3 “Perfect 10” Stocks With Double-Digit Upside Potential

3 "Perfect 10" Stocks With Double-Digit Upside Potential

Share this:

This past Friday we got our first hint of the route our economic recovery from coronavirus may take – and the news was unequivocally good. Despite an uneven reopening, with some states all in and others continuing their lockdowns, the May jobs report showed the largest surge in employment in the survey’s history.

As the recovery proceeds, investors have to find the right stocks to take advantage of the jump in the market. TipRanks has the data tools to bring clarity from the market conditions – especially the Smart Score tool. Building on eight separate factors, the Smart Score collates all the available data on a stock and distills it down to a single number. Some stocks – the best options out there – get the coveted ‘perfect 10.’

Using the Smart Score tool, we managed to pinpoint 3 stocks that currently present perfect investing opportunities — all receive a score of a “perfect 10.”

Universal Technical Institute (UTI)

The first “perfect 10” name on today’s list is Universal Technical Institute, a network of technical post-secondary schools and colleges throughout the US. Courses are offered in automotive repair, diesel/industrial technology, and collision repair. The school offers manufacturer specific training in marine and motorcycle mechanics, and partners with NASCAR.

Earnings turned negative in Q1, even though revenues grew year-over-year. In Q2, reported last month, EPS came in at a 4-cent loss, again, while revenues grew. The Q2 top line, $82.7 million, beat the forecast and was up modestly from the year before.

B. Riley FBR analyst Rajiv Sharma believes that UTI will see a fast turnaround once COVID-19 restrictions are eased. He writes, “the bevy of lower income jobs (retail, restaurants etc) that typically compete with a student’s stint at UTI, are now more likely to take longer to come back if not impacted severely. Soaring unemployment rates too, as shown from recessions in the past, are also expected to start causing a rise in student enrollments soon. Ongoing enrollments, seasonally slow during this period anyway, have not been out of the ordinary. UTI, for the first time, had several hundred enroll into their recently-launched online+workshop curriculum.”

Sharma’s $11 price target on UTI implies a robust upside of 46%, and backs up his Buy rating. (To watch Sharma’s track record, click here)

Overall, we’re looking at a stock with a unanimous Strong Buy analyst consensus rating. Wall Street has given UTI 4 thumbs up in recent weeks. The $9.50 average price target suggests room for 26% growth from the $7.51 share price. (See UTI stock analysis on TipRanks)

InterDigital (IDCC)

Next up is InterDigital, a technology R&D firm that specializes in wireless and video tech for mobile devices and networks. The company’s technologies are integral in streaming media, 5G, and virtual reality. As can be imagined, the current corona crisis – with its sudden surge in remote connection use and telecommuting work – has been an opportunity for InterDigital.

IDCC’s first quarter earnings broke even, doing better than the Street had anticipated. On the top line, revenues of $76.2 million also beat the forecast and were substantially higher year-over-year.

Roth Capital analyst Scott Searle sees a clear path forward for IDCC. He writes of the company, “With an attractive long-term model, strong balance sheet (~$13+ net cash/share) and defensible IP position, IDCC currently trades at 13x 2021 pro forma EPS (net of cash). We believe that the company has competently managed implementation and communication of accounting confusion around ASC 606 and expect the major contributor to the disparity (Huawei) to be rectified in 2019.”

Searle’s rates IDCC a Buy and his $104 price target suggests an impressive upside of 76% for the coming year. (To watch Searle’s track record, click here)

Overall, Wall Street agrees with Searle. IDCC has a unanimous Strong Buy analyst consensus rating, based on 3 recent reviews. Shares are priced at $58.51, and the $93.67 average price target implies a one-year upside of 60%. (See InterDigital stock analysis on TipRanks)

Cirrus Logic (CRUS)

Last on our list is a mid-cap player in the semiconductor chip industry. Cirrus is a fabless chipmaker; that is, the company designs and markets its chips, while outsourcing the manufacturing process. Cirrus’ chips are widely used in audio and voice reproduction systems. The company reported $1.28 billion in revenue for FY20, ending last month, and a solid financial position. Cirrus claims some $600 million in available cash and do outstanding debt – an enviable position for any company, but especially so during these difficult times.

Still, despite the company’s strong performance, it has been impacted by the coronavirus and the economic shutdowns. Travel and trade restrictions have disrupted supply and distribution chains, as they have across the board. CRUS shares are down 11.3% from its pre-bear market levels.

Ruben Roy, 5-star analyst with Benchmark, is optimistic about this stock, writing, “We continue to believe that as audio and voice technologies continue to proliferate, CRUS will remain amongst the biggest beneficiaries… with a growing portfolio of technologies and continued strength of customer relationships, we continue to expect CRUS to be well positioned as market trends improve.”

Roy’s Buy rating is backed by a $95 price target that indicates his confidence in 39% upside growth for the coming year. (To watch Roy’s track record, click here)

The analyst consensus rating on CRUS is a Moderate Buy, based on 3 Buys and 2 Holds set in the last couple of months. The shares have an $86 average price target, which suggests a 20% growth potential from the current $71.60 trading price. (See Cirrus Logic stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

The post 3 "Perfect 10" Stocks With Double-Digit Upside Potential appeared first on TipRanks Financial Blog.

Uncategorized

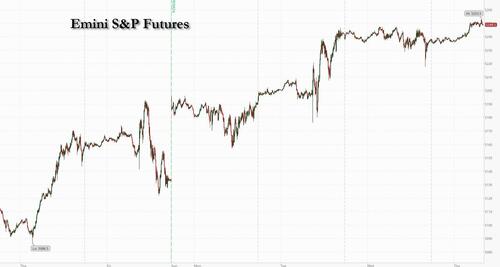

Futures Rise To New Record High Ahead Of Data Deluge

Futures Rise To New Record High Ahead Of Data Deluge

Another day, another all time high on deck. US equity futures are higher ahead of today’s…

Share this:

Another day, another all time high on deck. US equity futures are higher ahead of today’s PPI / Retail sales data, which we expect to be a big miss to expectations based on real-time card spending data. As of 8:00am, S&P futures were 0.3% higher trading around 5,250 while Nasdaq futures gained 0.4%, led by tech with the Mag7 stocks higher premarket (ex-NVDA, TSLA) as semis outperform pre-market. Europe trades mainly higher led by France while Asia is mixed on light overnight news. The yield curve is seeing some bear steepening with 10Y yield unchanged at 4.19%; keep an eye on the backend of the curve as we approach next week’s BOJ. The USD is stronger and commodities are mixed: energy is leading as WTI crude futures rise higher by almost 1% on the day after IEA projected a supply deficit for the rest of 2024. Today’s macro data focus includes Retail Sales (consensus +0.4%, last -0.4%), PPI (cons +0.2%, last +0.5% core PPI m/m) and Jobless Claims (exp. 218k, last 217k).

In premarket trading, Netflix and Meta Platforms rose with analysts flagging potential benefits to social-media and streaming companies from legislation targeting TikTok. Dollar General jumped after an upbeat forecast. Here are some other notable premarket movers:

- Citigroup shares rise 1.9% as Goldman Sachs raised the recommendation on the lender to buy from neutral. The broker sees “a realistic path” to higher returns and “compelling valuation support.”

- Hello Group the parent firm of Chinese dating apps Momo and Tantan, trades 16% lower after reporting a drop in paying users for both apps.

- Fisker shares plunge 38% after the Wall Street Journal reported the electric-vehicle startup has hired advisers to assist with a possible bankruptcy filing.

- Robinhood shares rise 12% after the online brokerage platform reported positive operating data in February including rising assets under custody and surging trading volume.

- SentinelOne shares drop 11% after the security software company gave a full-year revenue forecast that was weaker than expected at the midpoint of the range.

- Turtle Beach shares soar 27% after the sound technology company reported its fourth-quarter results and said it would buy PDP at an enterprise value of $118 million.

- UiPath shares rise 7.0% after the automation software company reported fourth-quarter results that beat expectations.

- Under Armour shares are down 7.2% after the company announced the return of Kevin Plank as chief executive officer, replacing Stephanie Linnartz, who was in the role for just over a year. Jefferies said the surprise change in leadership suggests uncertainty on the strategic direction of the sportswear maker.

- Weibo ADRs climb 5.5% after the Chinese social media company declared its second special cash dividend of $200m in a year, offsetting adjusted earnings and active users that missed analyst expectations.

While traders have been trimming bets on deep and imminent rate cuts, that hasn’t dampened enthusiasm for stocks, with the S&P 500 setting new records in its longest stretch since 2018 without a decline of at least 2%, according to Bloomberg data. Today's PPI data will be the final inflation report before next week’s Fed policy meeting. Officials are expected to hold interest rates steady for a fifth straight meeting, but the question is when they’ll start lowering borrowing costs.

“We’ve just upgraded our price target on the S&P 500, European stocks and Japanese equities because underlying data continues to be pretty resilient,” said Grace Peters, head of global investment strategy at JPMorgan Private Bank, who sees the US benchmark reaching 5,600 in a bull-case scenario. “The most realistic bull case is that corporate profits are stronger than expected.”

In politics, Donald Trump floated hedge fund titan John Paulson as possible Treasury secretary if he wins the November presidential election, and has held a series of meetings with other potential cabinet picks. Treasury Secretary Janet Yellen said it’s “unlikely” that market interest rates will return to levels that prevailed before the Covid-19 pandemic.

ECB Governing Council member Yannis Stournaras recommended two interest-rate cuts before the August summer break, and another two by the end of the year. Money markets maintained wagers on the scope for rate cuts this year, with the first quarter-point move seen by June, followed by two more and a 70% chance of a fourth. Bunds trimmed a small decline and the euro was steady.

Sentiment remained fragile in Chinese markets despite officials pledging central government funds to encourage consumers and businesses to replace old equipment and goods. Shares linked to Asian copper miners advanced after the metal jumped to an 11-month high on likely capacity cuts at Chinese smelters.

European stocks rose for a third day as Stoxx 600 touches a fresh record even as tech firms extend their decline for a second session. The mood points to a sector rotation in the background as retail, real estate and consumer products lead this month’s Stoxx 600 gains. Here are some of the biggest movers on Thursday:

- Encavis gains as much as 28% and trades slightly below the value of KKR’s recommended cash offer for the renewable-energy producer. Analysts see a high likelihood of deal completion, even as the offer price is below their respective PTs.

- Trainline shares jump as much as 12%, reaching the highest intraday since September 2022, after the train-ticketing platform reported full-year net ticket sales that topped estimates. Morgan Stanley highlighted the company’s performance in the UK, which was a main driver of the beat to net ticket sales.

- K+S shares rise as much as 9% after the German agricultural chemicals firm posted results which Citi called “encouraging” and guidance that showed scope for further earnings growth. Analysts pointed to the cash flow outlook as bringing some relief.

- NEL shares rise as much as 5.9% after the Norwegian hydrogen technology firm received $84 million of funding from the State of Michigan and the US Department of Energy, which RBC said confirms the company as a key green hydrogen player.

- IG Group rises as much as 4.9% after the UK trading platform reported third-quarter earnings which RBC said were better-than-expected and showed resilient trading revenues, client numbers and cash balances.

- RWE gains as much as 3.7% after the German utility reiterated its guidance, which Morgan Stanley said will trigger renewed interest in the stock. The company also expects to raise its dividend for the current fiscal year.

- OSB Group shares slump as much as 30%, the biggest drop since July, as the British banking group’s weaker-than-expected guidance for net interest margin overshadowed a full-year results beat.

- Basic-Fit drops as much as 16% as the health and fitness club operator’s growth plans disappoint.

- Lanxess shares fall as much as 11% after the German specialty chemicals firm’s 2023 sales and margins fell short of estimates, while its first-quarter adjusted Ebitda outlook also undershot consensus.

Earlier in the session, Asian stocks edged lower, with the regional gauge on track for its first weekly drop in two months, weighed down by losses in Chinese technology shares and Australian banks. The MSCI Asia Pacific Index fell as much as 0.2% amid choppy trading. Financial names including Westpac Banking and ANZ were among the biggest drags on the index after Macquarie downgraded the Australian lenders. Copper miners were a bright spot in the region after the metal jumped to an 11-month high. BHP was the top positive contributor to the Asian gauge as Citigroup raised the stock to buy.

Equities in mainland China and Hong Kong ended lower, with the Hang Seng Tech Index falling more than 1% despite officials pledging central government funds to encourage consumers and businesses to replace old equipment and goods. Shares linked to Asian copper miners advanced after the metal jumped to an 11-month high on likely capacity cuts at Chinese smelters. The US House of Representatives passed a bill to ban TikTok in the country unless its Chinese owner sells the video-sharing app.

In FX, bloomberg dollar spot index gained 0.1% to erase Wednesday’s decline. The yen reversed an initial gain as Treasury yields turned higher and ahead of Rengo wage outcomes on Friday, which may affect the Bank of Japan’s policy decision. SEK and CHF are the weakest performers in G-10 FX, NZD and GBP outperform.

In rates, treasuries were narrowly mixed after yields edged to new weekly highs ahead of economic data slate including PPI and retail sales. US yields slightly richer from front-end out to belly of the curve and slightly cheaper across long-end, steepening 2s10s by almost 1bp on the day; 10-year yields around 4.19% with gilts outperforming by 1.2bp in the sector. Gilts outperform slightly, and core European rates drew support from comments by ECB’s Yannis Stournaras, who recommended two interest-rate cuts before the summer break in August. S&P 500 futures advance toward last week’s all-time high and WTI crude oil futures top $80/bbl; peripheral spreads tighten to Germany with 10y BTP/Bund narrowing 2.9bps to 119.8bps amid dovish remarks from ECB speakers. German, gilt and Treasury 10-year yields are steady as traders await US producer-price data, which comes after a sticky consumer reading earlier this week.

In commodities, crude oil added to the biggest gain in about five weeks after the International Energy Agency said global oil markets face a supply deficit throughout 2024 as OPEC+ looks set to continue output cuts. Iron ore extended its decline toward $100 a ton, with few signs of a turnaround in Chinese steel demand. Gold edged lower. Spot gold falls roughly $5 to trade near $2,170/oz.

Bitcoin took a breather after soaring to highs yesterday, and currently holds just shy of USD 73.5k.

The US economic data calendar includes February retail sales and PPI and weekly jobless claims (8:30am) and January business inventories (10am). No scheduled Fed speakers due before March 20 policy decision. From central banks, we’ll hear from ECB Vice President de Guindos, along with the ECB’s de Cos, Schnabel, Knot and Stournaras.

Market Snapshot

- S&P 500 futures up 0.3% to 5,184.75

- STOXX Europe 600 up 0.2% to 508.44

- MXAP up 0.2% to 176.55

- MXAPJ little changed at 540.98

- Nikkei up 0.3% to 38,807.38

- Topix up 0.5% to 2,661.59

- Hang Seng Index down 0.7% to 16,961.66

- Shanghai Composite down 0.2% to 3,038.23

- Sensex up 0.3% to 73,006.82

- Australia S&P/ASX 200 down 0.2% to 7,713.63

- Kospi up 0.9% to 2,718.76

- German 10Y yield little changed at 2.38%

- Euro little changed at $1.0941

- Brent Futures up 0.2% to $84.19/bbl

- Gold spot down 0.2% to $2,169.72

- US Dollar Index little changed at 102.85

Top Overnight News

- US Treasury Secretary Janet Yellen said it’s “unlikely” that market interest rates will return to levels that prevailed before the Covid-19 pandemic triggered a wave of inflation and higher yields. BBG

- BOJ Governor Kazuo Ueda will likely take his time normalizing ultra-loose monetary policy after ending negative interest rates, former central bank executive Hideo Hayakawa said on Thursday. RTRS

- Japan's largest industrial union said on Thursday the average pay rise offered by 231 firms for both full-time and part-time employees was the biggest since 2013, amid signs wage hikes were broadening. RTRS

- Chinese wheat importers have cancelled or postponed about one million metric tons of Australian wheat cargoes, trade sources with direct knowledge of the deals said, as growing world stockpiles drag down prices. RTRS

- The crude market faces a supply deficit throughout 2024 — instead of the surplus previously expected — as OPEC+ looks set to continue output cuts in the second half, the IEA said. The agency bolstered forecasts for global demand growth by 9% to 1.3 million barrels a day, on a stronger US outlook. BBG

- The ECB must lower borrowing costs twice before its August summer break and two more times before the end of the year, without being swayed by the US Federal Reserve, according to Governing Council member Yannis Stournaras. BBG

- The US has held secret talks with Iran this year in a bid to convince Tehran to use its influence over Yemen’s Houthi movement to end attacks on ships in the Red Sea, according to US and Iranian officials. FT

- Tuesday’s CPI report shouldn’t fundamentally alter expectations that the Fed will cut rates around three times this year because it isn’t likely to justify a meaningful revision in officials’ forecasts for inflation as measured by that index, said Eric Rosengren, who headed the Boston Fed from 2007 to 2021. WSJ

- Donald Trump has talked about hedge fund titan John Paulson as Treasury secretary if he wins the November presidential election, and has held a series of meetings with potential cabinet picks. Other potential names in the mix for the top Treasury post, should Trump defeat incumbent President Joe Biden, include former US trade representative Robert Lighthizer, Susquehanna International Group LLP founder Jeff Yass and Key Square Group LP founder Scott Bessent. BBG

- Microsoft (MSFT) and Oracle (ORCL) expand partnership to satisfy global demand for oracle database Azure.

MicroStrategy Incorporated (MSTR) - The crypto investor announced its intention to offer USD 500mln of convertible senior notes due 2031, with an additional option for purchasers to buy up to USD 75mln more. MSTR intended to use the proceeds to purchase additional bitcoin and for general corporate purposes. Shares +4.5 pre-market trade - Under Armour (UAA) - Kevin Plank will assume the roles of President and CEO from April 1st, succeeding Stephanie Linnartz. Mohamed El-Erian will become the non-executive Chair of the Board. Plank, founder of Under Armour, transitions from the Executive Chair role, while Linnartz will remain to advise until April 30th. Shares -4.5% in pre-market trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed after the indecisive performance stateside amid light catalysts and tech weakness, with participants lacking conviction ahead of next week's central bank bonanza. ASX 200 was subdued as losses in financials and tech overshadowed the gains in the commodity-related sectors. Nikkei 225 traded indecisively after a slew of BoJ-related source reports suggesting a policy shift next week. Hang Seng and Shanghai Comp. were somewhat varied with the Hong Kong benchmark pressured amid tech-related headwinds after the US House approved the bill which threatens to ban TikTok, while the mainland was indecisive with downside initially cushioned after China issued plans to promote trading in consumer goods and equipment upgrades.

Top Asian news

- BoJ will discuss whether to end its negative interest rate policy as pay hikes by major companies bring the central bank's 2% price stability target within reach. Furthermore, with more BoJ policymakers embracing the idea, the decision is seen coming down to the results of Japan's annual wage negotiations, to be published by top labour confederation Rengo on Friday, according to Nikkei.

- Japanese Federation of Textile, Chemical, Commerce, Food and General Services Workers' Unions which is the largest industrial union and known as UA Zensen stated that the average pay increase offered by 231 firms reached the biggest on record since 2013 compared with the same period last year.

- Taiwan Central Bank Governor said they are concerned potential electricity price hikes will result in a chain reaction effect on inflation expectations and they will be very prudent about discussions on interest rates this time, while he added that they will not likely cut interest rates before June, according to Reuters.

- Foxconn (2317 TT) sees 2024 revenue to increase significantly Y/Y; sees Q1 revenue to slightly decline Y/Y, sees Q1 revenue for smart consumer electronics to slightly decline Y/Y. Q4 net profit TWD 53.14bln (exp. 43.5bln; prev. 43.1bln Q/Q). Sees Q1 revenue for cloud and networking products to be flat Y/Y. Sees Q1 revenue for computing products to be flat Y/Y. Says major growth momentum this year will be AI servers, expects the servers business to grow strongly this year; sees very strong demand in AI from clients. AI server growth in 2023-25 could be stronger than the market average, potentially above 30% or higher annually. Semiconductor revenue will surpass TWD 100bln this year.

- China's Commerce Ministry on the review into Australian wine tariffs says the final ruling will be made in accordance with the investigation procedures.

- Chinese State Planner has issued a draft rules to support high-quality firms to take on medium and long-term foreign debt.

European bourses are mostly in the green, with sentiment lifted after dovish remarks from ECB's Stournaras. The SMI (-0.3%) underperforms, hampered by post-earnings weakness in Swiss Life (-5.7%). European sectors are mixed, with Basic Resources found at the foot of the pile, hampered by broader weakness in base metals, whilst Energy benefits from firmer crude prices. US equity futures (ES +0.2%, NQ +0.5%, RTY +0.2) are trading on a firmer footing, with slight outperformance in the NQ, attempting to pare back some of its losses from the prior session.

Top European news

- ECB's Stournaras says they have to cut rates twice prior to the summer break, via Bloomberg; four cuts in 2024 seems reasonable. Need to begin cutting soon; policy must not become too restrictive. Dismisses the idea that the ECB cannot cut before the Fed. Don't exaggerate the risk of a wage-price-spiral. Structural portfolio will include government bonds. Remarks which sparked a modest uptick in EGBs.

- ECB Chief Economist Lane says the ECB has a bit more confidence that they are heading towards the inflation goal, more data will help gain more confidence, via CNBC; Better not to analyse whether it is April or June when it comes to lowering rates

- Norges Bank Regional Network Report Q1 2024 : Expects overall activity to remain virtually unchanged in the first half of 2024. Prospects have been revised up somewhat since the previous survey.Employment plans for 2024 Q1 have been revised up slightly since the previous survey. Contacts expect annual wage growth of 4.9% in 2024, which is an upward revision from the 4.5% estimate in November.

FX

- DXY is broadly flat vs. peers ahead of a slew of Tier 1 US data, with the index contained within yesterday's 102.66-103.02 range. Strong data could see DXY reclaim 103 and approach the weekly high at 103.17. A soft release could see the index approach the post-NFP low at 102.35.

- EUR is steady vs. the USD and contained within yesterday's 1.0920-1.0963 range. ECB's Stournaras sparked modest pressure for the Single-Currency, though the move quickly faded.

- JPY is a touch softer vs. the USD but ultimately contained within yesterday's 147.23-148.05 range. Markets are on tenterhooks ahead of tomorrow's Rengo announcement which will likely shape expectations for next week's BoJ decision.

- AUD/USD is flat vs. the USD in what has been a week of contained price action, and currently sits within yesterday's 0.6599-0.6635 range. NZD is trivially firmer vs. USD after edging above yesterday's peak at 0.6170.

- SEK is weaker vs. peers given soft inflation metrics which has seen odds of a May cut creep higher. EUR/SEK made a new high for the week at 11.218 but still some way off March highs.

Fixed Income

- Once again, USTs are marginally in the red within the European morning. Specifics since the 30yr auction (strong) have been light and USTs are now back to pre-auction levels of 110-30; data and 20yr announcement due.

- Gilts are the relative laggard as they continue to pare from the outperformance seen on Tuesday's labour data, with few fresh drivers able to change the narrative. Gilts hold towards the lower end of a 99.01-98.80 range.

- Bunds are in the red but off the 132.42 trough after remarks from ECB's Stournaras who said that two cuts are needed before the summer break and four for 2024 is reasonable. Commentary which has helped to lift Bunds to a 132.66 high. Comments from ECB's Lane failed to spark any price action in Bunds.

Commodities

- Crude is firmer with gains facilitated by Russian facility outages, bullish US energy inventory data and several geological updates. Brent May rose from support at USD 83.98/bbl and currently holds just shy of USD 84.75/bbl.

- A subdued morning thus far for precious metals and with overall trade rangebound, awaiting impetus from US Tier 1 data. XAU trades within a tight range between USD 2,167.47-2,177.05/oz.

- Base metals are mostly subdued as a function of the Dollar and quiet macro updates. Copper holds onto a bulk of the prior day's gains (following reports that major Chinese copper smelters agreed to curb output) whilst iron ore overnight continued trundling lower amid ongoing Chinese demand woes.

- IEA OMR: Raises 2024 oil demand growth forecast by 110k BPD to 1.3mln BPD; says if OPEC+ voluntary cuts remain in place through 2024, market is seen in a slight deficit rather than a surplus. While 2024 growth has been revised up by 110 kb/d from last month’s Report, the pace of expansion is on track to slow from 2.3 mb/d in 2023 to 1.3 mb/d, as demand growth returns to its historical trend while efficiency gains and EVs reduce use. World oil production is projected to fall by 870 kb/d in 1Q24 vs 4Q23 due to heavy weather-related shut-ins and new curbs from the OPEC+ bloc. Refining margins improved through mid-February before receding, with the US Midcontinent and Gulf Coast as well as Europe leading the gains. In this Report, we are now holding OPEC+ voluntary cuts in place through 2024 – unwinding them only when such a move is confirmed by the producer alliance (see OPEC+ cuts extended). On that basis, our balance for the year shifts from a surplus to a slight deficit, but oil tanks may get some relief as the massive volumes of oil on water reach their final destination.

Geopolitics: Middle East

- US Secretary of State Blinken held a video call with officials from Cyprus, Britain, UAE, Qatar, EU and the UN to discuss getting a new maritime corridor for delivering humanitarian aid into Gaza up and running, according to Reuters.

- US is expected to impose new sanctions on two illegal outposts in the occupied West Bank that were used as a base for attacks by extremist Israeli settlers against Palestinian civilians, according to three US officials cited by Axios.

- US CENTCOM said Iranian-backed Houthis fired one anti-ship ballistic missile in the Gulf of Aden although the missile did not impact any vessels and there was no damage reported, while its forces successfully engaged and destroyed four unmanned aerial systems and one surface-to-air missile in Houthi-controlled areas of Yemen.

Geopolitics: Other

- Taiwan and China authorities both dispatched teams to join a rescue mission after a Chinese fishing boat capsized near Taiwan-controlled Kinmen Islands on Thursday morning, according to Taiwanese press.

- Philippines President Marcos and US Secretary of State Blinken to meet on March 19th to discuss cooperation and security matters, while Marcos vowed to defend maritime rights in the face of a 'more active attempt by China to annex some territories'.

- North Korean leader Kim guided a military demonstration involving a tank unit on Wednesday, according to KCNA.

US Event Calendar

- 08:30: Feb. Retail Sales Ex Auto and Gas, est. 0.3%, prior -0.5%

- Feb. Retail Sales Control Group, est. 0.4%, prior -0.4%

- Feb. Retail Sales Ex Auto MoM, est. 0.5%, prior -0.6%

- 08:30: March Initial Claims, est. 218K, prior 217K

- March Continuing Claims, est. 1.91m, prior 1.91m

- 08:30: Feb. PPI Final Demand MoM, est. 0..3%, prior 0.3%

- Feb. PPI Final Demand YoY, est. 1.2%, prior 0.9%

- Feb. PPI Ex Food and Energy YoY, est. 1.9%, prior 2.0%

- Feb. PPI Ex Food and Energy MoM, est. 0.2%, prior 0.5%

- 10:00: Jan. Business Inventories, est. 0.2%, prior 0.4%

DB's Jim Reid concludes the overnight wrap

Markets struggled to keep up their momentum yesterday, with the S&P 500 (-0.19%) falling back from its all-time high, whilst yields on 10yr Treasuries (+3.9bps) moved up for a third day running. That came amidst growing concern about how stretched the rally was becoming, with the S&P 500 having risen by more than +25% in less than 100 trading days. Moreover, there’s still quite a bit of focus on inflation, and the US CPI release this week has led to some scepticism about whether the Fed will be able to cut rates by June after all.

That focus on inflation is likely to remain today, as we’ll get the US PPI release at 12:30 London time. That’s an important one, because several components from the PPI feed into the PCE measure of inflation, which is the one that the Fed officially targets. According to our US economists, one category to focus on will be portfolio management and investment advice, which tends to follow equity prices with a one-month lag, and added about 8bps to the core PCE print in January. So even though we won’t get the PCE inflation data until March 29th, the reading today will offer a better sense of what that’s likely to be.

Ahead of that release, there was a further selloff for sovereign bonds, which came as investors dialled back the chance of near-term rate cuts again. For instance, the chance of a rate cut by June was down to 73%, down from 78% the previous day. And for the year as a whole, the number of cuts priced by the December meeting came down by -4.9bps to 80bps, the lowest in a couple of weeks. In turn, that helped yields rise further, and the 2yr yield rose +4.8bps to 4.63%, whilst the 10yr Treasury yield was up +3.9bps to 4.19%. The sell-off in Treasuries came despite a strong 30yr auction, which saw $22bn of bonds issued 2bps below the pre-sale yield, with the highest bid-to-cover ratio since last June. And in overnight trading, the 10yr Treasury yield has risen by another +1.2bps, and is currently at 4.20%.

Over in Europe, there were also losses for sovereign bonds across most of the continent. That was led by gilts, where the 10yr yield rose +7.4bps after data showed UK GDP rose by +0.2% in January, up from a -0.1% contraction in December. Elsewhere, 10yr yields on bunds (+3.7bps) and OATs (+2.7bps) also moved higher. But I talian BTPs (-1.2bps) continued to outperform, and their spread over 10yr bund yields tightened to 123bps, the lowest since November 2021. Speaking of spreads, there was also a further tightening in credit spreads yesterday, with both European and US HY spreads down to their lowest since January 2022.

Elsewhere in Europe, one notable event in the central bank space was the outcome of the ECB’s operational framework review. In line with expectations, the ECB will take a hybrid approach to providing the liquidity needed to operate a floor-type system. Among the details, it will shrink the gap between the depo and the refi rate from 50bp to 15bp starting in September, while keeping banks’ required minimum reserves (which earn zero interest) at 1% of eligible deposits. The review has few immediate market implications, but will have long-term ramifications for the direction of ECB balance sheet policy and functioning of Euro Area money markets. See our economists' reaction note here for more.

For equities, there was a mixed performance yesterday, with the S&P 500 (-0.19%) moving off from its all-time high the previous day. However, that was driven by weakness among tech stocks, with the NASDAQ down -0.54%, whilst the Magnificent 7 fell -0.74%. The latter was led by a -4.54% decline for Tesla, which overtook Boeing as the weakest performer in the S&P 500 year-to-date with a -31.79% decline. Otherwise though, there was a better performance, with the equal-weighted S&P 500 marginally up by +0.01% to an all-time high, and the small-cap Russell 2000 rose +0.30%. Meanwhile in Europe there were further all-time highs, with new records for the STOXX 600 (+0.16%) and the CAC 40 (+0.62%).

Overnight in Asia we’ve also seen a divergent performance for equities. On the one hand, there’ve been gains for the Nikkei (+0.21%) and the KOSPI (+0.86%). But the CSI 300 (-0.10%), the Shanghai Comp (-0.09%) and the Hang Seng (-0.87%) have all lost ground. Elsewhere, US equity futures are indicating a positive start, with those on the S&P 500 up +0.12%.

Finally in the commodity space, Brent crude oil prices rose to their highest level since November, up +2.58% to $84.03/bbl, while WTI rose +2.78% to $79.72/bbl. The moves came amid Ukrainian drone strikes against Russian oil refineries and with data showing that US crude stockpiles declined for the first time in seven weeks. Higher oil prices have been filtering through to consumer prices since the start of the year, and the AAA’s measure of US daily gasoline prices has already risen from $3.110 per gallon at the end of 2023 to $3.396 per gallon yesterday.

To the day ahead now, and data releases include US PPI and retail sales for February, along with the weekly initial jobless claims. From central banks, we’ll hear from ECB Vice President de Guindos, along with the ECB’s de Cos, Schnabel, Knot and Stournaras.

Uncategorized

Good news and bad news Thursday: the good news is jobless claims . . .

– by New Deal democratThis morning brought us both good and bad economic news.The good news was that initial jobless claims continue very low, at 209,000,…

Share this:

- by New Deal democrat

This morning brought us both good and bad economic news.

Government

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Donald Trump tried to overturn the 2020 election results. But the work of others, from lawmakers to judges to regular citizens, stopped him. There are…

Share this:

{kind=link}

{kind=link}

Elections are the bedrock of democracy, essential for choosing representatives and holding them accountable.

The U.S. is a flawed democracy. The Electoral College and the Senate make voters in less populous states far more influential than those in the more populous: Wyoming residents have almost four times the voting power of Californians.

Ever since the Civil War, however, reforms have sought to remedy other flaws, ensuring that citizenship’s full benefits, including the right to vote, were provided to formerly enslaved people, women and Native Americans; establishing the constitutional standard of one person, one vote; and eliminating barriers to voting through the 1965 Voting Rights Act.

But the Supreme Court has, in recent years, narrowly construed the Voting Rights Act and limited courts’ ability to redress gerrymandering, the drawing of voting districts to ensure one party wins.

The 2020 election revealed even more disturbing threats to democracy. As I explain in my book, “How Autocrats Seek Power,” Donald Trump lost his reelection bid in 2020 but refused to accept the results. He tried every trick in the book – and then some – to alter the outcome of this bedrock exercise in democracy.

A recent New York Times story reports that when it comes to Trump’s time in office and his attempt to overturn the 2020 election, “voters often have a hazy recall of one of the most tumultuous periods in modern politics.” This, then, is a refresher about Trump’s handling of the election, both before and after Nov. 3, 2020.

Trump began with a classic autocrat’s strategy – casting doubt on elections in advance to lay the groundwork for challenging an unfavorable outcome.

Despite his efforts, Trump was unable to control or change the election results. And that was because of the work of others to stop him.

Here are four things Trump tried to do to flip the election in his favor – and examples of how he was stopped, both by individuals and democratic institutions.

Anticipating defeat

Expecting to lose in November 2020, in part because of his disastrous handling of the Covid-19 pandemic, Trump proclaimed that “all over the country, especially in California, voter fraud is rampant.” He called mail ballots “a very dangerous thing.” Jared Kushner, his son-in-law and aide, declined to “commit one way or the other” about whether the election would be held in November, because of the COVID pandemic. No efforts to postpone the election ensued.

Trump warned that Russia and China would “be able to forge ballots,” a myth echoed by Attorney General William Barr. Trump illegally threatened to have law enforcement officers at polling places. He falsely asserted that Kamala Harris “doesn’t meet the requirements” for serving as vice president because her parents were immigrants. Asked if he would agree to a transition if he lost, he responded: “There won’t be a transfer, frankly. There’ll be a continuation.”

Threatening litigation

Aware that polls showed Biden ahead by 8 percentage points, Trump declared, “As soon as that election is over, we’re going in with our lawyers,” and they did just that. Adviser Steve Bannon correctly predicted that on Election Night, “Trump’s gonna walk into the Oval (Office), tweet out, ‘I’m the winner. Game over, suck on that.’”

Trump followed the script, asserting at 2:30 am: “we did win this election. … This is a major fraud in our nation,” though the actual results weren’t clear until days later, when, on Nov. 7, the networks declared Biden had won.

Although many advisers said he had lost, Trump kept claiming fraud, repeating Rudy Giuliani’s false allegation that Dominion election machines had switched votes – a lie for which Fox News agreed to pay $787 million to settle the defamation case brought by Dominion.

Taking direct action

Trump allies pressured state legislators to create false, “alternative” slates of electors as a key strategy for overturning the election. Trump contemplated declaring an emergency, ordering the military to seize voting machines and replacing the attorney general with a yes-man who would pressure state legislatures to change their electoral votes.

Encouraging violence

Trump summoned supporters to protest the Jan. 6 certification by Congress, boasted it would be “wild,” and encouraged them to march on the Capitol and “fight like hell,” promising to accompany them. Once they had attacked the Capitol, he delayed for four hours before asking them to stop.

Yet Trump’s efforts to overturn the election failed.

Resisting Trump

Trump claimed that voting by mail produced rampant fraud, but state legislatures let voters vote by mail or in drop boxes because of the pandemic. Postal Service workers delivered those ballots despite actions taken by Trump’s postmaster general, Louis DeJoy, that made processing and delivery more difficult.

DeJoy denied any sabotage in testimony before Congress.

Most state election officials, regardless of party, loyally did their jobs, resisting Trump’s pressure to falsify the outcome. Courts rejected all but one of Trump’s 62 lawsuits aimed at overturning the election. Government lawyers refused to invoke the Insurrection Act and authorize the military to seize voting machines. The military remained scrupulously apolitical. And Vice President Mike Pence presided over the certification, in which 43 Republican senators and 75 Republican representatives joined all the Democrats to declare Biden the winner.

That experience contains invaluable lessons about what to expect in 2024 and how to defend the integrity of elections.

Richard L. Abel does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

white house congress senate trump pence pandemic covid-19 russia china

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Health Officials: Man Dies From Bubonic Plague In New Mexico

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Five Aerospace Investments to Buy as Wars Worsen Copy

Analyst reviews Apple stock price target amid challenges

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International6 days ago

International6 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges