Black Monday: All Hell Breaks Loose As Stocks Plunge Into Bear Market, Curve Inverts, Cryptos Crater

Black Monday: All Hell Breaks Loose As Stocks Plunge Into Bear Market, Curve Inverts, Cryptos Crater

For all those claiming that stocks had…

Share this:

For all those claiming that stocks had priced in 3 (or more) 50bps (or more) rate hikes, we have some bad news.

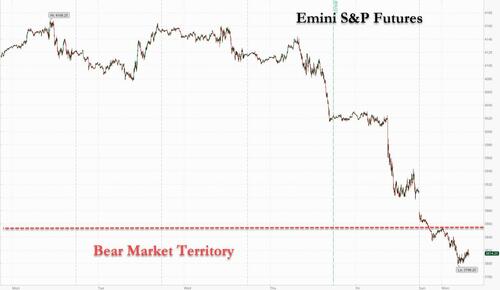

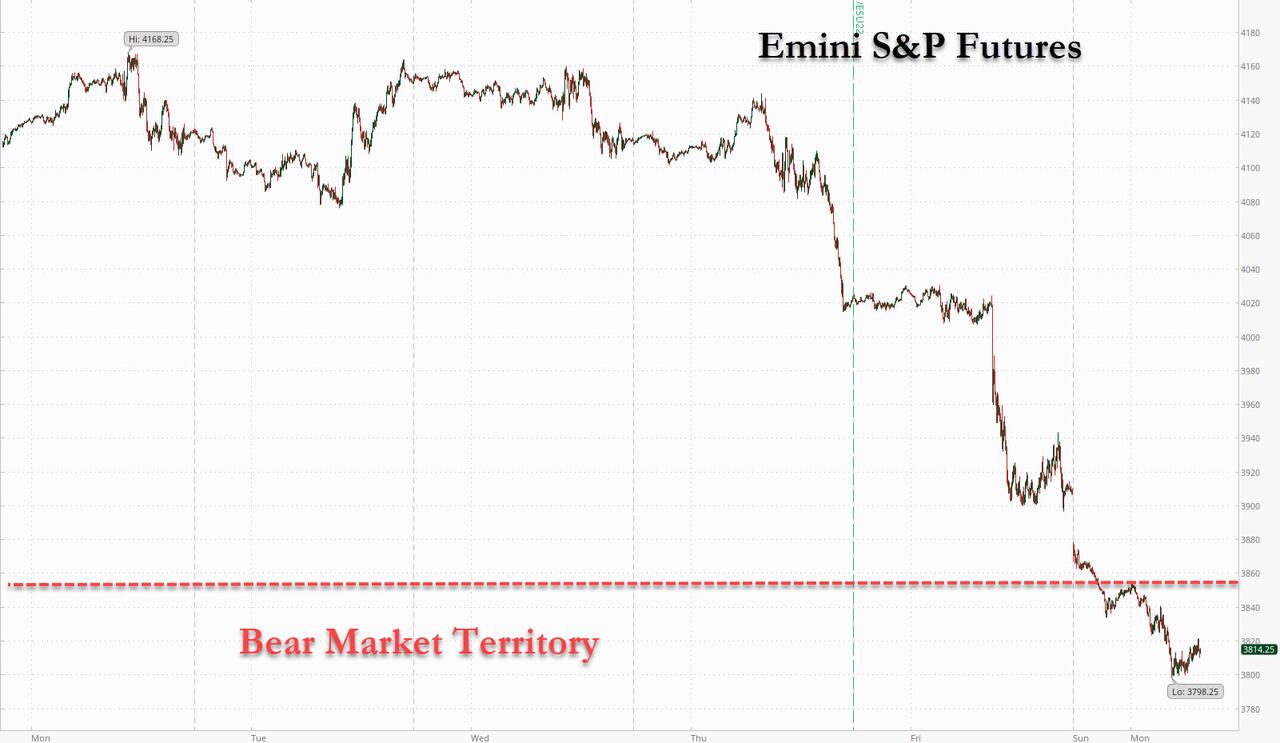

All hell is breaking loose on Monday, with futures tumbling (again) into bear market territory, sliding below the 20% technical cutoff from January's all time high of 3,856 and tumbling as low as 3,798.25 - taking out the May 10 intraday low of 3,810 - before reversing some modest gains. S&P 500 futures sank 2.5% and Nasdaq 100 contracts slid 3.1%, in a session that has seen virtually everything crash. Dow futures were down 567 points at of 730am ET.

The global selloff - which has dragged Asian and European markets to multi-month lows and which was sparked by a hotter than expected US CPI print which heaped pressure on the Federal Reserve to step up monetary tightening - accelerated on Monday as panicking traders now bet the Fed will raise rates by 175 bps by its September decision, implying two 50-bp moves and one hike of 75 bps, with Barclays and now Jefferies predicting such a move may even come this week. If that comes to pass it would be the first time since 1994 the Fed resorted to such a draconian measure.

The selling in stocks was matched only by the puke in Treasuries, as yields on 10-year US Treasuries reached 3.24%, the highest since October 2018, yet where 2Y yields sold off more, sending the 2s10s curve to invert again...

... for the second time ahead of the coming recession, an unprecedented event.

The US yield curve appears destined to invert again in coming weeks after Wednesday’s CPI data: BBG

— zerohedge (@zerohedge) May 12, 2022

We'll get two concurrent recessions

Meanwhile, the selloff in European government bonds also gathered pace, with the yield on German’s two-year government debt rising above 1% for the first time in more than a decade and Italian yields exploding and nearing 4%, ensuring that another European sovereign debt crisis is just a matter of time (recall that all Italian net bond issuance in the past decade has been monetized by the ECB... well that is ending as the ECB pivots away from QE and NIRP).

The exodus from stocks and bonds is gaining momentum on fears that central banks’ battle against inflation will end up killing economic growth. Inversions along the Treasury yield curve point to fears that the Fed won’t be able to stave off a hard landing.

“The Fed will not be able to pause tightening let alone start easing,” said James Athey, investment director at abrdn. “If all global central banks deliver what’s priced there are going to be some significant negative shocks to economies.”

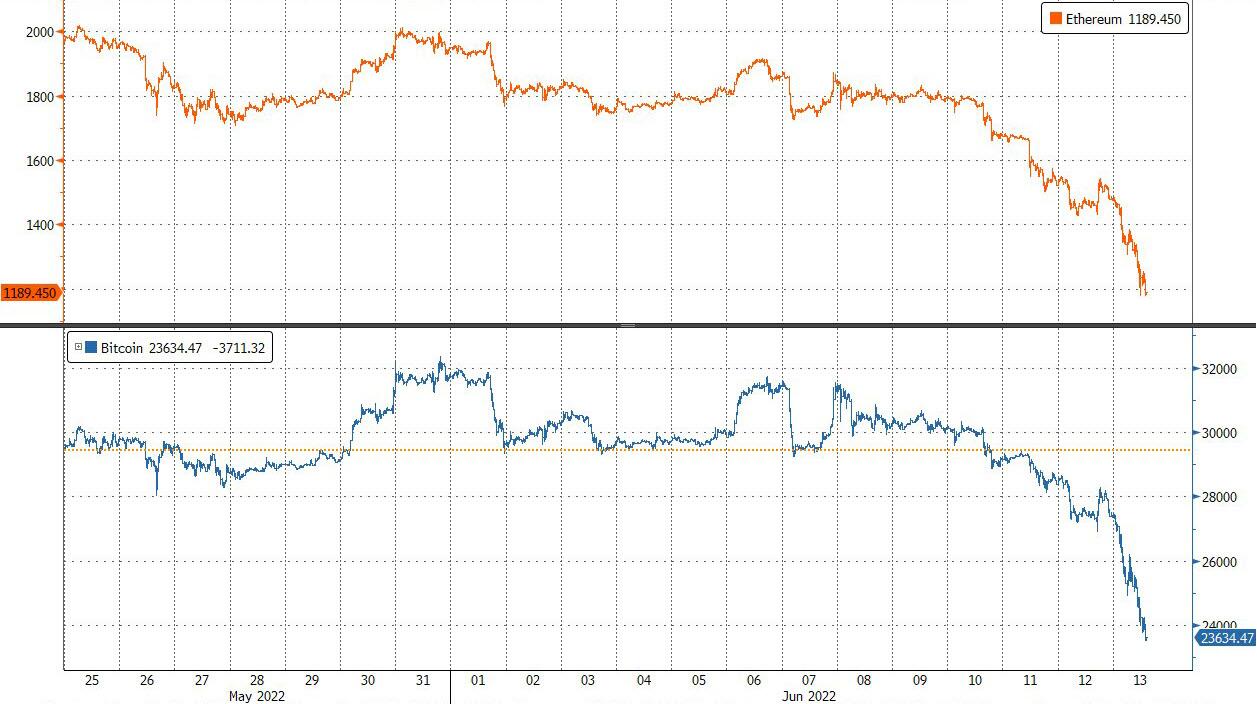

Going back to the US market, big tech stocks slumped in US premarket trading as bets that the Federal Reserve hikes rates more aggressively sent bond yields higher, and Nasdaq futures dropped. Cryptocurrency-exposed stocks cratered as Bitcoin continued its recent decline to hit an 18- month low, precipitated by news that crypto lender Celsius had halted withdrawals...

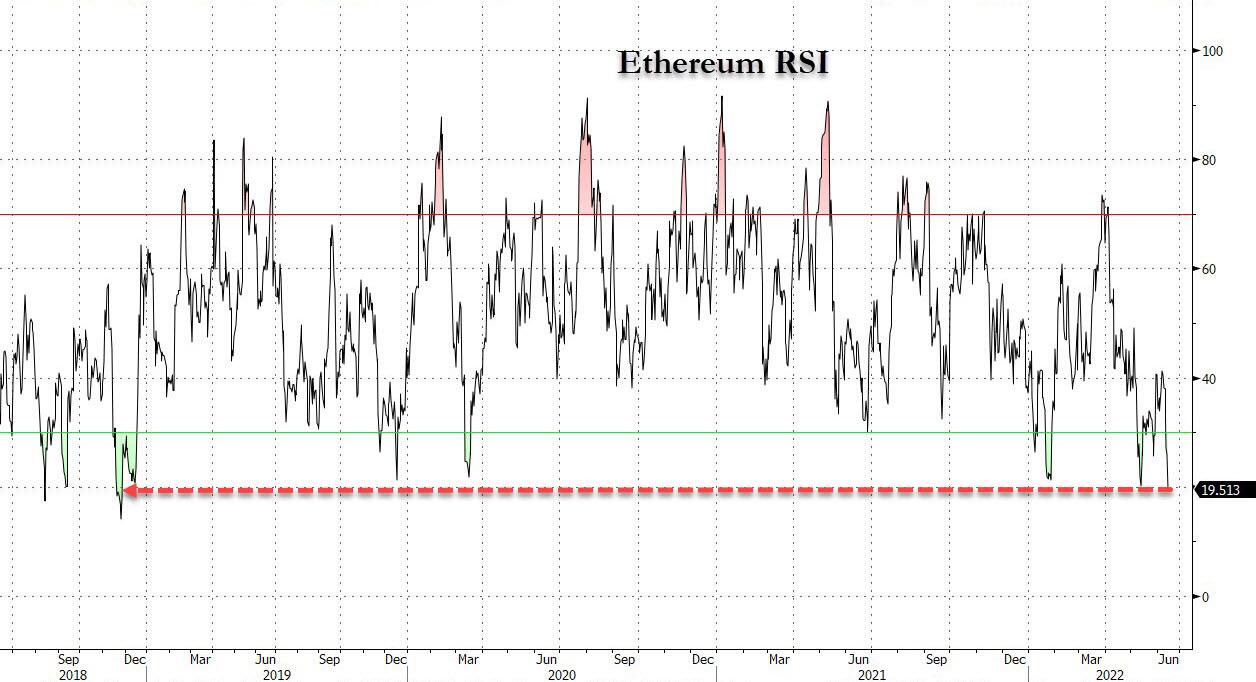

... which sent Ethereum to the most oversold level in 4 years.

Here are some of the biggest U.S. movers today:

- Apple shares (AAPL US) -3.1%, Amazon (AMZN US) -3.4%, Microsoft (MSFT US) -2.8%, Alphabet (GOOGL US) -3.7%, Netflix -3.8% (NFLX US), Nvidia (NVDA US) -4.5%

- Tesla (TSLA US) shares dropped as much as 3.1% in US premarket trading amid losses across big tech stocks, while the electric-vehicle maker also filed to split shares 3-for-1 late Friday.

- MicroStrategy (MSTR US) -18.4%, Riot Blockchain (RIOT US) -15%, Marathon Digital (MARA US) -14%, Coinbase (COIN US) -12.5%, Bit Digital (BTBT US) -10%, Silvergate Capital (SI US) -11%, Ebang (EBON US) -4%

- Bluebird Bio (BLUE US) shares surge as much as 86% in US premarket trading and are set to trim year-to- date losses after the biotech firm’s two gene therapies won backing from an FDA advisory panel.

- Chinese education stocks New Oriental Education (EDU US) and Gaotu Techedu (GOTU US) jump 8.3% and 3.4% respectively in US premarket trading after peer Koolearn’s endeavors into livestreaming e-commerce went viral and sent its shares up 95% in two sessions.

- Astra Space (ASTR US) shares slump as much as 25% in US premarket trading, after the spacetech firm’s TROPICS-1 mission saw a disappointing launch at the weekend.

- Invesco (IVZ US) and T. Rowe (TROW US) shares may be in focus today as BMO downgrades its rating on the two companies in a note saying it favors alternative asset managers over traditional players as a way to hedge beta risk against the current macro backdrop.

In Europe, the Stoxx 600 also extended declines to a three-month low, plunging mover than 2%, with over 90% of members declining, as meeting-dated OIS rates price in 125bps of tightening, one 25bps move and two 50bps hikes by October. Tech leads the declines as bond yields rise, with cyclical sectors such as autos and consumer products also lagging as recession risks rise. The Stoxx 600 Tech Index falls as much as 4.3% to its lowest since November 2020. Chip stocks bear the brunt of the selloff: ASML -3%, Infineon -4.2%, STMicro -3.6%, ASM International -2.9%, BE Semi -2.8%, AMS -5.3% as of 9:36am CET. As if inflation fears weren't enough, French banks tumbled after a first round of legislative elections showed that President Emmanuel Macron could lose his outright majority in parliament. Here is a look at the biggest movers:

- Atos shares decline as much as 12%; Oddo says the company’s reported decision to retain and restructure its legacy IT services business in a separate legal entity is bad news for the company.

- Getinge falls as much as 7.6% after Kepler Cheuvreux cut its recommendation to hold from buy, cautioning that headwinds and supply chain challenges may intensify as Covid-related tailwinds abate.

- Elior plunges as much as 15% amid renewed worries over inflation and rising interest rates impacting a caterer that’s still looking for a new CEO following the unexpected departure of the previous one.

- Valneva falls as much as 27% in Paris after saying its effort to salvage an agreement to sell Covid-19 shots to the European Union looks likely to fail.

- Subsea 7 drops as much as 13% after the offshore technology company lowered its 2022 guidance, with analysts noting execution challenges on some of its offshore wind projects.

- French banks decline after a first round of legislative elections showed that President Emmanuel Macron could lose his outright majority in parliament.

- Societe Generale shares fall as much as 4.5%, BNP Paribas -4.2%

- Euromoney rises as much as 4.4% after UBS raises the stock to buy from neutral, saying the financial publishing and events firm’s “ambitious” growth targets for 2025 are broadly achievable.

Earlier in the session, Asian stocks also declined across the board following the hot US CPI data and amid fresh COVID concerns in China. Nikkei 225 fell below the 27k level with sentiment not helped by a deterioration in BSI All Industry data. Hang Seng and Shanghai Comp. conformed to the downbeat mood with heavy losses among tech stocks owing to the higher yield environment and with mainland bourses constrained after the latest COVID outbreak and containment measures.

The Emerging-market stocks index dropped about 3%, falling for a third day in the steepest intraday drop since March, as a fresh high in US inflation sparked concerns that the Fed may need to be more aggressive with rate hikes.

In FX, the Bloomberg dollar rose a fourth day as the dollar outperformed all its Group of 10 peers apart from the yen, which earlier weakened to a 24-year low with NOK and AUD the worst G-10 performers. In EMs, currencies were led lower by the South Korean won and the South African rand as the index fell for a fifth day, the longest streak since April. The onshore yuan dropped to a two-week low as a jump in US inflation boosted the dollar and China moved to re-impose Covid restrictions in key cities. India’s rupee dropped to a new record low amid a selloff in equities spurred by continuous exodus of foreign investors. The euro fell for a third day, touching an almost one-month low of 1.0456. Sterling fell after weaker-than-expected UK GDP highlighted the risks to the economy, with a global risk-off mood adding pressure on the currency, UK GDP fell 0.3% from March. The yen erased earlier losses after earlier falling to a 24-year low while Japanese bonds tumbled, prompting a warning from the Bank of Japan as its easy monetary policy increasingly feels the strain of rising interest rates globally. Bank of Japan Governor Haruhiko Kuroda said a recent abrupt weakening of the yen is bad for the economy and pledged to closely work with the government hours after the yen hit the lowest level since 1998.

Bitcoin is hampered amid broad-based losses in the crypto space with the likes of Celsius pausing withdrawals/transfers due to the "extreme market conditions". Currently, Bitcoin is at the bottom-end of a USD 23.7-27.9 range for the session.

In rates, the US two-year yield exceeded the 10-year for the first time since early April, an unprecedented re-inversion. The 2-year Treasury yield touched the highest level since 2007 and the 10-year yield the highest since 2018.

Treasuries continued to sell off in Asia and early European sessions, leaving 2-year yields cheaper by 15bp on the day into the US day as investors continue to digest Friday’s inflation data. Into the weakness a flurry of block trades in futures added to soaring yields. Three-month dollar Libor jumps 8.4bps. US yields remain close to cheapest levels of the day into early US session, higher by 13bp to 6bp across the curve: 2s10s, 5s30s spreads flatter by 5bp and 5.5bp on the day -- 5s30s dropped as low as -16.6bp (flattest since 2000) while 2s10s bottomed at -2bp. US 10-year yields around 3.235%, remain cheaper by 8bp on the day and lagging bunds, gilts by 2.5bp and 5bp in the sector. Fed-dated OIS now pricing in one 75bp move over the next three policy meetings with 175bp combined hikes priced by September, while 55bp -- or 20% chance of a 75bp move is priced into Wednesday’s meeting. A selloff of European government bonds gathered pace as traders priced in a more aggressive pace of tightening from the ECB, with traders now wagering on two half-point hikes by October.

The Bank of Japan announced it would conduct an additional bond-buying operation, offering to purchase 500b yen in 5- to 10-year government bonds Tuesday after 10-year yields rose above the upper limit of its policy band.

In commodities, oil and iron ore paced declines among growth-sensitive commodities; crude futures traded off worst levels. WTI remains ~1% lower near 119.30. Spot gold gives back half of Friday’s gains to trade near $1,855/oz. Base metals are in the red with LME tin lagging

While it's a busy week ahead, with the FOMC meeting on deck where the Fed is set to hike 50bps, or maybe 75bps and even 100bps, there is nothing on Monday's calendar. Fed Vice Chair Lael Brainard will discuss the Community Reinvestment Act in a pre-recorded video and an audience Q&A; she is not expected to discuss monetary policy given the FOMC blackout period.

Market Snapshot

- S&P 500 futures down 2.4% to 3,803.50

- STOXX Europe 600 down 2.0% to 414.12

- MXAP down 2.7% to 161.61

- MXAPJ down 2.8% to 534.45

- Nikkei down 3.0% to 26,987.44

- Topix down 2.2% to 1,901.06

- Hang Seng Index down 3.4% to 21,067.58

- Shanghai Composite down 0.9% to 3,255.55

- Sensex down 3.2% to 52,585.17

- Australia S&P/ASX 200 down 1.3% to 6,931.98

- Kospi down 3.5% to 2,504.51

- Brent Futures down 1.9% to $119.71/bbl

- Gold spot down 0.8% to $1,857.56

- U.S. Dollar Index up 0.39% to 104.55

- German 10Y yield little changed at 1.54%

- Euro down 0.3% to $1.0484

- Brent Futures down 1.9% to $119.69/bbl

Top Overnight News

- “Sell everything but the dollar” is resounding across trading desks as investors reprice the risk that the Federal Reserve hikes rates more aggressively than previously thought

- Investors rushed to price in more aggressive Federal Reserve rate hikes Monday as the US inflation shock continued to reverberate, sending two-year Treasury yields to a 15-year high and strengthening the dollar

- UK Prime Minister Boris Johnson risks reopening divisions that tore his Conservative Party apart in 2019, with his government set to propose a law that would let UK ministers override parts of the Brexit deal he signed with the European Union

- Crypto lender Celsius Network Ltd. paused withdrawals, swaps and transfers on its platform, fueling a broad cryptocurrency selloff and prompting a competitor to announce a potential bid for its assets

- French President Emmanuel Macron has a week to convince voters to give him an outright majority in parliament to ease the way for the controversial social and economic reforms he promised. Shares in France fell on the results

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks declined across the board following the hot US CPI data which rose to a 40-year high and amid fresh COVID concerns in China. Nikkei 225 fell below the 27k level with sentiment not helped by a deterioration in BSI All Industry data. Hang Seng and Shanghai Comp. conformed to the downbeat mood with heavy losses among tech stocks owing to the higher yield environment and with mainland bourses constrained after the latest COVID outbreak and containment measures.

Top Asian News

- Beijing government said the scale of Beijing’s latest outbreak linked to bars is ferocious and explosive in nature after the city reported 166 cases in a bar cluster and with 6,158 people determined as close contacts linked to the bar cluster, while Beijing announced to halt offline sports events from today and the district of Chaoyang is to launch mass COVID testing on June 13th-15th, according to Reuters.

- Shanghai re-imposed a ban on dine-in restaurant services in most districts and punished officials for a management lapse at a quarantine hotel, according to Business Times.

- At least three Chinese cities of Beijing, Nanjing and Wuhan are trialling a shorter quarantine period of 7+7 days for international arrivals at entry points, according to Global Times.

- Beijing government spokesperson says that the Beijing COVID-19 bar outbreak still presents risks to the community; Beijing City reports 45 new local cases of 3pm, according to a health official, via Reuters, adding that the COVID-19 bar outbreak is still developing and epidemic control is at a critical juncture.

- Chinese Defence Minister Wei said China firmly rejects accusations and threats by the US against China, while he added the US Indo-Pacific strategy will create confrontation and that Taiwan is first and foremost China’s Taiwan. Wei also said those that pursue Taiwan's independence will come to no good end and that China will fight to the end if anyone attempts to secede Taiwan from China, according to Reuters. Furthermore, Wei reiterated that Beijing views the annexation of Taiwan as a historic mission that must be achieved which its military would be willing to fight for but added that peaceful unification remained the biggest hope of the Chinese people and they are willing to make the biggest effort to achieve it, according to FT.

- China urges local governments to raise revenue and sell assets to resolve debt risks, via Reuters. Urges local govt's to lower the debt burden; adding, they will crackdown on illegal debt raising.

- Japanese Defence Minister Kishi met with his Chinese counterpart in Singapore and said Japan and China agreed to promote defence dialogue and exchanges, while Japan warned China against attempting to alter the status quo in the South and East China sea, according to Reuters.

- Australian and Chinese defence ministers met in Singapore on Sunday for the first time in three years at the sidelines of the Shangri-La Dialogue summit with the talks described as an important first step following a period of strained ties, according to AFP News Agency.

European bourses are hampered across the board, Euro Stoxx 50 -2.5%, in a continuation of the fallout from Friday's US CPI and amid fresh COVID concerns in China. US futures are in-fitting with this price action, ES -2.4% (sub-3800 at worst), ahead of the FOMC where the likes of Barclays now look for a 75bp hike after the May inflation release. Sectors in Europe are all in the red and feature Travel & Leisure as the underperformer given further cancellations going into the summer period.

Top European News

- UK Northern Ireland Secretary Lewis said the government will publish legislation on the Northern Ireland Protocol on Monday and that the bill will rectify the issues in the protocol, according to Reuters. Reports suggest that the new law could see European judges blocked from having the final say on Northern Ireland-related disputes, according to the Telegraph.

- UK Tory MPs accused PM Johnson of ‘damaging the UK and everything the Conservatives stand for’ as he plans to release legislation on Monday to tear up the Northern Ireland protocol, according to FT.

- UK government ministers are drawing up plans to cut the link between gas and electricity to help reduce household bills for millions of families, according to The Times.

- UK Foreign Minister Truss says she has spoken to EU VP Sefcovic about the Nothern Ireland protocol and the preference is for a negotiated solution; adding, the EU needs to be willing to change the protocol.

- French President Macron’s majority in parliament is at risk as an IFOP initial estimate showed that Macron’s centrist camp is seen qualified for winning 275-310 out of 577 seats after the first round of the French lower house elections, while the IPSOS initial estimate shows the centrist camp is qualified for winning 255-295 seats, according to Reuters. Note, 289 seats are required for a majority

FX

- Greenback extends US inflation data gains as near term Fed hike expectations crank up; DXY hits 104.750 to eclipse May 16 high and expose 105.010 YTD peak.

- Pound undermined by negative UK GDP and output prints plus NI protocol jitters, Cable perilously close to 1.2200 and EUR/GBP tops 0.8575.

- Aussie hit by heightened Chinese Covid concerns and demand implication for commodities, Kiwi feeling contagion and Loonie lurching as oil prices retreat; AUD/USD sub-0.7000, NZD/USD near 0.6300 and USD/CAD just shy of 1.2850.

- Euro and Franc make way for outperforming Buck, but Yen claws back losses on risk dynamics allied to technical retracement; EUR/USD under 1.0500, USD/CHF above 0.9900 and USD/JPY below 134.50 vs 135.20 apex overnight.

- Yuan falls as Beijing suffers ferocious and explosive virus outbreak and Shanghai reimposes restrictions in most districts, USD/CNH pivots 6.7500 and USD/CNY straddles 6.7350.

Commodities

- WTI & Brent are hampered amid the broader market pressure; though, did experience a fleeting move off lows during a break in the newsflow.

- Currently, the benchmarks are lower by circa. USD 2.00/bbl given Friday's CPI, China COVID, geopolitics around US-China-Taiwan and Iran-IAEA developments (or lack of) following last week's camera removal.

- Iraq set July Basrah medium crude OSP to Asia at a premium of USD 3.30/bbl vs Oman/Dubai average and set OSP to Europe at a discount of USD 7.60/bbl vs dated Brent, while it set OSP to North and South America at a discount of USD 1.70/bbl vs ASCI, according to Reuters citing Iraq’s SOMO.

- Libya’s Minister of Oil and Gas Aoun said Libya is currently losing more than 1.1mln bpd of oil production and that most oil fields are closed except for the Hamada field and the Mellitah complex, while the Al-Wafa field continues operations from time to time, according to The Libya Observer.

- QatarEnegy signed an agreement with TotalEnergies (TTE FP) for the North Field East expansion project, while it will announce subsequent signings with partners in the gas field expansion in the near future and possibly at the end of next week, according to Reuters.

- Norwegian Oil and Gas Association reached an agreement in principle with three unions of offshore workers to avert a strike although two of the unions will ask members before signing a deal, according to Reuters.

- Spot gold is pressured by circa. USD 15/oz amid a stronger USD and pronounced yield action; however, the yellow metal is yet to drop below USD 1850/oz and the 10-, 21- & 200-DMAs at USD 1852, 1847 & 1842 respectively.

Fixed Income

- Bond bears still in control and pushing futures down to fresh troughs, at 145.85 for Bunds, 112.33 for Gilts and 115-30+ for 10 year T-note.

- Cash yields test or breach psychological levels, like 1.50%, 2.5% and 3.25%, while 2-10 year US spread inverts briefly on rising recession risk.

- Monday agenda very light, but big week ahead including top tier data and multiple Central Bank policy meetings.

Central Banks

- BoJ announces new offer for bond buying programme in which it is to purchase JPY 500bln in 5yr-10yr JGBs tomorrow and will increase amount of offers for its bond buying as needed.

- BoJ fixed-rate bond purchases exceed JPY 1tln, at their highest since 2018, via Bloomberg; Further reported that the BoJ accepts JPY 1.5tln of bids for the daily offers to purchase 10yr bonds.

- BoJ Governor Kuroda says they must support the economy with monetary easing to achieve higher wages; adding, the domestic economy is still in the midst of a COVID recovery. Increasing raw material costs are increasing downward pressure, recent sharp JPY dalls are undesirable. Additionally, Japan's Finance Minister says a weak JPY has both merits and demerits.

- BoJ buys JPY 70.1bln in ETF, according to a disclosure.

DB's Jim Reid concludes the overnight wrap

This week is squarely and firmly all about the FOMC meeting on Wednesday. We go into it with the 2yr US note up +25bps on Friday and another c.+10bps this morning in Asia. The 2s10s curve has flattened around 20bps since Friday morning to c.2bps as we type. So some dramatic moves.

The problem as we enter the next couple of Fed and ECB meetings is that the central banks haven't quite been able to let go of forward guidance and are a little trapped. To recap, forward guidance has prevented the Fed and the ECB from hiking as early as they needed to, largely because both saw the need to gradually wind down asset purchases over several months first as promised. However this hasn't deterred them, and they have continued to try to flag their intentions to the market in advance with the Fed having previously all but signalled a 50bps this Wednesday, as well as in July, with the ECB now signalling 25bps in July and a strong possibility of 50bps in September.

Providing clarity is admirable but in the wake of another shocking US CPI print on Friday, should a 75bps hike not be a serious consideration? It seems strange that most think policy needs to be restrictive but that it's going to take several meetings to get there from a still highly accommodative position. Without the recent Fed guidance, 75bps would be firmly on the table for Wednesday. This is highly unlikely this week, but our economists think they could break cover from their own guidance and leave the door open for 75bps in July.

DB Research has long been at the hawkish end on inflation and the Fed, and on Friday our US economists further raised their hiking expectations. In addition to 50bps at the next two meetings they have now added 50bps in September and November, before a return to 25bps in December (to 3.125%). They now see the peak at 4.125% in mid-2023. This is closer to the 5% view in the "Why the upcoming recession will be worse than expected" (link here) that David Folkerts-Landau, Peter Hooper and myself published back in April. If we do have a terminal Fed rate approaching a 5-handle it does raise the question as to where 10yr yields top out. My guess would be a slightly inverted curve but it would likely mean the 4.5-5% range discussed in the note from April, mentioned above, is within reason.

We'll recap details of the big US CPI print in last week's recap in the second half of this piece, but it wasn't just this that was the problem on Friday, as the University of Michigan long-term inflation expectations series hit 3.3% (3.0% last month) which was the highest since 2008. This series first hit 3% last May so has actually been range trading for a year, which has been a hope for the doves. However it now risks breaking out to the upside.

It's not just the Fed this week as the BoE (Thursday) and the BoJ (Friday) will also meet. For the UK, a preview from our UK economists can be found here. The team expects a +25bps hike this week and have updated their terminal rate forecast from 1.75% to 2.5%. Staying in the UK, labour market data releases will be out tomorrow with retail sales on Friday.

The week will conclude with a decision from the BoJ and how they address pressures from the yen hovering around a 20-year low, as well as the growing monetary policy divergence between Japan and other G7 economies. Our chief Japan economist previews the meeting here. He expects a shortening or even the abandonment of yield curve control in H2 2023.

In data terms we go back to the US for the main highlights, with PPI (tomorrow) and retail sales (Friday) the main events. China's key May indicators on Wednesday will also have global implications as we await industrial production, retail sales and property investment numbers.

Elsewhere in the US, we have June's Philadelphia Fed business outlook (Wednesday), and May industrial production and capacity utilisation (Friday) numbers. April business inventories will be out on Wednesday and provide markets with a check on corporate stockpiling after Target's renewed warning last week. Finally, a slew of housing market data is due. This includes the June NAHB housing market index (Wednesday) and May building permits and housing starts (Thursday). The impact of rising mortgage rates will be in focus.

In Europe, Germany's ZEW survey for June (tomorrow) is among the key data highlights. We will also see April industrial production and trade balance data for the Eurozone on Wednesday and Eurozone construction output and April trade balance data for Italy on Friday. ECB speakers will also be on the radar for investors as they tend to start to break the party line on the Monday after the ECB meeting. A lengthy line up includes ECB President Lagarde on Wednesday and six other speakers.

Asian stock markets have started the week on a weaker footing with all the major indices trading deep in the red after a rough week on Wall Street. The Hang Seng (-2.81%) is leading losses across the region in early trade amid a tech sell-off whilst the Shanghai Composite (-1.20%) and CSI (-1.07%) are both sliding as a resurgence of Covid cases in China is threating global growth. Elsewhere, the Nikkei (-2.64%) is also sharply down this morning, with the Kospi declining as much as -2.50%, hitting its lowest level since November 2020.

As discussed at the top, 10yr USTs (+2.81 bps) have moved higher to 3.18% while the 2yr yield (+9.8 bps) has exploded higher to 3.16%. Will we see a fresh inversion in the hours and days ahead? Oil prices are lower with Brent futures -1.36% to $120.35/bbl and WTI futures -1.48%, falling below the $120/bbl mark. On the FX side, there is no respite for the Japanese yen from rising Treasury yields as the currency hit a fresh 24yr low, declining -0.50% to 135.08 versus the dollar.

DMs equity futures point to further losses with contracts on the S&P 500 (-1.33%), NASDAQ 100 (-1.87%) and DAX (-1.37%) all trading in negative territory.

Moving on to the French legislative elections. In the first round, exit polls indicate that President Emmanuel Macron is at risk of losing his outright majority after a strong showing by the left-wing alliance in the first round of the country’s parliamentary election. According to the official results, Jean-Luc Mélenchon's left-wing NUPES alliance (+25.61%) finished neck and neck with Mr Macron's Ensemble (+25.71%), in terms of votes cast in Sunday's first round. An average of 5 pollsters expect Macron to win 262-301 seats, with 289 needed to keep his majority. So a nervy wait ahead of the second round.

Turning back to review last week now. The business end of the week had two huge macro events that sent markets into some degree of upheaval.

On Thursday, the ECB met, confirming the end of net APP purchases this month, paving the way for liftoff in July. Beyond July they opened the door for 50 basis point hikes if inflation persists or deteriorates. Judging by their upgraded forecasts, they are now in the ‘persists’ camp. President Lagarde in the press conference took great pains to commit to fighting inflation in a hawkish tone shift. The bigger market reaction was on the apparent lack of progress on any implementation tool designed to avoid fragmentation. President Lagarde tried to downplay the lack of new tool, leaning on PEPP reinvestment flexibility, but the market wasn’t comfortable that this would be enough.

All told, 2yr bunds increased +30.9bps (+13.6bps Friday) on the tighter expected policy path, with the end-2022 policy rate implied by OIS markets ending the week at 0.99%, a new high and in line with our Euro economists updated call (their full review and new call here). The lack of an immediate anti-fragmentation tool saw peripheral spreads underperform, moving to new post-Covid wides, as 10yr BTPs increased +35.9bps (+16.0bps Friday) with 10yr Spanish bonds increasing +34.0bps (+15.6bps Friday), versus a 10yr bund increase of +24.3bps (+8.6bps Friday).

The Friday moves above were given a further boost by yet another above consensus US CPI report, with YoY inflation gaining +8.6% in May versus expectations it would stay consistent with the prior month’s +8.3% reading. FOMC officials have consistently cited deceleration in MoM readings as necessary to find clear and convincing evidence that inflation was stabilising and returning to target, evidence which they surely didn’t get on Friday, as MoM inflation increased +1.0% from +0.3% in April, beating lofty expectations of +0.7%.

The dramatic beats drove the expected path of Fed tightening sharply higher, with 2yr Treasury yields increasing +40.9bps on the week after a +25.0bp gain Friday, it’s largest one-day move since June 2009. The expected fed funds rate by the end of the year reached a new high of 3.22%. The curve aggressively bear flattened, as the reality that the Fed will have to induce slower growth to tame inflation set in; 10yr yields gained +22.0bps on the week and +11.2bps on Friday, with almost all of the increase coming in real yields. That brings 2s10s to 8.8bps, its flattest since its early-April rebound after its brief inversion.

The sharp global policy repricing weighed on equity indices. All major transatlantic indices fell, including the STOXX 600 (-3.95% week, -2.69% Friday), DAX (-4.83%, -3.08%), CAC (-4.60%, -2.69%), S&P 500 (-5.05%, -2.91%), NASDAQ (-5.60%, -3.52%), FANG+ (-2.87%, -3.37%), and Russell 200 (-4.26%, -2.60%). That brings the STOXX 600 -14.49% below its YTD highs reached in the first days of the year, with the S&P 500 -18.40% below the same corresponding metric. Both indices ended the week hovering just above YTD lows.

US CDX HY and Euro Crossover were +58bps and +47bps on the week and around +30bps and +25bps wider on Friday. Both are now at their post covid wides.

Uncategorized

Wendy’s teases new $3 offer for upcoming holiday

The Daylight Savings Time promotion slashes prices on breakfast.

Share this:

Daylight Savings Time, or the practice of advancing clocks an hour in the spring to maximize natural daylight, is a controversial practice because of the way it leaves many feeling off-sync and tired on the second Sunday in March when the change is made and one has one less hour to sleep in.

Despite annual "Abolish Daylight Savings Time" think pieces and online arguments that crop up with unwavering regularity, Daylight Savings in North America begins on March 10 this year.

Related: Coca-Cola has a new soda for Diet Coke fans

Tapping into some people's very vocal dislike of Daylight Savings Time, fast-food chain Wendy's (WEN) is launching a daylight savings promotion that is jokingly designed to make losing an hour of sleep less painful and encourage fans to order breakfast anyway.

Image source: Wendy's.

Promotion wants you to compensate for lost sleep with cheaper breakfast

As it is also meant to drive traffic to the Wendy's app, the promotion allows anyone who makes a purchase of $3 or more through the platform to get a free hot coffee, cold coffee or Frosty Cream Cold Brew.

More Food + Dining:

- Taco Bell menu tries new take on an American classic

- McDonald's menu goes big, brings back fan favorites (with a catch)

- The 10 best food stocks to buy now

Available during the Wendy's breakfast hours of 6 a.m. and 10:30 a.m. (which, naturally, will feel even earlier due to Daylight Savings), the deal also allows customers to buy any of its breakfast sandwiches for $3. Items like the Sausage, Egg and Cheese Biscuit, Breakfast Baconator and Maple Bacon Chicken Croissant normally range in price between $4.50 and $7.

The choice of the latter is quite wide since, in the years following the pandemic, Wendy's has made a concerted effort to expand its breakfast menu with a range of new sandwiches with egg in them and sweet items such as the French Toast Sticks. The goal was both to stand out from competitors with a wider breakfast menu and increase traffic to its stores during early-morning hours.

Wendy's deal comes after controversy over 'dynamic pricing'

But last month, the chain known for the square shape of its burger patties ignited controversy after saying that it wanted to introduce "dynamic pricing" in which the cost of many of the items on its menu will vary depending on the time of day. In an earnings call, chief executive Kirk Tanner said that electronic billboards would allow restaurants to display various deals and promotions during slower times in the early morning and late at night.

Outcry was swift and Wendy's ended up walking back its plans with words that they were "misconstrued" as an intent to surge prices during its most popular periods.

While the company issued a statement saying that any changes were meant as "discounts and value offers" during quiet periods rather than raised prices during busy ones, the reputational damage was already done since many saw the clarification as another way to obfuscate its pricing model.

"We said these menuboards would give us more flexibility to change the display of featured items," Wendy's said in its statement. "This was misconstrued in some media reports as an intent to raise prices when demand is highest at our restaurants."

The Daylight Savings Time promotion, in turn, is also a way to demonstrate the kinds of deals Wendy's wants to promote in its stores without putting up full-sized advertising or posters for what is only relevant for a few days.

Related: Veteran fund manager picks favorite stocks for 2024

stocks pandemicUncategorized

Inside The Most Ridiculous Jobs Report In Recent History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In Recent History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the…

Share this:

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Uncategorized

Shipping company files surprise Chapter 7 bankruptcy, liquidation

While demand for trucking has increased, so have costs and competition, which have forced a number of players to close.

Share this:

{kind=link}

{kind=link}

The U.S. economy is built on trucks.

As a nation we have relatively limited train assets, and while in recent years planes have played an expanded role in moving goods, trucks still represent the backbone of how everything — food, gasoline, commodities, and pretty much anything else — moves around the country.

Related: Fast-food chain closes more stores after Chapter 11 bankruptcy

"Trucks moved 61.1% of the tonnage and 64.9% of the value of these shipments. The average shipment by truck was 63 miles compared to an average of 640 miles by rail," according to the U.S. Bureau of Transportation Statistics 2023 numbers.

But running a trucking company has been tricky because the largest players have economies of scale that smaller operators don't. That puts any trucking company that's not a massive player very sensitive to increases in gas prices or drops in freight rates.

And that in turn has led a number of trucking companies, including Yellow Freight, the third-largest less-than-truckload operator; J.J. & Sons Logistics, Meadow Lark, and Boateng Logistics, to close while freight brokerage Convoy shut down in October.

Aside from Convoy, none of these brands are household names. but with the demand for trucking increasing, every company that goes out of business puts more pressure on those that remain, which contributes to increased prices.

Image source: Shutterstock

Another freight company closes and plans to liquidate

Not every bankruptcy filing explains why a company has gone out of business. In the trucking industry, multiple recent Chapter 7 bankruptcies have been tied to lawsuits that pushed otherwise successful companies into insolvency.

In the case of TBL Logistics, a Virginia-based national freight company, its Feb. 29 bankruptcy filing in U.S. Bankruptcy Court for the Western District of Virginia appears to be death by too much debt.

"In its filing, TBL Logistics listed its assets and liabilities as between $1 million and $10 million. The company stated that it has up to 49 creditors and maintains that no funds will be available for unsecured creditors once it pays administrative fees," Freightwaves reported.

The company's owners, Christopher and Melinda Bradner, did not respond to the website's request for comment.

Before it closed, TBL Logistics specialized in refrigerated and oversized loads. The company described its business on its website.

"TBL Logistics is a non-asset-based third-party logistics freight broker company providing reliable and efficient transportation solutions, management, and storage for businesses of all sizes. With our extensive network of carriers and industry expertise, we streamline the shipping process, ensuring your goods reach their destination safely and on time."

The world has a truck-driver shortage

The covid pandemic forced companies to consider their supply chain in ways they never had to before. Increased demand showed the weakness in the trucking industry and drew attention to how difficult life for truck drivers can be.

That was an issue HBO's John Oliver highlighted on his "Last Week Tonight" show in October 2022. In the episode, the host suggested that the U.S. would basically start to starve if the trucking industry shut down for three days.

"Sorry, three days, every produce department in America would go from a fully stocked market to an all-you-can-eat raccoon buffet," he said. "So it’s no wonder trucking’s a huge industry, with more than 3.5 million people in America working as drivers, from port truckers who bring goods off ships to railyards and warehouses, to long-haul truckers who move them across the country, to 'last-mile' drivers, who take care of local delivery."

The show highlighted how many truck drivers face low pay, difficult working conditions and, in many cases, crushing debt.

"Hundreds of thousands of people become truck drivers every year. But hundreds of thousands also quit. Job turnover for truckers averages over 100%, and at some companies it’s as high as 300%, meaning they’re hiring three people for a single job over the course of a year. And when a field this important has a level of job satisfaction that low, it sure seems like there’s a huge problem," Oliver shared.

The truck-driver shortage is not just a U.S. problem; it's a global issue, according to IRU.org.

"IRU’s 2023 driver shortage report has found that over three million truck driver jobs are unfilled, or 7% of total positions, in 36 countries studied," the global transportation trade association reported.

"With the huge gap between young and old drivers growing, it will get much worse over the next five years without significant action."

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy bankruptcies pandemic stocks commodities

Walmart launches clever answer to Target’s new membership program

Wendy’s has a new deal for daylight savings time haters

EyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

Watch Live: President Biden Reminds Americans Just How Good They’ve Got It Thanks To Him

Catastrophic Risk: Investing and Business Implications

The Digest #187

Redefining Poverty: Towards a Transpartisan Approach

Watch: President Biden Delivers The “Darkest, Most Un-American Speech Given By A President”

Where Is R‑Star and the End of the Refi Boom: The Top 5 Posts of 2023

Is the biotech market rally real? Data suggest comeback in private, public markets

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International4 hours ago

Walmart launches clever answer to Target’s new membership program

-

International1 month ago

International1 month agoWar Delirium

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex