April Payrolls Preview: Get Ready For A Big Miss

April Payrolls Preview: Get Ready For A Big Miss

With the Fed unleashing the most aggressive tightening campaign in decades just days after…

Share this:

With the Fed unleashing the most aggressive tightening campaign in decades just days after US GDP unexpectedly printed negative - a technical recession just one more subzero quarter away - and both the US stock and housing market careening in scary reruns of the 1970s, the only pillar of strength the US has left is the overheating labor market. But, as we noted earlier today, even that is starting to crack.

Which is why tomorrow's April payrolls will be closely scrutinized, not just whether there is an unexpectedly poor jobs print further confirming that the US is on the verge of recession, but also for information on whether red-hot wage growth - a byproduct of the runaway wage-price spiral - is finally cooling, and hinting at peak inflation.

So here's what Wall Street expects tomorrow, courtesy of Newsquawk:

The consensus expects 391k non-farm payrolls to be added in April, with the pace easing from recent averages as well as the prior rate. The breakdown of expectations by bank is as follows:

- Daiwa +500K

- JPM +475K

- Jeff +475K

- MS +475K

- SocGen +475K

- BNP +460K

- BofA +450K

- Barx +450K

- AP +440K

- RBC +420K

- HSBC +405K

- NW +400K

- Scotia +400K

- TD +400K

- BMO +380K

- Citi +360K

- CS +350K

- Miz +350K

- Nom +340K

- DB +300K

- GS +300K

- UBS +300K

- WF +300K

- Median +380K

It is likely that traders will place a great deal of emphasis on the average hourly earnings metrics given that the Fed is more focused on the inflation part of its mandate. Proxies of labor market progress have been mixed in the month: the ADP’s gauge of payrolls disappointed expectations and was below the analyst forecast range; although initial jobless claims inched up slightly comparing the reference periods for the March and April jobs reports, the four-week moving average has fallen, as have continuing claims; within the two ISM reports on business, the employment sub-indices both fell in the month, with the services sector down beneath the 50.0 neutral level. Meanwhile, other reports continue to note the tightness within labor markets, and there are some data points–like the Employment Costs Index–which continue to allude to strongly rising wages as consumer prices continue to rise.

HEADLINE EXPECTATIONS:

- Consensus expects 380k nonfarm payrolls (Wall Street's thought leader Goldman is at 300K) to be added to the US economy in April (vs the prior 431k), with the rate of payroll growth seen further easing below recent trend rates (3-month average at 562k, 6-month average at 600k, 12-month average at 541k).

- The unemployment rate is likely to fall by one-tenth of a percentage point to 3.5%; note, the FOMC projects the jobless rate will fall to that level this year, and currently forecasts it will remain there through the end of 2023, before moving up to around 4.0% in the longer-run. The central bank will next update its projections in June, but at his post-meeting press conference this week, Fed Chair Powell said that job gains have been robust in recent months, and noted that the unemployment rate has declined substantially.

- Average hourly earnings are expected to rise 0.4% compared to March, the same as last month's increase. On an annual basis, hourly earnings as expected to slow down modestly to 5.5% from 5.6% the previous month.

PROXIES: The ADP’s gauge of private payrolls was soft relative to expectations, printing 247k against an expected 395k–below the 300-585k forecast range–although the March data saw an upward revision to 479k from 455k. Analysts at Pantheon Macroeconomics were dismissive about the relevance of the data, noting that it is just a model-driven forecast with a “patchy record”. The consultancy says that the “ADP talks about how it incorporates data from firms which use their payroll processing services, but that’s not the core of their model, which also includes regular macro data and the lagged official payroll numbers,” adding that its estimate “is not statistically significant when incorporated into a payroll model using the Homebase numbers, so we aren’t changing our 300K forecast for Friday’s official headline reading.” Elsewhere, the weekly data that coincides with the typical reference period for the establishment survey showed initial jobless claims rising to 185k from 177k heading into the March jobs report, although the four-week average slipped to 177.5k from 188.75k; continuing claims eased to 1.408mln from 1.542mln, with the four-week average also falling.

BUSINESS SURVEYS: Within the ISM manufacturing survey, the Employment sub-component fell by 5.4 points to 50.9, a shade above the 50.0 neutral level, indicating that labour market momentum in the manufacturing sector was slowing. (NOTE: ISM says that an employment index above 50.5, over time, is generally consistent with an increase in the BLS data on manufacturing employment). The report noted that panellists were still struggling to meet labour management plans, with fewer signs of improvement compared to March. ISM said that there was a smaller share of comments noting greater hiring ease in the month, while an overwhelming majority of panellists were again indicating that their companies were hiring. That said, 34% of those surveyed expressed difficulty in filling positions, which was higher than the 28% in March; turnover rates remained elevated, and there were fewer indications of hiring improvement. The ISM said employment levels, driven primarily by turnover and a smaller labour pool, remained the top issue affecting further output growth. The Services ISM, meanwhile, saw its employment sub-index decline by 4.5 points, taking it to 49.5 – below the 50.0 neutral mark. The survey noted that comments from respondents included “job openings exist, but finding talent to fill them remains a struggle across most industry sectors and job categories” and “demand for employment remains hypercompetitive; there is just not enough qualified personnel available.”

WAGES: The street expects average hourly earnings to rise by 0.4% M/M in April, although the annual measure is seen slipping by one-tenth of a percentage point to 5.5% Y/Y. Much of the market’s focus will be on these wage components, particularly after the Q1 employment cost index (ECI) rose by 1.4%, topping the consensus 1.1%; on an annualized basis; the ECI was up 5.2% Y/Y. Analysts have been paying more attention to the ECI data after Fed Chair Powell last November cited it as a measure that he was monitoring closely when gauging how employment compensation was faring. Analysts generally agree that the trends seen in this report suggest the labour market is tight and consistent with the need for the FOMC to front-load rate hikes to put a lid on price pressures. UBS says that a composition-adjusted average hourly earnings measure that it constructed has recently been running at a little below 4%, which is a bit below the pace of annualised gains seen in the ECI data. The bank is expecting that the April AHE data will likely surprise to the upside, however, this would be due to calendar shifts, and should not be taken as a strong economic signal.

ARGUING FOR A WEAKNER THAN EXPECTED REPORT:

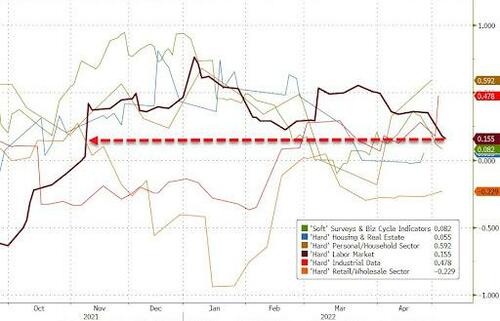

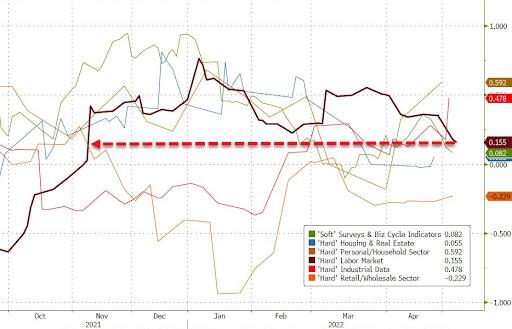

- Labor supply constraints. As shown in Exhibit 1, when the labor market is tight, job growth tends to slow during the spring hiring season. This reflects the combination of a high seasonal hurdle—the BLS adjustment factors assume roughly 800k of seasonal hiring in April—with fewer available workers. The arrival of the youth summer labor force tends to ease these constraints in June and July.

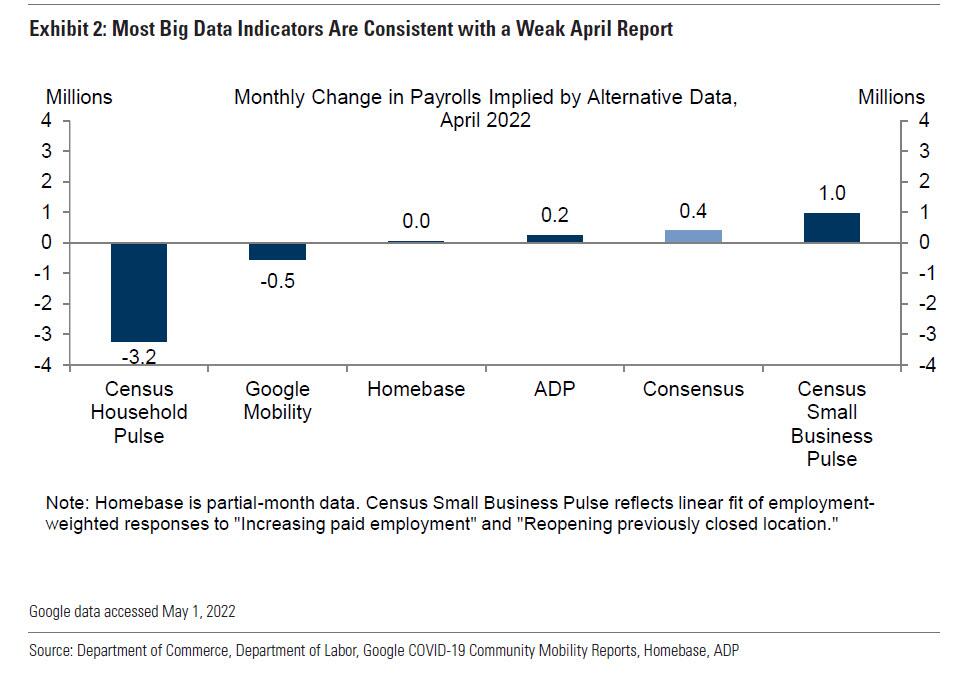

- Big Data. High-frequency data on the labor market generally indicate weakness in April employment, with four of the five indicators we track consistent with a below-consensus report (see Exhibit 2). The Census Household Pulse Survey is an outlier to the downside; however, that has series has been very volatile in recent months (-3.2mn in April after +3.1mn in March, +4.8mn in February, and -3.7mn in January).

- Employer surveys. The employment components of business surveys generally decreased in April. Our services survey employment tracker decreased by 0.9pt to54.8 and our manufacturing survey employment tracker decreased 1.3pt to 56.8.

- Job cuts. Announced layoffs reported by Challenger, Gray & Christmas increased by 8% month-over-month in April, after increasing by 5% in March (SA by GS).

- ADP. Private sector employment in the ADP report increased by 247k in April, below consensus expectations. We believe the ADP miss reflected the combination of slowing underlying job growth and a drag from the other inputs to the ADP model.

ARGUING FOR A STRONGER-THAN-EXPECTED REPORT:

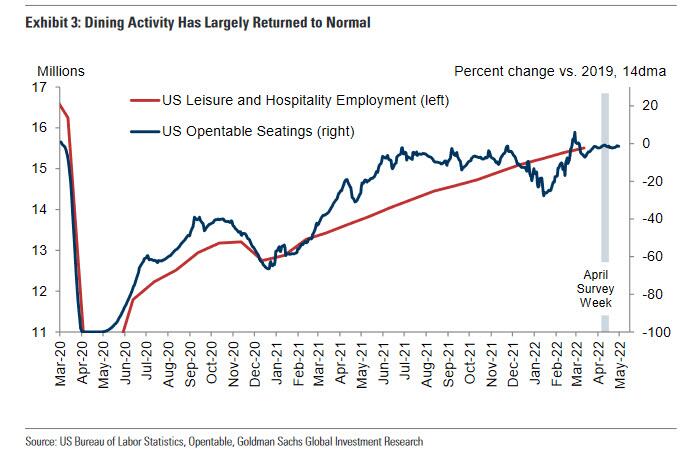

- Public health. After reaching new highs in December and early January, domestic covid infections fell sharply in the early spring. And while infections have begun to rise again from low levels, consumer and business activity has not been significantly impacted. For example, as shown in Exhibit 3, dining activity has been relatively stable at pre-pandemic levels since mid-March. Forecasts assume a roughly100k rise in leisure-sector payrolls in Friday’s report (mom sa).

- Evolution of the seasonal factors. The April seasonal factors have evolved favorably in recent years (+787k in April 2021 vs. +897k in April 2016), likely reflecting the seasonal adjustment refitting to the weaker-than-expected April payroll prints during the pandemic. This lower seasonal hurdle represents a tailwind of roughly 100k, other things equal, in our view. However, we still view April seasonality as a net negative factor due to binding constraints on labor supply duringa rehiring month.

- Jobless claims. Initial jobless claims decreased during the April payroll month, averaging 175k per week vs. 209k in March. Continuing claims in regular state programs decreased 139k from survey week to survey week.

- Job availability. The Conference Board labor differential—the difference between the percent of respondents saying jobs are plentiful and those saying jobs are hard to get—decreased by 2.5pt to +44.6. JOLTS job openings increased by 205k in March to an all-time high of 11.5mn

The take home message is simple: bulls should pray for a huge miss, the bigger the better, because between negative GDP and a big hit to the "overheating labor market" stories, the Fed's aggressive hiking and QT will last at most a few months, before it is followed by its logical successor: ZIRP (or NIRP) and QE, both of which will sent stocks, gold and cryptos to new all time highs.

International

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canadaGovernment

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

{kind=link}

{kind=link}

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

{kind=link}

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Mortgage rates fall as labor market normalizes

Economic Earthquake Ahead? The Cracks Are Spreading Fast

February Employment Situation

Low Iron Levels In Blood Could Trigger Long COVID: Study

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex