Clorox Stock- Anything But A Value Stock

In The Graduate, a young Dustin Hoffman, upon his college graduation, is taken aside by a family friend for career advice. The friend offers Dustin one…

Share this:

In The Graduate, a young Dustin Hoffman, upon his college graduation, is taken aside by a family friend for career advice. The friend offers Dustin one word; “plastics.” He encourages Hoffman’s character to pursue a career in the explosive growth, up-and-coming plastics industry. We may want to think of similar advice for our children and their friends with graduation ceremonies upon us. It is also incumbent on us to consider the same advice regarding our portfolios. If we have a longer-term window and can ignore short-term volatility, should we invest in a volatile growth stock like Nvidia or a stable low growth company like Clorox?

Many investment pundits may rephrase the question as a choice between a value stock and a growth stock. The terms “value” and “growth” have become blurred in recent years. What appears to be a value stock may be in its reputation only.

Valuations Matters

Most readers with long-term investment horizons will answer our earlier question by selecting the semiconductor giant Nvidia.

We confidently state that the semiconductor industry will grow multiples of the bleach industry.

However, the value growth investment question is not which stock is considered growth or value, but which is priced cheaper given their distinctly different growth rates. At the right price, Clorox may be a much better investment than Nvidia, despite Nvidia’s substantial growth potential.

Unfortunately, many passive investors assume companies with long successful histories and mature products in low-growth industries are value stocks. Conversely, a semiconductor company or other high-growth technology must be a growth company in many investors’ eyes. Such assumptions get investors in trouble.

Nvidia or Clorox: Where is the Value?

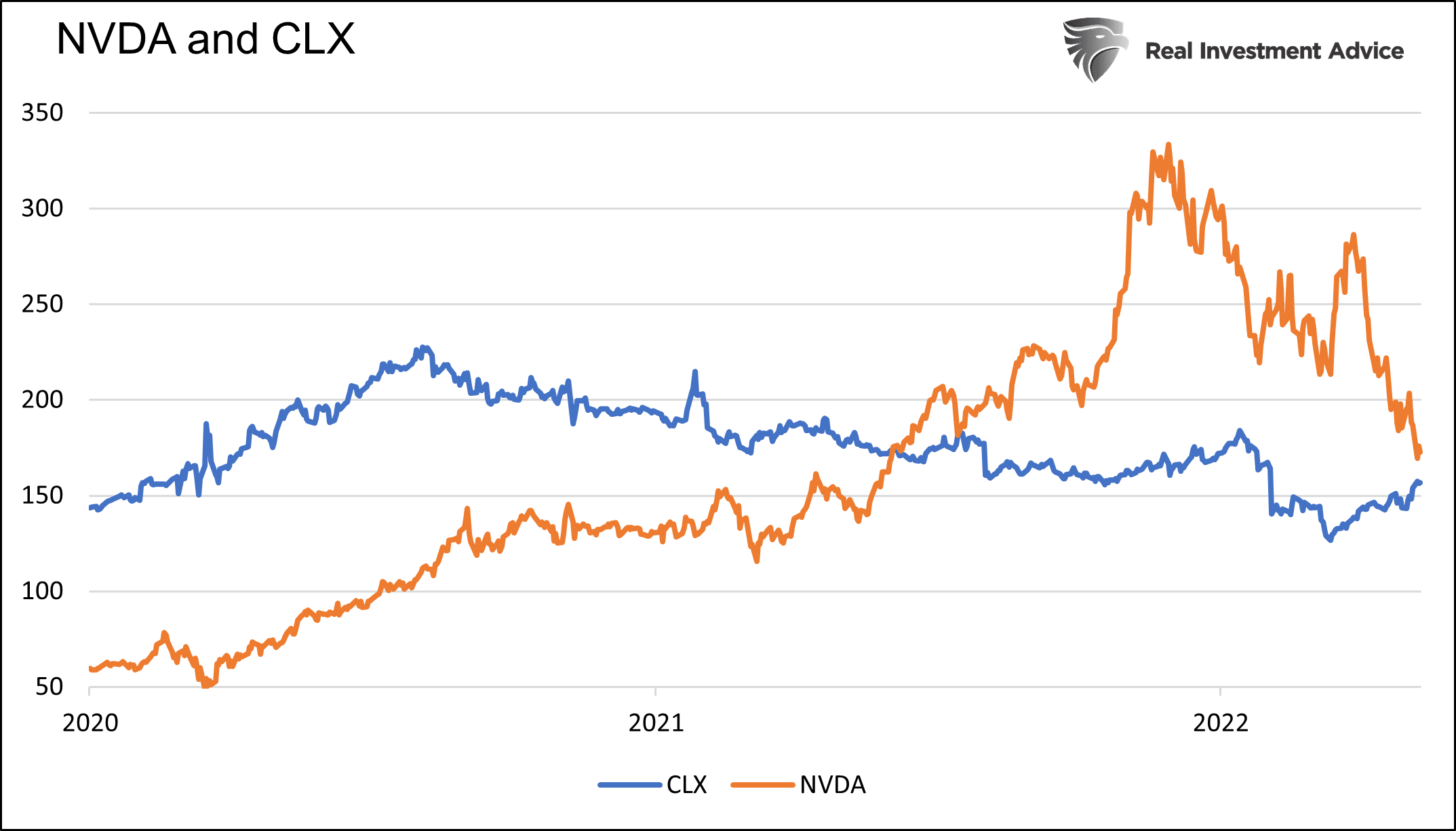

To help answer our question, we start with a cursory view of their share prices since 2020.

As the graph below shows, CLX had a nice run during the height of the pandemic as bleach was in high demand. After a 60% surge, it gradually erased the gains and is back to similar levels as two years ago.

NVDA initially fell by 35% in March 2020 but stormed back, growing from $50 to a peak of $333. Since hitting a record high in November 2021, it has fallen nearly 50%, although still trading at a reasonable premium to its pre-pandemic levels.

Fundamentals

While most investors stare at stock prices all day, fundamentals are what matter. Simply, what are you getting for the price? This is where the Nvidia and Clorox valuations and recent performance get interesting. Further, it is where the line between value and growth gets hazy.

Since 2020, NVDA has grown its revenue by 146%, while CLX has grown revenue by 15%. Sales are a significant consideration in stock analysis, but how well sales revenue translates into bottom-line growth is more important. NVDA has grown EBITDA by 242%, while CLX has seen a 23% decline in EBITDA over the same period. Earnings are a function of sales and margins. Operating margins at NVDA are up nearly 11 points since 2020, while CLX has dropped 7.5.

NVDA’s Price to Earnings ratio (P/E) has fallen by 14 since 2020. At the same time, CLX has risen by 13.5.

Current Valuations

The above data certainly points to NVDA as the higher growth company with more robust fundamentals. However, we want to stress that price and fundamentals matter, but only in the context of valuations.

A company can have poor growth rates and weakening margins, but it may be an excellent investment at a low enough valuation. Conversely, a company like Tesla is experiencing tremendous growth, but its market cap equals that of the entire auto industry.

With that background, let’s compare NVDA and CLX valuations.

If you only looked at the table above and didn’t know which companies they were, you would likely struggle to pick the value stock. NVDA has a higher P/E but a lower forward P/E. NVDA also has a much lower price to book value but a much higher price to sales ratio.

To help break the tie, let’s compare their PEG ratios. The PEG ratio or price to earnings growth is the price to earnings ratio divided by earnings growth. This ratio helps make sense of P/E within the context of expected growth. A P/E of 100 may be cheap, for instance, if earnings are growing at 200%. Conversely, a P/E of five may be expensive if earnings are shrinking.

A PEG ratio of one typically defines the border between over and undervaluation. By this metric, both companies are overvalued, with ratios well above one. However, NVDA’s PEG ratio is decently lower than CLX.

We believe that NVDA is trading at a lower valuation than Clorox based on the data above.

SimpleVisor Models

To add to the analysis, we share our internal model. The model helps assess if stocks are rich or cheap to their long-running normalized valuations. The model assigns a fair value price based on its normalized P/E ratio. It then tracks how the stock price trades around that ratio.

In the Clorox graph below, the stock price (black line) tended to gravitate around the gray fair value line from 2012 to 2019. When it was above the gray line, we would say Clorox stock is overvalued and vice versa for when it is below. Currently, Clorox is over two standard deviations or 60% above the model’s fair value.

The following graph shows a similar analysis for NVDA. From 2012 to 2019, it also bounced around its fair value level. However, once the pandemic struck, it traded well above fair value. Until November 2021, Nvidia stock, like Clorox, was over two standard deviations above its fair value. Since then, it has fallen back much closer to fair value, currently trading at a 19% premium.

Neither stock is cheap using this model, but the model asserts Nvidia, not Clorox is the more reasonable of the two companies. Dare we say if we must pick a value stock from the two choices, it would be Nvidia, not Clorox.

Summary

NVDA is growing earnings and revenues much faster than Clorox. That in and of itself is not a surprise. The real revelation is that these two companies trade at similar valuations despite vastly different growth trajectories.

Given that NVDA is proliferating and CLX growth appears limited, our analysis questions why hold a “value” stock in CLX versus a “growth” stock in NVDA. This article is not a prompt to buy Nvidia or sell Clorox stock, but it highlights that some stocks are perceived as value stocks despite valuations that are on par with growth stocks offering significantly greater growth potential.

Investors tend to lump certain stocks within broad classifications. Clorox, for example, is widely touted as a value stock. NVDA is known as a high-growth stock. The problem with these classifications is that it is not the underlying business that matters; it is the price you pay for their earnings potential.

The post Clorox Stock- Anything But A Value Stock appeared first on RIA.

stocks pandemicSpread & Containment

Another major retailer cracks down on self-checkout at its stores

The value retailer is discouraging theft at its self-checkout counters by introducing more associate-assisted checkout transactions in its stores.

Share this:

Huge retail chains like Walmart (WMT) , Target (TGT) , CVS (CVS) and others have faced a high amount of retail theft, or what they call inventory shrink, since 2020 and have been implementing measures to eliminate those costly losses.

Among the most common measures used by Walmart, Target and some others has been locking up popular items behind glass cases to prevent shoplifting. Customers shopping at these stores have encountered a lot of their favorite products, such as cosmetics, shampoo, over-the-counter drugs and even laundry detergent locked up in those cases.

Related: Target limits self-checkout, makes a change customers will love

Shoppers need to either push a button near the product to alert a worker to unlock the case or, in some situations, run around the store looking for a worker with the proper key to open the case. It's a very inconvenient problem for shoppers, and not all stores are consistent with their lockup policies.

For example, one Walmart store might lock up some of their instant coffee products, while another cross-town Walmart location, or even a Target competitor, doesn't lock up any coffee.

Retail stores have also implemented new self-checkout rules to discourage inventory shrink, but again, stores are inconsistent with their rules. Walmart stores have a 20 items or less rule for their self-checkout lanes to try to steer shoppers with more items to checkout clerks that might help reduce the occurrence of theft. But neither customers, nor workers seem to be observing that rule. Target on March 17 implemented a new 10 items or fewer rule in its self-checkout lanes, but we'll see if anyone enforces it.

These self-checkout requirements are also supposed to speed up the checkout process, but that only works if all the self-check registers are working and an adequate amount of checkout clerks are working registers as well.

The next step for retailers in addressing inventory shrink at self-checkout would be to eliminate self-check altogether.

Pat Greenhouse/The Boston Globe via Getty Images

Five Below cuts back on self-checkout lanes

After finishing the fourth quarter of 2023 with a "higher-than-planned shrink," or higher level of theft than expected in its stores, value retailer Five Below (FIVE) has implemented associate-assisted checkout in all of its stores for 2024, CEO Joel Anderson said on the company's earnings call on March 20.

"In addition, in our high-shrink stores, the primary option for checkout is more of the traditional, over-the-counter associate checkout," Anderson said. "We expect to have 75% of our transactions chain-wide assisted by an associate with a goal of 100% in our highest shrink, highest-risk stores to be fully transacted by an associate."

The retailer also checks receipts and adds guards

"Additionally, in those stores, we’re implementing further mitigation efforts, including receipt checking, additional store payroll and guards. We intend to measure progress as soon as Q2 when we perform a limited number of store counts," Anderson said.

Five Below tested several inventory shrink mitigation initiatives late in the third quarter and into the fourth quarter of 2023, which included product-related tests, front-end initiatives and guard programs, Anderson said in the earnings call. He said the most significant change the Philadelphia-based company made across most of the chain was to limit the number of self-checkout registers that were open, while positioning an associate upfront to further assist customers.

Anderson said he is confident the company's measures will help it over time, but the company has not included any financial impact for shrink reduction in its 2024 guidance. The company, however will aggressively pursue returning to pre-pandemic levels of shrink or offsetting the impact over the next few years, he said.

mitigation pandemicGovernment

CCP-Linked Virologist Fired After Transferring Ebola From Winnipeg To Wuhan Resurfaces In China – And Is Collaborating With Military Scientists

CCP-Linked Virologist Fired After Transferring Ebola From Winnipeg To Wuhan Resurfaces In China – And Is Collaborating With Military Scientists

…

Share this:

A virologist who had a "clandestine relationship" with Chinese agents and was subsequently fired by the Trudeau government has popped back up in China - where she's conducting research with Chinese military scientists and other virology researchers, including at the Wuhan Institute of Virology, where she's allegedly studying antibodies for coronavirus, as well as the deadly Ebola and Niaph viruses, the Globe and Mail reports.

Xiangguo Qiu and her husband Keding Cheng were fired from the National Microbiology Laboratory in Winnipeg, Canada and stripped of their security clearances in July of 2019.

Declassified documents tabled in the House of Commons on Feb. 28 show the couple had provided confidential scientific information to China and posed a credible security threat to the country, according to the Canadian Security Intelligence Service.

The Globe found that Dr. Qiu’s name appears on four Chinese patent filings since 2020, two with the Wuhan Institute of Virology – whose work on bat coronaviruses has placed it at the centre of concerns that it played a role in the spread of COVID-19 – and two with the University of Science and Technology of China, or USTC. The patents relate to antibodies against Nipah virus and work related to nanobodies, including against coronaviruses. -Globe and Mail

Canadian authorities began questioning the pair's loyalty, as well as the potential for coercion or exploitation by a foreign entity, according to more than 600 pages of documents reported by The Counter Signal.

Highlights (via CTVNews.ca):

- Qiu and Cheng were escorted out of Winnipeg's National Microbiology Laboratory in July 2019 and subsequently fired in January 2021.

- The pair transferred deadly Ebola and Henipah viruses to China's Wuhan Institute of Virology in March 2019.

- The Canadian Security Intelligence Service assessed that Qiu repeatedly lied about the extent of her work with institutions of the Chinese government and refused to admit involvement in various Chinese programs, even when evidence was presented to her.

- [D]espite being given every opportunity in her interviews to describe her association with Chinese entities, "Ms. Qiu continued to make blanket denials, feign ignorance or tell outright lies."

- A November 2020 Public Health Agency of Canada report on Qiu says investigators "weighed the adverse information and are in agreement with the CSIS assessment."

- A Public Health Agency report on Cheng's activities says he allowed restricted visitors to work in laboratories unescorted and on at least two occasions did not prevent the unauthorized removal of laboratory materials.

- Cheng was not forthcoming about his activities and collaborations with people from government agencies "of another country, namely members of the People's Republic of China."

Following their firings, Qiu returned to China despite it being under a pandemic travel lockdown until January, 2023.

"It’s very likely that she received quite preferential treatment in China on the basis that she’s proven herself. She’s done a very good job for the government of China," said Brendan Walker-Munro, senior research fellow at Australia’s University of Queensland Law School. "She’s promoted their interests abroad. She’s returned information that is credibly useful to China and to its ongoing research."

More via the Globe and Mail;

Documents reviewed by The Globe show that Dr. Qiu is most closely aligned with the University of Science and Technology of China (USTC) in Hefei. In March, 2023, a document posted by a Chinese pharmaceutical company listed Dr. Qiu as second amongst “major completion personnel” on a project awarded by the Chinese Preventive Medicine Association for study related to an anti-Ebola virus therapeutic antibody. Most of the other completion personnel were associated with the Chinese People’s Liberation Army.

USTC was founded by the Chinese Academy of Sciences and initially established to build up Chinese scientific expertise useful to the military, which at the time was pursuing technology to build satellites, intercontinental ballistic missiles and atomic bombs. The university has continued to maintain close military ties.

The document says Dr. Qiu works for USTC. Jin Tengchuan, the principal investigator at the Laboratory of Structural Immunology at USTC, lists her as a co-inventor on a patent. Mr. Jin did not respond to requests for comment.

A person who answered the phone at USTC told The Globe, “I don’t have any information about this teacher.”

In 2012, USTC signed a strategic co-operation agreement with the Army Engineering University of the People’s Liberation Army, designed to strengthen research on cutting-edge technology useful for communications, weaponry and other national-defence priorities.

Dr. Qiu is also listed as a 2019 doctoral supervisor for students studying virology at Hebei Medical University.

“Well, that makes me wonder what circumstances she was under when she emigrated to Canada. Why did she come?” asked Earl Brown, a professor emeritus of biochemistry, microbiology and immunology at the University of Ottawa’s faculty of medicine who has worked extensively in China in the past. “People leave for more freedom from China, or to make more money. But China keeps tabs on most people so I am not sure if she came over to infiltrate or whether she came and the infiltration happened later through contact with China.”

It may be impossible to answer that question. Three former colleagues at the National Microbiolgy Lab have indicated that Dr. Qiu and her husband were diligent and pleasant to deal with, but largely kept to themselves outside of work. They say Dr. Qiu was a brilliant scientist with a strong work ethic, although her English was weak. The Globe is not identifying the three who did not want to be named.

Dr. Qiu is a medical doctor from Tianjin, China, who came to Canada for graduate studies in 1996. She started at the University of Manitoba, but began working at the national lab as a research scientist in 2006, working her way up to become head of the vaccine development and antiviral therapies section in the National Microbiology Laboratory’s special pathogens program.

She was also part of the team that helped develop ZMapp, a treatment for the deadly Ebola virus, which killed more than 11,000 people in West Africa between 2014 and 2016.

“My sense is this was part of a larger strategy by China to get access to our innovation system,” said Filippa Lentzos, an associate professor of science and international security at King’s College London. “It was a way for them to to find out what was going on in Canada’s premier lab.”

Initially trained as a medical doctor, Dr. Qiu graduated in 1985 from Hebei University in the coastal city of Tianjin, which lies southeast of Beijing. Dr. Qiu went on to obtain her master of science degree in immunology at Tianjin Medical University in 1990.

Her career at Canada’s top infectious disease lab in Winnipeg began in 2003, only four years after Ottawa opened this biosafety level 4 facility at the Canadian Science Centre for Human and Animal Health.

Over time, she built up a reputation for academic collaboration, particularly with China. It was welcomed by management who felt her work was helping build a name internationally for the National Microbiology Lab.

By the time Canadian officials intervened in 2018 and began investigating, documents show, Dr. Qiu was running 44 separate projects at the Winnipeg lab, an uncommonly large workload.

Her work with former colleague and microbiologist Gary Kobinger vaulted Dr. Qiu into the international spotlight. The pair developed a treatment for Ebola, one that in its first human application led to the full recovery of 27 patients with the infection during a 2014 outbreak in Liberia.

Mr. Kobinger’s career continued to soar and he is now director of the Galveston National Laboratory, a renowned biosafety level 4 facility in Texas. In 2022, he told The Globe that it was “heartbreaking” to see what had happened to his colleague. He declined to speak for this article.

“She had lost a lot of weight with all the stress. She was so convinced that this was all a misunderstanding … and she would go back to her job,” he said in 2022. “ Her career has been destroyed with all this. She was one of the top female Canadian scientists of virology and Canada has lost that.”

Over a period of 13 months, though, the Chinese-Canadian microbiologist and her biologist husband’s lives were turned upside down.

She went from being feted at Ottawa’s Rideau Hall with a Governor-General’s Award in May, 2018, to being locked out of the Winnipeg lab in July, 2019 – the high-security facility where she had made her name as a scientist in Canada. By January, 2021, she and Mr. Cheng were fired.

Last month, after being pressed into explaining what happened, the Canadian government finally disclosed the reasons for this extraordinary dismissal: CSIS found the pair had lied about and hid their co-operation with China from Ottawa.

A big question remains following their departure: Why would Dr. Qiu risk her career, including the stature associated with developing an Ebola treatment, for China?

Read the rest here...

International

You can now enter this country without a passport

Singapore has been on a larger push to speed up the flow of tourists with digital immigration clearance.

Share this:

{kind=link}

{kind=link}

In the fall of 2023, the city-state of Singapore announced that it was working on end-to-end biometrics that would allow travelers passing through its Changi Airport to check into flights, drop off bags and even leave and exit the country without a passport.

The latter is the most technologically advanced step of them all because not all countries issue passports with the same biometrics while immigration laws leave fewer room for mistakes about who enters the country.

Related: A country just went visa-free for visitors with any passport

That said, Singapore is one step closer to instituting passport-free travel by testing it at its land border with Malaysia. The two countries have two border checkpoints, Woodlands and Tuas, and as of March 20 those entering in Singapore by car are able to show a QR code that they generate through the government’s MyICA app instead of the passport.

Here is who is now able to enter Singapore passport-free

The latter will be available to citizens of Singapore, permanent residents and tourists who have already entered the country once with their current passport. The government app pulls data from one's passport and shows the border officer the conditions of one's entry clearance already recorded in the system.

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

While not truly passport-free since tourists still need to link a valid passport to an online system, the move is the first step in Singapore's larger push to get rid of physical passports.

"The QR code initiative allows travellers to enjoy a faster and more convenient experience, with estimated time savings of around 20 seconds for cars with four travellers, to approximately one minute for cars with 10 travellers," Singapore's Immigration and Checkpoints Authority wrote in a press release announcing the new feature. "Overall waiting time can be reduced by more than 30% if most car travellers use QR code for clearance."

More countries are looking at passport-free travel but it will take years to implement

The land crossings between Singapore and Malaysia can get very busy — government numbers show that a new post-pandemic record of 495,000 people crossed Woodlands and Tuas on the weekend of March 8 (the day before Singapore's holiday weekend.)

Even once Singapore implements fully digital clearance at all of its crossings, the change will in no way affect immigration rules since it's only a way of transferring the status afforded by one's nationality into a digital system (those who need a visa to enter Singapore will still need to apply for one at a consulate before the trip.) More countries are in the process of moving toward similar systems but due to the varying availability of necessary technology and the types of passports issued by different countries, the prospect of agent-free crossings is still many years away.

In the U.S., Chicago's O'Hare International Airport was chosen to take part in a pilot program in which low-risk travelers with TSA PreCheck can check into their flight and pass security on domestic flights without showing ID. The UK has also been testing similar digital crossings for British and EU citizens but no similar push for international travelers is currently being planned in the U.S.

stocks pandemic link testing singapore uk eu

Analysts issue unexpected crude oil price forecast after surge

Study: Life’s building blocks are surprisingly stable in Venus-like conditions

ARPA-H appoints Etta Pisano to lead its Advancing Clinical Trials Readiness Initiative

COVID-19 Infection Increases Risk Of Autoimmune Diseases By Up To 30 Percent: Study

QE By A Different Name Is Still QE

This country became first in the world to let in tourists passport-free

“Are you better off than you were four years ago?”

IVI starts technology transfer to Biological E. Limited to manufacture oral cholera vaccine for India and global markets

Analyst revamps MicroStrategy stock price target after Bitcoin buy

John Lewis relies too heavily on its heritage – here’s what it could do instead

-

Spread & Containment1 week ago

Spread & Containment1 week agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized1 month ago

Uncategorized1 month agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges