2021 was a complete break from the norm of the last decade. We’re experiencing the first serious bout of inflation since the 1970s, a rally in commodities that some are calling a new “supercycle,” and some of the craziest short squeezes in history. …

2021 was a complete break from the norm of the last decade. We’re experiencing the first serious bout of inflation since the 1970s, a rally in commodities that some are calling a new “supercycle,” and some of the craziest short squeezes in history.

Many of 2021’s most compelling stories will surely have some place in the financial history books, and the pandemic is a catalyst for most of them.

I’ve collected a mass of charts throughout this year from a barrage of sources, with the biggest source being The Daily Shot’s daily newsletter which is packed with charts, as well as financial Twitter, news articles, blogs, and the like.

The 2021 Mega Theme: Inflation

It comes as no surprise that after printing trillions of dollars and shutting down portions of the US economy that we’re experiencing inflation.

The Federal Reserve, for better or worse, responded to coronavirus with “unlimited” quantitative easing to stimulate a shutdown economy following the coronavirus panic.

The combination of heaps of economic stimulus (much of it driven directly to consumers, like PPP and stimulus checks), pent-up demand from lockdowns easing, and supply chain constraints driven by labor shortages and sudden demand are the perfect storm for inflation.

Nassim Taleb put it this way: buying 50 things in 2020 and 50 things in 2021 are not the same as buying 0 things in 2020 and 100 things in 2021.

One of the primary post-pandemic investing battlegrounds is between the “hyperinflationistas,” who believe destruction of the US dollar is imminent, and that we’re due for massive inflation, and the “transitory” crowd, who think that inflation will be short-lived merely as a result of short-term supply chain constraints that will sort themselves out.

These charts tell the story of that battle. Let’s hope that whoever ends up being right in the end has the P&L to match that, or else what’s the point right?

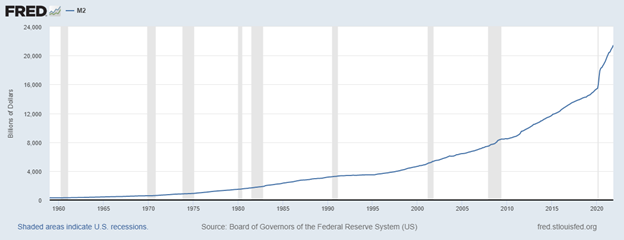

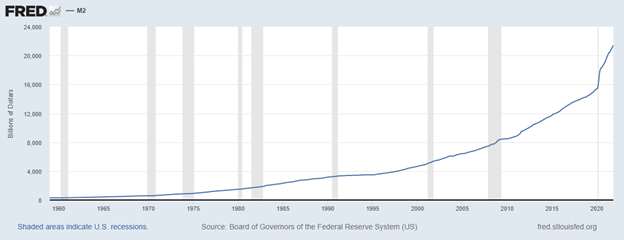

M2: How Much Money Is There?

At its most basic, inflation occurs when there is more money chasing fewer goods. You can get that from increasing the money supply, or deflating the goods supply.

One way we can measure how much money is in the economy is the Federal Reserve’s M2 money supply.

This essentially counts up all of the money in cash, checking accounts, savings accounts, money market accounts, and time deposits like CDs.

Below is a chart of M2 from the late 1950s to 2021:

Higher M2 means more money is floating out there in the economy. This number is almost always going up, and that’s by design. As you can see, the money supply has been steadily growing over the last several decades. And this makes sense. Both GDP and population have been growing, and arguably, a good currency (which is transactional and not an investment or store of value) steadily loses value over time to encourage actual investment and not the hoarding of cash.

But the rate of change massively accelerated in 2020 and 2021. The chart almost looks like a stock which had a huge surprise earnings beat. The upshot here is that there’s a ton more money in circulation than there was before.

CPI: The Official Inflation Rate

CPI gets a lot of flak for questionable weightings and whatnot, but it’s the official inflation benchmark used by the US government and tons of inflation-pegged securities, so even if it’s not the best gauge of inflation, it’s still pretty important.

CPI hit an annualized rate of 7% in December 2021, the highest since the 1970s. It’s inarguable that inflation is back, the argument now is whether it’s temporary or here to stay. Fed Chair Jerome Powell, who popularized calling inflation “transitory” stepped back from that tone back in December, though, after repeated ugly CPI prints. For now, Team Inflation is in the driver’s seat.

Below is a chart of CPI since the BLS started tracking the data in the 1940s:

Let’s take a more granular look at the components driving the inflation:

Lumber

Lumber prices went way up in 2021, way down, then way up again. This volatility was driven by the boom in housing development and renovation post-pandemic, which account for roughly 70% of lumber demand.

All of this new development is driven by migration out of cities and into the suburbs and rural areas.

Just look at this rally compared to the previous 10 years of price action:

Estimates puts $36,000 as the average added cost to a new home as a result of lumber prices at those elevated levels.

The Devaluation of the Turkish Lira

Turkey, like many nations right now, has an inflation problem. But Turkey’s is potentially regime-breaking, while the US and Europe’s are merely headache-making.

Turkish President Erdogan ordered the printing of tons of money while simultaneously cutting interest rates: this makes money plentiful and hence, worth less.

Let’s take a look at the US Dollar to Turkish Lira exchange rate:

Turkish citizens responded by exchanging their Lira for crypto in yet another instance of victims of inflation turning to crypto. Tether trading volume was more than 50% in Turkish Lira briefly in December:

Returns of Equity Strategies

One of the main equity themes of early 2021 was the ‘reflation’ trade, in other words, selling long-duration assets like unprofitable tech, and buying companies with strong cash flows that are resistant to inflation.

A good proxy for this is simply growth vs. value. Let’s see how the primary equity factors performed in 2021:

It’s a pretty mixed bag, mostly owed to the different quantitative definitions for different factor indexes created by S&P Global. And much of this could be distorted by the fact that S&P 500 returns were driven primarily by the FAANG universe of stocks:

The retail trader played a huge role in the 2021 equity markets, accounting for 23% of all US equity trading, compared to just half that in 2019.

Source: FT

Their increased interest in trading makes market makers more interested in trading, because retail trades are ‘uninformed order flow,’ which is profitable to trade against. So the more retail trades, the more MMs want to trade. This leads us to the following graph:

We can’t talk about retail without talking about some of their favorite stocks: GameStop and AMC. These were historic short squeezes achieved by retail traders collaborating on Reddit, Twitter, and the like to buy the same highly-shorted, relatively illiquid names in size.

After the pandemic, the writing was pretty much on the wall for GameStop and AMC. The former relies on people buying physical video games from the mall when most of that business is digital, and the latter is a movie theater chain in an era of at-home streaming during a pandemic. Both had pretty ugly financials and are classic ‘melting ice-cube’ shorts.

So hedge funds shorted them in size. Shorting stocks like these provides a downside hedge, this allows hedge funds to buy their favorite stocks on margin because of the protection their shorts provides. The theory goes that if they’re good at picking both good and bad companies, their good companies will go up more than the bad ones, and they’ll make a nice return without taking massive risk.

But Redditors figured out GameStop and AMC were “hedge fund hotels,” stocks which hedge funds crowd into, making it a game of hot potato. And this gets more violent on the short side, as was on display with the Volkswagen short squeeze during the financial crisis.

While these trades were discussed all throughout the internet, Reddit’s WallStreetBets was definitely the central hub.

Here’s a chart of GameStop (GME), the first of the mega short squeezes:

AMC squeezed alongside GME in January 2021, but it wasn’t the main event until summer 2021:

Perhaps most impressive is the staying power of these stocks. While most short squeezes are fleeting; they last a few days before returning to the pre-squeeze price, GME and AMC were different.

The traders in these stocks actually believed in these companies and many remain as long-term investors. Partly due to their belief in the company, partly because they believe more short squeezes are imminent, and partly as a form of protest against hedge funds that they believe are market manipulators.

While both AMC and GME have cooled off considerably since their squeezes, their prices have remained steady above their post-squeeze levels for several months each, a testament to the unpredictability of retail investors:

Beyond just trading short squeezes, retail traders became enamored with options trading in 2020 and 2021, driving record volumes in the options market.

Much of this increased retail trading activity is attributed to the pandemic. People were stuck at home and found Robinhood and WallStreetBets. As evidence, Robinhood almost doubled their users in 2021 alone. Bloomberg’s Matt Levine calls this phenomenon the “boredom markets hypothesis.”

Before his blow-up, Bill Hwang was a pretty legendary investor. He was a Tiger Cub, meaning he opened up his own Tiger fund under the guidance of Julian Robertson. He opened Tiger Asia Management which eventually grew to over $5 billion at its peak.

He minted a fortune from managing the Tiger fund and opened a family office, which managed his own and close associates’ $10 billion of money.

In dealings with several different investment banks, Hwang bought total return swaps on a concentrated portfolio of media and Chinese tech stocks with considerable leverage. He controlled so much of the float of these stocks that there was nobody to sell to should things go wrong.

Well, one of his stocks, ViacomCBS, announced a secondary offering which must’ve given him a margin call as his brokers began aggressively selling shares to recoup their principal. But because he was so leveraged and the selling was so aggressive, the prime brokers ended up eating large losses. Credit Suisse lost an estimated $5.5 billion in the debacle.

Here’s a Bloomberg chart of a few of his key portfolio holdings:

However, you don’t see the real damage unless you look at individual charts.

ViacomCBS (VIAC):

Discovery (DISCA):

Many of these stocks have yet to recover their massive one-day losses. But that could simply be due to the fact that Hwang’s buying was pushing the price up to unsustainable levels, and once he exited the market they reverted to fair prices:

Crypto vs Metals

Precious metals like gold and silver are seen as long-term stores of value and a hedge against US dollar inflation. But the growth of crypto is threatening its status as an inflation hedge.

In the year with the highest inflation on record in decades, Bitcoin handily outperformed precious metals, which actually went down in value:

Many gold investors are disappointed, as this really seems like gold’s time to shine and it’s asleep at the wheel, moving sideways for all of 2021:

However, Bitcoin is not without its own issues. Rather than lack of action, like gold, the entire crypto market has been predictably volatile in 2021. If the start and end dates were a bit different, gold may have outperformed:

Bottom Line

2021 was such an exciting year in the financial markets. This article could easily be two or three times as long as it is, there were so many compelling stories. Among some of those I’ve left out:

The US dollar’s relative strength against global currencies

The interesting developments between labor and capital, between work-from-home and labor shortages.

The parabolic moves in the used car market

How energy became centrally important to Europe in 2021

Supply chain bottlenecks, and the projections of industry insiders

U.S. Sen. Elizabeth Warren (D-MA) wants answers from one of the top student loan service companies in the country for allegedly botching its student loan forgiveness process involving the federal Public Service Loan Forgiveness program, leaving borrowers confused and without answers.

The senator sent a letter to Mohela CEO Scott Giles on March 18 inviting him to testify before Congress at a hearing on April 10 titled “MOHELA’s Performance as a Student Loan Servicer.” During the hearing, Giles will have to answer for why his company allegedly failed to send billing statements to student loan borrowers in a timely manner and miscalculated monthly payments for borrowers when it was time for them to repay their loans in September last year.

Also, in the letter, Warren highlighted a report that claimed that Mohela failed to perform basic servicing functions for borrowers eligible for PSLF, which led to over 800,000 public service workers facing delays in receiving student debt relief. The report also accuses the company of using a “‘call deflection’ scheme” to keep customers away from speaking to a customer service representative and instead redirecting them to parts of their website.

“Your company has contributed to student loan borrowers’ difficulties by mishandling borrowers’ return to repayment following the COVID-19 pandemic-related pause on payments, interest, and collections and by impeding public servants’ access to PSLF relief,” wrote Warren in the letter.

The move from Warren comes after the U.S. Department of Education withheld $7.2 million in payments to its servicer Mohela in October as punishment because it failed to issue timely billing statements to 2.5 million borrowers which resulted in 800,000 borrowers becoming delinquent on their loans. The department ordered Mohela to put those affected by the issues into forbearance until the mess was resolved.

U.S. President Joe Biden is joined by Education Secretary Miguel Cardona (L) as he announces new actions to protect borrowers after the Supreme Court struck down his student loan forgiveness plan in the Roosevelt Room at the White House on June 30, 2023 in Washington, DC.

Mohela is also currently facing two class-action lawsuits, one filed in December last year and another in January this year, for its alleged “failure to timely process and render decisions for student loan borrowers enrolled in the Public Service Loan Forgiveness program.”

In response to recent criticism surrounding its alleged issues and failures regarding the PSLF program, Mohela claimed in a statement to the Missouri Independent that it “does not have authority to process loan forgiveness until authorization is provided by FSA, which can take months to occur.”

The company also claimed that there are “false accusations” inside of the bombshell report, which was released in February, that details the company’s servicing failures.

“It is unfortunate and irresponsible that information is being spun to create a false narrative in an attempt to mislead the public. False accusations are being disingenuously branded as an investigative report,” said Mohela.

Over the last two years, multiple airlines have dealt with crowding in their lounges. While they are designed as a luxury experience for a small subset of travelers, high numbers of people taking a trip post-pandemic as well as the different ways they are able to gain access through status or certain credit cards made it difficult for some airlines to keep up with keeping foods stocked, common areas clean and having enough staff to serve bar drinks at the rate that customers expect them.

In the fall of 2023, Delta Air Lines (DAL) caught serious traveler outcry after announcing that it was cracking down on crowding by raising how much one needs to spend for lounge access and limiting the number of times one can enter those lounges.

Some airlines saw the outcry with Delta as their chance to reassure customers that they would not raise their fees while others waited for the storm to pass to quietly implement their own increases.

A photograph captures a Qantas Airways lounge in Sydney, Australia.

Shutterstock

This is how much more you'll have to pay for Qantas lounge access

Australia's flagship carrier Qantas Airways (QUBSF) is the latest airline to announce that it would raise the cost accessing the 24 lounges across the country as well as the 600 international lounges available at airports across the world through partner airlines.

Unlike other airlines which grant access primarily after reaching frequent flyer status, Qantas also sells it through a membership — starting from April 18, 2024, prices will rise from $600 Australian dollars ($392 USD) to $699 AUD ($456 USD) for one year, $1,100 ($718 USD) to $1,299 ($848 USD) for two years and $2,000 AUD ($1,304) to lock in the rate for four years.

Those signing up for lounge access for the first time also currently pay a joining fee of $99 AUD ($65 USD) that will rise to $129 AUD ($85 USD).

The airline also allows customers to purchase their membership with Qantas Points they collect through frequent travel; the membership fees are also being raised by the equivalent amount in points in what adds up to as much as 17% — from 308,000 to 399,900 to lock in access for four years.

Airline says hikes will 'cover cost increases passed on from suppliers'

"This is the first time the Qantas Club membership fees have increased in seven years and will help cover cost increases passed on from a range of suppliers over that time," a Qantas spokesperson confirmed to Simple Flying. "This follows a reduction in the membership fees for several years during the pandemic."

The spokesperson said the gains from the increases will go both towards making up for inflation-related costs and keeping existing lounges looking modern by updating features like furniture and décor.

While the price increases also do not apply for those who earned lounge access through frequent flyer status or change what it takes to earn that status, Qantas is also introducing even steeper increases for those renewing a membership or adding additional features such as spouse and partner memberships.

In some cases, the cost of these features will nearly double from what members are paying now.

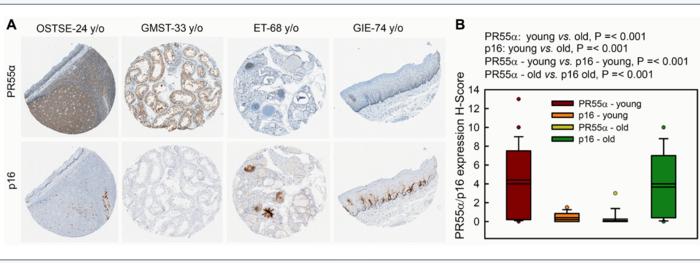

“Our results show that PR55α specifically reduces p16 expression […]”

Credit: 2024 Palanivel et al.

“Our results show that PR55α specifically reduces p16 expression […]”

BUFFALO, NY- March 19, 2024 – A new research paper was published inAging (listed by MEDLINE/PubMed as “Aging (Albany NY)” and “Aging-US” by Web of Science) Volume 16, Issue 5, entitled, “PR55α-controlled protein phosphatase 2A inhibits p16 expression and blocks cellular senescence induction by γ-irradiation.”

Cellular senescence is a permanent cell cycle arrest that can be triggered by both internal and external genotoxic stressors, such as telomere dysfunction and DNA damage. The execution of senescence is mainly by two pathways, p16/RB and p53/p21, which lead to CDK4/6 inhibition and RB activation to block cell cycle progression. While the regulation of p53/p21 signaling in response to DNA damage and other insults is well-defined, the regulation of the p16/RB pathway in response to various stressors remains poorly understood.

In this new study, researchers Chitra Palanivel, Lepakshe S. V. Madduri, Ashley L. Hein, Christopher B. Jenkins, Brendan T. Graff, Alison L. Camero, Sumin Zhou, Charles A. Enke, Michel M. Ouellette, and Ying Yan from the University of Nebraska Medical Center report a novel function of PR55α, a regulatory subunit of PP2A Ser/Thr phosphatase, as a potent inhibitor of p16 expression and senescence induction by ionizing radiation (IR), such as γ-rays.

“During natural aging, there is a gradual accumulation of p16-expressing senescent cells in tissues [76]. To investigate the significance of PR55α in this up-regulation of p16, we compared levels of the p16 and PR55α proteins in a panel of normal tissue specimens derived from young (≤43 y/o) and old (≥68 y/o) donors.”

The results show that ectopic PR55α expression in normal pancreatic cells inhibits p16 transcription, increases RB phosphorylation, and blocks IR-induced senescence. Conversely, PR55α-knockdown by shRNA in pancreatic cancer cells elevates p16 transcription, reduces RB phosphorylation, and triggers senescence induction after IR. Furthermore, this PR55α function in the regulation of p16 and senescence is p53-independent because it was unaffected by the mutational status of p53. Moreover, PR55α only affects p16 expression but not p14 (ARF) expression, which is also transcribed from the same CDKN2A locus but from an alternative promoter. In normal human tissues, levels of p16 and PR55α proteins were inversely correlated and mutually exclusive.

“Collectively, these results describe a novel function of PR55α/PP2A in blocking p16/RB signaling and IR-induced cellular senescence.”

Read the full paper: DOI:https://doi.org/10.18632/aging.205619

Corresponding Authors: Michel M. Ouellette, Ying Yan

Click here to sign up for free Altmetric alerts about this article.

About Aging:

Agingpublishes research papers in all fields of aging research including but not limited, aging from yeast to mammals, cellular senescence, age-related diseases such as cancer and Alzheimer’s diseases and their prevention and treatment, anti-aging strategies and drug development and especially the role of signal transduction pathways such as mTOR in aging and potential approaches to modulate these signaling pathways to extend lifespan. The journal aims to promote treatment of age-related diseases by slowing down aging, validation of anti-aging drugs by treating age-related diseases, prevention of cancer by inhibiting aging. Cancer and COVID-19 are age-related diseases.

Agingis indexed byPubMed/Medline (abbreviated as “Aging (Albany NY)”), PubMed Central, Web of Science: Science Citation Index Expanded (abbreviated as “Aging‐US” and listed in the Cell Biology and Geriatrics & Gerontology categories), Scopus (abbreviated as “Aging” and listed in the Cell Biology and Aging categories), Biological Abstracts, BIOSIS Previews, EMBASE, META (Chan Zuckerberg Initiative) (2018-2022), and Dimensions (Digital Science).

Please visit our website at www.Aging-US.com and connect with us:

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}