Government

China equity – A viable investment for long-term investors

China equity – A viable investment for long-term investors

Share this:

The COVID-19 epidemic in China is now mostly contained, allowing it to lift restrictions gradually and retraining our focus on the prospect of a post-coronavirus revival and the investment opportunities in the world’s second-largest economy.

Looking at longer-term trends, we believe investors should welcome the gradual inclusion of Chinese companies in global equity indices as they look for diversification and sustainable returns. Valuations that are currently more attractive than those of global equities enhance the opportunity. Furthermore, stock multiples could benefit from the Chinese market becoming more institutional in its makeup.

Below we list a number of reasons for our confidence in Chinese equities.[1]

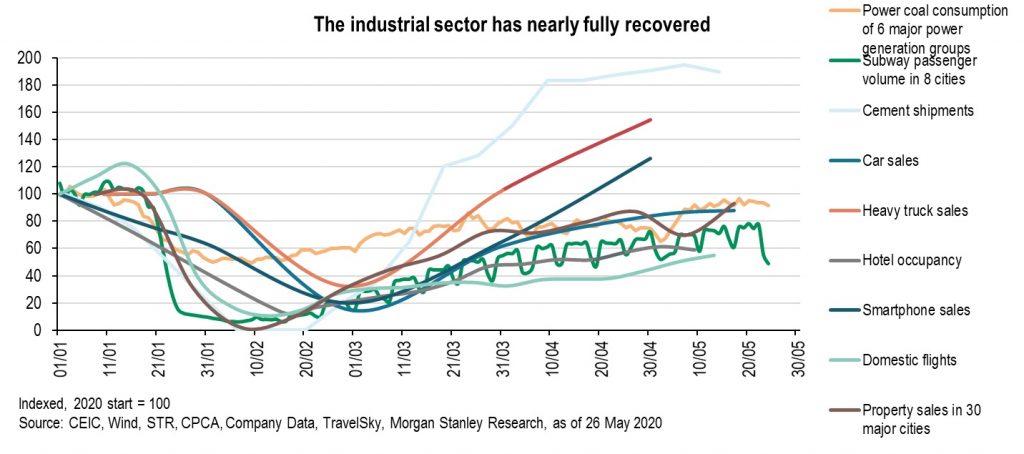

1. China is back at work

Over the past two months, China’s industry returned to nearly full capacity, even in Hubei region. In the services and consumer sectors, the recovery is progressing more slowly, constrained by partial travel restrictions and the loss of jobs and income. Overall, though, the gradual return to normality underscores how the government’s swift actions enabled the nation to get back on its feet relatively quickly.

Exhibit 1:

Exhibit 2:

2. Selective stimulus

In Q1 2020, China’s GDP contracted by 6.8% year-on-year. Full-year 2020 growth is likely to come in at around 3%, but with risks to the downside, depending on the pandemic’s development globally.

Since the Covid-19 outbreak, the People’s Bank of China (PBoC) has rolled out a series of measures to provide epidemic relief and stabilise demand. During the recent annual National People’s Congress, the key focus was the size of fiscal stimulus. Beijing’s spending plans imply a fiscal deficit of 8%-10% of 2020 GDP. This is less than the 12% of GDP deployed after the Global Financial Crisis.

More aggressive stimulus will be needed to support the resumption of normal operations, including more local government investment in infrastructure, education and public health. Tax and fee cuts are likely to support small and medium enterprises along with a lifting of restrictions on car purchases.

3. Easier access to China A-shares

The Stock Connect programme linking the Shanghai and Shenzhen markets to Hong Kong, launched in 2014, has made investing in onshore shares easier for international investors. They can deploy capital quickly, and the more than 1 500 stocks listed in Shanghai and Shenzhen offer investors abundant opportunities to earn alpha.

Growing participation by global investors is rendering the A-shares market more mature and is favouring long-term growth. This market provides more diversified access to structural growth opportunities, making it a complement to exposure in the China offshore markets.

As A-shares tend to be less sensitive to global market sentiment, the correlation of this market with the rest of the world is low. Adding A-shares to a portfolio can thus enhance the risk/return profile of emerging market equity exposure and even of a China offshore equity portfolio. We believe an all-China equity solution helps investors gain access to the full opportunity set, maximising the return potential.[2]

4. Key risks are monitored closely

Tensions between China and the US remain a focus for investors and we are following the situation closely. One area of attention is the US Holding Foreign Companies Accountable Act. This requires foreign issuers of securities to establish that a foreign government does not own or control them. US-listed foreign companies will be delisted if the accounting oversight board cannot inspect the issuer’s accounting firm for three consecutive years.

We view the near-term risks as manageable. A forced delisting could happen by 2023 at the earliest. In the worst-case scenario, if Chinese American depositary receipts (ADRs) are forced to delist by then, the companies can opt to list in Hong Kong. One e-commerce giant has already done so and other leading companies including a leading online retailer and a prominent internet technology company are seeking to have a secondary listing there this month.[3]

We believe such a law should have a limited impact on the ability of Chinese companies to tap capital markets. Most Chinese firms have issued shares in Hong Kong and Shanghai rather than in the US in the past five years.

Besides, Chinese and US regulators have been negotiating on this oversight-related issue for years. There is still a possibility that compromises by China will allow it to be settled. In such a scenario, US exchanges will try to guide issuers to meet the requirements and maintain their listing in the interest of the exchanges and investors.

5. Three investment themes for long-term structural growth

Although digitalisation was already shaping China’s economy, the COVID-19 outbreak has accelerated the trend. We have sharpened our focus on tech localisation themes, cloud businesses, software and hardware.

We continue to see three structural trends that spur sustainable growth:

- Technology innovation: China has shifted towards medium to high-end manufacturing. The size of the domestic market, higher R&D spending and a vast talent pool support this shift.

- Consumption upgrading: We see significant growth opportunities, especially in services. Rising household income, low household debt and more diversified consumer profiles support this trend.

- Industry consolidation: We believe this trend has longer to run in an environment of slower growth. The emergence of leading companies should provide attractive investment opportunities. Faster industry consolidation should play favourably for industry leaders over the long term.

Portfolio strategy over the long term

In summary, while investors should not overlook the risks, we believe China is too big to ignore. It is essential for investors to monitor events closely given the market’s history of volatility. Changes in valuations and earnings may necessitate tactical portfolio adjustments. Navigating China’s waters requires local expertise and a well-resourced investment team to capture the long-term growth opportunities.

Our latest webcast China’s growth challenged covers the economic and market implications for China’s growth of the COVID-19 crisis amid a trade war. We also discuss the policy and structural reform outlook after the recent National People’s Congress. We highlight our long-term portfolio strategy and its focus on structural growth stories.

[1] Click here to watch our China’s growth challenged webcast with Caroline Yu Maurer and Chi Lo

[2] For information on our strategies or investment policies, please contact your dedicated client relationship manager.

[3] Source: China’s JD.com, NetEase Win Hong Kong Approval for Listings.

Any views expressed here are those of the author as of the date of publication, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may take different investment decisions for different clients.

The value of investments and the income they generate may go down as well as up and it is possible that investors will not recover their initial outlay. Past performance is no guarantee for future returns.

Investing in emerging markets, or specialised or restricted sectors is likely to be subject to a higher-than-average volatility due to a high degree of concentration, greater uncertainty because less information is available, there is less liquidity or due to greater sensitivity to changes in market conditions (social, political and economic conditions).

Some emerging markets offer less security than the majority of international developed markets. For this reason, services for portfolio transactions, liquidation and conservation on behalf of funds invested in emerging markets may carry greater risk.

Writen by Jessica Tea. The post China equity – A viable investment for long-term investors appeared first on Investors' Corner - The official blog of BNP Paribas Asset Management.

Government

Survey Shows Declining Concerns Among Americans About COVID-19

Survey Shows Declining Concerns Among Americans About COVID-19

A new survey reveals that only 20% of Americans view covid-19 as "a major threat"…

Share this:

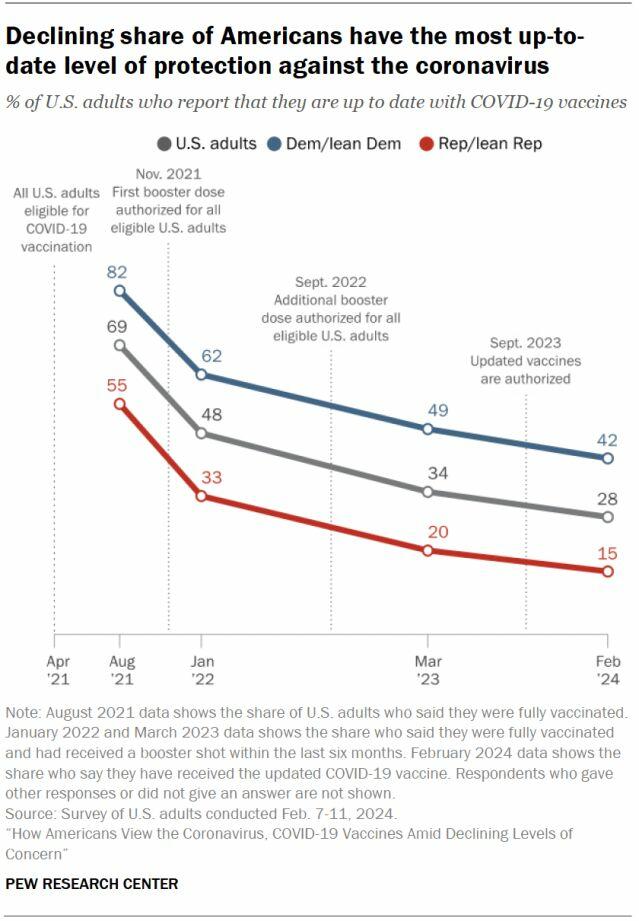

A new survey reveals that only 20% of Americans view covid-19 as "a major threat" to the health of the US population - a sharp decline from a high of 67% in July 2020.

What's more, the Pew Research Center survey conducted from Feb. 7 to Feb. 11 showed that just 10% of Americans are concerned that they will catch the disease and require hospitalization.

"This data represents a low ebb of public concern about the virus that reached its height in the summer and fall of 2020, when as many as two-thirds of Americans viewed COVID-19 as a major threat to public health," reads the report, which was published March 7.

According to the survey, half of the participants understand the significance of researchers and healthcare providers in understanding and treating long COVID - however 27% of participants consider this issue less important, while 22% of Americans are unaware of long COVID.

What's more, while Democrats were far more worried than Republicans in the past, that gap has narrowed significantly.

"In the pandemic’s first year, Democrats were routinely about 40 points more likely than Republicans to view the coronavirus as a major threat to the health of the U.S. population. This gap has waned as overall levels of concern have fallen," reads the report.

More via the Epoch Times;

The survey found that three in ten Democrats under 50 have received an updated COVID-19 vaccine, compared with 66 percent of Democrats ages 65 and older.

Moreover, 66 percent of Democrats ages 65 and older have received the updated COVID-19 vaccine, while only 24 percent of Republicans ages 65 and older have done so.

“This 42-point partisan gap is much wider now than at other points since the start of the outbreak. For instance, in August 2021, 93 percent of older Democrats and 78 percent of older Republicans said they had received all the shots needed to be fully vaccinated (a 15-point gap),” it noted.

COVID-19 No Longer an Emergency

The U.S. Centers for Disease Control and Prevention (CDC) recently issued its updated recommendations for the virus, which no longer require people to stay home for five days after testing positive for COVID-19.

The updated guidance recommends that people who contracted a respiratory virus stay home, and they can resume normal activities when their symptoms improve overall and their fever subsides for 24 hours without medication.

“We still must use the commonsense solutions we know work to protect ourselves and others from serious illness from respiratory viruses, this includes vaccination, treatment, and staying home when we get sick,” CDC director Dr. Mandy Cohen said in a statement.

The CDC said that while the virus remains a threat, it is now less likely to cause severe illness because of widespread immunity and improved tools to prevent and treat the disease.

“Importantly, states and countries that have already adjusted recommended isolation times have not seen increased hospitalizations or deaths related to COVID-19,” it stated.

The federal government suspended its free at-home COVID-19 test program on March 8, according to a website set up by the government, following a decrease in COVID-19-related hospitalizations.

According to the CDC, hospitalization rates for COVID-19 and influenza diseases remain “elevated” but are decreasing in some parts of the United States.

International

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Rand Paul Teases Senate GOP Leader Run – Musk Says "I Would Support"

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump…

Share this:

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump into the race to become the next Senate GOP leader, and Elon Musk was quick to support the idea. Republicans must find a successor for periodically malfunctioning Mitch McConnell, who recently announced he'll step down in November, though intending to keep his Senate seat until his term ends in January 2027, when he'd be within weeks of turning 86.

So far, the announced field consists of two quintessential establishment types: John Cornyn of Texas and John Thune of South Dakota. While John Barrasso's name had been thrown around as one of "The Three Johns" considered top contenders, the Wyoming senator on Tuesday said he'll instead seek the number two slot as party whip.

Paul used X to tease his potential bid for the position which -- if the GOP takes back the upper chamber in November -- could graduate from Minority Leader to Majority Leader. He started by telling his 5.1 million followers he'd had lots of people asking him about his interest in running...

Thousands of people have been asking if I'd run for Senate leadership...

— Rand Paul (@RandPaul) March 8, 2024

...then followed up with a poll in which he predictably annihilated Cornyn and Thune, taking a 96% share as of Friday night, with the other two below 2% each.

????????️VOTE NOW ????️ ???? Who would you like to be the next Senate leader?

— Rand Paul (@RandPaul) March 8, 2024

Elon Musk was quick to back the idea of Paul as GOP leader, while daring Cornyn and Thune to follow Paul's lead by throwing their names out for consideration by the Twitter-verse X-verse.

I would support Rand Paul and suspect that other candidates will not actually run polls out of concern for the results, but let’s see if they will!

— Elon Musk (@elonmusk) March 8, 2024

Paul has been a stalwart opponent of security-state mass surveillance, foreign interventionism -- to include shoveling billions of dollars into the proxy war in Ukraine -- and out-of-control spending in general. He demonstrated the latter passion on the Senate floor this week as he ridiculed the latest kick-the-can spending package:

This bill is an insult to the American people. The earmarks are all the wasteful spending that you could ever hope to see, and it should be defeated. Read more: https://t.co/Jt8K5iucA4 pic.twitter.com/I5okd4QgDg

— Senator Rand Paul (@SenRandPaul) March 8, 2024

In February, Paul used Senate rules to force his colleagues into a grueling Super Bowl weekend of votes, as he worked to derail a $95 billion foreign aid bill. "I think we should stay here as long as it takes,” said Paul. “If it takes a week or a month, I’ll force them to stay here to discuss why they think the border of Ukraine is more important than the US border.”

Don't expect a Majority Leader Paul to ditch the filibuster -- he's been a hardy user of the legislative delay tactic. In 2013, he spoke for 13 hours to fight the nomination of John Brennan as CIA director. In 2015, he orated for 10-and-a-half-hours to oppose extension of the Patriot Act.

Among the general public, Paul is probably best known as Capitol Hill's chief tormentor of Dr. Anthony Fauci, who was director of the National Institute of Allergy and Infectious Disease during the Covid-19 pandemic. Paul says the evidence indicates the virus emerged from China's Wuhan Institute of Virology. He's accused Fauci and other members of the US government public health apparatus of evading questions about their funding of the Chinese lab's "gain of function" research, which takes natural viruses and morphs them into something more dangerous. Paul has pointedly said that Fauci committed perjury in congressional hearings and that he belongs in jail "without question."

Musk is neither the only nor the first noteworthy figure to back Paul for party leader. Just hours after McConnell announced his upcoming step-down from leadership, independent 2024 presidential candidate Robert F. Kennedy, Jr voiced his support:

Mitch McConnell, who has served in the Senate for almost 40 years, announced he'll step down this November.

— Robert F. Kennedy Jr (@RobertKennedyJr) February 28, 2024

Part of public service is about knowing when to usher in a new generation. It’s time to promote leaders in Washington, DC who won’t kowtow to the military contractors or…

In a testament to the extent to which the establishment recoils at the libertarian-minded Paul, mainstream media outlets -- which have been quick to report on other developments in the majority leader race -- pretended not to notice that Paul had signaled his interest in the job. More than 24 hours after Paul's test-the-waters tweet-fest began, not a single major outlet had brought it to the attention of their audience.

That may be his strongest endorsement yet.

Government

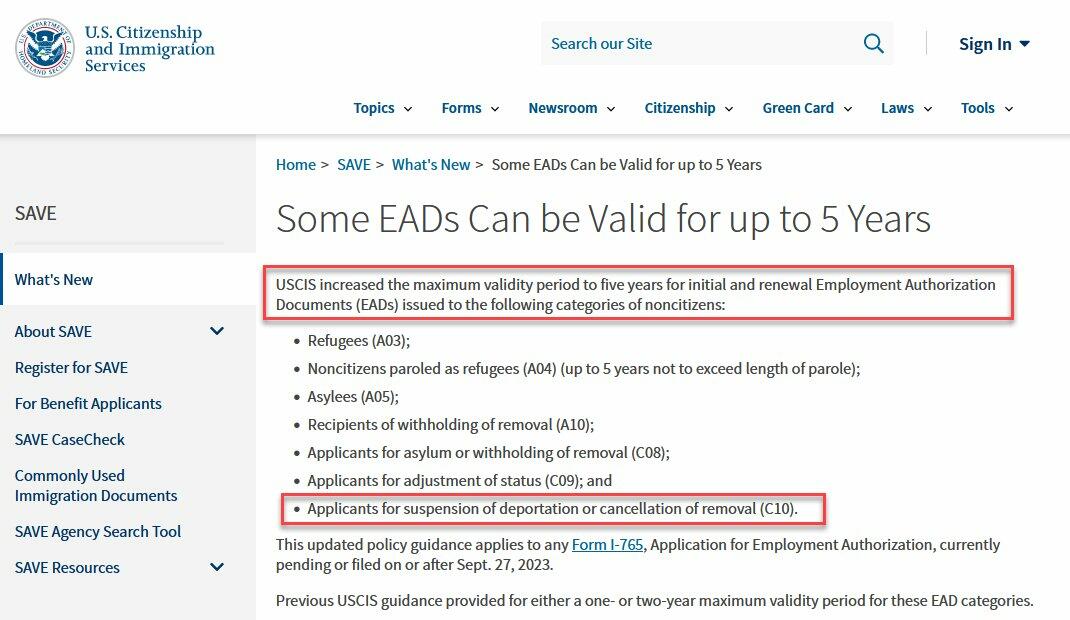

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While "Waiting" For Deporation, Asylum

Over the past several…

Share this:

{kind=link}

{kind=link}

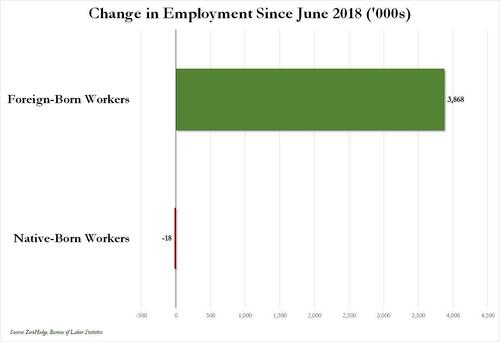

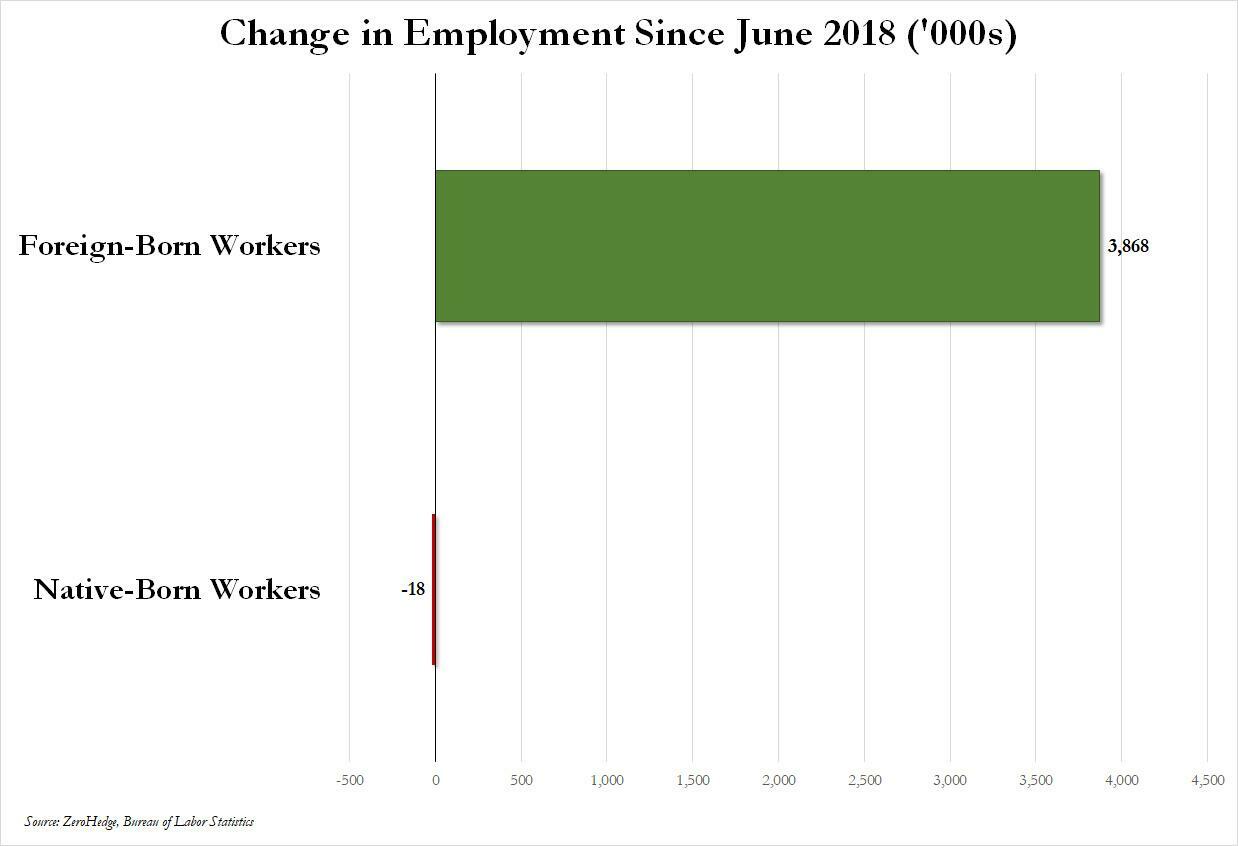

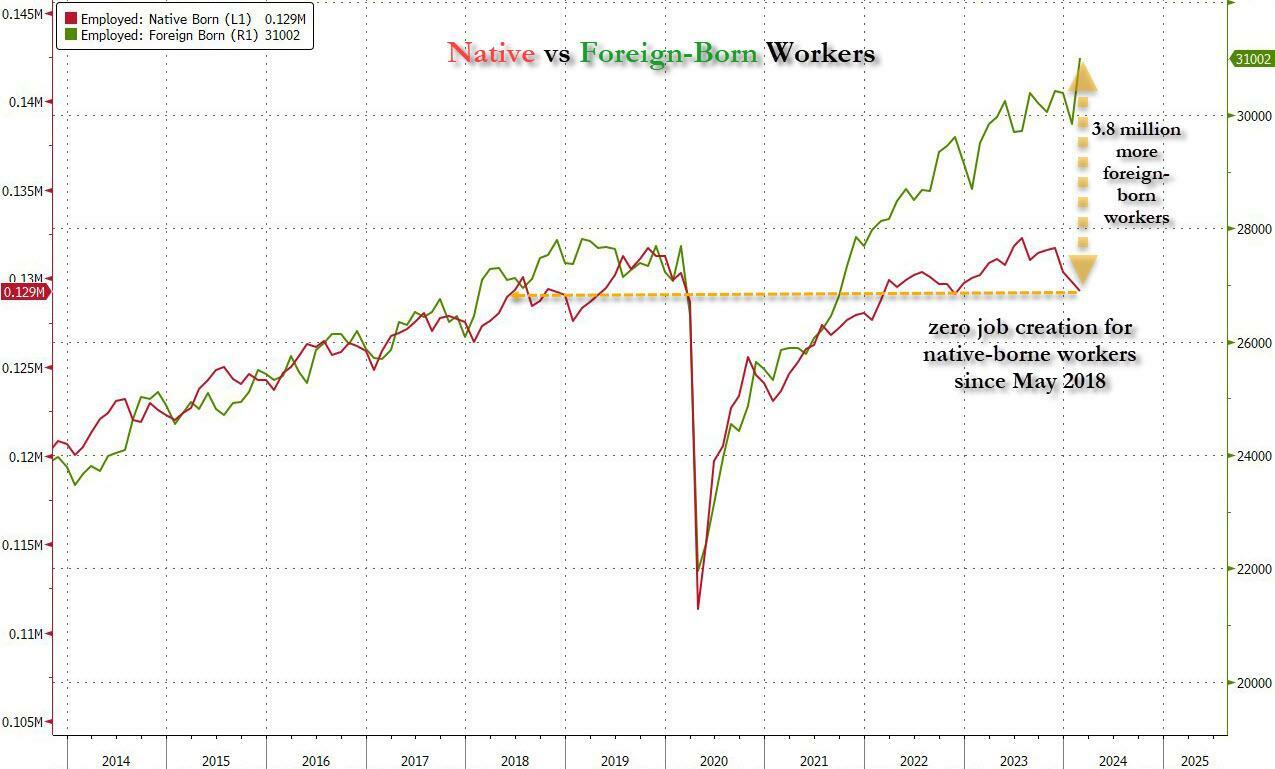

Over the past several months we've pointed out that there has been zero job creation for native-born workers since the summer of 2018...

{kind=link}

... and that since Joe Biden was sworn into office, most of the post-pandemic job gains the administration continuously brags about have gone foreign-born (read immigrants, mostly illegal ones) workers.

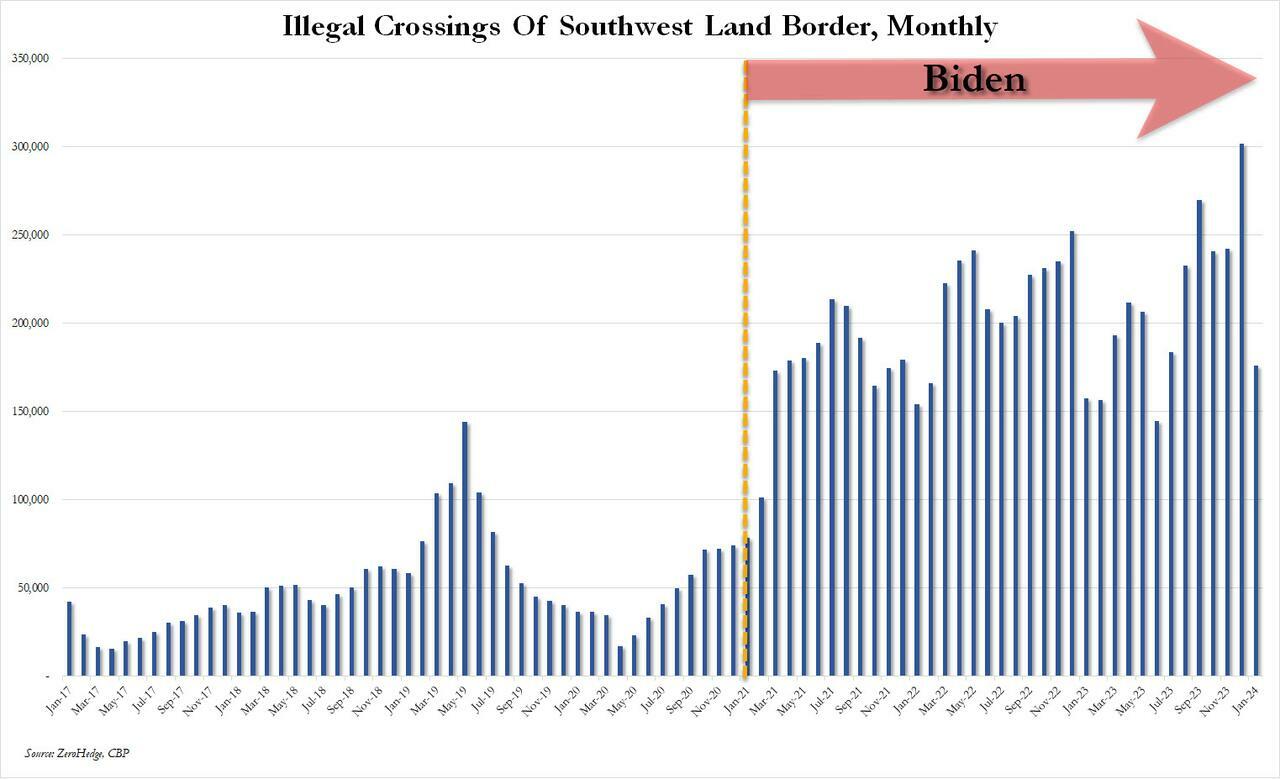

And while the left might find this data almost as verboten as FBI crime statistics - as it directly supports the so-called "great replacement theory" we're not supposed to discuss - it also coincides with record numbers of illegal crossings into the United States under Biden.

In short, the Biden administration opened the floodgates, 10 million illegal immigrants poured into the country, and most of the post-pandemic "jobs recovery" went to foreign-born workers, of which illegal immigrants represent the largest chunk.

'But Tyler, illegal immigrants can't possibly work in the United States whilst awaiting their asylum hearings,' one might hear from the peanut gallery. On the contrary: ever since Biden reversed a key aspect of Trump's labor policies, all illegal immigrants - even those awaiting deportation proceedings - have been given carte blanche to work while awaiting said proceedings for up to five years...

... something which even Elon Musk was shocked to learn.

Wow, learn something new every day https://t.co/8MDtEEZGam

— Elon Musk (@elonmusk) March 10, 2024

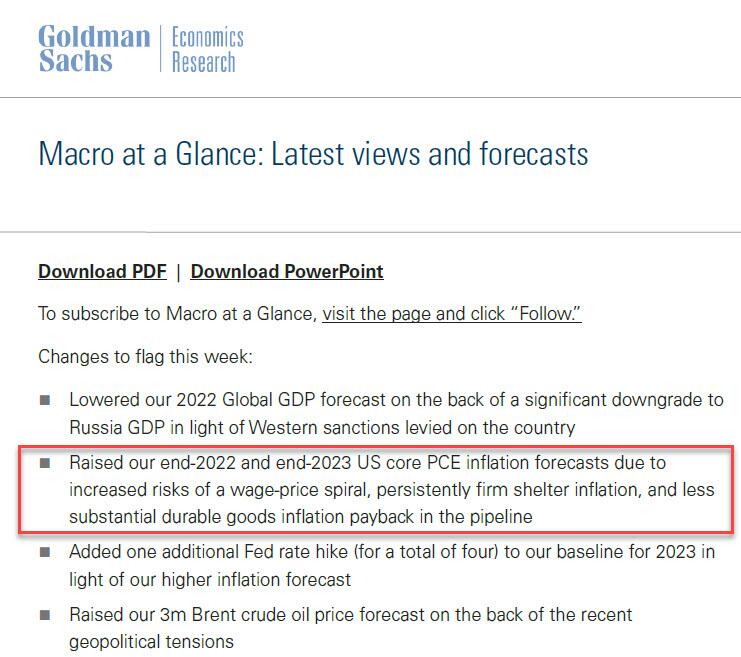

Which leads us to another question: recall that the primary concern for the Biden admin for much of 2022 and 2023 was soaring prices, i.e., relentless inflation in general, and rising wages in particular, which in turn prompted even Goldman to admit two years ago that the diabolical wage-price spiral had been unleashed in the US (diabolical, because nothing absent a major economic shock, read recession or depression, can short-circuit it once it is in place).

Well, there is one other thing that can break the wage-price spiral loop: a flood of ultra-cheap illegal immigrant workers. But don't take our word for it: here is Fed Chair Jerome Powell himself during his February 60 Minutes interview:

PELLEY: Why was immigration important?

POWELL: Because, you know, immigrants come in, and they tend to work at a rate that is at or above that for non-immigrants. Immigrants who come to the country tend to be in the workforce at a slightly higher level than native Americans do. But that's largely because of the age difference. They tend to skew younger.

PELLEY: Why is immigration so important to the economy?

POWELL: Well, first of all, immigration policy is not the Fed's job. The immigration policy of the United States is really important and really much under discussion right now, and that's none of our business. We don't set immigration policy. We don't comment on it.

I will say, over time, though, the U.S. economy has benefited from immigration. And, frankly, just in the last, year a big part of the story of the labor market coming back into better balance is immigration returning to levels that were more typical of the pre-pandemic era.

PELLEY: The country needed the workers.

POWELL: It did. And so, that's what's been happening.

Translation: Immigrants work hard, and Americans are lazy. But much more importantly, since illegal immigrants will work for any pay, and since Biden's Department of Homeland Security, via its Citizenship and Immigration Services Agency, has made it so illegal immigrants can work in the US perfectly legally for up to 5 years (if not more), one can argue that the flood of illegals through the southern border has been the primary reason why inflation - or rather mostly wage inflation, that all too critical component of the wage-price spiral - has moderated in in the past year, when the US labor market suddenly found itself flooded with millions of perfectly eligible workers, who just also happen to be illegal immigrants and thus have zero wage bargaining options.

None of this is to suggest that the relentless flood of immigrants into the US is not also driven by voting and census concerns - something Elon Musk has been pounding the table on in recent weeks, and has gone so far to call it "the biggest corruption of American democracy in the 21st century", but in retrospect, one can also argue that the only modest success the Biden admin has had in the past year - namely bringing inflation down from a torrid 9% annual rate to "only" 3% - has also been due to the millions of illegals he's imported into the country.

We would be remiss if we didn't also note that this so often carries catastrophic short-term consequences for the social fabric of the country (the Laken Riley fiasco being only the latest example), not to mention the far more dire long-term consequences for the future of the US - chief among them the trillions of dollars in debt the US will need to incur to pay for all those new illegal immigrants Democrat voters and low-paid workers. This is on top of the labor revolution that will kick in once AI leads to mass layoffs among high-paying, white-collar jobs, after which all those newly laid off native-born workers hoping to trade down to lower paying (if available) jobs will discover that hardened criminals from Honduras or Guatemala have already taken them, all thanks to Joe Biden.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Low Iron Levels In Blood Could Trigger Long COVID: Study

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Walmart has really good news for shoppers (and Joe Biden)

Walmart joins Costco in sharing key pricing news

Are Voters Recoiling Against Disorder?

The Great Replacement Loophole: Illegal Immigrants Score 5-Year Work Benefit While “Waiting” For Deporation, Asylum

Survey Shows Declining Concerns Among Americans About COVID-19

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex