3 5G Stocks With Double Digit Upside Potential

3 5G Stocks With Double Digit Upside Potential

Share this:

In 2008, in the midst of the financial crisis, we learned that some banks were considered “too big to fail.” The phrase was used to justify the controversial Troubled Asset Relief Program, which funneled money to the giant Wall Street firms to keep them solvent.

Today, we’re bracing for the Coronavirus Recession – if it hasn’t arrived already. But times are different, and now we’re likely to find out that some trends are too transformational to derail – not even the coronavirus pandemic will stop them. The switchover to 5G is one of these. The technology has been available since 2017, and the networks started going online in 2019. 5G promises faster wireless internet access, with greater bandwidth and less latency, and is seen by some tech sector experts as the future of communications.

T-Mobile, AT&T, and Verizon have all rolled out 5G networks in the US, and 5G capable smartphones hit the markets last year (Samsung offers three such devices in the Galaxy line). The COVID-19 epidemic has slowed the advance of the new tech, mainly by shutting down the infrastructure work required to support the new network and by forcing delays in the launch of the latest 5G smartphones (for example, Apple normally announced new smartphone models in September, but there are reports that the iPhone 12 will be pushed back two months).

With 5G still on the horizon, even if that horizon is slightly more distant than anticipated, the tech sector is going to attract investors. Semiconductor chip makers, providing the microchips essential to all aspects of the 5G networks – from the transmitters to the towers to the handsets and more – will be on the front lines of the gains.

Investment research firm Craig-Hallum has tapped three such stocks as primed for big gains in 2H20; we’ve used the TipRanks database to pull the details.

Qorvo, Inc. (QRVO)

Qorvo is a well-known chip maker in the wireless niche. The company is best known for integrated circuits for communications apps – the chips that let your PCs, tablets, and smartphones connect to wifi networks. The company’s chips are used in cordless phones, industrial radio, remote meter readings, and wireless security.

Qorvo’s position as a chip supplier for 5G devices, however, supported the company’s fiscal Q3 2020 results. The company showed solid sales in wifi and 5G components, while the popularity of Qorvo chips in the Chinese, Japanese, and Korean markets – all of which are moving steadily into 5G – helped quarterly revenue rise 4.4% year-over-year. The company’s Mobile Products division was both deeply connected to 5G and a main driver of QRVO’s gains.

5-star analyst Anthony Stoss, reviewing QRVO for Craig-Hallum, sees the current COVID-19 containment measures presenting a possible long-term gain for Qorvo stock. He writes, “With the world currently moving online, networks are being constrained. Countries/governments as well as businesses are now aggressively pushing to roll out 5G… We think QRVO will benefit from a faster 5G rollout as they should see higher content in 5G phones as well as 5G base stations.”

Stoss gives QRVO shares a $100 price target and a Buy rating. His target suggests an upside potential this year of 16%. (To watch Stoss’ track record, click here)

The Street largely seems to echo Stoss’ positive sentiment, considering TipRanks analytics showcase QRVO as a Buy. Out of 18 analysts tracked by TipRanks in the last 3 months, 11 are bullish on Qorvo stock, while 7 remain sidelined. With a potential upside of 30%, the stock’s consensus target price stands at $112.27. (See Qorvo stock analysis on TipRanks)

Skyworks Solutions (SWKS)

Next on our list is Skyworks, a mid-cap semiconductor maker that is a major supplier to Apple’s iPhone line. Skyworks is a well-regarded company with quality products, but it does provide a lesson in the dangers of over-specialization: it brought in 51% of its total 2019 revenue from Apple. Skyworks had trouble gaining traction through much of 2019, until Apple started gaining solidly in final third of the year.

That weakness can also be a source of strength. As a major chip supplier for the iPhone line, Skyworks shares the 900-million strong – and very loyal – Apple customer base. And with Apple preparing to release 5G capable iPhones later this year, even if they arrive late, Skyworks is looking at strong demand for its own products in 2H20.

Skyworks has at least one other latent advantage, as well. Its manufacturing facilities are US-based. When COVID-19 epidemic restrictions are lifted, that domestic supply chain will have an easier recovery than competitor companies with greater international exposure.

In his review of SWKS, Craig-Hallum's Anthony Stoss sees Skyworks’ Apple exposure as a possible risk, but one that is outweighed by the company’s overall strong outlook in 5G and Wifi 6 products. He writes of the company, “We think SWKS will benefit from a faster 5G rollout as they should see higher content in 5G phones as well as 5G base stations. Additionally, with people moving to work from home and students moving to online learning, we see rising demand for better Wi-Fi connectivity as well. SWKS should benefit as Wi-Fi 6 adoption ramps up.”

Stoss backs his Buy rating on SWKS with a $110 price target, indicative of a 15% upside potential over the next 12 months. (To watch Stoss’ track record, click here)

All in all, Wall Street sizes up Skyworks as a ‘Moderate Buy’ stock, as the bulls edge out the cautious on the chip maker. In the last 3 months, SWKS has received 15 bullish Buy ratings versus 6 Holds. The consensus price target of $116.44 hints there could be 22% upside for investors, with the stock fetching $95. (See Skyworks stock analysis on TipRanks)

Marvell Technology (MRVL)

Last on our list is Marvell, a smaller name in the semiconductor chip market. This Silicon Valley company brought in $2.86 billion in revenues last year, realizing $179 million in profits. Marvell operates in 14 countries around the world and even after recent share losses boasts a market cap of $16.1 billion.

More importantly, Marvell boasts a strong industry position, bolstered by recent partnership agreements with major handset makers Samsung and Nokia. Marvell will provide the chips needed to power the new 5G devices by both companies. The Finnish device maker is getting ready to release a line of 5G products, and has said that Marvell’s role will be to “solve its 5G chip problems.” And by locking in a 5G agreement with Samsung, one of the world’s largest smartphone makers, Marvell has secured its position against competitors. Market watchers describe Marvell’s Samsung and Nokia agreements as ‘major wins.’

Guaranteeing major customers just ahead of their 5G device rollouts puts Marvell in a solid position in the semiconductor field. The news comes after the company beat its Q4 revenue and EPS forecasts; the combination of good news helps explain why, in the same time that the overall markets have dropped 17%, shares in MRVL has only slipped a net of 3.4%.

5-star Craig-Hallum analyst Christian Schwab points out that MRVL’s forward guidance has already taken COVID-19 disruptions into account, and is rosy otherwise. He writes, “The company’s Q1 revenue guidance is ~5% lower than it would have been without any impact from the virus.” Schwab also points out that the partnerships with Samsung and Nokia will propel Marvell for the long term: “The company highlighted it has begun the ramp of Samsung’s first generation 5G processor, won their next generation 5G baseband processor, and announced a deeper collaboration with the customer. Nokia also announced earlier yesterday a broadening relationship for the development of multiple generations of 5G infrastructure processors. 5G business with Nokia is expected to ramp largely in 2021.”

Schwab’s $30 price target implies a 16% upside for the stock and backs up his Buy rating. (To watch Schwab’s track record, click here)

All in all MRVL shares have a Strong Buy from the analyst consensus, based on no fewer than 12 Buy ratings overbalancing 2 Holds and 1 Sell. Meanwhile, the $28.79 average price target suggests that there is room here for a 11% upside potential. (See Marvell stock analysis on TipRanks)

To find good ideas for 5G stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

The post 3 5G Stocks With Double Digit Upside Potential appeared first on TipRanks Financial Blog.

Government

Mike Pompeo Doesn’t Rule Out Serving In 2nd Trump Administration

Mike Pompeo Doesn’t Rule Out Serving In 2nd Trump Administration

Authored by Jack Phillips via The Epoch Times (emphasis ours),

Former Secretary…

Share this:

Authored by Jack Phillips via The Epoch Times (emphasis ours),

Former Secretary of State Mike Pompeo said in a new interview that he’s not ruling out accepting a White House position if former President Donald Trump is reelected in November.

“If I get a chance to serve and think that I can make a difference ... I’m almost certainly going to say yes to that opportunity to try and deliver on behalf of the American people,” he told Fox News, when asked during a interview if he would work for President Trump again.

“I’m confident President Trump will be looking for people who will faithfully execute what it is he asked them to do,” Mr. Pompeo said during the interview, which aired on March 8. “I think as a president, you should always want that from everyone.”

He said that as a former secretary of state, “I certainly wanted my team to do what I was asking them to do and was enormously frustrated when I found that I couldn’t get them to do that.”

Mr. Pompeo, a former U.S. representative from Kansas, served as Central Intelligence Agency (CIA) director in the Trump administration from 2017 to 2018 before he was secretary of state from 2018 to 2021. After he left office, there was speculation that he could mount a Republican presidential bid in 2024, but announced that he wouldn’t be running.

President Trump hasn’t publicly commented about Mr. Pompeo’s remarks.

In 2023, amid speculation that he would make a run for the White House, Mr. Pompeo took a swipe at his former boss, telling Fox News at the time that “the Trump administration spent $6 trillion more than it took in, adding to the deficit.”

“That’s never the right direction for the country,” he said.

In a public appearance last year, Mr. Pompeo also appeared to take a shot at the 45th president by criticizing “celebrity leaders” when urging GOP voters to choose ahead of the 2024 election.

2024 Race

Mr. Pompeo’s interview comes as the former president was named the “presumptive nominee” by the Republican National Committee (RNC) last week after his last major Republican challenger, former South Carolina Gov. Nikki Haley, dropped out of the 2024 race after failing to secure enough delegates. President Trump won 14 out of 15 states on Super Tuesday, with only Vermont—which notably has an open primary—going for Ms. Haley, who served as President Trump’s U.S. ambassador to the United Nations.

On March 8, the RNC held a meeting in Houston during which committee members voted in favor of President Trump’s nomination.

“Congratulations to President Donald J. Trump on his huge primary victory!” the organization said in a statement last week. “I’d also like to congratulate Nikki Haley for running a hard-fought campaign and becoming the first woman to win a Republican presidential contest.”

Earlier this year, the former president criticized the idea of being named the presumptive nominee after reports suggested that the RNC would do so before the Super Tuesday contests and while Ms. Haley was still in the race.

Also on March 8, the RNC voted to name Trump-endorsed officials to head the organization. Michael Whatley, a North Carolina Republican, was elected the party’s new national chairman in a vote in Houston, and Lara Trump, the former president’s daughter-in-law, was voted in as co-chair.

“The RNC is going to be the vanguard of a movement that will work tirelessly every single day to elect our nominee, Donald J. Trump, as the 47th President of the United States,” Mr. Whatley told RNC members in a speech after being elected, replacing former chair Ronna McDaniel. Ms. Trump is expected to focus largely on fundraising and media appearances.

President Trump hasn’t signaled whom he would appoint to various federal agencies if he’s reelected in November. He also hasn’t said who his pick for a running mate would be, but has offered several suggestions in recent interviews.

In various interviews, the former president has mentioned Sen. Tim Scott (R-S.C.), Texas Gov. Greg Abbott, Rep. Elise Stefanik (R-N.Y.), Vivek Ramaswamy, Florida Gov. Ron DeSantis, and South Dakota Gov. Kristi Noem, among others.

International

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Is there a light forming when it comes to the long, dark and…

Share this:

Is there a light forming when it comes to the long, dark and bewildering tunnel of social justice cultism? Global events have been so frenetic that many people might not remember, but only a couple years ago Big Tech companies and numerous governments were openly aligned in favor of mass censorship. Not just to prevent the public from investigating the facts surrounding the pandemic farce, but to silence anyone questioning the validity of woke concepts like trans ideology.

From 2020-2022 was the closest the west has come in a long time to a complete erasure of freedom of speech. Even today there are still countries and Europe and places like Canada or Australia that are charging forward with draconian speech laws. The phrase "radical speech" is starting to circulate within pro-censorship circles in reference to any platform where people are allowed to talk critically. What is radical speech? Basically, it's any discussion that runs contrary to the beliefs of the political left.

Open hatred of moderate or conservative ideals is perfectly acceptable, but don't ever shine a negative light on woke activism, or you might be a terrorist.

Riley Gaines has experienced this double standard first hand. She was even assaulted and taken hostage at an event in 2023 at San Francisco State University when leftists protester tried to trap her in a room and demanded she "pay them to let her go." Campus police allegedly witnessed the incident but charges were never filed and surveillance footage from the college was never released.

It's probably the last thing a champion female swimmer ever expects, but her head-on collision with the trans movement and the institutional conspiracy to push it on the public forced her to become a counter-culture voice of reason rather than just an athlete.

For years the independent media argued that no matter how much we expose the insanity of men posing as women to compete and dominate women's sports, nothing will really change until the real female athletes speak up and fight back. Riley Gaines and those like her represent that necessary rebellion and a desperately needed return to common sense and reason.

In a recent interview on the Joe Rogan Podcast, Gaines related some interesting information on the inner workings of the NCAA and the subversive schemes surrounding trans athletes. Not only were women participants essentially strong-armed by colleges and officials into quietly going along with the program, there was also a concerted propaganda effort. Competition ceremonies were rigged as vehicles for promoting trans athletes over everyone else.

The bottom line? The competitions didn't matter. The real women and their achievements didn't matter. The only thing that mattered to officials were the photo ops; dudes pretending to be chicks posing with awards for the gushing corporate media. The agenda took precedence.

Lia Thomas, formerly known as William Thomas, was more than an activist invading female sports, he was also apparently a science project fostered and protected by the athletic establishment. It's important to understand that the political left does not care about female athletes. They do not care about women's sports. They don't care about the integrity of the environments they co-opt. Their only goal is to identify viable platforms with social impact and take control of them. Women's sports are seen as a vehicle for public indoctrination, nothing more.

The reasons why they covet women's sports are varied, but a primary motive is the desire to assert the fallacy that men and women are "the same" psychologically as well as physically. They want the deconstruction of biological sex and identity as nothing more than "social constructs" subject to personal preference. If they can destroy what it means to be a man or a woman, they can destroy the very foundations of relationships, families and even procreation.

For now it seems as though the trans agenda is hitting a wall with much of the public aware of it and less afraid to criticize it. Social media companies might be able to silence some people, but they can't silence everyone. However, there is still a significant threat as the movement continues to target children through the public education system and women's sports are not out of the woods yet.

The ultimate solution is for women athletes around the world to organize and widely refuse to participate in any competitions in which biological men are allowed. The only way to save women's sports is for women to be willing to end them, at least until institutions that put doctrine ahead of logic are made irrelevant.

Uncategorized

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-March 2024

A brief excerpt: This 2-part overview for mid-March provides a snapshot of the current housing market.

I always like to star…

Share this:

{kind=link}

{kind=link}

A brief excerpt:

This 2-part overview for mid-March provides a snapshot of the current housing market.There is much more in the article.

I always like to start with inventory, since inventory usually tells the tale!

...

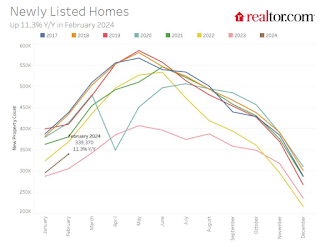

Here is a graph of new listing from Realtor.com’s February 2024 Monthly Housing Market Trends Report showing new listings were up 11.3% year-over-year in February. This is still well below pre-pandemic levels. From Realtor.com:

However, providing a boost to overall inventory, sellers turned out in higher numbers this February as newly listed homes were 11.3% above last year’s levels. This marked the fourth month of increasing listing activity after a 17-month streak of decline.Note the seasonality for new listings. December and January are seasonally the weakest months of the year for new listings, followed by February and November. New listings will be up year-over-year in 2024, but we will have to wait for the March and April data to see how close new listings are to normal levels.

There are always people that need to sell due to the so-called 3 D’s: Death, Divorce, and Disease. Also, in certain times, some homeowners will need to sell due to unemployment or excessive debt (neither is much of an issue right now).

And there are homeowners who want to sell for a number of reasons: upsizing (more babies), downsizing, moving for a new job, or moving to a nicer home or location (move-up buyers). It is some of the “want to sell” group that has been locked in with the golden handcuffs over the last couple of years, since it is financially difficult to move when your current mortgage rate is around 3%, and your new mortgage rate will be in the 6 1/2% to 7% range.

But time is a factor for this “want to sell” group, and eventually some of them will take the plunge. That is probably why we are seeing more new listings now.

{kind=link}

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Four Years Ago This Week, Freedom Was Torched

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Analyst reviews Apple stock price target amid challenges

The SNF Institute for Global Infectious Disease Research announces new advisory board

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

Digital Currency And Gold As Speculative Warnings

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges