Government

Delta Variant Saps Risk Taking Appetites, Sending the Greenback Higher even as Rates Fall

Overview: Concerns that the Delta mutation will slow or even reverse the recovery efforts appear to be sapping risk-taking appetites. Equities are under pressure. Nearly all the markets in the Asia Pacific region and Europe are lower. The MSCI Asia…

Share this:

Overview: Concerns that the Delta mutation will slow or even reverse the recovery efforts appear to be sapping risk-taking appetites. Equities are under pressure. Nearly all the markets in the Asia Pacific region and Europe are lower. The MSCI Asia Pacific is paring last week's 1.4% advance, while the Dow Jones Stoxx 600 in Europe is off for the fourth consecutive session at six-week lows. Only the consumer staples and health care sectors are posting small gains. The S&P 500 futures are off nearly 0.5%. The Dow futures are off more, while the NASDAQ futures are down a little less. Bonds are bid, and the US 10-year yield is around three basis points lows near 1.26%. Core European benchmark yields are softer, and most are trading at new three-month lows today. Peripheral bonds have come under pressure as the European morning progressed. The dollar rides high, with the Scandis and dollar-bloc currencies off leading the move with losses of mostly 0.3%-0.7%, with the Canadian dollar being tagged for more than 1%. The yen is the notable exception, and it is posting modest gains. Emerging market currencies are all lower, led by the Czech koruna and South Korean won. Gold, which had been flirting with $1835 a couple of sessions ago, is testing the $1800 area. The OPEC+ agreement is pushing oil lower. September WTI is trading below $70. The next technical target is seen in the $66.80-$68.60 area. Copper is off for the fifth session in the past six.

Asia Pacific

OPEC+ struck a deal yesterday that had been rumored last week. The output will increase by 400k barrels a day next month. Gradually, the 5.8 mln barrels a day that have been shuttered will come back to the market. The key to the deal was the baseline of not just the protesting UAE, but others will be adjusted higher. The UAE's baseline from where cuts will be measured was boosted to 3.5 mln barrels a day from 3.17 mln, and not quite what it had initially sought (3.8 mln). Saudi Arabia and Russia saw their baselines increase by 500k barrels to11.5 mln. September WTI fell 3% last week, the most in three months. It was the second weekly decline after a nine-of-ten-week advance (~21%). While the political compromise resolves the immediate crisis, there are fissures with the bloc and, for many, the baseline may be than a little embellished.

The surge of the Delta virus and reports of a "Delta plus" mutation gaining ground is emerging as a powerful economic and political factor. The Reserve Bank of Australia meets on August 3, and there are already forecasts that it will take back its recent decision to taper (from A$5 bln a week to A$4 bln). The governing coalition is slipping in the polls, and the opposition Labour is now six percentage points ahead. According to Newspoll, satisfaction with the vaccine rollout has fallen to 40% from 53% in April. Meanwhile, two polls show support for the Japanese cabinet is continuing to decline, and the pre-Olympic build-up is marred with new covid cases among athletes. The Kyodo poll showed support for the cabinet falling more than eight percentage points to 35.9%. A Mainichi Shimbun poll had the support rating falling four points to 30.

The dollar is trading near session lows against the Japanese yen in the European morning but has not taken out last week's lows near JPY109.70. Below there is this month's low, slightly above JPY109.50, which stands in the way of a move toward JPY109. The Australian dollar finished last week at new lows for the year, and follow-through selling has pushed it beyond the (61.8%) retracement target of the rally since the end of last October (~$0.7380). The next important support area is not until closer to the $0.7230-$0.7250 area. The US dollar firmed for the second consecutive session against the Chinese yuan. It is at a six-day high near CNY6.4850. The greenback has been trading in the CNY6.45-CNY6.50 range for the past several weeks. The PBOC's dollar reference range was the tightest to expectations (CNY6.4700 vs. CNY6.4705) for several sessions.

Europe

A bit of a caricature of"Freedom Day" in the UK has materialized. The health minister Javid, who recently returned to the government, acknowledged he tested positive for covid. Prime Minister Johnson and the Chancellor of the Exchequer have also been ordered into quarantine due to their contact with Javid. "Freedom Day" drops the mandatory mask-wearing and social distancing requirements. Ironically, Israel, one of the most vaccinated countries, has reimposed some restrictions (e.g., mask-wearing indoors) dubbed "soft suppression" to avoid a fourth national lockdown due to the contagion of the new variant. Separately, there seems to be a dispute in the UK government over a potential GBP10 bln healthcare tax that the Prime Minister and Health Minister Javid are pushing for, but meeting resistance from the Chancellor of the Exchequer Sunak. In Germany, the polls have yet to show the impact of the flooding. The national election is in just over two months. CDU/CSU candidate Laschet's attempt at jest seemed to go over like a lead balloon. The Green's maybe in the best position to gain.

The economic highlight of the week is the ECB meeting followed the preliminary PMI. The central bank needs to bring its forward guidance into line with its redefined symmetrical inflation target of 2%. The adjustment is expected to begin preparing the groundwork that lifts the bar to an exit from the extraordinary monetary policy. In fact, it seems likely that what was once regarded as extraordinary--bond purchases, long-term loans at negative rates, and a negative deposit rate--will be part of the standard operating procedure even after the Pandemic Emergency Purchase Program is completed next year. As we have noted, the ECB has not hiked rates since 2011, and even then, the move was seen as a mistake, and Draghi unwound the two hikes in his first two meetings as ECB President. The Bloomberg survey found a median expectation for the manufacturing PMI to ease a bit, while the service PMI is expected to quicken. The net result is a marginal new high in the composite PMI.

The euro's 0.6% loss from last week is being extended today, and the single currency looks to be heading toward the low for the year set at the end of March near $1.1700. There may be some chart support around $1.1740. A move above $1.1820 would help stabilize the tone. We note that the latest Commitment of Traders shows that as of July 13, the net long speculative euro position is the smallest since last March at around 59.7k contracts, down from 165k contracts in early January. The fifth loss in six sessions has brought sterling to nearly $1.37, where the 200-day moving average is found. Sterling had not traded below this moving average since last September, when it was closer to $1.27. The sell-off is pushing sterling through the lower Bollinger Band (~$1.3715). There is some old congestion around $1.3670 that may offer some near-term support. However, the next important chart area is not until closer to $1.3550. The net long speculative sterling position in the futures market fell by nearly 2/3 in the CFTC reporting week through July 13. At below 8k contracts, it is the smallest since early January.

America

A simmering dispute over the terms of the new North American free-trade agreement broke into the open last week. Ironically for many observers, in some important respects, the Biden administration is taking a tougher line on trade than Trump. This applies not only to China, where sanctions have been extended, and as we learned last week, there are no plans for regular high-level meetings on economic matters, as there were under Bush and Obama. Mexico and Canada argue that the Biden administration is backtracking from the understanding struck with Trump officials about the technical rules for cars and parts shipped across the regional borders. As a result, they are threatening to launch a formal complaint under the terms of the treaty. If the case goes against them, it will be harder for Mexico and Canada to meet the thresholds. Yet rather than necessarily move production capacity to the US, as the US administration and the United Auto Workers seem to assume, producers in Mexico and Canada could forfeit the advantage and pay the WTO tariff schedule of 2.5% on passenger vehicles (and a much stepper 25% on light trucks).

The US economic calendar is dominated by housing markets reports (starts and sales) and the preliminary PMI at the end of the week. In addition to bills, the government auctions 20-year bonds and 10-year TIPS. Fed officials enter the quiet period ahead of July 27-28 FOMC meeting. The highlight for Canada is the May retail sales report on Friday, which is expected to be soft. Mexico also reports May retail sales at the end of the week, but before that, it will report the biweekly CPI measure. Banxico meets on August 12, and the market appears to have about a 50% chance of a 25 bp hike discounted. Brazil reports July inflation figures, and another rise is expected (8.50% vs. 8.13%), which underscores expectations for another 75 bp when the central bank meets on August 4.

The US dollar has soared against the Canadian dollar, jumping through the 200-day moving average (CAD1.2625) to reach CAD1.2780, its highest level since early February. The weakness in equities and oil are sources of pressure. The next important chart point is not until closer to CAD1.2850, the (61.8%) retracement objective of the US dollar slump since the end of last October. The greenback is now well beyond the upper Bollinger Band (~CAD1.2680). The CAD1.28-area corresponds to three standard deviations from the 20-day moving average. The net long speculative position in the futures market was chopped by nearly 15k contracts in the week through last Tuesday, the most since last March. It stands near 26.4k, the smallest since early May. The US dollar is firm against the Mexican peso, but it remains below last week's high (~MXN20.0820). The greenback continues to trade within last Tuesday's range (~MXN19.8150-MXN20.8020). Speculators in the futures market have been net short the peso since the end of April.

Disclaimer

bonds pandemic dow jones sp 500 nasdaq equities monetary policy fomc fed currencies us dollar canadian dollar euro yuan trump vaccine testing social distancing quarantine lockdown suppression recovery gold oil brazil mexico canada european europe uk germany czech russia china

International

Four Years Ago This Week, Freedom Was Torched

Four Years Ago This Week, Freedom Was Torched

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare…

Share this:

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare quotes the soothsayer’s warning Julius Caesar about what turned out to be an impending assassination on March 15. The death of American liberty happened around the same time four years ago, when the orders went out from all levels of government to close all indoor and outdoor venues where people gather.

It was not quite a law and it was never voted on by anyone. Seemingly out of nowhere, people who the public had largely ignored, the public health bureaucrats, all united to tell the executives in charge – mayors, governors, and the president – that the only way to deal with a respiratory virus was to scrap freedom and the Bill of Rights.

And they did, not only in the US but all over the world.

The forced closures in the US began on March 6 when the mayor of Austin, Texas, announced the shutdown of the technology and arts festival South by Southwest. Hundreds of thousands of contracts, of attendees and vendors, were instantly scrapped. The mayor said he was acting on the advice of his health experts and they in turn pointed to the CDC, which in turn pointed to the World Health Organization, which in turn pointed to member states and so on.

There was no record of Covid in Austin, Texas, that day but they were sure they were doing their part to stop the spread. It was the first deployment of the “Zero Covid” strategy that became, for a time, official US policy, just as in China.

It was never clear precisely who to blame or who would take responsibility, legal or otherwise.

This Friday evening press conference in Austin was just the beginning. By the next Thursday evening, the lockdown mania reached a full crescendo. Donald Trump went on nationwide television to announce that everything was under control but that he was stopping all travel in and out of US borders, from Europe, the UK, Australia, and New Zealand. American citizens would need to return by Monday or be stuck.

Americans abroad panicked while spending on tickets home and crowded into international airports with waits up to 8 hours standing shoulder to shoulder. It was the first clear sign: there would be no consistency in the deployment of these edicts.

There is no historical record of any American president ever issuing global travel restrictions like this without a declaration of war. Until then, and since the age of travel began, every American had taken it for granted that he could buy a ticket and board a plane. That was no longer possible. Very quickly it became even difficult to travel state to state, as most states eventually implemented a two-week quarantine rule.

The next day, Friday March 13, Broadway closed and New York City began to empty out as any residents who could went to summer homes or out of state.

On that day, the Trump administration declared the national emergency by invoking the Stafford Act which triggers new powers and resources to the Federal Emergency Management Administration.

In addition, the Department of Health and Human Services issued a classified document, only to be released to the public months later. The document initiated the lockdowns. It still does not exist on any government website.

The White House Coronavirus Response Task Force, led by the Vice President, will coordinate a whole-of-government approach, including governors, state and local officials, and members of Congress, to develop the best options for the safety, well-being, and health of the American people. HHS is the LFA [Lead Federal Agency] for coordinating the federal response to COVID-19.

Closures were guaranteed:

Recommend significantly limiting public gatherings and cancellation of almost all sporting events, performances, and public and private meetings that cannot be convened by phone. Consider school closures. Issue widespread ‘stay at home’ directives for public and private organizations, with nearly 100% telework for some, although critical public services and infrastructure may need to retain skeleton crews. Law enforcement could shift to focus more on crime prevention, as routine monitoring of storefronts could be important.

In this vision of turnkey totalitarian control of society, the vaccine was pre-approved: “Partner with pharmaceutical industry to produce anti-virals and vaccine.”

The National Security Council was put in charge of policy making. The CDC was just the marketing operation. That’s why it felt like martial law. Without using those words, that’s what was being declared. It even urged information management, with censorship strongly implied.

The timing here is fascinating. This document came out on a Friday. But according to every autobiographical account – from Mike Pence and Scott Gottlieb to Deborah Birx and Jared Kushner – the gathered team did not meet with Trump himself until the weekend of the 14th and 15th, Saturday and Sunday.

According to their account, this was his first real encounter with the urge that he lock down the whole country. He reluctantly agreed to 15 days to flatten the curve. He announced this on Monday the 16th with the famous line: “All public and private venues where people gather should be closed.”

This makes no sense. The decision had already been made and all enabling documents were already in circulation.

There are only two possibilities.

One: the Department of Homeland Security issued this March 13 HHS document without Trump’s knowledge or authority. That seems unlikely.

Two: Kushner, Birx, Pence, and Gottlieb are lying. They decided on a story and they are sticking to it.

Trump himself has never explained the timeline or precisely when he decided to greenlight the lockdowns. To this day, he avoids the issue beyond his constant claim that he doesn’t get enough credit for his handling of the pandemic.

With Nixon, the famous question was always what did he know and when did he know it? When it comes to Trump and insofar as concerns Covid lockdowns – unlike the fake allegations of collusion with Russia – we have no investigations. To this day, no one in the corporate media seems even slightly interested in why, how, or when human rights got abolished by bureaucratic edict.

As part of the lockdowns, the Cybersecurity and Infrastructure Security Agency, which was and is part of the Department of Homeland Security, as set up in 2018, broke the entire American labor force into essential and nonessential.

They also set up and enforced censorship protocols, which is why it seemed like so few objected. In addition, CISA was tasked with overseeing mail-in ballots.

Only 8 days into the 15, Trump announced that he wanted to open the country by Easter, which was on April 12. His announcement on March 24 was treated as outrageous and irresponsible by the national press but keep in mind: Easter would already take us beyond the initial two-week lockdown. What seemed to be an opening was an extension of closing.

This announcement by Trump encouraged Birx and Fauci to ask for an additional 30 days of lockdown, which Trump granted. Even on April 23, Trump told Georgia and Florida, which had made noises about reopening, that “It’s too soon.” He publicly fought with the governor of Georgia, who was first to open his state.

Before the 15 days was over, Congress passed and the president signed the 880-page CARES Act, which authorized the distribution of $2 trillion to states, businesses, and individuals, thus guaranteeing that lockdowns would continue for the duration.

There was never a stated exit plan beyond Birx’s public statements that she wanted zero cases of Covid in the country. That was never going to happen. It is very likely that the virus had already been circulating in the US and Canada from October 2019. A famous seroprevalence study by Jay Bhattacharya came out in May 2020 discerning that infections and immunity were already widespread in the California county they examined.

What that implied was two crucial points: there was zero hope for the Zero Covid mission and this pandemic would end as they all did, through endemicity via exposure, not from a vaccine as such. That was certainly not the message that was being broadcast from Washington. The growing sense at the time was that we all had to sit tight and just wait for the inoculation on which pharmaceutical companies were working.

By summer 2020, you recall what happened. A restless generation of kids fed up with this stay-at-home nonsense seized on the opportunity to protest racial injustice in the killing of George Floyd. Public health officials approved of these gatherings – unlike protests against lockdowns – on grounds that racism was a virus even more serious than Covid. Some of these protests got out of hand and became violent and destructive.

Meanwhile, substance abuse rage – the liquor and weed stores never closed – and immune systems were being degraded by lack of normal exposure, exactly as the Bakersfield doctors had predicted. Millions of small businesses had closed. The learning losses from school closures were mounting, as it turned out that Zoom school was near worthless.

It was about this time that Trump seemed to figure out – thanks to the wise council of Dr. Scott Atlas – that he had been played and started urging states to reopen. But it was strange: he seemed to be less in the position of being a president in charge and more of a public pundit, Tweeting out his wishes until his account was banned. He was unable to put the worms back in the can that he had approved opening.

By that time, and by all accounts, Trump was convinced that the whole effort was a mistake, that he had been trolled into wrecking the country he promised to make great. It was too late. Mail-in ballots had been widely approved, the country was in shambles, the media and public health bureaucrats were ruling the airwaves, and his final months of the campaign failed even to come to grips with the reality on the ground.

At the time, many people had predicted that once Biden took office and the vaccine was released, Covid would be declared to have been beaten. But that didn’t happen and mainly for one reason: resistance to the vaccine was more intense than anyone had predicted. The Biden administration attempted to impose mandates on the entire US workforce. Thanks to a Supreme Court ruling, that effort was thwarted but not before HR departments around the country had already implemented them.

As the months rolled on – and four major cities closed all public accommodations to the unvaccinated, who were being demonized for prolonging the pandemic – it became clear that the vaccine could not and would not stop infection or transmission, which means that this shot could not be classified as a public health benefit. Even as a private benefit, the evidence was mixed. Any protection it provided was short-lived and reports of vaccine injury began to mount. Even now, we cannot gain full clarity on the scale of the problem because essential data and documentation remains classified.

After four years, we find ourselves in a strange position. We still do not know precisely what unfolded in mid-March 2020: who made what decisions, when, and why. There has been no serious attempt at any high level to provide a clear accounting much less assign blame.

Not even Tucker Carlson, who reportedly played a crucial role in getting Trump to panic over the virus, will tell us the source of his own information or what his source told him. There have been a series of valuable hearings in the House and Senate but they have received little to no press attention, and none have focus on the lockdown orders themselves.

The prevailing attitude in public life is just to forget the whole thing. And yet we live now in a country very different from the one we inhabited five years ago. Our media is captured. Social media is widely censored in violation of the First Amendment, a problem being taken up by the Supreme Court this month with no certainty of the outcome. The administrative state that seized control has not given up power. Crime has been normalized. Art and music institutions are on the rocks. Public trust in all official institutions is at rock bottom. We don’t even know if we can trust the elections anymore.

In the early days of lockdown, Henry Kissinger warned that if the mitigation plan does not go well, the world will find itself set “on fire.” He died in 2023. Meanwhile, the world is indeed on fire. The essential struggle in every country on earth today concerns the battle between the authority and power of permanent administration apparatus of the state – the very one that took total control in lockdowns – and the enlightenment ideal of a government that is responsible to the will of the people and the moral demand for freedom and rights.

How this struggle turns out is the essential story of our times.

CODA: I’m embedding a copy of PanCAP Adapted, as annotated by Debbie Lerman. You might need to download the whole thing to see the annotations. If you can help with research, please do.

* * *

Jeffrey Tucker is the author of the excellent new book 'Life After Lock-Down'

Government

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Authored by Jack Phillips via The Epoch Times (emphasis ours),

A…

Share this:

Authored by Jack Phillips via The Epoch Times (emphasis ours),

A U.S. Centers for Disease Control (CDC) paper released Thursday found that thousands of young children have been taken to the emergency room over the past several years after taking the very common sleep-aid supplement melatonin.

The agency said that melatonin, which can come in gummies that are meant for adults, was implicated in about 7 percent of all emergency room visits for young children and infants “for unsupervised medication ingestions,” adding that many incidents were linked to the ingestion of gummy formulations that were flavored. Those incidents occurred between the years 2019 and 2022.

Melatonin is a hormone produced by the human body to regulate its sleep cycle. Supplements, which are sold in a number of different formulas, are generally taken before falling asleep and are popular among people suffering from insomnia, jet lag, chronic pain, or other problems.

The supplement isn’t regulated by the U.S. Food and Drug Administration and does not require child-resistant packaging. However, a number of supplement companies include caps or lids that are difficult for children to open.

The CDC report said that a significant number of melatonin-ingestion cases among young children were due to the children opening bottles that had not been properly closed or were within their reach. Thursday’s report, the agency said, “highlights the importance of educating parents and other caregivers about keeping all medications and supplements (including gummies) out of children’s reach and sight,” including melatonin.

The approximately 11,000 emergency department visits for unsupervised melatonin ingestions by infants and young children during 2019–2022 highlight the importance of educating parents and other caregivers about keeping all medications and supplements (including gummies) out of children’s reach and sight.

The CDC notes that melatonin use among Americans has increased five-fold over the past 25 years or so. That has coincided with a 530 percent increase in poison center calls for melatonin exposures to children between 2012 and 2021, it said, as well as a 420 percent increase in emergency visits for unsupervised melatonin ingestion by young children or infants between 2009 and 2020.

Some health officials advise that children under the age of 3 should avoid taking melatonin unless a doctor says otherwise. Side effects include drowsiness, headaches, agitation, dizziness, and bed wetting.

Other symptoms of too much melatonin include nausea, diarrhea, joint pain, anxiety, and irritability. The supplement can also impact blood pressure.

However, there is no established threshold for a melatonin overdose, officials have said. Most adult melatonin supplements contain a maximum of 10 milligrams of melatonin per serving, and some contain less.

Many people can tolerate even relatively large doses of melatonin without significant harm, officials say. But there is no antidote for an overdose. In cases of a child accidentally ingesting melatonin, doctors often ask a reliable adult to monitor them at home.

Dr. Cora Collette Breuner, with the Seattle Children’s Hospital at the University of Washington, told CNN that parents should speak with a doctor before giving their children the supplement.

“I also tell families, this is not something your child should take forever. Nobody knows what the long-term effects of taking this is on your child’s growth and development,” she told the outlet. “Taking away blue-light-emitting smartphones, tablets, laptops, and television at least two hours before bed will keep melatonin production humming along, as will reading or listening to bedtime stories in a softly lit room, taking a warm bath, or doing light stretches.”

In 2022, researchers found that in 2021, U.S. poison control centers received more than 52,000 calls about children consuming worrisome amounts of the dietary supplement. That’s a six-fold increase from about a decade earlier. Most such calls are about young children who accidentally got into bottles of melatonin, some of which come in the form of gummies for kids, the report said.

Dr. Karima Lelak, an emergency physician at Children’s Hospital of Michigan and the lead author of the study published in 2022 by the CDC, found that in about 83 percent of those calls, the children did not show any symptoms.

However, other children had vomiting, altered breathing, or other symptoms. Over the 10 years studied, more than 4,000 children were hospitalized, five were put on machines to help them breathe, and two children under the age of two died. Most of the hospitalized children were teenagers, and many of those ingestions were thought to be suicide attempts.

Those researchers also suggested that COVID-19 lockdowns and virtual learning forced more children to be at home all day, meaning there were more opportunities for kids to access melatonin. Also, those restrictions may have caused sleep-disrupting stress and anxiety, leading more families to consider melatonin, they suggested.

The Associated Press contributed to this report.

International

Red Candle In The Wind

Red Candle In The Wind

By Benjamin PIcton of Rabobank

February non-farm payrolls superficially exceeded market expectations on Friday by…

Share this:

{kind=link}

{kind=link}

{kind=link}

By Benjamin PIcton of Rabobank

February non-farm payrolls superficially exceeded market expectations on Friday by printing at 275,000 against a consensus call of 200,000. We say superficially, because the downward revisions to prior months totalled 167,000 for December and January, taking the total change in employed persons well below the implied forecast, and helping the unemployment rate to pop two-ticks to 3.9%. The U6 underemployment rate also rose from 7.2% to 7.3%, while average hourly earnings growth fell to 0.2% m-o-m and average weekly hours worked languished at 34.3, equalling pre-pandemic lows.

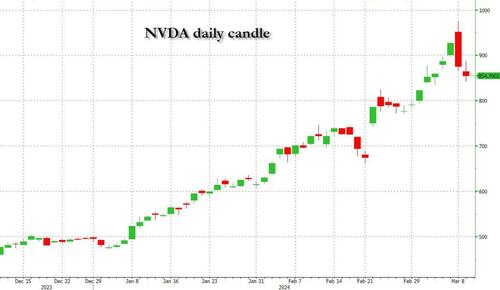

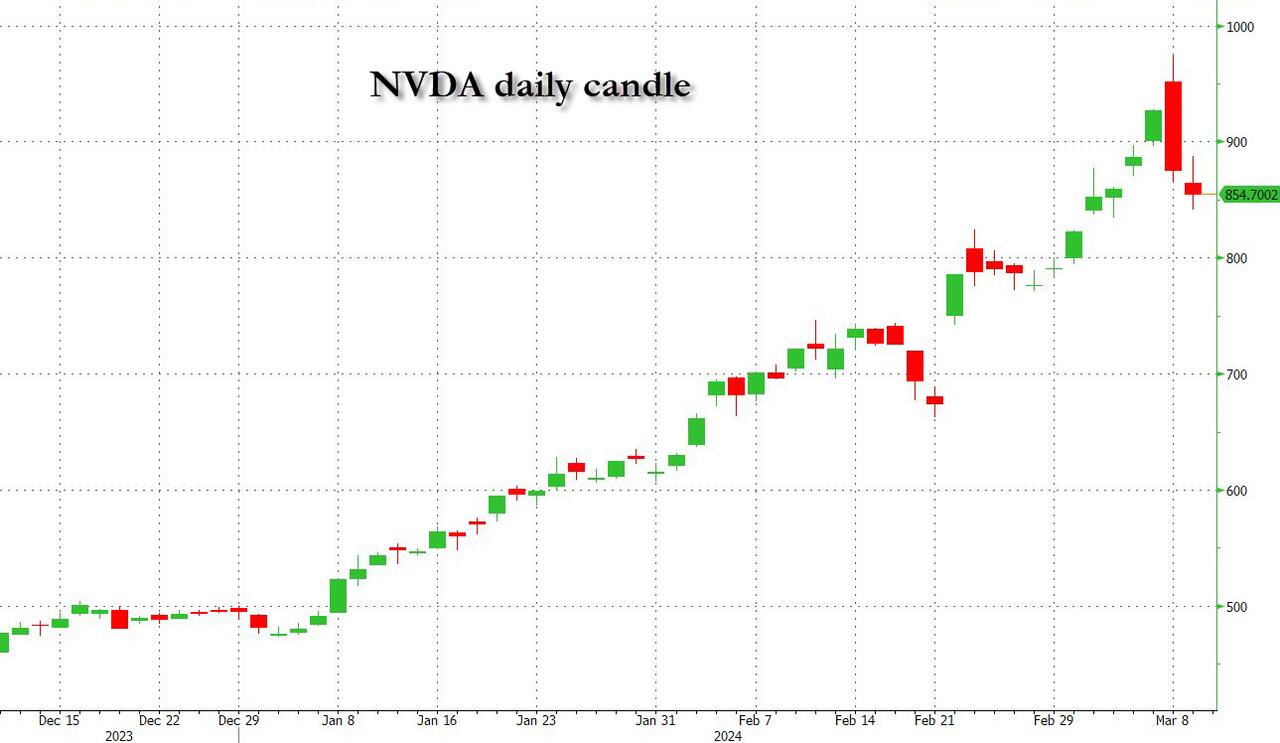

Undeterred by the devil in the detail, the algos sprang into action once exchanges opened. Market darling NVIDIA hit a new intraday high of $974 before (presumably) the humans took over and sold the stock down more than 10% to close at $875.28. If our suspicions are correct that it was the AIs buying before the humans started selling (no doubt triggering trailing stops on the way down), the irony is not lost on us.

The 1-day chart for NVIDIA now makes for interesting viewing, because the red candle posted on Friday presents quite a strong bearish engulfing signal. Volume traded on the day was almost double the 15-day simple moving average, and similar price action is observable on the 1-day charts for both Intel and AMD. Regular readers will be aware that we have expressed incredulity in the past about the durability the AI thematic melt-up, so it will be interesting to see whether Friday’s sell off is just a profit-taking blip, or a genuine trend reversal.

{kind=link}

AI equities aside, this week ought to be important for markets because the BTFP program expires today. That means that the Fed will no longer be loaning cash to the banking system in exchange for collateral pledged at-par. The KBW Regional Banking index has so far taken this in its stride and is trading 30% above the lows established during the mini banking crisis of this time last year, but the Fed’s liquidity facility was effectively an exercise in can-kicking that makes regional banks a sector of the market worth paying attention to in the weeks ahead. Even here in Sydney, regulators are warning of external risks posed to the banking sector from scheduled refinancing of commercial real estate loans following sharp falls in valuations.

Markets are sending signals in other sectors, too. Gold closed at a new record-high of $2178/oz on Friday after trading above $2200/oz briefly. Gold has been going ballistic since the Friday before last, posting gains even on days where 2-year Treasury yields have risen. Gold bugs are buying as real yields fall from the October highs and inflation breakevens creep higher. This is particularly interesting as gold ETFs have been recording net outflows; suggesting that price gains aren’t being driven by a retail pile-in. Are gold buyers now betting on a stagflationary outcome where the Fed cuts without inflation being anchored at the 2% target? The price action around the US CPI release tomorrow ought to be illuminating.

Leaving the day-to-day movements to one side, we are also seeing further signs of structural change at the macro level. The UK budget last week included a provision for the creation of a British ISA. That is, an Individual Savings Account that provides tax breaks to savers who invest their money in the stock of British companies. This follows moves last year to encourage pension funds to head up the risk curve by allocating 5% of their capital to unlisted investments.

As a Hail Mary option for a government cruising toward an electoral drubbing it’s a curious choice, but it’s worth highlighting as cash-strapped governments increasingly see private savings pools as a funding solution for their spending priorities.

Of course, the UK is not alone in making creeping moves towards financial repression. In contrast to announcements today of increased trade liberalisation, Australian Treasurer Jim Chalmers has in the recent past flagged his interest in tapping private pension savings to fund state spending priorities, including defence, public housing and renewable energy projects. Both the UK and Australia appear intent on finding ways to open up the lungs of their economies, but government wants more say in directing private capital flows for state goals.

So, how far is the blurring of the lines between free markets and state planning likely to go? Given the immense and varied budgetary (and security) pressures that governments are facing, could we see a re-up of WWII-era Victory bonds, where private investors are encouraged to do their patriotic duty by directly financing government at negative real rates?

That would really light a fire under the gold market.

Red Candle In The Wind

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Four Years Ago This Week, Freedom Was Torched

Is the National Guard a solution to school violence?

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

The next pandemic? It’s already here for Earth’s wildlife

Mathematicians use AI to identify emerging COVID-19 variants

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

International4 days ago

International4 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International4 days ago

International4 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges