secretary of DHHS, congressional staff, and a number of HHS groups on the development of biodefense-related research, and public health priorities. He is leading the development of a series of research initiatives, has coordinated fast-track initiatives for academia and industry participation in biodefense-related research, and is responsible for the development of future intermediate and long-range research plans and policies for a sustained and committed biomedical research response to bioterrorism threats. During FY2004, under Dr. Fauci’s leadership, NIAID significantly expanded, intensified, and accelerated its research programs in biodefense.”

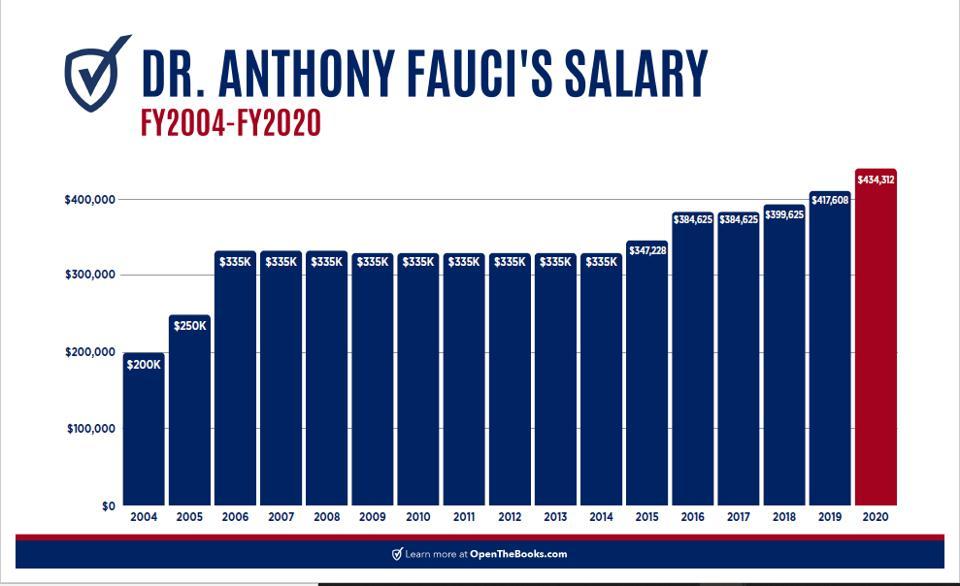

The timeline leading up to Dr. Fauci’s “permanent pay adjustment” is key to understanding Dr. Kingston’s recommendation letter and its approval by Dr. Zerhouni.

- After 9/11 and the ensuing anthrax attacks in the fall of 2001, Dr. Fauci’s NIAID published, in February 2002, a 15-page document for the agency he oversaw at NIH. It was titled “NIAID Strategic Plan for Biodefense Research” and would kick start the NIAID efforts over the next 19 years to try and keep the country safe from bioterrorism.

- Two years later, on December 15, 2004, Dr. Fauci’s increased workload was recognized by a permanent pay adjustment. To this day, Fauci’s portfolio still includes overseeing NIAID’s biodefense research, a portfolio that recently has grown by billions of dollars.

Biodefense Funding and NIAID’s Pandemic Pathogen Research

Over the years, NIH funding has gone towards numerous grants categorized as pandemic-prevention research, including grants for research on bat coronaviruses, both in the U.S. and abroad. Justification for the funding centered around trying to prevent the next pandemic and preventing a possible spillover of viruses from nature to humans.

Some of the biodefense research Dr. Fauci’s NIAID funding came under fire from fellow scientists as too risky. Critics said that Fauci was funding research in labs that was actually creating pandemic pathogens that, if leaked or if fell into the wrong hands, might create the very human pandemic they were trying to prevent.

- In 2014, President Barack Obama’s Administration enacted a federal funding pause for what was termed “gain-of-function” research. It turns out, through waivers and pause exemptions, Dr. Fauci’s institute was funding many of the very scientists doing the potentially risky pandemic research, including the University of North Carolina coronavirus researcher Ralph Baric, who collaborated with Shi Zhengli, the Wuhan Institute of Virology’s so-called “bat lady,” and New York-based EcoHealth Alliance’s Peter Daszak.

- In December 2017, weeks after President Donald Trump’s first Health and Human Services (HHS) Secretary resigned over a private plane charter scandal, and while the agency was still without a confirmed Secretary (Alex Azar was not confirmed and sworn in until January 2018), NIH and Dr. Fauci’s NIAID quietly restarted funding, with guidance, for what was then termed “enhanced potential pandemic pathogens.” News of the funding restart surprised many in the scientific community.

- In 2019, Dr. Fauci’s NIAID secretly approved funding for some of the controversial gain-of-function scientists whose very research caused the scientific community’s concern and led to the funding pause under the Obama Administration in 2014.

- Last month, a rejected 2018 Defense Advanced Research Projects Agency (DARPA) grant proposal was leaked and published online by a collaborate group of scientists and researchers known as DRASTIC, a leak detailed in The Intercept. The DARPA proposal included an idea to create a chimeric bat virus in the lab, to insert a special furin cleavage site, to test it in “humanized” mice, and do this all, in part, to study its potential to emerge as a pandemic.

DARPA documents included in the leak show the agency rejected the grant proposal as too risky, but the fact that most all of the DARPA grant applicants are or were at the time recipients of NIH NIAID funds, under Dr. Fauci, either directly or through subgrants, has raised more than a few eyebrows.

Few of these controversies made it into mainstream news cycles, most likely never would have except that in December 2019 the world learned of a novel respiratory coronavirus emerging in Wuhan, China – the very same city that had a lab that did pandemic bat virus research. Ironically, the Wuhan lab was funded with $600,000 in NIAID subgrants from Fauci’s agency’s biodefense funds, as the doctor himself admitted to Congress.

Further background

On January 27 and May 17, 2021, we asked NIH for Dr. Fauci’s fiscal year 2020 and 2021 financial and conflict-of-interest disclosure forms; job descriptions; and all employment contracts, amendments, modifications, and addendums; respectively.

Dr. Fauci is required by federal law to file these forms with his employer, the National Institutes of Health. It has been nine months and NIH has yet to produce most of the requested documents.

To say that that the details of Dr. Fauci’s employment are of the public interest – after almost two years of government decisions influenced by him – is an understatement.

Note: Dr. Fauci and his agency did not respond to our request for comment before publication.

{kind=link}

{kind=link}